Global Investment Perspective

12

1 Highlights • 2011provedanextremelyvolatileyear, largelyduetoongoinguncertainty surroundingtheeurozonesovereigndebt situation. • Growthhasslowedthroughouttheyear , withtheInternationalMonetaryFund(IMF) cuttingits2011GrossDomesticProduct (GDP)economicgrowthforecastforWestern economiesfrom2.5%to1.6%. • Develo pede conomie s–with theU Sa major exception–areengagedinausterity measures,whiletheemergingworldis lookingtodampenitsmuchstrongergrowth tostaveoffanythreatofination. • Anyimpr ovemen tnext yearr estsl argely on theeurozonendinganappropriatesolution toitsproblems. • Against thisb ackgrou nd,man yinves torsh ave edtowhattheysawassafehavens,forcing goldpricestorecordhighsandgovernment bondyieldstogenerationallows. • Short -termi smisri fein suchvo latile market s, creatingopportunitiesinsomeassetclasses forinvestorswhocantakealonger-termview. • Equitiescurrentlylooktoofferthebestvalue, withmanycorporatesinsolidnancialshape afterapplyingtheirownausteritymeasures amidthecreditcrunch.Strongbalancesheets areallowingongoingdividendgrowth. • Sharev aluationsrema inlow ,ree cting themutedeconomicoutlookinthe West.Thisignorestwokeyfactors: thatmanyWesterncompanieshave growingEasternearningsexposure,and thatemergingmarketequitieshavethe potentialtobenetfromtheemerging markets’strongermacrooutlook. • CoreWestern gover nment bonds representpoorvalue,withshort-term safehaveninvestingforcingyields down.Insomeinstancesthisassetclass currentlyofferstheprospectofnegative realreturns(returnsafteradjustingfor ination). • Acombinationofmorepersistentlonger- terminationandtheindustrialization ofemergingmarketsfavorsphysical assetslikerealestateandcommodities. Apositivesupplyanddemandpictureis alsosupportiveforthelatter. • Goldh asprovenpo pulara sasafe haven, butwithnoyield,thepreciousmetalis challengingtovalueandislikelytosuffer wheninvestorswanttomoveintomore risk-orientedassetsagain. Marketslookedinto theabyssonce againin2011 Havingstartedtheyearrobustlyenough,theoutlookdeterioratedsharplyastheyearprogressed, withinvestorsfacingtheprospectofrecession(andsomewouldarguedepression)andeven questioningthefutureofthenancialsystem.Faultlineswereevidentearlyon,withcivilunrest intheMiddleEastspreadingtoLibyaandresultinginoilpricesrisingtoatwo-and-a-half-yearhigh. Japanthensufferedahugeearthquake,tsunamiandnuclearincidentinMarch,causingsupplychain issuesformuchoftheyear. Therealtestforinvestornervescameoverthesummer.FearscenteredonEurope,withmanynations sufferingfromhighsovereigndebttoGDPlevels,budgetdecitsandlowgrowth.Whilethisfocused onperipheralEuropeuntiltheautumn,signsofcontagionspreadtolargernationssuchasItalyand Spainasbondyieldsrosethrough7%and6%,respectively.Thisinturnputpressureonthebanking INTHISISSUE 1 Highlights 1 Market Review 3 Outlook for 2012 4 The shift to short- termism 5 The case for equities 7 Commodities and global real estate 8 The case against government bonds 9 Our outlook for the asset classes December 2011 Outlookfor2012 Lookingpasttheabyss

-

Upload

vajirapanie-bandaranayake -

Category

Documents

-

view

224 -

download

0

Transcript of Global Investment Perspective

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 1/12

Highlights

• 2011provedanextremelyvolatileyear,

largelyduetoongoinguncertainty

surroundingtheeurozonesovereigndebt

situation.

• Growthhasslowedthroughouttheyear,

withtheInternationalMonetaryFund(IMF)

cuttingits2011GrossDomesticProduct

(GDP)economicgrowthforecastforWestern

economiesfrom2.5%to1.6%.

• Developedeconomies–withtheUSa

major exception–areengagedinausterity

measures,whiletheemergingworldis

lookingtodampenitsmuchstrongergrowth

tostaveoffanythreatofination.

• Anyimprovementnextyearrestslargelyon

theeurozonendinganappropriatesolution

toitsproblems.

• Againstthisbackground,manyinvestorshave

edtowhattheysawassafehavens,forcing

goldpricestorecordhighsandgovernment

bondyieldstogenerationallows.

• Short-termismisrifeinsuchvolatilemarkets,

creatingopportunitiesinsomeassetclasses

forinvestorswhocantakealonger-termview.

• Equitiescurrentlylooktoofferthebestvalue,

withmanycorporatesinsolidnancialshape

afterapplyingtheirownausteritymeasures

amidthecreditcrunch.Strongbalancesheets

areallowingongoingdividendgrowth.

• Sharevaluationsremainlow,reecting

themutedeconomicoutlookinthe

West.Thisignorestwokeyfactors:

thatmanyWesterncompanieshave

growingEasternearningsexposure,and

thatemergingmarketequitieshavethe

potentialtobenetfromtheemerging

markets’strongermacrooutlook.

• CoreWesterngovernmentbonds

representpoorvalue,withshort-term

safehaveninvestingforcingyields

down.Insomeinstancesthisassetclass

currentlyofferstheprospectofnegative

realreturns(returnsafteradjustingfor

ination).

• Acombinationofmorepersistentlonger-

terminationandtheindustrialization

ofemergingmarketsfavorsphysical

assetslikerealestateandcommodities.

Apositivesupplyanddemandpictureis

alsosupportiveforthelatter.

• Goldhasprovenpopularasasafehaven,

butwithnoyield,thepreciousmetalis

challengingtovalueandislikelytosuffer

wheninvestorswanttomoveintomore

risk-orientedassetsagain.

