for the year ended 31 March 2018

34

23 July 2018 This presentation is available at www.eskom.co.za/IR2018 Eskom group annual results for the year ended 31 March 2018

Transcript of for the year ended 31 March 2018

23 July 2018 This presentation is available at www.eskom.co.za/IR2018

Eskom group annual results for the year ended 31 March 2018

Contents

From “business as usual” to

“transition towards

sustainability”

Key priorities to position

Eskom for growth

Conclusion

Operational performance

Financial performance

From “business as usual” to

“transition towards sustainability”

• Eskom has experienced difficult years following leadership and governance

instability

• A new board and leadership team was appointed to clean up, stabilise,

and set Eskom up for future growth

• Despite experiencing a difficult year:

o Improved liquidity

o Continued improvement in operational performance

o Advancement in governance and control systems

• A strategic review is being undertaken in partnership with the shareholder

to build the Eskom of the future

3

There will be pressure until FY2020, as we transition towards financial and

operational sustainability, requiring resolute, tough and decisive leadership

Stabilisation for transition to a sustainable future

Pre-January 2018: business as usual

• Lack of long-term integrated strategy

• Skewed towards compliance, minimum

strategic engagement

• Compounding this is poor performance

o Qualified audit opinion

o Allegations of corruption and

mismanagement

o Governance challenges

o Negative investor sentiment

• Procrastination on decisions and actions

by all stakeholders

• Leadership instability

o 10 CEOs in 10 years

o 6 Boards in 10 years

New Minister of Public Enterprises in 2018 emphasised the importance of alignment of

the shareholder compact, Corporate Plan and business strategy

• Dislocation between operations and

government expectations (statement of

intent, corporate plans & shareholder

compacts)

“The overall financial performance of the

business had been good, with the Design-

to-Cost strategy showing positive results

as reflected by an increase in revenue…”

Minister of Public Enterprises, June

2017

4

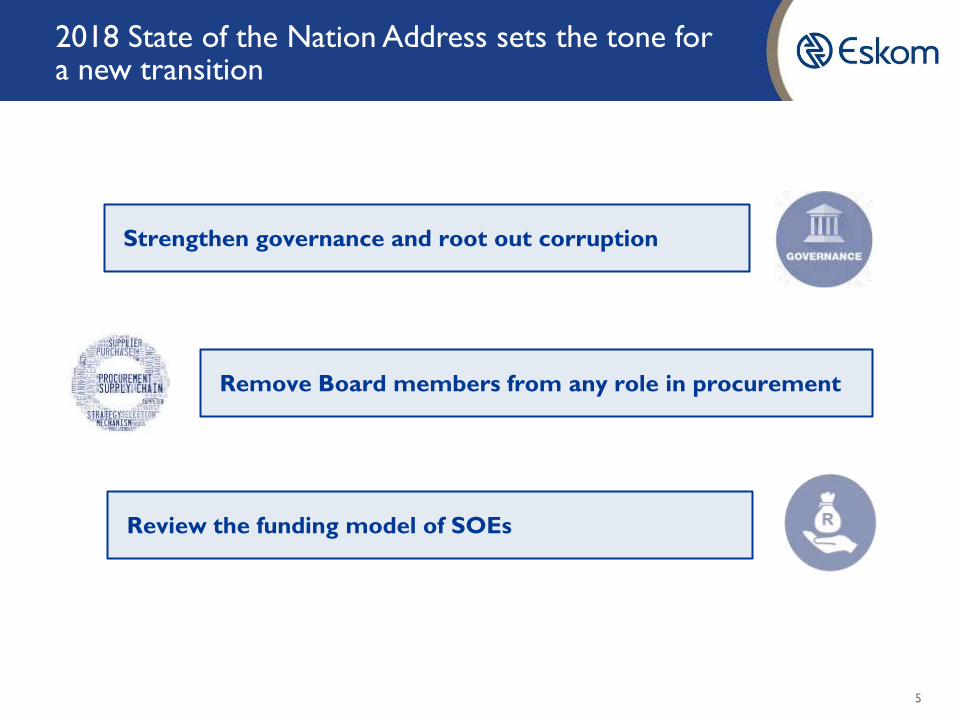

From “business as usual” to “transition towards sustainability”

Strengthen governance and root out corruption

5

2018 State of the Nation Address sets the tone for a new transition

Review the funding model of SOEs

Remove Board members from any role in procurement

January 2018: Eskom

transition

• Appointment of new

Board

• Immediate Board focus:

