FILE C3 PtY Appraisal of Bombay High Offshore ... No. 1569a-IN FILE C3 PtY Appraisal of Bombay High...

129

Report No. 1569a-IN FILE C3 PtY Appraisal of BombayHigh Offshore Development Project India June 10, 1977 Regional ProjectsDepartment South Asia Regional Office FOR OFFICIAL USE ONLY U Document of the World Bank This document hasa restricted distribution and may be usedby recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of FILE C3 PtY Appraisal of Bombay High Offshore ... No. 1569a-IN FILE C3 PtY Appraisal of Bombay High...

Report No. 1569a-IN FILE C3 PtYAppraisal of Bombay HighOffshore Development Project IndiaJune 10, 1977

Regional Projects DepartmentSouth Asia Regional Office

FOR OFFICIAL USE ONLY

U

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Except where otherwise indicated, all figures arequoted in Indian Rupees (Rs)

Rs 1.0 = US$0.111Rs 9.0 = US$1.00Rs 1,000,000 = US$111,111

WEIGHTS AND MEASURES

1 Metric Ton (mt) = 1,000 Kilograms (kg)1 Metric Ton (mt) = 2,204 Pounds1 Kilometer (km) = 0.62 Miles1 Ton of oil equivalent

(Toe) = 10 million Kilocalories1 American barrei (b) = 0.15899 Cubic meter

1 Cubic meter (m ) -= 6.289 Barrels1 Cubic foot (cf) = 0.02832 Cubic meter

All conversions from tons to barrels are based on a crudeoil of average specific gravity of 0.84, or 37 degrees API

PRINCIPAL ABBREVIATIONS AND ACRONYMS USED

GOI - Government of IndiaONGC - Oil and Natural Gas CommissionMPC - Ministry of Petroleum and ChemicalsMOF - Ministry of FinanceBHDP - Bombay High Development ProgramHPCL - Hindustan Petroleum Co. Ltd.FCI - Fertilizer Corporation of IndiaOIDB - Oil Industry Development BoardAOC - Assam Oil CompanyOIL - Oil India Ltd.LPG - Liquefied Petroleum GasBH - Bombay HighBN - Bassein North

l

INDIAN FISCAL YEAR

April 1 - March 31

-FOR OFFICIAL USE ONLY

INDIA

APPRAISAL OF BOMBAY HIGH OFFSHORE DEVELOPMENT PROJECT

Table of Contents

Page No.

SUMMARY AND CONCLUSIONS ........ . . . . ................. ......... . . . i-iii

I. INTRODUCTION ............................................ t .............. 1

II. BACKGROUND ..................................................... ... 0... 2

A. General ..... ..................... .... 2B. Past and Projected Demand and Supply

of Commercial Energy . ............. .. ......... . . 2

III. THE OIL AND GAS SECTOR .................................. 5

A. Historical Development ............ ................. 5B. Recent Developments ................................ 7

C. Longer-Term Perspectives ........................... 8D. The Role of the Bank ............................... 9

IV. THE PROGRAM AND THE PROJECT ............................. 9

A. Main Characteristics of the Bombay HighArea .......................................................... 9

B. The Development Program ................... *...* .... 10C. Status of Development .............................. 11D. The Project ........................................ 11E. Status of Engineering .......................... 12F. Cost Estimates ...... ............................... 13

G. Items Proposed for Bank Financing .................. 15H. Financing Plan ..................................... 16I. Project Execution, Supervision and Reporting ....... 16J. Procurement and Disbursement ............ ........... 18K. Right-of-Way and Land Acquisition ............. 18L. Operations and Training ........................ .. 18X. Ecology and Safety .19N. Project Risks. . 190. Further Expansion of the Bombay High Offshore Area 20

T his document has a restricted distribution and may be use by recipients only in the perforrnuie of their ofhciol duties. Its contents may not otherwise be disck3ed without World Bank authorization.|

-2-

Page No.

V. JUSTIFICATION .................................. . 00 .......... 20

A. General ............................... o......... ...o ....... .... o . 20B. Sector Objectives ... o ........ .... .. . .. ..... 21C. Justification of the Bombay High Offshore

Development Program ... ........................ 22D. Economic Justification ........................... 24

VI. THE OIL AND NATURAL GAS COMMISSION ..................... 26

A. General .. ...................... ... .... . . 26B. Organization and Management .. .......o .......... 26C. Operations .... ........ o. oo ...... o ............ 28Do Insurance .. .................... ..... . ...... oo. 29E. Finances ............. oo .... .... .... 29F. Audit ......... o...... ooo ........................ 29G. Prices . .. ...... o..o .............oo 30

VII. FINANCIAL ASPECTS ...o ...... .o... .. .... .... . ... .. o. . ..... 30

A. Introduction. .......... o....o ........o ....... 30B. Present Financial Position ......no.... ............. 31C. Financing Plan.. ........... . .. . . . . 32D. Future Finances ................... oo..o .......... 34

VIII. RECOMMENDATIONS ... o ..... o..oo ..... o.................... 35

I'

-3 -

LIST OF ANNEXES

1. Bank Group Projects in the Energy Sector2. Glossary of Technical Terms3. Past Commercial Energy Production and Consumption4. Energy Demand Projections5. Development of Energy Resources of India6. Past Petroleum Production and Consumption7. Development of Hydrocarbon Resources in India8. Evaluation of Bombay High and Bassein Reserves9. Details of Engineering Evaluation10. Capital Cost Estimate11. Procurement and Construction Schedule12. Projected Program Disbursements13. Estimated Schedule of Disbursements14. Environmental Impact15. ONGC - Organization Chart as of December 31, 197616. Bombay High Offshore Development Project - Organization Chart17. Particulars of the Insurance Coverage Maintained by ONGC

for Bombay High Development Project as of January 197718. Notes and Assumptions to Financial Statements and Projections19. Consolidated Financial Statements for the Period

1973/74 - 1981/82 - Income Statements20. Consolidated Financial Statements for the Period

1973/74 - 1981/82 - Balance Sheets21. Consolidated Financial Statements for the Period

1973/74 - 1981/82 - Sources and Applications of Funds22. Financial Viability of the Bombay High Offshore Development Project23. Assumptions Used in the Economic Evaluation24. Utilization of the Crude Oil, Natural Gas and Natural Gas

Liquids

MAP S

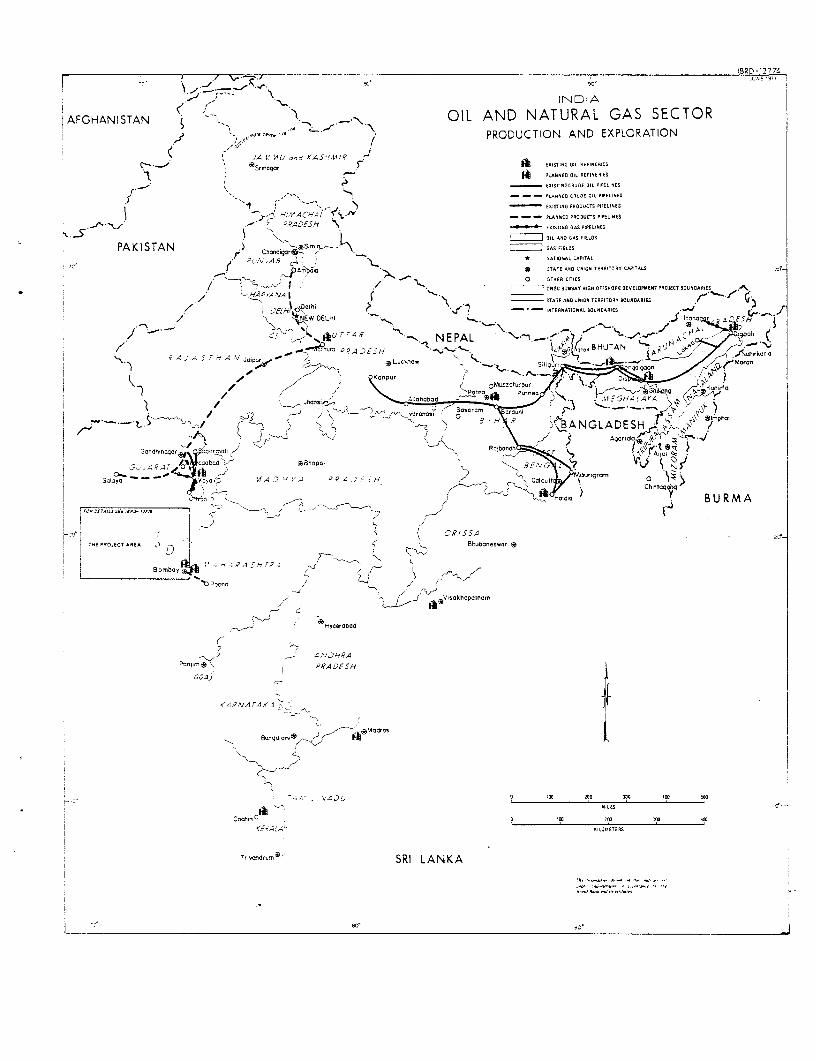

IBRD 12774 Oil and Natural Gas Sector - Production and Exploration

IBRD 12775 Bombay High Offshore Area.

t

INDIA

APPRAISAL OF BOMBAY HIGH OFFSHORE DEVELOPMENT PROJECT

SUMMARY AND CONCLUSIONS

i. In 1975 India's total internal demand for commercial energy wasestimated at 93.2 million tons of oil equivalent, of which petroleum accountedfor about 24%. Per capita consumption was about 11% of the world average.Despite maximum economic use of its domestic energy resources (coal, hydro-power and more recently petroleum and natural gas), India has not achievedenergy self-sufficiency and has to import about 62% of its petroleum require-ments. Following the increase in world oil prices of 1973/74 and subsequentyears, the cost of petroleum imports rose from US$265 million in FY73 to aboutUS$1.6 billion in FY76 when they accounted for about 25% of total imports.Energy demand projections show that, despite conservation and development ofalternative sources of energy (mainly coal), demand for petroleum will con-tinue to grow in the future. Total requirements are estimated at about 50million tons in 1985 and 67.5 million tons in 1990 compared to 22.3 milliontons in 1975.