Marketslookedintotheabyssonceagainin2011Havingstartedtheyearrobustlyenough,theoutlookdeterioratedsharplyastheyearprogressed,

withinvestorsfacingtheprospectofrecession(andsomewouldarguedepression)andeven

questioningthefutureofthenancialsystem.Faultlineswereevidentearlyon,withcivilunrest

intheMiddleEastspreadingtoLibyaandresultinginoilpricesrisingtoatwo-and-a-half-yearhigh.

Japanthensufferedahugeearthquake,tsunamiandnuclearincidentinMarch,causingsupplychain

issuesformuchoftheyear.

Therealtestforinvestornervescameoverthesummer.FearscenteredonEurope,withmanynations

sufferingfromhighsovereigndebttoGDPlevels,budgetdecitsandlowgrowth.Whilethisfocused

onperipheralEuropeuntiltheautumn,signsofcontagionspreadtolargernationssuchasItalyand

Spainasbondyieldsrosethrough7%and6%,respectively.Thisinturnputpressureonthebanking

INTHISISSUE

1 Highlights

1 Market Review

3 Outlook for 2012

4 The shift to short-

termism

5 The case for equities

7 Commodities and

global real estate

8 The case against

government bonds

9 Our outlook for the

asset classes

December 2

Outlookfor2012Lookingpasttheabyss

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 2/12

2

sector,asignicantholderofsovereigndebt,andconcernsresurfaced

thatmanyinEuropewouldneedtorecapitalizeoracceleratedeleveraging

(loweringdebtlevels).Furthermore,asbankfundingcostsrose,their

abilitytonancethemselveswasrestricted,preventingthemfrom

supplyingcredittotherealeconomy.Anotherchallengefacedbymarkets

wasoneofslowingeconomicgrowth.Globalgrowthhadbeenrecovering

steadilysincetheendoftherecessioncausedbythe2008nancialcrisis

(albeitratherunevenly,withmutedgrowthindevelopedregionsandmuchstrongerguresinemergingmarkets).

Movingthrough2011,however,thisgrowthstartedtofallrapidly.In

January,theIMFforecast2011GDPgrowthinadvancedeconomies

of2.5%andthenrevisedthisdownto1.6%bySeptember.Emerging

economiescontinuedtobenetfromstructuralgrowthdrivers,butthey

werenotcompletelyimmunefromtheslowdowninthedevelopedworld

andhadtoraiseinterestratesintheirbattleagainstination.Asaresult,

theIMFcutits2011growthforecastfrom6.5%to6.4%.Allinall,the

combinationofslowingeconomicgrowthandfearsthattheeuroandeven

theEuropeanUnionmayceasetoexistintheircurrentformssawinvestors

eeriskierinvestmentcategoriessuchasequitiesandcommodities.They

lookedforsolaceintraditionallydefensiveareassuchas‘safehaven’

governmentbondsandgold.Unusuallyhighlevelsofvolatilityinthevalue

ofdifferenttypesofinvestmentswasevidentformuchoftheyear.

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 3/12

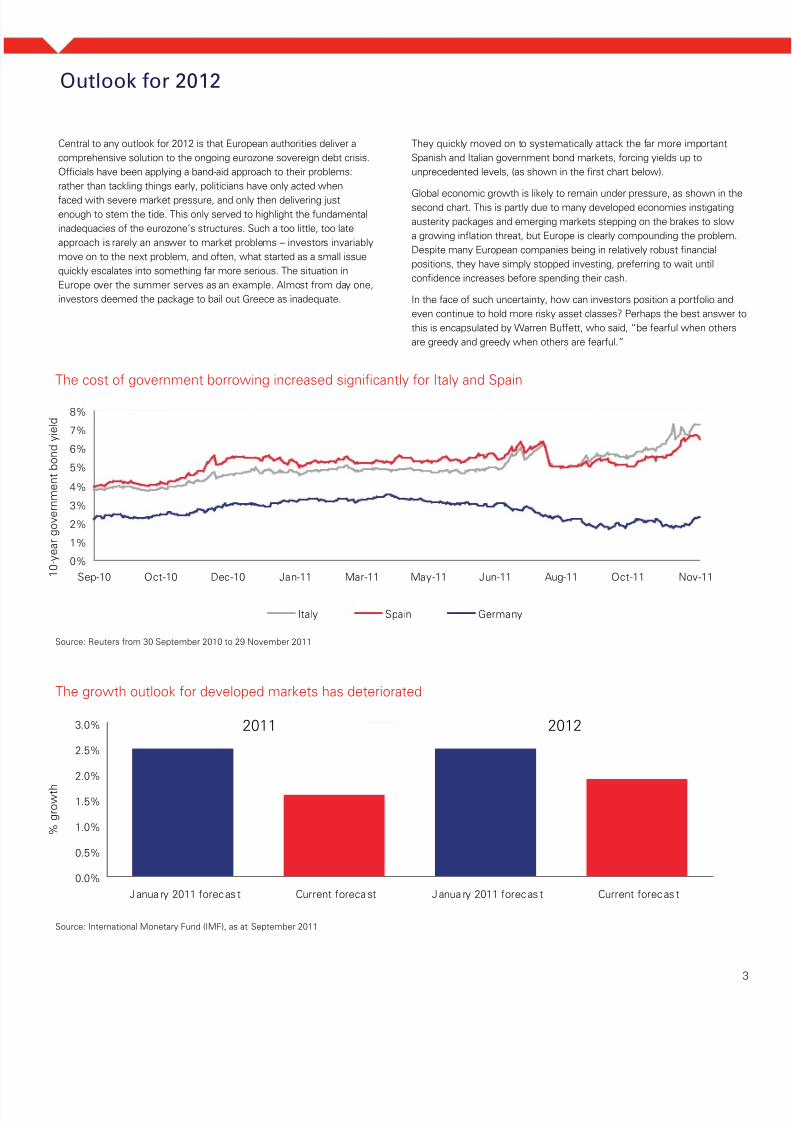

Centraltoanyoutlookfor2012isthatEuropeanauthoritiesdelivera

comprehensivesolutiontotheongoingeurozonesovereigndebtcrisis.

