Foreword - Hypo Vorarlberg · Claudio Zanini, HPB Bludenz Branch Office Christian Vonach, BOH...

69

Passionate. Sound. Advice.

-

Upload

hoangnguyet -

Category

Documents

-

view

215 -

download

0

Transcript of Foreword - Hypo Vorarlberg · Claudio Zanini, HPB Bludenz Branch Office Christian Vonach, BOH...

Foreword

Passionate. Sound. Advice.

ViennaWels

GrazBolzano

St. Gallen

Vaduz

Bregenz

Como

Bergamo

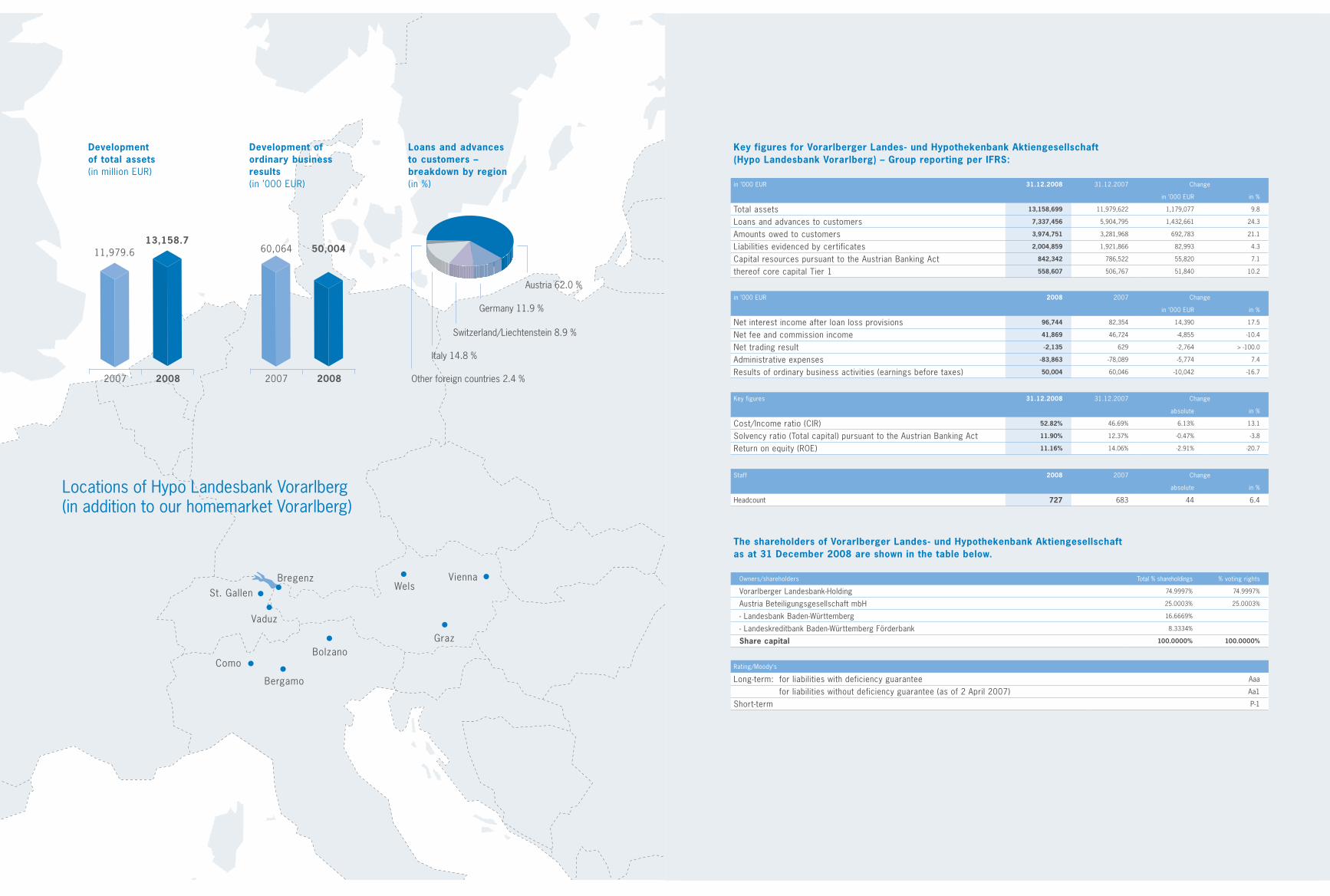

Locations of Hypo Landesbank Vorarlberg(in addition to our homemarket Vorarlberg)

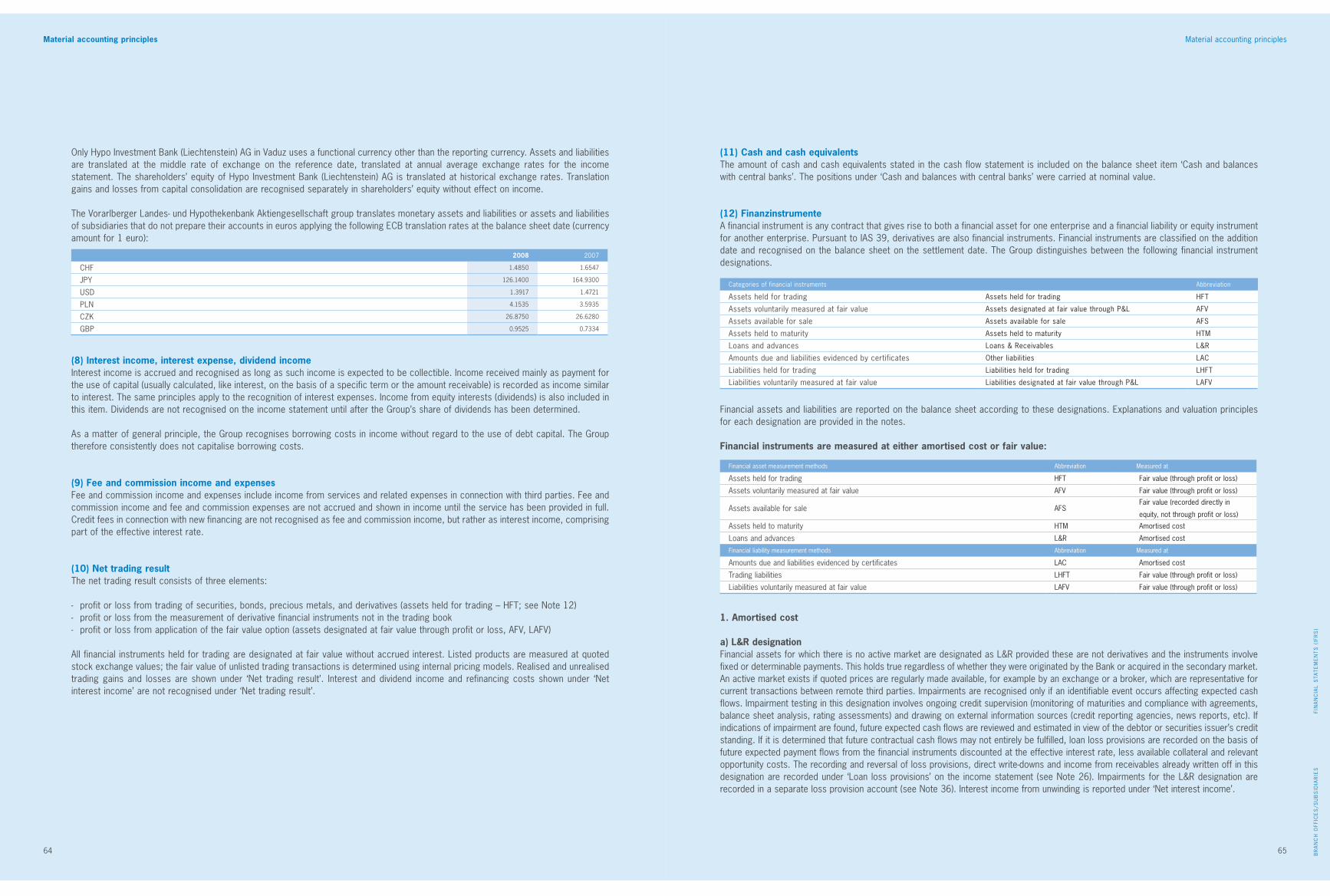

Key figures for Vorarlberger Landes- und Hypothekenbank Aktiengesellschaft (Hypo Landesbank Vorarlberg) – Group reporting per IFRS:

in ’000 EUR 31.12.2008 31.12.2007 Change

in ’000 EUR in %

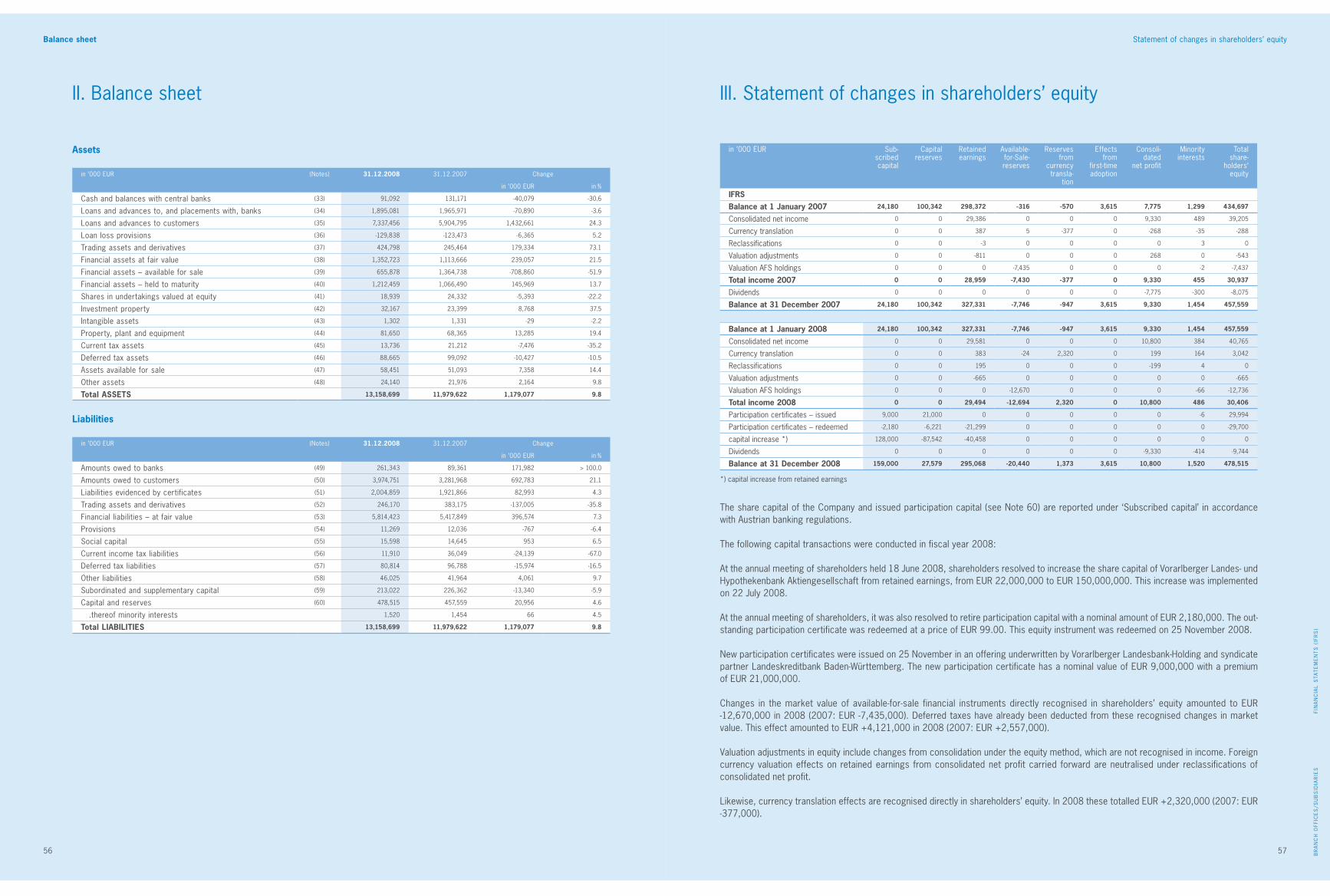

Total assets 13,158,699 11,979,622 1,179,077 9.8

Loans and advances to customers 7,337,456 5,904,795 1,432,661 24.3

Amounts owed to customers 3,974,751 3,281,968 692,783 21.1

Liabilities evidenced by certificates 2,004,859 1,921,866 82,993 4.3

Capital resources pursuant to the Austrian Banking Act 842,342 786,522 55,820 7.1

thereof core capital Tier 1 558,607 506,767 51,840 10.2

in ’000 EUR 2008 2007 Change

in ’000 EUR in %

Net interest income after loan loss provisions 96,744 82,354 14,390 17.5

Net fee and commission income 41,869 46,724 -4,855 -10.4

Net trading result -2,135 629 -2,764 > -100.0

Administrative expenses -83,863 -78,089 -5,774 7.4

Results of ordinary business activities (earnings before taxes) 50,004 60,046 -10,042 -16.7

