Foreign investment in us real estate august 10 2012 - jg updated

16

FOREIGN INVESTMENT IN U.S. REAL ESTATE Roger Royse Royse Law Firm, PC 1717 Embarcadero Road Palo Alto, CA 94303 [email protected] www.rroyselaw.com Skype: roger.royse IRS Circular 230 Disclosure: To ensure compliance with the requirements imposed by the IRS, we inform you that any tax advice contained in this communication, including any attachment to this communication, is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of (1) avoiding penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to any other person any transaction or matter addressed herein. Commercial REO Brokers Association August 10 th , 2012

-

Upload

roger-royse -

Category

Business

-

view

433 -

download

1

Transcript of Foreign investment in us real estate august 10 2012 - jg updated

FOREIGN INVESTMENT IN U.S. REAL ESTATE

Roger RoyseRoyse Law Firm, PC

1717 Embarcadero RoadPalo Alto, CA 94303

Skype: roger.royse

IRS Circular 230 Disclosure: To ensure compliance with the requirements imposed by the IRS, we inform you that any tax advice contained in this communication, including any attachment to this communication, is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of (1) avoiding penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to any other person any transaction or matter addressed herein.

Commercial REO Brokers

AssociationAugust 10th, 2012

2

OUTLINE

1. Income Tax and Withholding

Obligations

2. Structuring Foreign Investment in U.S. Real Estate

3. Like-Kind Exchange Transactions

4. Estate and Gift Issues

3

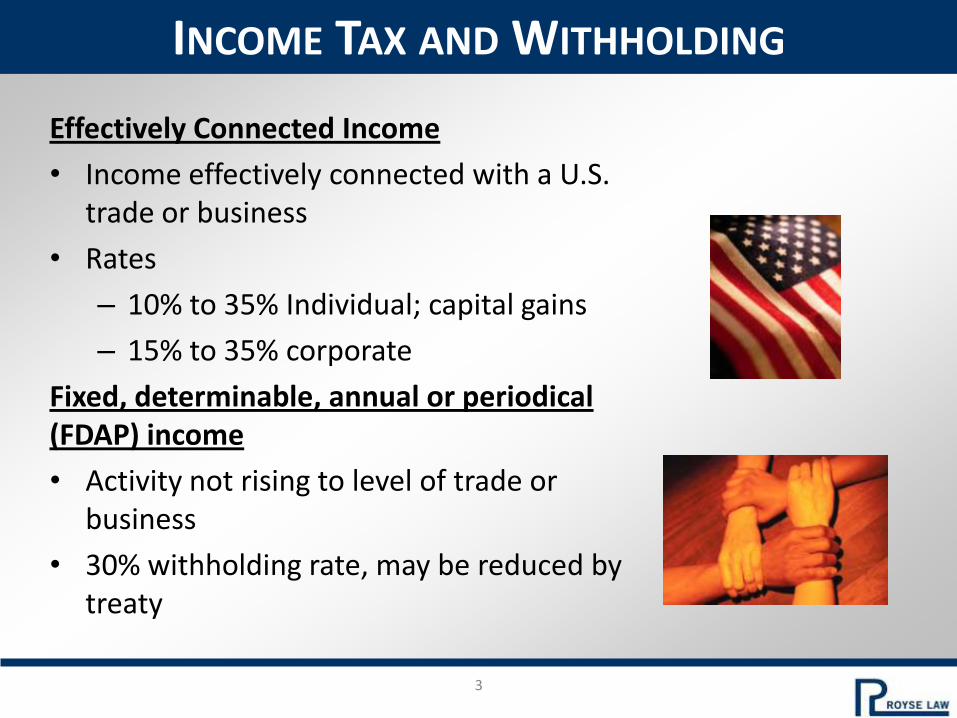

INCOME TAX AND WITHHOLDING

Effectively Connected Income

• Income effectively connected with a U.S. trade or business

• Rates

– 10% to 35% Individual; capital gains

– 15% to 35% corporate

Fixed, determinable, annual or periodical (FDAP) income

• Activity not rising to level of trade or business

• 30% withholding rate, may be reduced by treaty

4

INCOME TAX AND WITHHOLDING

Foreign Investment in Real Property Tax Act of 1980 (FIRPTA)

• 10% gross withholding on dispositions of a U.S. Real Property Interest or U.S. Real Property Holding Corporation (USRPHC)

• Exemptions from withholding– Affidavit of non foreign status– Non recognition transactions

