Futures And Spot Commodity Prices, Options, And Forward ... · Di erent traders have di erent...

209

Futures And Spot Commodity Prices, Options, And Forward interest rates: Model And Empirical Analysis YU MIAO (B.Sc., NANJING UNIVERSITY) A THESIS SUBMITTED FOR THE DEGREE OF DOCTOR OF PHILOSOPHY DEPARTMENT OF PHYSICS NATIONAL UNIVERSITY OF SINGAPORE 2017 Supervisor: Dr. Wang Qinghai Examiners: Professor. Wang Jiansheng Associate Professor. Tan Mengchwan Professor. Emmanuel Haven, Memorial University of Newfoundland

Transcript of Futures And Spot Commodity Prices, Options, And Forward ... · Di erent traders have di erent...

Futures And Spot Commodity Prices,

Options, And Forward interest rates:

Model And Empirical Analysis

YU MIAO

(B.Sc., NANJING UNIVERSITY)

A THESIS SUBMITTED

FOR THE DEGREE OF DOCTOR OF PHILOSOPHY

DEPARTMENT OF PHYSICS

NATIONAL UNIVERSITY OF SINGAPORE

2017

Supervisor:

Dr. Wang Qinghai

Examiners:

Professor. Wang Jiansheng

Associate Professor. Tan Mengchwan

Professor. Emmanuel Haven, Memorial University of

Newfoundland

Declaration

I hereby declare that the thesis is my original work and it has been written by me in its

entirety. I have duly acknowledged all the sources which have been used in the thesis.

This thesis has also not been submitted for any degree in any university previously.

YU MIAO

JULY 2017

i

Acknowledgements

I would like to thank all people who have supported me during my graduate study.

First and foremost, I would like to express my sincerest gratitude and greatest respect to

Professor Belal E Baaquie and my supervisor Dr. Wang Qinghai. My main work is under

the guidance of Professor Baaquie. Without his encouragement, supervision, and support,

the dissertation is definitely not possible. His deep and distinctive view of quantum physics

guided me to think of the world in the language of quantum field theory. Besides the research

field, the opinion and experiences for the life that he shares with me will affect my whole life.

I thank my supervisor Dr. Wang Qinghai for vast advices and guidance for my research and

my PhD thesis.

My sincere thanks also goes to Du Xin, Jiten Bhanap, and Cao Yang for their useful

discussion and collaboration. I thank National University of Singapore and Department of

Physics for the financial support.

Last but not least, I would like to thank my parents, my father Yu Jianxin and my mother

Yu Xiuying, and my wife Tian Maoshan for their unconditional support and precious love.

iii

Summary

Financial market is a platform to improve the efficiency and convenience for all traders in the

world. Different traders have different purposes for their trading and there are three main

types of traders including hedgers, speculators and arbitrageurs, due to three vital purposes.

Whether you aim to hedge, speculate or arbitrage in the market, quantitative analysis is a

strong tool to help you make a better decision. Although recent quantitative study using

statistics and stochastic process as the basic method has already made huge achievements in

financial domain, there are still great numbers of unsolved financial fields which may require

new theories to fill in. In this thesis, quantum field theory is chosen as a new method to analyse

financial instruments. In Chapter 2, a new correlation factor among different commodities

is defined by a new microeconomics theory based on quantum field theory. In Chapter 3,

a new theory of commodity futures with two-Dimension quantum field is proposed and the

theory may fill the gap of the futures theory for financial market. In Chapter 4, an indicator is

designed by comparing option pricing with stochastic method and quantum method to reflect

the market instability. In Chapter 5, a new theory of pricing bond option is raised up to give

contract makers a better reference to price the bond option contract.

v

vi

Publication List

[1] B.E. Baaquie, Miao Yu∗, and Xin Du. ”Multiple Commodities in Statistical Microe-

conomics: Model and Market.” Physica A: Statistical Mechanics and its Applications 462

(2016): 912-929.

[2] B.E. Baaquie and Miao Yu∗. Statistical Field Theory of Futures Commodity Prices.

Submitting paper.

[3] B.E. Baaquie, Miao Yu∗. ”Option Price and Market Instability.” Physica A: Statistical

Mechanics and its Applications 471 (2017): 512-535.

[4] B.E. Baaquie, Miao Yu∗ and Jitendra Bhanap. Risky Forward Interest Rates and

Swaptions: Quantum Finance Model and Empirical Results. Submitting paper.

* Corresponding author

Contents

Declaration i

Acknowledgements iii

Summary v

List of Tables xiv

List of Figures xxi

List of Symbols xxii

1 Introduction 1

§ 1.1 Review of financial market and financial modeling . . . . . . . . . . . . . . . . 1

§ 1.2 Introduction of financial instrument . . . . . . . . . . . . . . . . . . . . . . . . 3

§ 1.2.1 Commodity price and Futures . . . . . . . . . . . . . . . . . . . . . . . 3

§ 1.2.2 Option price . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

§ 1.2.3 Interest rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

vii

CONTENTS viii

§ 1.2.4 Bond . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

§ 1.2.5 One type of swaption: bond option . . . . . . . . . . . . . . . . . . . . 7

§ 1.3 Introduction of financial models . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

§ 1.3.1 Lagrangian model based on supply and demand . . . . . . . . . . . . . 8

§ 1.3.2 Black-Scholes model for option pricing . . . . . . . . . . . . . . . . . . 10

§ 1.3.3 HJM Model for forward interest rate . . . . . . . . . . . . . . . . . . . 12

2 Multiple Commodities in Statistical Microeconomics: Model and Market 14

§ 2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

§ 2.2 The microeconomic action functional . . . . . . . . . . . . . . . . . . . . . . . . 16

§ 2.3 Correlation Function . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

§ 2.3.1 Expansion of Potential . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

§ 2.3.2 Auto-correlation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

§ 2.3.3 Cross-correlation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

§ 2.3.4 Nonlinear terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

§ 2.4 Market data and model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

§ 2.5 Fitting with Market Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

§ 2.6 Fits for GII , GIJ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

§ 2.6.1 Two commodities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

§ 2.6.2 Three commodities fit . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

§ 2.6.3 Four commodities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

CONTENTS ix

§ 2.6.4 Six commodities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

§ 2.7 Comparison of single and multiple commodities fit . . . . . . . . . . . . . . . . 44

§ 2.8 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

§ 2.9 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

§ 2.9.1 Derivation of D(0)IJ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

§ 2.9.2 Consistency check for D(0)IJ . . . . . . . . . . . . . . . . . . . . . . . . . 50

3 Statistical Field Theory of Futures Commodity Prices 53

§ 3.1 Futures commodity prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

§ 3.2 Single commodity; Gaussian approximation . . . . . . . . . . . . . . . . . . . . 57

§ 3.3 Propagator . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

§ 3.4 Propagator for spot prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

§ 3.4.1 Boundary condition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

§ 3.4.2 Special case γ = γ2 = γ1 . . . . . . . . . . . . . . . . . . . . . . . . . . 65

§ 3.4.3 Limit of γ → 0 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

§ 3.5 Contour map of G(t, ξ; 0, 0) and α . . . . . . . . . . . . . . . . . . . . . . . . . 67

§ 3.6 Spot rate G(t, t; t′, t′): empirical and model . . . . . . . . . . . . . . . . . . . . 68

§ 3.7 Spot-futures G(t, ξ; 0, 0): empirical and model . . . . . . . . . . . . . . . . . . . 70

§ 3.8 Algorithm for empirical GE(z+, z−) . . . . . . . . . . . . . . . . . . . . . . . . . 72

§ 3.9 Binning of empirical D(k)E (a, b, c) . . . . . . . . . . . . . . . . . . . . . . . . . . 76

§ 3.10 Empirical results for GE(z+; z−) . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

CONTENTS x

§ 3.11 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

§ 3.12 Appendix I(τ, θ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

§ 3.12.1 Appendix: Algorithm for binning the propagator . . . . . . . . . . . . . 82

4 Option Price and Market Instability 85

§ 4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

§ 4.2 Quantum finance formulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

§ 4.3 Transition amplitude K . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

§ 4.4 BY Model option price . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

§ 4.4.1 Martingale condition . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

§ 4.4.2 BY Option: market time . . . . . . . . . . . . . . . . . . . . . . . . . . 94

§ 4.5 Mapping BY Model to data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

§ 4.6 Calibration of the BY Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

§ 4.7 Fitting Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

§ 4.8 Global crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108

§ 4.9 Result for five major FX options . . . . . . . . . . . . . . . . . . . . . . . . . . 110

§ 4.9.1 Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

§ 4.9.2 Australia Dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

§ 4.9.3 Swiss Franc . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

§ 4.9.4 British Pound . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

§ 4.9.5 Japanese Yen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

CONTENTS xi

§ 4.10 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

§ 4.11 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

§ 4.11.1 Classical Solution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

5 Risky Forward Interest Rates and Swaptions: Quantum Finance Model and

Empirical Results 121

§ 5.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121

§ 5.2 Quantum finance model of forward interest rates . . . . . . . . . . . . . . . . . 123

§ 5.3 Correlation functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

§ 5.4 Stiff propagator . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

§ 5.5 Market correlators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

§ 5.6 Empirical volatility and propagators . . . . . . . . . . . . . . . . . . . . . . . . 135

§ 5.6.1 Stand-alone Singapore rates . . . . . . . . . . . . . . . . . . . . . . . . 137

§ 5.7 Calibration of US and Singapore models . . . . . . . . . . . . . . . . . . . . . . 138

§ 5.8 Determination of ∆(θ, θ′): Coupling of US-Singapore rates . . . . . . . . . . . . 140

§ 5.8.1 Malaysian forward interest rates . . . . . . . . . . . . . . . . . . . . . . 143

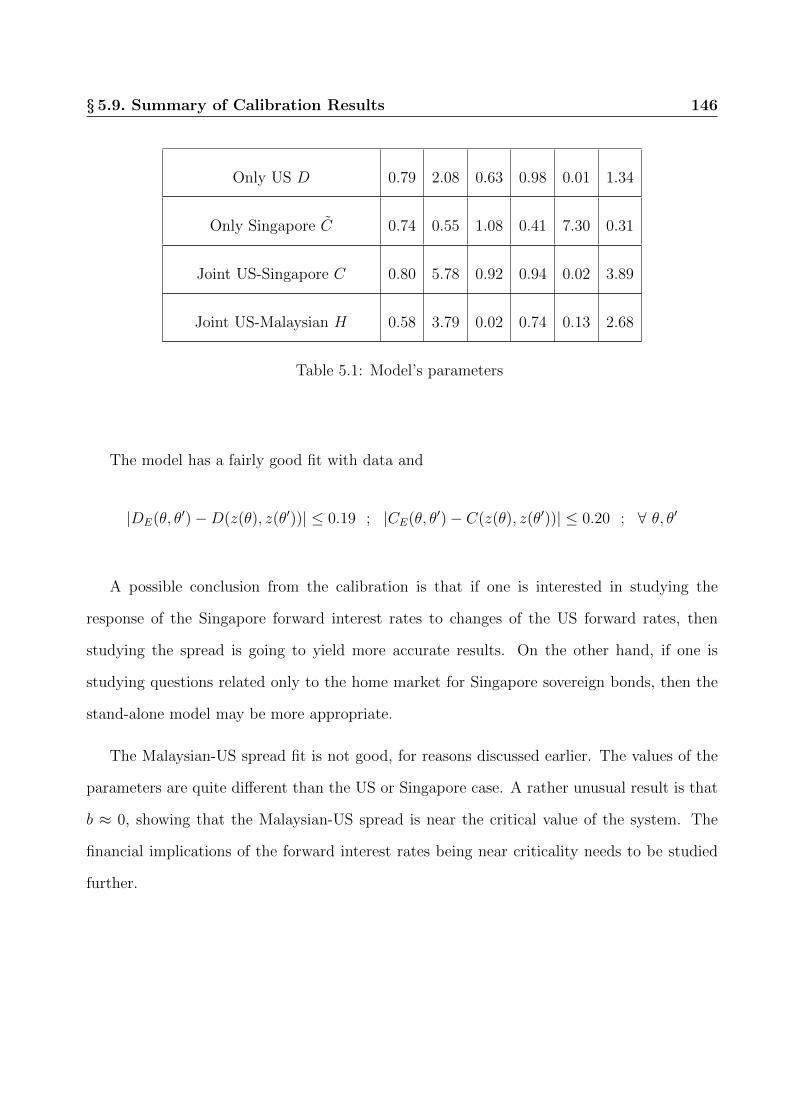

§ 5.9 Summary of Calibration Results . . . . . . . . . . . . . . . . . . . . . . . . . . 145

