FARSTAD SHIPPING ASA - Solstad Farstad · Underwriter, Regional Manager Vesta Forsikring AS, Marine...

49

FARSTAD SHIPPING ASA ANNUAL REPORT 1999

Transcript of FARSTAD SHIPPING ASA - Solstad Farstad · Underwriter, Regional Manager Vesta Forsikring AS, Marine...

FA R S TA D S H I P P I N G A S A

A N N U A L R E P O RT 1 9 9 9

2

Farstad Shipping ASA

IThe Board of Directors 4

Report of the Board of Directors 5

Profit and loss account 10

Balance sheet 11

Cash flow statement 12

Notes to the financial statement 13

Auditor’s report 20

II1999 Positive - Negative 22

Organisation and administration 24

Main financial figures 26

Analytical information 28

Shareholder matters 30

Strategy 31

The Market for offshore supply vessels

Fleet structure 32

Brazil 34

Far East / Australia 36

North Sea 38

Other markets 41

Health, Safety and Environment 42

Training - recruitment 45

Fleet gallery 46

The Farstad fleet - employment 47

Glossary 49

Finance calendar

Result for 1. quarter 10. May Annual General Meeting 10. MayPayment to shareholders 29. May Result for 1. halfyear 22. Aug.Result for 3. quarter 31. Oct.

(subject to change)

Farstad Shipping’s strategy is to be along-term, important internationaloperator of large, modern offshoreservice vessels. Farstad Shipping ASAhas concentrated its business in that partof the market which demands the largestand most advanced share of tonnage, i.e.anchor handling tug supply (AHTS)vessels with horse power greater than10,000 BHP and platform supply vessels(PSV’s) with a cargo capacity greaterthan 2,000 DWT.

In 1973, Farstad Shipping ASA began itsoffshore activity as one of the pioneers inthe North Sea. At that time the companyacquired its first supply vessel, a modelUT 704 AHTS vessel, which was,incidentally, the Ulstein Group’s firstdesign. The company has, up to today,contracted a total of 28 vessels. Inaddition, the purchase and sale oftonnage at favourable times has beendecisive in the building up of today’sbusiness.The company has been listed on thestock exchange since 1988. In 1993, thecompany became a fully integratedshipping company when all of theoperator functions were incorporatedinto the company. Farstad Shipping hasconsolidated its international effortthrough collaboration with P&O,Australia (IOS), and the Brazilianoffshore company, Petroserv. (BrazilianOffshore Services).

The company’s fleet consists of 35 ships,whereof 16 are PSV’s and 18 AHTSvessels and one vessel for laying offlexible pipelines. Of these 2 PSV’s and 7AHTS vessels are jointly owned, via apartnership company, with P&O,Australia (Farstad’s owns a 50% share),whilst 1 AHTS vessel is chartered to thiscompany on a bareboat charter.The company’s business is run fromAalesund, Aberdeen and Macaé (Brazil)with 50 employees in all. Vessels in theFar East and Australia are run by P&OMaritime Services in Melbourne. Thenumber of sailors was by the yearendapproximately 750.The company’s vessels are run in linewith our customers’ expectations of highquality. They are operated at a level thatexceeds the requirements of national andinternational regulations with respect tosafety and the conservation of theenvironment. The vessels undergoplanned maintenance programmes thatare set up according to recommendationsfrom equipment suppliers’, classificationcompanies and the authorities, as well asthe company’s own experience. Thecompany will maintain a long-termchartering profile.The number of shareholders isapproximately 2,500. The company’sshare price at the end of the year wasNOK 25.50. This gives the company amarket capitalisation of approximatelyNOK 1,156 million.

T H I S I S F A R S T A D S H I P P I N G A S A

3

Financial development Farstad Shipping

The Farstad Fleet10 AHTS>10000 BHP

12 PSV>2000 DWT

2 PSV<2000 DWT

1 Pipelayer flexible

pipes

IOS-Fleet

8 AHTS> 10000 BHP

2 PSV>2000 DWT

*) Cash flow (CF) is defined as the result before tax and sales of vessels + depreciation + change concerning the revaluation of foreign currency liabilities

AHTS

PSV

1992 1993 1994 1995 1996 1997 1998 1999

1000

800

600

400

200

0

100

80

60

40

20

0

(mill. NOK)

Freight income Cash flow*) CF-margin

%

Farstad Shipping ASA

4

T H E B O A R D O F D I R E C T O R S

Sigmund Borgundvåg (61), Member of the Board

Engineer/marine architect.

Design manager in the Ulstein Ship

Technology AS since 1972.

Designer of the UT 700 series

offshore service vessels.

Managing Director in Brødrene Dyrøy AS.

Managment experience from aviation,

shipbuilding and manufacturing of

equipment for fishing industry. Various

Board appointments.

Per Erik Dalen (46),Member of the Board

High Court lawyer.

Law degree from Oslo, 1972.

Experience from banking etc.

Established his own law firm in 1977.

Holds a number of Board appointments

in industry and shipping.

Per Norvald Sperre (53), Deputy Chairman

of the Board

Engineering degree,

University of Newcastle upon Tyne.

Associate Director in AS Toluma, Oslo. Various

shipping experience from 1973, with the last 15 years

mainly being in offshore. Previously responsible for

marketing in Wilhelmsen Offshore Services (service

vessels) and Wilh. Wilhelmsens rig division.

