Fomc 20080430 Material

75

Appendix 1: Materials used by Mr. Dudley April 29–30, 2008 192 of 266 Authorized for Public Release

-

Upload

fraser-federal-reserve-archive -

Category

Documents

-

view

217 -

download

0

Transcript of Fomc 20080430 Material

Appendix 1: Materials used by Mr. Dudley

April 29–30, 2008 192 of 266Authorized for Public Release

Page 1 of 12Class II FOMC – Restricted FR

110

120Index to 100 on 8/1/07

110

120 Index to 100 on 8/1/07(1) U.S. Equity Indices Stabilize

August 1, 2007 – April 25, 2008

70

80

90

100

70

80

90

100

S&P 500Nasdaq

Percent BPS(2) Corporate Credit Spreads Decline

January 1 2007 – April 25 2008

60

70

08/01/07 09/01/07 10/01/07 11/01/07 12/01/07 01/01/08 02/01/08 03/01/08 04/01/0860

70S&P 500 Financials

Source: Bloomberg

89

101112

500600700800900

High-Yield Yield (LHS)Investment Grade Yield (LHS)High-Yield Spread (RHS)Investment Grade Spread (RHS)

January 1, 2007 – April 25, 2008

34567

0100200300400

800BPS

200BPS

ITRAXX Crossover (LHS)

(3) Global Credit Default Swap Spreads NarrowMarch 1, 2007 – April 25, 2008

301/01/07 03/01/07 05/01/07 07/01/07 09/01/07 11/01/07 01/01/08 03/01/08

0

Source: Bloomberg

200

400

600

50

100

150CDX IG (RHS)

0

200

03/01/07 05/01/07 07/01/07 09/01/07 11/01/07 01/01/08 03/01/080

50

Source: JP Morgan

April 29–30, 2008 193 of 266Authorized for Public Release

Page 2 of 12

160

200BPS

40

50 Percent

MOVE (LHS)

(4) Implied Volatility DecreasesJanuary 1, 2007 – April 25, 2008

Class II FOMC – Restricted FR

80

120

20

30VIX (RHS)

1-Month Dollar-Yen Vol

0

40

01/01/07 03/01/07 05/01/07 07/01/07 09/01/07 11/01/07 01/01/08 03/01/080

101-Month Euro-Dollar Vol (RHS)

Source: Bloomberg(5) Prices for AAA-Rated Tranches on ABX Indices Rise

80

90

100

110Dollars

80

90

100

110Dollars

2007 012006-02

2006-01

AAA-Rated Tranches on ABX by Vintage

(5) Prices for AAA-Rated Tranches on ABX Indices Rise January 1, 2007 – April 25, 2008

40

50

60

70

80

40

50

60

70

802007-01

2007-02

on ABX by Vintage

4001/01/07 03/01/07 05/01/07 07/01/07 09/01/07 11/01/07 01/01/08 03/01/08

40

Source: JP Morgan

1.2Ratio

1.2Ratio

10-Year

(6) Ten and Thirty Year AAA –Rated Municipals* Recover January 1, 2007 – April 25, 2008

0.8

0.9

1.0

1.1

0.8

0.9

1.0

1.130-Year

0.6

0.7

01/01/07 03/01/07 05/01/07 07/01/07 09/01/07 11/01/07 01/01/08 03/01/080.6

0.7

Source: Bloomberg *This chart shows the ratio of municipal debt yields to Treasury yields

April 29–30, 2008 194 of 266Authorized for Public Release

Page 3 of 12

100

120Index to 100 on 01/01/08

100

120Index to 100 on 01/01/08(7) Investment Bank Equity Prices Stabilize

January 1, 2008 – April 25, 2008

Class II FOMC – Restricted FR

60

80

100

60

80

100

Morgan Stanley Equity

Goldman Sachs Equity

4001/01/08 02/01/08 03/01/08 04/01/08

40

Lehman Brothers Equity

Merrill Lynch Equity

Source: Markit and Bloomberg

BPS BPS(8) Investment Bank CDS Spreads Narrow

January 1 2008 – April 25 2008

300

400

500

300

400

500Morgan Stanley CDSGoldman Sachs CDS

Lehman Brothers CDSMerrill Lynch CDS

January 1, 2008 – April 25, 2008

0

100

200

0

100

200

001/01/08 02/01/08 03/01/08 04/01/08

0

Source: Markit and Bloomberg

April 29–30, 2008 195 of 266Authorized for Public Release

Page 4 of 12Class II FOMC – Restricted FR

(9) Collateral Haircuts Stabilize at Higher LevelsFebruary 1, 2008 – April 9, 2008

MaturityOvernight 1-Month 3-Month

COLLATERAL Date Average High Low Average High Low Average High Low9-Apr 0.5% 1.5% 0.0% 0.6% 1.5% 0.0% 0.7% 2.0% 0.0%

10-Mar 0.3% 1.5% 0.0% 0.4% 1.5% 0.0% 0.4% 1.5% 0.0%3-Mar 0.2% 1.5% 0.0% 0.3% 1.5% 0.0% 0.4% 1.5% 0.0%1-Feb 0.2% 1.5% 0.0% 0.2% 1.5% 0.0% 0.3% 1.5% 0.0%9-Apr 1.3% 3.5% 0.0% 2.1% 7.5% 0.0% 1.6% 5.0% 0.0%

10-Mar 0.7% 2.0% 0.0% 1.9% 7.5% 0.0% 1.7% 5.5% 0.0%3 M 0 6% 2 0% 0 0% 1 1% 3 0% 0 0% 1 4% 4 5% 0 0%

Treasury

Agency Debt3-Mar 0.6% 2.0% 0.0% 1.1% 3.0% 0.0% 1.4% 4.5% 0.0%1-Feb 0.5% 2.0% 0.0% 1.1% 3.0% 0.0% 1.2% 4.5% 0.0%9-Apr 5% 7% 3% 6% 8% 3% 6% 9% 3%

10-Mar 5% 7% 3% 5% 8% 3% 6% 10% 3%3-Mar 3% 3% 3% 3% 3% 3% 4% 5% 3%1-Feb 3% 5% 2% 3% 6% 3% 4% 5% 3%

Non-agency MBS9-Apr 21% 28% 15% 27% 35% 15% 25% 35% 15%

g y

Agency MBS

9-Apr 21% 28% 15% 27% 35% 15% 25% 35% 15%10-Mar 18% 28% 10% 19% 28% 12% 19% 28% 15%3-Mar 16% 18% 15% 16% 18% 15% 18% 18% 18%1-Feb 13% 20% 5% 11% 20% 4% 14% 20% 7%9-Apr 38% 43% 30% 36% 43% 30% 33% 43% 23%

10-Mar 28% 43% 18% 28% 43% 18% 30% 43% 18%3-Mar 14% 18% 10% 16% 20% 10%1-Feb 19% 43% 10% 16% 43% 10% 28% 43% 13%

Prime

Alt-A

Corporate Debt9-Apr 17% 25% 10% 18% 25% 11% 19% 25% 12%

10-Mar 12% 25% 5% 15% 25% 5% 18% 25% 15%3-Mar 11% 25% 3% 13% 25% 3% 18% 25% 15%1-Feb 10% 25% 3% 10% 25% 3% 13% 25% 3%9-Apr 36% 70% 19% 39% 70% 25% 39% 70% 25%

10-Mar 28% 70% 10% 27% 70% 15% 36% 70% 25%High Yield

High Grade

Source: Survey of 14 Hedge Funds and 1 REIT

3-Mar 26% 70% 9% 27% 70% 10% 35% 70% 20%1-Feb 25% 70% 6% 24% 70% 10% 28% 70% 10%

High Yield

April 29–30, 2008 196 of 266Authorized for Public Release

Page 5 of 12

100

120BPS

100

120BPS

U.S.U.K.

