![[MS-PPPI]: PPP Over IrDA Dialup Protocol](https://static.fdocuments.net/doc/165x107/61a409ba0dc068626e4d892d/ms-pppi-ppp-over-irda-dialup-protocol.jpg)

For personal use only - ASX · Investor Presentation May 2008 3 Westnet Financials* 56% 6% 2% 18%...

20

1 Investor Presentation May 2008 Westnet Acquisition Investor Presentation 6 th - 8 th May 2008 For personal use only

Transcript of For personal use only - ASX · Investor Presentation May 2008 3 Westnet Financials* 56% 6% 2% 18%...

1 Investor Presentation May 2008

Westnet Acquisition Investor Presentation 6th - 8th May 2008

For

per

sona

l use

onl

y

2 Investor Presentation May 2008

Deal Parameters

Consideration of $81 million to acquire all the shares in Westnet for 100% cash settlement on 18 May 2008

$41 million placement – supported by major shareholders (Amcom Telecommunications Limited and AAPT)

Balance from cash and $50 million undrawn debt facility

Retention of existing staff and management team

Acquisition of Westnet

Clear Rationale for Acquisition

Accretive transaction pre synergies

Opportunity to leverage iiNet scale and infrastruture

Cements position as 3rd Largest ISP in Australia and clear leader in WA

Acquisition of best-in-class service and organic sales capabilities

Complementary metro and regional customer bases

For

per

sona

l use

onl

y

3 Investor Presentation May 2008

Westnet Financials*

56%

6%

2%

18%

13% 5%

Revenue by Product

ADSL

Dialup

Corporate

Telephony

Satellite

Other

Other key metrics (1)

Historic Capex of $2-3m p.a. on IT & property infrastructure

Property, Plant and Equipment of $7.0m as at 31 March 2008

No debt & cash of $2.0m as at 31 March 2008

Source: Westnet management accounts

Source: Westnet financial and management accounts For

per

sona

l use

onl

y

4 Investor Presentation May 2008

Attractive Acquisition Multiple

For

per

sona

l use

onl

y

5 Investor Presentation May 2008

Westnet Background

Specific

More than 10% WA market share

Predominantly wholesaling Telstra and Optus

Significant regional presence – 40% Metro / 60% Regional

Consistent winner of best-in-class ISP service awards

1,000 strong national reseller network

General

Perth based ISP, established in 1994

6th largest ISP in Australia – one of the last significant subscriber bases in Australia without network

100% privately owned – 4 equal main shareholders

Well established and respected leadership team

For

per

sona

l use

onl

y

6 Investor Presentation May 2008

Westnet Subscribers

Other key metrics

ADSL ARPU consistent with iiNet – $51 per subscriber per month

Very low churn / loyal customer base – ADSL averaging 1.3% per month

Strong historical growth – 23k net increase in ADSL customers in 2007

Dial Migration – 1/3 of customers leaving dial being successfully converted to ADSL

Source: Westnet management accounts

For

per

sona

l use

onl

y

7 Investor Presentation May 2008

Combined Scale

50%

19%

15%

11%

3% 2%

Revenue by State

WA

QLD

NSW

VIC

SA / NT

Other

Combined revenues of c$375 million and significant scale

Source: iiNet and Westnet management accounts Sources iiNet management accounts as at 30 April 2008 Westnet management accounts as at 31 March 2008 F

or p

erso

nal u

se o

nly

8 Investor Presentation May 2008

Clear No 3 in Australia

0

500

1,000

1,500

2,000

2,500

3,000 Top ISPs by Broadband Subscriber Numbers (000’s)

*All competitor subscriber numbers estimates as at Dec 2007. IIN+Westnet as at 31 Mar 2008

...and the market leader in Western Australia

For

per

sona

l use

onl

y

9 Investor Presentation May 2008

iiNet

Proven infrastructure leverage

Largely fixed cost network/bandwidth

Innovative ADSL2+ & Naked DSL

VoIP

Strong metro presence & Brand

Advanced business products

Westnet

Strong regional presence & Brand

Loyal growing customer base & low churn

High performing reseller channel

Great hosting platforms

Wholesale b2b capable

Solid gaming presence

Logical fit

Cultural focus on plain-talking genuine service

For

per

sona

l use

onl

y

10 Investor Presentation May 2008

Deal Synergies

Significant value from the acquisition of Westnet is flowing from expected synergies

Synergies

Substantial synergies from scale benefits of iiNet infrastructure and improved costs from Telstra Wholesale

Reduced transmission costs through the use of iiNet’s infrastructure

Significant bandwidth savings via agreements with Pipe Networks

Excludes synergy opportunities from supplier integration and other operating costs