Key figures 31.12.2008 31.12.2007 Change

absolute in %

Cost/Income ratio (CIR) 52.82% 46.69% 6.13% 13.1

Solvency ratio (Total capital) pursuant to the Austrian Banking Act 11.90% 12.37% -0.47% -3.8

Return on equity (ROE) 11.16% 14.06% -2.91% -20.7

Staff 2008 2007 Change

absolute in %

Headcount 727 683 44 6.4

The shareholders of Vorarlberger Landes- und Hypothekenbank Aktiengesellschaft as at 31 December 2008 are shown in the table below.

Owners/shareholders Total % shareholdings % voting rights

Vorarlberger Landesbank-Holding 74.9997% 74.9997%

Austria Beteiligungsgesellschaft mbH 25.0003% 25.0003%

- Landesbank Baden-Württemberg 16.6669%

- Landeskreditbank Baden-Württemberg Förderbank 8.3334%

Share capital 100.0000% 100.0000%

Rating/Moody‘s

Long-term: for liabilities with deficiency guarantee Aaa

for liabilities without deficiency guarantee (as of 2 April 2007) Aa1

Short-term P-1

2007 2008

11,979.613,158.7

Development of total assets(in million EUR)

2007 2008

60,064 50,004

Development of ordinary business results(in ’000 EUR)

Austria 62.0 %

Switzerland/Liechtenstein 8.9 %

Germany 11.9 %

Italy 14.8 %

Other foreign countries 2.4 %

Loans and advances to customers – breakdown by region(in %)

Passionate. Sound. Advice.

Foreword

Managing Board/Supervisory Board

Economic environment

Management report

Financial Statements (IFRS)

Branch offices/Subsidiaries

Foreword by the Managing Board

Organisational chart

Managing Board/Supervisory BoardManaging BoardAdvisory Board

Economic environment

Questions to Jodok Simma, CEO and Chairman Managing Board

Questions to Johannes Hefel, Managing Board Private Customer, Private Banking, Portfolio and Asset Management

Questions to Michael Grahammer, Managing Board Risk Management, Leasing and Real Estate

Management reportDevelopment by segmentMajor subsidiariesOutlook

Business policyHuman resourcesMarketing and Advertising

Consolidated Financial Statements in accordance with International Financial Reporting Standards (IFRS)I. Income statementII. Balance sheetIII. Statement of changes in shareholder’s equityIV. Cash flow statementV. NotesVI. Supervisory BoardVII. Subsidiaries/Holdings

Managing Board declaration

Report of the Supervisory Board

Audit opinion

Branch offices/Subsidiaries

This translation of the original German version of the annualreport has been prepared for the convenience of English-speakingreaders. The German version is authoritative.

Table of Contents

4

6

101012

16

20

22

23

26303639

424244

48

5052535455

126127

128

128

129

130

7

FOR

EW

OR

DM

AN

AG

ING

BO

AR

D/S

UP

ER

VIS

OR

y B

OA

RD

EC

ON

OM

IC E

NV

IRO

NM

EN

TM

AN

AG

EM

EN

T R

EP

OR

TFI

NA

NC

IAL

STA

TE

ME

NT

S (

IFR

S)

BR

AN

CH

OFF

ICE

S/S

UB

SID

IAR

IES

6

Strong roots create a feeling of safety. For 111 years we have remained true to our busi-

ness model. We feel connected to Austria and to our Vorarlberg roots. This consistency

has led to successful development. The stable ownership structure in a globally shifting

market makes us a favorite partner for Vorarlberg businesses as well as a financial anchor

for the populace. Security has never been so modern.

8 9

FOR

EW

OR

DM

AN

AG

ING

BO

AR

D/S

UP

ER

VIS

OR

y B

OA

RD

EC

ON

OM

IC E

NV

IRO

NM

EN

TM

AN

AG

EM

EN

T R

EP

OR

TFI

NA

NC

IAL

STA

TE

ME

NT

S (

IFR

S)

BR

AN

CH

OFF

ICE

S/S

UB

SID

IAR

IES

ForewordForeword

Dear customers, business partners, shareholder representatives and employees,

Behind us lies an exceptional business year, in every respect. We have all witnessed developments that were previously unimaginable in their magnitude and pace. The end of the crisis is not in sight. The following lessons for companies, and this includes banks, are pivotal:

There is no substitute for healthy common senseComputer models with multiple decimal places, based on unsure or past assumptions, create make-believe security. Even supposedly ingenious methods and instruments can fail, even skew the entire system. Technocratic thinking and feasibility studies are no substitute for a professional sense of proportion and common sense. It is also important to keep a cool head, keep an eye on overall interests and not to succumb to impulsive action.

Trees do not grow right up to the skyBusinesses and investors were reminded of this truth again in 2008 in harsh fashion. No economic expansion lasts forever, nor do financial markets always go up. High returns involve high risks. The question of security must always be a theme with monetary investments.

Hypo Landesbank Vorarlberg’s down to earth business model has proven its worth for 111 yearsWe are pleased to present the positive results of Hypo Landesbank Vorarlberg with this annual report. Our figures and our more than 111 year business history confirm that our measured, risk-aware, organic business strategy is the right course, and is why we have grown to be Vorarlberg’s largest bank.

We reached our planned goal of 50 million euros annual profit in spite of the very difficult conditions. Our business model is solid and has proven itself again in turbulent times. Hypo Landesbank Vorarlberg is a safe haven in the banking sector. This is shown by the sharp increase in customer deposits. Our liquidity and equity capital is sufficient and provides us additional security. The trust of our customers – the number one commodity a bank can have – is intact.

We remain consistent with our proven, long-term corporate and investment policies.

Credit volume increased 24.3%The reasons for the above-average growth were the stable economy in the first half of 2008 and, at the same time, the sharp decrease in loan loss provisions. From a total loan volume of over 7.3 billion euros, 70% went to corporate customers. These figures show two things. One, that Hypo Landesbank Vorarlberg is the absolute leading corporate bank in Vorarlberg; three-fourths of the top 100 companies in Vorarlberg have a business relationship with Hypo Landesbank Vorarlberg. And two, these figures show clearly that Hypo Landesbank Vorarlberg is not experiencing the oft-mentioned credit crunch.

Passionate. Sound. Advice.The stable and enduring success of Hypo Landesbank Vorarlberg certainly has to do with our basic principles – to always be committed to our customers and to long-term success. The new focus of our marketing with the slogan “Passionate. Sound. Advice.” brings us closer to our customers and underlines – with heart and head – our commitment to them.

We are giving the highest priority to granting the requests of our customers, even during the financial crisis. In the past year we gained many new customers for the bank. We want to prove, through quality advisory and support services, that they have chosen the right bank. It is essential to continually change the defined standards of customer service so that customers, like banks, ask critical questions concerning which product is right for which customer, and which risk (including emotional risk) a customer is prepared to take on.

Our heartfelt thanks2008 showed us all that trust is the most important commodity a bank can have. We thank our customers, shareholders and business partners for the loyalty that we could count on during these difficult market conditions. Above all we thank our employees for their great dedication and for the excellent results.

The Members of the Managing BoardJodok SimmaJohannes HefelMichael Grahammer

Foreword – Managing Board

Johannes HefelMember Managing Board

Jodok SimmaCEO, Chairman Managing Board

Michael GrahammerMember Managing Board

Foreword

10 11

Foreword

11

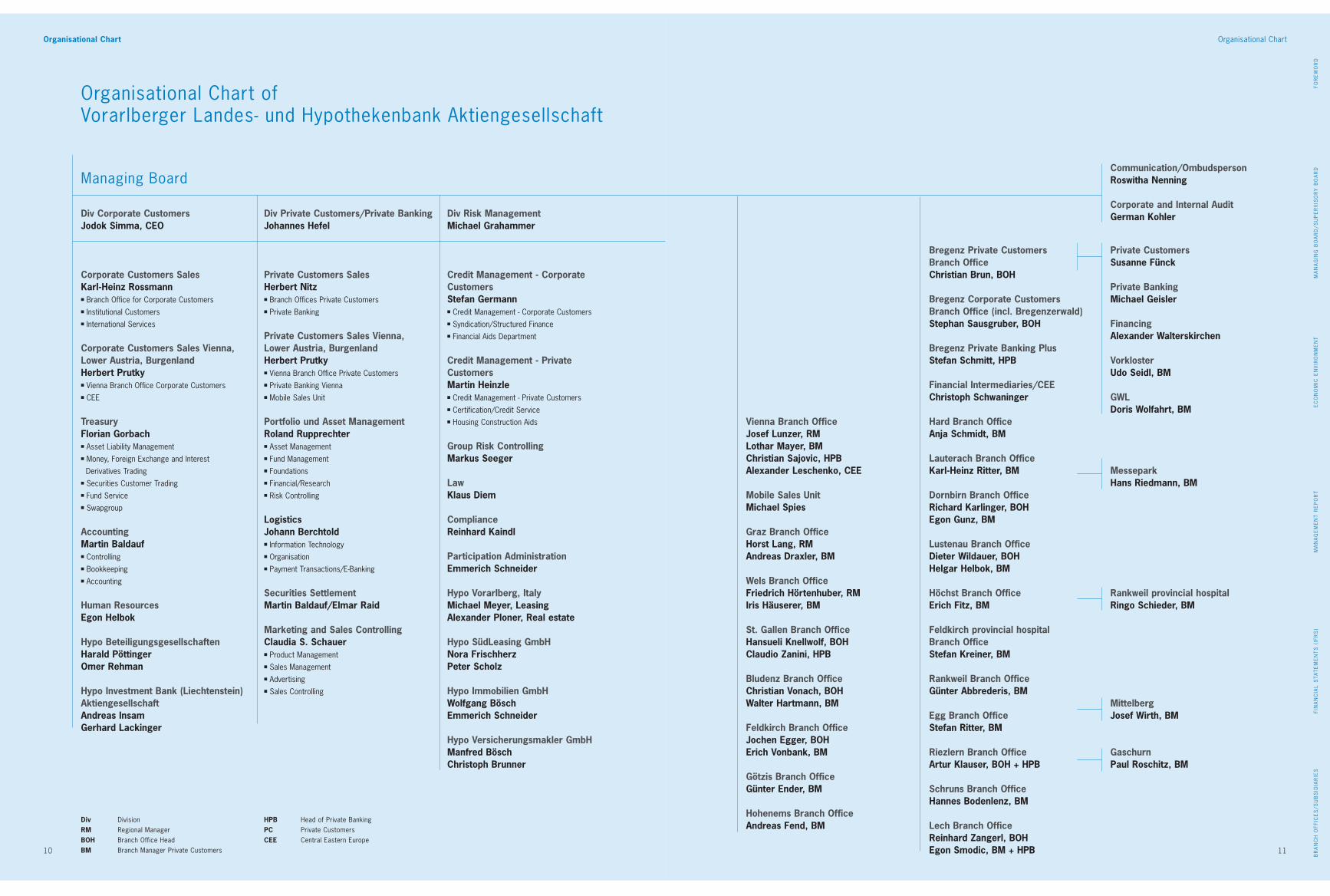

Organisational ChartOrganisational Chart

Managing Board

Div Corporate CustomersJodok Simma, CEO

Corporate Customers SalesKarl-Heinz Rossmann■ Branch Office for Corporate Customers■ Institutional Customers■ International Services