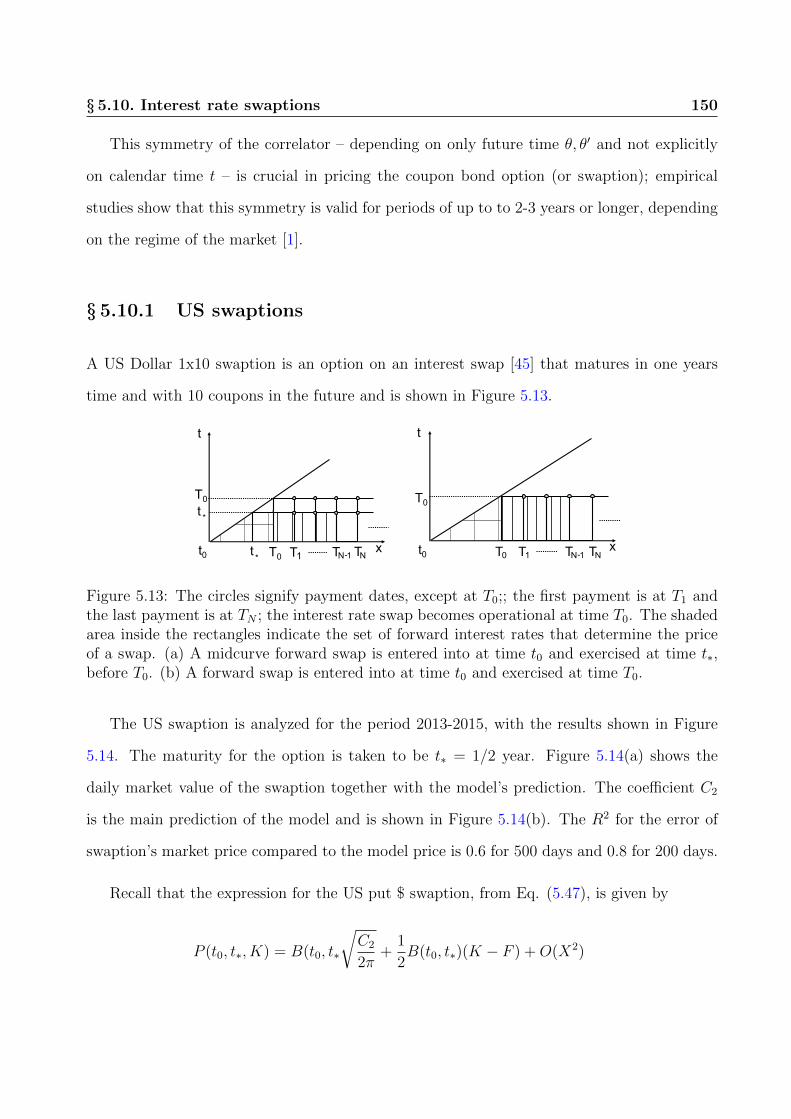

§ 5.10 Interest rate swaptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 147

§ 5.10.1 US swaptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150

§ 5.10.2 Singapore swaptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

§ 5.10.3 Malaysian swaptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

CONTENTS xii

§ 5.11 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

§ 5.12 Appendix 1: Risky coupon bond option . . . . . . . . . . . . . . . . . . . . . . 156

§ 5.13 Appendix 2: Swaptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

§ 5.14 Appendix 3: Black’s Model for Swaption . . . . . . . . . . . . . . . . . . . . . . 167

§ 5.14.1 Par value of fixed payments . . . . . . . . . . . . . . . . . . . . . . . . 169

§ 5.15 Appendix 4: Zero coupon bonds from coupon bonds . . . . . . . . . . . . . . . 169

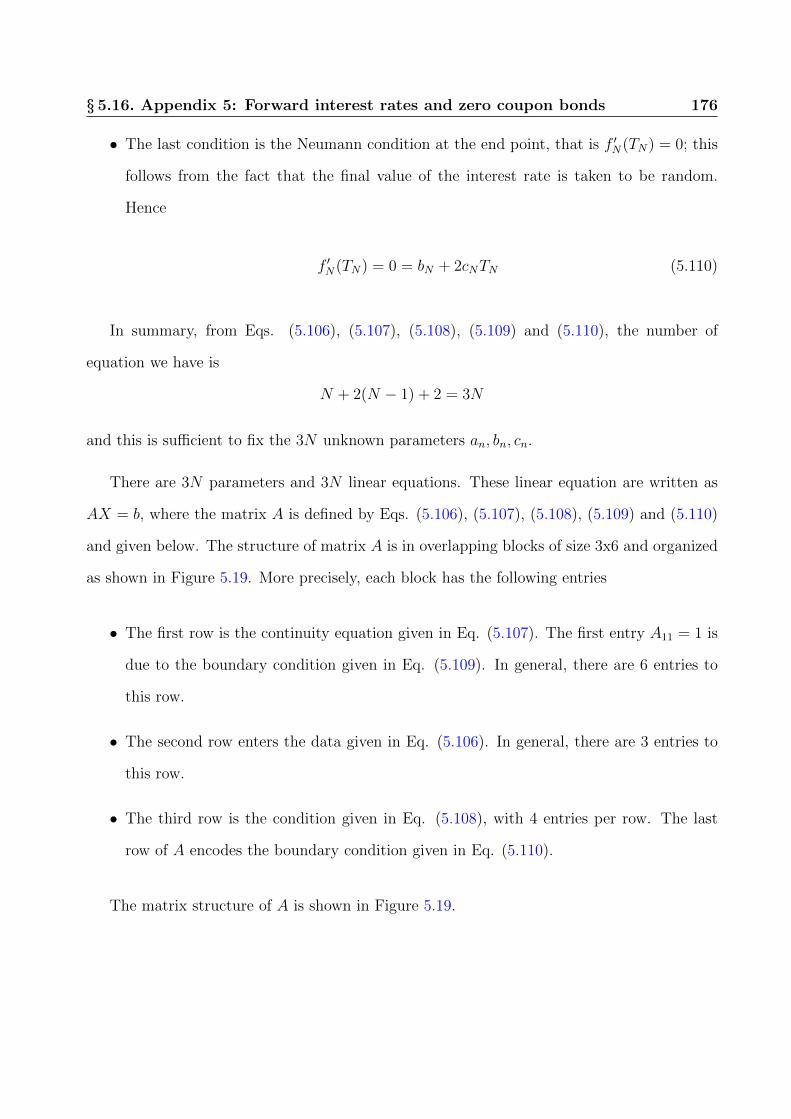

§ 5.16 Appendix 5: Forward interest rates and zero coupon bonds . . . . . . . . . . . 173

List of Tables

2.1 Number and Type of Commodity . . . . . . . . . . . . . . . . . . . . . . . . . 29

2.2 Gold-Silver. η = 0.7; λ = 0.1004 . . . . . . . . . . . . . . . . . . . . . . . . . . 34

2.3 Crude oil-Heating oil-Brent oil. η = 0.7; λ = 0.775 . . . . . . . . . . . . . . . . 35

2.4 Orangejuice-Cattle-Soybean. η = 0.7;λ = 1.132 . . . . . . . . . . . . . . . . . 36

2.5 Gold-Silver-Platinum. η = 0.7; λ = 0.344 . . . . . . . . . . . . . . . . . . . . . 38

2.6 Crude oil-Platinum-Cocoa. η = 0.70; λ = 0.54 . . . . . . . . . . . . . . . . . . 39

2.7 Gold-Silver-Crude oil-Natural gas. η = 0.70; λ = 0.260. . . . . . . . . . . . . . 41

2.8 Gold-Silver-Crude oil-Natural gas-Soybean oil-Cattle. η = 0.70; λ = 0.699. . . 42

2.9 Comparison of Single-Commodity fit(S-) with Multiple-Commodities fit(M-).

Group 1 is Gold-Silver-Crude oil (GSC) and Group 2 is Crude Oil-Platinum-

Cocoa (CPC) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

3.1 Calibration: Spot-Futures Correlations . . . . . . . . . . . . . . . . . . . . . . 72

3.2 Crude oil Calibration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

4.1 Fitting Parameters for Group 1 and 2 . . . . . . . . . . . . . . . . . . . . . . . 95

xiii

LIST OF TABLES xiv

4.2 Parameters for EURUSD Fitting . . . . . . . . . . . . . . . . . . . . . . . . . 105

5.1 Model’s parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

List of Figures

1.1 Option payoffs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.2 Supply and Demand in economics . . . . . . . . . . . . . . . . . . . . . . . . . 8

1.3 Supply and Demand as potential . . . . . . . . . . . . . . . . . . . . . . . . . 9

1.4 Random paths of the security . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.1 α = 0.1, β = 0.15, φ = 30, θ = 20 . . . . . . . . . . . . . . . . . . . . . . . . . . 25

2.2 α = 0.1, β = 0.15, φ = 20, θ = 20 . . . . . . . . . . . . . . . . . . . . . . . . . . 25

