FIFO Costing

13

FIFO Costing: EBS Manufacturing’s best-kept secret David E. Sweas | Manager, Technology Solutions | Grant Thornton LLP Abstract In today's challenging economic environment, manufacturers and distributors have an increasing need for accurate product profitability and cost of goods sold (COGS) information. The FIFO Costing feature of the Oracle E-Business Suite (EBS) Discrete Cost Management application is an automated actual costing tool that is easy to implement, use and control, and which delivers timely and accurate material COGS and inventory valuation. This white paper explains what FIFO Costing is, how it is generated and viewed in EBS, and the factors to be considered in implementing FIFO Costing and its fit for the entity. The paper also compares and contrasts EBS FIFO and Standard Cost, and touches on how to change an organization’s EBS costing methods. One other point worth mentioning is that this white paper covers only EBS Discrete FIFO; EBS Process Manufacturing also contains actual costing functionality, which differs from Discrete in several key areas. About Grant Thornton Grant Thornton LLP is an international audit, tax and advisory services firm based in Chicago. Within the Business Advisory Services practice is its national Technology Solutions (Oracle) group, of which the author is a member of the EBS Financials and Cost Management implementation team. Grant Thornton’s Oracle practice is an Oracle Platinum Partner. Overview and features of FIFO Costing Oracle EBS FIFO Costing is an actual item costing feature available in both Releases R12 and 11i. It is based, in a sense, on the accounting valuation principle of specific identification and grounded in the time-honored textbook accounting concept of first in, first out (i.e., “last in, still here”). FIFO Costing uses the most recent actual material purchase price for valuing Buy Item Material (MTL) transactions. For Make items, it uses actual Material, Outside Processing (OP) purchase price and Resource Rates, plus actual Material and Resource usage, for valuation of MTL Completion transactions. FIFO values MTL Transactions, including COGS. As a byproduct, FIFO also values on-hand inventory at any point in time (without running any incremental processes other than the ongoing Cost Manager). Like other EBS Costing Methods (Standard, Average and LIFO), the FIFO Costing method is specified at the Inventory Organization level and pertains to all items of that Organization. Like other costing methods, once it is in place and items have been assigned to the org, the FIFO Costing method flag cannot be changed in a manner that Oracle will currently support.

description

FIFO Costing

Transcript of FIFO Costing

FIFO Costing: EBS Manufacturing’s best-kept secret David E. Sweas | Manager, Technology Solutions | Grant Thornton LLP Abstract In today's challenging economic environment, manufacturers and distributors have an increasing need for accurate product profitability and cost of goods sold (COGS) information. The FIFO Costing feature of the Oracle E-Business Suite (EBS) Discrete Cost Management application is an automated actual costing tool that is easy to implement, use and control, and which delivers timely and accurate material COGS and inventory valuation. This white paper explains what FIFO Costing is, how it is generated and viewed in EBS, and the factors to be considered in implementing FIFO Costing and its fit for the entity. The paper also compares and contrasts EBS FIFO and Standard Cost, and touches on how to change an organization’s EBS costing methods. One other point worth mentioning is that this white paper covers only EBS Discrete FIFO; EBS Process Manufacturing also contains actual costing functionality, which differs from Discrete in several key areas. About Grant Thornton Grant Thornton LLP is an international audit, tax and advisory services firm based in Chicago. Within the Business Advisory Services practice is its national Technology Solutions (Oracle) group, of which the author is a member of the EBS Financials and Cost Management implementation team. Grant Thornton’s Oracle practice is an Oracle Platinum Partner. Overview and features of FIFO Costing Oracle EBS FIFO Costing is an actual item costing feature available in both Releases R12 and 11i. It is based, in a sense, on the accounting valuation principle of specific identification and grounded in the time-honored textbook accounting concept of first in, first out (i.e., “last in, still here”). FIFO Costing uses the most recent actual material purchase price for valuing Buy Item Material (MTL) transactions. For Make items, it uses actual Material, Outside Processing (OP) purchase price and Resource Rates, plus actual Material and Resource usage, for valuation of MTL Completion transactions. FIFO values MTL Transactions, including COGS. As a byproduct, FIFO also values on-hand inventory at any point in time (without running any incremental processes other than the ongoing Cost Manager). Like other EBS Costing Methods (Standard, Average and LIFO), the FIFO Costing method is specified at the Inventory Organization level and pertains to all items of that Organization. Like other costing methods, once it is in place and items have been assigned to the org, the FIFO Costing method flag cannot be changed in a manner that Oracle will currently support.