Corporate Customers Sales Vienna,Lower Austria, BurgenlandHerbert Prutky■ Vienna Branch Office Corporate Customers■ CEE

TreasuryFlorian Gorbach■ Asset Liability Management■ Money, Foreign Exchange and Interest

Derivatives Trading■ Securities Customer Trading■ Fund Service■ Swapgroup

AccountingMartin Baldauf■ Controlling■ Bookkeeping■ Accounting

Human ResourcesEgon Helbok

Hypo BeteiligungsgesellschaftenHarald PöttingerOmer Rehman

Hypo Investment Bank (Liechtenstein)AktiengesellschaftAndreas InsamGerhard Lackinger

Div Private Customers/Private Banking Johannes Hefel

Private Customers SalesHerbert Nitz■ Branch Offices Private Customers■ Private Banking

Private Customers Sales Vienna, Lower Austria, BurgenlandHerbert Prutky■ Vienna Branch Office Private Customers■ Private Banking Vienna■ Mobile Sales Unit

Portfolio und Asset ManagementRoland Rupprechter■ Asset Management■ Fund Management■ Foundations■ Financial/Research■ Risk Controlling

LogisticsJohann Berchtold■ Information Technology■ Organisation■ Payment Transactions/E-Banking

Securities SettlementMartin Baldauf/Elmar Raid

Marketing and Sales ControllingClaudia S. Schauer■ Product Management■ Sales Management■ Advertising■ Sales Controlling

Div Risk ManagementMichael Grahammer

Credit Management - Corporate CustomersStefan Germann■ Credit Management - Corporate Customers■ Syndication/Structured Finance■ Financial Aids Department

Credit Management - Private CustomersMartin Heinzle■ Credit Management - Private Customers■ Certification/Credit Service■ Housing Construction Aids

Group Risk ControllingMarkus Seeger

LawKlaus Diem

ComplianceReinhard Kaindl

Participation AdministrationEmmerich Schneider

Hypo Vorarlberg, ItalyMichael Meyer, LeasingAlexander Ploner, Real estate

Hypo SüdLeasing GmbHNora FrischherzPeter Scholz

Hypo Immobilien GmbHWolfgang BöschEmmerich Schneider

Hypo Versicherungsmakler GmbHManfred BöschChristoph Brunner

Div DivisionRM Regional ManagerBOH Branch Office HeadBM Branch Manager Private Customers

HPB Head of Private BankingPC Private CustomersCEE Central Eastern Europe

Communication/OmbudspersonRoswitha Nenning

Corporate and Internal AuditGerman Kohler

Vienna Branch OfficeJosef Lunzer, RMLothar Mayer, BMChristian Sajovic, HPBAlexander Leschenko, CEE

Mobile Sales UnitMichael Spies

Graz Branch OfficeHorst Lang, RMAndreas Draxler, BM

Wels Branch OfficeFriedrich Hörtenhuber, RMIris Häuserer, BM

St. Gallen Branch OfficeHansueli Knellwolf, BOHClaudio Zanini, HPB

Bludenz Branch OfficeChristian Vonach, BOHWalter Hartmann, BM

Feldkirch Branch OfficeJochen Egger, BOHErich Vonbank, BM

Götzis Branch OfficeGünter Ender, BM

Hohenems Branch OfficeAndreas Fend, BM

Organisational Chart ofVorarlberger Landes- und Hypothekenbank Aktiengesellschaft

Bregenz Private CustomersBranch OfficeChristian Brun, BOH

Bregenz Corporate CustomersBranch Office (incl. Bregenzerwald)Stephan Sausgruber, BOH

Bregenz Private Banking PlusStefan Schmitt, HPB

Financial Intermediaries/CEEChristoph Schwaninger

Hard Branch OfficeAnja Schmidt, BM

Lauterach Branch OfficeKarl-Heinz Ritter, BM

Dornbirn Branch OfficeRichard Karlinger, BOHEgon Gunz, BM

Lustenau Branch OfficeDieter Wildauer, BOHHelgar Helbok, BM

Höchst Branch OfficeErich Fitz, BM

Feldkirch provincial hospitalBranch OfficeStefan Kreiner, BM

Rankweil Branch OfficeGünter Abbrederis, BM

Egg Branch OfficeStefan Ritter, BM

Riezlern Branch OfficeArtur Klauser, BOH + HPB

Schruns Branch OfficeHannes Bodenlenz, BM

Lech Branch OfficeReinhard Zangerl, BOHEgon Smodic, BM + HPB

Private CustomersSusanne Fünck

Private BankingMichael Geisler

FinancingAlexander Walterskirchen

VorklosterUdo Seidl, BM

GWLDoris Wolfahrt, BM

MesseparkHans Riedmann, BM

Rankweil provincial hospitalRingo Schieder, BM

MittelbergJosef Wirth, BM

GaschurnPaul Roschitz, BM

FOR

EW

OR

DM

AN

AG

ING

BO

AR

D/S

UP

ER

VIS

OR

y B

OA

RD

EC

ON

OM

IC E

NV

IRO

NM

EN

TM

AN

AG

EM

EN

T R

EP

OR

TFI

NA

NC

IAL

STA

TE

ME

NT

S (

IFR

S)

BR

AN

CH

OFF

ICE

S/S

UB

SID

IAR

IES

13

MA

NA

GIN

G B

OA

RD

/SU

PE

RV

ISO

Ry

BO

AR

DE

CO

NO

MIC

EN

VIR

ON

ME

NT

MA

NA

GE

ME

NT

RE

PO

RT

FIN

AN

CIA

L S

TAT

EM

EN

TS

(IF

RS

)B

RA

NC

H O

FFIC

ES

/SU

BS

IDIA

RIE

S

12

The values we adhere to affect the way others perceive us. This is reflected in our per-

sonal commitment to important topics concerning the future such as energy efficiency,

renewable energy and environmental protection. An extremely low cost-income-ratio,

cost awareness, Austrian efficiency, productivity and a conscientious use of resources

are part of our mindset, and have noticeable effect. We are responsible on all levels – in

our advising with passion and professionalism as well as in our social involvement with

spirit and vision.

14 15

MA

NA

GIN

G B

OA

RD

/SU

PE

RV

ISO

Ry

BO

AR

DE

CO

NO

MIC

EN

VIR

ON

ME

NT

MA

NA

GE

ME

NT

RE

PO

RT

FIN

AN

CIA

L S

TAT

EM

EN

TS

(IF

RS

)B

RA

NC

H O

FFIC

ES

/SU

BS

IDIA

RIE

S

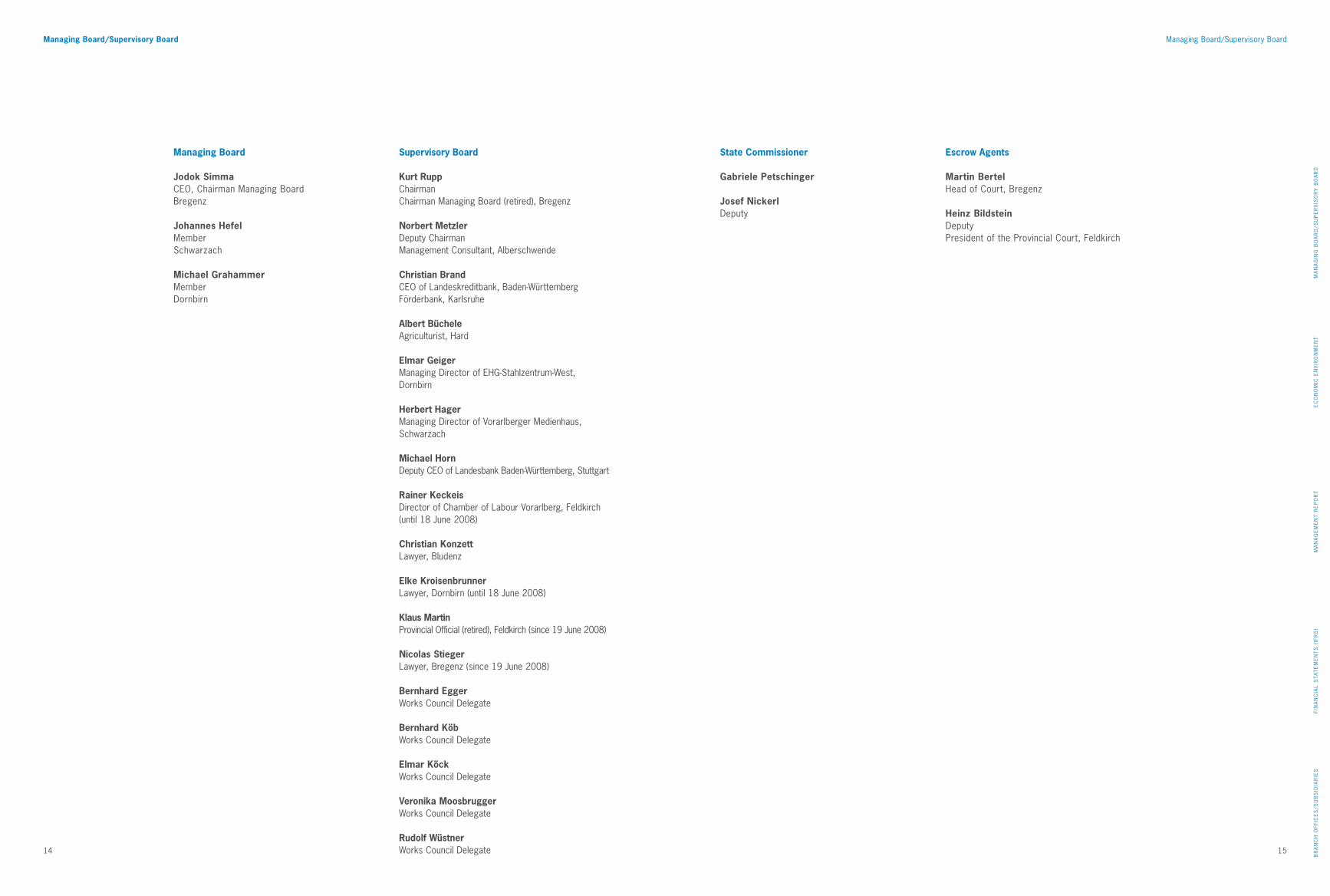

Managing Board/Supervisory Board

Managing Board

Jodok SimmaCEO, Chairman Managing Board Bregenz

Johannes HefelMember Schwarzach

Michael GrahammerMember Dornbirn

Supervisory Board

Kurt RuppChairmanChairman Managing Board (retired), Bregenz

Norbert MetzlerDeputy Chairman Management Consultant, Alberschwende

Christian BrandCEO of Landeskreditbank, Baden-Württemberg Förderbank, Karlsruhe

Albert BücheleAgriculturist, Hard

Elmar GeigerManaging Director of EHG-Stahlzentrum-West, Dornbirn

Herbert HagerManaging Director of Vorarlberger Medienhaus, Schwarzach

Michael HornDeputy CEO of Landesbank Baden-Württemberg, Stuttgart

Rainer KeckeisDirector of Chamber of Labour Vorarlberg, Feldkirch (until 18 June 2008)