2.3 Matrix of ∆ij for 18 commodities. Note that for all pairs, |∆IJ | < 0.08 but one

case. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

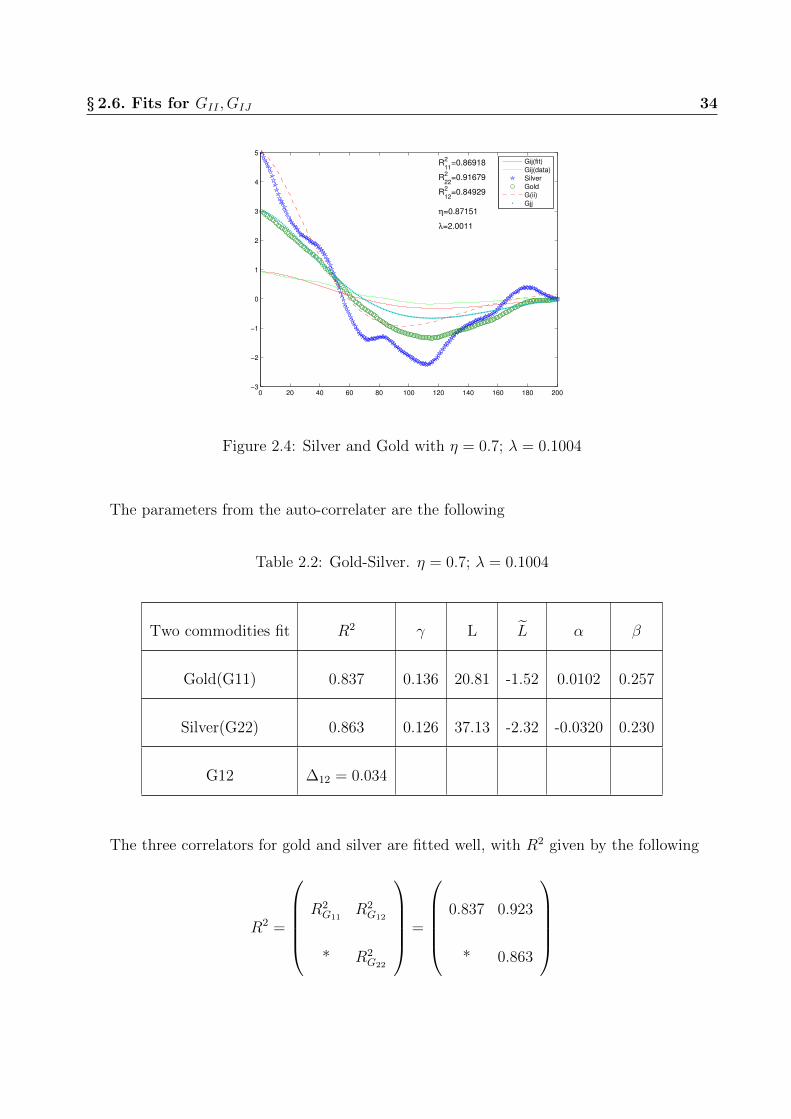

2.4 Silver and Gold with η = 0.7; λ = 0.1004 . . . . . . . . . . . . . . . . . . . . . 34

2.5 Crude oil-Heating oil-Brent oil (a)Autocorrelation and (b)Crosscorrelation with

η = 0.7; λ = 0.775 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

2.6 Orange juice-Cattle-Soybean (a)Autocorrelation and (b)Crosscorrelation with

η = 0.7;λ = 1.132 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

2.7 Gold-Silver-Platinum (a)Autocorrelation and (b)Crosscorrelation with η = 0.7;

λ = 0.344 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

xv

LIST OF FIGURES xvi

2.8 Crude oil-Platinum-Cocoa (a)Autocorrelation and (b)Crosscorrelation with η =

0.70; λ = 0.54. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

2.9 Gold-Silver-Crude oil-Natural gas (a)Autocorrelation and (b)Crosscorrelation

with η = 0.70; λ = 0.260. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

2.10 Gold-Silver-Crude oil-Natural gas-Soybean oil-Cattle (a)Autocorrelation and

(b)Crosscorrelation with η = 0.70; λ = 0.699. . . . . . . . . . . . . . . . . . . . 42

3.1 Points on the boundary are calendar time (t, t); (t′, t′) and points (t, ξ); (t′, ξ′)

are in future time. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

3.2 Theoretical plot of G(z+; z−) as a function of z+, z−, with α=1,L=1, γ1=1,γ2=2 61

3.3 Shape of the model for futures for a) α = 1, b) α > 1 and c) α < 1. . . . . . . 67

3.4 Fitting spot rates for a) Gold, b) Soybeans and c) Corn. The smooth curve is

the model’s best fit to data. (Jan 1 2011- Oct 18 2011) . . . . . . . . . . . . . 69

3.5 Model and market correlators for crude oil, with R2 = 0.93. (Sep 20 2014- June

11 2015) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

3.6 Spot and futures prices correlation G(t, ξ; 0, 0), plotted against t, ξ, of corn

futures prices with the spot price. a) The empirical propagator. b) The model

propagator. (Jan 1 2011- Oct 18 2011) . . . . . . . . . . . . . . . . . . . . . . 70

3.7 G(t, ξ; 0, 0) of Crude oil futures data. (Jan 1 2011- Oct 18 2011) . . . . . . . . 71

3.8 G(t, ξ; 0, 0) of Rice futures data. (Jan 1 2011- Oct 18 2011) . . . . . . . . . . . 71

3.9 G(t, ξ; 0, 0) of Gold futures data. (Jan 1 2011- Oct 18 2011) . . . . . . . . . . 71

LIST OF FIGURES xvii

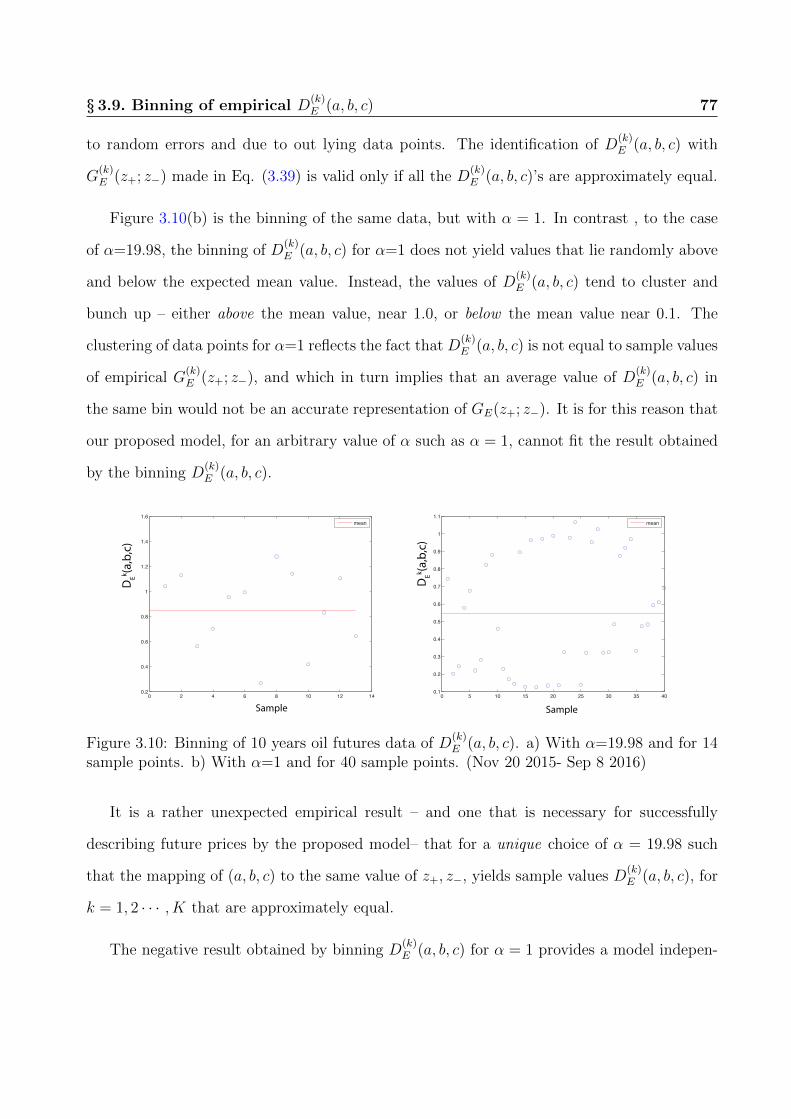

3.10 Binning of 10 years oil futures data of D(k)E (a, b, c). a) With α=19.98 and for

14 sample points. b) With α=1 and for 40 sample points. (Nov 20 2015- Sep

8 2016) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

3.11 a) Empirical GE(z+; z−) and b) Model GE(z+; z−) for market Oil futures prices.

(Nov 20 2015- Sep 8 2016) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

4.1 ν2(τ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

4.2√ν2/τ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

4.3 ξ(τ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

4.4 ζ(τ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

4.5 Shape of parameters with a = 5; b = 8; c = 100. τ is remaining time. . . . . . 92

4.6 The Forex martingale process. . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

4.7 The t and z values when η < 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

4.8 ν2(z) for Group 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.9 ν2(z) for Group 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.10 ξ(z) for Group 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.11 ξ(z) for Group 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.12 ζ(z) for Group 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.13 ζ(z) for Group 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.14 (a) The model variable x(t, τ) with different calendar times t, t′ but with the

same remaining time τ . (b) Model variable for fixed maturity time T , with

remaining time τ(t) 6= τ(t′). . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

LIST OF FIGURES xviii

4.15 (a) Model velocity for fixed remaining time τ . (b) Model velocity for fixed

maturity time T is found by comparing x(t, z(τ) to x(t− δ, z(τ + δ). . . . . . . 99

4.16 Pattern A, 2009-09-23 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

4.17 Pattern B, 2009-02-02 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

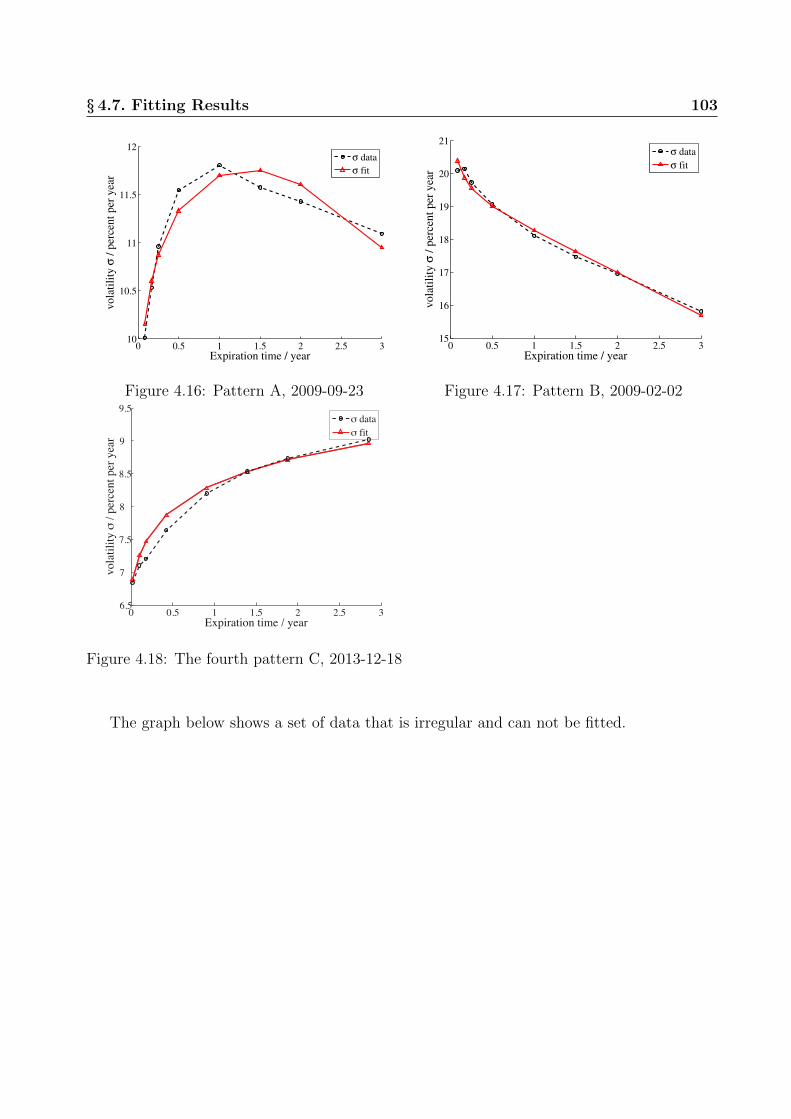

4.18 The fourth pattern C, 2013-12-18 . . . . . . . . . . . . . . . . . . . . . . . . . 103

4.19 Irregular data, 2008-08-28 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

4.20 Option price fitting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

4.21 ν2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

4.22 ξ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

4.23 ζ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

4.24 Option price fitting R2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

4.25 Option fitting rmse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

4.26 r . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

4.27 ω . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

4.28 λ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

4.29 η . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

4.30 TED and the financial crisis in 2008. . . . . . . . . . . . . . . . . . . . . . . . 108

4.31 (a) R2 of EURUSD and (b) Fx volatility of EURUSD . . . . . . . . . . . . . . 110