5

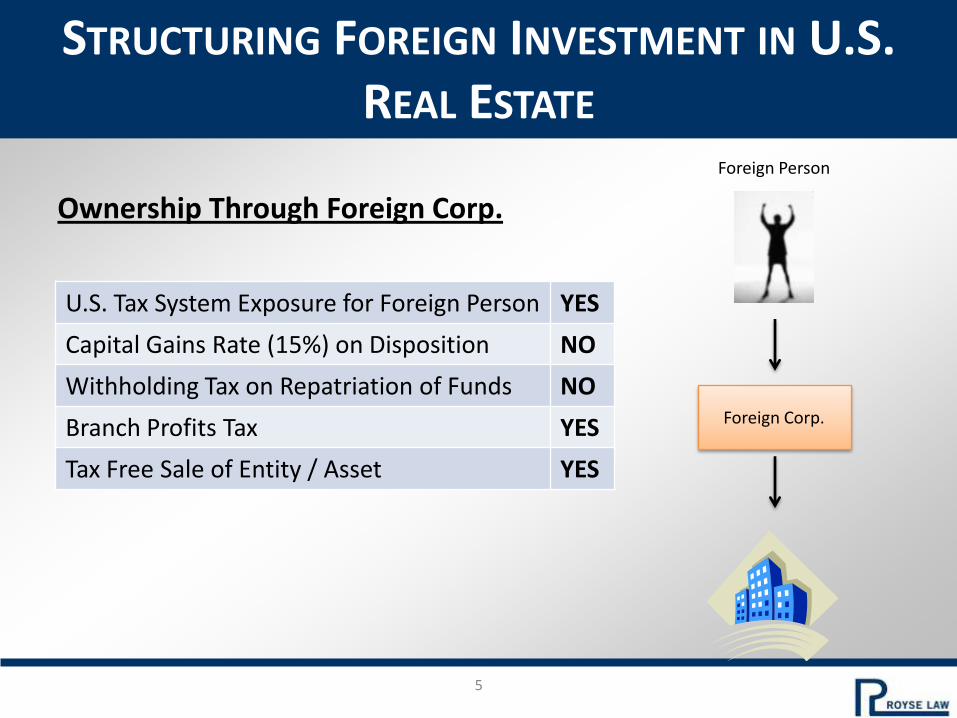

STRUCTURING FOREIGN INVESTMENT IN U.S. REAL ESTATE

Ownership Through Foreign Corp.

Foreign Person

Foreign Corp.

U.S. Tax System Exposure for Foreign Person YES

Capital Gains Rate (15%) on Disposition NO

Withholding Tax on Repatriation of Funds NO

Branch Profits Tax YES

Tax Free Sale of Entity / Asset YES

6

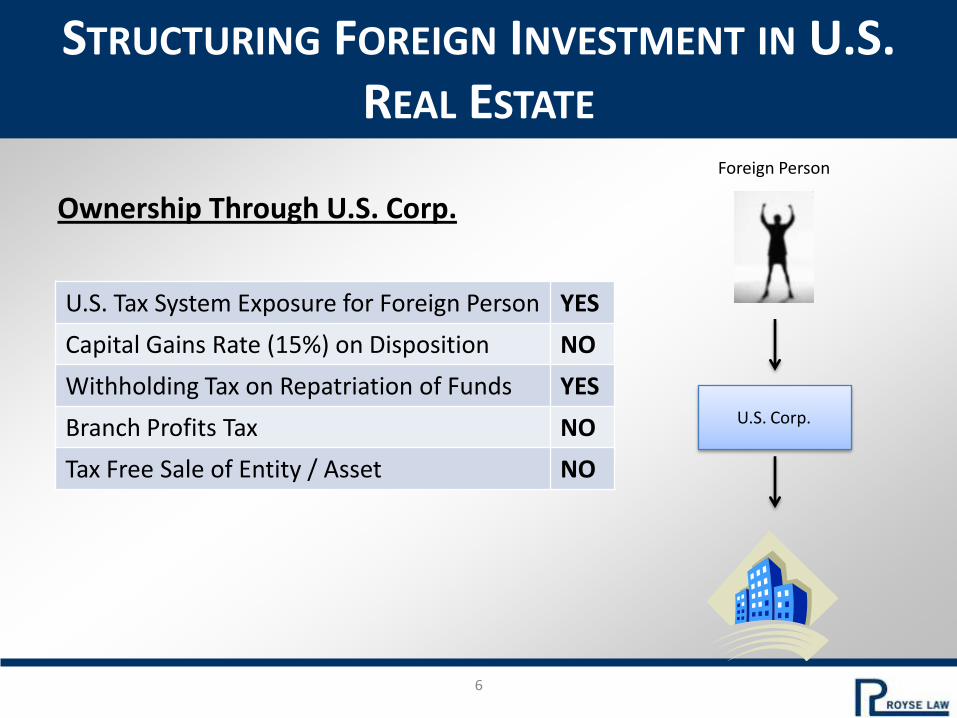

STRUCTURING FOREIGN INVESTMENT IN U.S. REAL ESTATE

Ownership Through U.S. Corp.