1. Clean up

2. Stabilisation

• Transition from

“business as usual” to

the Eskom of the future

• Noting Eskom’s size,

challenges, complexity

and role in the

economy, the Board

approved a three-

person top team

comprising a GCE,

CFO and COO

Key decisions by the Board

Governance

Corporate

Plan

Financial

sustainability

• Committed to the highest level of governance

• Reviewing the purpose, mandate and powers of all

sub-committees

• Decision making by board sub-committees

temporarily elevated to the board

• Concerns raised regarding 2017 Corporate Plan

o Debt to increase from R387 billion to

R600 billion within four years

o Gearing increasing from 72% to 80%

• Permission from the shareholder to submit a

one-year plan

• Emphasis to be placed on maximising revenue and

containing costs

• Challenge NERSA decision in court – 2018/19

tariff increase insufficient

6

Transition from “business as usual” approach towards sustainability

Key priorities to position

Eskom for growth

Clean up

Reposition Eskom as the most trusted state-owned entity

• Instill transparent and effective governance

• Initiative to address qualified audit identified more irregular expenses

Improve financial health

• 21% increase in EBITDA from R37.5 billion in FY2017 to R45.4 billion in

FY2018

• RCA determination of R32.7 billion

• Improved liquidity by raising R57 billion since January 2018

• Capex and opex reduction to achieve financial viability

Future Eskom

to grow the

business

Stabilise

Efficiency

optimisation

Prepare for growth - New initiatives to increase EBITDA

• Target 500MW additional demand

• Reduce arrear debt

• Manage risk of increasing coal costs

• Optimise staff productivity levels

Become an innovative and data-driven utility

• Grow new markets and products while retaining and growing existing clients

• Achieve long-term sustainability and developmental mandate

• Sustainable business model for Eskom

8

Driving key priorities to position Eskom for growth

10 implicated senior executives exited. Finalisation of outstanding disciplinary hearings relating to senior executives being accelerated

11 criminal cases opened, five of which involve nine senior executives

Total of 1 049 outstanding disciplinary cases since April 2018, of which 628 have been finalised, resulting in 75 employee exits

239 whistle-blowing cases investigated, 122 of which have been concluded. Disciplinary process is under way in respect of 67 confirmed cases

Remedial action has been taken against 25 staff doing business with Eskom; 7 exited

Lifestyle audits of senior management in progress. There is effective declaration of interest

Investigated all irregular supplier contracts (so far five no longer doing business with Eskom – the amount spent with these companies in the past three years was R2.3 billion). Recovered R902 million from McKinsey; pursuing interest recovery

Cooperating with eight regulatory bodies conducting major investigations 1

1. National Treasury procurement investigations, Zondo Commission, Hawks, SIU, Parliamentary Inquiry, National Director of Public Prosecutions, Standing

Committee on Public Accounts and SAPS

CLEAN UP: GOVERNANCE

9

Significant progress towards becoming a trusted SOC

Improved liquidity Financial viability

• Raised R57 billion since January 2018

• Raised 22% to date of R72 billion borrowing

requirement for 2018/19

• Firm commitment to increase funding to

62% of 2018/19 borrowing requirement

• Discussion with lender at advance stage; will

increase funding to more than 80% of

2018/19 borrowing requirement

• In addition, firm commitment to secure

34% of R56 billion funding for 2019/20

borrowing requirement

• Growing investor appetite for Eskom bonds

Reprioritise capex

• Restricted capex to R45 billion over the

next five years, a saving of R55 billion

• Risks and tradeoffs have been identified

to mitigate against impact of capex

reduction

Reduced opex

• Restrict total operating cost to below

inflation, releasing efficiencies of

R11 billion per annum

• Kept maintenance at current levels

However this is not sufficient, and tough decisions are required

Initiatives identified to increase EBITDA margin to 35% by optimising capex, opex and

maintenance, while improving productivity and efficiency

10

STABILISE LIQUIDITY

Efforts are improving liquidity and financial viability to achieve positive shift in investor confidence

Grow sales

• Stimulate sales by developing new products and services and optimising tariffs

• Confirmed 3.5 TWh sales growth initiatives, resulting in R2.9 billion additional revenue over two years, with nine deals signed