4.32 (a) R2 of AUDUSD and (b) Fx volatility of AUDUSD . . . . . . . . . . . . . . 111

4.33 (a) R2 of CHFUSD and (b) Fx volatility of CHFUSD . . . . . . . . . . . . . . 111

LIST OF FIGURES xix

4.34 (a) R2 of GBPUSD and (b) Fx volatility of GBPUSD . . . . . . . . . . . . . . 113

4.35 (a) R2 of JPYUSD and (b) Fx volatility of JPYUSD . . . . . . . . . . . . . . 114

5.1 a) The semi-infinite domain with two boundaries on which f(t, x) and A(t, x)

are defined. b) The zero coupon bond for two different times t0 and T0. . . . . 123

5.2 (a) Volatility of US forward interest rates. (b) Volatility of the spread of the

Singapore -US forward interest rates. Period from 9 May 2011 to 18 January,

2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 135

5.3 Empirical volatility function σ(θ) =√E[δf 2(t, θ)]c and kurtosis κ(t, θ) = E[δf(t, θ)4]/σ4(t, θ)−

3 of the forward interest rates; θ = x− t. (Reference: [1]). . . . . . . . . . . . 136

5.4 (a) Volatility of the Singapore stand-alone forward interest rates. (b) Compar-

ison of volatility of Singapore stand-alone forward interest rates of the US and

spread of the Singapore -US forward interest rates. Period from 9 May 2011 to

18 January, 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

5.5 US forward interest rates. (a) The empirical correlator DE(θ, θ′). (b) The

model correlator D(θ, θ′). Data from 9 May 2011 to 18 January, 2012. . . . . . 139

5.6 Singapore forward interest rates. (a) The empirical correlator CE(θ, θ′). (b)

The model correlator C(θ, θ′). Data from 9 May 2011 to 18 January, 2012. . . 139

5.7 Joint US-Singapore forward curve. (a) The empirical spread correlator CE(θ, θ′).

(b) The model spread correlator C(θ, θ′). Data from 9 May 2011 to 18 January,

2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

5.8 Inverse of propagator: (a) D−1DE (b) C−1CE (c) The Dirac delta function

δ(θ − θ′). Data from 9 May 2011 to 18 January, 2012. . . . . . . . . . . . . . . 141

LIST OF FIGURES xx

5.9 Correlation of Singapore - US forward interest rates spread with the US forward

interest rates. (a) The cross-correlator TE. (b) ∆E of the US forward interest

rates with the spread with the Singapore forward interest rates. (c) The model

coefficient function ∆. Data from 9 May 2011 to 18 January, 2012. . . . . . . . 142

5.10 (a) The Malaysian forward interest rates volatility v2(θ); half-yearly time steps

in the future time direction. (b) The volatility ζ(θ) of the Malaysian spread

over the US forward interest rates. Data from 9 May 2011 to 18 January, 2012. 144

5.11 (a) The Malaysian stand-alone propagator H(θ, θ′). (b) Propagator for the

spread, given by H(θ, θ′), of the Malaysian above the US forward interest rates.

(c) The model fitting the spread for Malaysian forward interest rates. Data from

9 May 2011 to 18 January, 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . 144

5.12 Domain for Gij. (a) For the case of Ti = Tj. (b) For the case of Ti 6= Tj. . . . . 149

5.13 The circles signify payment dates, except at T0;; the first payment is at T1 and

the last payment is at TN ; the interest rate swap becomes operational at time

T0. The shaded area inside the rectangles indicate the set of forward interest

rates that determine the price of a swap. (a) A midcurve forward swap is

entered into at time t0 and exercised at time t∗, before T0. (b) A forward swap

is entered into at time t0 and exercised at time T0. . . . . . . . . . . . . . . . . 150

5.14 The daily price of a US Dollar 1x10 swaption for the period 2013-2015. The

heavy (red) line is data. The blue line is the full model value of the swaption

with C2 The broken line is the value of the swaption withoutthe C2 coefficient.

(b) The value of C2 as a function of time. . . . . . . . . . . . . . . . . . . . . . 151

LIST OF FIGURES xxi

5.15 (a) Swaption of US, Singapore stand-alone and Singapore spread interest rates.

(b) Swaption of US and stand-alone Malaysian interest rates . Data for the

period 12 January 2012 to 20 October 2012. . . . . . . . . . . . . . . . . . . . 151

5.16 The shaded area is the domain of integration Ri. . . . . . . . . . . . . . . . . 157

5.17 The shaded domain of the forward interest rates contribute to Gij. For a typical

point t in the time integration, the figure shows the typical correlation function

M(x, x′; t) connecting two different values of the forward interest rates at future

time x and x′. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

5.18 Forward interest rate and future time lattice. . . . . . . . . . . . . . . . . . . . 174

5.19 The 3x6 block structure, with three elements overlapping between successive

rows, is shown in the figure. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 177

List of Symbols

Symbol Definition

p commodity price

x = ln p logarithmic commodity price

y = x−xσx

x after rescaled

D(p) demand function

S(p) supply function

V(p) potential

S,L action and Lagrangian

CIJ(t, t′) non-equal empirical correlation

GIJ(t, t′) non-equal time propagator

E(...) expectation of variable in the bracket

∆IJ correlation factor

z = λ(t/λ)η market time

C call option price

P put option price

K strike price of option

K(x, x′; v, v′; t) transition amplitude

P(x, x′; v, v′; t) conditional probability

xxii

xxiii

Symbol Definition

r spot rate

f(t, x) forward interest rate, at calendar time t, interest rate for

instantaneous deposit at future time x

for a loan from Tn to Tn + `

` Bond tenor, 90 days

B(t, T ) coupon bond price

R(t) Gaussian white noise

A(t, x) Gaussian quantum field

α(t, x) drift

σ(t, x) volatility

ζ(t, x) drift

D(t;x, x′), C(t;x, x′) forward rate propagator for different products

DE(t;x, x′), CE(t;x, x′) empirical forward rate propagators

Chapter 1

Introduction

§ 1.1 Review of financial market and financial modeling

The financial market is originally formed for easy transactions between buyers and sellers from

all over the world. As economics developing rapidly, bond, equity, commodity, option, futures

and other derivatives were invented to satisfy different requirements of different customers. In

comparison to the traditional economics, the finance nowadays becomes paperless transactions

and a platform for investor to predict the trend of the global economics and make money.

However, anyone interested in financial market soon discovers that the trend of the market is

always hard to forecast by experiences.

Due to the difficulty to predict the market, the quantitative finance is introduced to analyse

the trend of the market and help the country and people avoid the market inflation risk.

Although the mathematicians use quite complicated stochastic theories, partial differential

equations and other theories to analyse the market, some important factors and big waves

like the financial crisis cannot be predicted by these theories. New angle of view and theory

need to be considered to model the market.

As Simon Benninga said in his book [2], I liken the modeling of market to cooking and the

market data to the vegetables; the way one used in the financial modeling is like the sauce

1

§ 1.1. Review of financial market and financial modeling 2

you use. In this dissertation, the path integral and the quantum mechanics are the new sauce.

Quantum mechanics is firstly proposed by Max Planck in 1900. Quantum theory nowadays

has been developed and fully applied to optics, life science, cosmology, and so on, except the

finance. Baaquie opened the quantum finance chapter in 2001. The word “quantum” refers to

the quantum mathematics and theoretical methods of quantum mechanics and quantum field

theory which is powerful for analysing financial market data. Quantum mechanics represents

a random system by elements of a state space, and the time evolution of states is determined

by the Hamiltonian differential operator [3]. The main tool in analysing finance data, path

integral, is used for solving the time-series case in the financial market. The Feynman path

integral [3] calculates the probability amplitude of the element by multiplying together the

contributions of all paths in configuration space. Therefore the Feynman path integral is

efficient and logical for analysing the time dependent behaviour of the market data.

The path integral in finance is applied to the commodity market [4] modeled by an action

functional according to statistical microeconomics. The correlation functions are studied by

using perturbation expansion in Feynman path integral. The calibration fitting shows a very

good result which the index r-square is more than 0.97(1 means perfect fitting) for nine

main commodities. Although the model describes the market data very well, it ignores the

correlations between different commodities. Only in the whole market, the model is complete.

Hence the multiple commodities model and the correlations between the multiple commodities

still remain to be investigated.

Another application of the path integral is to describe and predict financial crisis by

modeling the Forex option pricing. Baaquie and Yang modelled the Forex option price by

the acceleration Lagrangian with the classical solution under strict boundary conditions [5].

Although the signal she found in her model is enough to illustrate the 2008 financial crisis, the

model has a shortage that one typical shape of the data can not be fitted by Baaquie-Yang

model. Some revisions need to be done to find out more reasonable model for the Forex option

§ 1.2. Introduction of financial instrument 3

price.

In addition, future is another important derivative in the market. However, it is very

difficult to model future price because the future price depends on two time parameters - one

is the calendar time; the other one is the future time. In physics, two time parameters are

described by the two-dimensional Lagrangians. Because of this reason, no one has worked out

a well-accepted model for the future price yet.

Finally the risk forward interest rate is a quite complicated concept in financial derivatives.

The model needs to be considered in two parts. Firstly, the risk-free forward interest rate,

US forward interest rate, has its own model. Secondly, the risk forward interest rate, such as

other country’s rate, depends on the risk-free rate and the behaviour of its own development.

So the model for both the risk-free and risk forward rate need to be designed properly. The

biggest challenge for this project is how to keep balance with this two parts.

§ 1.2 Introduction of financial instrument

§ 1.2.1 Commodity price and Futures

In finance, when we talk about commodity, it refers to the basic product instead of the

industrial product. Commodities in financial market are divided into two types. The first

type is called soft commodity, which are mainly agricultural products such as corn, soybean,

and wheat. The other type is called hard commodity, which consists of metal and oil such as

gold, silver, and crude oil. In the old time, people took their products to the market and tried

to sell them at a good price. The trading price is the“spot” price for the current market and

current time. In modern finance, commodity futures are one of the most original investing way

in commodity trading. Hence the spot price that shown on the screen is no longer the “spot”

§ 1.2. Introduction of financial instrument 4

price as before. It generates from a couple of different future contracts on the corresponding

commodity. Futures contract is a forward contract that allow the buyer or seller to buy or sell

some products at a deal price at an exact time in the future. The deal price that the buyer

and seller agreed is called the forward price. The exact time in the future is the time that the

seller delivers the product and the buyer pays for that.

§ 1.2.2 Option price

Option is another derivative in financial market. Due to its special design, it gives a broad

space for quantitative analysis.

There are two types of option, call option and put option, separately. A call option gives

the right to the holder to buy the underlying asset on an exact price on a determined date.