ii. Current production of crude oil and natural gas is about 8.9 mil-lion tons and 2,300 million cubic meters, respectively, and comes mainly fromonshore fields in Gujarat and Assam. Total onshore reserves are estimated atabout 230 million tons of oil, sufficient to meet about 10 years of cur-rent requirements. India's onshore potential has been partially explored butno exploration of the Continental Shelf took place before 1973 since it wasthought that offshore oil would not be economical at pre-1973 prices. In1973/74 the GOI decided to step up oil exploration offshore and entrustedthis responsibility to the Oil and Natural Gas Commission (ONGC), a statutorybody created in 1959, which had been exploring for and developing hydrocarbonresources onshore. In 1974 ONGC drilled its first offshore exploratory wellin the Bombay High structure, located 160 km offshore Bombay, and struck oil.Subsequent drilling led to the discovery of the North and South Bassein fieldslocated some 100 km west of Bombay. As of March 1977, proven recoverableoffshore reserves are estimated at about 280 million tons of oil equivalent,of which 90% is crude oil and 10% natural gas. The Bombay High and BasseinNorth fields should yield up to 13 million tons of oil equivalent at maximumproduction. ONGC is competent to undertake the development of these twofields and has hired Compagnie Francaise des Petroles (CFP) to assist theirown staff in reservoir engineering studies. Bombay High and Bassein Northproduction will be substituted for crude oil imports and is expected to bringabout net savings of US$16 billion over the next 20 years.

iii. ONGC has already carried out the first two phases of development ofBombay High. Commercial production started in May 1976 and reached twomillion tons per year in March 1977. The project for which the Bank assist-ance is requested consists of Phase III of the development program, which wasapproved by the government in May 1977. It includes drilling of about 20

- ii -

development wells and the construction of about five well platforms, threeprocessing platforms, two subsea lines to shore, subtransmission lines andonshore facilities. Design of the pipeline is completed and the contractfor pipes has been awarded. Tender documents for construction of the pipelineand of the first processing platform have been issued; those for the BombayHigh and North Bassein platforms should be issued shortly.

iv. The project cost is estimated at US$571 million of which 73% (US$417million) is foreign exchange. The cost estimates are based on ONGC's histori-cal costs for drilling and well platforms, and consultants' estimates formajor infrastructure. Physical and price contingencies of about 15% and 8%,respectively, have been applied.

v. A Bank loan of US$150 million to the Government of India is proposedfor a 20-year term including three years of grace; it would cover 26% of thetotal cost of the project. The balance will be financed from ONGC's ownresources, Government equity and loans, bilateral aid, loans from the OilIndustry Development Board, and commercial borrowing. The Government hasagreed to relend the proceeds of the Bank loan to ONGC for a period of notmore than 20 years including three years of grace at an interest rate of10-1/4% per annum. The Government has also undertaken to cover promptly allof ONGC's financing requirements, including its working capital requirements.

vi. ONGC, with the assistance of consultants, will be responsiblefor carrying out the project and is competent to do so. ONGC has agreed tohire management consultants to assist in the establishment of adequate projectmanagement procedures and a management information system prior to December31, 1977. Construction of the project is expected to start in the fall of 1977and be completed in 1979. This schedule is tight but manageable.

vii. The proposed Bank loan will finance the foreign exchange cost ofthe construction of the two subsea pipelines and of the construction andequipment of two well platforms, two processing platforms and the gas process-ing plant. Procurement of the Bank-financed items will be according to inter-national competitive bidding. ONGC's procurement procedures, which are satis-factory, will be used for all other items.

viii. The project presents ecological risks inherent to offshore petroleumdevelopment, but ONGC has taken steps to ensure that design and constructionwill be of appropriate standards. A preliminary study of the environmentalimpact of the project has been carried out and will be supplemented by anin-depth study to be financed by UNDP. Adequate protection against sea andair pollution is included in the project.

ix. ONGC is a large organization with a staff of more than 23,000.Its methods of operation are generally adequate. ONGC is implementing acomprehensive training program for offshore operations. In the course of

- iii -

project preparation a number of institutional issues were identified anddiscussed with ONGC and the GOI. Satisfactory steps have been taken toresolve these issues, particularly in planning and budgeting and staffingof the offshore project organization.

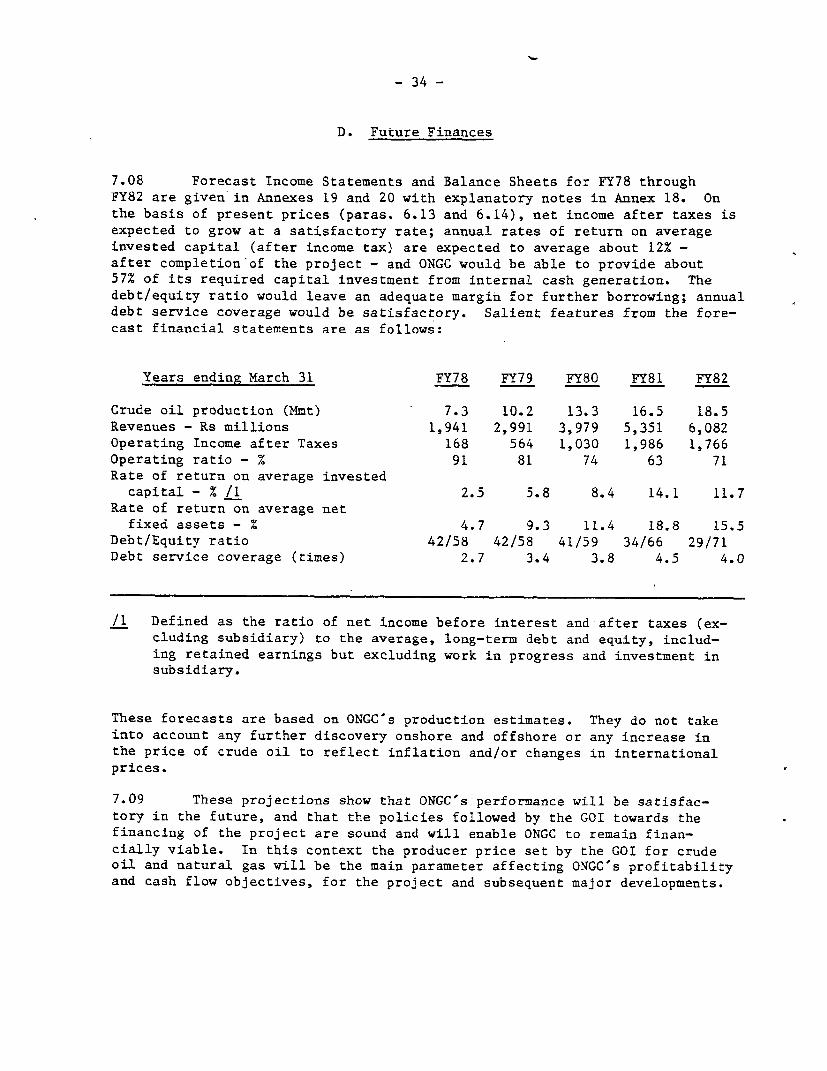

x. ONGC's financial situation has been satisfactory in the past, andthe GOI has taken the necessary steps to raise the price of crude oil toONGC when required. Financial projections show that ONGC will generatesufficient funds to repay its debt and contribute toward the cost of futureoil and gas development. Since the GOI has decided to finance the developmentof Bombay High by equity and borrowings in equal ratios, ONGC's debt/equityratio will remain satisfactory and will leave a margin for further borrowings.

xi. The GOI has set the price of offshore crude oil at US$5/barrel.At this price the development of Bombay High should yield a discounted cashflow (DCF) return to ONGC of about 19.8%, which is satisfactory. The GOIhas agreed that it will carry out from time to time a review of the price ofthe oil and gas produced by ONGC to determine the price levels needed toenable ONGC, under conditions of efficient operation, to meet its operat-ing expenses and earn a return on invested capital sufficient to cover itsdebt service requirements, maintain adequate working capital and finance asubstantial portion of its proposed capital expansion. ONGC has agreed thatit will prepare and furnish each year to the GOI an economic and financialevaluation of the project and of any subsequent major development which willindicate the level of price required for ONGC to earn a DCF return of atleast 15% and which will also provide information on ONGC's future financialperformance. In the light of ONGC's past and projected performance, it isexpected that ONGC's financial viability will be reflected in rates of returnon invested capital of 10 to 14%, a capacity to self-finance 30 to 50% of itsdevelopment expenditures and an annual debt service coverage of 2 to 2.5times. It is expected that prices which would ensure a DCF return of 15%would bring about at least-such results.

xii. The development of Bombay High will increase India's domesticenergy resources and drastically reduce its dependence on imports. Oiland gas will be used in domestic refineries, fertilizer and other indus-trial plants. The Bombay High development program would yield an economicreturn of 165% if sunk costs are excluded; this return would be 66% if sunkcosts are included. The return is less sensitive to variations in programcosts than to delays in production. A delay of one year would reduce thereturn (including sunk costs) to 50%, which would still be very satisfactory.

xiii. Subject to the recommendations in Chapter VIII of this report,the project is suitable for a Bank loan of US$150, million to the Goveramentof India for a 20-year term including three years grace.

t

I. INTRODUCTION

1.01 The increases in the world oil prices in 1973/74 and in subsequentyears have led a number of countries to reassess their energy supply policiesand to look more intensively for domestic sources which could be substitutedfor imports. In India, which imports 62% of its petroleum requirements, theimpact of the oil crisis on the balance of payments was very severe. The costof petroleum imports rose from US$265 million in 1973 to US$1.6 billion in1976, when they accounted for about 25% of total imports. Since India'spetroleum consumption is low and limited to sectors where other sources ofenergy cannot economically be substituted for petroleum, there is little scopefor reducing petroleum imports by developing alternative sources of energy.The Government decided, therefore, to concentrate on developing indigenouspetroleum resources, particularly offshore where potential oil-bearing struc-tures were known to exist but had not been explored since they were not deemedcommercial at pre-1973 prices. The Government entrusted the responsibilityfor offshore exploration to the Oil and Natural Gas Commission, a statutorybody created in 1959, which had been exploring for and developing hydrocarbonresources onshore. In 1974 the Commission drilled its first exploratory wellin the Bombay High structure, located 160 km offshore Bombay, and struck oil.Subsequent drilling led to the discovery of the North and South Bassein fields100 km west of Bombay. The development of Bombay High proceeded rapidly;commercial production started in May 1976 and rose to about two million tonsper year by March 1977. As of March 1977 proven recoverable reserves areestimated at about 250 million tons of oil and 30,000 million cubic meters ofgas, which could yield up to 13 million tons of oil per year and 1,500 mil-lion cubic meters of gas per year, at peak production.