• Target revenue recovery of R600 million per annum

• Accelerate customer connections

• Intensify credit management

• Collect additional R1 billion per annum from municipalities

• Together with Government, seek solutions to solve municipal arrear debt

• Installation of prepaid meters to continue

Manage risk of increasing coal costs

• Prioritisation of capex investments into cost-plus mines

• Optimisation of logistics costs, including migration from road to rail

• Collaboration with state-owned mining company

Reduce arrear debt

Optimise productivity levels

• Holistic review and robust stakeholder discussions to identify optimal productivity improvement solutions

11

EFFICIENCY OPTIMISATION

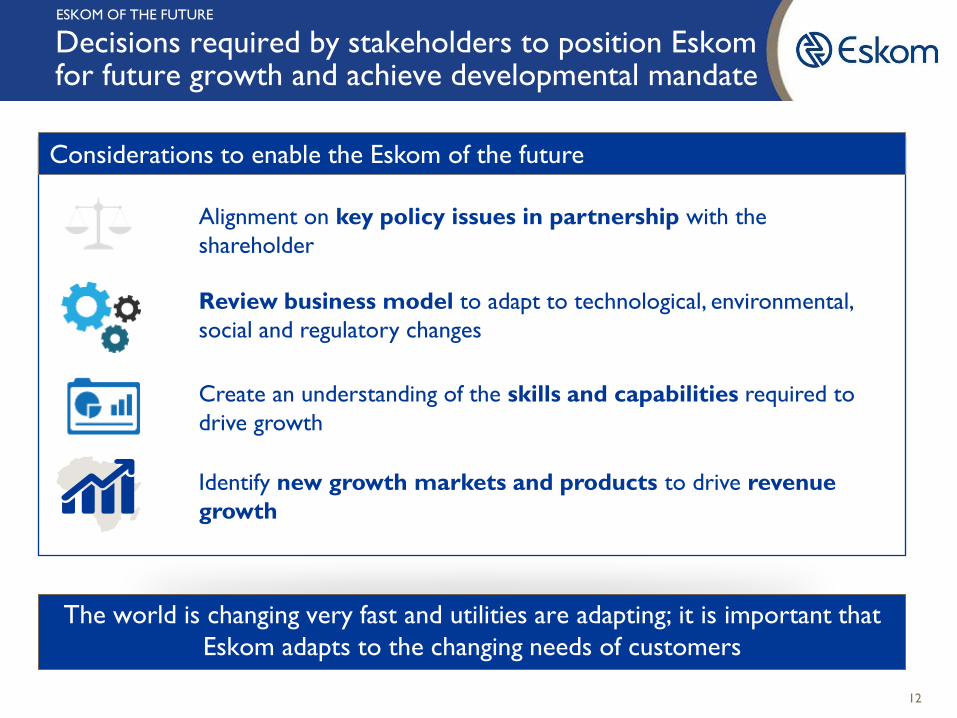

Key initiatives to drive growth and efficiency

Review business model to adapt to technological, environmental,

social and regulatory changes

Alignment on key policy issues in partnership with the

shareholder

Considerations to enable the Eskom of the future

Create an understanding of the skills and capabilities required to

drive growth

Identify new growth markets and products to drive revenue

growth

The world is changing very fast and utilities are adapting; it is important that

Eskom adapts to the changing needs of customers

12

ESKOM OF THE FUTURE

Decisions required by stakeholders to position Eskom for future growth and achieve developmental mandate

Operational performance

• Generation plant availability improved from 77.3%

to 78%

• Significant improvement in environmental

performance:

o Particulate emissions from 0.30 to

0.27kg/MWhSO

o Water usage from 1.42 to 1.30l/kWhSO

• Transmission achieved best performance in 10

years: system minutes lost improved from 3.8 to 2.1

• Distribution network improvement

o (SAIFI1) improved from 18.9 to 18.7 events

o (SAIDI2) improved from 38.9 to 38.8 hours

• Reviewed Medupi and Kusile dates

o Three units of Medupi and one unit of Kusile in

commercial operation, with combined installed

capacity of 3 181MW

• 2 510MVA transformer capacity installed; 722km of

high-voltage transmission lines commissioned

15

20

25

30

35

40

45

1.5

2.0

2.5

3.0

3.5

4.0

2016 2015 2014 2017 2013 2018

SAIFI

SAIDI System minutes lost for events < 1 minute

7877

71

7475

78 78

75

83838482

65

70

75

80

85

2017 2018 2013 2015 2014 2016

EUF % EAF %

Plant availability & utilisation

Network performance

%

Minutes Events/hours

1. System average interruption frequency index 2. System average interruption duration index 14

Operational performance continues to improve

• 215 519 households connected (2017:

207 436)

• More than one million households

connected since 2013

• Lost-time injury rate improved to 0.23

(2017: 0.39), the best since 2008

• Regrettably, Eskom suffered three

employee fatalities (2017: four) and 12

contractor fatalities (2017: six)

• B-BBEE attributable spend of 80%

• Spend with black-owned suppliers of 45%

• Employment of female employees in senior

management positions 38% (2017: 37%)

• Coal stock remains a focus area to achieve

adequate levels

200

100

180

120

140

220

160

1 000

0

800

1 200

200

400

600

2018 2017 2016 2015 2014 2013

Cummulative Annual

Electrification

Number 000 Number 000

15

Operational performance continues to improve

Financial performance

Overview of financial performance

17

• EBITDA of R45.4 billion (2017: R37.5 billion)

• Net loss after tax of R2.3 billion

(2017: R0.9 billion profit)

• Net cash from operations of

R37.6 billion (2017: R45.8 billion)

• Liquid assets of R22.3 billion

(2017: R32.5 billion)

• 22% of funding requirement for 2018/19

secured to date

• Modified audit opinion

Public Finance

Management Act, 1999

International Financial

Reporting Standards

State-owned company

• An external auditor expresses an

opinion about the fairness of the

financial position and financial

performance of an entity:

• Unmodified: a true and fair view of the

entity’s operations

• Modified

o Qualified: auditors take exception to a

certain accounting application

o Adverse: a conflict between the auditor

and entity

o Disclaimer: no opinion due to

limitations by the entity

The purpose of the PFMA is to regulate

financial management of expenditure, and

ensure assets and liabilities of entities are

managed efficiently and effectively

• Irregular expenditure: expenditure other

than unauthorised expenditure, incurred in

contravention of or that is not in

accordance with a requirement of any

applicable legislation or policy

• Fruitless and wasteful expenditure:

expenditure which was made in vain and

would have been avoided had reasonable

care been exercised

18

Eskom complies with IFRS and PFMA reporting

requirements and is audited on that basis

March 2017

September 2017

(interim review) March 2018

IFRS

Going concern

PFMA n/a

Independent auditors’ opinions

Modified

(1) Prior year restatement due to non-accounting for assets built by customers

(2) Uncertainty that may cast significant doubt on the group’s ability to continue

as a going concern (similar to emphasis of matter)

(3) Incomplete reporting of irregular expenditure

(4) No reporting requirement at half-year

(5) Incomplete reporting of irregular expenditure, fruitless and wasteful

expenditure and losses due to criminal conduct

(2)

(4) Unmodified

Emphasis of matter (2)

(3) (5)

(1)