(10) Bank Term Funding Pressures Revive: One-Month Libor–OIS Spread August 14, 2007 – April 28, 2008

Class II FOMC – Restricted FR

40

60

80

40

60

80Euro-Area

BPS BPS

0

20

08/01/07 09/01/07 10/01/07 11/01/07 12/01/07 01/01/08 02/01/08 03/01/08 04/01/080

20

Source: Bloomberg(11) Three-Month Libor – OIS Spread

A t 14 2007 A il 28 2008

60

80

100

120

60

80

100

120August 14, 2007 – April 28, 2008

0

20

40

60

0

20

40

60

U.S.U.K.Euro-Area

08/01/07 09/01/07 10/01/07 11/01/07 12/01/07 01/01/08 02/01/08 03/01/08 04/01/08Source: Bloomberg

3.00Percent

3.00 Percent

LIBOR Fixing WSJ Article

(12) Range of One-Month LIBOR Rates from 16 Contributing BanksApril 4, 2008 – April 28, 2008

2 70

2.80

2.90

2 70

2.80

2.90g

on LIBOR Manipulation

2.60

2.70

04/04/08 04/08/08 04/10/08 04/14/08 04/16/08 04/18/08 04/22/08 04/24/08 04/28/082.60

2.70

Source: Bloomberg

April 29–30, 2008 197 of 266Authorized for Public Release

Page 6 of 12Class II FOMC – Restricted FR

100

120

140BPS

40

50

60BPS

Spread between 3-Month LIBOR and OIS Rate (LHS)

Spread between Implied 3-Month FX Swap Financing and 3-Month LIBOR Rate (RHS)

(13) Three-month FX Swap Financing Cost to Three-Month LIBOR August 1, 2007 – April 28, 2008

40

60

80

100

10

20

30

40

Percent BPS(14) Spread between Jumbo and Conforming Mortgage Rates Remains Wide January 1 2007 – April 25 2008

0

20

08/01/07 10/01/07 12/01/07 02/01/08 04/01/08-10

0

Source: JP Morgan

6.50

7.00

7.50

8.00

90

120

150

180Conforming Mortgage Rates (LHS)

Jumbo Mortgage Rates (LHS)Spread (RHS)

January 1, 2007 April 25, 2008

5.00

5.50

6.00

01/01/07 03/01/07 05/01/07 07/01/07 09/01/07 11/01/07 01/01/08 03/01/080

30

60

01/01/07 03/01/07 05/01/07 07/01/07 09/01/07 11/01/07 01/01/08 03/01/08

Source: Bloomberg

75

90BPS

50

60Billions of Dollars

Auction Size (RHS)

TAF Stop-out Spread to Minimun Bid Rate (LHS)

(15) TAF Auction ResultsDecember 20, 2007 – April 21, 2008

30

45

60

20

30

40

p p ( )

0

15

12/20/07 12/27/07 01/17/08 01/31/08 02/14/08 02/28/08 03/13/08 03/27/08 04/10/08 04/24/080

10

Source: Federal Reserve Board

April 29–30, 2008 198 of 266Authorized for Public Release

Page 7 of 12

(16) Federal Reserve Term Securities Lending Facility Results

Class II FOMC – Restricted FR

Auction Settlement

Term Collateral Amount Minimum Fee Rate

Stop-out Rate

Propositions Bid/Cover

3/28/2008 28 Days Schedule 2 $75 b 0.25% 0.33% $86.1 b 1.15

4/4/2008 28 Days Schedule 1 $25 b 0.10% 0.16% $46.9 b 1.88

4/11/2008 28 Days Schedule 2 $50 b 0.25% 0.25% $40.0 b 0.68

4/18/2008 28 Days Schedule 1 $25 b 0.10% 0.10% $35.1 b 1.40

4/25/2008 28 Days Schedule 2 $75 b 0 25% 0 25% $ 59 5 b 0 79

Source: Federal Reserve Board

4 00Percent

4 00 Percent

(17) GC Treasury Repo Market Improves as a Result of TSLF AuctionsFebruary 1, 2008 – April 25, 2008

4/25/2008 28 Days Schedule 2 $75 b 0.25% 0.25% $ 59.5 b 0.79

2.002.503.003.504.00

2.002.503.003.504.00

TSLF

TSLF

TSLF

TSLF

0.000.501.001.50

02/01/08 03/01/08 04/01/080.000.501.001.50

Overnight GC Treasury Repo Rate

Target Fed Funds Rate

S F d l R B k f N Y kSource: Federal Reserve Bank of New York

100

120BPS

100

120BPS

DW Rate Cut Increase TAF size

Intermeeting Rate Cut

Increase

DW Rate Cut and PDCF

(18) One-Month Libor -OIS Spread Declines After Fed Actions August 1, 2007 – April 28, 2008

40

60

80

40

60

80Increase

TAF size and Term

MBS Repo

PDCF Introduced

FOMC Cuts Policy Rate by 50 bps

0

20

08/01/07 09/01/07 10/01/07 11/01/07 12/01/07 01/01/08 02/01/08 03/01/08 04/01/080

20TAF Introduced

TSLF Introduced

Source: Bloomberg

April 29–30, 2008 199 of 266Authorized for Public Release

Class II FOMC – Restricted FR Page 8 of 12

3.00

3.50Percent

3.00

3.50 Percent

1/29/2008 3/17/2008 4/25/2008

(19) Fed Funds Futures Curve Shifts Upward

1.50

2.00

2.50

1.50

2.00

2.50

1.00Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08

Fed Funds Futures Contracts

1.00

Source: Bloomberg

4.00Percent

4.00 Percent(20) Eurodollar Futures Curve: A Bigger Upward Shift

2.50

3.00

3.50

2.50

3.00

3.50

1.00

1.50

2.00

Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09Eurodollar Futures Contracts

1.00

1.50

2.00

1/29/2008 3/17/2008 4/25/2008

Source: BloombergSource: Bloomberg

April 29–30, 2008 200 of 266Authorized for Public Release

Class II FOMC – Restricted FR Page 9 of 12

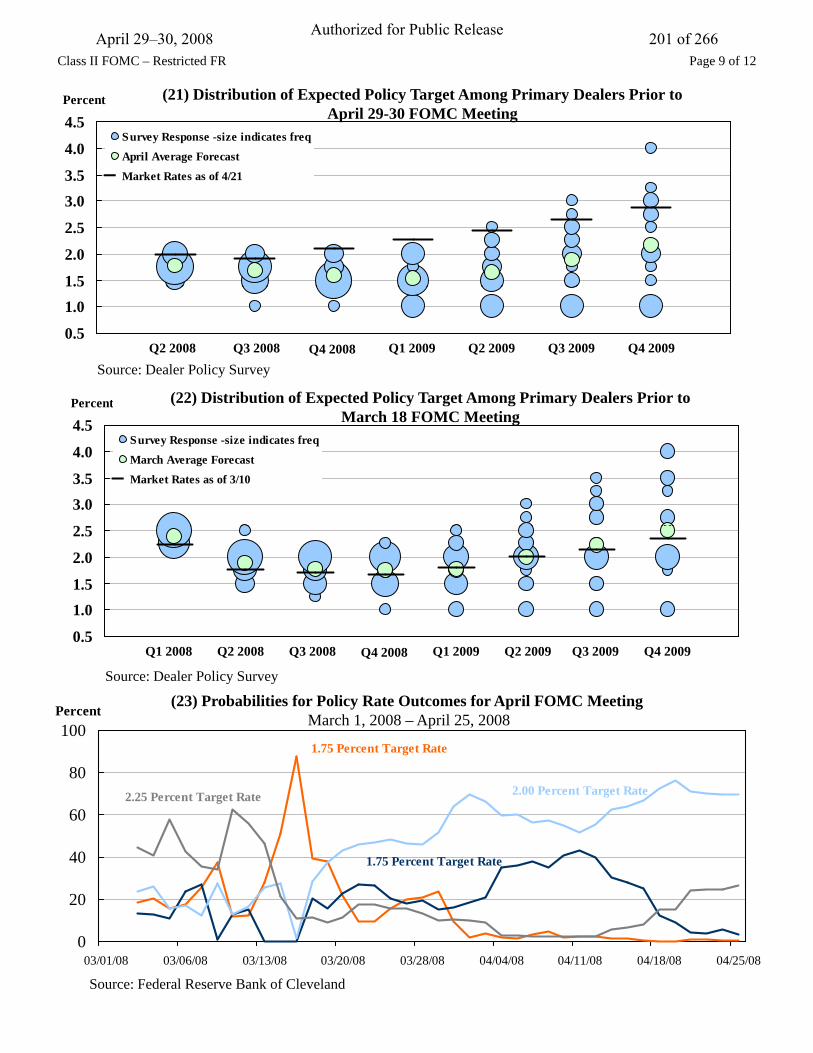

4.0

4.5Percent

Survey Response -size indicates freq

April Average Forecast

(21) Distribution of Expected Policy Target Among Primary Dealers Prior to April 29-30 FOMC Meeting