Foreign Person

U.S. Corp.

U.S. Tax System Exposure for Foreign Person YES

Capital Gains Rate (15%) on Disposition NO

Withholding Tax on Repatriation of Funds YES

Branch Profits Tax NO

Tax Free Sale of Entity / Asset NO

7

STRUCTURING FOREIGN INVESTMENT IN U.S. REAL ESTATE

Foreign Person

Foreign Corp.

U.S. Corp.

U.S. Tax System Exposure for Foreign Person NO

Capital Gains Rate (15%) on Disposition NO

Withholding Tax on Repatriation of Funds NO

Branch Profits Tax NO

Tax Free Sale of Entity / Asset YES

Ownership Through Foreign Corp. and U.S. Corp.

8

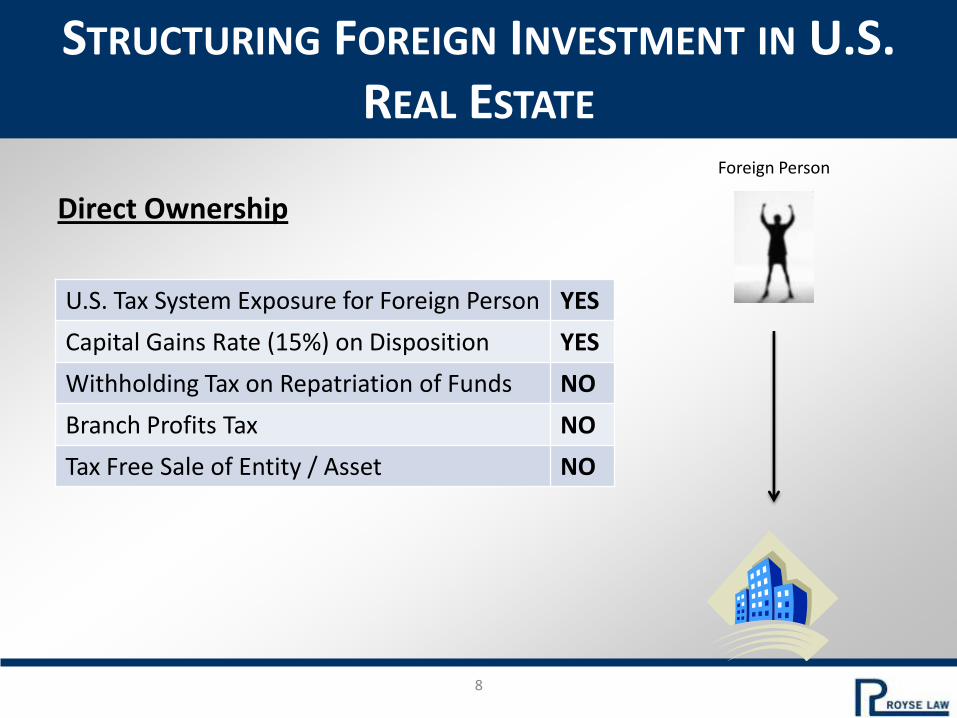

STRUCTURING FOREIGN INVESTMENT IN U.S. REAL ESTATE

Foreign Person

U.S. Tax System Exposure for Foreign Person YES

Capital Gains Rate (15%) on Disposition YES

Withholding Tax on Repatriation of Funds NO

Branch Profits Tax NO

Tax Free Sale of Entity / Asset NO

Direct Ownership

9

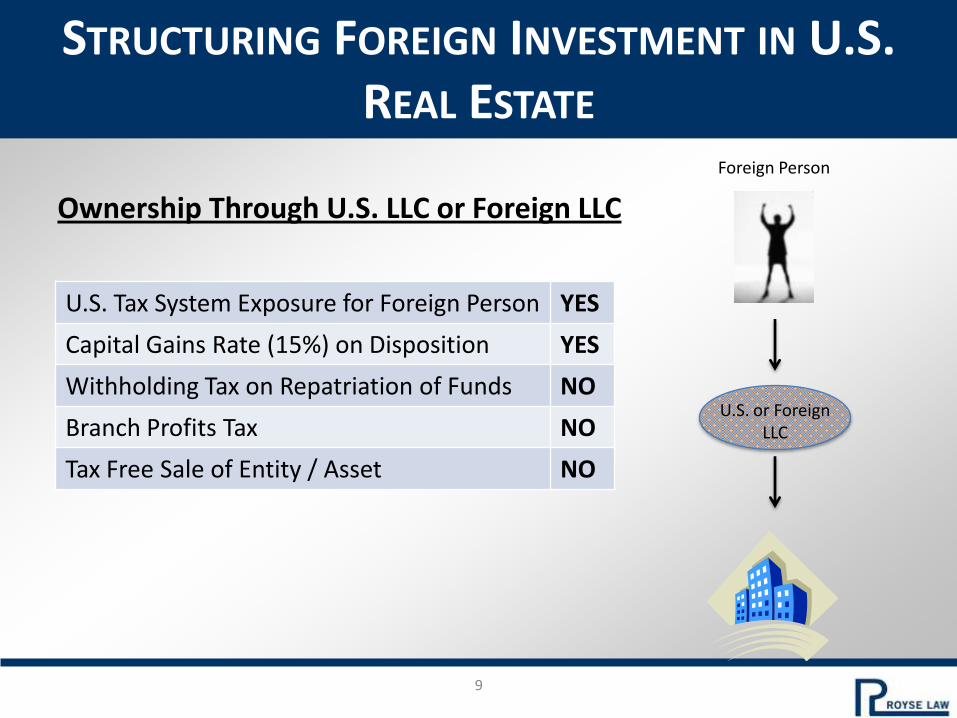

STRUCTURING FOREIGN INVESTMENT IN U.S. REAL ESTATE

Ownership Through U.S. LLC or Foreign LLC

Foreign Person

U.S. or Foreign LLC

U.S. Tax System Exposure for Foreign Person YES

Capital Gains Rate (15%) on Disposition YES

Withholding Tax on Repatriation of Funds NO

Branch Profits Tax NO

Tax Free Sale of Entity / Asset NO

10

LIKE-KIND EXCHANGE TRANSACTIONS

• Section 1031 like-kind exchange transactions

– Permits tax deferral

– U.S. property is only “like-kind” to other U.S. property, and foreign property is only “like-kind” to other foreign property

11