19

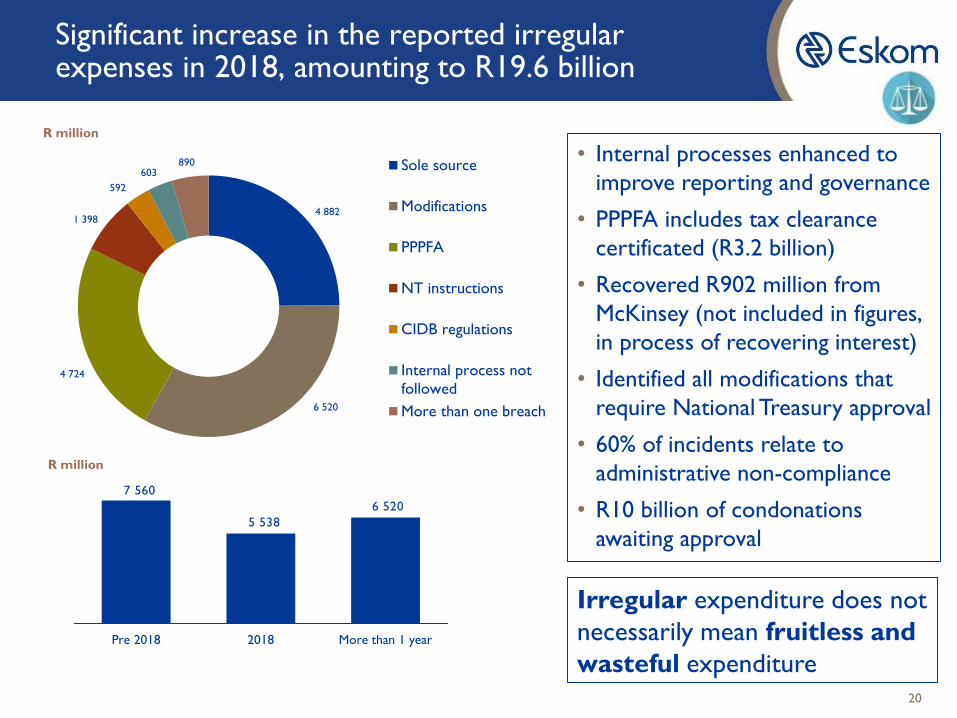

Significant increase in the reported irregular expenses in 2018, amounting to R19.6 billion

4 882

6 520

4 724

1 398

592

603 890 Sole source

Modifications

PPPFA

NT instructions

CIDB regulations

Internal process not

followed

More than one breach

R million

R million

• Internal processes enhanced to

improve reporting and governance

• PPPFA includes tax clearance

certificated (R3.2 billion)

• Recovered R902 million from

McKinsey (not included in figures,

in process of recovering interest)

• Identified all modifications that

require National Treasury approval

• 60% of incidents relate to

administrative non-compliance

• R10 billion of condonations

awaiting approval

6 520

5 538

7 560

Pre 2018 2018 More than 1 year

Irregular expenditure does not

necessarily mean fruitless and

wasteful expenditure 20

R billion

March

2018

March

2017

YoY %

change

Revenue 177 177 –

Other income 1 2 (13)

Primary energy (85) (83) (3)

Net employee benefit expenses (29) (33) 11

Net impairment loss (1) (2) 67

Other expenses (18) (24) 23

EBITDA (Profit before depreciation

and amortisation and net fair value loss) 45 38 21

Depreciation and amortisation

expenses (23) (20) (14)

Net fair value loss on financial

instruments and embedded

derivatives

(2) (2) (3)

Net finance cost

(23) (14) (61)

(Loss)/profit before tax (3) 1

Income tax – –

Net (loss)/profit for the year (2) 1

21

• Sales down by 0.9%;

revenue up by 0.8%

• Primary energy cost

contained

• Employee benefit costs and

operating expenses lower

due to decrease in

provisions

• Depreciation growth due

to commissioning of new

assets and power station

units

• Finance costs linked to less

costs capitalised and

growth in borrowings

Income statement for the year ended 31 March 2018

R billion March 2018

March 2017

YoY % change

Property, plant and equipment and intangible assets 635 593 7

Working capital 46 44 14

Liquid assets 23 33 (31)

Other assets 36 41 (5)

Total assets 739 710 4

Equity 170 176 (4)

Debt securities and borrowings 389 355 9

Working capital 44 52 (15)

Other liabilities 136 127 8

Total equity and liabilities 739 710 4

Financial position at 31 March

22

23

R billion

March

2018

March

2017

YoY %

change

Net cash from operating activities 38 46 (18)

Cash required for debt servicing (44) (36) (22)

Net cash movement before investment activities (7) 10

Cash flow used in investment activities (55) (62) 11

Cash flow from financing activities 58 44 32

Net decrease in cash and cash equivalents (4) (8)

1.0

Provisions Advance receipts

/ payments

EBITDA

2.0

45.4

0.6

Derivative

instruments

1.7

2.4

Cash from

operations

Working capital

37.6

Other

Cash flow statement for the year ended 31 March 2018

Ratio March

2018

March

2017

EBITDA margin, % 25.9 21.4

Cash interest cover, ratio 1.22 1.73

Debt service cover, ratio 0.87 1.37

Gross debt/EBITDA, ratio 9.71 10.84

Debt/equity (including long-

term provisions), ratio 2.52 2.11

Gearing, % 72 68

Free funds from operations as

% of gross debt, % 1 9.09 11.69

Free funds from operations as

% of total capex, % 1 77.84 75.11

1. Shareholder compact definition

12

14

16

18

20

22

24

26

25

20

15

35

45

10

5

0

-5

40

30

50

2018 2017 2016 2015 2014 2013

Net profit after tax (Rbn)