Christian KonzettLawyer, Bludenz

Elke KroisenbrunnerLawyer, Dornbirn (until 18 June 2008)

Klaus MartinProvincial Official (retired), Feldkirch (since 19 June 2008)

Nicolas StiegerLawyer, Bregenz (since 19 June 2008)

Bernhard EggerWorks Council Delegate

Bernhard KöbWorks Council Delegate

Elmar KöckWorks Council Delegate

Veronika MoosbruggerWorks Council Delegate

Rudolf WüstnerWorks Council Delegate

State Commissioner

Gabriele Petschinger

Josef Nickerl Deputy

Escrow Agents

Martin BertelHead of Court, Bregenz

Heinz BildsteinDeputyPresident of the Provincial Court, Feldkirch

Managing Board/Supervisory Board

16 17

EC

ON

OM

IC E

NV

IRO

NM

EN

TM

AN

AG

EM

EN

T R

EP

OR

TFI

NA

NC

IAL

STA

TE

ME

NT

S (

IFR

S)

BR

AN

CH

OFF

ICE

S/S

UB

SID

IAR

IES

Managing Board/Supervisory Board

Advisory Board

Herbert SausgruberChairmanProvincial Governor, Höchst

Hans Dietmar SauerDeputy ChairmanRetired Chairman Managing Board, Karlsruhe

Werner AbbrederisManaging Director of GIKO Verpackungen AG, Weiler

Fritz AmannChairman of the Parliamentary Group of the Austrian Freedom Party, Fraxern

Gerhart BachmannPresident Vorarlberg Dental Chamber, Feldkirch

Wilfried BerchtoldMayor, President of the Association of Municipalities of Vorarlberg, Feldkirch

Hubert BertschPresident, Vorarlberg Industrial AssociationConsul of The NetherlandsManaging Director of Bertsch Holding GmbH, Bludenz

Ernst BitscheManaging Director of Erne Fittings GmbH, Schlins

Herbert BlumManaging Director of Julius Blum GmbH, Höchst

Martin DechantChairman, Junior Chamber VorarlbergManaging Director of ikp Vorarlberg PR & Lobbying GmbH, Dornbirn

Guntram DrexelManaging Director of ASPIAG Management AG, St. Margrethen Switzerland

Rudi FeursteinDean, University of Applied Sciences Vorarlberg, Dornbirn

Gerald FleischManaging Director of Vorarlberger Krankenhaus-Betriebsges.m.b.H., Dornbirn

Georg FrühCFO of Alpla Werke Alwin Lehner GmbH & Co KG, Hard

Rainer GögeleChairman of the Parliamentary Group of the Austrian Conservative Party, Mäder

Hans-Dieter GrabherMayor, Lustenau

Heinz HämmerleEntrepreneur, Lustenau

Hubert HämmerlePresident of the Chamber of Labour, Lustenau

Gebhard HalderPresident of the Provincial Parliament, Bregenz-Fluh

Anton HallerHotelier, Mittelberg

Dietmar HefelCEO of Hefel Textil AG, Schwarzach

Josef HuberManaging Director of Huber Invest GmbH, Götzis

Nivard HuberAdministrator of the Monastery of Mehrerau, Bregenz

Robert JanschekManaging Director of Walter Bösch KG, Lustenau

Siegfried JaschinskiChairman of the Managing Board of Landesbank Baden-Württemberg, Stuttgart

Walter KlausEntrepreneur, Klaus

Urs-Peter KollerEntrepreneur, Gossau

Oswin LängleManaging Director of Anton Längle KG, Götzis

Wilfried LenzTax Advisor and Auditor, Dornbirn

Markus LinhartMayor, Bregenz

Hans-Peter LorenzManaging Director of Vorarlberger gemeinnützige Wohnungsbau- und Siedlungsgesellschaft mbH, Dornbirn

Sepp ManhartPresident of the Bar Association of Vorarlberg,Lawyer, Bregenz

Erhard MeierManaging Director of Meier Verpackungen GmbH, Hohenems

Siegfried MetzlerPresident of the Chamber of Public Accountants in Vorarlberg, Dornbirn

Egon MohrProvincial Official, Wolfurt

Josef MoosbruggerPresident of the Chamber of Agriculture, Dornbirn

Lothar NatauPresident of the Administrative Council of Glessmann AG, Wittenbach

Johannes RauchChairman of the Parliamentary Group of the Austrian Green Party, Rankweil

Hubert RhombergChairman, young Industry VorarlbergManaging Director of Rhomberg Gruppe, Bregenz

Michael RitschChairman of the Parliamentary Group of the Austrian Social-democratic Party, Bregenz

Karl-Heinz RüdisserMember of the Provincial Government, Lauterach

Günter SchertlerManaging Director of Schertler-Alge GmbH, Lauterach

Karl SchiemerDirector of the Health Insurance Fund of Vorarlberg, Dornbirn

Hannelore SchneiderHotelier, Lech

Thomas SohmManaging Director of Carini Etiketten GmbH, Lustenau

Werner StrohmaierMayor, Mittelberg

Ludwig SummerCEO of the Illwerke/VKW Group, Bregenz

Eduard TschofenPublic Accountant, Feldkirch

Ingrid WieseneggerManaging Director of Scheyer Verpackungstechnik GmbH, Klaus

Peter WößPresident of the Chamber of Physicians, Rankweil

Managing Board/Supervisory Board

MA

NA

GIN

G B

OA

RD

/SU

PE

RV

ISO

Ry

BO

AR

D

19

MA

NA

GE

ME

NT

RE

PO

RT

FIN

AN

CIA

L S

TAT

EM

EN

TS

(IF

RS

)B

RA

NC

H O

FFIC

ES

/SU

BS

IDIA

RIE

S

18

EC

ON

OM

IC E

NV

IRO

NM

EN

T

Conservative trendsetter – one way to describe Hypo Landesbank Vorarlberg. As a

result of the financial crisis regional banks are enjoying a renaissance. Our unwavering

corporate policies have shown themselves to be valuable and are suddenly “in”. We

finance the local business economy, residential real estate and operate as a partner for

finding mutual solutions for investment. Our new slogan „Passionate. Sound. Advice.“

delivers the message of our professional and ethical commitment to our clients with

renewed clarity.

20 21

EC

ON

OM

IC E

NV

IRO

NM

EN

TM

AN

AG

EM

EN

T R

EP

OR

TFI

NA

NC

IAL

STA

TE

ME

NT

S (

IFR

S)

BR

AN

CH

OFF

ICE

S/S

UB

SID

IAR

IES

Economic environment

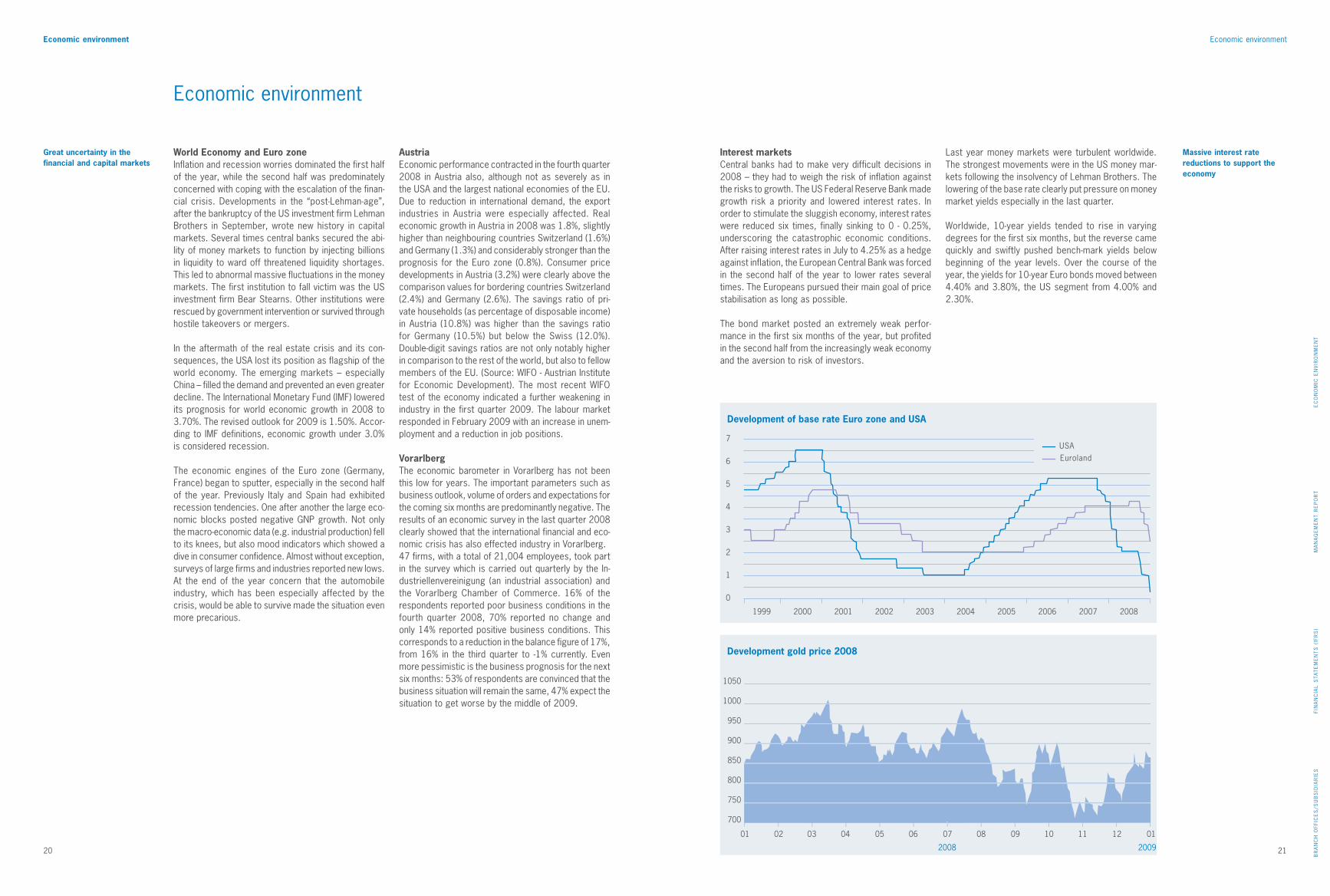

World Economy and Euro zoneInflation and recession worries dominated the first half of the year, while the second half was predominately concerned with coping with the escalation of the finan-cial crisis. Developments in the “post-Lehman-age”, after the bankruptcy of the US investment firm Lehman Brothers in September, wrote new history in capital markets. Several times central banks secured the abi-lity of money markets to function by injecting billions in liquidity to ward off threatened liquidity shortages. This led to abnormal massive fluctuations in the money markets. The first institution to fall victim was the US investment firm Bear Stearns. Other institutions were rescued by government intervention or survived through hostile takeovers or mergers.

In the aftermath of the real estate crisis and its con-sequences, the USA lost its position as flagship of the world economy. The emerging markets – especially China – filled the demand and prevented an even greater decline. The International Monetary Fund (IMF) lowered its prognosis for world economic growth in 2008 to 3.70%. The revised outlook for 2009 is 1.50%. Accor-ding to IMF definitions, economic growth under 3.0% is considered recession.

The economic engines of the Euro zone (Germany, France) began to sputter, especially in the second half of the year. Previously Italy and Spain had exhibited recession tendencies. One after another the large eco-nomic blocks posted negative GNP growth. Not only the macro-economic data (e.g. industrial production) fell to its knees, but also mood indicators which showed a dive in consumer confidence. Almost without exception, surveys of large firms and industries reported new lows. At the end of the year concern that the automobile industry, which has been especially affected by the crisis, would be able to survive made the situation even more precarious.