1.02 In February 1976, the GOI requested the Bank to provide guidancein a study of the utilization of natural gas and natural gas liquids to beproduced at Bombay High. A Bank mission visited India to assist in,the pre-paration of terms of reference for this study, and at ONGC's request extendedits assistance to the preparation of terms of reference for a feasibilitystudy of facilities required to produce, transport and process the oil and gasproduction of Bombay High. In 1976 the GOI requested Bank financing for thedevelopment of the Bombay High (BH) and Bassein North (BN) fields.

1.03 The proposed project will be the first project in the Indian oil andgas sector in which the Bank is involved. 1/ It includes the drilling ofdevelopment wells and the construction of production, processing, transportand storage facilities required to utilize the oil and gas production of theBH and BN fields. The total cost of the project is estimated at US$571million, of which 73% is foreign exchange. A Bank loan of US$150 million isrecommended to finance the foreign exchange cost of the construction of twosubsea pipelines, and the construction and equipment of two processing plat-forms, two well platforms and a gas processing plant. 2/ The Borrower willbe the Government of India which will relend the proceeds of the loan tothe Oil and Natural Gas Commission.

1/ Annex 1 provides a list of Bank Group-financed projects in the energysector.

2/ Annex 2 provides a glossary of technical terms used in this report.

-2-

1.04 The present report is based on the conclusions of a preappraisalmission in October-November 1976 and of an appraisal mission in January-February 1977 consisting of Messrs. P. Bourcier (Economist), J. Chang(Financial Analyst), L. Forget (Lawyer), H. Schober (Engineer) and R. Williams(Financial Consultant, U.S.). The estimation of the hydrocarbon reserves isbased on two reports by DeGolyer and MacNaughton (Consultants, U.S.), whichwere commissioned by the Bank.

II. BACKGROUND

A. General

2.01 A striking feature of energy consumption in India is the very largeshare of non-commercial energy in total energy supply. In FY71, the totalshare of non-commercial fuels (animal and vegetable wastes, firewood, char-coal, etc.) was estimated 1/ at 58% of total final consumption, the remainderbeing divided among coal (16.5%), electricity (15.7%) and oil (9.8%). Tenta-tive projections by various institutions and individuals in India and othercountries indicate that, while demand for non-commercial energy will decreasein relative terms in the future, it will continue to increase at about thesame annual rate as the population.

B. Past and Projected Demand and Supply of Commercial Energy

2.02 In 1975, per capita consumption of commercial primary energy inIndia was .157 tons of oil equivalent (Toe), or 11% of the world average.Over the past ten years total demand for commercial primary energy grewfrom 51.8 million Toe (MToe) to 93.2 MToe at an average rate of 6% per annum(Annex 3). Energy elasticity to GNP, over the same period, was 1.85, com-pared to an average of 1.4 for developing countries in the same income group.The main consuming sectors are the mining, manufacturing and transport sec-tors, which together account for about 78% of total demand. The remainder isdivided among residential and commercial (12.5%), agriculture (4.5%) andothers (5%). Since 1965 the sectoral distribution of energy demand has notchanged substantially. Demand projections by the GOI Fuel Policy Committee 2/indicate that demand for commercial primary energy should grow at a somewhatfaster pace (8%) in the future to reach about 300 MToe by 1990 (Annex 4).On the basis of these projections (which take into account the effect of the

1/ P.D. Henderson. India: The Energy Sector. 1974.

2/ Fuel Policy Committee Report, 1974.

-3..

increase in world oil prices in 1973/74), per capita consumption should reach.350 Toe by 1990, which would be equivalent to the per capita consumption ofBrazil in the early 1970's.

2.03 India's energy policy is predicated on the maximum economic use ofdomestic resources, mainly coal and hydropower and, since the late 1950's, pet-roleum and natural gas.

(i) Coal

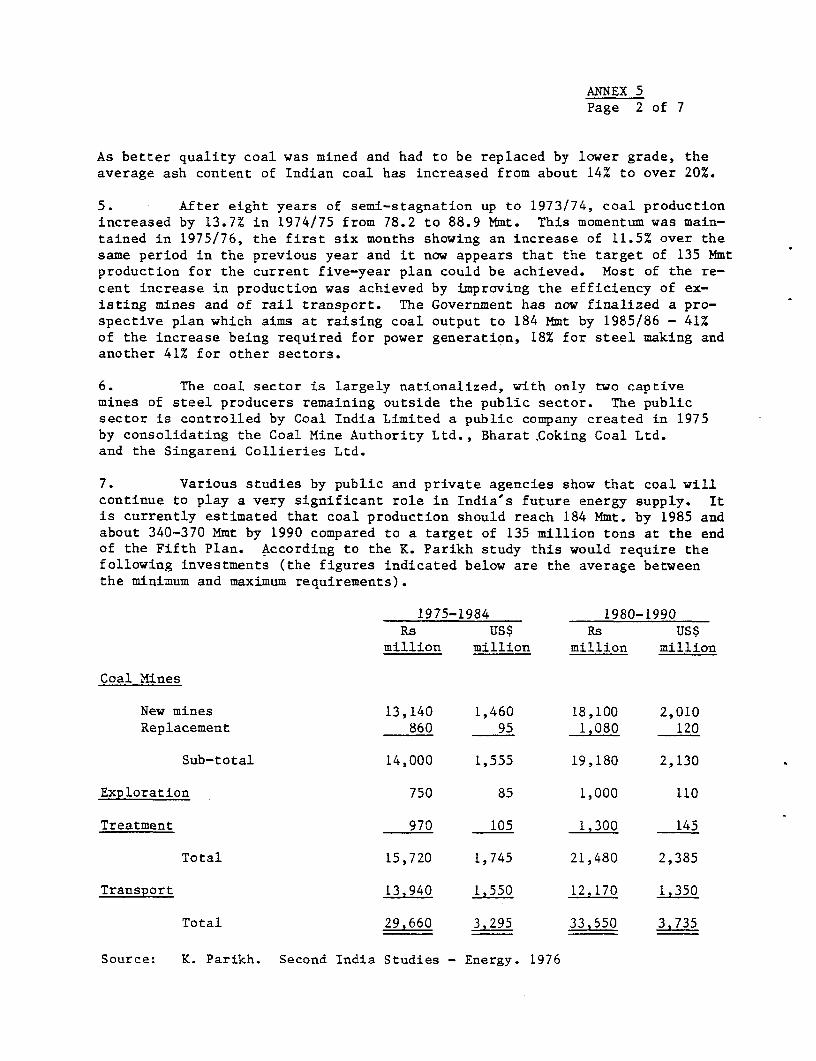

2.04 India's total coal reserves are estimated at 83,000 million metrictons (Mmt) which should be sufficient to cover the needs of India for thenext 50 years under current assumptions of economic growth. Most coal seamsare concentrated in the northern and north-eastern parts of the country.The coal sector is largely nationalized. Current coal production is about100 Mmt and is expected to increase substantially in the future to reach about135 Mmt by the end of 1978, and about 350 Mmt by 1990. The total investmentrequired to bring about this level of production is estimated at US$7 billion,spread over a period of 15 years. Most of the coal is used in power genera-tionr (35%), steel industry (20%), other industry (15%) and railways (10%).

(ii) Hydropower and Nuclear Fuels

2.05 India's hydroelectric power potential has been estimated at 41,000Megawatts (MW) based on a 60% load factor, of which 8,000 MW will have beendeveloped at the end of the Fifth Plan period (March 1979). The currentshare of hydroelectric generation in total generation is 40% and is expectedto decrease to about 35% by 1990. India's resources of nuclear fuels consistmainly of uranium and thorium, the former being used for the generation ofelectric power. On the basis of current reserves, uranium supplies would meetthe demand for only a limited time, depending on the rate at which nuclearfacilities are built. Currently nuclear power generation accounts for only 2%of total generation but is expected to reach about 10% by 1990.

(iii) Hydrocarbons

2.06 India has a large prospective area onshore (1.7 million sq. km)which has only been partly explored. Its offshore prospective area (.3 mil-lion sq. km) is currently under active exploration. By the end of 1974 atotal of about 330 Mmt of hydrocarbon reserves had been discovered onshore,of which 70% were crude oil and 30% gas. Cumulative production to date isabout 100 MToe. In 1974 and 1976 the Bombay High and Bassein fields werediscovered. Proven reserves to date are estimated to be about 280 MToeof which 90% are crude oil and 10% gas. Other hydrocarbon-bearing structuresin the same area are still under evaluation (Annex 5 and para. 4.01). Crudeoil production in FY77 was 8.9 Mmt of which about .5 Mmt was offshore; itcovered about 38% of total in ernal demand (Annex y); natural gas productionis about 2,300 million m (Mm ), of which 1,300 Mm are used in fertilizer and

-4-

other industries; the remainder is used on the fields or is flared becausethere is no accessible market. Onshore production is concentrated in twoStates: Assam in the northeast and Gujarat in the northwest. Petroleum ismainly used in transportation (49%), the residential sector (28%) and industry(11%) .

