Benchmarking Help Center Guide - Institute for Market Transformation

F i n a n c i a l B e n c h m a r k i n g a n d M a r k e t T r e n d s f o r G o v e r n m e n t C o n t r a c t o r s :

H o w D o e s Y o u r C o m p a n y C o m p a r e ?

Presented by: Lynne Gummo, CPAChristine Williamson, CPA

Partners, CohnReznickJune 14, 2017

P L E A S E R E A D

This presentation has been prepared for information purposes and general guidance only and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice.

No representation or warranty (express or implied) is made as to the accuracy or completeness of the information contained in this publication, and CohnReznick LLP, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

This presentation and its content are the property of CohnReznick LLP and are protected by applicable copyright laws. Any unauthorized use of the information herein will be considered a violation of CohnReznick LLP’s intellectual property rights. Unless stated otherwise herein, no part of this presentation may be copied, distributed, or published, in whole or in part, without the prior written agreement of CohnReznick LLP.

1

A G E N D A

2

• Current Environment

• Demographics

• Financial Benchmarking

• FTE Benchmarking

• Contract Activity

• DCAA TrendsFinancial Ratios• Key Take Aways

Trump-onomics

Growing internal & external pressures currently impacting

theGC industry

Federal Budget Passed Through September 2017

Government’s Need for Greater Efficiencies

Impending Tax ReformPricing Pressure

Middle Market No-Mans Land

Increased Competition

Need to Grow Revenue & Profits

Increasing interest rates Increasing

combinations and M&A activity

C U R R E N T E N V I R O N M E N T

3

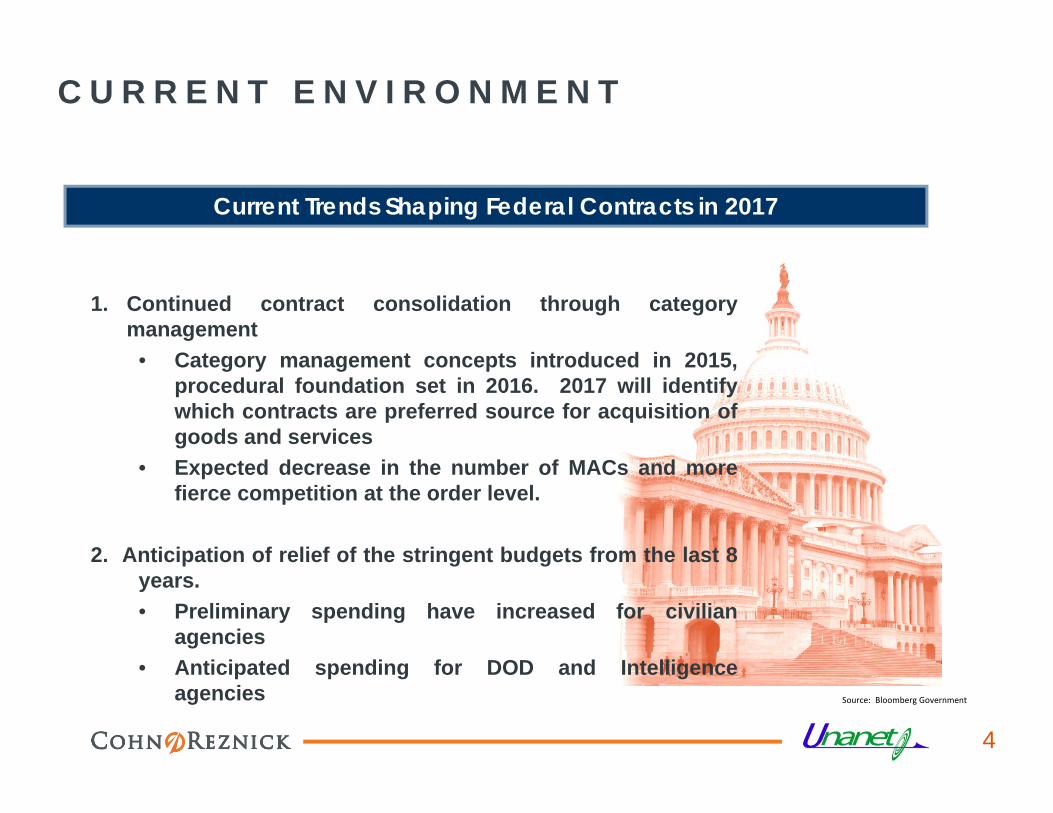

1. Continued contract consolidation through categorymanagement

• Category management concepts introduced in 2015,procedural foundation set in 2016. 2017 will identifywhich contracts are preferred source for acquisition ofgoods and services

• Expected decrease in the number of MACs and morefierce competition at the order level.