For

per

sona

l use

onl

y

11 Investor Presentation May 2008

Integration Strategy

A simple integration

• Operate Westnet independently and continue to grow the Westnet brand & customer base

• Unique culture and service focus, critical to retain Westnet management and staff

• Joint management to identify opportunities to leverage iiNet infrastructure and combined scale

• No legacy networks and existing billing platform is both robust and scalable

• Opportunity for Westet to offer innovative new products (VoIP, Naked DSL and SME/SOHO products)

• iiNet customers who cannot get ADSL may be able to get Westnet satellite

Form an exciting new culture from the best of both organisations

For

per

sona

l use

onl

y

12 Investor Presentation May 2008

iiNet Trading Update 1st Half FY08 • Record first half EBITDA

result • Declared 3cps interim dividend

• Delivered cost base certainty

• Reduced dependency on Telstra

• Strong net cash position • Re-entered M&A activity

• First to offer Naked DSL • On-net customers exceed 150,000

2nd Half FY08 Update

• Strong growth in Naked DSL to 17,552 customers

• Cape Town call centre implementation well on-track

• Leading market consolidation

• On track to exceed first half EBITDA and NPAT result For

per

sona

l use

onl

y

13 Investor Presentation May 2008

Summary

• A logical and value accretive deal pre synergies

• Significant savings by leveraging iiNet’s infrastructure and scale

• Upside from complementary cultures, products, markets & capabilities

For

per

sona

l use

onl

y

14 Investor Presentation May 2008

Event Date ASX Trading Halt commences Pre-market Tuesday, 6 May 2008

Book Build opens for Placement Tuesday, 6 May 2008

Roadshow Melbourne & Sydney Tuesday & Wednesday, 6-7 May 2008

Firm Bids for Placement Shares 6pm (AEST) Wednesday, 7 May 2008

Allocations advised to successful bidders 7pm (AEST) Wednesday, 7 May 2008

Letters of Offer sent 7pm (AEST) Wednesday, 7 May 2008

Return of signed Acceptance Advices Thursday, 8 May 2008

ASX announcement of Placement & Westnet acquisition Thursday, 8 May 2008

DvP Settlement of Tranche 1 of Placement Wednesday, 14 May 2008

EGM to approve Placement Friday, 13 June 2008

DvP Settlement of Tranche 2 of Placement Monday, 16 June 2008

Indicative Placement Timetable

For

per

sona

l use

onl

y

15 Investor Presentation May 2008

Appendices Regulatory Update

For

per

sona

l use

onl

y

16 Investor Presentation May 2008

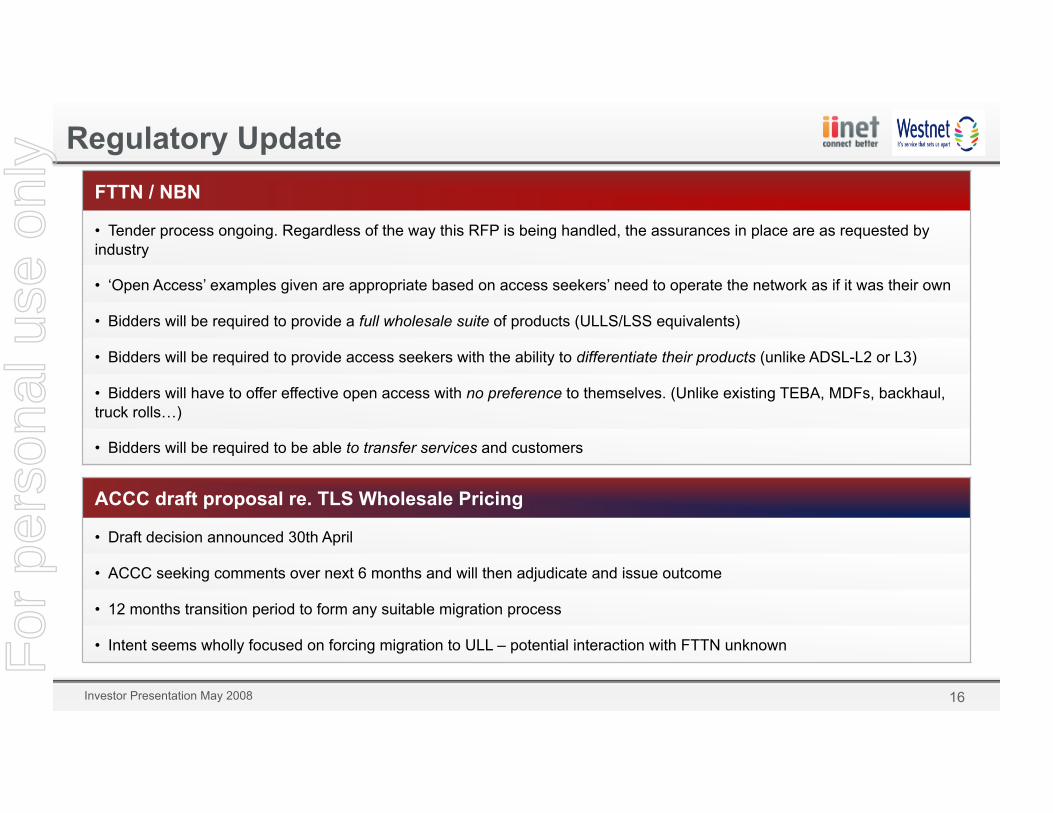

Regulatory Update FTTN / NBN

• Tender process ongoing. Regardless of the way this RFP is being handled, the assurances in place are as requested by industry

• ‘Open Access’ examples given are appropriate based on access seekers’ need to operate the network as if it was their own

• Bidders will be required to provide a full wholesale suite of products (ULLS/LSS equivalents)

• Bidders will be required to provide access seekers with the ability to differentiate their products (unlike ADSL-L2 or L3)

• Bidders will have to offer effective open access with no preference to themselves. (Unlike existing TEBA, MDFs, backhaul, truck rolls…)

• Bidders will be required to be able to transfer services and customers

ACCC draft proposal re. TLS Wholesale Pricing

• Draft decision announced 30th April

• ACCC seeking comments over next 6 months and will then adjudicate and issue outcome