Ofcialshavebeenapplyingaband-aidapproachtotheirproblems:

ratherthantacklingthingsearly,politicianshaveonlyactedwhen

facedwithseveremarketpressure,andonlythendeliveringjust

enoughtostemthetide.Thisonlyservedtohighlightthefundamental

inadequaciesoftheeurozone’sstructures.Suchatoolittle,toolate

approachisrarelyananswertomarketproblems–investorsinvariably

moveontothenextproblem,andoften,whatstartedasasmallissue

quicklyescalatesintosomethingfarmoreserious.Thesituationin

Europeoverthesummerservesasanexample.Almostfromdayone,

investorsdeemedthepackagetobailoutGreeceasinadequate.

Theyquicklymovedontosystematicallyattackthefarmoreimportant

SpanishandItaliangovernmentbondmarkets,forcingyieldsupto

unprecedentedlevels,(asshownintherstchartbelow).

Globaleconomicgrowthislikelytoremainunderpressure,asshowninthesecondchart.Thisispartlyduetomanydevelopedeconomiesinstigating

austeritypackagesandemergingmarketssteppingonthebrakestoslow

agrowinginationthreat,butEuropeisclearlycompoundingtheproblem.

DespitemanyEuropeancompaniesbeinginrelativelyrobustnancial

positions,theyhavesimplystoppedinvesting,preferringtowaituntil

condenceincreasesbeforespendingtheircash.

Inthefaceofsuchuncertainty,howcaninvestorspositionaportfolioand

evencontinuetoholdmoreriskyassetclasses?Perhapsthebestanswert

thisisencapsulatedbyWarrenBuffett,whosaid,“befearfulwhenothers

aregreedyandgreedywhenothersarefearful.”

The cost of government borrowing increased significantly for Italy and Spain

Source: Reuters from 30 September 2010 to 29 November 2011

0%

1%

2%

3%

4%

5%

6%

7%

8%

Sep-10 Oct-10 Dec-10 Jan-11 Mar-11 May-11 Jun-11 Aug-11 Oct-11 Nov-11

Italy Spain Germany

The growth outlook for developed markets has deteriorated

Source: International Monetary Fund (IMF), as at September 2011

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

January 2011 forecas t Current forecast January 2011 forecas t Current forecas t

20122011

% g

r o w t h

1 0 - y e a r g o v e r n m e n t b o n d y i e l d

Outlook for 2012

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 4/12

4

0

1

2

3

4

5

6

7

8

1945 1952 1959 1966 1973 1980 1987 1994 2001 2008

US institutional investors have become more focused on the short term

Source: Based on Morningstar and NYSE data, Goldman Sachs Research estimates, f rom 1945 to 2008

H o l d

i n g

p e r i o d s

i n

y e a r s

Underlyingthesewords,however,issomethingfarmorefundamental.

Inshort,marketshavegonefrombeingdominatedbyinvestorswith

longer-terminvestmenthorizonstobeingdrivenbyshort-termism.Toa

largedegreethisisunderstandable.Whenvolatilityishigh,asitisnow,

investorsquicklyturnfromtargetingwealthgenerationtofocusingon

preservingit.Theprospectofseeinghard-earnedcapitalfallsharply

invalueissimplytoomuchformanyinvestorstobear.Theywould

ratheravoidriskierareasandinvestinmoreconservativeassetclasses,

evenifthelatterappearexpensiveinthelongterm.Compoundingthis

shifttoshort-terminvestingaresomedeeper,structuraltrendswithin

worldstockmarkets.Historically,pensionfundswereclassiclong-term

investors.Theyhadlong-termliabilitiesandneededtoinvestinassets

thatcouldgrowtomeetthese–importantly,short-termvolatilitywas

notamajorconcernandseenasapriceworthpayingforcapitalgrowth.

Morerecently,however,therehasbeenashiftinbehavior,with

manyfundsnownolongertargetingfutureliabilitiesbutratherfocusingon

contributions.Theneedforholdingriskassetclasseshasfallen,withbonds

doingthejobregardlessofwhetherornottheygeneratevalueinthelong

term.Weseethisasafundamentalweaknessinhowindividualsfundtheir

retirement.Further,regulationissuchthatmanyfundshavebeenrequired

toselldowntheirriskierassetclassesandswitchintobonds.Theriseof

hedgefundsandhigh-frequencyinvestorshasexacerbatedthisproblemby

accentuatingvolatilityfurther.

Herethoughistheopportunityforinvestorspreparedandabletoinvest

forthelongerterm;short-termismcreatessomeexceptionalinvestment

opportunities.

The shift to short-termism

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 5/12

Ifyoucanlookthroughtheshort-termfog,equitiesoffersomeexcellent

opportunitiesforbuildingwealthinthelongertermaspartofabalanced

portfolio.Companies,incontrasttogovernmentsandtheconsumer,

havebeenmanagingthemselvesextremelyprudently.Whilethelatter

werebuildingdebttounsustainablelevels,companieswerepaying

downborrowingandbuildingcashbalances.Equitydividendyields

currentlystandatattractivelevelscomparedwithgovernmentbonds,

whilecompanybalancesheetsareenablingthemtogrowdividends–a

veryattractivecombinationinalowinterestrateenvironment.