2.07 Despite the preferential use of coal, the share of oil and naturalgas in total commercial energy supply grew steadily from 21% in 1965 to about32% in 1973. It has remained constant since, as a result of the increase inthe domestic price of refined products and of the steps taken to increase coalproduction and to substitute coal for liquid fuels, wherever feasible.Domestic production of petroleum has not kept pace with requirements, andIndia's petroleum imports grew from 9.3 Mmt in 1965 to 15.4 Mmt in 1975 at acost of US$1.6 billion, equivalent to 24.5% and 34.5% of total merchandiseimports and exports, respectively. It is projected 1/ that the share ofpetroleum products will be contained to about 20 to 30% of total primaryenergy requirements, which appears reasonable. On this basis petroleum demandin India (for fuel and non-energy use) should reach about 50 Mmt by 1985. Atthat time, the combined production of existing onshore fields and of BH and BNshould peak at about 26.5 Mmt, thus covering about 53% of total requirementscompared to 38% at present. Unless other fields are discovered and broughtinto production, India's imports requirements would then be about 23.5 Mmt ata cost of US$2.3 billion at present oil prices.

(iv) Non-conventional energy prospects in India

2.08 Recently the Indian Government has shown considerable interest indeveloping the use of bio-gas (methane produced from organic waste) as a sourceof energy in rural areas. Even large-scale development would have little effecton the demand for commercial energy since it would substitute principally fornon-commercial fuels. The potential for the use of solar water heaters fordomestic and small-scale commercial use exists but has not yet been developed.In the future solar energy may substitute for commercial fuels to some extent,but is more likely to meet an energy demand which would otherwise remain un-fulfilled. Investigations of the geothermal potential are being carried onin the Himalayan foothills, but the scope for large-scale geothermal develop-ment in India is limited by unsuitable geological conditions in most of thesub-continent, and its overall effect on the energy situation is likely to bemarginal at best.

1/ From Report of the Fuel Policy Committee, 1974, and Second India Studies:Energy (K. Parikh - 1976).

-5-

III. THE OIL AND GAS SECTOR

A. Historical Development

3.01 According to the GOI's Industrial Policy Resolutions of 1948 and1956, the development of the oil and gas sector is the responsibility of theCentral Government, and private firms are given a secondary role except whentheir intervention is deemed to be in the national interest. Over time,India's policies regarding the development of the oil and gas sector havechanged from an almost total reliance on foreign oil companies after Inde-pendence to a strong emphasis on self-reliance until 1973/74. Recently,India has followed a policy of compromise between national autonomy andcooperation with foreign oil companies. (Annex 7 provides a historical over-view of India's policies regarding the development of the oil and gas sector.)

3.02 Today the oil and gas sector consists mainly of public and semi-public enterprises under the Ministry of Petroleum and Chemicals. Over thepast 30 years, the relative importance of these enterprises has varied accord-ing to the resources that were available to them or to the role that theycould play in India's petroleum supplies.

(i) Refining and Marketing

3.03 In 1948 India was almost totally dependent on imports of refinedproducts. However, the GOI soon realized that future economic growth wouldlead to ever-increasing demand for petroleum and that the reliance on importsof refined products would be costly. The GOI therefore approved the con-struction of domestic refineries, owned, supplied and operated by foreign com-panies. This decision was a departure from the Industrial Policy Resolution(1948); however it was expected that it would save foreign exchange 1/, pro-vide expertise in the petroleum field and encourage oil companies to explorefor oil in India. This policy was followed until the early 1960's when theGOI realized that existing supply contracts with foreign companies preventedIndia from taking full advantage of the overall decrease in oil prices thatwas taking place at that time. The GOI then decided to take over the pro-curement of part of its crude oil requirements, to limit the expansion ofprivate refineries and to create sufficient public refining capacity to usewhatever crude oil it could obtain at lower cost. This led to the construc-tion of several public refineries, with the assistance of Eastern Europeancountries, which were integrated into the Indian Oil Corporation in 1964.By 1970 public refineries accounted for about 60% of the total crude oilthroughput.

3.04 Following the increase in world oil prices of 1973/74, the GOIdecided to limit domestic consumption of petroleum to the minimum compati-ble with the projected economic growth. Among other things, this policy

1/ Several studies indicate that from 1955 to 1960 India saved someUS$150 million by refining imported crude oil rather than import-ing petroleum products.

- 6 -

included drastic increases in the prices of refined products and a plan tomaximize the production of middle distillates (kerosene, diesel and gas oil)which are in short supply. At the same time the GOI entered into a seriesof negotiations to acquire part or all the assets of foreign companies.These negotiations have been completed successfully and the GOI now ownsmore than 85% of total refining capacity and has controlling interest in theremainder.

(ii) Exploration and Development

3.05 Oil was first discovered in India by the Assam Oil Company (AOC) inthe 1880's. AOC produces very small quantities of oil from a virtually de-pleted field in Assam. It is not active in exploration, and the GOI is cur-rently negotiating its takeover.

3.06 The first major steps towards the exploration for and developmentof hydrocarbon resources in India were taken in the early 1950's when theGOI entered into joint ventures with Standard Vacuum Oil Company and withBurmah Oil. The former, known as the Indo-Stanvac Project, was terminated in1960 without positive results. The latter was successful in discovering oilin the north-east and led to the creation of Oil India Ltd. (OIL), in whichthe GOI had a participation of 33% initially which was increased to 50% in1960. OIL's production started in 1959 and reached 3 Mmt in 1970; it has re-mained constant since.

3.07 In the late 1950's, the GOI decided to increase exploration.This decision was based upon the conclusions of Indian geologists, con-firmed by a panel of international experts, that India's prospective areawas under-explored and that the potential for oil discovery was good. In1959 the GOI created the Oil and Natural Gas Commission (ONGC), which wasgiven the task of exploring for and developing petroleum resources in India,outside the areas being prospected by OIL. ONGC started operations with theassistance of experts from the USSR, and soon after (January 1961) discoveredoil and gas in Gujarat. ONGC's production started in 1961, reached 1.1 Mmtin 1965, 3 Mmt in 1970 and 5.7 Mmt in 1976. ONGC-'s initial success was notfollowed by the discovery of any significant oil and/or gas reserves onshore.The increase in world oil prices, however, led the GOI to intensify itssearch for domestic oil and to promote exploration offshore. This effortwas successful and resulted in the discovery of Bombay High in 1974 and ofBassein North and South in 1976.

3.08 ONGC has become India's main organization for the exploration forpetroleum and natural gas. It has exclusive rights to undertake and/orsupervise these activities onshore (except in the areas allocated to OIL) andoffshore. ONGC is a large organization with considerable experience in on-shore operations. Until recently ONGC's experience offshore was limited tosome shallow-water fields in Gujarat.

-7-

B. Recent Developments

3.09 The increase in the world oil prices of 1973/74 led to a drasticincrease in the cost of petroleum imports and introduced the need for areappraisal of earlier programs for exploration and development and forlong-term supply of petroleum. The Report of the Fuel Policy Committee (1974)analyzes the consequences of higher petroleum prices and makes the followingpolicy recommendations:

(i) steps should be taken to reduce the cost of production ofpetroleum products;

(ii) steps should be taken to improve the long-term securityof supply; and

(iii) imports of petroleum should be reduced by substitutingother fuels (coal) for petroleum and by increasing theindigenous production of crude oil.

To achieve these objectives, the Fuel Policy Committee recommended inter aliaan optimization of the refining pattern to meet the projected product demandmix at least cost, the negotiation of long-term supply agreements with OPECcountries and the possibility of developing oil resources in the Middle East,and an intensification of exploration in India, particularly offshore wherethe most promising prospects were located.

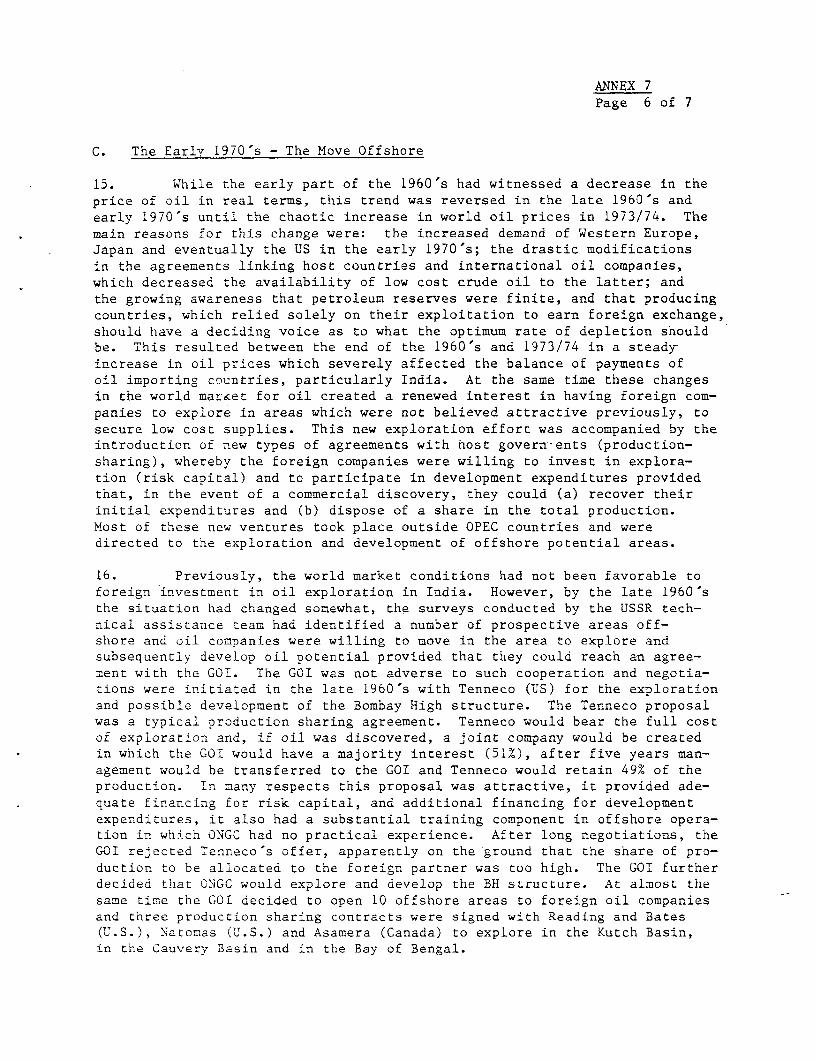

3.10 The policy followed by the GOI since 1974, which is analyzed indetail in World Bank Report 1172-IN 1/ and summarized below, is generallyin line with the Fuel Policy Committee's recommendations. The GOI has takensteps to increase petroleum product prices and rationalize refinery operationsand expansion. It has also negotiated supply contracts with Iraq and Iran, andONGC has entered into joint venture and service contracts in Iraq, Iran andTanzania; The contract with Iran should provide about .7 Mmt per annum ofparticipation crude oil. Other foreign ventures may be considered in thefuture. The most dramatic steps, however, were taken in exploration for anddevelopment of domestic hydrocarbon resources and particularly in the explora-tion and development of the offshore potential. ONGC's exploration programonshore was expanded considerably. Offshore, first priority was given to thedevelopment of the Bombay High and Bassein North fields which mark a turningpoint in India's oil industry. In addition, the GOI decided to open tenoffshore areas to foreign exploration under production-sharing contracts.Three contracts, in which ONGC has a working interest, were signed withReading and Bates (U.S.), Natomas (U.S.) and Asamera (Canada) to explorein the Kutch Basin, the Bay of Bengal and the Cauvery Basin, respectively.The first exploratory wells were sunk in 1975 and 1976 but no commercialdiscovery has yet been made.