AustriaEconomic performance contracted in the fourth quarter 2008 in Austria also, although not as severely as in the USA and the largest national economies of the EU. Due to reduction in international demand, the export industries in Austria were especially affected. Real economic growth in Austria in 2008 was 1.8%, slightly higher than neighbouring countries Switzerland (1.6%) and Germany (1.3%) and considerably stronger than the prognosis for the Euro zone (0.8%). Consumer price developments in Austria (3.2%) were clearly above the comparison values for bordering countries Switzerland (2.4%) and Germany (2.6%). The savings ratio of pri-vate households (as percentage of disposable income) in Austria (10.8%) was higher than the savings ratio for Germany (10.5%) but below the Swiss (12.0%). Double-digit savings ratios are not only notably higher in comparison to the rest of the world, but also to fellow members of the EU. (Source: WIFO - Austrian Institute for Economic Development). The most recent WIFO test of the economy indicated a further weakening in industry in the first quarter 2009. The labour market responded in February 2009 with an increase in unem-ployment and a reduction in job positions.

VorarlbergThe economic barometer in Vorarlberg has not been this low for years. The important parameters such as business outlook, volume of orders and expectations for the coming six months are predominantly negative. The results of an economic survey in the last quarter 2008 clearly showed that the international financial and eco-nomic crisis has also effected industry in Vorarlberg.47 firms, with a total of 21,004 employees, took part in the survey which is carried out quarterly by the In-dustriellenvereinigung (an industrial association) and the Vorarlberg Chamber of Commerce. 16% of the respondents reported poor business conditions in the fourth quarter 2008, 70% reported no change and only 14% reported positive business conditions. This corresponds to a reduction in the balance figure of 17%, from 16% in the third quarter to -1% currently. Even more pessimistic is the business prognosis for the next six months: 53% of respondents are convinced that the business situation will remain the same, 47% expect the situation to get worse by the middle of 2009.

Last year money markets were turbulent worldwide. The strongest movements were in the US money mar-kets following the insolvency of Lehman Brothers. The lowering of the base rate clearly put pressure on money market yields especially in the last quarter.

Worldwide, 10-year yields tended to rise in varying degrees for the first six months, but the reverse came quickly and swiftly pushed bench-mark yields below beginning of the year levels. Over the course of the year, the yields for 10-year Euro bonds moved between 4.40% and 3.80%, the US segment from 4.00% and 2.30%.

Economic environment

Economic environment

7

6

5

4

3

2

1

0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

EurolandUSA

Development of base rate Euro zone and USA

01 02 03 04 05 06 07 08 09 10 11 12 01

1050

1000

950

900

850

800

750

700

2008 2009

Development gold price 2008

Interest marketsCentral banks had to make very difficult decisions in 2008 – they had to weigh the risk of inflation against the risks to growth. The US Federal Reserve Bank made growth risk a priority and lowered interest rates. In order to stimulate the sluggish economy, interest rates were reduced six times, finally sinking to 0 - 0.25%, underscoring the catastrophic economic conditions. After raising interest rates in July to 4.25% as a hedge against inflation, the European Central Bank was forced in the second half of the year to lower rates several times. The Europeans pursued their main goal of price stabilisation as long as possible.

The bond market posted an extremely weak perfor-mance in the first six months of the year, but profited in the second half from the increasingly weak economy and the aversion to risk of investors.

Great uncertainty in the financial and capital markets

Massive interest rate reductions to support the economy

22 23

EC

ON

OM

IC E

NV

IRO

NM

EN

TM

AN

AG

EM

EN

T R

EP

OR

TFI

NA

NC

IAL

STA

TE

ME

NT

S (

IFR

S)

BR

AN

CH

OFF

ICE

S/S

UB

SID

IAR

IES

Economic environment

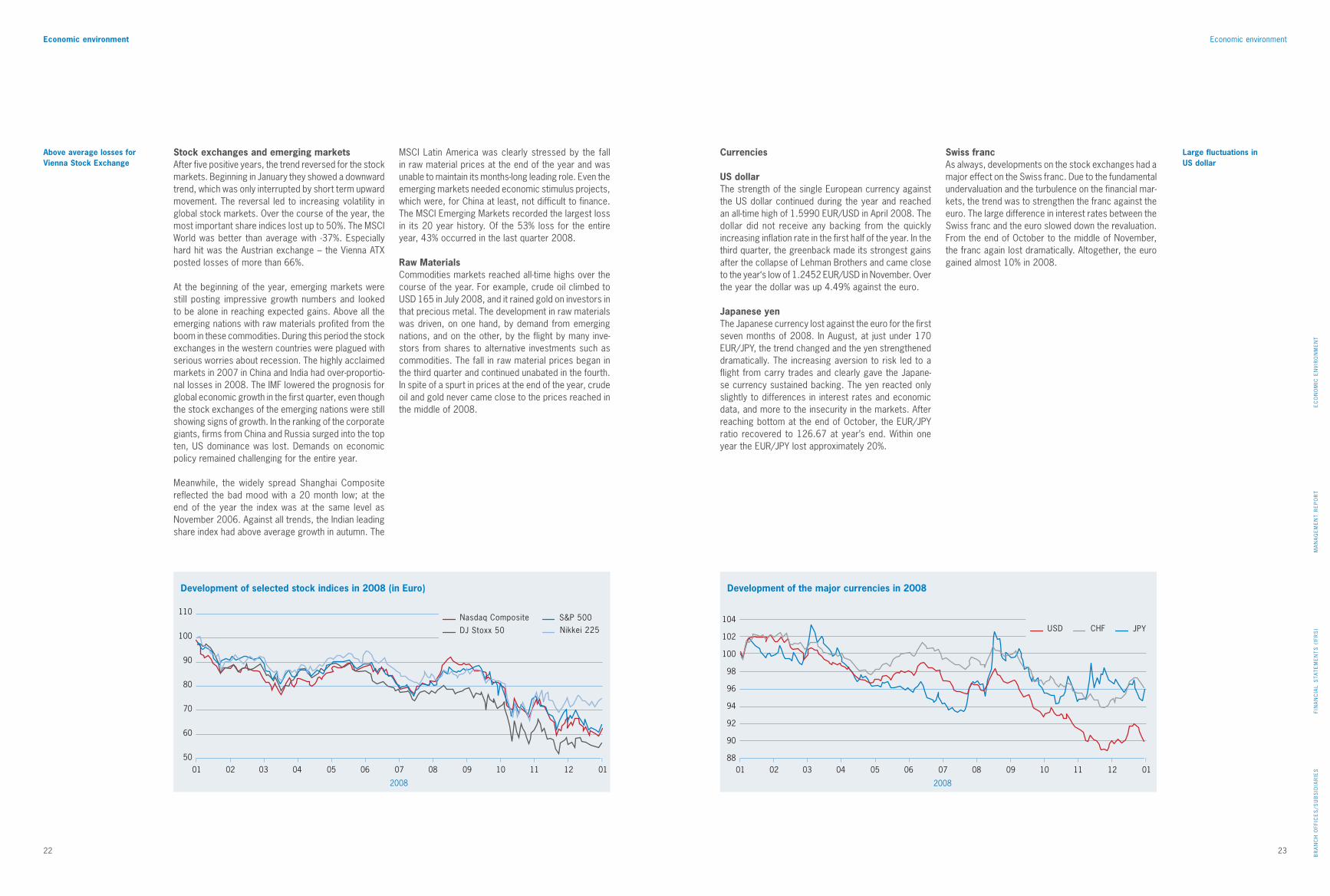

Currencies

US dollarThe strength of the single European currency against the US dollar continued during the year and reached an all-time high of 1.5990 EUR/USD in April 2008. The dollar did not receive any backing from the quickly increasing inflation rate in the first half of the year. In the third quarter, the greenback made its strongest gains after the collapse of Lehman Brothers and came close to the year‘s low of 1.2452 EUR/USD in November. Over the year the dollar was up 4.49% against the euro.

Japanese yenThe Japanese currency lost against the euro for the first seven months of 2008. In August, at just under 170 EUR/JPy, the trend changed and the yen strengthened dramatically. The increasing aversion to risk led to a flight from carry trades and clearly gave the Japane-se currency sustained backing. The yen reacted only slightly to differences in interest rates and economic data, and more to the insecurity in the markets. After reaching bottom at the end of October, the EUR/JPy ratio recovered to 126.67 at year’s end. Within one year the EUR/JPy lost approximately 20%.

Swiss francAs always, developments on the stock exchanges had a major effect on the Swiss franc. Due to the fundamental undervaluation and the turbulence on the financial mar-kets, the trend was to strengthen the franc against the euro. The large difference in interest rates between the Swiss franc and the euro slowed down the revaluation. From the end of October to the middle of November, the franc again lost dramatically. Altogether, the euro gained almost 10% in 2008.

Stock exchanges and emerging marketsAfter five positive years, the trend reversed for the stock markets. Beginning in January they showed a downward trend, which was only interrupted by short term upward movement. The reversal led to increasing volatility in global stock markets. Over the course of the year, the most important share indices lost up to 50%. The MSCI World was better than average with -37%. Especially hard hit was the Austrian exchange – the Vienna ATX posted losses of more than 66%.

At the beginning of the year, emerging markets were still posting impressive growth numbers and looked to be alone in reaching expected gains. Above all the emerging nations with raw materials profited from the boom in these commodities. During this period the stock exchanges in the western countries were plagued with serious worries about recession. The highly acclaimed markets in 2007 in China and India had over-proportio-nal losses in 2008. The IMF lowered the prognosis for global economic growth in the first quarter, even though the stock exchanges of the emerging nations were still showing signs of growth. In the ranking of the corporate giants, firms from China and Russia surged into the top ten, US dominance was lost. Demands on economic policy remained challenging for the entire year.

Meanwhile, the widely spread Shanghai Composite reflected the bad mood with a 20 month low; at the end of the year the index was at the same level as November 2006. Against all trends, the Indian leading share index had above average growth in autumn. The

MSCI Latin America was clearly stressed by the fall in raw material prices at the end of the year and was unable to maintain its months-long leading role. Even the emerging markets needed economic stimulus projects, which were, for China at least, not difficult to finance. The MSCI Emerging Markets recorded the largest loss in its 20 year history. Of the 53% loss for the entire year, 43% occurred in the last quarter 2008. Raw MaterialsCommodities markets reached all-time highs over the course of the year. For example, crude oil climbed to USD 165 in July 2008, and it rained gold on investors in that precious metal. The development in raw materials was driven, on one hand, by demand from emerging nations, and on the other, by the flight by many inve-stors from shares to alternative investments such as commodities. The fall in raw material prices began in the third quarter and continued unabated in the fourth. In spite of a spurt in prices at the end of the year, crude oil and gold never came close to the prices reached in the middle of 2008.

Large fluctuations in US dollar

Economic environment

01 02 03 04 05 06 07 08 09 10 11 12 01

110

100

90

80

70

60

50

2008

Nikkei 225DJ Stoxx 50

Nasdaq Composite S&P 500

Development of selected stock indices in 2008 (in Euro)

01 02 03 04 05 06 07 08 09 10 11 12 01

104

102

100

98

96

94

92

90

88

2008

CHFUSD JPY

Development of the major currencies in 2008

Above average losses for Vienna Stock Exchange

24 25

EC

ON

OM

IC E

NV

IRO

NM

EN

TM

AN

AG

EM

EN

T R

EP

OR

TFI

NA

NC

IAL

STA

TE

ME

NT

S (

IFR

S)

BR

AN

CH

OFF

ICE

S/S

UB

SID

IAR

IES

Questions to Jodok Simma

Assessment of the business year 2008?Hypo Landesbank Vorarlberg ended the 2008 business year with group results of EUR 50 million. This corre-sponds exactly to plan and is an impressive indication that our mix of profit pillars puts us in an excellent strategic and crisis resistant position.

Both the interest business and low credit risk costs clearly contributed to the positive year end results. Due to growth in volume in lendings and the strong reduction in credit risk costs, net interest income after loan loss provisions increased by 17.5% to EUR 96.7 million. Although net fee and commission income fell by 10.4% due to the market turbulence, it remained at a high level with EUR 41.9 million.

