Freescale Strategy - library.corporate-ir.netand Seamless Mob ility Bil $ 0.1 1 10 100 1000 ... •...

37

Sumit Sadana Senior Vice President, Strategy, Business Development and Acting CTO Freescale Strategy 25 July 2006

Transcript of Freescale Strategy - library.corporate-ir.netand Seamless Mob ility Bil $ 0.1 1 10 100 1000 ... •...

Sumit SadanaSenior Vice President, Strategy, Business Development and Acting CTO

Freescale Strategy25 July 2006

The forward-looking statements in this presentation include statements regarding market growth and our potential capacity, financial position, expanded addressable market, business strategy and other plans and objectives for future operations, as well as any other statements which are not historical facts.

Although we believe that these statements are based on reasonable assumptions, they are subject to numerous factors, risks and uncertainties that could cause actual outcomes and results to be materially different from those projected. These factors, risks and uncertainties are listed in our Form 10K for the year ended December 31, 2005 and other SEC filings.

Agenda

• Industry Overview

• Freescale Strategy

• Growth Initiatives

• Technology and Innovation

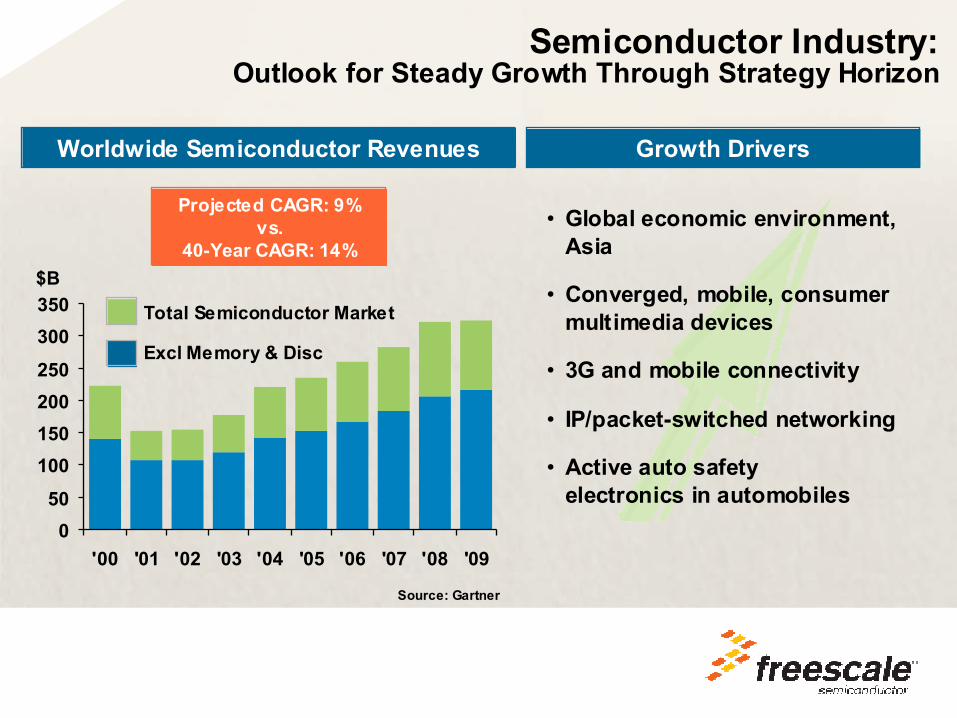

Source: Gartner

Worldwide Semiconductor Revenues

050

100150200250

300350

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09

Total Semiconductor Market

Excl Memory & Disc

Projected CAGR: 9%vs.