EBITDA (Rbn)

EBITDA margin (%)

Profitability

50

52

54

56

58

60

62

64

66

68

70

72

1,6

1,2

1,8

2,4

2,2

2,0

2,6

1,4

1,0

2018 2016 2017 2015 2014 2013

Gearing

Debt/equity

Solvency

24

Most financial ratios deteriorated and are expected to deteriorate further before improving

Overview of capital expenditure

25

Total Eskom funded capital expenditure

R billion

• Total Eskom group funded capital

of R47 billion (2017: R56 billion)

with R28 billion used to expand

the asset base and R17 billion

spent on existing assets

• Department of Energy funded

electrification capex of

R3.4 billion (not included in

graph)

2837

30 31 3428

30

1820

19

17

29

0

10

20

30

40

50

60

70

1

2017

2

2016

2

2015 2018

0

2014

3

2013

2

New asset base (Rbn)

Existing asset base (Rbn)

Other (Rbn)

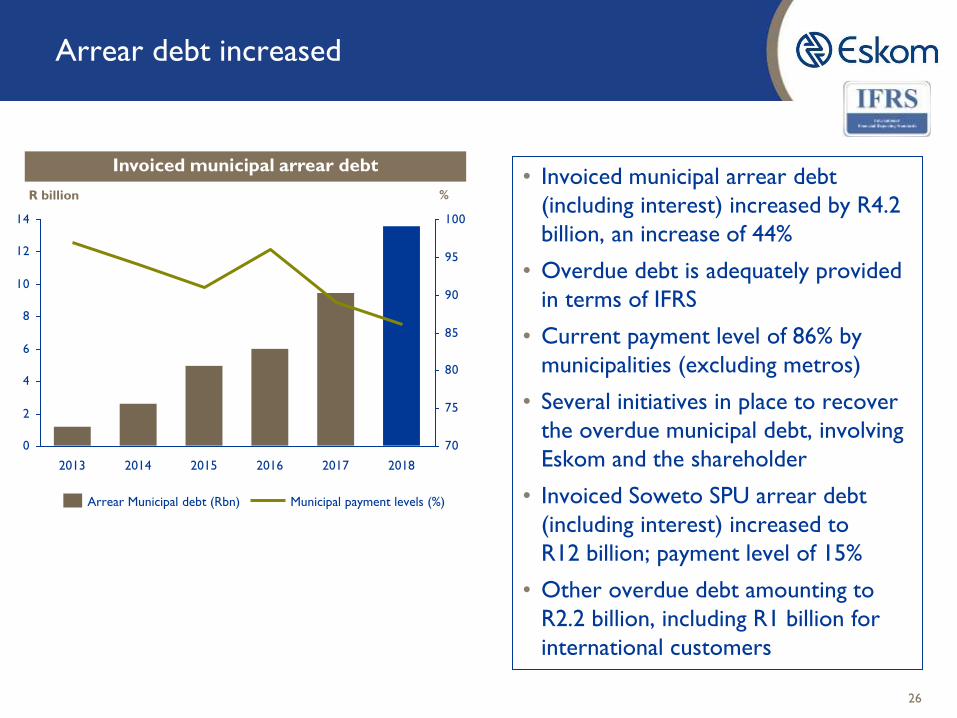

• Invoiced municipal arrear debt

(including interest) increased by R4.2

billion, an increase of 44%

• Overdue debt is adequately provided

in terms of IFRS

• Current payment level of 86% by

municipalities (excluding metros)

• Several initiatives in place to recover

the overdue municipal debt, involving

Eskom and the shareholder

• Invoiced Soweto SPU arrear debt

(including interest) increased to

R12 billion; payment level of 15%

• Other overdue debt amounting to

R2.2 billion, including R1 billion for

international customers

Arrear debt increased

Invoiced municipal arrear debt

0

2

4

6

8

10

12

14

70

75

80

85

90

95

100

2018 2017 2016 2015 2014 2013

Municipal payment levels (%) Arrear Municipal debt (Rbn)