0%

1%

2%

3%

4%

5%

6%

7%

1999 2001 2003 2005 2007 2009 2011

USA World

Equity dividend yields are currently at attractive levels

Source: UBS from 31 December 1999 to 30 November 2011

Equity valuations look attractive

Source: HSBC as at 30 September 2011

0

5

10

15

20

25

30

J a n - 9 1

J a n - 9 2

J a n - 9 3

J a n - 9 4

J a n - 9 5

J a n - 9 6

J a n - 9 7

J a n - 9 8

J a n - 9 9

J a n - 0 0

J a n - 0 1

J a n - 0 2

J a n - 0 3

J a n - 0 4

J a n - 0 5

J a n - 0 6

J a n - 0 7

J a n - 0 8

J a n - 0 9

J a n - 1 0

J a n - 1 1

MSCI All-Country World Index

W o r l d e q u i t y P / E r a t i o

G l o b a l a n d U S

e q u i t y y i e l d

The case for equities

Valuationsarealsoextremelylowbypaststandards.Tosome

degree,thisisjustiedwithgrowthindevelopedeconomieslikelytobesomewhatlowerthanitwashistorically.Butfocusingonlower

growthratesindevelopedeconomiesignorestwokeyfeatures.First,

companiesindevelopedmarketsareincreasinglyglobalintheiroutlook.

Theyarenotjustaplayontheeconomicgrowthofthecountryoftheirdomicile,butinsteadcanbenetfromhigherglobalgrowth.

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 6/12

6

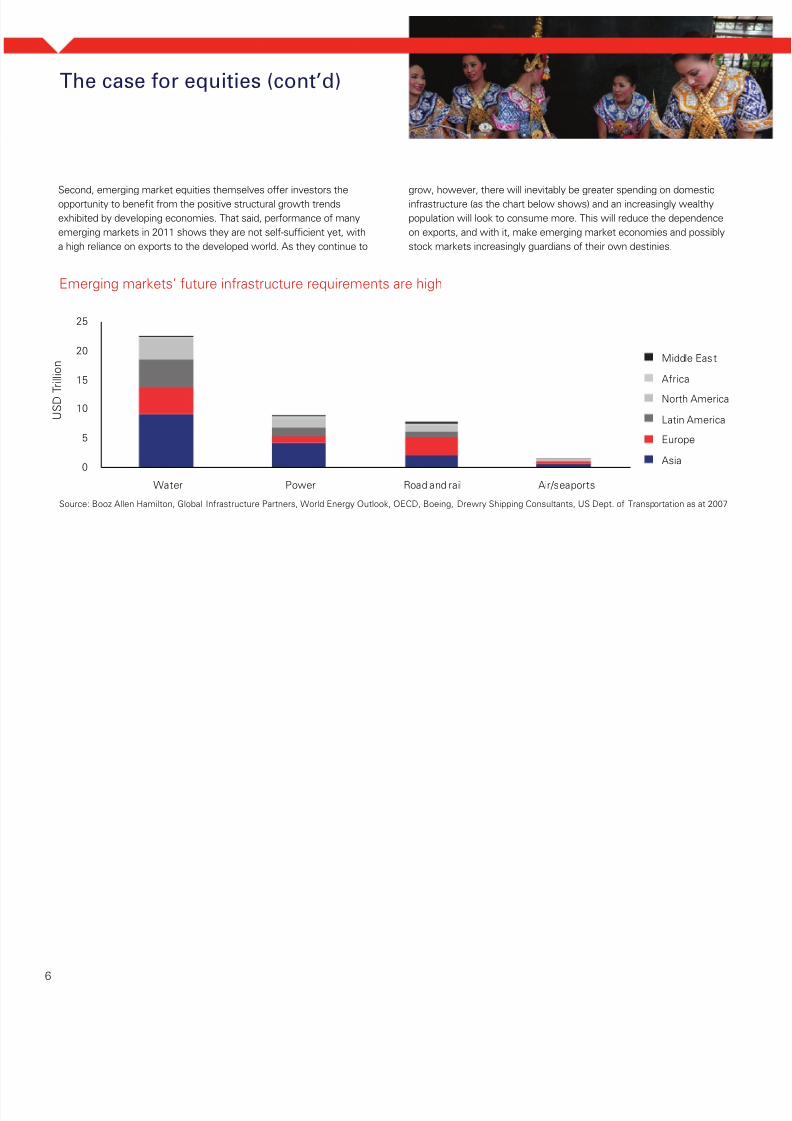

Second,emergingmarketequitiesthemselvesofferinvestorsthe

opportunitytobenetfromthepositivestructuralgrowthtrends

exhibitedbydevelopingeconomies.Thatsaid,performanceofmany

emergingmarketsin2011showstheyarenotself-sufcientyet,with

ahighrelianceonexportstothedevelopedworld.Astheycontinueto

grow,however,therewillinevitablybegreaterspendingondomestic

infrastructure(asthechartbelowshows)andanincreasinglywealthy

populationwilllooktoconsumemore.Thiswillreducethedependence

onexports,andwithit,makeemergingmarketeconomiesandpossibly

stockmarketsincreasinglyguardiansoftheirowndestinies.

The case for equities (cont’d)

Emerging markets’ future infrastructure requirements are high

Source: Booz Allen Hamilton, Global Infrastructure Partners, World Energy Outlook, OECD, Boeing, Drewry Shipping Consultants, US Dept. of Transportation as at 2007

U S D

T r i l l i o n

Middle East

Africa

North America

Latin America

Europe

Asia0

5

10

15

20

25

Water Power Road and rail Air/seaports

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 7/12

7

Acombinationofinationprovingincreasinglypersistentandthe

industrializationofemergingmarketsfavorsphysicalassets.Areas

ofthemarketsuchascommoditiesandrealestateseetheirvalues

risewithinationandalsobenetfromgrowingdemandasemerging

marketsurbanize.Althoughmanycommoditieshaveseenpricedeclines

in2011,reectingtheglobalslowdownineconomicgrowth,theyshould

benetlongertermfromtheseeminglyunstoppablepressuresofrising

demandfrominfrastructureprojectsandlimitedsupplyinmanycases.