1/ India, The Oil and Gas Sector. May 11, 1976.

-8-

3.11 This increase in domestic exploration and development activities,which will be carried out almost entirely by ONGC, is reflected in the suc-cessive increases in the Plan allocation to the oil and gas sector. Therevised Fifth Plan target for exploration, development and refining duringthe Plan period is Rs. 16,913 million (US$1,879 million), or 4.3% of totalPlan outlay. ONGC's allocation, which was originally Rs. 6,940 million(US$771 million), is currently estimated at Rs. 10,561 million (US$1,173million), equivalent to 62% of the sector's total expenditures excludingpetrochemicals. But even this amount, which is greatly increased over thedraft Fifth Plan, both in real and relative terms, is likely to be exceeded.From a total FY75 Plan outlay of over Rs. 800 million, ONGC's Plan expendi-tures rose to over Rs. 1,800 million and Rs. 2,800 million in FY76 and FY77,respectively.

3.12 ONGC's current Five-Year Plan provides for the expansion of itsonshore activities to reach a production of about 33.3 Mmt over the FifthPlan period compared to 19.4 Mmt in the previous one. This will be achievedmainly by introducing secondary recovery wherever feasible. In addition,survey work, exploratory and development drilling will be intensified.Modern digital equipment and computer facilities are being introduced, andby March 1979, the number of drilling rigs will be increased by 19. Drill-ing targets for FY78 are 294,000 meters compared to 191,000 in FY75. Thetotal cost of the onshore program through FY79 is estimated at aboutRs. 3,600 million (US$400 million).

3.13 Offshore, the emphasis will be on the completion of the developmentof Bombay High and of North Bassein. The cost of this program, includingprice contingencies, is estimated at US$1,774 million. The program, which isdescribed in Chapter IV, will be implemented by ONGC with the assistance ofoutside consultants and contractors. The proposed project for which a Bankloan of US$150 million is recommended consists of Phase III of the offshoredevelopment program.

C. Longer-Term Perspectives

3.14 India has a large prospective offshore area which needs to beexplored and developed as soon as possible to offset future increases inthe cost of petroleum imports. However, the time frame in which this poten-tial can be developed depends largely on the resources which are allocatedto the oil and gas sector and on ONGC's capability to manage a much largerexploration and development program in the future. The GOI is aware of thisand has taken steps to secure a reliable resource base for the oil and gassector. Crude oil prices have been set at a level which will ensure that ONGCwill generate sufficient resources internally to finance a reasonable share ofthe Bombay High and North Bassein development. In addition the GOI has givenhigh priority to the financing of the offshore program from Central Budgetresources and from the Oil Industry Development Board, created in 1974 toassist in the financing of oil and gas projects, and is also mobilizingalternative sources of financing (bilateral aid and commercial bank loans)(para. 7.07).

D. The Role of the Bank

3.15 The discovery and development of Bombay High has presented theGOI and the Commission with technical and managerial challenges to whichthey have responded in a pragmatic way. However, further developments willrequire further improvement in ONGC's managerial and technical capabilities,particularly in long-term planning and budgeting. The Bank has been involvedin the preparation of the Bombay High Development Project (BHDP) and, cancontinue to assist ONGC by providing advice on project evaluation methodscurrently used in the oil industry. ONGC is instituting managerial andfinancial improvements in offshore operations, and Bank involvement in theproposed project can also be useful in this regard.

IV. THE PROGRAM AND THE PROJECT

A. Main Characteristics of the Bombay High Area

4.01 The Bombay High and Bassein fields are located some 160 km and100 km, respectively, offshore Bombay. They are part of a number of struc-tures which were identified during a seismic survey in 1966 and which arecurrently under-exploration. The Bombay High field was discovered in 1974and the Bassein field in 1976. -Map 12775 shows the location of thesefields.

4.02 Total proven recoverable reserves of oil are currently estimated atabout 250 Mmt, using primary and secondary recovery techniques (depletion, gaslift and water injection). In addition it is estimated that the Bombay Highand Bassein North fields could yield an additional 85 Mmt of oil when probablereserves currently under evaluation have been confirmed. For the purposeof this report, only proven reserves have been considered. Reserves esti-mates are based on studies made by ONGC, the Indian Institute of PetroleumExploration and foreign consultants (Geoman, U.S., and Compagnie Francaisedes Petroles, France) and on an independent evaluation carried out by DeGolyerand MacNaughton (consultants, U.S.) at the request of the Bank. The resultsof these studies are summarized in Annex 8.

4.03 According to these studies, Bombay High maximum production shouldreach about 225,000 barrels per day (b/d) of crude oil and about 3.4 Mm3 /dayof associated gas by 1982. These projections are based on a production ex-perience of about 12 months and are considered reasonable. The maximumproduction of Bassein North is currently estimated at about 40,000 b/d whichis considered conservative. Continuous review of reservoir behavior will be

- 10 -

required during the life of the field, to optimize development and hydrocar-bons recovery. ONGC geologists have extensive experience in reservoir engi-neering but are not familiar with this type of reservoir (limestone forma-tion). ONGC has entered into a four-year contract with Compagnie Francaise''des Petroles (CFP), whereby CFP will assist ONGC staff'in the interpretatiorn' 'of seismic data, in mathematical reservoir modelling and in production optimi-zation using primary and enhanced recovery techniques. ONGC has agreed tosubmit to the Bank an updated development plan of the Bombay High and NorthBassein fields by the end of each calendar year starting in 1977.

B. The Development Program

4.04 On the basis of existing reserves studies ONGC, the potential'usersand their consultants have prepared plans for the development and utilizationof the crude oil and natural gas to be produced in the Bombay High area untt1982. '"

4.05 ONGC's development program was approved by the Commission in January1977, at a meeting attended by the Secretary (Economic Affairs),. Ministry- ofFinance and the Secretary (Petroleum), Ministry of Petroleum and chemicals.These plans call for development in five phases. Phases I and II; ..' ch ea.Xalmost completed, consist of the construction of the production,f'acilitie X(wells, well and production platforms) required to reach a productlon.'cap''- ity of 80,000 b/d (4 Mmt/year) by the end of 1977 and of the constructionffof0temporary tanker transport facilities to bring crude oil to shore. Duing -Phase I and II all the associated gas will be flared offshore. Phase IIf-wasapproved by the Government in May 1977 and consists of the drilling of a 20 development wells and the construction of about five well platforms to-6~, t, 2_,reach a production of 140,000 bld by the end of 1978, as wellt as the. const -tion of three processing platforms, permanent pipeline transport faciilties~and shore facilities. Phase IV and V will consist of the constructione ofadditional facilities to reach a production of 265,000 b/d by 1982, ining the drilling of about 60 to 70 development wells and about.30: waterin-jection wells and the construction of the corresponding well platforms- andX iprocessing facilities. The entire program is expected to extend into ithe,iearly 1980's at a total cost estimated at US$1,774 million, of vhich DS204'million will be for Phase I and II, US$571 million for Phase III I/:a 'iI

US$999 million for Phases IV and V.

4.06 The crude oil and natural gas produced at Bombay High and Bassein lWNorth will be substituted for imported crude oil supplies to domestic 're'-2 + ';.2.';^fineries and used in fertilizer and other industrial plants. Because of-,'`.-

1/ The cost of Phase III as approved by the Government is US$593.3 million,but it includes interest during construction which is not included in:',the Bank's estimates.

- 11 -

the characteristics of the Bombay High crude oil (high wax content, highpour point), some modifications are required at existing refineries. TheTrombay refineries, which are the first concerned, have already completedmost of the revamping and other refineries are expected to carry out thenecessary adjustments during the execution of Phase III. Current plans areto use the associated gas in the Trombay fertilizer complex of the Fertil-izer Corporation of India (FCI). The decision to convert some units tonatural gas at FCI's Trombay plant has already been taken and further gasutilization studies are being carried out with the assistance of Stone andWebster (Consultants, U.S.). Liquefied Petroleum Gas (LPG) will be used inthe residential and commercial market.

C. Status of Development

4.07 The first phase was completed in March 1977, three months behindschedule because of unexpected problems in the driving of piles for oneplatform. It consisted of the drilling of ten development wells and of-theconstruction of three well platforms and one, production platform in thenorthern part of the Bombay High field to achieve a production of 40,000 b/d.It also included the construction of two Single Buoy Moorings to anchor astorage tanker and a shuttle tanker. This temporary transportation systempermitted commercial production to start in May 1976, but had to be inter-rupted during the monsoon. The second phase, which is essentially identicalto the first, is virtually completed and total production from Bombay Highwill reach 80,000 b/d by the end of 1977 as planned. During Phase I and IImost of the exploratory and development drilling was carried out by contrac-tors under the supervision of ONGC Offshore Operations Division (para. 4.19).Construction of the well platforms and of two production platforms was carriedout by McDermott (Contractors, U.S.) under the supervision cf ONGC's OffshoreConstruction Division (para. 4.19).