40-Year CAGR: 14%$B

Semiconductor Industry:Outlook for Steady Growth Through Strategy Horizon

Growth Drivers

• Global economic environment, Asia

• Converged, mobile, consumer multimedia devices

• 3G and mobile connectivity

• IP/packet-switched networking

• Active auto safety electronics in automobiles

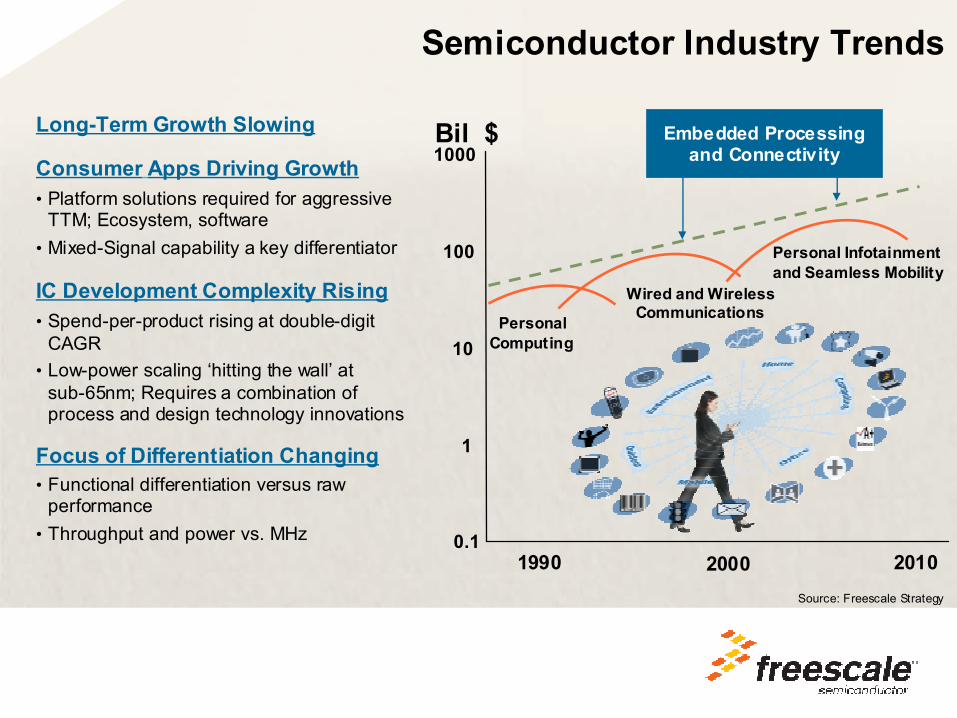

Semiconductor Industry Trends

Long-Term Growth Slowing

Consumer Apps Driving Growth• Platform solutions required for aggressive

TTM; Ecosystem, software• Mixed-Signal capability a key differentiator

IC Development Complexity Rising• Spend-per-product rising at double-digit

CAGR• Low-power scaling ‘hitting the wall’ at

sub-65nm; Requires a combination of process and design technology innovations

Focus of Differentiation Changing• Functional differentiation versus raw

performance• Throughput and power vs. MHz

Source: Freescale Strategy

PersonalComputing

Wired and WirelessCommunications

Personal Infotainment and Seamless Mobility

Bil $

0.1

1

10

100

1000

1990 2000 2010

Embedded Processing and Connectivity

Agenda

• Industry Overview

• Freescale Strategy

• Growth Initiatives

• Technology and Innovation

Initiatives underwayto drive

benchmark performance

Financial Performance

12%

25%29%

37%42%

2001 2002 2003 2004 2005 2Q 2006

46.0%

-20%

-7%-5%

7%11%

2001 2002 2003 2004 2005

15.7%

2Q 2006

Gross Margin %*

Operating Earnings %*

$5.1 $5.0 $4.9$5.7 $5.8

2001 2002 2003 2004 2005

Sales $B

1H’06 revenue up 7.2% over year ago

* OE and GM excludes unusuals

Freescale Business Groups

Wireless & Mobile Systems Group

Networking & Computing Systems Group

Transportation & Standard Products GroupW

MSG

NC

SG

TSPG

# 1 in Comms Processors

# 1 in RF for Wireless Inf.

# 2 in DSP

# 1 in Total Auto ICs

# 2 in Microcontrollers

# 3 in Sensors

# 2 in DSP

# 2 in GSM/GPRS Cellular Handset Baseband

# 3 in Wireless Handset RF

9%$27B

CAGR (’05-’08)SAM (’08)

14%$28B

CAGR (’05-’08)SAM (’08)

12%$18B

CAGR (’05-’08)SAM (’08)

Revenue: $1.4B (LTM) Revenue: $2.0B (LTM) Revenue: $2.6B (LTM)

Source: Gartner, iSuppli, F orward Concepts, Strategy Analytics

Freescale Strategy

Drive benchmark operational performance:• Continued focus on margin expansion• Asset-lite model; Manufacturing, supply chain excellence

Vision: Global leadership in embedded processing and connectivity solutions

Accelerate revenue growth:• Shift investment to high-priority growth initiatives: Consumer,

Merchant Wireless, Analog Power Management• Reinvigorate technology / innovation focus; NPI excellence

People focus:• Strengthen leadership and management talent• Increase investment in system / software expertise• Winning culture