The put option is just the opposite guarantee for the holder to keep the right to sell the

underlying asset on an exact price on an determined date. The fixed price in option is called

strike price. It is a comparable price with the spot price of the underlying asset and should be

determined after discounting and premium. The exact date in option is called option expiry.

the option expiry is when the option goes to its maturity. When an option has expired, it can

no longer be traded.

There are two popular options that are highly active, which are European option and

American option respectively. The holder of the European option is able to exercise the right

of the option at the expiration date. In contrast, the American option gives the holder the

right to exercise at any time before the option expires.

Similarly as futures, each option has a maturity date in the future. Option is a derivative

that allows the holder to exercise or not. Therefore, assuming that there is an underlying

security S, let K be the strike price, T be the time expiry. For an European option, the pay

§ 1.2. Introduction of financial instrument 5

off functions are shown in the figure 1.1 .

Figure 1.1: Option payoffs

The figures are Long call (buy call option), Long Put (buy put option), Short Call (write calloption) and Short Put (write put option) and from https://en.wikipedia.org/wiki/Option.

Take the call option as an example for illustration. When time goes to the maturity date

T , the call option payoff function is as below

§ 1.2. Introduction of financial instrument 6

C(T, S(T )) =

S(T )−K, S(T ) > K,

0, S(T ) < K,

≡ [S(T )−K]+.

(1.1)

§ 1.2.3 Interest rate

The interest rate is originally created to define how much one should pay when he borrow

some amount of money before. Now the concept interest rate mainly used for the special

lender, banks. Assuming that the annual interest rate is r, consider one borrows money M

from a bank. After T years, he should pay M(1 + rT ) back because of the inflation. The

compounded interest occurs if one can reinvest immediately when the money is payed back.

Suppose the money can be reinvested n times per year, the total pay back is M(1 + r/n)nT .

When n goes to infinity, the payback becomes MerT .

The forward interest rate is the interest rate in the future. The forward interest rate for

a specified future time can be determined with the current interest rate and the unbiased

expectation of the future. In comparison with the current interest rate, the forward interest

rate will be shown as after one year, the one year interest rate’ which represents the interest

rate of next year.

§ 1.2.4 Bond

The bond is a fix-income security, under which the issuer owes the holders a debt and is

obliged to pay them the coupon or to repay the principal at a later date, termed the maturity

date. The coupon can be considered as the interest. The current yield shows the annual

§ 1.2. Introduction of financial instrument 7

return calculated with the annual coupon payments and the current price of the bond. Let

the current market price be MP and the annual coupon paid be C. The current Yield is CMP

.

The current yield simply shows the return for the total year but it doesn’t include the time

variance. The yield to maturity (YTM) is introduced to show the interest rate including the

future cash flow. The expression of the bond price B is as below

B =C1

(1 + y)1+

C2

(1 + y)2+ ...+

Clast(1 + y)n

, (1.2)

where

Cn is the nth coupon payment,

B is the bond price,

y is the yield to maturity,

Clast is equal to the principal P + CN and

N is the total number of payment.

§ 1.2.5 One type of swaption: bond option

Bond option is a typical swaption that gives the holder the right to buy a bond at the maturity

date. Because both option and bond are including the future time, Bond option is invested

highly depending on the personal prospection of the future market and since the Black-Sholes

model assumes constant volatility [6], which cannot describe the bond option, the Black-Sholes

model cannot easily be used in the bond option.

§ 1.3. Introduction of financial models 8

§ 1.3 Introduction of financial models

§ 1.3.1 Lagrangian model based on supply and demand

In microeconomics, the “supply and demand” is the basic model of price determination for

commodities. It describes the market that in a competitive market, the price of any commodity

will keep changing until it reaches to a point that the quantity demanded equals the quantity

supplied.

Figure 1.2: Supply and Demand in economics

Figure copies from http://www.investopedia.com/university/economics/economics3.asp

The point (P ∗, Q∗) in figure 1.2 is the equilibrium point for one commodity. In physics,

the potential is defined based on supply and demand. The equilibrium point is the deepest

point of the potential V as showed in figure 1.3.

The potential V is designed as below

§ 1.3. Introduction of financial models 9

Figure 1.3: Supply and Demand as potential

V [p] = D[p] + S[p]

= m

[N∑i=1

dipaii

+N∑i=1

sipbii

]; di, si > 0 ; a, b > 0, (1.3)

where di, si, ai, bi are independent constants for each commodity. The Lagrangian is combined

with the potential term and kinetic term. The dynamics of the market are described by the

kinetic term of the Lagrangian. With the numerical analyse, the total Lagrangian is optimised

as the following

L(t) =1

2

N∑i,j=1

[Lij

∂2xi∂t2

∂2xj∂t2

+ Lij∂xi∂t

∂xj∂t

]+

N∑i=1

dipaii

+N∑i=1

sipbii (1.4)

The quantities Lij, Lij, di, si, ai, bi are all real and independent parameters. Matrix Lij is

symmetric and positive definite. Because prices (and quantities) are always positive and

hence represented by exponential variables as pi = pi0exi . The Lagrangian is given by

§ 1.3. Introduction of financial models 10

L(t) =1

2

N∑i,j=1

[Lij

∂2xi∂t2

∂2xj∂t2

+ Lij∂xi∂t

∂xj∂t

]+

N∑i=1

dip0i

e−aixi +N∑i=1

sip0iebixi (1.5)

The Lagrangian given in Eq. (1.5) is nonlinear.

§ 1.3.2 Black-Scholes model for option pricing

In 1973, Fisher Black, Myron Scholes, and Robert Merton gives a mathematical model for a

European option price [6], which is well known as the Black-Sholes model. This model is now

widely used in options market.

The assumptions of the Black-Scholes model are shown as the following:

• No arbitrage opportunity in the market (efficient market)

• People can borrow or lend money at a risk-free rate

• Volatility of the underlying is known and constant

• No transaction fees or dividends during the life of the option

• The log security (return of the security) follows a normal distribution

Let t be the calendar time. The underlying asset price S(t) yields

dS(t)

dt= αS(t) + σS(t)R(t), (1.6)

where α is the drift and σ is the volatility of underlying. The white noise R(t) satisfies

E[R(t)] = 0; E[R(t)R(t′)] = δ(t− t′). (1.7)

§ 1.3. Introduction of financial models 11

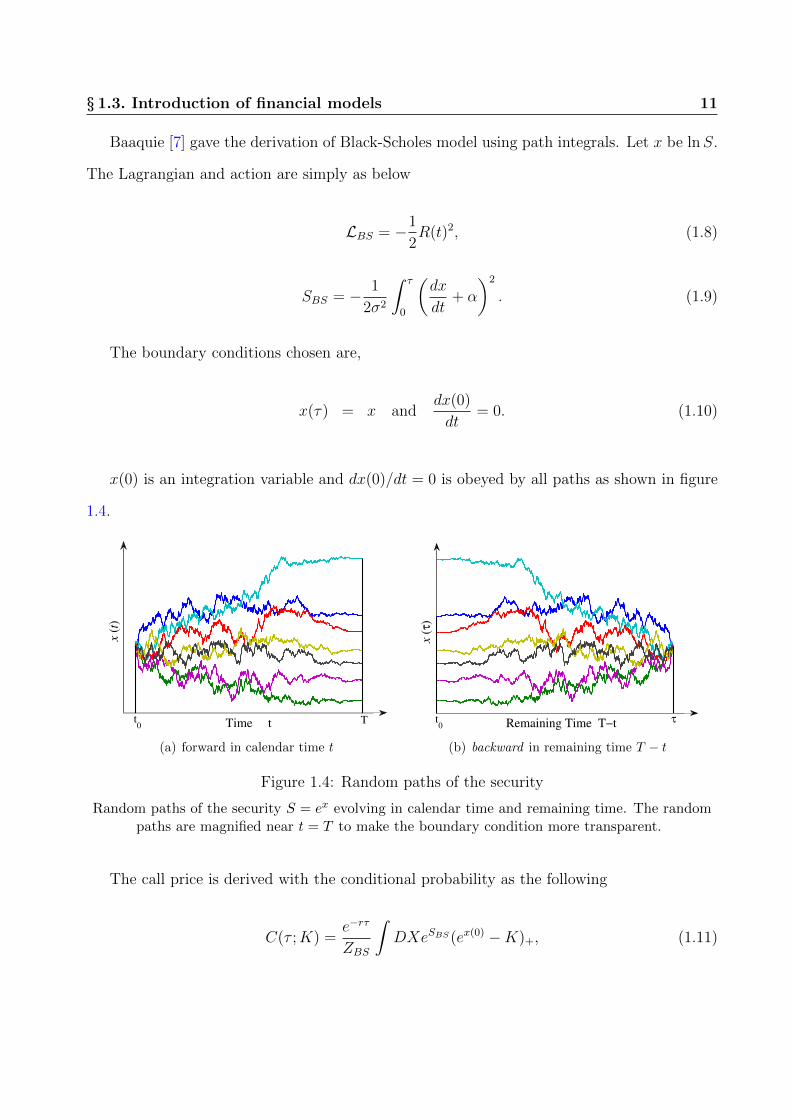

Baaquie [7] gave the derivation of Black-Scholes model using path integrals. Let x be lnS.

The Lagrangian and action are simply as below

LBS = −1

2R(t)2, (1.8)

SBS = − 1

2σ2

∫ τ

0

(dx

dt+ α

)2

. (1.9)

The boundary conditions chosen are,

x(τ) = x anddx(0)

dt= 0. (1.10)

x(0) is an integration variable and dx(0)/dt = 0 is obeyed by all paths as shown in figure

1.4.

Time t

x (

t)

t0

T

(a) forward in calendar time t

Remaining Time T−t

x (

τ)

t0

τ

(b) backward in remaining time T − t

Figure 1.4: Random paths of the security

Random paths of the security S = ex evolving in calendar time and remaining time. The randompaths are magnified near t = T to make the boundary condition more transparent.

The call price is derived with the conditional probability as the following

C(τ ;K) =e−rτ

ZBS

∫DXeSBS(ex(0) −K)+, (1.11)

§ 1.3. Introduction of financial models 12

where

ZBS =∞∏n=0

N∏i=1

∫ ∞−∞

dxnieSBS . (1.12)

From Eq. (1.11), Black-Scholes formula can be derived with the boundary condition as in

Eq. (1.10) and is shown as below

C = SN(d+)− e−rτKN(d−),

d± =ln(S/K) +

(r ± σ2

2

)τ

σ√τ

,

(1.13)

where K is the strike price of the option, σ is the volatility, r is the spot interest rate, and

σ√τ is the standard deviation of x. N(x) is the cumulative distribution given by

N(x) =1√2π

∫ x

−∞e−

12z2dz. (1.14)

The volatility can be calculated by historical data. Since the Black-Sholes model is recog-

nized by financial market, the market quotes the price of option in implied volatility.

§ 1.3.3 HJM Model for forward interest rate

The most widely used model in bond and interest rate field nowadays is Health-Jarraw-

Morton(HJM) model [8]. The forward interest rate f(t, x), is the prediction of interest rate

fixed by future time x > t at time t. The bond market is determined by f(t, x). Let R(t) be

Gaussian white noise and the expectation and correlation of R(t) is given by

E[R(t)] = 0 ; E[R(t)R(t′)] = δ(t− t′).