D. The Project

4.08 The project comprises Phase III of ONGC's development program andincludes the facilities listed below. Annex 9 gives a detailed descriptionof the project facilities and of the operations for which they are required.

(i) Development drilling. About 16 production wells willbe drilled at Bombay High North and 4 at Bassein alongwith the necessary well platforms. Four deviated wellsdraining an area of about 6 sq. km. will be drilledfrom each platform. These will be connected bysubsea gathering lines to the main processing plat-forms.

- 12 -

(ii) Processing platforms. A total of three processing platformswill be installed, two in the northern part of the BombayHigh field and one at Bassein North. The BH platforms willhave a combined capacity of 160,000 b/d and the capacity ofthe BN platform will be 60,000 b/d.

(iii) Subsea pipelines. Two 209 km subsea pipelines, 30" and 26"in diameter, will be laid to transport oil and gas, respec-tively.

(iv) Onshore terminal. The two subsea pipelines will terminateat Uran (in the Bay of Trombay), where a terminal will bebuilt, including a crude oil stabilization unit, a gasprocessing plant and storage facilities, from which thecrude oil will be pumped to the Trombay refineries. Ex-isting pipelines between Butcher Island and Trombay willbe used to load the crude aboard tankers for shipment tocoastal refineries or for export.

(v) Supply lines. Four different supply lines, 8" to 30" indiameter, will cross the Bay of Trombay to connect the Uranterminial to the various users.

(vi) Supply base. Berthing facilities for supply vessels,repair shops, warehouses, administrative buildings andoffices will be built at Nhava Sheva, a site recentlyacquired by ONGC.

(vii) Telecommunications and control. A telemetric communica-tion and control system will be installed to cover theentire Bombay High program.

(viii) Engineering and technical services. Consultants have beenor will be engaged to prepare detailed engineering designs,supervise construction and assist ONGC in overall projectmanagement.

E. Status of Engineering

4.09 The Phase III facilities are based on a feasibility study preparedin 1976 by Pipe Line Technologists (PLT), Consultants, UK. This study definedthe main parameters of the pipelines, processing platforms and onshore facil-ities. In addition ONGC retained Engineers India Limited (EIL) in collabora-tion with Crest Engineering (U.S.) to carry out additional studies on theBombay High North and Bassein North processing platforms. These consultingorganizations were subsequently assigned to engineer, design and assist inthe supervision of the construction of the pipelines and interim platform(para. 4.20) (PLT) and of the Bassein North and Bombay High processing plat-forms (EIL/ Crest).

- 13 -

4.10 PLT have completed design and procurement documents for the two sub-sea pipelines, the land and harbor supply pipelines and the interim processingplatform at Bombay High North. Contracts for pipe and related materialshave been awarded. Bids have been received for the interim platform andare being evaluated. The pipe construction bid documents have been issuedand contract awards are scheduled for the latter part of July 1977.

4.11 EIL/Crest are designing the Bassein North process platform and arescheduled to have bid documents ready for issue by July 1977. They will thendesign and prepare bid documents for the Bombay High North platform for whichbid invitations are scheduled to be issued during August 1977.

4.12 Engineering consultants for the onshore terminal at Uran have beenselected. It is expected that the crude oil stabilization, oil storage andpumping portion of the work will be assigned to Humphreys and Glasgow (Con-sultants, U.K.) after the GOI has approved the contract. A consulting firmmust still be selected for the gas processing plant, but there is no immediateurgency in starting this work.

4.13 Peter Fraenkel and Partners (Consultants, U.K.) have been givenengineering and design responsibility for the Nhava Sheva supply base. Tele-communication and control facilities have been assigned to Burmah Oil Engi-neering and the Defense Ministry. All engineering consultants engaged byONGC are experienced and qualified for the tasks assigned to them. ONGChas agreed that they will continue to use consultants whose qualifications,experience and terms and conditions of employment are satisfactory to theBank, until the completion of the Project.

F. Cost Estimates

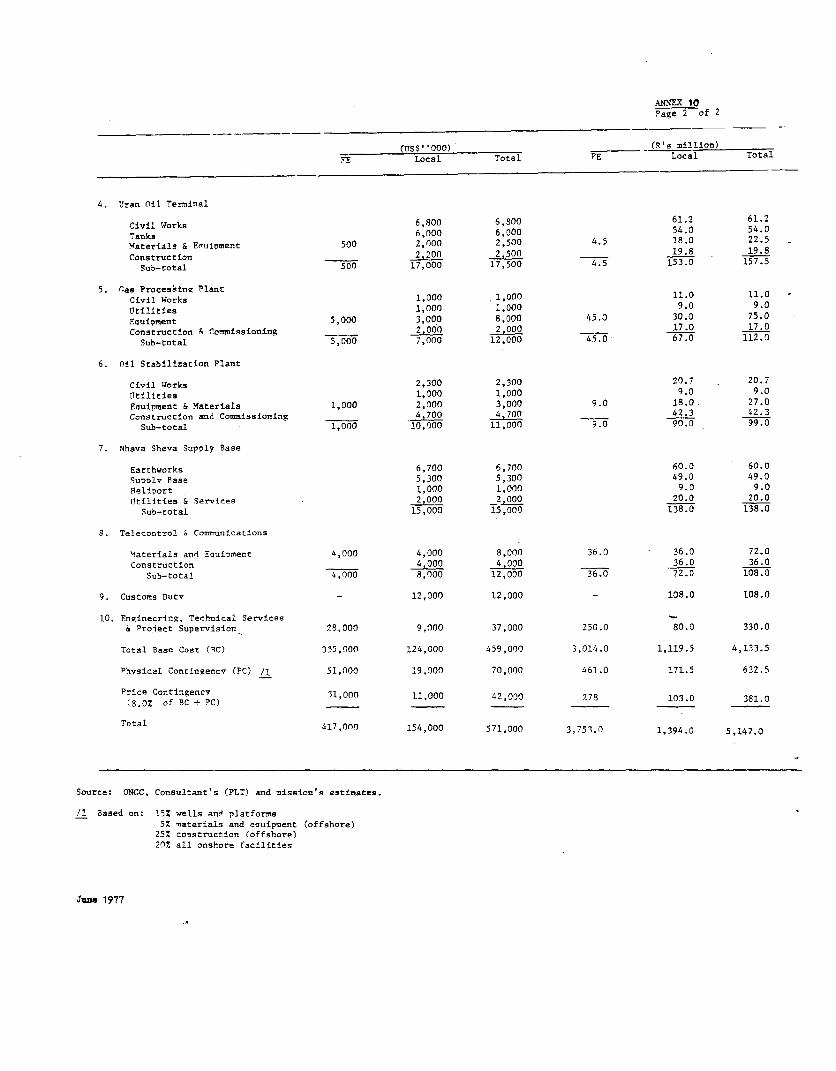

4.14 The Project cost is estimated at US$571.0 million, including con-tingencies and customs duties (from which part of the offshore facilities areexempted). The foreign exchange component is estimated at US$417.0 millionor 73%. Annex 10 gives details of the cost estimates which are summarizedbelow. Annex 12 indicates the phasing of expenditures over the period 1977-1981.

- 14 -

SUMMARY OF PROJECT COSTS

(Rs million) (US$ million)Local Foreign Total Local Foreign Total %

Development drilling

Wells 110.0 332.0 442.0 12.0 37.0 49.0 8.6Well Platforms 80.0 250.0 330.0 9.0 28.0 37.0 6.5

Subtotal 190.0 582.0 772.0 21.0 65.0 86.0 15.1

Infrastructure

Land 40.0 - 40.0 4.5 - 4.5 0.8Pipelines 159.0 1,345.0 1,504.0 18.0 149.0 167.0 29.2Processing Plat-forms 22.5 742.5 765.0 2.5 82.5 85.0 14.9Uran Oil Terminal 153.0 4.5 157.5 17.0 .5 17.5 3.1Gas ProcessingPlant 67.0 45.0 112.0 7.0 5.0 12.0 2.1Oil StabilizationPlant 90.0 9.0 999.0 10.0 1.0 11.0 1.9Nhava Sheva SupplyBase 138.0 - 138.0 15.0 - 15.0 2.6Telecom and

Control 72.0 36.0 108.0 8.0 4.0 12.0 2.1Custom Duty 108.0 - 108.0 12.0 - 12.0 2.1Engineering;Technical Ser-

vices and ProjectSupervision 80.0 250.0 330.0 9.0 28.0 37.0 6.5

Subtotal 929.5 2,432.0 3,361.5 103.0 270.0 373.0 65.3

Total Base Cost 1.119.5 3.014.0 4,133.5 124.0 335.0 459.0 80.4

Physical Contin-gencies (15.3%) 171.5 461.0 632.5 19.0 51.0 70.0 12.3

Price Contin-gencies (8.0%) 103.0 278.0 381.0 11.0 31.0 42.0 7.3

TOTAL 1,394.0 3,753.0 5,147.0 154.0 417.0 571.0 100.0

- 15 -

Development drilling costs were derived from ONGC's historical costs andreflect conditions likely to prevail in the next two years. However, anoverall physical contingency of 15% was applied to the cost of wells andwell platforms to account for non-productive wells. The costs of infra-structure are based on PLT cost estimates and reflect conditions in early1977. Physical contingencies of 57 and 25%, 1/ respectively, were appliedon the cost of materials and construction for the main offshore facilities(pipelines and platforms). For the shore facilities and telecommunicationssystem, which have not yet been designed in detail, an overall physicalcontingency of 20% was applied. Price contingencies amount to 8% of theproject cost (including physical contingencies) and are based on an annualrate of escalation of 7% for material and equipment and of 9% for civilworks.

4.15 The cost of consultants' services was estimated on the basisof actual contracts and of prevailing rates in India and abroad. 2/ Totalmanpower requirements are estimated to be 11,000 man-months of which about70% will be foreign. The average cost per man-month is estimated atUS$3,600 and US$1,800 for foreign and local consultants, respectively.