1.5

2.0

2.5

3.03.5 Market Rates as of 4/21

Percent (22) Distribution of Expected Policy Target Among Primary Dealers Prior to

0.5

1.0

Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009Source: Dealer Policy Survey

2 5

3.03.5

4.0

4.5Percent

Survey Response -size indicates freq

March Average Forecast

Market Rates as of 3/10

March 18 FOMC Meeting

0.5

1.01.5

2.0

2.5

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009

Source: Dealer Policy Survey

100Percent

1.75 Percent Target Rate

(23) Probabilities for Policy Rate Outcomes for April FOMC MeetingMarch 1, 2008 – April 25, 2008

40

60

802.00 Percent Target Rate2.25 Percent Target Rate

1.75 Percent Target Rate

0

20

03/01/08 03/06/08 03/13/08 03/20/08 03/28/08 04/04/08 04/11/08 04/18/08 04/25/08

Source: Federal Reserve Bank of Cleveland

April 29–30, 2008 201 of 266Authorized for Public Release

Class II FOMC – Restricted FR Page 10 of 12

180

200Index to 100 on 1/1/07

180

200Index to 100 on 1/1/07

GSCI SpotGSCI Energy

(24) Recent Commodity Price Pressures Concentrated in Energy January 1, 2007 – April 25, 2008

120

140

160

120

140

160GSCI AgricultureGSCI Industrial Metals

(25) TIPS Implied Average Rate of Inflation: 5-10 Year Horizon

80

100

01/01/07 03/01/07 05/01/07 07/01/07 09/01/07 11/01/07 01/01/08 03/01/0880

100

Source: Bloomberg

2 80

3.00

3.20

3.40Percent

2 80

3.00

3.20

3.40Percent

Barclays

Federal Reserve Board

( ) p gAugust 1, 2007 – April 25, 2008

2.20

2.40

2.60

2.80

2.20

2.40

2.60

2.80

08/01/07 09/01/07 10/01/07 11/01/07 12/01/07 01/01/08 02/01/08 03/01/08 04/01/08

Source: Federal Reserve Board and Barclays Capital

April 29–30, 2008 202 of 266Authorized for Public Release

Class II FOMC – Restricted FR Page 11 of 12

5.00

6.00Percent

5.00

6.00 Percent

High on 4/4 10%

High on 1/7: 7% High on

4/23 10%

(26) Volatility in the Fed Funds Market January 1, 2008 – April 25, 2008

2.00

3.00

4.00

2.00

3.00

4.00

ff i

4/4: 10% 4/23: 10%

0.00

1.00

01/01/08 02/01/08 03/01/08 04/01/080.00

1.00Effective RateTarget Rate

Source: Federal Reserve Bank of New York

(27) Primary Credit Facility and Primary Dealer Credit Facility Borrowing

40

50

60Billions of Dollars

PDCF

PCF

(27) Primary Credit Facility and Primary Dealer Credit Facility BorrowingJanuary 1, 2008 – April 25, 2008

10

20

30

001/01/08 01/21/08 02/08/08 02/28/08 03/19/08 04/08/08

Source: Federal Reserve Bank of New York

April 29–30, 2008 203 of 266Authorized for Public Release

Class II FOMC – Restricted FR Page 12 of 12APPENDIX: Reference Exhibits

4.00

4.50Percent

4.00

4.50 Percent

1/29/2008 3/17/2008 4/25/2008

(28) Treasury Yield Curve Shifts Upward

2.00

2.50

3.00

3.50

2.00

2.50

3.00

3.50

1.00

1.50

Tenor1.00

1.50

Source: Bloomberg

1-Year 2-Year 3-Year 5-Year 7-Year 10-Year

115Index to 100

115Index to 100

(29) Dollar Remains Weak January 1, 2006 – April 25, 2008

9095

100105110115

9095100105110115y , p ,

Yen vs. Dollar: Index as of Jan06

Dol

lar

App

reci

atio

n

Broad Trade-Weighted Dollar: Index as of Jan 97

7075808590

01/01/06 04/01/06 07/01/06 10/01/06 01/01/07 04/01/07 07/01/07 10/01/07 01/01/08 04/01/087075808590

Euro vs. Dollar: Index as of Jan06D

olla

r D

epre

ciat

ion

01/01/06 04/01/06 07/01/06 10/01/06 01/01/07 04/01/07 07/01/07 10/01/07 01/01/08 04/01/08Source: Bloomberg and Federal Reserve Board

80

120BPS

1.28

1.32

$/Euro

Eurodollar-Euribor* (LHS)

$ per Euro (RHS)

(30) Dollar Tracks Interest Rate Differentials January 1, 2007 – April 25, 2008

120

-80

-40

040 1.36

1.40

1.44

1.481 52

p ( )

-200

-160-120

01/01/07 03/01/07 05/01/07 07/01/07 09/01/07 11/01/07 01/01/08 03/01/08

1.52

1.56

1.60

Source: Bloomberg * Based on December 2008 calendar spread.

April 29–30, 2008 204 of 266Authorized for Public Release

Appendix 2: Materials used by Mr. Madigan

April 29–30, 2008 205 of 266Authorized for Public Release

Class I FOMC – Restricted Controlled (FR)

Material for Briefing on FOMC Participants’ Economic Projections Brian Madigan April 29, 2008

April 29–30, 2008 206 of 266Authorized for Public Release

2008 2009 2010Central Tendencies

Real GDP Growth 0.3 to 1.2 2.0 to 2.8 2.6 to 3.1January projections 1.3 to 2.0 2.1 to 2.7 2.5 to 3.0

Unemployment Rate 5.5 to 5.7 5.2 to 5.7 4.9 to 5.5January projections 5.2 to 5.3 5.0 to 5.3 4.9 to 5.1

PCE Inflation 3.1 to 3.4 1.9 to 2.3 1.8 to 2.0January projections 2.1 to 2.4 1.7 to 2.0 1.7 to 2.0

Core PCE Inflation 2.1 to 2.4 1.9 to 2.1 1.7 to 1.9January projections 2.0 to 2.2 1.7 to 2.0 1.7 to 1.9

RangesReal GDP Growth 0.0 to 1.5 1.8 to 3.0 2.0 to 3.4

January projections 1.0 to 2.2 1.8 to 3.2 2.2 to 3.2

Unemployment Rate 5.3 to 6.0 5.1 to 6.3 4.7 to 5.9January projections 5.0 to 5.5 4.9 to 5.7 4.7 to 5.4

PCE Inflation 2.8 to 3.8 1.7 to 3.0 1.5 to 2.0January projections 2.0 to 2.8 1.7 to 2.3 1.5 to 2.0

Core PCE Inflation 1.9 to 2.5 1.7 to 2.2 1.3 to 2.0January projections 1.9 to 2.3 1.7 to 2.2 1.4 to 2.0

1. Projections of real GDP growth, PCE inflation and core PCE inflation are fourth-quarter-to-fourth-quarter growth rates, i.e. percentage changes from the fourth quarter of the prior year to the fourth quarter of the indicated year. PCE inflation and core PCE inflation are the percentage rates of change in the price index for personal consumption expenditures and the price index for personal consumption expenditures excluding food and energy, respectively. Each participant's projections are based on his or her assessment of appropriate monetary policy. The range for each variable in a given year includes all participants' projections, from lowest to highest, for that variable in the given year; the central tendencies exclude the three highest and three lowest projections for each variable in each year.