R billion %

26

• The external auditors raised an emphasis of matter on Eskom’s status

as a going concern in their review for the six months ended

30 September 2017

• The steps taken by the shareholder and the Board boosted investor

confidence, and the liquidity position improved since January 2018

• Eskom continues to face significant financial and liquidity challenges in

the short to medium term, mainly due to the high debt burden, low

sales growth and increased finance costs

• Eskom is awaiting the outcomes of the liquidation of the R32.7 billion

RCA balance and the MYPD 4 decision, which influences future

revenue streams

• The auditors raised uncertainty that may cast significant doubt on the

group’s ability to continue as a going concern

Liquidity and going concern

27

28

17

75

350

58

275

Remaining Unallocated

portion

Under

negotiation

Portion

allocated

Total

Government

Guarantee

R billion

Guarantee utilisation allocation

20

6

12

27

2019 2020 2022 2021

Nominal maturities of guaranteed debt

R billion

• Eskom successfully raised R57 billion for the

year ended 31 March 2018

• R43 billion of this was raised between

January and March 2018

R billion

Funding

plan Committed

DFIs 15.3 8.8

ECAs 5.8 1.0

International bonds 20.0 –

Domestic bonds and

notes > 1 year 13.0 5.5

Domestic bonds and

notes < 1 year 10.0 0.8

Structured products 8.0 –

Total funding 72.1 16.1

% secured 22%

Eskom has secured 22% of funding for 2018/19 financial year to date

Summary of financial performance

29

• Liquidity position improved since January 2018

• Improved investor sentiment

• EBITDA and EBITDA margin % increased

• However, reported a net loss due to increased

depreciation and finance costs

• Reduced cash from operations

• Most financial ratios deteriorated and are expected

to deteriorate further, before stabilising and

improving

• Additional work is required to ensure continued

and enhanced PFMA reporting

• Financial performance needs to improve to ensure

financial sustainability

Conclusion

• Liquidity improved, operational performance continues to improve

• We are committed to turning around this institution

• Need for alignment between the shareholder compact, Corporate Plan and business

operations

• Shareholder support for Board and management

• The transition towards financial and operational sustainability requires resolute,

tough and decisive leadership

• A strategic review is being undertaken to re-energise, shift direction and set a firm

foundation for Eskom’s growth:

o Strengthening Eskom’s financial position and balance sheet

o Reviewing the business model to respond to global energy industry changes

o Growing the business into new markets and products

o Improving trust and restoring labour, investor and stakeholder confidence

o Reviewing the IPP and coal strategy

31

Eskom is transitioning towards sustainability

Eskom Contractor

Academy Top three position in the 2017

community upliftment category

Awarded the 2017

Technology Transfer Award

for research conducted on

the 765kV insulator project

Most attractive key

occupation (electrical

engineers) from engineering

professionals

The Foundation, with the

University of Limpopo, won

the Africa Gold Award and

Overall Global Thematic

Award in Norway, for

entrepreneurship and for

enterprise skills development

National and international recognition for best performance

32

This presentation does not constitute or form part of and should not be construed as, an offer to sell, or the solicitation or

invitation of any offer to buy or subscribe for or underwrite or otherwise acquire, securities of Eskom Holdings SOC Ltd

(Eskom), any holding company or any of its subsidiaries in any jurisdiction or any other person, nor an inducement to enter

into any investment activity. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied

on in connection with, any contract or commitment or investment decision whatsoever. This presentation does not constitute a

recommendation regarding any securities of Eskom or any other person.

Certain statements in this presentation regarding Eskom’s business operations may constitute “forward looking statements”. All

statements other than statements of historical fact included in this presentation, including, without limitation, those regarding

the financial position, business strategy, management plans and objectives for future operations of Eskom are forward looking

statements.

Forward-looking statements are not intended to be a guarantee of future results, but instead constitute Eskom’s current

expectations based on reasonable assumptions. Forecasted financial information is based on certain material assumptions. These

assumptions include, but are not limited to continued normal levels of operating performance and electricity demand in the

Customer Services, Distribution and Transmission divisions and operational performance in the Generation and Primary Energy

divisions consistent with historical levels, and incremental capacity additions through the Group Capital division at investment

levels and rates of return consistent with prior experience, as well as achievements of planned productivity improvements

throughout the business activities.

Actual results could differ materially from those projected in any forward-looking statements due to risks, uncertainties and

other factors. Eskom neither intends to nor assumes any obligation to update or revise any forward-looking statements,

whether as a result of new information, future events or otherwise.

In preparation of this document certain publicly available data was used. While the sources used are generally regarded as

reliable the content has not been verified. Eskom does not accept any responsibility for using any such information.

Disclaimer

33