G. Items Proposed for Bank Financing

4.16 The proposed Bank Loan of US$150.0 million would finance the for-eign exchange cost of the construction of the two subsea pipelines and theequipment and installation of the Bassein North and Bombay High North pro-cessing platforms, two well platforms and the gas processing plant. Thesecontracts are suitable for international competitive bidding and are likelyto attract a large number of suppliers and contractors. The proposed Bankloan would finance about 26% of the total cost, and about 36% of the foreignexchange cost of the project, including contingencies.

1/ The high physical contingencies reflect the difficulty of offshore

construction which depends on unpredictable weather conditions.

2/ These costs do not include the cost of CFP's services which will extendbeyond the scope of the proposed project and will not be limited toBombay High.

- 16 -

H. Financing Plan

4.17 ONGC's total financial requirements from FY78 to FY80 for BombayHigh and Bassein North development expenditures, are currently estimated at

Rs 8,438 million (US$937.6 million), of which Rs 5,147 million (US$571 mil-lion) is for the project and Rs 3,291 million (US$366.6 million) is forPhases IV and V. ONGC's financial projections show that Rs 3,486 million(US$387.3 million) will be financed from internal cash generation. The

balance will be financed, in equal ratios, by equity contributions fromthe GOI and loans from the GOI and the Oil Industry Development Board, asindicated below:

Summary Finance Plan, FY78-80Rs million US$ million %

Total requirements:of whichThe Project 5,147 571.0 61.0Phases IV and V 3,291 366.6 39.0

Total 8,438 937.6 100.0

Financed by:internal cash generation 3,486 387.3 41.4GOI equity /1 2,476 275.2 29.3loans /2 2,476 275.1 29.3

Total 8,438 937.6 100.0

/1 Including an estimated US$50 million of bilateral aid (e.g.,Japan, France, U.K., Germany).

/2 Including the proceeds of the Bank loan (US$150 million)loans from OIDB (US$70.3 million), the GOI (US$4.8 mil-lion) and commercial banks (US$50 million).

4.18 The GOI has agreed that it would relend the proceeds of the Bankloan to ONGC at an interest rate of 10-1/4% per annum for a period not exceed-ing 20 years including three years of grace. The GOI has further agreed thatit would provide sufficient funds to meet ONGC's financial requirements forthe project and other investments.

I. Project Execution, Supervision and Reporting

Execution

4.19 The Offshore Operations and Construction Divisions will be respon-sible for project implementation and supervision with the assistance of out-side consultants (para. 4.w9-4.13) and of ONGC's advisory services. The

- 17 -

Operations Division, which will supervise and coordinate development drilling,is qualified and sufficiently staffed to supervise drilling contractors. Thestaff of the Construction Division is competent and is currently being in-creased to meet the additional work load generated by the project. ONGChas already transferred experienced personnel from its onshore operationsto the project staff and has appointed an offshore project manager who willalso be responsible for the entire Construction Division. Experienced sub-project managers have been appointed for the pipelines, platforms and crudeoil stabilization plant. The selection of subproject managers for telecom-munications and for the gas processing plant is underway. These arrangementsare satisfactory. However, there is a need to improve the ConstructionDivision's capability in project scheduling and in overall project management.ONGC has agreed to hire management consultants to assist in the establishmentof adequate project management procedures and of an appropriate managementinformation system prior to December 31, 1977.

Construction Schedule

4.20 The project should be constructed over a period of two years withmost of the offshore facilities being completed by mid-1978 (Annex 11 showsthe proposed construction schedule). Because of the impossibility of under-taking any major construction offshore during the monsoon (June to October),ONGC has decided to complete the two subsea pipelines, the Bassein Northplatform, the critical facilities of the onshore terminal and the supply lineby May 1978. The Bombay High North platform will be completed only at the endof 1978 or early in 1979. However, in order to ensure that the two pipelinescan be used during the 1978 monsoon to transport oil and gas (the latter wouldcontinue to be flared otherwise), ONGC has decided that an interim platformwill be installed at Bombay High by May 1978. This platform, will be builtadjacent to the location of, and will be subsequently connected to, the BombayHigh North platform. Although the construction schedule is tight, it isachievable and the fact that there is a temporary worldwide lull in offshoreconstruction activity should help ONGC achieve its objectives.

Supervision and Reporting

4.21 ONGC is competent to supervise the execution of the project with theassistance of management consultants (para. 4.19) and of the consultantsreferred to in paras 4.09 to 4.13. ONGC's internal reporting procedureswill be improved under the provision of para. 6.08. ONGC has agreed to sendcopies of quarterly progress reports to the Bank.

- 18 -

J. Procurement and Disbursement

4.22 International competitive bidding procedures, in accordance withBank guidelines, will be followed for the Bank-financed items. No localsuppliers or contractors are expected to bid on these terms; however, for thepurpose of bid evaluation, a preference of 15% or the custom duty, whicheveris less, will be applied to any local bid. Bid invitation and evaluation willbe the responsibility of ONGC with assistance from consultants as required.ONGC's normal procurement procedure for foreign supplies requires worldwidebidding similar to the Bank's ICB. It is expected that this procedure will beapplied for all imported equipment and services not financed by the proceedsof the Bank loan. ONGC has indicated that, in order to save time, it wastheir intention to call for lump sum bids for the Bassein North and BombayHigh North platforms; since this procedure will not restrict competition, itis acceptable to the Bank. Bid invitations for critical items with limitedavailability, which are essential to efficient execution of the project andestimated to cost less than US$2 million, may be sent directly to the quali-fied available suppliers, provided that the Bank's prior approval is obtainedfor these items and the list of suppliers and that the aggregate amountprocured under this procedure does not exceed US$7.5 million.

4.23 Disbursement will cover 100% of the foreign cost of Bank financed

contracts. Disbursement of the Bank loan is expected to be completed inthree years. (Annex 13 gives the estimated schedule of disbursement ofthe Bank loan.) The closing date of the proposed loan would be December 31,1980.

K. Right-of-Way and Land Acquisition

4.24 No right-of-way problem is expected offshore, since ONGC's proposedpipeline route does not cross any shipping channel. Onshore, ONGC is in theprocess of acquiring the land required for the Uran terminal and the supplybase. Negotiations are at an advanced stage and no difficulties are expected.The onshore supply lines have to be routed so as to minimize right-of-wayproblems and negotiations with the Port Authority and other State Governmentagencies are progressing satisfactorily. Obtaining formal title may taketime but is not expected to delay project execution. ONGC has agreed totake all actions necessary to acquire as and when needed the land and rights-of-way required for construction of the project facilities.

L. Operations and Training

4.25 ONGC's staff is adequately trained to carry on its present off-shore operations, but operating and maintaining the new and more complexfacilities of the Bombay High project will require additional operationaland supervisory staff training. (See Annex 9 for a description of ONGC'soperations and facilities.) ONGC's management recognizes the need for

- 19 -

this training and has budgeted the equivalent of US$700,000 to fund a train-ing program. A detailed program is being formulated. It will comprise localand on-the-job training, training abroad at equipment manufacturers' plantsand foreign installations, and various special training related to offshoreoperations, safety, pollution control and related subjects. As part of itsprogram, ONGC plans to accept offers of offshore training by the British andNorwegian governments. These arrangements are satisfactory.

M. Ecology and Safety

4.26 Pipelines properly protected, maintained and operated pose noserious environmental hazards. Accordingly, all necessary precautions willbe taken during design and construction of the oil and gas pipelines tominimize the chances of overpressurization, corrosion and third-partydamage. The offshore and terminal facilities will not cause noticeableatmospheric pollution, and effluents, essentially oily water and humanwaste, will be adequately treated before disposal. ONGC is procuring avessel outfitted for offshore fire-fighting and oil spill clean-up. Inaddition the GOI is activating a National Coast Guard service, which willbe assigned responsibility to assist in offshore oil emergencies. Allmanned platforms will be equipped for fire-fighting and will be providedwith proper emergency escape and survival systems (Annex 14). In addition,ONGC plans to adopt the North Sea safety regulations during construction,and has commissioned an in depth study of the environmental and safetyaspects of the project. The study will be financed by UNDP.

N. Project Risks

4.27 The risks normally associated with hydrocarbon development projectsare compounded for offshore ventures by weather conditions. However, overthe years the industry has developed techniques and technologies which, ifthey do not eliminate risks, reduce them to an acceptable level. The tech-nical solutions selected by ONGC have been proved reliable, ONGC's con-sultants have considerable experience in the design and construction ofoffshore and onshore facilities, and experienced contractors will be selectedfor project implementation. ONGC's staff is qualified and experienced in allthe facets of oil and gas production, processing and utilization and, there-fore, the risk of errors in design and/or operation is minimal. Weatherconditions, however, are not predictable and may cause delays despite theprecautions taken to avoid major construction work offshore during the monsoon.

4.28 9'ere is a risk that the fields will not live up to ONGC's expecta-tions. It is impossible to fully predict the behavior of a reservoir, andfields have been known to "dry up" much sooner than expected. ONGC has beencareful and conservative in its approach to the evaluation of the fields and

- 20 -

has used experienced consultants to assess both the reserves and the produc-tion mechanisms. All estimates are consistent and show that the fieldsshould eventually produce more than was anticipated originally. During theearly years of production, ONGC staff and CFP will monitor the behavior ofthe reservoirs and provide sufficiently advanced warning of any problems forONGC to take remedial actions.

0. Further Expansion of the Bombay High Area

4.29 The two main structures, Bombay High and Bassein North, are underintensive development. Another structure, Bassein South, has been identified,and is a gas field. Other structures at the periphery of BH are still underexploration; several wells have been drilled which have indicated the pres-ence of hydrocarbons but not of commercial quantity. There are several un-explored structures in the area which, on the basis of seismic data, appearto be as promising as the two Bassein fields. It is likely that the total oiland gas recovery from this area will exceed what is currently planned for BHand BN. For this reason the pipeline and platforms have been designed for ahigher ultimate capacity so as to avoid costly capacity expansion if more oiland/or gas is discovered. This is standard practice in offshore development,and the impact on the project cost is minimal as the costs of the pipeline andof the platforms are not very sensitive to size.