2003 2004 2005 Q1'06

Waf

er V

olum

es

Manufacturing Strategy

• Asset-lite modelCapex ~10% of revenue

• Flexible manufacturing strategy Maximize internal capacity utilization, ROICAssurance of supply

• Crolles Full Build-out: 2006-7 Capex

• 2005-2007: C90 qualified in 4 fabs, 65nm in 3 fabs

2003 2004 2005 2006 2007 2008

# of

Qua

lifie

d Te

chno

logy

Sou

rces

Advanced Technologies(<=130nm)

InternalExternal

Faster Learning Rates

Manufacturing Excellence

Innovative methods; Holistic approach

Zero Defect Culture

+Time

Def

/cm

2

180nm130nm90nm

Crolles2 Alliance:Partnering on Advanced Manufacturing

• 130nm production 2003• 90nm production 2005• 65nm qual/ramp 2006/7• 45nm qual/ramp 2008

• Freescale, STMicroelectronics and Philips

• TSMC alignment for security of supply

• Shared 300mm capacity• Alliance Technologies

• CMOS: 90nm to 32nm• SOI• Analog• RF• Embedded memories

Alliance Facts

Status

Manufacturing Capital Programs• 90nm Capacity

300mm CMOS, RF200mm SOI, NVM

• Power Management SMARTMOS7, 8, 10 – 200mm

• 65nm Ramp• 45nm Capability/Sampling• Assembly and test capacity• Yield enhancement• Lead-free initiative