Pricesinthelongtermareseeingsignicantupwardpressure.Global

realestateyieldsalsooftengiveinvestorsadecentupliftovermany

governmentbonds(asshowninthechartbelow),whichisanattractive

featureformanyinvestorsinalowinterestrateenvironment.

Theoneexceptiontothisisgold,asillustratedbelow.Tomany,this

representstheultimatesafehaveninvestment–itisaphysicalasset

and,muchtotheuneaseofmanyacentralbanker,youcannotprintany

moreofit.Tosomeextent,wesympathizewiththisview,withgold

typicallyenhancingportfolioreturnsatthesametimeasreducingrisks.

Itdoes,however,haveonemajorproblem:withnointrinsicreturn,

youjustcannotassignafundamentalvaluetoit.Inallprobability,as

aninvestment,itrepresentstheipsideofthecointoinvestinginrisk

assets–thatis,themorepeopleavoidriskassets,themoretheywill

looktobuygoldwiththeircapital.Whenriskyassetsturn,however,you

reallydonotwanttobethelastpersonholdinggold.

Real estate yields look attractive compared with government bonds

Source: Datastream from 29 December 2006 to 06 December 2011

Y i e l d

Gold is seen as a relative safe haven

Source: Reuters from 03 January 2005 to 30 November 2011

G o l d

p r i c e

U S D p

e r o

u n c e

0%

1%

2%

3%

4%

5%6%

7%

8%

9%

10%

Dec-06 Apr-07 Aug-07 Dec-07 Apr-08 Aug-08 Dec-08 Apr-09 Aug-09 Dec-09 Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11

Developed world listed real estate yield 10-year treasury yield

0

250

500

750

1,000

1,2501,500

1,750

2,000

Jan-05 Sep-05 May-06 Jan-07 Oct-07 Jun-08 Feb-09 Nov-09 Jul-10 Mar-11 Nov-11

Commodities and

global real estate

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 8/12

Themirrorimageofthisvalueinequitiesistheovervaluationwithin

manygovernmentbondmarkets,withyieldsinmanycasesnot

sufcientenoughtocoverination.Governmentbondshavenotonly

beenoneofthemainbeneciariesoftheshifttoshort-termismbut

alsothelong-termdowntrendinglobalinationandinterestrates.

Again,muchofthishasbeendrivenbyemergingmarkets,whichhave

increasinglybecomethemanufacturingengineoftheglobaleconomy.

Thisphenomenonhashadtworelatedimpacts,withbothdrivingdown

bondyields.First,byexportingcheaperconsumergoodsintoWestern

economies,inationrateshavebeenhelddown.Second,theseexports

havecreatedsignicantcurrentaccountsurpluseswithindeveloping

markets,whichhaveinmanycasesbeenrecycledintoWestern

governmentbonds,furtherpushingdownyields(asthechartbelow

illustrates).

Whileinationarypressureslookmutedintheneartermasausterity

packagesintheWestkickin,weseethestructuraldowntrendin

inationcomingtoanend.

Wagesinmanyemergingmarketsarenowrisingrapidlyasthese

economiesgrowricherandtheirworkersdemandhigherwages.

Also,astheglobaleconomyrebalancesoverthelongterm,theows

intoWesterngovernmentbondsofrecentyearsareunlikelytobe

repeated.Hencebondshavebeenthebeneciaryofanalmostperfect

storm–along-termdownwardshiftinyields,asthechartbelowshows,

acceleratedbyinvestorspursuingsafetyintheshortterm.However,

surelyjustasthebondevangelists’callsforstructurallyloweryields

becomemorevocal,investorswithalong-termoutlookshouldbe

avoidingthiscategorygiventheprospectofnegativereallong-term

returns.

The case against government

bonds

Wearekeennottounderplaytherisksofinvestinginglobalstockmarketsatpresent.However,theshort-termdirectionisinthehandsofpoliticians.

IntheWest,politiciansaregrapplingwithexcessdebt,globaleconomicimbalancesand,perhapsmostimportantly,howtosolvetheeurozonedebtcrisis

inthefaceofinadequategovernance.Conversely,inAsia,centralbankersarewalkingatightropeofreducinginationwithoutkillingoffgrowthcompletely.

Historically,theChineseauthoritiesinparticularhavebeensuccessfulinachievingthisbuttherisksremain.Thismakestheshorttermuncertain,but

forthosewiththeluxuryofbeingabletotakelong-terminvestmentdecisions,thisincreasinglyshort-termworldiscreatingsomerareopportunitiesto

generatewealth.Thestartpointmaybeuncertainbuteventualupsideispotentiallysignicant.

Conclusion

Government bond yields have fallen dramatically

Source: Reuters from 02 January 1992 to 03 October 2011

1%

2%3%

4%

5%

6%

7%

8%

9%

10%

11%

Jan-92 Jun-94 Dec-96 May-99 Nov-01 May-04 Oct-06 Apr-09 Oct-1

1 0 - y e a r b o n d y

i e l d

UK Germany France US

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 9/12

Our outlook for the asset classes

TheoutlookfortheUSeconomyremainstough,particularlyasunemploymentisstubbornlyhigh,atabout9%,andconsumerspendingakeydriverofgrowth.However,theUSdoesappeartobeseeingstrongergrowththanotherdevelopedeconomies.Thismayprovidesomesupport

to2012corporateearnings,atleastcomparedwithotherdevelopedmarkets,especiallyifeconomicstimulusmeasuresareextendedinto2012.

Althoughvaluationsaresomewhathigherthanforotherdevelopedmarkets,witha2012forecastprice/earningsratioof10.9times,weconsider

thisafairpremiumgiventhestrongereconomicmomentum.PoliticaldeadlockhasbeenasevereimpedimenttotheUSdealingwithitsbudgetary

problems,withthecountrystandingaloneamongmajoreconomiesinnotenactingscalausterity.2012seespresidentialandcongressional

electionsandwewouldhopethataftertheprimarystagesofthecontest,whicharelikelytoseecandidatesappealtotheirnarrowpartybases,

theyseekcommongroundandrealisticwaysofresolvingthelong-termbudgetpressures.