Table 1: Economic Projections of Federal Reserve Governors and Reserve Bank Presidents 1

April 29–30, 2008 207 of 266Authorized for Public Release

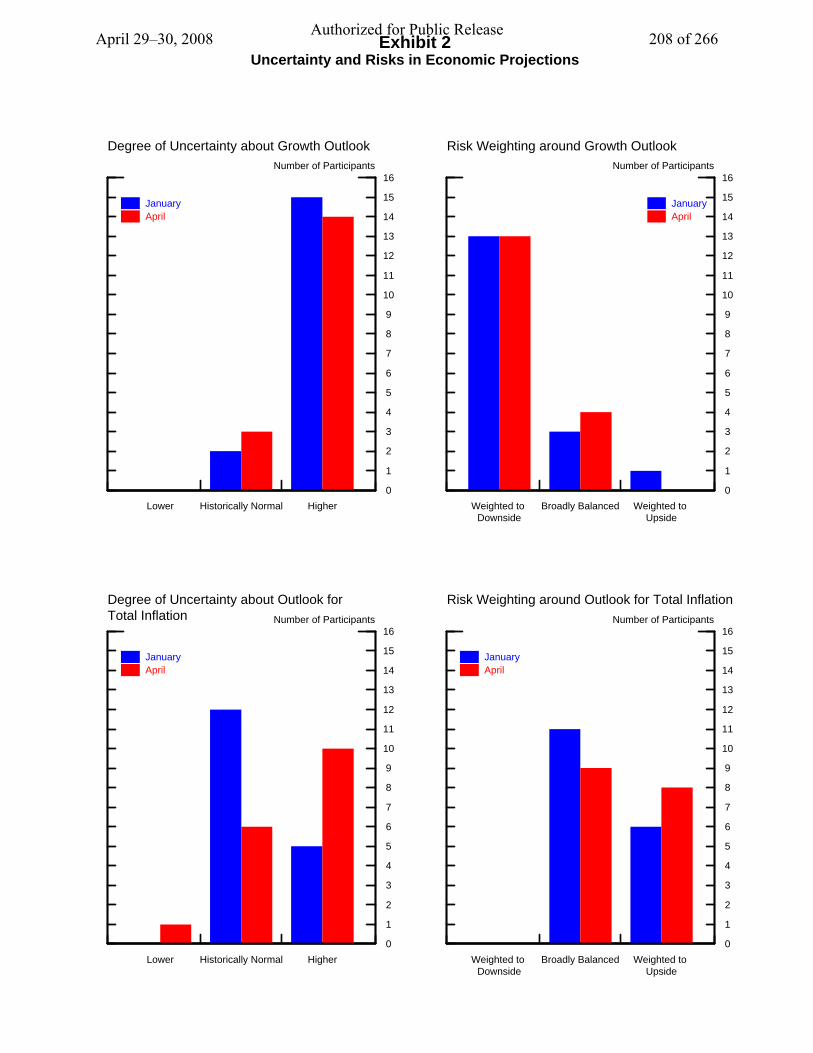

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16Number of Participants

Lower Historically Normal Higher

January April

Degree of Uncertainty about Growth Outlook

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16Number of Participants

Weighted to Downside

Broadly Balanced Weighted to Upside

January April

Risk Weighting around Growth Outlook

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16Number of Participants

Lower Historically Normal Higher

January April

Degree of Uncertainty about Outlook for Total Inflation

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16Number of Participants

Weighted to Downside

Broadly Balanced Weighted to Upside

January April

Risk Weighting around Outlook for Total Inflation

Exhibit 2Uncertainty and Risks in Economic Projections

April 29–30, 2008 208 of 266Authorized for Public Release

Appendix 3: Materials used by Mr. English

April 29–30, 2008 209 of 266Authorized for Public Release

Class I FOMC – Restricted Controlled (FR) Material for the FOMC Briefing on Monetary Policy Alternatives William B. English April 29-30, 2008

April 29–30, 2008 210 of 266Authorized for Public Release

Class I FOMC – Restricted Controlled (FR) Table 1: Alternative Language for the April 2008 FOMC Announcement April 29-30, 2008

March FOMC Alternative A Alternative B Alternative C

Policy Decision

1. The Federal Open Market Committee decided today to lower its target for the federal funds rate 75 basis points to 2-1/4 percent.

The Federal Open Market Committee decided today to lower its target for the federal funds rate 50 basis points to 1-3/4 percent.

The Federal Open Market Committee decided today to lower its target for the federal funds rate 25 basis points to 2 percent.

The Federal Open Market Committee decided today to keep its target for the federal funds rate at 2-1/4 percent.

2. Recent information indicates that the outlook for economic activity has weakened further. Growth in consumer spending has slowed and labor markets have softened. Financial markets remain under considerable stress, and the tightening of credit conditions and the deepening of the housing contraction are likely to weigh on economic growth over the next few quarters.

Recent information indicates that economic activity remains weak. Household and business spending has been subdued and labor markets have softened further. Financial markets remain under considerable stress, and tight credit conditions and the deepening housing contraction are likely to weigh on economic growth over the next few quarters.

Recent information indicates that economic activity remains weak. Household and business spending has been subdued and labor markets have softened further. Financial markets remain under considerable stress, and tight credit conditions and the deepening housing contraction are likely to weigh on economic growth over the next few quarters.

Recent information indicates that economic activity remains weak. Household and business spending has been subdued and labor markets have softened further. Financial markets remain under considerable stress, and tight credit conditions and the deepening housing contraction are likely to weigh on economic growth over the next few quarters.

Rationale 3. Inflation has been elevated, and some indicators of inflation expectations have risen. The Committee expects inflation to moderate in coming quarters, reflecting a projected leveling-out of energy and other commodity prices and an easing of pressures on resource utilization. Still, uncertainty about the inflation outlook has increased. It will be necessary to continue to monitor inflation developments carefully.

Inflation has been elevated, and some indicators of inflation expectations have risen in recent months. The Committee expects inflation to moderate in coming quarters, reflecting a projected leveling-out of energy and other commodity prices and an easing of pressures on resource utilization. Still, uncertainty about the inflation outlook remains high. It will be necessary to continue to monitor inflation developments carefully.

Although readings on core inflation have improved somewhat, energy and other commodity prices have increased, and some indicators of inflation expectations have risen in recent months. The Committee expects inflation to moderate in coming quarters, reflecting a projected leveling-out of energy and other commodity prices and an easing of pressures on resource utilization. Still, uncertainty about the inflation outlook remains high. It will be necessary to continue to monitor inflation developments carefully.

Inflation has been elevated, and some indicators of inflation expectations have risen in recent months. The Committee expects inflation to moderate in coming quarters, but uncertainty about the inflation outlook remains high. It will be necessary to continue to monitor inflation developments carefully.

Assessment of Risk

4. Today’s policy action, combined with those taken earlier, including measures to foster market liquidity, should help to promote moderate growth over time and to mitigate the risks to economic activity. However, downside risks to growth remain. The Committee will act in a timely manner as needed to promote sustainable economic growth and price stability.

The Committee judged that a further reduction in interest rates was appropriate to foster moderate growth over time and to mitigate the risks to economic activity. The Committee will act in a timely manner as needed to promote sustainable economic growth and price stability.

The substantial easing of monetary policy to date, combined with ongoing measures to foster market liquidity, should help to promote moderate growth over time and to mitigate risks to economic activity. The Committee will continue to monitor economic and financial developments and will act as needed to promote sustainable economic growth and price stability.

Although downside risks to growth remain, the substantial easing of monetary policy to date, combined with ongoing measures to foster market liquidity, should help to promote moderate growth over time and to mitigate risks to economic activity. The Committee will continue to monitor economic and financial developments and will act as needed to promote sustainable economic growth and price stability.