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 2

FIFO Costing is a “perpetual item costing engine.” Note that Cost Rollup and item cost maintenance are not required in a FIFO Costing Organization. FIFO Costing utilizes actual cost of Material and OP Elements. It also captures actual Resource costs (if these costs are captured in Resource Rates via external interface, Oracle Payroll, etc.) In addition, Make items when manufactured capture not only the Material, OP and Resource actual costs, but actual usage of Material (and hence Material Overhead), Resource, Overhead (via its Resource Association), and OP. Given this feature, no general ledger (GL) variances are produced. FIFO Costing produces a FIFO Cost Layer, consisting of all transaction quantity for an item on a given PO Receipt or WIP Completion. The configuration behind FIFO Costing is quite simple. Two Cost Types are required: the seeded FIFO Cost Type, and one that is a user-specified Cost Type for FIFO Rates. These Cost Types are covered in more detail in the following terminology section. Additionally, a Cost Variance Account is required on the Org Parameters form. This GL Account captures the slight journal entry (JE) impact that results when a FIFO Layer is “over-consumed” via an item’s on-hand quantity being driven below zero, then positive. Finally, an optional but recommended setup is a separate GL Account for the impact of a Layer Cost Update. This Account is entered at the time the Concurrent Request for the Layer Cost Update is submitted. (Please see the following terminology section for Layer Cost Update definition.) Terminology There are several key terms within FIFO Costing. Two Cost Types are required: FIFO and a user-specified Cost Type for FIFO Rates. FIFO Cost Type is seeded for a FIFO Inventory Org. This is where the above-mentioned MTL Transaction costs are captured, by Element. The Cost Type that is user-specified is entered into the Inventory Org Parameters, in the FIFO Rates field. FIFO Rates is where the material overhead (MOH) Rates, Resource Rates, Overheads and OP Rates (OP whether manually maintained or via PO price) are entered. Another important term is FIFO Cost Layer. Layers are at the Item level, consisting of all quantities within an MTL transaction of Receipt or Completion. A Cost Layer, once auto-created, is then auto-depleted (consumed, shipped, transferred, adjusted off, etc.) on a first in, first out basis. That Layer is fully depleted before the next Layer created can be decremented. New Layers can be built alongside existing Layers. (For example, three individual Receipts of an item will result in three Layers, even if the cost of the item in each Layer is same. The consumption will be out of the earliest of those three Layers.) Layers are assigned a system-generated identification number. It is important to note that there is no EBS or GAAP requirement that the quantity within a Layer be specifically tracked in and physically transacted from that Layer. Experience with the author’s clients is that EBS FIFO Costing has withstood audit tests and has been accepted for GAAP inventory valuation purposes. Equally worth noting is that FIFO Cost Layers are auto-created and auto-maintained without regard to Lots and Serialization. Another important term is Layer Cost Update. Layer Cost Updates are utilized to correct an item’s FIFO cost within a Layer or Layers (due to PO Price error, Resource Rate error, etc.). The goal should be to always avoid using the Layer Cost Update. As discussed below, Layer Cost Updates can become time-intensive when there is a need to correct multiple Layers of a Make item, due to the need to locate the related Layer(s) that are improperly costed and still on hand. It goes without saying that a reasonable degree of accuracy in PO prices, bill of materials (BOMs), Routings and transaction quantities is the discipline required to make FIFO Costing successful.

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 3

Simple FIFO Costing example In order to illustrate the mechanics of FIFO Costing in EBS, below is a simple non-EBS example using Receipts of a Buy Item and manufacture of a Make Item. Assume MTL transaction activity as such: Raw material Item A has purchases of 100 units at $1 per unit (Layer 1 is auto-created). A second purchase of 100 units at $1.20 per unit auto-creates Layer 2. Result: Two 100-quantity Layers are on hand at a total value of $220. Assume Make Item B (finished goods) has BOM quantity of 1.00 of Item A. After the raw materials have been purchased as above, 160 units of Item B are produced, which consumes 160 units of Item A. These units of Item A are consumed out of Layers 1 and 2 on a FIFO basis, valued as such: 100 units x $1 consumed from Layer 1, and 60 units x $1.20 consumed from Layer 2. On-hand inventory value is now: Finished goods Item B = $172 (100 x $1.00) + (60 x $1.20). Raw material Item A = $48 (0 x $1.00) + (40 x $1.20). When the 100 units of Item B are shipped, COGS will be debited for $172 and finished goods inventory credited for $172. Thus, the COGS of $172 is recorded on a FIFO basis. FIFO Costing example in EBS To further illustrate the mechanics of EBS FIFO Costing utilizing screen views from the Cost Management application, see the following example. In viewing the Item Cost History screen in Exhibit 1, note that there are presently on hand 100 units of Item CM22680, at a FIFO Layer Cost of $27.25 per unit. Also observe that there was zero on-hand quantity prior to the addition of the current 100 units. In addition, observe that the cost of the previous Layer at the time it went to zero was $27.25. The reason the current 100 units are at the same $27.25 per unit FIFO cost is that only a PO Receipt Delivery or Completion can create a new FIFO cost. Since the current 100-quantity Layer was created as an Account Alias Receipt (note that in Exhibit 1), the cost of that new Layer is at the previous Layer’s cost of $27.25. Exhibit 1: Item Cost History screen after Account Alias Receipt