US EQUITIES

POSITIVE

Despitevolatilitystemmingfromtheeurozonedebtcrisis,CanadianequitiesmanagedtonishNovemberlargelyunchanged.Animprovingpicture

intheUS–Canada’skeytradingpartner–helpedshoreupCanadianequities.China’sdecisiontoloosenmonetarypolicyalsobodeswellfor

demandforkeycommoditiesproducedinCanada.CommoditypricescameunderpressureinNovemberandearlyDecember,butthelong-termdemandpictureisstillpromising.Canadiancompaniesalsocontinuetomaintainsolidbalancesheetsandaredeliveringdecentearnings.Thewider

equitymarketoffersanaveragedividendofcloseto3%andaprice/earningsratioofabout11.5timesexpected2012earnings.Thissuggeststhat

Canadianequitiesaretradingatadiscountrelativetorecenthistory,giventhatthe25-yearaverageratioisapproximately15times.

CANADIAN EQUITIES

POSITIVE

ProspectsforcontinentalEuroperemaindominatedbytheeurozonedebtcrisis.Europeanequitiestradeonalowmultipleof8.8timesforward

earnings,implyingtheassetclassofferssignicantvalueshouldasolutionbefound.Abreak-upoftheeurozone,whichisnotourcentralscenario,

wouldhaveseverenegativeimplicationsfortheEuropeaneconomyandequitieswouldlikelyseesignicantdownsideinthisevent.Whilethe

outlookfortheUKeconomyremainssubduedanddependentondevelopmentsintheeurozone,wehaveamorepositiveviewonUKequities.

Theybenetfromsignicantexposuretointernationaleconomies.Valuationsareattractivewithaforwardearningsratioofabout8.6times

(comparedtoa10-yearaverageofabout14times)andadividendyieldofabout3.6%.

EUROPEAN EQUITIES

POSITIVE

Japaneseequitiesfrequentlytradedinadisconnectedmannerfromothermarketsin2011.Likeotherequitymarkets,valuationsremainattractive,

particularlyifJapanesecompaniescanboosttheirlevelsofreturnonequity,althoughthisislikelytobealonger-termdevelopment.For2012,

Japaneseequitiesarelikelytobeaffectedbytheslowdowninglobalgrowth,whilewewouldalsoexpectappreciationtodampencorporate

performance.

JAPANESE EQUITIES

POSITIVE

Powerfullonger-termphenomenasuchasindustrializationandurbanization,aswellasmorerobustscalpositions,underpinourpositiveviewonemergingmarketequities.Wecontinuetoseestrongergrowthfromemergingeconomiescomparedwithdevelopedeconomiesin2012,albeitat

slowerratesthanpreviously.Emergingmarketequitieshaveunderperformeddevelopedmarketequitiesin2011.Thereissomeriskthatfurther

downwardrevisionsinglobalgrowthcouldleadtothemcontinuingtotradeashigher-riskplaysratherthanreectingthesuperiorstructuralfeatures

oftheireconomies.However,valuationsareattractive,withaggregateemergingmarketequitiestradingatabout9timesnextyear’searnings,against

a10-yearaverageofabout11times.EasternEuropeanequitiesareexposedtotheriskofacreditcrunchasdeleveragingbankswithdrawcreditfrom

theregion.WithinEasternEurope,wefavorRussianequities,wherevaluationsremainlowatabout4.9timesearnings(againsta10-yearaverageof

about8times).Thecountryisaplayonoilandotherhardcommoditieswherewehavepositiveviews.Theoutlookfortheoilpricerepresentsthe

keyriskfortheassetclass,andamorepronouncedeconomicslowdown,whichwilllikelyleadtoamaterialfallintheoilprice,wouldbeparticularly

negativeforRussianequities.Thisisnotourcentralscenario.Politicalrisksalsoremain,particularlyinapresidentialelectionyear.

EMERGING MARKET EQUITIES

POSITIVE

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 10/12

10

Our outlook for the asset classes

LatinAmericanequitiesarealsoextremelyattractivelyvaluedonaP/Eratioof9times2012forwardearnings,comparedwithave-yearaverageof11.4times.SlowingworldwidedemandandfallingcommoditypriceshaveraisedfearsforLatinAmerica,however,despitethis,commoditysupplies

remaintightoveralland,sofar,thelikelihoodofacrashsimilartothatof2008/2009seemslow.Shouldtherebeaprolongeddownturn,theregion’s

economieshavemanytoolsattheirdisposaltocounterthis–forexample,thereisampleroomtocutratesifnecessary(Brazilhasalreadystarted

thismeasure).Onamacroeconomiclevel,manyLatinAmericancountriesareinbettershapethantheirdevelopedmarketpeers,supportedbyhigher

levelsofconsumercondenceandsolidscalaccounts.

EMERGING MARKET EQUITIES (CONTINUED)

POSITIVE

TheslowdowninglobaleconomicactivityhashadanimpactonAsiaex-Japan,givenitsrelativelyhighlevelsofexportstodevelopedcountries.

However,westillviewtheeconomicbackdropfavorably,withitseconomiesofferingstrongergrowththanthedevelopedworld.Inationisshowing

signsofmoderatingandwecouldseelooseningmonetarypoliciesin2012,whichwewouldregardaspositivefortheregion’seconomiesandequity

markets.WithinAsiaex-Japan,wefavorChineseequitieswherevaluationsarelowinourview,withthemarkettradingonabout8.2times2012

earnings,signicantlybelowthemarket’s10-yearaverageofabout12.5times.Therearerisksinthattherapidrisesinresidentialrealestatepricescouldreverseandbecomedestabilizingtopartsoftheeconomy,butoverall,weforecastasoftratherthanahardlandingfortheeconomyandforecast

2012economicgrowthofaround8%.