April 29–30, 2008 211 of 266Authorized for Public Release

Appendix 4: Materials used by Mr. Stockton

April 29–30, 2008 212 of 266Authorized for Public Release

Class II FOMC - RESTRICTED (FR)

2007-Q4Final Greenbook Advance

Real GDP 0.6 0.4 0.6

Final Sales 2.4 -0.3 -0.2

Personal Consumption 2.3 1.0 1.0 Durables 2.0 -7.0 -6.1 Nondurables 1.2 -0.9 -1.3 Services 2.8 3.6 3.4

Business Fixed Investment 6.0 -1.1 -2.5 Nonresidential Structures 12.4 -2.8 -6.2 Equipment and Software 3.1 -0.2 -0.7

Residential Investment -25.2 -30.9 -26.7

Government 2.0 0.7 2.0 Federal 0.5 1.9 4.6 State and Local 2.8 0.1 0.5

Exports 6.5 6.2 5.5

Imports -1.4 2.4 2.5

Level in chained 2000 dollars:

Change in nonfarm business inventories -21.7 -2.4 2.7

Change in farm inventories 2.2 0.8 -0.7

Net Exports -503.2 -492.4 -495.9

Price Indexes:

Total PCE Chain Price Index 3.9 3.5 3.5

Core PCE Chain Price Index 2.5 2.1 2.2

Gross Domestic Product(percent change at an annual rate)

2008-Q1

Page 1 of 1

April 29–30, 2008 213 of 266Authorized for Public Release

Appendix 5: Materials used by Messrs. Madigan, Meyer, Clouse, Hilton, and Dudley

April 29–30, 2008 214 of 266Authorized for Public Release

Implications of Interest on Reserves forImplications of Interest on Reserves for Monetary Policy Implementation

Presentation by Federal Reserve StaffatJoint Meeting of Board of Governors and Federal Open Market CommitteepApril 30, 2008

Class I FOMC - Restricted Controlled (FR)

April 29–30, 2008 215 of 266Authorized for Public Release

New powers effective October 2011

Board may authorize Reserve Banks to pay interest Board may authorize Reserve Banks to pay interest on balances maintained by depository institutions at a rate or rates not to exceed the general level of short-term interest rates

Board may set required reserve ratios on transaction d it i f 0 t 14 t ( tl 8 tdeposits in a range of 0 to 14 percent (currently 8 to 14 percent) Permits effective elimination of reserve requirementsq

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 2 of 52

April 29–30, 2008 216 of 266Authorized for Public Release

Remaining statutory constraints

Reserve requirements can be applied only to transaction Reserve requirements can be applied only to transaction deposits, nonpersonal time deposits, and eurodollar liabilities Only depository institutions subject to reserves Reserve requirements were designed to facilitate control of M1 Reserve requirements were designed to facilitate control of M1

Prohibition against payment of interest on demand deposits by depository institutions

Statutory constraints on open market purchases

Statutory requirements for cost recovery on priced services

Absence of interest payments to Treasury and foreign central banks on their Fed accounts

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 3 of 52

April 29–30, 2008 217 of 266Authorized for Public Release

Process to date

Chairman asked staff to begin background work Chairman asked staff to begin background work

System workgroup undertook a preliminary study of a range of options for implementing monetary policyrange of options for implementing monetary policy

System workgroup initiated work on implications for priced services and accountingpriced services and accounting

Board hosted a workshop on monetary policy implementation attended by five foreign central banksp y g

Today’s joint Board-FOMC meeting

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 4 of 52

April 29–30, 2008 218 of 266Authorized for Public Release

Outline of briefing

Overview (Madigan) Overview (Madigan)

Current approach to implementing U.S. monetary policy (Meyer)policy (Meyer)

Discussion of five options (Clouse and Hilton)

C l di t (D dl ) Concluding comments (Dudley)

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 5 of 52

April 29–30, 2008 219 of 266Authorized for Public Release

Following the briefing, we will seek your comments on:

Criteria for evaluating options Criteria for evaluating options

Options

Process and Timeline

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 6 of 52

April 29–30, 2008 220 of 266Authorized for Public Release

Implementing U.S. Monetary Policy:p g y yCurrent Framework and Operating Procedures

Summarize Summarize banking system’s demand for central bank balances Desk’s management of the supply of balances equilibrium in the federal funds market

Focus on policy implementation in normal times brief discussion of policy implementation since August

Conclude with strengths and shortcomings of current approachapproach

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 7 of 52

April 29–30, 2008 221 of 266Authorized for Public Release

Demand: Reserve Requirements2008 Reserve Requirement Ratios2008 Reserve Requirement Ratios

Type of liability Requirement (% of liabilities)

Net transaction accounts

$0 to $9.3 million 0 %

> $9.3 million to $43.9 million 3 %

> $43.9 million 10 %$ %

Nonpersonal time deposits 0 %

Eurocurrency liabilities 0 %

For details on the multitude of complex definitions, rules, carryover provisions, etc., see the 135 page Reserve Maintenance Manual

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 8 of 52

April 29–30, 2008 222 of 266Authorized for Public Release

Demand: Reserve Requirements

DIs meet reserve requirements by holding DIs meet reserve requirements by holding currency in vaults and ATMs reserve balances at a Federal Reserve Bank balances at a correspondent bank

No remuneration, so DIs try to reduce required t th l l f lt h d b l threserves to the level of vault cash and balances they

would hold if there were no requirements sweep programs reduce reservable depositsp p g p only 1,500 of 17,000 DIs need to hold reserve balances required reserve balances ≈ 0.1% of total deposits

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 9 of 52

April 29–30, 2008 223 of 266Authorized for Public Release

Demand: Contractual Clearing Balances

Many DIs want working balances larger than their Many DIs want working balances larger than their required reserve balances to clear Fedwire and other payments to provide a cushion against overnight overdrafts

Thousands of DIs hold contractual clearing balances accrue “earnings credits” at 80% of 3-month T-bill rate credits can be used only to offset fees for priced services