Corporate philosophy and strategy?Over the years, Hypo Landesbank Vorarlberg has posi-tioned itself as a corporate, investment and residential real estate bank and is one of the top regional banks in Austria. We follow a down to earth business policy, speculation was never our business.

The stable and enduring success of Hypo Landesbank Vorarlberg certainly has to do with our basic principles – to always be committed to the customer and to long-term success. We believe in continuity and will stay with our proven, long-term business and credit policies.

We view our entire market area as an “expanded home market”. We are active in Vorarlberg, the Lake Constance region and in Austria as well as selectively in the border areas of Eastern Switzerland, Liechtenstein, Southern Germany, and Northern Italy. We will continue to be on the offensive in our market. Quick decision tak-ing, absolute discretion, fair conditions and the safety and stability of our owners are strong arguments for choosing a banking relationship, especially in difficult financial times.

Hypo Landesbank Vorarlberg self-image as corporate bank?We not only support businesses in financial matters, we also offer a comprehensive pallet: from interest ma-nagement, international services, and support services to solutions for company-specific investment queries. These banking services are complemented by our subsidiaries Hypo-Versicherungsmakler (insurance), Hypo-Immobilien GmbH (real estate), Hypo SüdLeasing GmbH (property leasing), as well as HyPO EQUITy Management AG, specialised in equity capital invest-ments. In addition, the Hypo Academy and the popular semi-annual Hypo breakfast for entrepreneurs have developed into excellent communication platforms. We want to offer our customers added value – particularly in difficult times.

Credit crunch?Loans are being awarded everyday and we have noted healthy competition. There cannot be a credit crunch when customers are able to get loans from several banks. All viable loans are granted and loans that would have been denied before are still denied. Although we are observing a noticeable reduction in requests for loans, there are still many companies that are cautiously but optimistically implementing investment plans.

From a total lending volume of EUR 7.3 billion, 70% went to corporate customers. These figures prove two things. The first is that Hypo Landesbank Vorarlberg is the leading corporate bank in Vorarlberg; three-fourths of the top 100 businesses in Vorarlberg have a relation-ship with us. And secondly, these figures show clearly that Hypo Landesbank Vorarlberg is not experiencing the oft-mentioned credit crunch.

Economic crisis?Every crisis contains opportunities. A crisis forces the choice between the essential and the non-essential. Nice to do becomes need to do. Nice to have becomes need to have.

A crisis means questioning habits and this can be a great opportunity. A crisis means decision making and implementation. The results count more. A crisis – whether business or private – pulls people out of the comfort zone. But this is also very important: in a crisis real leaders show themselves and this is now required of us on the Managing Board as well as our executive team. It has fallen to us to make strategic decisions and goals to meet the new conditions.

Committed to long-term success

Questions to Jodok Simma CEO, Chairman Managing Board

Questions to Jodok Simma

Outlook for the business year 2009?An exact prognosis for the current year is difficult. We consider the outlook in our region to be positive com-pared to other countries and regions. In accordance with plans we will be decelerating growth in total assets and systematically reallocating resources into loans and advances to customers in our core markets.

Our bank will continue to be confronted with uncertain-ties from the financial crisis and the threat of recession. Against that background, 2009 has begun on a some-what muted note. We anticipate results for 2009 to be lower than the 2008 results if loan loss provisions rise substantially and adjustments become necessary.

Curriculum Vitae Jodok Simma

Jodok Simma (62), CEO and Chair-man of the Board, has been a member of the Managing Board of Hypo Landesbank since 1975. After his commercial science studies at the Vienna University of Business Administration, Mr. Simma began his career in the accounting depart-ment of Girozentrale in Vienna. In 1980, he was appointed Deputy Chairman of the bank’s Board, becoming Chairman of the Board in 1997. Jodok Simma has been Section Representative and thus Spokesman for all banks and insu-rance companies in Vorarlberg since 2000. Until 2006, he served as President of the Association of the Austrian Landes-Hypotheken-banken for two terms. Besides ser-ving as Spokesman for the Board, Jodok Simma is also the head of the departments Corporate Custo-mers Sales, Treasury, Accounting, Human Resources, the Hypo Invest-ment Bank (Liechtenstein) AG, and the associated companies HUBAG and HEMAG.

26 27

EC

ON

OM

IC E

NV

IRO

NM

EN

TM

AN

AG

EM

EN

T R

EP

OR

TFI

NA

NC

IAL

STA

TE

ME

NT

S (

IFR

S)

BR

AN

CH

OFF

ICE

S/S

UB

SID

IAR

IES

Questions to Johannes Hefel Questions to Michael Grahammer

Questions to Johannes Hefel, Managing Board Private Customer, Private Banking, Portfolio and Asset Management

Questions to Michael Grahammer, Managing Board Risk Management, Leasing and Real Estate

Curriculum VitaeJohannes Hefel

Johannes Hefel (51) has been a member of the Board of the Bre-genz-based Vorarlberger Landes- und Hypothekenbank AG since 1997. His responsibilities include the departments Private Custo-mer Sales, Private Banking, and Portfolio and Asset Management. He previously worked as financial analyst and asset manager, and as a business consultant and manage-ment trainer in Liechtenstein and Frankfurt am Main. In 1982, he con-cluded his business management studies with a Master’s degree, and went on to obtain a doctoral degree in economic and social sciences in 1985.

Curriculum VitaeMichael Grahammer

Michael Grahammer (43) was appointed member of the Board of Hypo Landesbank Vorarlberg as of 1 July 2004, and is respons-ible for Risk Management, Leasing, Real Estate, Legal Matters, and Equity Companies. After having obtained his doctoral degree in commercial sciences (Vienna Uni-versity of Business Administration), Mr. Grahammer began his career in 1993 as country adviser and team leader for Africa and Asia at Raiffeisen Zentralbank AG. In 1997, he became the head of the Risk Man-agement department of Raiffeisen-bank in the Czech Republic, and was appointed member of its Managing Board in 1999. In 2000, Vorarl-berg-born Grahammer returned to his home province, where he was appointed Regional Director of the commercial business of Erste Bank der Österreichischen Sparkassen AG. In late 2001, Mr. Grahammer changed to Hypo Landesbank Vorarl-berg, where he was put in charge of the leasing department.

Developments in Private Customer Sector in 2008?Lendings to Private Customers grew to EUR 1,491.4 million, more than double the amount in 2000. We plan to build on our position as a construction financing bank this year. With the Hypo-Klima-Kredit, the Hypo-Lebenswert-Kredit and the Hypo-Generationen-Kredit, we have an especially interesting range of products.

Developments in customer funds?Throughout 2008, and especially after the financial crisis intensified, Hypo Landesbank Vorarlberg noted a large inflow of customer funds. Savings deposits grew by 28.4% to EUR 1,407.7 million. In total, customer deposits increased by 21.1% to just under EUR 4 bil-lion. This inflow underlines the trust customers have in Hypo Landesbank Vorarlberg. Special-interest savings books were especially popular in 2008.

Hypo Landesbank Vorarlberg among top 5 Austrian private banksHypo Landesbank Vorarlberg was able to further strengthen its excellent position as an investment bank in Vorarlberg and Austria. Our standings in both the “Fuchsbriefe Report” and the “Elite Report” underscore the excellent quality of Hypo Landesbank Vorarlberg. We are the only bank to be ranked among the top five investment banks in Austria in both reports.

In 2008, the Hypo-Weltdepot Dynamik Aktien fund of funds, an asset management strategy with value protection first introduced in 2004, proved its value during a difficult year for the markets. The shares were systematically reduced to zero.

New asset management strategy Hypo-Weltdepot Dynamik AnleihenWith Hypo-Weltdepot Dynamik Anleihen, a bond fund, the bank has successfully found a fitting and quick answer to changing market conditions. In the five months from its start on 1 August 2008 to the end of the year, the asset management strategy reached a performance of 4.92% (11.8% annualised). This entails an asset management strategy with active duration controls – a bond strategy that can profit from both rising and falling interest rates equally.

Outlook for 2009?The investment area will continue to be uncertain in 2009. High on our list of priorities for our customers is the need for close supervision and counselling and we are making customer support a main focus in 2009. We understand that due to the current market conditions it will take time to rebuild customer trust in financial markets. Our advisory service will concentrate on com-municating our long-term investment philosophy as well as consistent attention to safeguarding assets.

It is certain that we will have – based on a record level – a worldwide decline in economic growth as well as decidedly lower profits from corporations. At the same time there is the danger of deflation as well as the threat from massive national debt in many countries due to economic stimulation measures.

What do you recommend to investors? We are current experiencing a situation that has not occurred for several generations, something like “driv-ing in fog”. Investors must proceed carefully, be well informed and use common sense. What is on offer? A relatively large part should be in a savings account. I recommend investing another part in short to middle-term bonds from bond issuers with excellent credit ratings. And up to 10% of the investment should be in gold, a recommendation the bank has been making for years, in preparation for the current market situ-ation. With gold investments it makes sense to take advantage of temporary price fluctuations in the gold position. A portion of the investment can also be put in shares, when the investor has the patience and the nerves. The handling of money was and remains con-servative at Hypo Landesbank Vorarlberg. Great value is placed on security – very positive for customers in these turbulent times.

Appraisal of 2008 from the risk side?From a risk management perspective, 2008 was a challenging year. In particular were the questions con-cerning which risks exist and how can the bank maintain an optimal chance-risk-ratio in terms of sustainable growth even under changing conditions. Among other measures, we do a risk bearing ability calculation every month.

Loan loss provisions were notably reduced and are in relation to lending volume at an historic low. Traditional-ly we have practised a conservative loan loss provisions policy. In parallel we were able to further improve the quality of our credit portfolios.

It has become evident that the organisational changes implemented over the last few years (centralised corporation-level bank risk management, enhanced credit management) were timely and proper steps in response to the new requirements for professional, comprehensive bank risk management.

Priority for 2008 – EnergyA priority for 2008 was environmental protection and support for renewable energy. With over EUR 260 million in energy saving and energy optimising invest-ments, we recognise a strong demand for this type of financing. Energy efficiency is essential in our own construction projects also. Through renovations in our new headquarters we have been able to halve energy costs. The Hypo Office in Dornbirn was conceived as an ultra-low energy project and is the first office building in Vorarlberg to be enlarged and renovated to Passive House standards.

Highlight: Headquarters reopening 17 October 20082008 was a special year for anniversaries and in-vestments in the 111 history of Hypo Landesbank Vorarlberg. With an investment of EUR 16.5 million, our headquarters has been expanded and modernised to offer our customers and our advisors the best possible support facilities.

Hypo subsidiaries under one roofHypo Immobilien GmbH, a subsidiary of Hypo Lan-desbank Vorarlberg, as developer of the Hypo Office Dornbirn project, proposed bringing several Hypo sub-sidiaries with know-how in real estate, insurance and leasing under one roof to provide one stop shopping for clients. The central location with excellent transport connections was a factor in the concept. Currently the Hypo Office Dornbirn has 141 workstations, 61 of these for employees of Hypo subsidiaries. This gives us the ideal conditions to create synergy in the real estate, leasing, insurance and banking areas and to offer tailor made, comprehensive support to our customers, thus giving them the assurance that they have found the optimal solution.

Leasing sector?Our leasing business is divided into two subsidiaries: Hypo SüdLeasing GmbH in Austria and in Italy the Hypo Vorarlberg Leasing AG. Together, the subsi-diaries reached a new volume level of over EUR 500 million in 2008. Significantly lower growth is expected in 2009.

Outlook 2009The flattened demand for credit in the first quarter 2009 was the first sign of an economic slowdown. We must therefore be especially careful in recognising and managing credit risk this year. In 2009, many of our corporate customers will need to adapt capacity in time. It is essential in a downturn to safeguard company success. This includes us – in addition to credit risk costs, we need to keep a watchful eye on our own administrative costs (staff and operating expenses).