2. Anticipation of relief of the stringent budgets from the last 8years.• Preliminary spending have increased for civilian

agencies• Anticipated spending for DOD and Intelligence

agencies

Current Trends Shaping Federal Contracts in 2017

Source: Bloomberg Government

C U R R E N T E N V I R O N M E N T

4

3. Increased agency use of Simplified AcquisitionProcedures

• Simplified Acquisition Procedures (SAP) spendinghas grown.

• Threshold amounts have changed and agenciesrelying on the SAP competition procedure to avoidprotest delays.

Current Trends in the Federal Market Place

Source: Bloomberg Government

C U R R E N T E N V I R O N M E N T

5

4. Increase in compliance and accountability• Contractors are required to submit various data

points monthly due to transactional datareporting rule

• Agencies must standardize their spendingreports to comply with DATA Act by May 2017.

Current Trends in the Federal Market Place

Source: Bloomberg Government

C U R R E N T E N V I R O N M E N T

6

5. Contractors will continue to divest, merge andrestructure

• Contractors need to change to protect profits amidhigher competition.

• Strategic sourcing, aggressive small-businessutilization strategies and continued use of LPTAbid evaluation strategies.

• Companies will restructure internal operations toreduce costs. Many operating in a “virtual”environment.

• Large Prime Contractors will separate lower-margin from higher margin work. Many shiftingfocus to weapon systems.

• Combinations, spin-offs and M&A activity on therise

• Increase focus on the use of Joint Ventures

Current Trends in the Federal Market Place

Source: Bloomberg Government

C U R R E N T E N V I R O N M E N T

7

S u r v e y R e s p o n d e n t D e m o g r a p h i c s

9

S E R V I C E T Y P E S

- Engineering Services

- Custom Computer Programs

- Computer System Design

- Other Computer Related Services

- Administrative Management

- Human Resources Consulting

- R & D, Physical Engineering & Life Sciences- Other Professional Scientific and Technical

E N T I T Y S T R U C T U R E

10

O W N E R S H I P

11

34%

33%

33%

ESOP

100%

26%-49%

less 25%

72%

14%

14%PE

100%

26%-49%

less 25%

C O N T R A C T T Y P E S

12

21%

40% 39%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Cost Plus Time and Material Fixed Price