ASIA EX-JAPAN EQUITIES

POSITIVE

USgovernmentbondyieldsremainextremelylowdespiteinvestorslosingcondenceintheroleofpoliticalinstitutionstotacklefundamental

budgetaryproblems.TheUSCongressionalBudgetSuperCommitteefailedtoreachabipartisandecitreductionagreementafterthreemonthsof

intensenegotiations,despiteasimilarpoliticaldeadlockoverthesummerleadingtotheUScreditratingbeingdowngradedbyonenotchbyStandard

&Poor’s.Morepositivelyfortreasuries,theFederalReservedecidedtolengthentheaveragematurityofitstreasuryholdingsbysellingUS$400

billionofshort-datedsecuritiesandpurchasinglonger-termbonds.TheyalsocommittedtokeepFedfundrateslowforalongerperiodoftime.

NotwithstandingFederalReserveactionsthatarecurrentlysupportingprices,weremaincautiouslynegativeonUStreasuriesasanassetclass.We

believethepositivesurpriseseenineconomicdatacancontinueandshouldtheeurozonereachagreementonalastingsolutiontoitssovereigndebt

crisis,thesafehavenpremiumembeddedinUStreasurypricesmaystarttoevaporate.Thiswouldforceyieldstorisetolevelsmorereectiveofthecurrenteconomicandscalbackdrop.

US GOVERNMENT BONDS (TREASURIES)

NEGATIVE

Canadaretaineditsstatusasasafehaveninthewakeoftheongoingeurozonedebtcrisis.ThebroaderCanadianbondmarketdelivereda0.84%

gaininNovember.GovernmentofCanadabondswere0.92%higher.Asexpected,onDecember6,theBankofCanadamaintaineditsovernightrate

at1%.Wedon’tseetheBankraisingratesuntillate2012orbeyond.Onbalance,recenteconomicindicatorsinCanadasuggestthatgrowthinthe

secondhalfofthisyearwasslightlystrongerthantheBankprojectedinOctober.Inationisalsoseendecliningfromitscurrentlevelofabout3%to

2%overthenext12months.WealsoforecastGDPgrowthof1.9%in2012.Againstthisbackdrop,westillprefercorporatebonds,despiterecent

underperformance,becausetheycontinuetoofferbettervaluesthangovernmentbonds.Companybalancesheetsarestrong,anddemandforyield

frominvestorsismaintaininghealthyinterestinnewcorporatedebtissuance.

CANADIAN BONDS

NEGATIVE

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 11/12

Our outlook for the asset classes

ConcernsoverthedifcultiesfacingGreeceandothertroubledEuropeannations,aswellasslowingeconomicmomentum,ledtocorporatebonds

underperforminggovernmentbondsin2011.Financialissueswereweakerthannon-nancial,largelydictatedbytheextentoftheirexposureto

peripheralEurope.Debtwithlesspriorityforrepaymentwithinthecapitalstructure–suchasTier1instruments–sufferedmost.Corporatebonds

issuedbyothernon-nancialsectorsalsosufferedduetocontagioneffectsandanincreasedexpectationthatcompanieswillfarelesswellifthe

economicbackdropdeteriorates.Thepoorperformanceofcorporatebondsin2011hasseenyielddifferentialsoverthesafestsovereignissuers

risetorelativelyattractivelevels,particularlyiffearsofadouble-diprecessionareoverdone.Thereforetheassetclasslooksattractiveonaforward

lookingbasis.

CORPORATE BONDS

POSITIVE

Emergingmarketdebtmarketshaveseenatransformationoverrecentyears,withcountriesshowingsignicantlyimprovedscalpositionsand

tradebalancesaswellasrobusteconomicgrowth.Valuationsremainreasonableandweseeemergingmarketsovereignbondsoutperformingthe

‘safehaven’developedeconomybondmarkets,thelatterofwhichofferverylowyieldstoinvestorsinourview.

SOVEREIGN EMERGING MARKET BONDS

NEUTRAL

Wearebroadlypositiveonglobalrealestateasanassetclass.Itoffersanattractiveyieldupliftovergovernmentbonds,whichshouldpersistas

centralbanksmaintainaccommodativemonetarypolicies.AsiaPacichasthestrongestfundamentals,althoughrentalgrowthmaymoderate

shouldtheglobaleconomyslow.HighlevelsofUSunemploymentandthetoughoutlookfortheEuropeaneconomyarelikelytoprovidea

challengingenvironmentforrentalgrowth.

GLOBAL REAL ESTATE

POSITIVE

Lowinterestrates,andtheprospectsforfurthercentralbankinterventionbygovernmentsindevelopedeconomies,havebeensupportiveforgold.

Weremainalerttotherisksthatabubblecouldbeformingintheassetclass.Thesharpsell-offinSeptember2011indicatesgoldisnotnecessarily

defensiveandcouldseesignicantdownsideintheeventthattheworld’simbalancesarecorrectedandtheuncertaintylifted.Thisriskandthedifculty

invaluinggoldmakesuswaryofholdingsignicantpositionsoverthelongerterm.However,asitcanprovidesomethingofahedgetoextreme

negativeevents,wecontinuetoadvocatemodestholdingsindiversiedportfolioswhiletheoutlookfortheglobaleconomyremainssouncertain.

GOLD

NEUTRAL

Webelievehardandsoftcommoditiesoffertheprospectsforattractivelonger-termreturns,givencontinueddemandgrowthfromemerging

markets.Thisisgrowingfromalowbase,andsupplyremainsrestrictedduetoadeclineinminingcapitalexpenditurefollowingthe2008nancial

crisis.Manycommoditymarketshaveseendeclinesin2011,aseconomicactivityhasslowed.However,asemergingeconomiesarethekey

driversofdemandgrowthandwedonotforecastaglobalrecession,webelievethepricedeclinesseenin2011arecorrectionsratherthantheend

ofpositivelonger-termtrends.