29

FIN

AN

CIA

L S

TAT

EM

EN

TS

(IF

RS

)B

RA

NC

H O

FFIC

ES

/SU

BS

IDIA

RIE

S

28

MA

NA

GE

ME

NT

RE

PO

RT

Quality goes hand in hand with transparency. Transparency fosters trust. And trust in turn

enhances quality. This is the cycle of healthy growth and the enduring corporate strategy

that Hypo Landesbank Vorarlberg is committed to. Our expansion course is being carried

out selectively and is characterised by sustainable success. We know our customers,

opportunities and limits. And therefore remain transparent and predictable.

30 31

MA

NA

GE

ME

NT

RE

PO

RT

FIN

AN

CIA

L S

TAT

EM

EN

TS

(IF

RS

)B

RA

NC

H O

FFIC

ES

/SU

BS

IDIA

RIE

S

Consolidated management report

Group management report The business model employed by Vorarlberger Landes- and Hypothekenbank Aktiengesellschaft has proven itself even in a tough market environment. The Hypo Vorarlberg Group closed out the year 2008 with result of ordinary business activities of EUR 50.0 million in line with estimates, and will be distributing a dividend to shareholders in the same amount as the previous year. Historically focused on risk-contained growth, continuity and sustainability, Hypo Landesbank Vorarlberg is seen by customers as a safe haven in turbulent times for the banking industry.

The Financial Times newspaper compiles and publishes annual international and national rankings of the 1,000 largest banks based on assets and earnings in the trade magazine The Banker. Hypo Landesbank Vorarlberg is ranked 10th among Austrian banks, advancing in the international rankings to 554 (from a previous 583).

Income statement 2008:A year-on-year comparison of the individual income statement positions is presented below.

Net interest incomeNet interest income came in higher at EUR 113.0 mil-lion, up by EUR 2.6 million or 2.4% due to a 24.3% increase in loans and advances to customers, despite margin pressures, particularly in the first half of the year. Interest business thus contributed substantially to earnings for 2008.

Loan loss provisionsLoan loss provisions required for the credit business declined sharply year-on-year to EUR 16.3 million (down 42.0%). This represented a considerable decline in relation to loan volume, principally reflecting the general stability of the Austrian economy in 2008.

We pursue a highly conservative risk policy. Concer-ning our risk management objectives, please refer to the statements concerning financial risk and risk management in the consolidated financial statements, and in particular the disclosures per Section 26 of the Austrian Banking Act posted on the bank’s website, www.hypovbg.at.

Net fee and commission incomeNet fee and commission income came in 10.4% lower year-on-year at EUR 41.9 million, but remained at a high level. The decline in net fee and commission income reflects changing investor behaviour accompanying the financial market turmoil.

Net trading resultThe net trading result of EUR -2.1 million mainly reflected lower income from securities trading and the valuation of assets held for trading and voluntarily designated at fair value through profit or loss, as a result of volatility related to the financial crisis.

Other operating income and expensesThe sharp decline in other operating income was due to one-time income from insurance benefits and other nonrecurring items from the previous year.

Administrative expensesPersonnel expenses increased 8.7% year-on-year to EUR 49.0 million. Wages and salaries increased 6.7% to EUR 36.6 million, although the Hypo Vorarlberg Group employed 44 more staff than in the year before. The average number of bank employees rose in the year under review from a previous 683 to 727 (weighted by capacity utilisation rate). Successful execution of our growth strategy over the last several years necessita-ted additional hiring of clients advisors and back-office reorganisation (Basel II, reporting). Plans are for staff levels to remain stable over the next few years.

Materials expenses increased 7.8% to EUR 29.2 million, due mainly to a number of construction and renovation projects. The corporate headquarters in Bregenz un-derwent a thorough renovation and the premises were expanded in 2007 and 2008. This work was concluded on schedule and on-budget in October 2008.

Operating resultsOperating income net of operating expenses yields operating results of EUR 58.6 million, down by EUR 2.4 million or 4.0% year-on-year.

As of 31 December 2008, the cost-income ratio for the Bank Group was 52.82% (versus a previous 46.69%). The increase in the CIR chiefly reflected a lower net trading result. We remain one of Austria’s leading banks with respect to this metric.

Net results from financial instrumentsIncreasing volatility due to a general increase in credit risk premiums and customer downgrades affected the valuations of certain securities held in the nostro account. Net results from financial instruments thus came to EUR -5.8 million

Results of ordinary business activities and profitability Results of ordinary business activities totalled EUR 50.0 million for fiscal year 2008, in line with estimates.

Business model proves its worth

EUR 50 million ordinary business results

Consolidated management report

Consolidated management report

46,724629

9,446110,422

41,869Net interest income

Net fee and commision incomeTrade results

Other operating results

6,007

113,030

2007 2008

2007 2008

11,979.613,158.7

Development of total assets(in million EUR)

2007 2008

60,064 50,004

Development of ordinary business results(in ’000 EUR)

Structure of resultsHypo Landesbank Vorarlberg(in ’000 EUR)

32 33

MA

NA

GE

ME

NT

RE

PO

RT

FIN

AN

CIA

L S

TAT

EM

EN

TS

(IF

RS

)B

RA

NC

H O

FFIC

ES

/SU

BS

IDIA

RIE

S

Consolidated management report

The Bank’s return on equity (ROE) before taxes was 11.16% (previous year: 14.06%). Consolidated net incomeA 55.7% decline in taxes on income to EUR 9.2 million resulted from a Bank audit last year. After deducting minority interests from earnings after taxes, the Hypo Vorarlberg Group reported consolidated net income of EUR 40.4 million (previous year: EUR 38.7 million), a 4.3% rise.

Proposal for profit distribution: Unchanged dividend

The Managing Board cancelled plans to issue new Hypo Landesbank Vorarlberg participation certificates in autumn 2008 in view of the tremendous uncertainty unleashed by the Lehman Brothers bankruptcy.

All outstanding participation certificates were redeemed on 21 November 2008 pursuant to an 18 June 2008 shareholder resolution at a price of EUR 99.00 set 25 November 2008. Upon publication of the redemption resolution, the participation certificates were delisted from the Vienna Stock Exchange and new participation capital with a nominal value of EUR 9 million was placed with the shareholders (Vorarlberger Landesbank-Holding, Landeskreditbank Baden-Württemberg Förderbank).

At the annual meeting of shareholders on 17 June 2009, the Managing Board will propose distributing to Vorarlberger Landesbank-Holding Austria Beteiligungs-gesellschaft mbH (Landesbank Baden-Württemberg and Landeskreditbank Baden-Württemberg Förderbank) and other shareholders dividends totalling EUR 8.79 million on share capital of EUR 150 million. Balance sheet

Group total assets rose 9.8% to EUR 13,158.7 million in fiscal year 2008. Customer business played a signifi-cant part in the growth of total assets, in terms of both assets and liabilities.

On the assets side, loans and advances to customers were up 24.3% to EUR 7,337.5 million, taking into account that compliance with IFRS 7 is mandatory as of 1 January 2007. This standard also requires finan-cial instruments to be shown separately by valuation category as per IAS 39. For this reason, the Group re-classified loans and advances to banks and customers voluntarily designated at fair value through profit or loss in the amount of EUR 684.2 million (2007: EUR 622.9 million) as ‘Financial assets – at fair value’ for fiscal year 2008 and the previous year. This item qualifies and is reportable as loans and advances to customers.

The increase in loans and advances to customers broke down regionally as follows: Austria + EUR 637.1 million, Germany + EUR 296.0 million, Italy + EUR 266.6 million, Switzerland and Liechtenstein + EUR 231.0 million. The expanding Vienna, Graz and Wels markets had the high-est growth rates in Austria. The most product growth was seen with other loans (+ 32.7%) and overdraft lines (+39.4%). This accounted for the 73.5% increase in loans and advances to customers repayable on demand to EUR 1,756.0 million

Under financial assets, primarily consisting of nostro accounts, securities designated available-for-sale de-creased by 51.9% in the year under review as a result of a reclassification to loans and advances to banks and customers. The Bank’s complete portfolio of financial assets totalled EUR 3,221.1 million (previous year: EUR 3,544.9 million).

On the liabilities side, amounts owed to customers increased most, up 21.1% by EUR 692.8 million to EUR 3,974.8 million as of December 31, 2008. This major increase in deposit volume reflected strong customer demand for special-interest savings books (+ 62%), un-derscoring customers’ confidence in Hypo Landesbank Vorarlberg. Financial liabilities at fair value increased 7.3% by EUR 396.6 million to EUR 5,814.4 million.

Capital resourcesShare capital was increased by EUR 128 million from reserves to EUR 150 million, participation capital in-creased from a nominal EUR 2.18 million to EUR 9 million.

The assessment basis of consolidated capital resources according to the Austrian Banking Act increased 11.4% to EUR 7,078.2 million in 2008. After the distribution of dividends totalling EUR 8.790 million, an amount of EUR 29.6 million was allocated to core capital (tier 1) as reserves. Core capital now totals EUR 558.6 million, a 10.2% year-on-year increase. As of 31 December 2008, the Hypo Vorarlberg Group recorded supple-mentary capital resources (tier 2) of EUR 287.0 million, resulting in attributable capital resources of EUR 842.3 million (+ 7.1%) after deductions. Based on required capital resources of EUR 591.8 million, surplus cover thus amounts to EUR 250.5 million. At 31 December 2008, the core capital ratio (banking book) was 7.89%, representing a 0.08% decrease year-on-year. At 11.90% the bank book debt-equity ratio (total capital ratio or solvency margin) was 0.47% lower year-on-year, though well above the 8.0% required by regulations. Barring changes in regulatory requirements, the Bank’s capital resources continue to be comfortable, also in view of the risk profile.

Above average growth in lendings by 24%

Increase of share capital to EUR 150 million

Consolidated management report

Austria 62.0 %

Switzerland/Liechtenstein 8.9 %

Germany 11.9 %

Italy 14.8 %

Other foreign countries 2.4 %

Loans and advances to cutomers 55.8 %

Financial assets 24.5 %

Loans and advances to, and placements with, banks 14.4 %

Other assets 5.3 %

Industry, Trade and Commerce 28.2 %

Leasing 18.6 %

Real estate 12.3 %

Public 8.4 %

Other 10.2 %

Employed and Independent Professionals 22.3 %

Amounts owed to customers 30.2 %

Shareholders' equity 3.7 %

Financial liabilities (AFV) 44.2 %

Other liabilities 6.7 %

Own issues 15.2 %

Loans and advances to customers – breakdown by region(in %)

Structure of assets(in %)

Loans and advances to customers –breakdown by sector(in %)

Structure of liabilities(in %)

34 35

MA

NA

GE

ME

NT

RE

PO

RT

FIN

AN

CIA

L S

TAT

EM

EN

TS

(IF

RS

)B

RA

NC

H O

FFIC

ES

/SU

BS

IDIA

RIE

S

Consolidated management report

Development of Hypo Landesbank Vorarlberg by segment

The Bank’s core business segments are Corporate Services/Public Sector and Private Customers, which are run as separate sales organisations. The Private Banking and Asset Management segment is attributed to both the Corporate Services and Private Customers segments on a split basis.

Corporate Customers and Public Sector – Hypo Landesbank Vorarlberg, the corporate bank

For years, Hypo Landesbank Vorarlberg has been a partner to corporate enterprises and a specialist in the creation of sophisticated financing solutions for private and public-sector organisations.

Dependable corporate partnerIn the Group, the Corporate Customers segment ac-counts for loans totalling EUR 4,773.1 million. This lending volume underscores the leading position of Hypo Landesbank Vorarlberg as a commercial lender and business bank. In 2008, the sector generating the most net growth for the Bank was industry, which contributed EUR 365.2 million, followed by leasing with EUR 301.5 million, trade with EUR 116.8 million and real estate with EUR 77.0 million.