A G E N C I E S

13

A C C O U N T I N G S Y S T E M S

14

F i n a n c i a l B e n c h m a r k i n g

D I R E C T C O S T S

Direct Labor

Subcontract Labor

Other Direct Costs

Gross Margin

Costs as a % of Revenue

16

D I R E C T C O S T S A S A % O F R E V E N U E

17

D I R E C T L A B O R A S A % O F R E V E N U E

18

33%

25%23%

38%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

S U B C O N T R A C T O R A S % O F R E V E N U E

19

18%

28%

17% 18%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

O D C A S A % O F R E V E N U E

20

3%7%

9%4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

G R O S S M A R G I N A S A % O F R E V E N U E

21

45%

31%

24%

29%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

I N D I R E C T C O S T S

Fringe Costs

Indirect Labor

Net Profit

Health Insurance Expense

Rent Expense

Business Development Expense

EBITDA

Costs as a % of Revenue

22

I N D I R E C T C O S T S A S A % O F R E V E N U E

23

I N D I R E C T C O S T S A S A % O F R E V E N U E

24

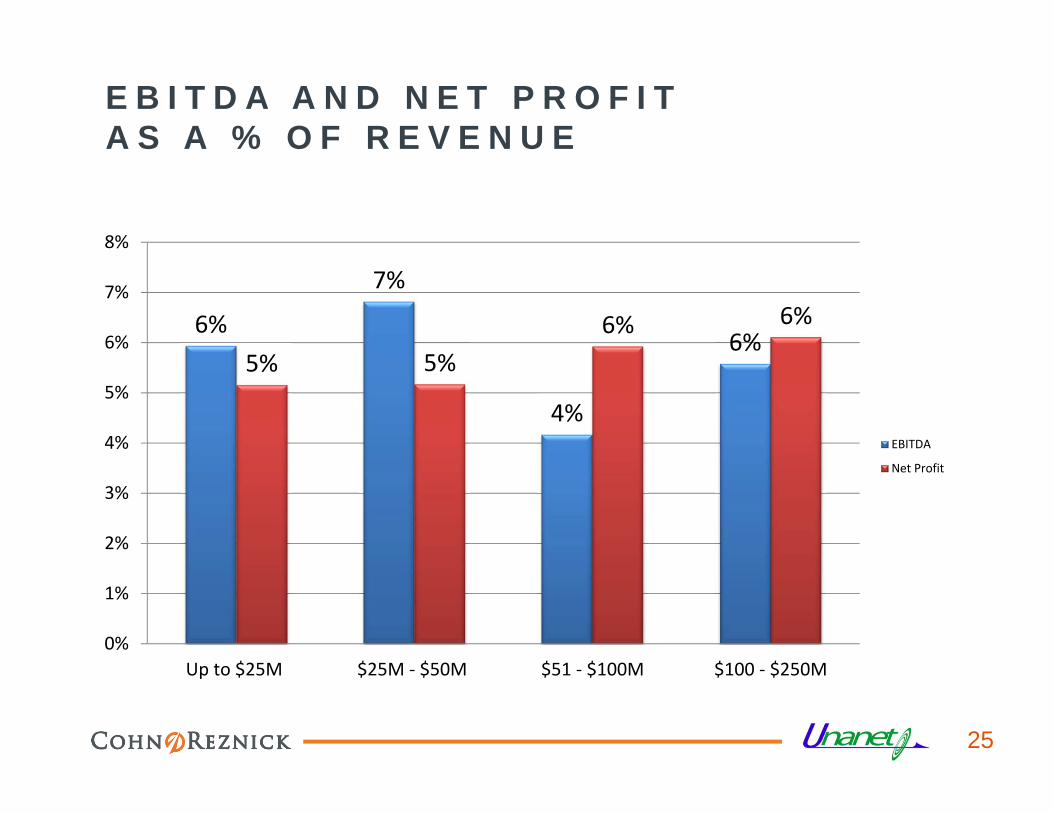

E B I T D A A N D N E T P R O F I T A S A % O F R E V E N U E

25

6%

7%

4%

6%5% 5%

6% 6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

EBITDA

Net Profit

F R I N G E C O S T S A S A % O F R E V E N U E

26

17%19%

16%14%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

I N D I R E C T L A B O R A S A % O F R E V E N U E

27

10%9%

16%

3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

N E T P R O F I T A S A % O F R E V E N U E

28

5.2% 5.2%

5.9% 6.1%

4.6%

4.8%

5.0%

5.2%

5.4%

5.6%

5.8%

6.0%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

H E A L T H I N S U R A N C E A S A % O F R E V E N U E

29

4%

3%3%

3%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

R E N T A S A % O F R E V E N U E

30

2%2%

3%2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

B D E X P E N S E A S A % O F R E V E N U E

31

2%

1%

6%

1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Up to $25M $25M - $50M $51 - $100M $100 - $250M