ESTATE AND GIFT TAX RATES

NON-U.S. DOMICILED NON-CITIZENS

Applicable to U.S. Situs Property

But, what about gifts or bequests to a

non-citizen spouse?

12

ESTATE AND GIFT TAX RATES

Applicable to U.S. Citizens or Domiciliaries:

13

INBOUND GIFT OR INHERITANCE

ASSET TRANSFER ISSUES

• Intangible Assets– Stocks, LLC & LP interests, patents, copyrights, etc.

– General rule—intangibles are located where the giver is located.

• Tangible Assets– Real estate, equipment, automobiles, jewelry, artwork, etc.

– General Rule—tangible assets have situs where they are physically located.

• But, what about cash, currency, bank accounts, etc.?

14

COMMON ESTATE PLANNING ISSUES FOR

CROSS-BORDER FAMILIES

• Inbound Cash Transfers– Gifts?

– Loans?

– Investments?

• Transfers of Stock/LLC interests?– U.S. Stock?

– Foreign Stock?

• Foreign Trustees & Successor Trustees– U.S. person is often preferable.

• U.S. income tax issues.

• U.S. reporting issues

• Logistics

Foreign Parent

U.S. Child

Gift or Loan $

Purchase $

$ Investment

$ Purchase

Investment

Entity(Corp. LLC, et al)

$ Rent

Lease

Gift of

Stock

32

16

PALO ALTO1717 Embarcadero Road

Palo Alto, CA 94303

LOS ANGELES11150 Santa Monica Blvd.,

Suite 1200Los Angeles, CA 90025

SAN FRANCISCO135 Main Street,

12th FloorSan Francisco, CA 94105

![sax quartet JG rgenic 2] CD Vol.02 Silver ! : JG sax JG ...](https://static.fdocuments.net/doc/165x107/6156fc9aa097e25c764fc051/sax-quartet-jg-rgenic-2-cd-vol02-silver-jg-sax-jg-.jpg)