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 4

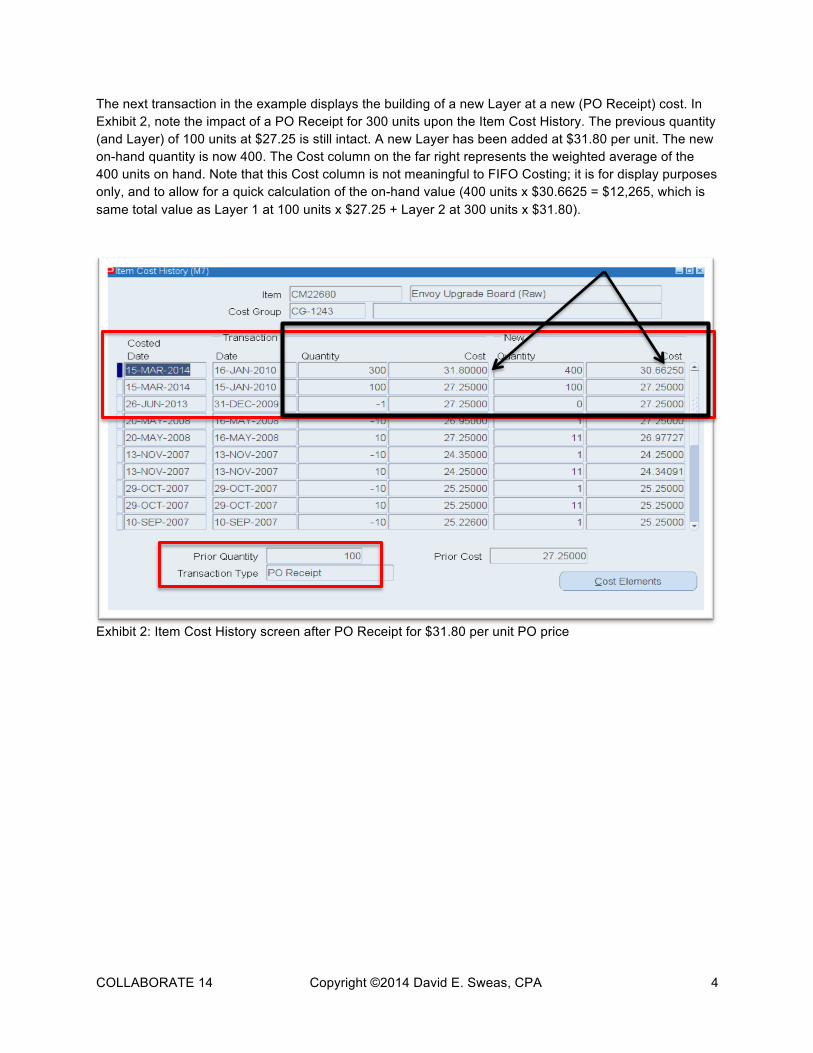

The next transaction in the example displays the building of a new Layer at a new (PO Receipt) cost. In Exhibit 2, note the impact of a PO Receipt for 300 units upon the Item Cost History. The previous quantity (and Layer) of 100 units at $27.25 is still intact. A new Layer has been added at $31.80 per unit. The new on-hand quantity is now 400. The Cost column on the far right represents the weighted average of the 400 units on hand. Note that this Cost column is not meaningful to FIFO Costing; it is for display purposes only, and to allow for a quick calculation of the on-hand value (400 units x $30.6625 = $12,265, which is same total value as Layer 1 at 100 units x $27.25 + Layer 2 at 300 units x $31.80). Exhibit 2: Item Cost History screen after PO Receipt for $31.80 per unit PO price