COMMODITIES

POSITIVE

Manycurrencymarketshavebeendrivenbysimilarfactorsasequitiesandbonds,suchastheSwissFranc,forexample,whichhasseensignicant

appreciation.WewouldseearesolutionoftheeurozonesovereigndebtcrisisaspositivefortheEuroandnegativefortheSwissFranc,andpossibly

theUSDollarandYen,shouldsucharesolutionbeaccompaniedbyawiderincreaseinriskappetite.Longerterm,weseetheemergingmarket

currenciesaswellplacedtoappreciate,reectingtheirlong-termstructuraladvantages,althoughpolicyactionsmayslowdowntheprocess.

CURRENCIES

POSITIVE

8/2/2019 Global Investment Perspective

http://slidepdf.com/reader/full/global-investment-perspective 12/12

Unless stated otherwise, all data and charts are sourced from Datastream, Bloomberg, Barclays Capital, Citigroup World Government

Bond indices and HSBC Global Asset Management. All returns are total monthly returns expressed in local currencies.

Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way.HSBC accepts no liability for any failure to meet such forecasts, projections or targets.

Securities and Annuity products are provided by Registered Representatives and Insurance Agents of HSBC Securities (USA) Inc., member NYSE/

FINRA/SIPC, a registered Futures Commission Merchant, a wholly owned subsidiary of HSBC Markets (USA) Inc. and an indirectly wholly owned

subsidiary of HSBC Holdings plc. In California, HSBC Securities (USA) Inc. conducts insurance business as HSBC Securities Insurance Services. Licens

#: OE67746. Insurance products are offered through Insurance Agents of HSBC Insurance Agency (USA) Inc., a wholly owned subsidiary of HSBC

Bank USA, N.A., and an indirectly wholly owned subsidiary of HSBC Holdings plc. Products and services may vary by state and are not available in all

states. California license #: OD36843. Securities, Annuity and Insurance Products are: Not a deposit or other obligation of the bank or any of

its affiliates; Not FDIC insured or insured by any federal government agency of the United States; Not guaranteed by the bank or any of its

affiliates; and subject to investment risk, including possible loss of principal invested. All decisions regarding the tax implications of your

investment(s) should be made in connection with your independent tax advisor.

Investing entails risks, including possible loss of principal. Investors should be aware that performance returns are affected by market fluctuations

and note that the use of derivatives and investments involving a currency other than their own involves special risks. Investments in commodities and

currencies may involve substantial risk as the prices can fluctuate significantly. International investing involves a greater degree of risk and increasedvolatility that is heightened when investing in emerging or frontiers markets. Foreign securities can be subject to greater risks than U.S. investments,

including currency fluctuations, less liquid trading markets, greater price volatility, political and economic instability, less publicly available information,

and changes in tax or currency laws or monetary policy. Emerging markets are often characterized by even less economic diversity and political stabilit

than more developed international markets, and individual securities may demonstrate greater price volatility and a lack of liquidity. Investors should

consider their investment objectives, whether or not they can assume these risks and should undertake their own appropriate professional advice.

Past performance does not guarantee future results.

The MSCI All Country World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market

performance of developed and emerging markets. The MSCI ACWI consists of 45 country indices comprising 24 developed and 21 emerging market

country indices. The developed market country indices included are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece,

Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and

the United States. The emerging market country indices included are: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia,

Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used to create afinancial instruments or products or any indices. The MSCI information is provided on an ‘as is’ basis and the user of this information assumes the ent

risk of any use it may make or permit to be made of this information. Neither MSCI, any of its affiliates or any other person involved in or related to

compiling, computing or creating the MSCI information (collectively, the ‘MSCI Parties’) makes any express or implied warranties or representations w

respect to such information or the results to be obtained by the use thereof, and the MSCI Parties hereby expressly disclaim all warranties (including,

without limitation, all warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpos

with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, specia

incidental, punitive, consequential or any other damages (including, without limitation, lost profits) even if notified of, or if it might otherwise have

anticipated, the possibility of such damages.

Outlook for 2012 is a joint publication of HSBC Global Asset Management (USA) Inc. and HSBC Global Asset Management (Canada) Limited (collective

“we”). This document is distributed by HSBC Global Asset Management (USA) Inc., HSBC Global Asset Management (Canada) Limited and HSBC

Global Asset Management (Bermuda) Limited. It should not be viewed as a solicitation or an offer to purchase or subscribe for any investment or

advisory service. The information contained in this document is for information purposes only and is based on sources believed to be reliable. Howeve

we have not independently verified such information and make no guarantee, representation or warranty and accept no responsibility or liability asto its accuracy or completeness. Opinions expressed in the document are subject to change without notice and this information is not intended to

provide professional advice and should not be relied upon in that regard. This information is not, and under no circumstances should be construed as,

a solicitation to act as a securities broker or dealer in any jurisdiction by any person or company that is not legally permitted to carry on the business of

a securities broker or dealer in that jurisdiction. HSBC Global Asset Management (USA) Inc., HSBC Global Asset Management (Canada) Limited and

HSBC Global Asset Management (Bermuda) Limited are part of HSBC Global Asset Management, the global investment management business of

HSBC Holdings plc. HSBC Global Asset Management (USA) Inc. is a separate legal entity registered with the United States Securities and Exchange

Commission. HSBC Global Asset Management (Canada) Limited is also a separate legal entity and is a subsidiary of HSBC Bank Canada. HSBC Global

Asset Management (Canada) Limited is registered in all provinces of Canada except for Prince Edward Island. HSBC Global Asset Management

(Bermuda) Limited of 6 Front Street, Hamilton, Bermuda, is a wholly owned subsidiary of HSBC Bank Bermuda Limited, and is licensed to conduct

investment business by the Bermuda Monetary Authority. CA#M1112356 (12/11)

Brokerage Customer Service

1 800 662 3343