E B I T D A A S A % O F R E V E N U E

32

I N D I R E C T R A T E S

Fringe

Overhead – Government Site

Overhead – Contractor Site

Material/Subcontractor Handling

General & Administrative

Wrap rate without fee

By Revenue Segment

33

F R I N G E R A T E

34

9%13%

9%13%

9%

9%

9%

13%

4%

4%

4%

4%

0%

5%

10%

15%

20%

25%

30%

35%

30% or less 31% - 35% 36%-40% 41% +

$100 - $250M

$51 - $100M

$25M - $50M

Up to $25M

18% 30% 26% 26%

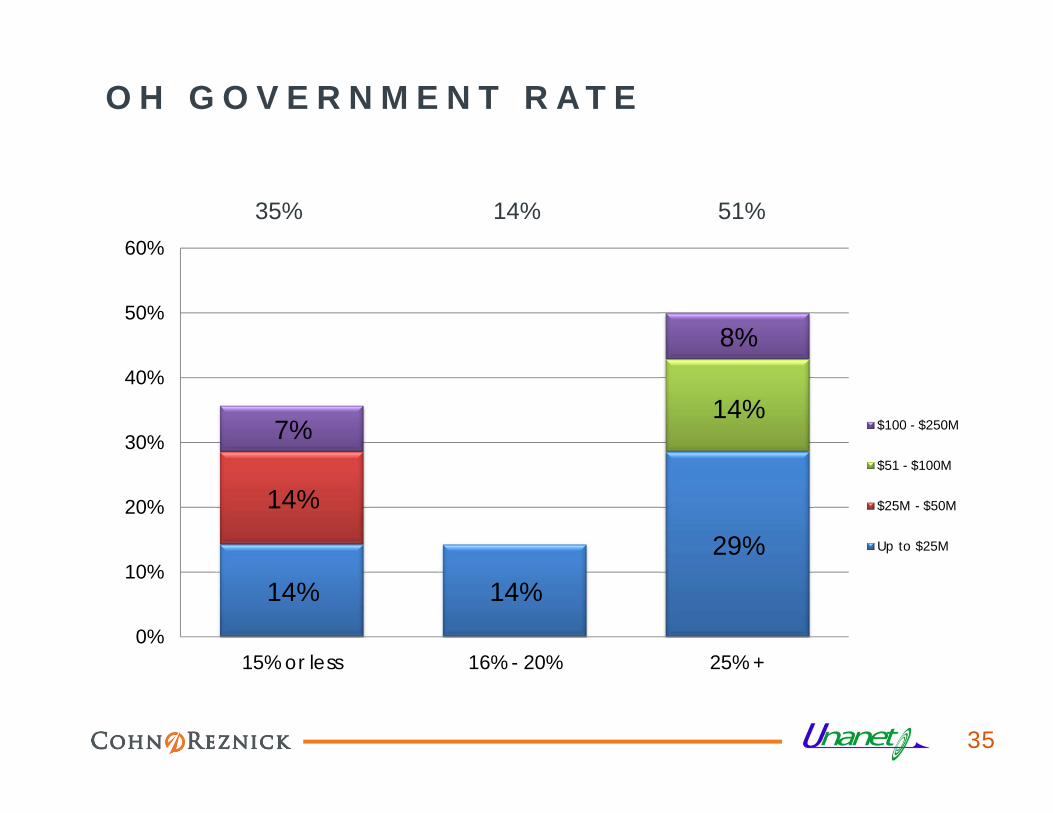

O H G O V E R N M E N T R A T E

35

14% 14%

29%

14%

14%7%

8%

0%

10%

20%

30%

40%

50%

60%

15% or less 16% - 20% 25% +

$100 - $250M

$51 - $100M

$25M - $50M

Up to $25M

35% 14% 51%

O H C O N T R A C T O R R A T E

36

18%28%

6%

6%

6%

6%

12%

6%

12%

0%

10%

20%

30%

40%

50%

60%

70%

20% or less 21% - 30% 31% +

$100 - $250M

$51 - $100M

$25M - $50M

Up to $25M

18% 24% 58%

H A N D L I N G R A T E

37

17% 67% 16%

25%

8%17%

25%

8%

17%

0%

10%

20%

30%

40%

50%

60%

70%

1% or less 2% - 5% 6% +

$100 - $250M

$51 - $100M

$25M - $50M

Up to $25M

G & A R A T E

38

9%13%

9%13%

4%

22%

9%4%

5%

4%

4%

4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

10% or less 11% - 15% 16%-20% 21% +

$100 - $250M

$51 - $100M

$25M - $50M

Up to $25M

17% 40% 22% 21%

W R A P R A T E W I T H O U T F E E( U S I N G G O V E R N M E N T R A T E )