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 5

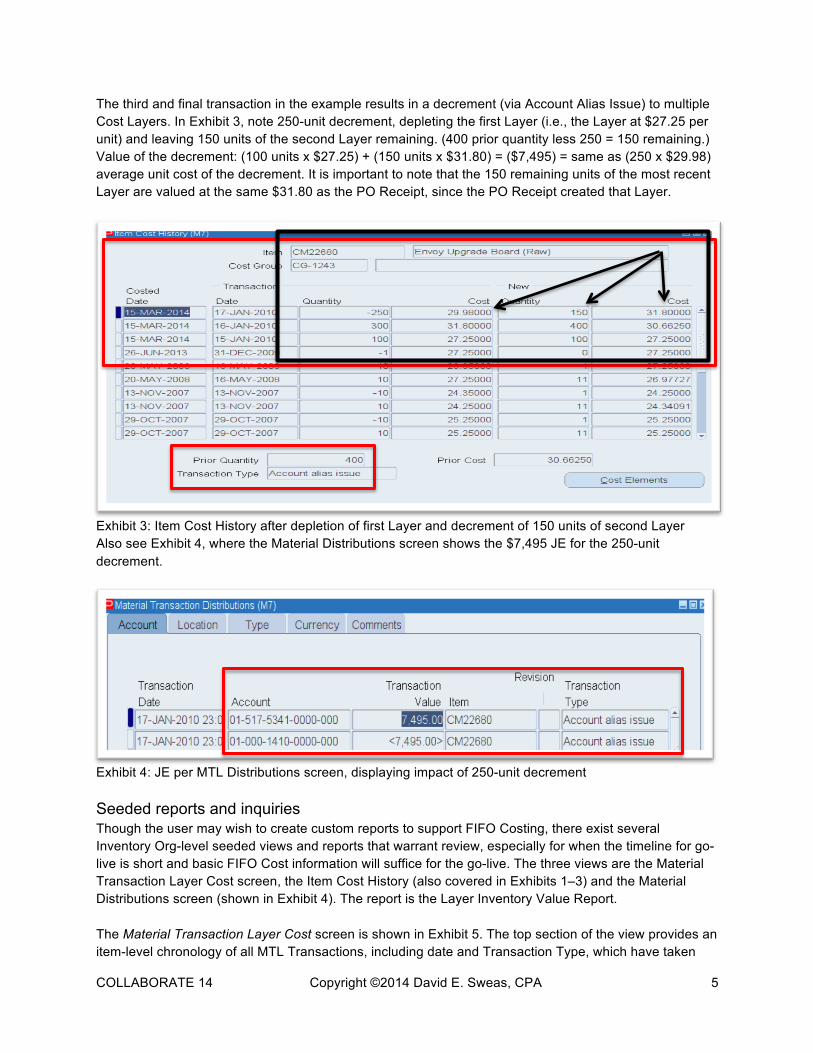

The third and final transaction in the example results in a decrement (via Account Alias Issue) to multiple Cost Layers. In Exhibit 3, note 250-unit decrement, depleting the first Layer (i.e., the Layer at $27.25 per unit) and leaving 150 units of the second Layer remaining. (400 prior quantity less 250 = 150 remaining.) Value of the decrement: (100 units x $27.25) + (150 units x $31.80) = ($7,495) = same as (250 x $29.98) average unit cost of the decrement. It is important to note that the 150 remaining units of the most recent Layer are valued at the same $31.80 as the PO Receipt, since the PO Receipt created that Layer. Exhibit 3: Item Cost History after depletion of first Layer and decrement of 150 units of second Layer Also see Exhibit 4, where the Material Distributions screen shows the $7,495 JE for the 250-unit decrement. Exhibit 4: JE per MTL Distributions screen, displaying impact of 250-unit decrement Seeded reports and inquiries Though the user may wish to create custom reports to support FIFO Costing, there exist several Inventory Org-level seeded views and reports that warrant review, especially for when the timeline for go-live is short and basic FIFO Cost information will suffice for the go-live. The three views are the Material Transaction Layer Cost screen, the Item Cost History (also covered in Exhibits 1–3) and the Material Distributions screen (shown in Exhibit 4). The report is the Layer Inventory Value Report. The Material Transaction Layer Cost screen is shown in Exhibit 5. The top section of the view provides an item-level chronology of all MTL Transactions, including date and Transaction Type, which have taken

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 6

place since the initial transaction. It can be filtered by beginning and end date, as well as Cost Layer. The bottom of the view is a summary of the item’s Cost Layers currently on hand. (Note that the data is for same item as reviewed in the previous section.) A key difference between the Material Transaction Layer Cost and the Item Cost History is that the Item Cost History does not display the system-generated Layer Number. The key feature of the Item Cost History (again, referring to Exhibits 1–3) and a difference between it and the Material Transaction Layer Cost is that the former displays both transaction chronology and on-hand balance throughout the timeline displayed. This can be useful for certain analyses. The Material Distributions screen is the same screen view as is present in a Standard Costing Org. (Again, refer to Exhibit 4.) Note that, as in Exhibit 5, which reflects the Account Alias Issue in which two Cost Layers were impacted, the Material Distributions screen aggregates all Layers for the transaction into one total JE. For example, in Exhibit 5, the $7,495 total is for values from two Cost Layers. The Material Distributions screen is useful for reviewing summarized FIFO Cost journal entries. The Layer Inventory Value Report is basically the Elemental Inventory Value Report used in Standard and Average Costing Orgs, except that it also contains FIFO Cost Layers for the on-hand inventory. See Exhibit 6. This report reflects the same data as seen at the bottom of the Material Transaction Layer Cost. Note that it also contains the Elemental breakout contained in the Elemental Inventory Value Report. When you give each Element on the Org’s Sub-Inventory setup a different Account Combination, you can tie each Element’s grand total per Layer Inventory Value Report to the GL Account Combination of the respective Sub-Inventory Element. As such, this report is commonly used both as an ongoing reasonableness check upon the inventory value and GL balances, and as an inventory valuation prepared by client (PBC) for year-end audits. Exhibit 5: Material Transaction Layer Cost for sample item