• 12 months transition period to form any suitable migration process

• Intent seems wholly focused on forcing migration to ULL – potential interaction with FTTN unknown For

per

sona

l use

onl

y

17 Investor Presentation May 2008

Network choices

Neighbourhood Local Exchange

State

Cop

per

Fibr

e

Competitive access points • Equivalent Access for all • Choice of interconnect locations • Control of QoS for VoIP, Video… • Preserve a copper option

Structural separation model

Pillar

Node

For

per

sona

l use

onl

y

18 Investor Presentation May 2008

Network choices

No Competitive access points • Resale only • No Control of QoS for VoIP, Video… • No copper option from exchange • Service differentiation only

Monopoly model

Neighbourhood Local Exchange

State

Fibr

e

Pillar

Node

For

per

sona

l use

onl

y

19 Investor Presentation May 2008

Tender Requests

1.3.1.10 The Commonwealth’s objectives for the NBN project are to establish a national broadband network that … facilitates competition through open access arrangements that ensure equivalence of price and non-price terms and conditions, and provide scope for access seekers to differentiate their product offerings

1.1.10 Proponents should submit arrangements for open access to their networks, including measures or models to ensure equivalence of access prices and non-price terms and conditions, and arrangements for allowing access seekers to differentiate their service offerings to customers

1.4.1. (a) Proponents should, as a minimum, provide a service description for each wholesale service to be offered by the NBN ... Amongst other things, Proponents should include …the extent to which the service is compatible with equivalent existing … and arrangements for seamless transfer of existing services and applications to the new service where appropriate.

Request for Proposals to roll-out and operate a National Broadband Network for Australia

For

per

sona

l use

onl

y

20 Investor Presentation May 2008

Tender Requests (cont’d)

1.4.1. (b) Wholesale services should be taken to include the full range of wholesale services including facilities access, interconnection, basic access (including bitstream), transmission (including backhaul) and other wholesale … and other services.

1.5.14 The Government is therefore determined to ensure that appropriate open access arrangements are in place to promote competition and ensure efficient investment. In this context it will be important to ensure that access is provided on equivalent price and non-price terms and conditions.

1.5.16 If a Proponent proposes to supply both wholesale and retail services it should demonstrate what structural measures or models it proposes be put in place and maintained to prevent inappropriate self-preferential treatment and ensure that effective open access is achieved on the terms required by the Commonwealth.

Request for Proposals to roll-out and operate a National Broadband Network for Australia

For

per

sona

l use

onl

y

![[MS-PPPI]: PPP Over IrDA Dialup Protocol... · Protocol (PPP Over IrDA Dialup Protocol), and includes contributions from Microsoft, Ericsson, and Nokia. The PPP Over IrDA Dialup Protocol](https://static.fdocuments.net/doc/165x107/5e904da7efdba9511f28b94d/ms-pppi-ppp-over-irda-dialup-protocol-protocol-ppp-over-irda-dialup-protocol.jpg)