Global Pharmaceutical Perspective

15

Daniel VIAL Vicepresidente IMS Europe Milano - 21 settembre 2007 Global Pharmaceutical Perspective

description

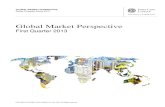

Global Pharmaceutical Perspective. Daniel VIAL Vicepresidente IMS Europe Milano - 21 settembre 2007. Global pharmaceutical sales 643 billions US $ in 06. % constant US $ growth. Billions US $. Source: IMS Health, IMS Market Prognosis International, Feb 2007. Europe. Size: $ 182 bn - PowerPoint PPT Presentation

Transcript of Global Pharmaceutical Perspective

Daniel VIALVicepresidente

IMS Europe

Milano - 21 settembre 2007

Global Pharmaceutical Perspective

Il Futuro Dell'Industria Farmaceutica - 21 settembre 20072

0

100

200

300

400

500

600

1999 2000 2001 2002 2003 2004 2005 20060%

2%

4%

6%

8%

10%

12%

14%

16%Total world market

Growth over previous year

Bill

ion

s U

S $

In billions USD1999 2000 2001 2002 2003 2004 2005 2006

Total World market 334 362 387 427 498 559 601 643

% Constant US $ growth 14.5 11.7 11.8 10.6 10.4 8.0 6.8 7.0

Source: IMS Health, IMS Market Prognosis International, Feb 2007

% c

on

stan

t U

S $

gro

wth

Global pharmaceutical sales643 billions US$ in 06

Il Futuro Dell'Industria Farmaceutica - 21 settembre 20073

2006: market dynamic is different accordingto the region

Source: IMS Health - Global Pharma Forecasts, March 2007

Size:$ 27.5 bn

% Growth: 12.9%

Size: $ 182 bn

% Growth: 4.8%

Size: $ 57 bn

% Growth: -0.7%

Size: $ 52 bn

% Growth: 9.8%

Size: $ 290 bn

% Growth: 8%

North America

Europe

Japan

Asia/Africa/Australia

Latin America

Il Futuro Dell'Industria Farmaceutica - 21 settembre 20074

* : Constant dollarSource : IMS Health – MIDAS – Retail market

+4%

France

26.3 bn $

+2.3%

Italy

15.3 bn $+0.5%

Germany

28.5 bn $

+ 6.3%

Spain

11.9 bn $

+3.1%

UK

16.3 bn $

+2.6%Top 5 Europe

98.3 bn $

2006: within the region, market dynamic is different according to the country

Il Futuro Dell'Industria Farmaceutica - 21 settembre 20075

Contribution to growthEmerging market contribute to 27% of the total growth

46

29

13

8

4

50

16

27

8

-1

-10 0 10 20 30 40 50 60

US

Europe

Emerging markets

Rest of the world

J apan

% CONTRIBUTION

Source: IMS Health, IMS Market Prognosis International, Feb 2007

2001+25.5 Billions US $

2006+42.4 Billions US $

Il Futuro Dell'Industria Farmaceutica - 21 settembre 20076

Number of Global BlockbustersFor the first time, “specialist driven” drugs represent half of the blockbusters

Num

ber

of

Blo

ckb

ust

ers

0

10

20

30

40

50

60

70

80

90

100

110

2000 2002 2004 2006

Specialist driven

Primary care driven

25%

75%

44

105

49%

51%

Source: IMS Health, MIDAS, MAT Dec 2006, Market Insights Team research

Il Futuro Dell'Industria Farmaceutica - 21 settembre 20077

Protection status in 5 key markets

Source: IMS Health, MIDAS, New Market Segmentation, RX only, MAT Dec 2006

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total 5markets

US Italy France Germany UK

% M

ark

et

Sh

are

US

$

In-Patent Off-Patent Generics Other

14

-22

12

11

15

-28

17

14

9

6

4

-9

-15

16

7

10

11

-22

-2

11

13

-20

12

7

Il Futuro Dell'Industria Farmaceutica - 21 settembre 20078

Italian retail market: reimbursable drugs Since the 2nd semester 06, a regular decrease of the growth for the units and a negative growth in value*

- 10,0

- 5,0

0,0

5,0

10,0

15,0

1H20

06

2H20

06

1H20

07

% g

row

th

% vs previous (Units) % vs. previous (Values)

-9%

- 3.4%

2.7%4.7%

5.9%

10.3%

*: in public price

Il Futuro Dell'Industria Farmaceutica - 21 settembre 20079

Italian retail market: reimbursable drugsIn units, the reimbursable market is becoming flat

Units

Il Futuro Dell'Industria Farmaceutica - 21 settembre 200710

Italian retail market: reimbursable drugsIn value*, the reimbursable market is declining

In €

*: in public priceTop 5 Europe: + 2% (1st 07 vs 1st 06)

-9%

Il Futuro Dell'Industria Farmaceutica - 21 settembre 200711

Italian pharma R&D Growth of pharma R&D investment is higher than the restof the industry during the last 6 years

R&D investment - in million €

+ 18.9%

+ 24.7%

8,4

8,6

8,8

9

9,2

9,4

9,6

9,8

10

10,2

2000 2001 2002 2003 2004 2005 2006

% of pharma investment on total industry

Il Futuro Dell'Industria Farmaceutica - 21 settembre 200712

Italian pharma R&D% of workers in the R&D

Rate of workers in pharma R&D is much more higher than in the industry

0

1

2

3

4

5

6

7

8

9

1999 2000 2001 2002 2003 2004 2005 2006

Pharma Total Industry

In % of total employees

Il Futuro Dell'Industria Farmaceutica - 21 settembre 200713

Source : IMS Health – R&D Focus

R&D : drugs in active development

Belgium: 401 - Poland : 155

1659

Germany

750

Italy

1217

France

2871

UK

465

Spain

Il Futuro Dell'Industria Farmaceutica - 21 settembre 200714

• Italy will be the 6th country in term of drugs’ consumption (in value)

• China will be the 7st country in term of drugs’ consumption (in value)

• Turkey, South Korea and India will be closed to Top 10

Source: IMS Health -IMS Market Prognosis 2002-2010

1 USA

2 JAPON

3 ALLEMAGNE

4 FRANCE

5 ITALIE

6 UK

7 ESPAGNE

8 CANADA

9 BRESIL

10 CHINE

1 USA

2 JAPON

3 FRANCE

4 ALLEMAGNE

5 UK

6 ITALIE

7 CHINE

8 CANADA

9 ESPAGNE

10 BRESIL

10 countries:

+80% of drugs’ consumption

(in value)

Top 10 market rankings to 2010 China just behind the old Europe

2002 2010

Daniel VIAL

Vicepresidente

Thank you very much for your attention ….