4.30 The Bassein South field will not be developed in the near futuresince there is no immediate outlet for the gas. Several alternatives arebeing considered for the future utilization of this gas, the most likelybeing to use the gas in the Trombay area or in Gujarat.

V. JUSTIFICATION-

A. General

5.01 The discovery and development of Bombay High and Bassein representsa significant step towards India's self-sufficiency in petroleum. Untilrecently, it was expected that the share of onshore production in totalpetroleum requirements would decrease in relative terms, although productionwould continue to increase at about 4% per annum. The development of offshorefields will reverse this trend and total domestic production from onshore andoffshore fields is now expected to reach about 50% and 36% of total internalrequirements in 1985 and 1990, respectively, thus saving India about US$16.0billion over the next 20 years.

- 21 -

B. Sector Objectives

5.02 ONGC is, and will continue to be, the main oil exploration anddevelopment agency in India, either on its own, as in the case of BombayHigh, or in association with foreign oil companies which are currentlyoperating under production-sharing contracts. In spite of its lack ofexperience offshore, ONG has managed the development of a giant field 1/very efficiently . The Commission has used outside consultants and contrac-tors to assist their staff in the design of the program and in the construc-tion of the first stage, while training their staff in offshore developmenttechniques. Faced with the single largest development program in the historyof India's oil and gas sector, the Government has taken steps to make foreignexchange available in time and to eliminate bureaucratic procedures, whichmight have delayed the program. India's offshore potential remains, how-ever, largely unexplored, and Bombay High is only the first step in a longprocess which could eventually lead to self-sufficiency in oil. It iscurrently estimated that about US$1.5 to 2 billion would have to be invested,in exploration alone, over the next 10 years to fully evaluate India's poten-tial. Part of the resources required may be provided by foreign oil companiesunder production-sharing contracts. However, the GOI and ONGC will have toallocate a substantial part of the income generated by Bombay High to financetheir own share of exploration and to develop any new resources that may bediscovered, if the current offshore momentum is to be maintained in thefuture.

5.03 For the first time, the Bank has been directly involved in the oiland gas sector. Its initial involvement, in the preparation of terms ofreference for the utilization of natural gas, was extended to the preparationof terms of reference for the initial feasibility studies of Phase III of thedevelopment program and the review of consultants' proposals. During thepreparation of the Project, the GOI, ONGC and the Bank have identified anddiscussed a number of institutional issues which have been or are in theprocess of being resolved satisfactorily, i.e., long-term planning and budget-ing (paras. 6.06 and 6.07), ONGC's management information system (para. 6.08)and the need for external consultants in project management (para. 4.19) andreservoir engineering (para. 4.03). But these are only the first steps in thestrengthening of ONGC's managerial and operational capabilities, which isrequired to manage the much larger and complex exploration and developmentprogram that lies ahead. The role of the Bank should therefore be viewed in asomewhat broader perspective, which is to assist ONGC in building up anorganization which will help India become self-sufficient in petroleum in the

1/ By industry standards, a giant field is a field that would yield morethan 500 million barrels (about 70 million tons) of recoverable oilreserves.

- 22 -

minimum possible time at least cost. One of the areas in which the Bank hasbeen and will continue to be of immediate assistance is in providing adviceon how the methods used by oil companies to evaluate the feasibility of oildevelopment projects (para. 5.05) can be used in ONGC's context.

C. Justification of the Bombay High Offshore Development Program

5.05 Oil companies have developed financial analysis procedures toassist management in deciding which projects should be developed and in whichorder, and how limited capital funds can be allocated in the most efficientway. To do this two levels of analysis are required. First, each projectmust yield a discounted cash flow (DCF) rate of return and payout time whichsatisfy the profitability and cash flow objectives of the enterprise. Second,since there are several ways in which a field can be produced, the rate of re-turn on incremental capital outlays for different alternatives must be eval-uated. While these procedures were originally developed for privateoil companies, they also apply to national oil companies such as ONGC.

5.06 The evaluation of the Bombay High Offshore Development Program(BHDP), including Phases Ito V, has been carried out on the basis of theproduction schedule-derived from the De Golyer and MacNaughton studies (para.4.02) and under two different price assumptions (US$13 per barrel, whichis the present international price and US$5 per barrel which is the priceset by the GOI for offshore crude oil). The results of the analysis arein Annex 22 and are summarized below. The purpose of this evaluation isto determine the impact of the entire program, as opposed to the Project,on the economy of India (US$13/barrel, excluding income tax) and on ONGC'scurrent and future financial viability (US$5/barrel, including income tax).

t

- 23 -

Summary Evaluation of the Bombay High Offshore Development Program

US$13/barrel US$5/barrelexcluding income tax including income tax

DCF return (%) 66.2 19.8

Maximum negativeCash Flow (Rs million) 3,238 6,129

Pay out time fromApril 1, 1977 (years) 1.7 4.8

Net Present Value(Rs million) at discountrates of:

- 10% 60,138

- 20% 30,258

- 40% 9,720

5.07 At US$13/barrel, excluding income tax, the development of BombayHigh and North Bassein would yield a DCF return of 66.2%. The Net PresentValue (NPV) of the savings generated by the Program at the opportunity costof capital (estimated at 10%) would be Rs 60,138 million (US$6,682 million)over the life of the fields, reflecting a discounted production cost perbarrel of about US$3.15 per barrel.

5.08 At US$5/barrel, the Program would yield a DCF return after taxesof 19.8% to ONGC. This return is comparable to what international oil com-panies normally require for their domestic operations and is consideredsatisfactory. The following table summarizes the breakdown of the cost ofoil per barrel calculated on the basis of annual depreciation:

Breakdown of the cost of oil per barrelUS$/barrel %

Exploration .33 5.5Production Cost /1 1.76 29.5Taxes 2.24 37.5Net profit 1.64 27.5

Total 5.97 100.0of which income derivedfrom natural gas and LPG .97

/1 Includes operating cost, depreciation and financial charges.

- 24 -

This shows that the current price of US$5/per barrel to ONGC is adequate tocover production and exploration costs, and generate a reasonable profitafter tax. Each discovery should, however, be considered as a separateproject and it would therefore be appropriate for the GOI to reconsider theprice paid to ONGC for oil and natural gas so that, within the limits set byinternational prices, prices are set at a level which would permit an effi-ciently operated ONGC to earn an acceptable DCF return and to finance areasonable portion of its exploration and development. Since ONGC's marketfor crude oil and natural gas is a captive market and since ONGC does notincur any political risk in its domestic operations, a DCF rate of returnof 15% over the life of the project would be considered satisfactory.

D. Economic Justification

Market

5.09 The production of Bombay High and Bassein North will consist ofcrude oil and associated gas. After treatment, the latter will yield leangas, consisting mainly of methane and liquefied petroleum gas (LPG) consistingof butane, propane and heavier fractions. The estimated production schedulefor these products is given in Annex 24. The three products -- crude oil,associated gas and LPG -- have different markets which have been investigatedseparately. Bombay High and North Bassein crude oil will be substituted forimports, lean gas will be used as feedstock in the fertilizer industry andLPG will be used initially in the residential and commercial sector. Thecost of the facilities required to utilize these products is estimated atUS$32.3 million of which US$10 million would be required to carry out minormodifications to existing refineries, US$18 million would be required forthe conversion of the Trombay fertilizer plant and US$4.3 million for LPGstorage and distribution facilities (Annex 24).

Cost/Benefit Analysis

5.10 Several production schedules for the Bombay High Field, involvingdifferent drilling and investment programs, were investigated by De Golyerand MacNaughton in their studies. Two cases were selected on technicalgrounds and a cost/benefit analysis was carried out to compare their eco-nomic merits. Details of the analysis are given in Annex 23 and summarizedbelow.

- 25 -

Summary Evaluation of Bombay High Development Program

Case I Case II

Life of the field (years) 31.0 31.0

Total oil recovered(million tons) 170.0 158.0

% of oil in place 21.0 19.5

Peak production(000 barrels per day) 225.0 280.0

Duration of plateauproduction (years) 8.0 2.0

Rate of return (%) 93.2 91.4

Net present value /1(US million) at discountrates of:

10% 4,787 4,585

20% 2,527 2,456

40% 866 845

/L Over 15 years.

ONGC current development plans are based on the first case which maximizeoil recovery and avoid the construction of peak facilities which would beused for a short period of time.

5.11 Annex 23 provides the assumptions used in the economic evaluationof the development program. On the basis of present international pricesfor crude oil (US$13/barrel) and-of the prices at which ONGC will sellnatural gas and LPG (US$55,000 m and US$90/T) the program would yield aneconomic return of 165% if sunk costs are excluded. If sunk costs are in-cluded the economic return would be 66%. Since sunk costs are essentiallyexploration and early development drilling expenditures, the latter pro-vides a better appreciation of the economic feasibility of the entire pro-gram. The economic return is not very sensitive to variations in the pro-gram costs; an increase in the program cost of 20% would bring the economic

- 26 -

return to 56%. It is more sensitive to delays in production; a delay of oneyear in the production schedule would bring the return to about 50%, which,however, would still be satisfactory. No attempt has been made to calculatean incremental return for the project since the facilities included in PhaseIII cannot be dissociated from those already constructed under Phases I andII and those planned for Phases IV and V.

VI. THE OIL AND NATURAL GAS COMMISSION

A. General

6.01 The Oil and Natural Gas Commission is a Government owned statutorybody created in 1959 by an Act of Parliament to "plan, promote and imple-ment the development of petroleum resources and the production and sale ofpetroleum products produced by it." ONGC's statutes provide that it is acorporate body with power to acquire, hold and dispose of property and tocontract. ONGC has authority to borrow. The Commission consists of aChairman, and not less than two and no more than eight Members appointed bythe Government for a period of five years.

6.02 At present, the Commission consists of the Chairman, four full-timeMembers (Finance, Materials, Production and Exploration) and of two part-timeMembers representing the Ministry of Finance and the Ministry of Petroleum.All decisions of the Commission must be approved by the majority of the mem-bers. ONGC owns Hydrocarbons India Ltd., a subsidiary which is in chargeof the Commission's ventures abroad (Iran, Iraq and Tanzania).

B. Organization and Management