• Manufacturing Methods

Freescale’s 2006 Capital Priorities

Manufacturing• Capacity Increase• Mix Renewal• Yield Enhancement &

Automation

Innovation• Process• Design

Infrastructure• IT• India

Freescale Evolution

2006 Focus

• Growth Initiatives

• Margin Improvement

• Revitalize NPI

• Marketing / Sales: Solutions, Portfolio Focus

• Winning CultureRESTRUCTURE

STRENGTHEN

ACCELERATE

GROWTH

Gain share, g

row OE

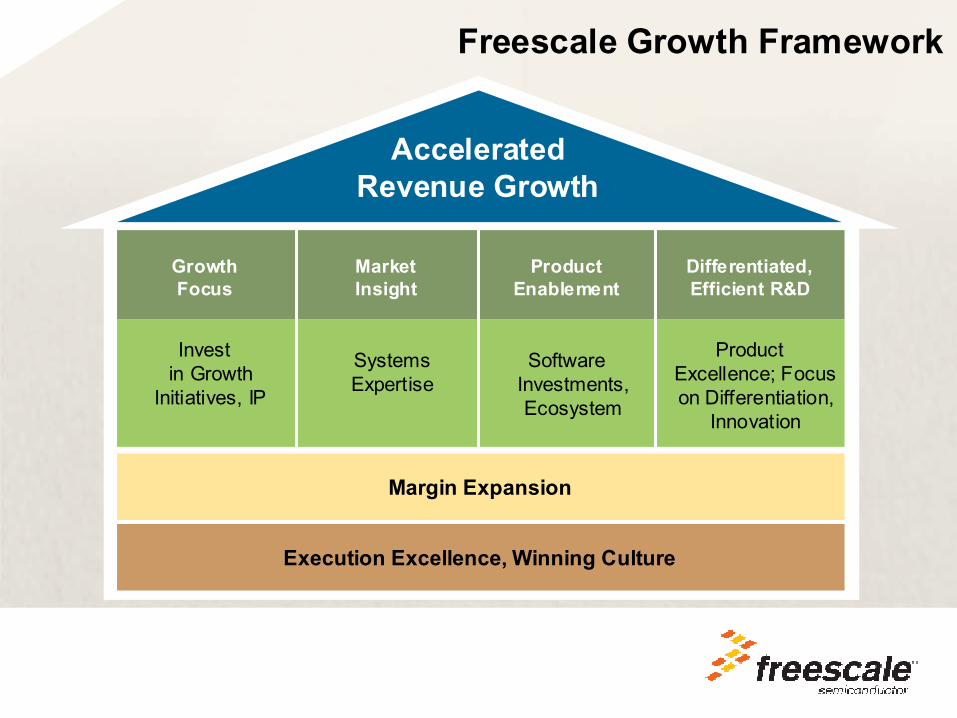

Freescale Growth Framework

Growth Focus

Investin Growth

Initiatives, IP

Market Insight

Systems Expertise

ProductEnablement

Software Investments, Ecosystem

Differentiated, Efficient R&D

Product Excellence; Focus on Differentiation,

Innovation

AcceleratedRevenue Growth

Execution Excellence, Winning Culture

Margin Expansion

Key Growth Initiatives

Strengthen Base

• Wireless Merchant Market

• Revitalize Distribution

• A-P, Japan Growth

GROWTH STRATEGY

Expand AddressableMarket

• Analog

• Mass Market / ConsumerFixed Consumer

Mobile Consumer

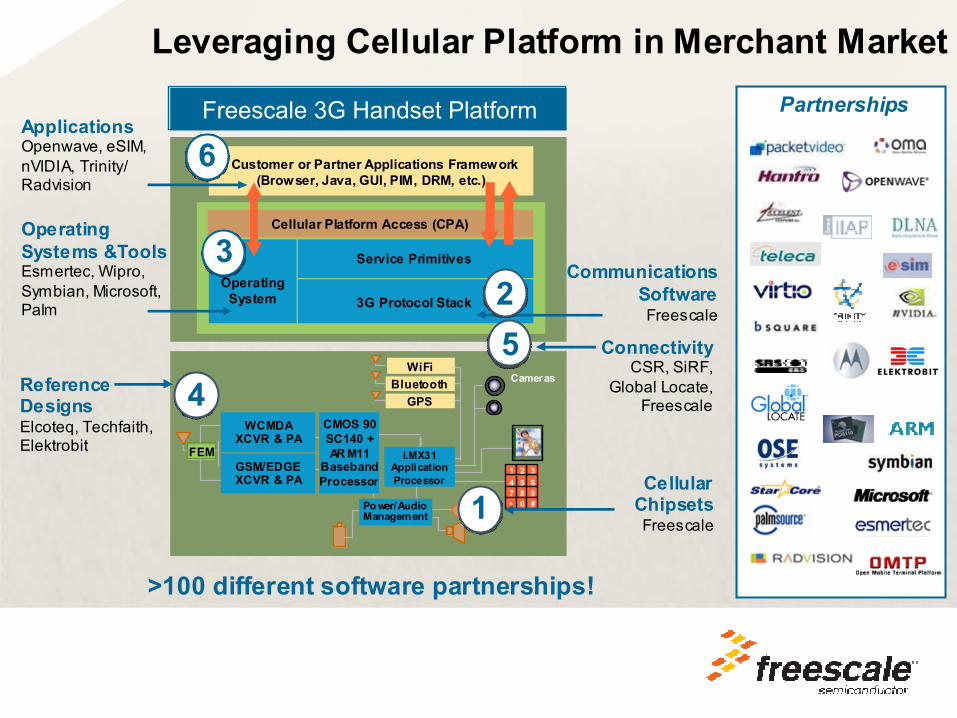

Customer or Partner Applications Framework(Browser, Java, GUI, PIM, DRM, etc.)

Cellular Platform Access (CPA)

OperatingSystem 3G Protocol Stack

FEM

Cameras

CMOS 90 SC140 + AR M11

BasebandProcessor

Po wer/AudioManagement

WiFiBluetooth

GPS

i.MX31ApplicationProcessor

GSM/EDGEXCVR & PA

WCMDAXCVR & PA

Leveraging Cellular Platform in Merchant Market

Freescale 3G Handset Platform

>100 different software partnerships!