§ 1.3. Introduction of financial models 13

The HJM model is a linear model

∂f(t, x)

∂t= α(t, x) + σ(t, x)R(t). (1.15)

where α(t, x) is the drift and σ(t, x) is the volatility of data. A single white noise R(t) is

used to describe the forward interest rates but it cannot fully cover the evolution of forward

rate correlation. It is proper to replace the one-dimension white noise by a two-dimension

quantum field A(t, x).

The derivation of the quantum HJM model [1] is shown as below

∂f

∂t(t, x) = α(t, x) + σ(t, x)A(t, x), (1.16)

f(t∗, x) = f(t0, x) +

∫ t∗

t0

dtα(t, x) +

∫ t∗

t0

dtσ(t, x)A(t, x), (1.17)

where the drift can be calculated by martingale as the following

α∗(t, x) = σ(t, x)

∫ x

t∗

dx′D(x, x′; t)σ(t, x′). (1.18)

Chapter 2

Multiple Commodities in Statistical

Microeconomics: Model and Market

§ 2.1 Introduction

The theory of prices proposed in [9] is based on the concept of the action functional; the

subsequent publication [4] provides strong empirical evidence in support of this formulation for

the case of single commodities. The present paper extends the analysis to multi-commodities

by modifying the single commodity model in a parsimonious manner.

The theory of commodity prices [10] is one of the bedrocks of microeconomics and usually

starts with the concept of the utility function of a typical consumer [11, 12] . A maximization

of the utility function with a budget constraint yields the demand for the commodities as a

function of price. The supply function is obtained by maximizing the profit for the producers

and the market prices of commodities in conventional microeconomics are fixed by equating

supply with the demand[11, 12].

In contrast to conventional microeconomics, in statistical microeconomics [9] the prices

of all commodities are taken to be intrinsically random – and the probability distribution

function of prices is fixed by the exponential of the so called action functional. The action

14

§ 2.1. Introduction 15

functional in turn is the sum of two parts, a ‘kinetic’ term that determines the dynamical

evolution of commodity prices and a microeconomic potential that is the sum of the supply

and demand functions. The action functional contains all the information of the market and

determines the distribution of market prices as well as the change in market prices as the

prices evolve in time [13, 14, 15].

The primary focus in the statistical microeconomic formulation is to describe the unequal

time correlation functions of market prices. The auto- and cross-correlation [16, 17] functions

for multiple commodities is modeled using the action functional and the Feynman path inte-

gral. The action functional is calibrated by matching the prediction of the model’s correlation

functions with the observed market and provides a stringent test of the accuracy of the model.

The microeconomic potential for commodity with price p is given by V [p] and has been

introduced in [9]; the potential has its minimum value at its extrema p, given by

∂V [p]/∂p = 0.

The price p is taken to be the average commodity price.

What happens when the price p is not equal to the average price p, that is, p 6= p? The

microeconomic potential V [p] in this case causes the prices to ‘move’, that is, to change and

tend towards p. Clearly, the more abrupt the change, the more unlikely it is; the change of

price should, for normal market conditions, be gradual and relatively ‘smooth’. To achieve this

smooth movement of the prices in general, a ‘kinetic term’ T [p(t)] is introduced. Although

the concept of the kinetic term is taken from physics, it finds a natural expression in the

evolution of the prices of commodities: the specific form of the kinetic term is determined by

the study of market data [9]. The kinetic term in the action functional is seen to be strongly

supported by market data, and as of now has no clear theoretical explanation. One can only

speculate that demand and supply are determined by consumers and producers, respectively

§ 2.2. The microeconomic action functional 16

and that the kinetic term reflects the process of circulation, distribution and exchange – as

well as the degree of market liquidity – that is necessary for the products to make a transition

from the producer to the final consumer in the market.

One rather unexpected result is that the kinetic term in the action functional has a domi-

nant role in the evolution of commodity prices; due to the high time derivative of prices in the

kinetic term, the short term evolution of commodity prices is completely dominated by the

kinetic term, with the microeconomic potential, containing the supply and demand functions,

come into play for the long term evolution.

§ 2.2 The microeconomic action functional

Consider N commodities, with market prices given by pI ; I = 1, .., N . Prices are always pos-

itive and can be represented by exponential variables as pI = p0exI ; the normalized logarithm

of prices, denoted by xI , is defined as follow

pI = p0IexI ; xI(t) = ln(pI(t)/p0I) ; I = 1, .., N.

The demand function and the supply function are modeled to be [9]

D[p] =N∑i=1

dip0ie−aixi ; S[p] =

N∑i=1

sip0iebixi ; di, si > 0 ; a, b > 0. (2.1)

The coefficients di, si, according to [9], are determined by macroeconomic factors such as

interest rates, unemployment, inflation and so on.

For the purpose of modeling, prices in statistical microeconomics are expressed in terms

of variables that are measured from the average value and normalized by the volatility of the

§ 2.2. The microeconomic action functional 17

stock.

yi(t) =xi(t)− xi

σi; i = 1, .., N. (2.2)

xI and σI are the average value of yI . The volatility of xI(t) for the time period being

considered and are given by

xi = E[xi] ; σ2i = E[

(xi − xi

)2].

The normalized variables yi are all of O(1) and hence one can model and compare commodities

with vastly different volatilities and prices. In the statistical microeconomic approach, the

microeconomic potential is the fundamental quantity that combines supply and demand by

considering their sum [9]. The supply and demand yield the microeconomic potential given

by

V =N∑i=1

[dip0ie

aixie−aiσiyi + sip0ie−bixiebiσiyi

]≡

N∑i=1

[die−aiyi + sie

biyi], (2.3)

where

di = dip0ieaixi ; si = sip0ie

−bixi ; ai = aiσi ; bi = biσi.

For the case of multiple commodities, the microeconomic potential for the N -commodities

is further generalized by including a term that depends on the product of the prices of com-

modities – and which cannot be placed either in the demand or in the supply component of

§ 2.2. The microeconomic action functional 18

the microeconomic potential. The multiple commodity microeconomic potential is given by

V [p] = D[p] + S[p] + corrrelation term

=N∑i=1

[die−aiyi + sie

biyi]

+1

2

N∑ij;i 6=j

∆ijyiyj. (2.4)

The ∆ij term is introduced to model the cross-correlation of the different commodities.

The motivation for the ∆ij term is the following. The fit for the single commodity using

the microeconomic potential is very accurate [4]. Hence, one would expect that the effect of

multiple commodities should be a perturbation on the single commodities potential. This is

the reason that the simplest modification of the single commodity microeconomic potential is

used for modeling multiple commodities, and for consistency we expect ∆ij to be small.

The dynamics of the prices for N -commodities is determined by the kinetic term T [p(t)]

that, in general, is given by

T [p(t)] =1

2

N∑i,j=1

[Lij

∂2yi∂t2

∂2yj∂t2

+ βij∂yi∂t

∂yj∂t

].

Similar to the reason that led to modeling the cross-correlations by the ∆ij term in the

microeconomic potential V , we continue to model the kinetic term to be solely determined by

the single commodity, with all the correlation coming from the ∆ij term. Hence, the kinetic

term is chosen to be diagonal, with no cross-terms amongst the different commodities and is

given by

T [p(t)] =1

2

N∑i

[Li

(∂2yi∂t2

)2

+ Li

(∂yi∂t

)2]. (2.5)

§ 2.2. The microeconomic action functional 19

The Lagrangian is given by the sum of the kinetic and potential factors and yields [9]

L(t) = T [p(t)] + V [p(t)].

The Lagrangian, from Eqs. (2.4) and (2.5), is the following

L(t) =1

2

N∑i

[Li

(∂2yi∂t2

)2

+ Li

(∂yi∂t

)2]

+N∑i=1

[die−aiyi + sie

biyi]− 1

2

N∑ij;i 6=j

∆ijyiyj. (2.6)

The Lagrangian given in Eq. (2.6) is nonlinear.

The action functional determines the dynamics (time evolution) of market prices and is

given by

A[p] =

∫ +∞

−∞dtL(t) =

∫ +∞

−∞dt(T [p(t)] + V [p(t)]

).

All prices of commodities are considered to be stochastic variables and the action functional

is assumed to determine the probability distribution, which is given by

Probability distribution for a specific time evolution ∝ e−A[y]

All correlation functions of the prices are given by the Feynman path integral [9, 3]

D123...n(t1, t2, ...tn) = E[y1(t1)y2(t2) · · · yn(tn)] =1

Z

∫Dye−A[y]y1(t1)y2(t2) · · · yn(tn)

with

Z =

∫Dye−A[y].

§ 2.3. Correlation Function 20

§ 2.3 Correlation Function

We study the leading terms in the Lagrangian by doing a Taylor expansion of the potential

term V about its minima, which will turn out to coincide with an expansion of V in a power

series in yi.

The minima xi is defined by

∂V(x)

∂xi= 0.

Hence from Eq. (2.4)

∂V(x)

∂xi= −aidip0ie

aixi + bisip0iebixi −

∑j,i6=j

∆ij(xj − xjσj

) = 0. (2.7)

In our model, we assume that the equilibrium price of the commodities x is given by its

average value x and yields

xi = xi. (2.8)

Hence, from Eq. (2.7)

− aidieaixi + bisiebixi = 0. (2.9)

Note that Eq. (2.9) is independent of p0i and hence p0i does not enter the calibration of the

model’s parameters. Eq. (2.9) yields

exi =

(aidi

bisi

)(1/(ai+bi))

. (2.10)

Eqs. (2.3), (2.8) and (2.10) yield

aidi = bisi. (2.11)

§ 2.3. Correlation Function 21

§ 2.3.1 Expansion of Potential

From the definition of yi given in Eq. (2.2), the minima of the action is about yi = 0. Hence,

expanding the Lagrangian about yi = 0 yields

L =∑i

(1

2Liyi

2 +1

2Liyi

2 +γi2y2i +

αi3!y3i +

βi4!y4i + · · · )− 1

2

∑ij,i6=j

∆ijyiyj.

Define the Lagrangian in terms of the quadratic and nonlinear terms as follow

L = L2 + L3 + L4 +O(y5).

L2(x) are the quadratic terms in the expansion of the Lagrangian given above and L3(x),L4(x)

are the cubic and quartic terms.

The quadratic Lagrangian is given by

L2 = L0 + Lc,

L0 =1

2

∑i

[Liyi

2 + Liyi2 + γiy

2i

]; Lc = −1

2

∑ij;i 6=j

∆ijyiyj,

and the nonlinear terms are

L3 =αi3!y3i ; L4 =

βi4!y4i .

The action is given by the following

A = A0 +Ac +AI =

∫dtL;

A0 =

∫dtL0 ; Ac =

∫dtLc

AI =

∫dt(L3 + L4).

§ 2.3. Correlation Function 22

From above we have

γi =1

2(dia

2i + sib

2i ), (2.12)

αi = (−a3i di + b3

i si) = (bi − ai)γi, (2.13)

βi = (a4i di + b4

i si) = (a2i − aibi + b2

i )γi. (2.14)

The linear term in yi is zero due to Eq. (2.11). We will determine the values of α, β, γ, y from

market data; the potential parameter of ai, bi, si, di are then given by the following

ai =±√

4βiγi − 3α2i − αi

2γi; bi = ai +

αiγi

;

si =γi

bi(ai + bi); di =

γiai(ai + bi)

.

The positive branch for ai is used since ai > 0.

§ 2.3.2 Auto-correlation

The correlation function for the A0 is given by the Gaussian propagator

D(0)(t− t′) =1

Z

∫Dye−A0[y]yI(t)yJ(t′).

and the auto-correlation function is given by

D(0)II (t− t′) ≡ D

(0)I (t− t′) =

1

Z

∫Dye−A0[y]yI(t)yI(t

′) +O(∆2).