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 7

Exhibit 6: Layer Inventory Value Report (Note same sample item as in Figures 1-5) Comparison: EBS Standard versus FIFO Costing As Standard Costing has historically been the overwhelming choice among Costing Methods for EBS supply chain installs, a comparison of Standard to FIFO Costing is worthwhile. As one might expect, there are significant differences between Standard and FIFO, not only in the data capture and display, but also in the ongoing processing and control. A discussion of these comparisons follows. The most significant difference between these two Costing Methods is the absence of a Cost Rollup and Cost Update to calculate a FIFO item transaction cost for a new Make Item in a FIFO Org. This is due to the fact that for FIFO, the Work Order Completion (or Completion without a Work Order in the case of Work Order-less Completion) serves the same purpose as a Cost Rollup in Standard Costing, in that the Completion produces a “rolled up” Make Item cost (including actual rather than standard Material, OP, and Resource usage, and FIFO Material and actual Resource and OP costs). This process is grounded in the concept that a Make item transactional cost is not needed until the point of the Work Order Completion. As discussed below, this is a major consideration for companies seeking productivity improvements in the cost accounting area of Finance. This difference is also a major paradigm hurdle for many entities. Equally as important for a FIFO Org is the fact that a Cost Rollup is not needed to capture BOM and Routing changes for transaction and inventory valuation purposes. (Changes may be due to product spec revisions, product reconfigurations, cost savings, process improvements, etc.) As with a new Make item, FIFO Costing produces a new rollup cost for an existing Make item at the time the Completion has been performed. Another feature of FIFO Costing is that the costing of the Make item at time of Completion safeguards against uncosted Make items, while in a Standard Costing Org the cost accountant must ensure that a Cost Rollup (and related Cost Update to Frozen) are run by the time the Completion is performed. Here again, the process efficiency/hands-off approach provided by FIFO Costing is appealing. One other area of time and effort savings for a FIFO Organization is that of new Buy item cost maintenance. In a Standard Costing Org, the Buy item standard cost must be entered to Frozen

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 8

prior to the PO Receipt Delivery. In a FIFO Org, this manual new Buy item cost maintenance is not needed. An area related to item cost maintenance that must be included in a comparison of Standard and FIFO Costing is that of correction of item cost errors. In Standard, the process would be to correct the Buy item cost or reroll the Make item cost, run the Cost Update to populate the cost to Frozen, and assess and address the financial impact on the P&L (e.g., offset to usage variance, purchase price variance (PPV), etc.). The cost correction resulting from the Cost Rollup would automatically correct all of the related item costs via the handoff from the BOM structure and Sourcing Rules (the latter if Supply Chain Costing is in use). In a FIFO Costing Org, the process would be to first calculate and validate the cost(s) by rolling up each incorrect item in a non-FIFO Cost Type, then performing a Layer Cost Update to correct the Layer(s) for each item that needs it. This would also include Buy item costs as necessary. Since the Make item costs are not corrected via the BOM and Sourcing Rules, this can be a very involved process in a FIFO Costing Org when multiple Layers, multiple items and more than one Inventory Org are affected. Obviously, transaction integrity and PO price relative accuracy are essential in a FIFO Org (though they are also essential in a Standard Costing Org, where the goal is to have meaningful variance reporting). Since accuracy in transactions and PO pricing affect not only FIFO Costing and variance reporting but also certain core business processes (supply chain planning, accounts payable (AP) invoice processing, customer service, inventory management), good practices in transaction processing and PO pricing are foundational to enterprise resource planning, with the side benefit of favorable impact on Costing (true no matter the Costing Method employed). One other disadvantage of the FIFO Layer Cost Update is the absence of a Pending (i.e., preliminary) Cost Update as exists in Standard Costing. Two final areas of item cost maintenance that must be included in the comparison of Costing Methods: Actual cost inventory valuation (normally required for financial statement presentation — GAAP, International Financial Reporting Standards (IFRS), etc.) and standard cost revaluation (for purposes of reflecting raw material price changes or usage variances, for example). In a Standard Costing Org, valuation of inventory at actual is accomplished via the Cost Mass Edit feature and full Org Cost Rollup at a specified point in time (based on Effectivity Date) BOM and Routing, then Cost Update to Frozen. In a Standard Costing Org, revaluation is arrived at via Buy item (historical or average) cost input, full Org Cost Rollup and Cost Update to Frozen, including the various analyses and Cost Rollup iterations that must accompany this process before the final Cost Update can be run. The timing is normally annual, though quarterly and monthly revaluation is often used when raw material price volatility is a factor. In a FIFO Costing Org, revaluation is not necessary, as the ongoing actual costing process ignores variances and includes actuals in the item cost. Both the Standard Costing revaluation process and the FIFO ongoing costing are designed with the goal of valuing the future COGS at actual cost. Note that FIFO Costing does this with no additional effort. Though Cost Rollups are not needed in order to value transactions in a FIFO Org, the question becomes: Are they permitted for what-if purposes or to measure effect of BOM/Routing changes, for product pricing decision support, etc.? The answer is that Cost Rollups can be run in a FIFO Org. The requirement is that the Cost Rollup must be run in a Cost Type other than FIFO. The process (Concurrent Request) to run a Rollup in a FIFO Org is identical to the process in a Standard Cost Org. Also it is important to point out that although the Supply Chain Costing feature does not populate FIFO item costs across Inventory Orgs as it does for Standard Costing Orgs, the supply chain cost rollup (SCCR) feature is for non-FIFO Cost Types in a FIFO Costing Org. The next area examined in the comparison is variance capture. FIFO Costing produces no variances, while Standard Costing produces PPV, material usage and Resource efficiency variances. The author