Operating Systems &ToolsEsmertec, Wipro, Symbian, Microsoft, Palm

3

Reference DesignsElcoteq, Techfaith, Elektrobit

4Connectivity

CSR, SiRF, Global Locate,

Freescale

5

PartnershipsApplicationsOpenwave, eSIM, nVIDIA, Trinity/ Radvision

6

Service PrimitivesCommunications

SoftwareFreescale

2

35

147 8

26

*9

0 #

CellularChipsetsFreescale

1

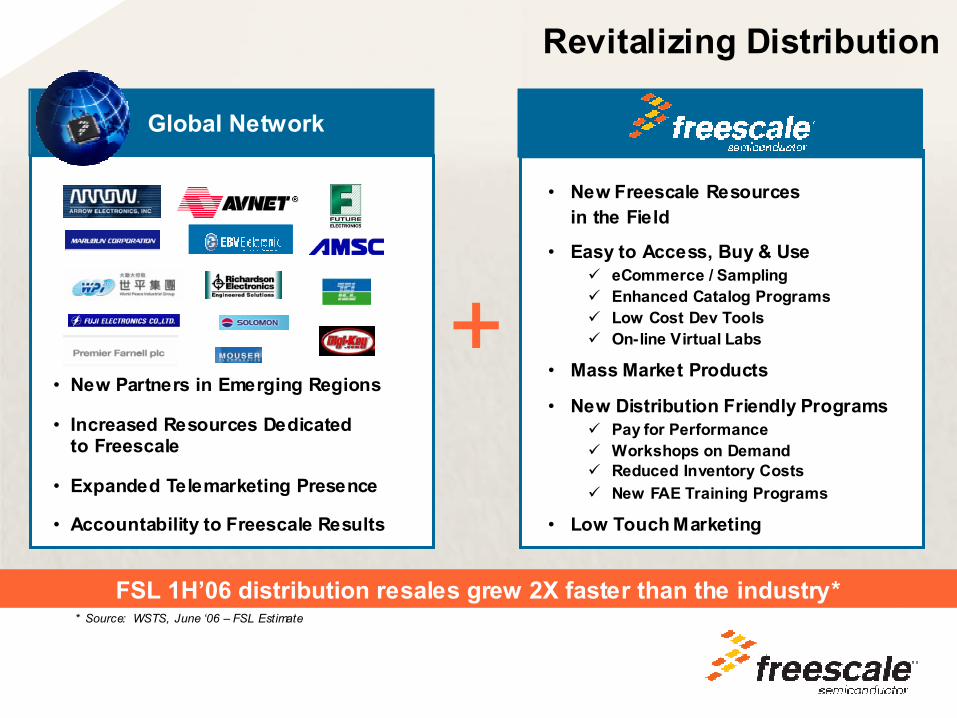

Revitalizing Distribution

+

• New Freescale Resources in the Field

• Easy to Access, Buy & UseeCommerce / SamplingEnhanced Catalog ProgramsLow Cost Dev ToolsOn-line Virtual Labs

• Mass Market Products

• New Distribution Friendly ProgramsPay for Performance Workshops on DemandReduced Inventory CostsNew FAE Training Programs

• Low Touch Marketing

• New Partners in Emerging Regions

• Increased Resources Dedicated to Freescale

• Expanded Telemarketing Presence

• Accountability to Freescale Results

Global Network

FSL 1H’06 distribution resales grew 2X faster than the industry* * Source: WSTS, June ‘06 – FSL Estimate

Asia-Pacific & Japan Thrust

► Total employees: ~9,600► Sales offices: 13► Design centers: 9► Manufacturing centers: 3

Freescale in Asia Pacific/Japan

Focused activity in region• Tier1 automotive & networking

customers

• Leverage 3G Platform at Tier1 cellular customers

• Expand direct / distribution sales presence in region

• Develop ecosystem, regional partnerships & alliances

• Ramping design capability in India & China

* Source: WSTS AP & Japan Region (Excludes Memory and Discretes), June ’06 – FSL Estmate

• ‘09 Goal: 2X ‘06 revenue • 1H’05 - 1H’06 revenue growth faster than industry*

Analog / Mixed-Signal Focus

Leveraging Strengths

Investing for the Future

•*Source: iSuppli May 2006•**Awarded January 2006

EDGE Radio Subsystem, shipping with five different industry standard basebands

Portable Design’s Editor’s Choice Award** for Power Management ICs won with SMARTMOS technology

Over $1B in revenue; Fastest ASSP growth among top 10*

• Broad IP Portfolio• SMARTMOS™ / LDMOS• Large Customer Base• Integration Expertise