§ 2.3. Correlation Function 23

Using a Fourier transform to evaluate the propagator for the prices, and dropping the

subscript I, yields

D(0)(t− t′) ≡∫ ∞−∞

dk

2π

eik(t−t′)

Lk4 + Lk2 + γ=

e−√a−|t−t′|√a−

− e−√a+|t−t′|√a+

2L(a+ − a−);

a± =L

2L± | L

2L|

√1− 4Lγ

L2.

Case I: Real branch. 4Lγ < L2 and a± is real; let

ω = (γ

L)14 , a± =

√γ

Le±2ϑ, e±2ϑ =

√L2

4Lγ+

√L2

4Lγ− 1.

Hence D(0)(t− t′) is given by

D(0)(t− t′) =ωe−ω|t−t

′| cosh(ϑ)

2γ sinh(2ϑ)sinh[ϑ+ ω|t− t′| sinh(ϑ)].

Case II: Complex branch. 4Lγ > L2 and a± are complex; let

ω = (γ

L)14 , a± =

√γ

Le±i2φ, cos(2φ) =

√L2

4Lγ, sin(2φ) =

√1− L2

4γL. (2.15)

We hence obtain the complex branch propagator

D(0)(t− t′) =ωe−ω|t−t

′| cos(φ)

2γ sin(2φ)sin[φ+ ω|t− t′| sin(φ)].

Define the normalization constant

N =ω

2γ sin 2φ.

§ 2.3. Correlation Function 24

and yields the complex branch propagator

D(0)(t− t′) = N e−ω|t−t′| cos(φ) sinφ+ ω|t− t′| sin(φ). (2.16)

The auto-correlation function of commodities will be seen to follow the behavior given by the

complex branch. The real branch cannot describe the data from market.

§ 2.3.3 Cross-correlation

The cross-correlation function is given by I 6= J. The model yields

E[yI(0)yJ(τ)] = DIJ(t) =1

Z

∫Dye−(A0+Ac)yI(0)yJ(τ)

=1

Z

∫Dye−A0[y]yI(0)yJ(τ)

[1 +

1

2

∑ij;i 6=j

∆ij

∫dtyi(t)yj(t) +O(∆2)

].

The first term is zero and hence

DIJ(τ) ' D(0)IJ (t), (2.17)

where

D(0)IJ (t) ≡

∫ ∞−∞

D(0)I (t)D

(0)J (t− τ)dt.

From Appendix Eq. (2.28):

D(0)IJ (t) =

C

LILJ

( 1

αe−|t|α cosφ[

1

R(h1/R) cos φ− (h2/R) sin φ − 1

T(h3/T ) cos φ− (h4/T ) sin φ]

+1

βe−|t|βcosθ[

1

P(h5/P ) cos θ − (h6/P ) sin θ − 1

Q(h7/Q) cos θ − (h8/Q) sin θ]

),

(2.18)

§ 2.3. Correlation Function 25

with

C =−1

4

1

α2β2 sin 2φ sin 2θ; φ = φ+ |t|α sinφ; θ = θ + |t|β sin θ.

Coefficients h1− h8, P,Q,R, T are given in Eq. (2.31)

Figures 2.1 and 2.2 below are plots of the cross-correlator for some typical values of the

model’s parameter of the complex branch. The shape of the cross-correlator given by the

model will be seen to be consistent with the result obtained by fitting the model to market

prices.

0 20 40 60 80 100 120 140 160 180 200−4

−3

−2

−1

0

1

2

3

4

5

6x 10

6

α=0.1β=0.15φ=30θ=20

Figure 2.1: α = 0.1, β = 0.15, φ = 30, θ = 20

0 20 40 60 80 100 120 140 160 180 200−1

−0.5

0

0.5

1

1.5

2

2.5x 10

6

α=0.1β=0.15φ=20θ=20

Figure 2.2: α = 0.1, β = 0.15, φ = 20, θ = 20

§ 2.3.4 Nonlinear terms

As discussed in detail in [4], the correlation function to leading order for the nonlinear coupling

yields

E[y2I (t)]c = D

(0)I (0)− βI

2D

(0)I (0)

∫dz(D

(0)I (z))2 +O(∆2), (2.19)

E[y3I (t)]c = −2αI

∫ ∞0

dz(D(0)I (z))2 +O(∆2), (2.20)

E[y4I (t)]c = 3(D

(0)I (0))2 − 2βI

∫ ∞0

dz(D(0)I (z))4 +O(∆2). (2.21)

§ 2.4. Market data and model 26

Some integrations that are useful to solve the potential prameters a, b, s, d are the following

[3] ∫ ∞0

D(0)(τ)dτ = N sin 2φ

ω,

∫ ∞0

(D(0)(τ))2dτ = N 2 secφ− cos 3φ

4ω,

∫ ∞0

(D(0)(τ))3dτ = N 3 2 sin3 φ(11 cosφ+ 2 cos 3φ)

4ω,

∫ ∞0

(D(0)(τ))4dτ = N 4 sinφ3(50 cos 2φ+ 6 cos 4φ+ 47) tanφ

16ω(3 cos 2φ+ 5).

Using four equations 2.11, 2.19, 2.20 and 2.21, potential parameters ai, bi, si, di can be ob-

tained.

§ 2.4 Market data and model

The empirical correlator is denoted by the notation of GIJ(t) and is defined by the expectation

value of the market prices. For a time series data set with time interval of ε, the prices are

given by yI(t) = yI(n), where t = nε and we have τ = kε; for N data points, the correlator is

given by the moving average

GIJ(τ) = GIJ(k) = E[yI(0)yJ(k)]c

∣∣∣market

=1

N

N−k∑n=0

yI(n)yJ(n+ k).

The numerical evaluation of the correlators is obtained by taking the moving average over the

data set. The model always yields a correlator that is a symmetric function of IJ , which is

not necessarily the case for the market correlator [9]. To equate the market correlator with

the model, it is made symmetrically, namely

GIJ(τ) = GJI(τ).

§ 2.4. Market data and model 27

and in terms of the underlying data we have

GIJ(τ) =1

2[

1

N

N−k∑n=0

yI(n)yJ(n+ k) +1

N

N−k∑n=0

yJ(n)yI(n+ k)].

The parameter of time for the market and model are not the same. The reason being that

time for traders is determined by the liquidity of the market and rate of transactions [7]. To

reflect this feature of the market, define market time z(τ) by

τ → z(τ).

The empirical correlator G(τ) is given by the exact model correlator D(τ) by the relation

GIJ(t) = DIJ(z(t)). (2.22)

For single commodity fit

D(0)II (z(t)) = N e−ωIz(t) cos(φI) sinφI + ωIz(t) sin(φI).

For cross-correlation DIJ , we use Eq. (2.18) to fit the market cross-correlator.

According to Ref. [4], for single commodity fit, using GII(t) ≡ GI(t), we have

GI(t) = D(0)I (z(t))− βI

2D

(0)I (0)

∫dτD

(0)I (z(t)− τ)D

(0)I (τ) +O(∆2). (2.23)

Let∫dτ(D

(0)I (τ))2 = CI . When τ equals to zero,

GI(0) ' D(0)I (0)− βI

2D

(0)I (0)CI = D

(0)I (0)(1− βI

2CI). (2.24)

§ 2.5. Fitting with Market Data 28

For the auto-correlation GII , note that the empirical definition of x and σ implies that

GI(0) = 1.

Hence

1 = GI(0) = D(0)I (0)− βI

2D

(0)I (0)CI ⇒ D

(0)I (0) =

1

1− βI2CI. (2.25)

Eq. (2.25) is consistent with Eq. (2.24). Substituting D(0)I (0) into GI(t), for t > 0 – using

Eq. (2.16) for the numerator and denominator – we obtain1

GI(t) =D

(0)I (z(t))

D(0)I (0)

=1

sinφe−ωz(t) cos(φ) sinφ+ ωz(t) sin(φ). (2.26)

We use D(0)I (z(t))/D

(0)I (0) to fit GI(t) in the single commodity case. Hence, once we have

obtained φI , ωI all the parameters of the complex branch of the model can be determined.

§ 2.5 Fitting with Market Data

As a rule, the correlators evaluated from the data are denoted by GIJ and the result obtained

by fitting the model are denoted by DIJ . The numbering for the indices I, J for the various

commodities is the one given in Table 2.1.

We analyze 18 commodities daily data drawn from four major groups of energy, metal,

food, grain, from 2014/01/01 to 2015/02/03 download from

Investing.com/commodities/real-time-futures.2 Since the correlators are symmetric, there are

1The approximation makes the result consistent with the value of GI(0) = 1.2Real-time streaming quotes for the top commodities futures CFDs. The quotes are available for a variety

of futures such as Gold, Crude Oil, Silver, Copper and many more Metals, Energies and Softs futures. Thelatest price as well as the daily high, low and the change for each future. The ”Base” price is the last close of

§ 2.5. Fitting with Market Data 29

153 correlators in total, with 18 auto-correlation functions and 153 cross-correlation functions.

Table 2.1: Number and Type of Commodity

Number commodity Type Number commodity Type

1 Crudeoil Energy 10 Cocoa Food

2 Heatingoil 11 Soybeansoil

3 Brentoil 12 Orangejuice

4 Natural gas 13 Livecattle

5 Copper Metal 14 Wheat Grain

6 Gold 15 Corn

7 Silver 16 Soybean

8 Platinum 17 Roughrice

9 Palladium 18 Cotton Misc

All the auto-correlation functions can be fit to a high degree of accuracy and confirms the

results found in [4] for single commodities.

The model can fit the majority of the cross-correlators Gij(i 6= j) which are generically

similar to the shape that the model generates from Eq. (2.18) and shown in Figures 2.1 and

2.2. Of the 153 cross-correlators, 110 are of the shape that the model can fit quite well. The

rest of the cross-correlators Gij have features that the model cannot fit; in particular, if the

each future contract (as of 16:30 ET). The change is calculated from the ”Base” price.

§ 2.5. Fitting with Market Data 30

cross-correlator has a maximum value at a time lag that is non-zero, then there are no choice

of parameters for Gij that can fit the cross-correlator.

The fitting is based on Eqs. (2.17) and (2.22)

GIJ(τ) = DIJ(z(τ)) ; I 6= J.

To leading order we approximate DIJ(t) by the Gaussian approximation D(0)IJ (t) given in

Appendix § 4.11.1 and obtain

GIJ(τ) ' D(0)IJ (z(τ)) = ∆IJ

∫ ∞−∞

dtD(0)I (t)D

(0)J (t− z(τ)) ; I 6= J.

Hence, the cross-correlation coupling ∆IJ is given by

GIJ(0) = ∆IJ

∫ ∞−∞

dtD(0)I (t)D

(0)J (t) ; I 6= J. (2.27)

The empirical cross-correlation of 18 commodities has been studied. Anticipating results

derived later on in the paper, the parameters ∆IJ are given in Figure 2.3 for all the cross-

correlators.

§ 2.5. Fitting with Market Data 31

5

10

15

0

5

10

15

20

−0.04

−0.02

0

0.02

0.04

0.06

0.08

0.1

0.12

Figure 2.3: Matrix of ∆ij for 18 commodities. Note that for all pairs, |∆IJ | < 0.08 but onecase.

The fitting of market correlator to the model is done in the following.