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 9

has experienced FIFO Costing implementations where custom reports have been written to capture usage and efficiency variances for management reporting purposes (i.e., even though FIFO Costing does not calculate variances for financial reporting, the data needed for variance tracking always exists in EBS). Even in a Standard Costing Org, it is common for variance reports to be customized due to inherent shortcomings in the seeded EBS variance reporting. Refer to the following section, Implementation Considerations, for a more in-depth discussion of upfront variance considerations included in a decision to implement FIFO Costing. It can be inferred from the comparison discussion that accuracy in material PO price maintenance is the most critical, fundamental factor in the enabling of FIFO Costing. As this can be an ownership and priority issue in many companies, it warrants attention. First of all, when material PO prices are not maintained by the time of PO Receipt and Delivery (not needed at time PO is cut, only when PO received) this will also have an adverse effect on the efficiency of the EBS three-way matching process. A related point is that the Transfer IPV to Work Orders functionality, available in an Average Costing Org, is not available in a FIFO Org. Secondly, though most raw material pricing can be ascertained prior to PO Receipt (via contracts, blanket PO (BPOs), PO lead times, etc.), some raw material prices cannot be fully known prior to Receipt (possibly due to industry practice). This would result in an after-the-fact Layer Cost Update. The impact of this practice must be understood before a decision to implement FIFO can be made. A recommendation (short of having the cost accountant review PO pricing upfront) is to retrofit the Expected Receipts Report to flag any upcoming Receipts that have missing or unreasonable PO prices. This has proven to be a simple, successful overall approach in several FIFO installs that the author is familiar with. The point is that proactive data controls (upfront PO price quality assurance/verification) will minimize the need for after-the-fact item cost fixes via Layer Cost Update. There are two areas of EBS supply chain transactions wherein Standard Costing will produce consistent results regardless of transaction timing, while FIFO Costing will require more discipline regarding transaction timing; one is Work Order Completions timing with Material Push (Component Issue) and/or Resource Manual Charge Type. The other is Interorganizational Transfers. In a FIFO Org, for both Material Push and Manual Charge Type, the goal is to keep the Material and Resource charges synced with Completion activity. In order words, if material is being added to the Work Order in 25% increments, there should be four Completions (one after each Push transaction), so that each of the four Cost Layers is created using the actual usage quantity. This actual quantity would include quantity inaccuracies. However, an attendant question would be: Are the Push quantities subject to variation versus BOM? If not, or if the variation is not significant, Assembly Pull (backflush) of Work Order components should be considered (if that election is consistent with the entity’s materials management and planning requirements). Or, if Push is required and there is variation versus BOM but the variation is insignificant, consider setting the flag “Auto Compute Final Completion” to Yes (in WIP Parameters). This will value each incremental Completion and its Cost Layer at component FIFO Costs and BOM quantities (thus making relative timing of Push irrelevant, until the final Completion). When the final Completion takes place (final Completion takes place when the total incremental Completion quantity reaches 100% of planned Work Order quantity), it absorbs all accumulated BOM variation onto the cost of that final Layer. Any Completion and Layer Cost created after the planned Completion quantity has been reached will be valued at component FIFO Costs and BOM quantities. Any Push quantity taking place after there are no more Completions will fall into Job Close Variance when the Work Order closes. (To contrast this with Standard Costing: In a Standard Org any Push taking place after final Completion will go to usage variance, not to Job Close Variance.) If all Work Orders use 100% Assembly Pull, then the difference between the Org’s material cost of Completion in FIFO versus Standard Costing Org will be that FIFO has valuation of Completion at Work Order BOM quantity x FIFO cost of components, while Standard (in Frozen Cost Type) uses rollup captive BOM quantity x rollup captive item costs.