• Power Management• Motor Control• RF Power Transistors• RF Cellular

• New Management in Place• SMARTMOS10W, 10T• High Performance Focus

• 2X Cellular/Portable PM

• Talent• Technology • Portfolio Expansion

MPC18730

i.MX Processors, Sensors,Power Management

Freescale Consumer Focus Home Appliances

Home Networking & Peripherals Mobile Consumer Electronics

PowerQUICC Processors, MCU,DSPs, Power Management

MCUs, Sensors,Power Management

2009 Goal: >20% of Freescale revenue from consumer segments*

FreescaleConsumer

Focus

MCUs, Audio DSPs,Class D Amps, i.MX Processors,

Power Management

Home Consumer Electronics

* Does not include cellular handsets

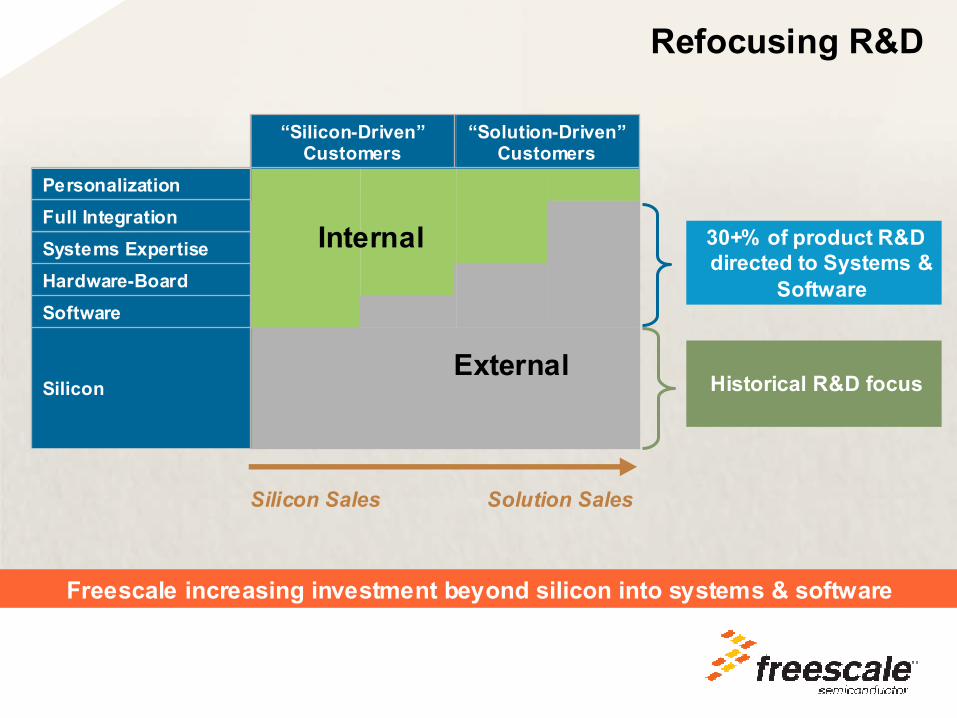

Refocusing R&D

Silicon Sales Solution Sales

“Solution-Driven”Customers

“Silicon-Driven”Customers

Silicon

SoftwareHardware-BoardSystems ExpertiseFull IntegrationPersonalization

Freescale increasing investment beyond silicon into systems & software

Historical R&D focus

30+% of product R&D directed to Systems &

Software

Internal

External

Freescale ZigBee™ PlatformComplete IEEE 802.15.4 & ZigBee™

HW & SW Development System

Strong Development Partners Network

Over 700 design wins to date!

Industrial

Medical

Communication Gateways

Consumer,Cellular

Automotive

Appliances

Freescale Symphony SolutionHigh-quality Comprehensive Audio Solutions

for Consumer and Automotive Markets and Customers

Hardware Software System

Aggressive Roadmap• 24-bit DSPs for digital

audio and radio

• Leading-edge technology for Class D Digital Amplification with advanced feedback

Reference Designs

• Symphony™ Surround Module

• DH1 (Dolby Headphone)

• DVS (Dolby Virtual Speaker)

• Symphony™ Class D Amplifier

Extensive S/W Library• Vast multi-channel decoder

libraries embedded on chip

• Plug ‘n Play software architecture for post-processing support

• Strong 3rd party algorithm developer network

The Controller ContinuumFreescale Controller Continuum Industry’s First 8/32-bit Compatible Architectures

Wide range of performance and peripherals – from low (S08) to high (68K/ColdFire)

Seamless transition between performance ranges, independent of bit-width

Automatic code generation with CodeWarriorTM development tool ensures compatibility across continuum

7000+ evaluation boards shipped within two months of 8-bit KA2 launch

Consistent user experience around a range of performance

Video 3D Graphics Security Audio Connectivity Low Power

Enterprise

i.MX Application Processors

Addressing multimedia-intensive applications with industry-leading low power solutions

Performance*• 35-61% better performance per MHz

• 2x faster MPEG4 Decode

Power*• 50% lower power consumption

Size*• High level of integration: 45% smaller die

Cellular

Entertainment

* Benchmarked to leading competition by independent 3rd party - Synchromesh

Agenda

• Industry Overview

• Freescale Strategy

• Growth Initiatives

• Technology and Innovation

Building on a 50+ Year Heritage of Innovation

(1) The “PowerP C” name is a tradem ark of IBM Corp. and is used under license.