Renewable energies and climate protection were a strategic focus in 2008. Hypo Landesbank Vorarlberg financed nearly 100 projects valued at a total EUR 262.8 million in 2008, half of which were in Austria. The primary alternative energy sources are wind, solar, biomass and water.

Due to the increase in lending volume, net interest income rose 16.3% to EUR 49.6 million. Net fee and commission income increased 3.6% to EUR 11.3 million, boosted by securities and documentary business in the Corporate Customer segment. Proprietary investment products have been well received by corporate custo-mers. The new team of Private Banking Plus specialists ensures our ability to provide professional support to businesses and owners. In our growth markets out-side Vorarlberg (Vienna, Graz, Wels, Switzerland and Southern Germany), we saw satisfactory growth in both sales and earnings. The Corporate Customer segment recorded earnings before taxes (results of ordinary business activities) of EUR 35.9 million (EUR 39.8 mil-lion including the Public Sector unit). This substantial earnings increase was due to the 50% reduction in loan loss provisions to EUR 7.5 million.

The significant rise in commercial lending volume illus-trates Hypo Landesbank’s importance as a dependable partner to corporate enterprises. Being a universal bank, Hypo Landesbank Vorarlberg offers customers both traditional banking products and a range of banking-related services including leasing, real estate services and insurance via subsidiaries. The portfolio of financing products is rounded out by equity financing, expert consulting and support/liaison in connection with funding programmes and public-sector institutions.

Vorarlberg Health Awareness AwardIn the year under review, for the third time Hypo Lan-desbank Vorarlberg presented the Vorarlberg Health Awareness Award to innovative companies based in Vorarlberg that show their commitment to addressing employee health issues through the implementation of creative and innovative health projects for staff members. Hypo Academy for EntrepreneursHypo Landesbank Vorarlberg looks back on a long and very successful history of commercial customer business. The Hypo Academy for Entrepreneurs was created especially for entrepreneurs, in conjunction with publishing a Hypo guideline for entrepreneurs. The Hypo Entrepreneurs Breakfast, held twice a year by Hypo Landesbank Vorarlberg, has become an ex-tremely popular communication forum for business decision-makers.

Private Customers

The Hypo Landesbank Vorarlberg Private Customers business has a dual focus on residential construction financing and banking services for affluent private cus-tomers. Because Hypo Landesbank understands that each customer is individual, we offer a spectrum of tailored financing and investment solutions.

Loans and advances to customers in the Private Cus-tomers segment increased 7.1% year-on-year to EUR 1,491.4 million. The big 21.4% increase in amounts owed to customers to EUR 2,113.7 million was due in particular to the special-interest savings books with a 12-months minimum holding period.

Net interest income from the Private Customers seg-ment rose 9.1% to EUR 38.7 million. The Private Custo-mers segment generated results of ordinary business activities of EUR 13.5 million, down 22.4% year-on-year. This decline primarily reflected lower net fee and com-mission income due to the market situation.

Residential real estate bank As a Landesbank state banking institution, residential construction financing is a traditional core element of our business model. In 2008, we further consolidated on our position as the residential real estate bank for the province of Vorarlberg. Residential construction loans increased 42% overall to EUR 1,459.2 million.

During the year under review the Bank added on the Hypo-Lebenszeit-Kredit to complement the Hypo-Le-benswert-Kredit financing product designed for older individuals. This generational loan is also available to EU citizens with official residence in Austria for properties located in Austria.

As trustee for the province of Vorarlberg, the bank ma-nages a portfolio of subsidised residential construction loans not recorded on the balance sheet. As of 31 De-cember 2008, a total of 54,013 loans were outstanding with a total volume of EUR 1,780.8 million. In 2008, approximately EUR 88.3 million in new loan subsidies were disbursed, offset by redemption repayments of EUR 74.1 million.

Energy-saving Hypo-Klima-Kredit loansThe Bank provides Hypo-Klima-Kredit loans to finance any form of energy-saving investment. The goal is to promote energy-conserving measures by offering at-tractive lending terms, in cooperation with the Energy Institute Vorarlberg.

Private Banking Hypo Landesbank Vorarlberg is the leading asset man-agement bank in the Vorarlberg province. We operate Private Banking Centres in all large branch offices in Vorarlberg, as well as in Lech, Vienna, Graz and Wels. These centres provide exceptionally high-quality advice, staffed exclusively by certified investment advisors. Raising the qualification level of Private Banking ad-visors even further was a particular training focus in fiscal year 2008. Seventeen staff members completed financial advisor training to receive the official Austrian certification of Diplom. Finanzberater (BAK).

The superior quality of our investment consulting and as-set management services has been confirmed through outside recognition in the Fuchsbriefe Report and the Elite Report. The Elite Report gave Hypo Landesbank Vorarlberg the elite “cum laude” distinction in its pro-minent peer rankings. The 2009 Fuchs Report ranked Hypo Vorarlberg a solid fourth place in Austria, making us the only bank to qualify in Austria’s top 5 with both ranking organisations.

Spotlight on securityRegional banks like Hypo Vorarlberg have been ex-periencing a renaissance since the outbreak of the financial crisis. Savings deposits of EUR 372.2 million in the Private Customers segment highlight the confidence customers have in Hypo Landesbank Vorarlberg. For Hypo Landesbank, handling money has always been something conservative. Security is a top priority, from which customers are benefiting in today’s troubled financ-ial markets through conservative asset management and diversification into gold, a long-recommended investment.

Asset management in volatile marketsThe financial and banking world saw unprecedented upheaval across many different markets in the year under review. The business and market environment was thus extremely troubled, particularly for Portfolio and Asset Management. At 31 December 2008, assets under management totalled EUR 644.6 million. This 27.0% year-on-year decline is due primarily to the effect of falling stock markets.

Leading corporate bank in Vorarlberg

Large growth in customer deposits

Consolidated management report

36 37

MA

NA

GE

ME

NT

RE

PO

RT

FIN

AN

CIA

L S

TAT

EM

EN

TS

(IF

RS

)B

RA

NC

H O

FFIC

ES

/SU

BS

IDIA

RIE

S

Consolidated management report

The impact on Portfolio and Asset Management was partially offset by continued inflows (EUR 25.3 Mio) into quantitative investment strategies. The chart below illustrates the capital-preservation effectiveness of the innovative Hypo Dynamik equity strategy during the year under review.

While the benchmark MSCI World equity index fell by over 40% in 2008, in the same period the Hypo-Welt-depot Dynamik Aktien 90 conservative equity strategy declined only by roughly 10%. This flexible investment concept thus retained most of the gains accumulated

between 2004 and 2007, unlike the MSCI World equity benchmark.

The new Hypo Dynamik Anleihen bond fund also perfor-med outstandingly last year. Returning 4.92% between 1 August 2008 and the year-end (11.8% annualised), this active maturity management strategy, which can generate returns in both rising and falling interest rate environments, substantially exceeded expectations. Despite these considerable asset management achieve-ments however, it remains difficult to generate positive returns across all asset classes. The short-term outlook

remains extremely uncertain. The financial markets and the real economy continued to face major problems. Distressed real estate markets in the US and several European countries, falling energy and commodity prices, and manufacturing overcapacity in particular are serving to accelerate deflationary tendencies. The credit and liquidity situation is still tight on international financial markets. Both private and institutional inve-stors are showing continued restraint.

Portfolio and Asset Management employs effective and dynamic investment strategies. Strict discipline in market and security selection and containing risk and costs remains a high priority. Hypo Vermögens-verwaltung is well-positioned in Vorarlberg, particularly given investors’ renewed interest in a safe haven (ca-pital preservation concepts and international investing standards).

Sole Austrian bank conforming to international asset management performance standardsSince 2005, Hypo Landesbank Vorarlberg has been the only Austrian bank offering asset management certified to comply with international standards. Pricewater-houseCoopers audits our asset management annually for compliance with Global Investment Performance Standards (GIPS®), most recently in March 2009.

The standards are designed to afford customers an objective comparison of investment results. The Bank itself benefits however from GIPS® quality control in investing and risk management processes, which again ultimately benefits the customer.

Treasury/Financial Markets

Treasury activities conducted by Hypo Landesbank Vorarlberg in fiscal year 2008 were substantially af-fected by the turmoil on international financial markets. Like virtually every other bank active in the capital markets, Hypo Landesbank Vorarlberg was confronted with an extremely difficult market environment. Falling bond prices on widening credit spreads weighed on Treasury earnings. However, in contrast to many banks the financial impact on Hypo Landesbank Vorarlberg was only limited, being effectively contained due to the solid, long-term orientation of our business. Our excellent liquidity and long-term funding position are particularly positive factors. The crisis has provided an opportunity to generate considerable investment management returns while maintaining a conservative risk profile. The liquidity buffer built up in 2007 made it possible to take positions in bonds and loans on a selective basis. In the current difficult financial crisis it has become particularly clear that our conservative strategic position and risk policies have had a positive impact; thus even in this difficult economic environment, Hypo Landesbank Vorarlberg is able to produce stable results.

Asset and Liability ManagementIn 2008, assets totalling EUR 1,022 million were purchased for fixed income nostro accounts. At 31 December 2008, bond holdings were valued at a total EUR 3,238 million. Margins increased substantially in fiscal year 2008.

The investment focus in 2008 was on covered bonds and assets of public institutions. Bond issuers from Austria and other European countries comprised the core of a broadly diversified portfolio.

In fixed income markets, the focus was on interest rate hedging and active asset and liability management. Bond yields fell in the second half of the year, followed by money market yields in the fourth quarter. Strategic fixed interest receiver positions were taken over the course of the entire year. In the second half of the year, interest rate risk management was stepped up in the areas of equity and credit, which made a major contribution to stabilising the overall portfolio.

Asset management proves itself with value protection

Accordance with Global Investment Performance Standards (GIPS)® again confirmed

Consolidated management report

01 02 03 04 05 06 07 08 09 10 11 12 01

110

100

90

80

70

60

2008

MSCI World Hypo Dynamik 90

Performance comparison

38 39

MA

NA

GE

ME

NT

RE

PO

RT

FIN

AN

CIA

L S

TAT

EM

EN

TS

(IF

RS

)B

RA

NC

H O

FFIC

ES

/SU

BS

IDIA

RIE

S

Consolidated management report

Asset and Liability Management – FundingThe bank enjoys an excellent liquidity situation thanks to prudent funding policies pursued in 2006 and 2007. As a result, the Bank did not have to secure funding from international capital markets on increasingly expensive terms.

Nine issues were implemented in the course of 2008 (private placements and retail bonds) with a total volume of EUR 195 million. To maintain at adequate capitalisation Hypo Landesbank Vorarlberg also issued upper tier 2 bonds in the amount of EUR 26.5 million.

The international rating agency Moody’s recently reite-rated its very good Aa1 rating. Our rating thus remains excellent even after the discontinuation of the state deficiency guarantee. In future, the covered pool will be increasingly drawn upon for the issuance of mortgage and municipal covered bonds in order to obtain more favourable funding for the Bank.

Nominal derivative volume managed by the Swaps unit increased in 2008 from EUR 9.3 billion to EUR 10.0 billion. This increase was mainly attributable to propri-etary trading in interest rate options and forward rate agreements for interest rate management and hedging of Bank issues. Nominal currency options volume in customer accounts doubled to EUR 211.6 million. A total 437 swap contracts with an approximate nominal volume of EUR 7.9 billion were on the books as of 31 December 2008. The number of new framework and collateral agreements negotiated was lower than in the previous year. However, in the last quarter of the year, a number of novation agreements in connection with bank acquisitions were signed.

Money market, currency and interest rate derivatives tradingThe solid liquidity situation greatly facilitated Hypo Landesbank’s ability to act in the crisis-stricken money markets. The level of cash and equivalents held stabilised at around EUR 1 billion after peaking at the end of the first quarter.