• Simultaneously fit all the auto-correlation functions DII(z(t)) = DI(z(t)) with the G(t),

as in Eq. (2.26), and evaluate the parameters ω, φ, η, λ. The value of η, λ does not enter

into the calibration of the other parameters.

• Using the values of ω, φ, as in Eq. (2.26), and the nonlinear terms given Eq.(2.19),

(2.20), (2.21), we evaluate L, L, γ, α and β.

• Use the parameters L, L, γ, α and β as in Eq. (2.11), (2.12), (2.13), (2.14) and find [a,

b, s, d].

• Evaluate the cross-correlation function DIJ ; I 6= J and determine ∆IJ .

• The correlators are fitted for a maximum time of lag τ = 200 days.

Note the remarkable fact, that ignoring one cross-correlator, the value of all the ∆IJ ’s is

such that |∆IJ | < 0.08. The fact |∆IJ | < 0.08 provides strong evidence of the correctness

§ 2.5. Fitting with Market Data 32

of our approach of considering the multi-commodities model as a perturbation of the single

commodities, which requires |∆IJ | << 1.

Note in extending the statistical model from single to N commodities, N(N − 1)/2 new

parameters ∆IJ are introduced, which in turn are fixed by only a single value of the cross-

correlators GIJ(0), as given in Eq. (2.27).

For our model, the entire dependence of GIJ(τ) for time lag τ > 0 is determined by the

auto-correlation functions D(0)I (z(τ)) and its convolution with itself – as given in Eq. (2.17).

The fact that the model can accurately describe all the auto- and cross-correlators, up to

N = 4 commodities, provides evidence for the correctness of the model. We will discuss

later how the model can be extended to accurately describe a collection of commodities with

arbitrary N .

Calibration for cocoa

1. Use cross-correlation Eq. (2.18) and auto-correlation Eq. (2.16) to fit each data to find ω

φ, λ, and η.

2. Substitute ω, φ, λ, and η into Eq. (2.19), (2.20), (2.21) and (2.15) to get γ, L, L, αI , βI

3. Using the value of all parameters obtained above as in Eq. (2.11), (2.12), (2.13), (2.14),

we can determine the indices [a, b, s, d] [4] of supply and demand function. The result obtained

in Table § 2.6.2 for cocoa from the fitting of the Crude oil, Platinum and Cocoa group is used

§ 2.6. Fits for GII , GIJ 33

below to illustrate the fitting procedure.

ω = 0.1535, φ = 1.2229, λ = 0.700, η = 0.54

⇒ γ = 0.113, L = 203.37, L = −7.35, α = 0.0199, β = 0.0747

⇒∫ ∞

0

dτG(τ) = 4.4413;

∫ ∞0

dτG2(τ) = 6.9973;∫ ∞0

dτG3(τ) = 4.5490;

∫ ∞0

dτG4(τ) = 4.2909

⇒ a = 0.72, b = 0.90, s = 0.094, d = 0.075

§ 2.6 Fits for GII , GIJ

All the fits of the model with data are carried out using the equations for the correlation

functions given in Eqs. (2.16) and (2.18). All auto-correlators are normalized such that

GII(0) = DII(0) = 1. However, for displaying the results clearly, the entire auto-correlator

is rescaled – such that sometimes we scale to GII(0) > 1 or GII(0) < 1 – so that the results

for the different commodities do not overlap and can be viewed clearly. Similarly, the cross-

correlators are also scaled and for four or more commodities are also shifted to avoid an overlap

of the graphs.

§ 2.6.1 Two commodities

Any two commodities, from different types as given in Table 2.1, can be fit to a high degree

of accuracy. The fit is even better if the two commodities belong to the same type. Figure

2.4 shows the fit for Gold and Silver.

§ 2.6. Fits for GII , GIJ 34

0 20 40 60 80 100 120 140 160 180 200−3

−2

−1

0

1

2

3

4

5

R2

11=0.86918

R2

22=0.91679

R2

12=0.84929

η=0.87151

λ=2.0011

Gij(fit)

Gij(data)

Silver

Gold

G(ii)

Gjj

Figure 2.4: Silver and Gold with η = 0.7; λ = 0.1004

The parameters from the auto-correlater are the following

Table 2.2: Gold-Silver. η = 0.7; λ = 0.1004

Two commodities fit R2 γ L L α β

Gold(G11) 0.837 0.136 20.81 -1.52 0.0102 0.257

Silver(G22) 0.863 0.126 37.13 -2.32 -0.0320 0.230

G12 ∆12 = 0.034

The three correlators for gold and silver are fitted well, with R2 given by the following

R2 =

R2G11

R2G12

* R2G22

=

0.837 0.923

* 0.863

§ 2.6. Fits for GII , GIJ 35

§ 2.6.2 Three commodities fit

We study commodities from the same group and from different groups as well.

Three commodities in same group

The figures for three commodities in one group are given below.

Crude oil-Heating oil-Brent oil:

0 20 40 60 80 100 120 140 160 180 200−4

−2

0

2

4

6

8

10

Crudoil(G11)

Heatoil(G22)

Brentoil(G33)

D11

D22

D33

0 20 40 60 80 100 120 140 160 180 200−10

0

10

20

30

40

50

D13(fit)

G13(data)

D23(fit)

G23(data)

D12(fit)

G12(data)

(a) (b)

Figure 2.5: Crude oil-Heating oil-Brent oil (a)Autocorrelation and (b)Crosscorrelation withη = 0.7; λ = 0.775

Table 2.3: Crude oil-Heating oil-Brent oil. η = 0.7; λ =

0.775

Three commodities fit R2 γ L L α β

Crude oil(G11) 0.804 0.0539 171.4 -1.434 0.0613 0.0813

Heating oil(G22) 0.797 0.0537 158.6 -1.182 0.0677 0.0688

§ 2.6. Fits for GII , GIJ 36

Brent oil(G33) 0.798 0.0536 167.4 -1.329 0.0638 0.0738

GIJ ∆12 = 0.032 ∆13 = 0.031 ∆23 = 0.032

R2 =

0.804 0.918 0.921

* 0.797 0.923

* * 0.798

Orange juice-Cattle-Soybean:

0 20 40 60 80 100 120 140 160 180 200−4

−2

0

2

4

6

8

10

Orangejuice(G11)

Cattle(G22)

Soybean(G33)

D11

D22

D33

0 20 40 60 80 100 120 140 160 180 200−30

−20

−10

0

10

20

30

40

D13(fit)

G13(data)

D23(fit)

G23(data)

D12(fit)

G12(data)

(a) (b)

Figure 2.6: Orange juice-Cattle-Soybean (a)Autocorrelation and (b)Crosscorrelation with η =0.7;λ = 1.132

Table 2.4: Orangejuice-Cattle-Soybean. η = 0.7;λ =

1.132

Three commodities fit R2 γ L L α β

§ 2.6. Fits for GII , GIJ 37

Orange juice(G11) 0.609 0.0512 116.06 0.0032 -0.0049 0.0057

Cattle(G22) 0.733 0.0477 236.95 -1.48 0.0290 0.0776

Soybean(G33) 0.685 0.0425 225.14 -0.308 -0.0576 0.0595

GIJ ∆12 = −0.030 ∆13 = 0.021 ∆23 = −0.019

R2 =

0.609 0.875 0.727

* 0.733 0.781

* * 0.685

§ 2.6. Fits for GII , GIJ 38

Gold-Silver-Platinum:

0 20 40 60 80 100 120 140 160 180 200−5

0

5

10

Gold(G11)

Silver(G22)

Plati(G33)

D11

D22

D33

0 20 40 60 80 100 120 140 160 180 200−10

0

10

20

30

40

50

D13(fit)

G13(data)

D23(fit)

G23(data)

D12(fit)

G12(data)

(a) (b)

Figure 2.7: Gold-Silver-Platinum (a)Autocorrelation and (b)Crosscorrelation with η = 0.7;λ = 0.344

Table 2.5: Gold-Silver-Platinum. η = 0.7; λ = 0.344

Three commodities fit R2 γ L L α β

Gold(G11) 0.827 0.0908 58.6 -1.863 0.0071 0.179

Silver(G22) 0.803 0.0752 88.1 -4.17 -0.0217 0.159

Platinum(G33) 0.799 0.0726 112.1 -2.26 -0.0320 0.180

GIJ ∆12 = 0.033 ∆13 = 0.031 ∆23 = 0.025

§ 2.6. Fits for GII , GIJ 39

R2 =

0.827 0.931 0.910

* 0.803 0.895

* * 0.799

Three commodities from different groups

Crude oil-Platinum-Cocoa:

0 20 40 60 80 100 120 140 160 180 200−4

−2

0

2

4

6

8

10

Crudoil(G11)

Plati(G22)

Cocoa(G33)

D11

D22

D33

0 20 40 60 80 100 120 140 160 180 200−15

−10

−5

0

5

10

15

20

25

30

35

G13(fit)

G13(data)

G23(fit)

G23(data)

G12(fit)

G12(data)

(a) (b)

Figure 2.8: Crude oil-Platinum-Cocoa (a)Autocorrelation and (b)Crosscorrelation with η =0.70; λ = 0.54.

Table 2.6: Crude oil-Platinum-Cocoa. η = 0.70; λ = 0.54

Three commodities fit R2 γ L L α β

Crude oil(G11) 0.871 0.0560 286.3 -3.54 0.0566 0.0742

Platinum(G22) 0.835 0.0585 305.2 -4.17 -0.0241 0.1346

§ 2.6. Fits for GII , GIJ 40

Cocoa(G33) 0.920 0.113 203.4 -7.35 0.0199 0.0747

GIJ ∆12 = 0.021 ∆13 = 0.045 ∆23 = 0.023

R2 =

0.871 0.612 0.920

* 0.835 0.943

* * 0.920

The R2 of three commodities fit are normally between 0.8-1. Although they are not quite

high, the values are high enough to be convincing.

§ 2.6.3 Four commodities

When we consider taking more commodities into the fit, such as 4 and 6 commodities, the fit

is not so good.

§ 2.6. Fits for GII , GIJ 41

0 20 40 60 80 100 120 140 160 180 200−30

−25

−20

−15

−10

−5

0

Silver(G11)

Gold(G22)

Crudeoil(G33)

Gas(G44)

D11

D22

D(33)

D(44)

0 20 40 60 80 100 120 140 160 180 200−20

0

20

40

60

80

100

D14(fit)

G14(data)

D24(fit)

G24(data)

D34(fit)

G34(data)

D13(fit)

G13(data)

D23(fit)

G23(data)

D12(fit)

G12(data)

(a) (b)

Figure 2.9: Gold-Silver-Crude oil-Natural gas (a)Autocorrelation and (b)Crosscorrelation withη = 0.70; λ = 0.260.

Four commodities fit R2 γ L L α β

Gold(G11) 0.834 0.0973 54.9 -2.051 0.0074 0.186

Silver(G22) 0.827 0.0835 105.2 -2.940 -0.0220 0.159

Crude oil(G33) 0.749 0.0769 35.3 -0.041 0.0962 0.128

Natural gas(G44) 0.377 0.0667 81.8 -0.921 0.0850 0.015

Table 2.7: Gold-Silver-Crude oil-Natural gas. η = 0.70;

λ = 0.260.

§ 2.6. Fits for GII , GIJ 42

R2 =

0.834 0.885 0.507 0.074

* 0.827 0.725 0.435

* * 0.749 0.809

* * * 0.377