19523 Amp power Transistor

197916-Bit Processor MC68000

198432-Bit Processor MC68020

1989MC68302 Communications Processor

1991PowerPC® (1) Alliance

1994First PowerPC®(1) MPC601

1995MPC860 PowerQUICC™

2001MPC7455 SOI Volume Production

2003Low-K Volume Produ ction

2003First single core modem: MXC. “Smartphone-on –a-postag e stamp”

2005First PowerQUICC communications processor with QUICC Engine (MPC8360E)

2003Tire pressure monitor sen sorwith cap acitive technology Introduced

Late 1980sDevelopment of the first surface micromachined inertial sensors for the automotive airbag

1975MC6800 is first microprocessor used in automotive application

2005i.MX31 processor for mobile multimedia entertainment

1998First PowerQUICC II communications processor (MPC8260)

2006MC9RS08KA2Ultra-low end MCUwith RS08 core

2006MSC8144 multicore DSP targeting wireless and wirelin e infrastructure

2006Industry’s First Commercial MRAMProduct

1996500-700Mhz 65W RF Plastic Package

2004First 130 nm MCU with 2MB eNVM

1993First RF-LDMOS device for1GHz Cellular handset and infrastru cture markets

1960Si-Base Tran sistor

Technology

Production Today Sampling Development

• Competitive process technology nodes • 65nm products sampled Q1’06• 45nm samples in Q4’07

Auto

Wire

less

Netw

orki

ng

Business DriversC

onsu

mer

n/a 0.13um 90nm 65nmSMARTMOS >0.18um

0.18um n/a 90nm 65nm 45nmRF/SiGe >0.18um

0.18um 0.13um 90nm 65nm 45nm 32nmCMOS/SOI/LP >0.18um

LDMOS/III-V

0.18umSGF 0.13umNVM 65nm>0.18um 90nm

Sensors

HV 7LDMOS GaNHV 8

LDMOSInGaPHBT

12V PHEMT

LinearHFET

26V PHEMT

Pressure; Safety/Alarm ICs; Capacitive; X,Y,Z axis accelerometers

Freescale Wafer Technology Development

~ 40% Size reduction in analog and power blocks vs. competitive processes

SMARTMOS TechnologyEnables Industry Leading Power System Integration

TM

Power + Analog + Digital + MemoryPower + Analog + Digital + Memory

High Precision Matching, Low noise,

High Power Efficiency

High Precision Matching, Low noise,

High Power Efficiency

Industry Leading Digital Capability(Completely modular NVM)

Industry Leading Digital Capability(Completely modular NVM)

Low Power,Cell Phone Power Management

ABS/ESP

Automotive

Consumer

NetworkingPower over Ethernet

Leveraged Across the Spectrum

SMARTMOS10

100V, precision converters, 0.13um logic, andNVM memory with automotive level reliability