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 10 of 52

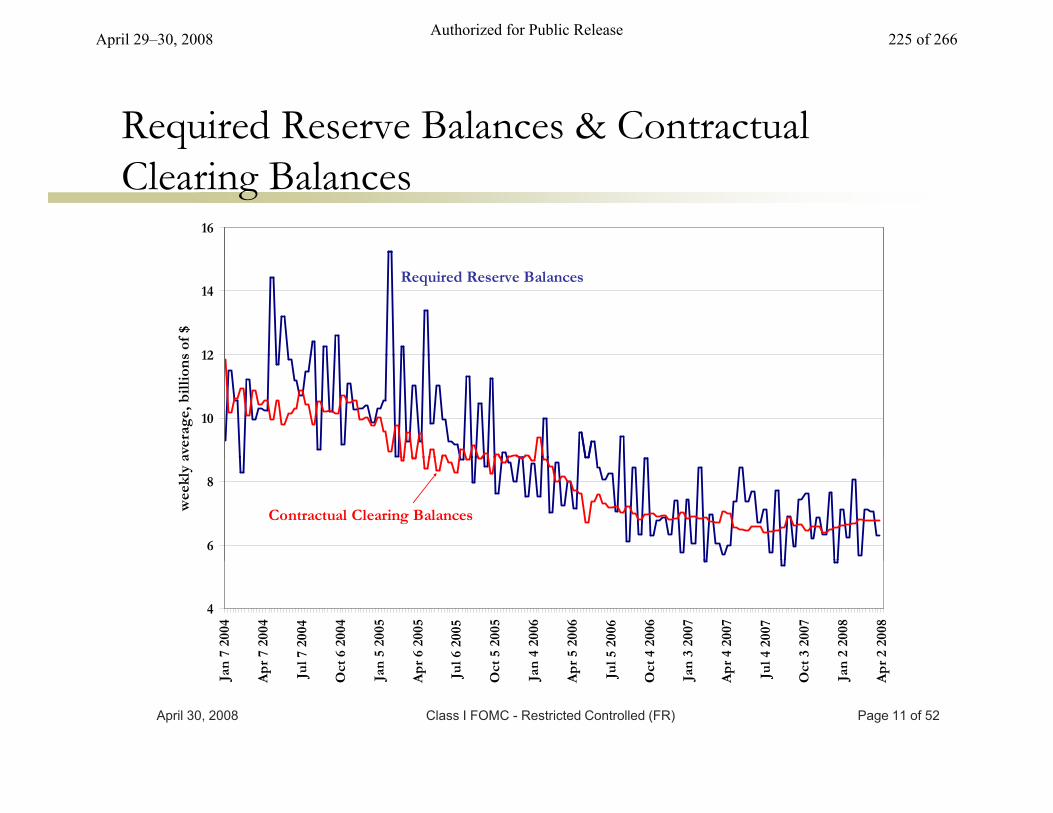

April 29–30, 2008 224 of 266Authorized for Public Release

Required Reserve Balances & Contractual

16

Clearing Balances

12

14

s of

$

Required Reserve Balances

10

12

aver

age,

bil

lion

s

6

8

wee

kly

a

Contractual Clearing Balances

4

n 7

200

4

r 7

2004

l 7 2

004

t 6

2004

n 5

200

5

r 6

2005

l 6 2

005

t 5

2005

n 4

200

6

r 5

2006

l 5 2

006

t 4

2006

n 3

200

7

r 4

2007

l 4 2

007

t 3

2007

n 2

200

8

r 2

2008

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 11 of 52

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

April 29–30, 2008 225 of 266Authorized for Public Release

Role of Required and Contractual Balances

Establish a predictable lower bound on period Establish a predictable lower bound on period-average demand for balances levels of required & contractual balances are set before each

reserve maintenance period

Averaging provision, carry-over, & clearing band make demand for balances interest elasticmake demand for balances interest-elastic until final day of maintenance period

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 12 of 52

April 29–30, 2008 226 of 266Authorized for Public Release

Demand: Excess Reserves

Large DIs seek to hold zero excess reserves on avg Large DIs seek to hold zero excess reserves on avg. but level varies widely from day to day, reflecting volume of

Fedwire payments

Small DIs hold $1.5 billion of ex. res. on avg. may need a cushion against overdrafts but not use priced

services so contractual clearing balance unappealingservices, so contractual clearing balance unappealing

Total balances (required + clearing + excess) vary between $10 and $25 billion per day in normal times;between $10 and $25 billion per day in normal times; wider variation since August

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 13 of 52

April 29–30, 2008 227 of 266Authorized for Public Release

Depository Institutions’ Total Balances

(daily, January 2007 to March 2008)55

at Federal Reserve Banks

45

50

55

30

35

40

ions

of $

15

20

25billi

5

10

1/07

6/07

1/07

5/07

2/07

7/07

1/07

6/07

1/07

6/07

1/07

5/07

0/07

5/07

0/07

4/07

9/07

3/07

8/07

3/07

28/

02/

077/

072/

0727

/0

1/08

6/08

0/08

5/08

1/08

6/08

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 14 of 52

1/ 1/1 6

1/3

2/1 5

3/2

3/17

4/ 4/1 6

5/ 5/1 6

5/3

6/1 5

6/30

7/15

7/30

8/14

8/29

9/13

9/28

10/

1310

/2

11/

1211

/27

12/

1212

/2

1/1

1/2 6

2/10

2/25

3/1

3/2 6

April 29–30, 2008 228 of 266Authorized for Public Release

Daylight Credit Reduces Demand for Balances

Fedwire processes > 0 5 million interbank payments Fedwire processes > 0.5 million interbank payments (with a value of ≈ $2.5 trillion) per day

Rather than holding large non-interest-bearing Rather than holding large non-interest-bearing balances at the Fed, DIs make heavy use of daylight credit to clear interbank payments. sum of end-of-minute overdrafts averages ≈ $60 billion per

day

Proposed revision to PSR Policy may further reduce Proposed revision to PSR Policy may further reduce demand for balances Fed now charges 36 basis points/yr for daylight credit

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 15 of 52

proposal would make collateralized daylight credit free

April 29–30, 2008 229 of 266Authorized for Public Release

Supply of Balances

Desk’s tries to keep S = D to keep ffr = target Desk s tries to keep S = D to keep ffr = target Desk seeks to offset changes in autonomous factors and

discount window credit that affect supply of balances also seeks to accommodate changes in demand

Outright purchases/sales, plus 14- & 28-day repo, supply a base of balances < projected demandsupply a base of balances < projected demand

Temporary open market operations add (or drain) balances almost every daybalances almost every day

Desk trades with 20 primary dealers interbank markets distribute balances

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 16 of 52

interbank markets distribute balances

April 29–30, 2008 230 of 266Authorized for Public Release

Supply: Autonomous Factors and D.W. Credit

Unanticipated changes in autonomous factors can Unanticipated changes in autonomous factors can make supply of balances differ from projected level currency in circulation float Treasury balance (Treasury deposits at FRBs) foreign repo pool foreign repo pool

Unexpected changes in PDCF credit also can make supply of balances differ from projectionpp y p j Changes in TAF credit are known in advance, and offset

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 17 of 52

April 29–30, 2008 231 of 266Authorized for Public Release

Supply: Temporary Open Market Operations

Desk executes repo almost every day Desk executes repo almost every day Size typically from $2 billion to $20 billion Maturities from 1 to 7 days, depending on persistence of

projected need Daily o.m.o. are in addition to 14-day & 28-day repo

Replacing maturing repo with larger repo adds to Replacing maturing repo with larger repo adds to supply of balances

Replacing maturing repo with smaller repo (or none) Replacing maturing repo with smaller repo (or none) reduces supply of balances Reverse repo to drain balances are rare

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 18 of 52

April 29–30, 2008 232 of 266Authorized for Public Release

How well does our current approach work?

In normal times current approach usually keeps In normal times, current approach usually keeps effective funds rate close to target

But current approach allows larger deviations during But current approach allows larger deviations during periods of stress in interbank markets

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 19 of 52

April 29–30, 2008 233 of 266Authorized for Public Release

Effective FFR minus Target:

(daily, January 2007 to March 2008)0.4

Normal Times vs. Market Turmoil

0

0.2

0.4

-0.4

-0.2

cen

tag

e p

oin

ts

-1

-0.8

-0.6

per

c

-1.2

an 1

200

7

n 1

9 20

07

eb 8

200

7

b 2

8 20

07

ar 2

0 20

07

Ap

r 9

2007

pr

27 2

007

y 17

200

7

un

6 2

007

n 2

6 20

07

ul 16

200

7

ug

3 2

007

g 2

3 20

07

p 1

2 20

07

Oct

2 2

007

ct 2

2 20

07

ov

9 20

07

v 29

200

7

c 19

200

7

an 8

200

8

n 2

8 20

08

b 1

5 20

08

ar 6

200

8

ar 2

6 20

08

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 20 of 52

Ja Jan

Fe

Feb

Ma A Ap

May Ju Jun

Ju Au

Au

g

Sep O Oc No

No

v

Dec Ja Jan

Feb M Ma

April 29–30, 2008 234 of 266Authorized for Public Release

Equilibrium in the Federal Funds Market (1)

DIs’ demand for balances varies from day to day DIs demand for balances varies from day to day, reflecting reserve requirements, clearing balance commitments, and volume of payments

In morning, fed funds usually trade at or near target rate because DIs expect Desk to supply enough b l t k ff t tbalances to make ffr ≈ target a firm or soft rate signals excess demand or supply

Desk conducts open market operation to make day’s Desk conducts open market operation to make day s projected supply = forecast of quantity demanded

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 21 of 52

April 29–30, 2008 235 of 266Authorized for Public Release

Equilibrium in the Federal Funds Market (2)

As day progresses autonomous factors and demand As day progresses, autonomous factors and demand are realized; banks make and settle payments and trade fed funds; and actual ffr is determined

Desk cannot adjust S of balances late in day, so if realized S ≠ actual D, ffr will deviate from target because balances are not remunerated, an excess supply

can push ffr down to zero in the afternoon reluctance to borrow means an excess demand can cause ffr

to rise above primary credit rate in the afternoon a small volume of trades at very low or very high rates can

make effective (daily average) ffr deviate from target

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 22 of 52

April 29–30, 2008 236 of 266Authorized for Public Release

Burdens Imposed by Current Approach

Reserve requirements deposit reports zero interest Reserve requirements, deposit reports, zero interest on balances impose unnecessary burdens on society Reserves tax from zero interest on required reserve

balances ≈ $380 million in 2006, $340 million in 2007

Sweep programs and other methods DIs use to minimize reserves tax waste real resourcesminimize reserves tax waste real resources