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 10

For Resource charges (basically labor hours — normally not machine hours), a similar sync with Completions is needed. As in the discussion regarding material Push, the Completion would build a Cost Layer using the actual Resource quantity (including any inaccuracies). Note also that the option of Auto Compute Final Completion does not enable charging of the Routing quantity per incremental Completion as it does for materials. Therefore, if it is optimal to use Routing quantities as opposed to actual hours for FIFO Completion value of Resources, having the WIP Move Charge Type on the Org Resources should be considered. Bear in mind that companies using Resource Charge Type of Manual will normally be job shop operations using a shop-floor labor data collection system like Oracle Time and Labor or a third-party system with interface to WIP; therefore, the ability to sync with incremental Completions becomes highly manageable. You must also specify (in the Costing tab of the WIP Parameters) whether you wish to use the Actual Resource Rate (from the FIFO Rates Cost Type) or fetch the Resource Rate from another specified Cost Type. Remember that this Rate fetch will also pertain to OP, so careful thought should be given before choosing the User Defined Cost Type option Interorganizational transfers is the other area of EBS supply chain where Standard Costing Orgs afford consistency in transaction valuation, while FIFO Orgs require careful coordination. Assume an item is shipped from FIFO Org A to FIFO Org B. Org B will receive the Layer Cost of the item from Org A in the Interorg Transfer (or the Standard Cost from Org A, if Org A is a Standard Cost Org). If Org B allows negative quantities, and consumes the item in WIP or transfers it before recording the Receipt from Org A, the Layer Cost issued or transferred in Org B will be zero. In order to mitigate the risk of this possibility when it is procedurally not possible to sequence the transactions, Org B’s Org Parameters could set Allow Negative Balances to No, or the Org A to B Shipping Network Transfer Type could be set to Direct. A Standard Costing Org would not have the above-mentioned risk of uncosted transfer. There are other, less significant comparisons between Standard and FIFO Costing Orgs that are covered here: Among them are the ability to vary GL Accounts by Subinventory. This can be done in a Standard Costing Org, but not in a FIFO Org that does not have EBS WMS installed. (While a difference in 11i, in R12 this difference in Standard versus FIFO Org at the Subledger level is totally mitigated by the use of sub ledger account (SLA) mapping.) Another difference is in how item costs are displayed on the Item Costs Summary form: For a FIFO Org, the costs are a weighted-average cost across all Layers (same as was seen in the Item Cost History screen example above). The following features are supported in both Standard and FIFO Cost Orgs: Cost Copy, COGS Recognition (pertains to R12 only), R12 Cost Management SLA, MOH and OH absorption calculations, and all key Cost Management seeded reports and views (including several others covered in the Seeded Reports and Views section). FIFO Costing — Key implementation considerations To understand the discussion about implementation considerations, it is helpful to first recap the current landscape for many discrete manufacturers. Discrete manufacturers find themselves at a point in time where raw material prices are under increasing pressure, far from the low to moderate inflation days of the past. Material costs continue to average anywhere from 65–80% of COGS value. At the same time, price increases passed along to customers are not an option for many without risk to the business. On the finance side of the organization, the trend toward a lean accounting staff has been coupled with the expectation of doing more with less, while management’s appetite for product profitability and gross margin information is greater than ever. Additionally, lean/Kaizen initiatives are being driven throughout many organizations. There is also a general comfort level with traditional standard costing, based on familiarity and similar factors.

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 11

Some of the key considerations in implementing FIFO Costing dovetail with points that were raised in the EBS Standard versus FIFO Organization comparison above. Among the key considerations for FIFO Costing fit for an Organization, the first is a consideration that would apply to any EBS Costing Method: It is not an easy process to change Costing Methods once the Inventory Organization is live. (See the following section, Changing from standard to FIFO Costing organization.) Another factor to consider is that an EBS Standard Costing Org’s on-hand inventory value cannot be stated at actual (for financial reporting purposes) without some effort (Cost Mass Edit, often several passes at Rollup, and Cost Update, in addition to review and reasonableness checks along the way). Ability to instill the discipline regarding timing and quality of transactions (Material and Resources in WIP and Interorg Transfers) also needs to be considered, including mitigating factors like Assembly Pull (backflush), WIP Move Charge Type, labor collection, Shipping Network setups to control timing of transfers to a FIFO Org, and the fact that accurate transactions are critical to more areas of the business than only Costing. Related to the quality and timing of transactions is relative PO price accuracy, which can be rationalized and controlled by upfront data controls and understanding the relative risk, impact and remediation effort related to the exceptions. A lesser factor to consider (important in and of itself but also necessary at some point in a Standard Costing Org) is BOM and timely Routing maintenance. Noting that after-the-fact item cost maintenance via Layer Cost Update is always a bad thing that can, at times, be a more extensive process than item cost correction in a Standard Cost Org, an honest assessment of these factors must be considered before moving forward with any plan to implement FIFO. General principles guiding a FIFO Org fit analysis are that FIFO fits best when: The greater the number of raw material stock keeping units (SKUs), the greater the raw material price fluctuation, the more the material backflush (Assembly Pull), the greater the number of Resources with WIP Move Charge Type, and the greater the proliferation of finished goods SKUs. Another major factor to be considered is that of process automation (which ties in with several points raised in the above-mentioned current landscape discussion). The impact of no Cost Rollups needed for COGS capture and inventory valuation (and hence no Cost Update, leading to no need for inventory revaluation) represents a large favorable impact upon a typical Finance staff. The process automation factor coupled with the fact that Cost Rollups are also available in a FIFO Costing Org (to be used for what-if purposes, etc.) provides the same Cost Rollup capability that a Standard Costing Org enjoys. Variances are also a key consideration. As noted above, Standard Orgs capture variances in GL, and FIFO Orgs do not. The questions to be pondered are: Do variances actually need to be in GL, or are they for management reporting purposes only? If variances are captured and reported, are they meaningful (i.e., would control over the variances lead to operational improvements that could save money or effort)? Are the variances being captured controllable? Is anyone on the hook for minimizing variances (process variation), or are these just P&L numbers? Some favorable variances may actually have a negative underlying reason. Are favorable variances seen as good, while unfavorable variances are seen as bad? PPV is generally the largest variance (and difficult to allocate in any meaningful way); is PPV meaningful in this entity, or is it an accumulation of incorrect PO prices, incorrect standard costs, or both? If the answers to these questions would make variance reporting suspect or not useful, this would favor FIFO Costing, all other things being equal. There are other considerations; in general, FIFO Costing would not be used for product pricing decision support needs (as mentioned above, in a FIFO Org, new product costing would be calculated via Cost Rollup, including SCCR). Also, FIFO Costing may not be acceptable for certain industries. For example, some U.S. defense contracts require use of average costing. While FIFO Costing may or may not be a fit for certain manufacturers, it is generally a good fit for distributors, who would, of course, own only Buy items and thus would not have the FIFO cost complexities relevant to WIP transactions discussed above.