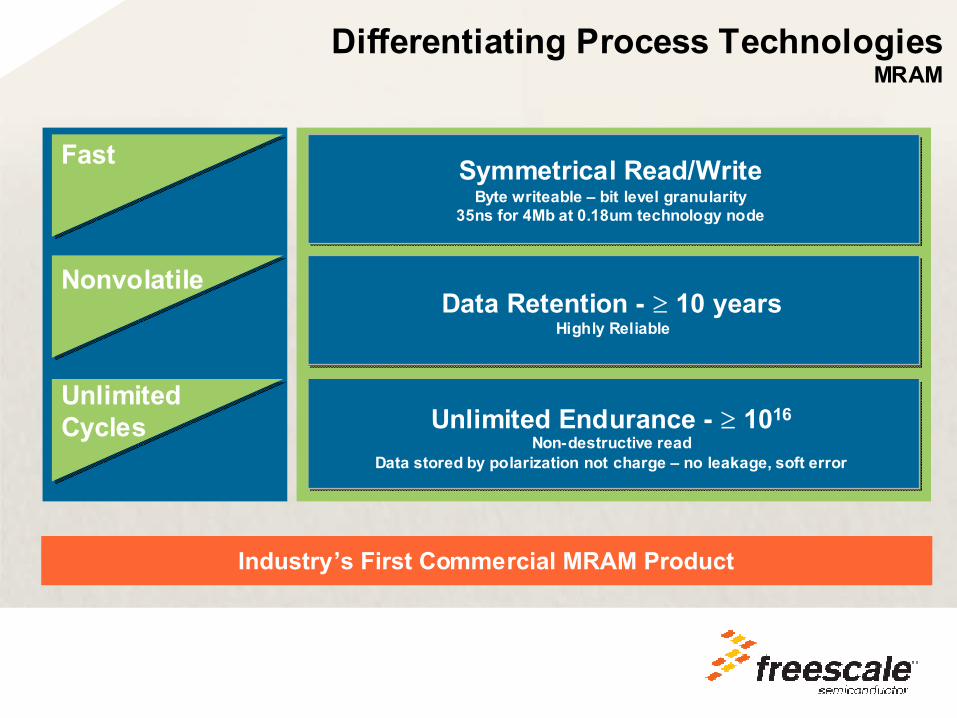

Data Retention - ≥ 10 yearsHighly Reliable

Symmetrical Read/WriteByte writeable – bit level granularity

35ns for 4Mb at 0.18um technology node

Unlimited Endurance - ≥ 1016Non-destructive read

Data stored by polarization not charge – no leakage, soft error

Nonvolatile

Fast

Unlimited Cycles

Differentiating Process TechnologiesMRAM

Industry’s First Commercial MRAM Product

Leadership & Innovation in PackagingRedistributed Chip Packaging

LTE2 MAPBGA13mm x 13mm x 1mm

LTE2 RCP9mm x 9mm x 0.7mm

Benefits• 30% reduction in size and thickness• Eliminates package substrate,

wirebond / flip chip bumps

• Flexible, Ultra Low-K compatible technology

• Single, Multi Chip, SiP, PoP• Good thermal management

• Green (Halogen and Pb free)

GSM EDGE i.275Radio in Package

Thickness

Footprint

1.4mm

RCP

FoldedPkg.

StackPkg.

PCBEmbed.

Die

POP

DieStack

Cost

MPC8641D

Industry’s highest performance programmable DSP: 4 x 1GHz performance!

MSC8144

Dual PowerPC™ cores >1.5GHz

• Multi-core embedded processor roadmap – Leveraging:

• PowerPC™

• StarCore™ DSP

• QUICC™ Engine

• Extreme Integration – MPC8641D• 225 million transistors

• High Performance SOI Technology

• 9 Levels Copper / Low-K interconnect

Leadership Technology - NCSG

MPC55xx family32bit PowerPC™ MCUUp to 4MB eNVM w/ ECC

Con

sum

er

I

ndus

tria

l

A

utom

otiv

e

S12X family0.25 0.18um SGF16bit MCU

• Leading technology platforms and architectures

• PowerPC, S12X, 68K/ColdFire, HCS08 cores

• 0.25u, 130nm eNVM CMOS process • SMARTMOS mixed-signal integration

platform• MEMS (bulk and surface), with

SMARTMOS, MCU, RF integration

• Product leadership – MPC 55xx family• 34M transistors, 130nm eNVM CMOS• 2–4MB embedded flash (highest in industry)• eTPU – independent, programmable Time

Processor unit

Leadership Technology - TSPG

Leadership Technology - WMSG

i.MX31

MXC91321

• Leadership Technology• Innovative single core modem architecture - MXC • Power / Performance optimized Applications Processors • RFCMOS and SMARTMOS process technology - highly

optimized RF subsystem and Power Management• Platform Solution - Stack, Codecs, Tools, Multi-OS

support, Reference Designs

• Integration & Low Power: MXC91321• ARM1136 (532MHz), StarCore DSP • 101 Million Transistors• Dynamic Voltage and Frequency Switching, Well-Bias

techniques for low power• Low power CMOS process

SVP

• 10 Director level hires are building a bench of next generation leaders• Targeted technical hiring across the enterprise • Talent Pipeline Management

Director and Technical

• Analog - Arman Naghavi• Design Technology - Chekib Akrout• High-Performance Processor Designs - Rick Morris• Back-end Manufacturing - Gulzar Ali• Chief Procurement Officer - Tom Linton• Chief Information Officer - Sam Coursen

SalesBill Bradford

VP• Global Distribution - Rick Bosshardt• Business Operations - Fred Glasgow• Talent - Drew Morton• Corporate Communications - Tim Doke• Treasurer - Greg Heinlein• Tax - David McDonald

WirelessSandeep Chennakeshu

Biz OperationsJan Monney

ManufacturingAlex Pepe

Strategy and Biz DevSumit Sadana

Human ResourcesKurt Twining

Redefining Freescale: New Leadership