39

15%

5%

15%10%

10%

15%

10%

5%

5%10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

1.51 - 1.75 1.76 - 2.0 2.01 - 2.25 2.26 +

$100 - $250M

$51 - $100M

$25M - $50M

Up to $25M

35% 20% 30% 15%

F T E B e n c h m a r k i n g

F T E A N A L Y S I S

Revenue per FTE

FTEs Per Function

By Revenue Segment

41

R E V E N U E P E R F T E

42

$196,866

$245,779

$221,745

$168,146

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

Up to $25M $25M - $50M $51 - $100M $100 - $250M

F T E S P E R F U N C T I O N

43

2.0 1.2 0.6 1.4 1.5 2.3 1.2

4.6

2.7 1.1

2.3

9.3

3.8 7.4

8.0

4.0

1.0

4.0

4.0

9.0 1.7

9.0

9.3

6.0

13.0

5.0

8.3

6.7

-

5.0

10.0

15.0

20.0

25.0

Accounting HR Recruiting IT Contracts BD ProjectControl

$100 - $250M

$51 - $100M

$25M - $50M

Up to $25M

C o n t r a c t A c t i v i t y

C O N T R A C T A C T I V I T Y

45

C O N T R A C T A C T I V I T Y

46

C O N T R A C T A C T I V I T Y

47

28

13

7 4

1 0 -

5

10

15

20

25

30

Active Bid Won Loss Delayed Protested

Up to $25M

Up to $25M

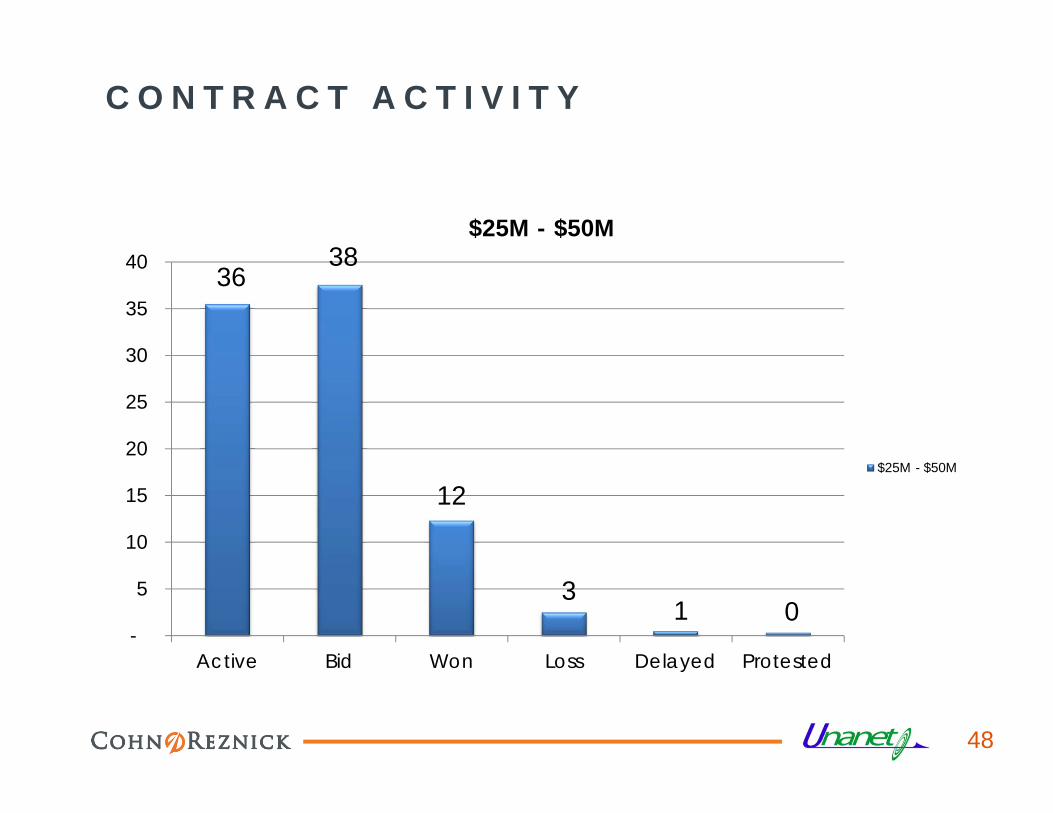

C O N T R A C T A C T I V I T Y

36 38

12

3 1 0

-

5

10

15

20

25

30

35

40

Active Bid Won Loss Delayed Protested

$25M - $50M

$25M - $50M

48

C O N T R A C T A C T I V I T Y

76 79

32 29

18

00

10

20

30

40

50

60

70

80

90

Active Bid Won Loss Delayed Protested

$51 - $100M

$51 - $100M

49

C O N T R A C T A C T I V I T Y

50

D C A A T r e n d s

D C A A T R E N D S

Types of DCAA Audits

Year Indirect Rates Audited Through

By Revenue Segment

52

T Y P E S O F D C A A A U D I T S I N 2 0 1 6

53

34%

11%

6%

11% 11% 11%

3%6% 6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

IncurredCost

Pre Award Purchasingsystem

AccountingSystem

Provisionalrates

Billing review ForwardPricing

Voucher Floor checks

D C A A T r e n d s

54

19%

35%

15%

8%

19%

4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2011 2012 2013 2014 2015 2016

Year Rates Audited Thru by DCAA

K E Y T A K E A W A Y S

Infrastructure (G&A) spending is up Be aware of the struggles of no-man’s land Government shifting to purchases thru MAC’s M&A is considered on the rise – lots of shoppers Monitor your wrap rate Use of the vertical income statement analysis Be prepared for any type of possible contract audit Monitor your largest indirect expenses Share results with management Begin budget process early to see where you co lands in comparison Its healthy to benchmark!

55

C O N T A C T I N F O R M A T I O N

Christine WilliamsonCohnReznick703-847-4412Christine.Williamson@cohnreznick.com

Lynne [email protected]

Donna [email protected]

56