High costs to collect/process deposit data and to monitor/ensure compliance with complex rules formonitor/ensure compliance with complex rules for required reserves and contractual clearing balances

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 23 of 52

April 29–30, 2008 237 of 266Authorized for Public Release

Strengths & Shortcomings of U.S. Approach

Usually keeps funds rate close to target in normal Usually keeps funds rate close to target in normal times but allows occasional large deviations

Allows larger and more frequent deviations from Allows larger and more frequent deviations from target during periods of market stress Large deviations reflect: projection errors; reluctance to

b ti f b l i bilit t dj tborrow; no remuneration of balances; inability to adjust supply of balances late in day

Even sophisticated market participants find current Even sophisticated market participants find current approach hard to understand, somewhat opaque

Reserve requirements & zero interest on balances

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 24 of 52

impose burdens, but are not needed to hit ffr target

April 29–30, 2008 238 of 266Authorized for Public Release

Core Structural Elements

Balance Targets: Mandatory Voluntary or None Balance Targets: Mandatory, Voluntary, or None

Bands Around Target Balances

Maintenance Period: Single or Multiple Day

Funds Rate Corridor Upper Bound: Standing Lending Facility Lower Bound: Interest on Excess Reserves (or Redeposit

Facility)

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 25 of 52

April 29–30, 2008 239 of 266Authorized for Public Release

Possible Limitations: Stigma and the Standing Lending Facility Standing lending facility should, in theory, place a cap on the

federal funds rate.

But stigma may impair the effectiveness of the cap.

P t ti ll d i ff ti f t th t l h il Potentially undermines effectiveness of systems that rely heavily on standing lending facility. Disadvantages institutions that are the least inclined to borrow.

AverageAverage Spread

Number Trade overof Size Primary Credit Rate

(March 24 - April 24)Overnight Borrowing in the Federal Funds Market

Institution Name Trades ($ Millions) (Basis Points)Citibank 108 340 18Bank of America 102 338 35JP Morgan Chase 185 345 44Wachovia 7 239 100State Street 4 312 31Bank of New York 43 381 23

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 26 of 52

Bank of New York 43 381 23Wells Fargo 32 199 73

April 29–30, 2008 240 of 266Authorized for Public Release

Multiple- and Single-Day Systems

Multiple Day Systems Multiple Day Systems Options 1 and 2 Intraperiod arbitrage to stabilize the funds rate

Single-Day Systems Options 3-5 Standing facilities and rates of remuneration to stabilize the

funds rate.

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 27 of 52

April 29–30, 2008 241 of 266Authorized for Public Release

Option 1: Remunerate Required and Excess Reserve Balances

Key Structural Featuresy Standing lending facility sets upper

bound on funds rate Interest on excess reserves sets

lower bound on funds rate Mandatory requirements and

two-week maintenance period

How it Should Work Downward sloping demand curve on last

day of maintenance period Demand curve on earlier days in the

period relatively flat at the target rate over a wide range.o e a de a ge Banks can substitute balances across

days of the maintenance period

Desk adjusts supply of balances each day to address daily demands and maintenance-period average needs.

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 28 of 52

p g

April 29–30, 2008 242 of 266Authorized for Public Release

O i 2 V l B l TOption 2: Voluntary Balance Targets

Key Structural Featuresy Voluntary Balance Target Multiple-day Period (between FOMC

meetings) Relatively narrow target bandy g Funds Rate Corridor

How it Should WorkB i h i i il t ti 1 Basic mechanics similar to option 1

Longer maintenance period should allow more scope for substitution of balances across days of the period

Might require less fine-tuning of daily Might require less fine-tuning of daily balances but…

Key question is the magnitude of voluntary requirements Low level could limit scope for

substitution and arbitrage

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 29 of 52

substitution and arbitrage

April 29–30, 2008 243 of 266Authorized for Public Release

Option 3: Simple Corridor

Key Structural Featuresy No target balance Narrow symmetric funds rate corridor

How It Should Work Downward sloping demand for reserves

within the corridor Demand for reserves stems from

precautionary motive to avoid overnight overdrafts

Staff would estimate daily demand at the target rate

Desk would supply daily balances to meet estimated demand at target rate

Demand curve could be rather steep Funds rate could be volatile within the

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 30 of 52

corridor

April 29–30, 2008 244 of 266Authorized for Public Release

O i 4 Fl i h Hi h B lOption 4: Floor with High Balances

Key Structural Featuresy No target balance Asymmetric funds rate corridor

Remuneration rate set just below target funds rate

High balances to keep funds rate near the floor of the corridor

How it Should Work Desk provides an ample supply of

balances each day ($50 billion) Funds rate should trade near the lower

bound of the corridor Fl ct ations in reser e factors sho ld Fluctuations in reserve factors should

have little impact on funds rate Could reduce daylight overdrafts Potential for strategic behavior?

Minimal costs in holding large reserve

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 31 of 52

Minimal costs in holding large reserve position

April 29–30, 2008 245 of 266Authorized for Public Release

Option 5: Voluntary Daily Target with Target BandKey Structural Elements Voluntary Daily Balance Target Relatively wide target band Upper bound on full remuneration of

balances Penalty for shortfalls Wide funds rate corridor

How it Should WorkHow it Should Work Demand curve relatively flat within the

target band But downward sloping near the

boundaries of the target band.

D k li b l h d l Desk supplies balances each day close to the midpoint of the target band.

Key Questions: How large would aggregate level of

targets be??

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 32 of 52

How wide to set target band?

April 29–30, 2008 246 of 266Authorized for Public Release

General Issues

Competitive issues Competitive issues Restrictions on payment of interest on demand deposits

Appropriate setting of remuneration rate Appropriate setting of remuneration rate Somewhat below target rate to reflect risk premium

Governance: FOMC and Board Roles Governance: FOMC and Board Roles FOMC target rate and Board-determined remuneration rate

Transition Moving from current system to new system could be

complicated

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 33 of 52

April 29–30, 2008 247 of 266Authorized for Public Release

Assessment of Different Options: Objectives

Reduce burdens and deadweight losses Reduce burdens and deadweight losses

Enhance monetary policy implementation

Promote efficient and resilient money markets and government securities markets

P t ffi i t d ili t t t Promote an efficient and resilient payments system

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 34 of 52

April 29–30, 2008 248 of 266Authorized for Public Release

Option 1: Remunerate Required and Excess Reserve p qBalances

Advantages: Advantages: Easy to implement given where we are now Tested basic framework that would represent an

improvement over the status quo

Disadvantages:R t i t d i i t ti b d Retains current administrative burdens

Limited flexibility in reserve averaging parameters

Open Issues Open Issues Uncertain by how much required reserve balances would

rise

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 35 of 52

April 29–30, 2008 249 of 266Authorized for Public Release

Option 2: Voluntary Balance Targets

Advantages: Advantages: Significant reduction in administrative burdens Also a tested basic framework Offers more flexibility in reserve targets

Disadvantages: Retains some administrative burden, for both DIs and FRS

Open issues:Id tif i t f l t t t th t i ld ffi i t Identifying a system of voluntary targets that yields sufficient balances and is administratively workable

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 36 of 52

April 29–30, 2008 250 of 266Authorized for Public Release

Option 3: Simple Corridor

Advantages: Advantages: Eliminates administrative burdens of reserve

requirements/targets and reserve maintenance periods Should keep funds rate within a narrow corridor Should keep funds rate within a narrow corridor

Disadvantages: Funds rate would be more volatile within the corridor Heavy use of standing facilities under a narrow corridor

increases role of Fed as market intermediary

Open issues: Open issues: Would our lending facility be sufficiently effective in limiting

rates on the upside? May need a better ability to make late-day reserve

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 37 of 52

May need a better ability to make late day reserve adjustments

April 29–30, 2008 251 of 266Authorized for Public Release

Option 4: Floor with High Balances Advantages:

Eli i d i i i b d f Eliminates administrative burdens of reserve requirements/targets and maintenance periods

Sharply reduces account management burden on DIsS bstantial balance sheet/reser e mo ements ma ha e little Substantial balance sheet/reserve movements may have little impact on rates (although a possible double-edged sword)

Disadvantages: A radical change from the current framework, with limited

experience of other central banks upon which to base informed judgments

Open issues: Implications for reserve demand and the functioning of the

interbank market, under both normal circumstances and periods of stress

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 38 of 52

periods of stress

April 29–30, 2008 252 of 266Authorized for Public Release

Option 5: Voluntary Daily Target with Clearing Band

Advantages: Advantages: Significant reduction in administrative burdens Reserve smoothing parameters (voluntary target levels and

bands) may be very flexible

Disadvantages:R t i d i i t ti b d f b th DI d FRS Retains some administrative burden, for both DIs and FRS

Limited experience with some features of this framework

Open issues: Open issues: Identifying a system of voluntary targets that yields sufficient

balances and is administratively workable

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 39 of 52

April 29–30, 2008 253 of 266Authorized for Public Release

Overall Assessment Against Objectives

1 Reduce burdens and deadweight losses1. Reduce burdens and deadweight losses All options eliminate the reserve tax, either by remunerating

required reserves or eliminating requirements But some options have fewer administrative burdens than

others

2 Enhance monetary policy implementation2. Enhance monetary policy implementation All options set a floor for the fed funds rate, and most

introduce additional features to help control rate volatilityB t ti h fl ibl t th t But some options may have more flexible parameters that could be adjusted during periods of stress

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 40 of 52

April 29–30, 2008 254 of 266Authorized for Public Release

Overall Assessment Against Objectives

3 Promote efficient and resilient money markets and3. Promote efficient and resilient money markets and government securities markets Most options would still rely on active short-term markets for

the distribution of liquidity But there are possible differences in the Fed’s role as market

intermediary, and in the impact on the interbank market

4. Promote an efficient and resilient payments system All options are consistent with proposed PSR policy changes But some could yield a higher level of reserves than others

as an alternative to daylight credit

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 41 of 52

April 29–30, 2008 255 of 266Authorized for Public Release

Interest on Reserves in a Broader Context

Consider as part of process of improving overall Consider as part of process of improving overall monetary policy framework

Current system works well during normal times Current system works well during normal times

Less robust during times of stress

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 42 of 52

April 29–30, 2008 256 of 266Authorized for Public Release

Weaknesses of Current Monetary Policy Framework

Volatility of the federal funds rate Volatility of the federal funds rate

PCF rate not a binding ceiling

Potential loss of control of federal funds rate after large reserve adds

Li it d bilit t t i d i t Limited ability to constrain upward pressure in term funding rates

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 43 of 52

April 29–30, 2008 257 of 266Authorized for Public Release

Federal Funds Rate Volatility (I)Daily Average less Target Federal Funds Rate: March 2007 to Present

0.000.100.200.30

-0.50-0.40-0.30-0.20-0.10

Perc

ent

-1 00-0.90-0.80-0.70-0.600.50P

-1.20-1.101.00

3/1/

2007

4/1/

2007

5/1/

2007

6/1/

2007

7/1/

2007

8/1/

2007

9/1/

2007

10/1

/200

7

11/1

/200

7

12/1

/200

7

1/1/

2008

2/1/

2008

3/1/

2008

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 44 of 52

April 29–30, 2008 258 of 266Authorized for Public Release

Federal Funds Rate Volatility (II)Daily Fed Funds Rates and Ranges: March 2008 to Presenty g

5PCF spread to target rate lowered to 25bp;PDCF introduced

(10%)(6%)

3

4

ent

1

2

Perc

0

1

3/3/08 3/17/08 3/31/08 4/14/08

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 45 of 52

Effective Rate Fed Funds Target Rate Primary Credit Rate

April 29–30, 2008 259 of 266Authorized for Public Release

Implications for Interest on Reserves Consider in tandem with changes to overall

f kframework Be willing to make significant adjustments to facilitate

monetary policy implementation and market y p y probustness

Options 1 and 2 eliminate reserve tax distortions and Option 2 eliminates most of regulatory burdenOption 2 eliminates most of regulatory burden

Option 2 has several advantages: Less regulatory burden, voluntary Averaging dampens shocks Considerable experience with this type of framework—

similarities with the contractual clearing program Bank of England has been using it successfully

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 46 of 52

Bank of England has been using it successfully

April 29–30, 2008 260 of 266Authorized for Public Release

Implications for Interest on Reserves

But other proposals go further in altering But other proposals go further in altering fundamental framework

Option 5 is potentially more robust than Option 3 or Option 5 is potentially more robust than Option 3 or Option 4: Flexible in that number of parameters that can be

dj t d idth f id d i f l tadjusted—width of corridor and size of voluntary reserve band

As a result, it could be adjusted readily in response to i d/ h i k t ditiexperience and/or changes in market conditions

But less empirical evidence available as no other central bank has adopted such a model

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 47 of 52

April 29–30, 2008 261 of 266Authorized for Public Release

Recommendation – Interest on Reserves

Reserve maintenance periods have advantages and Reserve maintenance periods have advantages and disadvantages

Smoothing reduces volatility but shocks get Smoothing reduces volatility, but shocks get dispersed through the reserve maintenance period

Single day systems, reserve shocks do not persist Single day systems, reserve shocks do not persist

Recommendation: Develop best proposal within each broad class

Focus on Options 2 and 5

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 48 of 52

April 29–30, 2008 262 of 266Authorized for Public Release

Next Steps Identify workable systems of voluntary targets for reserves Identify workable systems of voluntary targets for reserves,

needed for either option 2 or 5 Set clear objectives for aggregate size and distribution across DIs Determine how such a system would be applied to a y pp

heterogeneous banking system

Critically assess relative merits of maintenance periods vs. daily clearing bands as a source of reserve management flexibility and optimum sizes of maintenance period and clearing band width

Define the optimal width of a rate corridor under both options understand implications for rate dynamics and the functioning of the p y g

interbank market under normal conditions and during times of stress

Assess compatibility of either option with possible changes in

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 49 of 52

counterparties and collateral for central bank credit operations

April 29–30, 2008 263 of 266Authorized for Public Release

Possible Timeline (I)

Apr 08 Board announces System studying approaches toApr-08 Board announces System studying approaches to policy implementation and will consult with public

May-08 Publish white paper on possible approach(es) for y p p p pp ( )three months of public comment

Apr-08 to Nov-08 Intensive study of two options (options 2 and 5) –bli t lt ti ith S tpublic comment consultation with System groups

and publicOct-08 FRBNY conference on monetary policy

implementation

Dec-08 Staff proposes specific approach to Board and FOMC

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 50 of 52

FOMC

April 29–30, 2008 264 of 266Authorized for Public Release

Possible Timeline (II)

Jan 09 Board and FOMC discussion; preliminary decisionJan-09 Board and FOMC discussion; preliminary decision on approach

Jan-09 to Jul-09 Staff develops detailed proposal—further consultation with System groups and publicconsultation with System groups and public

Aug-09 Board publishes final proposal in Federal Register for public comment

Oct-09 Board publishes rules

Oct-09 to Oct-11 Prepare for implementationOct 09 to Oct 11 Prepare for implementation

Oct-11 Implement

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 51 of 52

April 29–30, 2008 265 of 266Authorized for Public Release

We seek your guidance on several key issues

Criteria for the evaluation of policy options Criteria for the evaluation of policy options In particular, the weight to place on reduction in burden and

distortions associated with reserve requirements

Specific options that should be studied further

Process and timeline going forwardg g

Interaction with other aspects of policy implementation

April 30, 2008 Class I FOMC - Restricted Controlled (FR) Page 52 of 52

April 29–30, 2008 266 of 266Authorized for Public Release