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 12

Last but not least in determining fit and readiness for FIFO Costing is the need for shifting the general paradigm that surrounds item costing (just as leading practices would dictate that all non-statutory/noncompliance-related accounting requirements should be challenged). For example, the paradigm would need to shift in order to embrace that an EBS item cost is not needed before the time of the transaction (PO Receipt and Work Order Completion), and variance capture in GL may not be necessary (and variances only matter if there is accountability for them). Also, given a normal inventory turns rate, the physical commingling of units of an item across the item’s Cost Layers does not invalidate FIFO’s GAAP/IFRS compliance and its usefulness as an analytical tool. In addition, item costing is a tool for the costing of transactions (especially COGS), while inventory valuation is an important yet secondary byproduct. In any case, before embarking on a FIFO implementation discovery and fit analysis, two tasks should be undertaken. The counsel of outside auditors should be sought (e.g., for GAAP/IFRS compliance, prior year restatement possibilities, any potential considerations regarding physical flow of goods). The second task is conducting a thorough Costing Method requirements workshop with all affected internal parties (Finance and Supply Chain), whether the FIFO Org install is a net-new EBS implementation or addition of a new Inventory Organization. Changing from standard to FIFO Costing organization Oracle presently does not support changes to the Costing Method once a single item has been assigned to the Inventory Organization. In order to change Costing Method, a process similar to a net-new Inventory Organization startup would need to be employed, creating a new Inventory Organization, including Sub-Inventories, Locators, etc., as needed. At the point of go-live conversion, close as many Work Orders as possible, and ensure no Pending or Uncosted MTL and WIP transactions exist. Convert into the new Org and validate Items, BOMs, Routings and beginning item costs. Run Cost Rollups to get Make Items costed, and then run the Cost Update. Then convert on-hand inventory quantities. Issue material to Work Orders. Any open Purchase Orders and Sales Orders must be pointed to the new Org. An optional step at the end of the conversion process is to change the Org Code of the old Org, and then give the new Org the same Org Code as the old Org previously had. (This last step may be needed in order to accommodate certain custom reports, processes, etc., that were put in place for the old Org.) Another way to change Costing Methods is to change, via SQL script, the Org’s Cost Method Type and Cost Method ID. It should be noted that testing and validation of the impact of this Cost Method change is presently being performed by members of the Oracle Applications Users Group Cost Management SIG. Business benefits FIFO Costing is an enhancement to the EBS item costing functionality that allows for a greater degree of accuracy of COGS and inventory, and hence margin analysis and product profitability, by including in item cost the actual material, OP and Resource costs, as well as actual Material and Resource usage. Equally as important, it provides a high degree of automation for the Finance group by eliminating the need for ongoing Cost Rollups, Cost Updates and standards revaluation. Cost Rollups are available in a FIFO Org, to be used for various analyses. In addition, FIFO Costing of inventory is widely accepted as compliant with accounting rules (GAAP, IFRS). A decision to implement FIFO Costing should consider all of these positives, but must also consider the entity’s capability in supporting transaction integrity and PO pricing (though the company would need this discipline to support more areas of the business than just Costing). The Layer Cost Update is available for any needed corrections. The seeded reports and screen views, though not all-encompassing, are generally sufficient to support go-live in most companies. Changing of

COLLABORATE 14 Copyright ©2014 David E. Sweas, CPA 13

Costing Method in an EBS Inventory Org is not presently supported by Oracle, though groups outside of Oracle are in the process of testing procedures to effect that change. For any entity considering implementing FIFO Costing, certain paradigms and traditional ways of thinking regarding item costing would need to be worked through. Also, counsel of outside auditors should be sought, and an internal educational and requirements Costing Method workshop should be conducted. It all adds up to the fact that FIFO Costing has been EBS Manufacturing’s best-kept secret.