Bjørn Havnes (53), Member of the Board

Bjarne Sælensminde (53), Member of the Board

Business degree NHH, Bergen.

Underwriter, Regional Manager Vesta

Forsikring AS, Marine & Energy Division.

Varied finance- and shipping background.

Previously Director of A/S Investa’s

shipping and offshore section.

Business degree - Heriot Watt

University, Edinburgh, Scotland.

Chairman of the Board of Tyrholm &

Farstad AS. Various Board

appointments and other positions in

banking, insurance and the

Shipowners Association.

Sverre A. Farstad (47), Chairman of the Board

Development 1999Following two very good years, 1999 wasa weaker year for the supply vesselcompanies. Reduced demand for supplyvessels combined with the effect of thelast few years’ large number of new buildorders, led to a large drop in rates. Inaddition, several companies experiencedhaving long-term contracts cancelled.The result of this negative marketdevelopment was that a large number ofvessels were laid up. Farstad Shippingalso chose to lay up a vessel.Developments in the market after thethird quarter provide hope that themarket is in the process of turning.Farstad Shipping particularly noticed thiswhen it came to the activity in the FarEast/Australia.Farstad Shipping ASA presents a resultthat, to a certain degree, bears the markof these market conditions. In addition,the result is negatively influenced by anunrealised currency exchange lossconnected with the company’s mortgageliabilities. Approximately 75% of thecompany’s earnings are in foreigncurrencies, therefore the generalexchange rate upturns for USD, GBPand AUD are positive for the company’sactivities.The operation of the vessels in 1999 hasbeen satisfactory and without majorincidents. The fleet was expanded by 4new vessels, which were all delivered bythe shipyards on time and within budget.

Result and dividendFarstad Shipping achieved an operatingincome of NOK 801.5 million in 1999(NOK 768.7 in 1998). No vessel saleshave been carried out during 1999,whilst the operating income for 1998includes a sales profit of NOK 60.2million. The increase in freight earningsmust be seen in the context of anincrease in the number of vessels in thefleet.The recorded result before tax was NOK86.0 million. The equivalent result for1998 was NOK 258.7 million. Thegroup’s cash flow *) during the periodwas NOK 292.8 million versus NOK309.3 million for the same period in1998. The cash flow per share was NOK6.46 (NOK 6.82).Operating costs for the period were NOK426.5 million (NOK 347.6 million). Themain reason for the increased costs wasthe increase in the number of ships. Theoperating result before depreciation and

finance in 1999, excluding sales profits,was NOK 374.9 million (NOK 359.1million). Ordinary depreciation comes toNOK 159.6 million (NOK 118.9 million).Net finance costs come to NOK 129.3million (NOK 43.3 million). Thisincludes an unrealised disagio of NOK47.3 million (disagio of NOK 6.3million), a consequence of the exchangerate adjustment of the company’s foreigncurrency mortgage liabilities. The foreigncurrency liabilities are serviced byincome from long-term charter contractsin foreign currency. The board will propose to the share-holders’ meeting that the parent com-pany’s surplus of NOK 16,203,426 beused in the following manner:

Transferred from other shareholders’ equity 29,125,944.00Dividend per share NOK 1.00 45,329,370.00

*) Cash flow is defined as the result before taxand sales of vessels + depreciation + changeconcerning the revaluation of foreign currencyliabilities

1993 1994 1995 1996 1997 1998 19990

2

4

6

8

10(NOK)

Excl. gain on sales Incl. gain on sales

REPORT OF THE BOARD OF

DIRECTORS

Cash flow per share (before tax)

5

0

50

100

150

200

250

1.quarter

2.quarter

3.quarter

4.quarter

(mill. NOK)

Operating incomeexcl. profit on sale offixed assets

Cash flowexcl. tax and profit onsale of fixed assets

0

10

20

30

40

50

Norwegian British Brazil Far East/Australia

Total

%

1998 1999

Operating result (EBIT) in % of freight income sorted by region

Financing and capital structureMortgage liabilities were repaid by NOK127.5 million (NOK 155.7 in 1998)during the period. Interest bearingmortgage liabilities were, as per31.12.99, NOK 1,693.1 million (NOK1,045.4 million). Of the company’smortgage liabilities at the end of lastyear: 38.4% was in USD, 18.8% in GBP,2.1% in AUD and 40.7% in NOK.Interest bearing current assets at thechange of the year came to NOK 199.6million (NOK 141.2 million).The group’s recorded shareholders’equity was, as per 31.12.99, NOK1,223.7 million (NOK 1,188.5 million),equivalent to NOK 27.00 (NOK 26.22)per share. At the end of last year, thecompany obtained estimates for themarket values of the vessels (charterparty free) from three shipbrokers. The

average of these valuation estimatesgives a value adjusted shareholders’equity of NOK 44.05 (NOK 48.72) pershare. There has been a fall in the valueof the fleet of approx. 12% during 1999.AdministrationWith the exception of the vessels inAsia/the Pacific Ocean region, thecompany’s vessels are operated from theoffice in Aalesund, by a staff of 30, andAberdeen, by a staff of 11. In total thereare 521 sailors attached to these offices.The operation of the vessels in Brazil isco-ordinated via our newly established,joint venture company in Macaè,Brazilian Offshore Services (BOS). Thiscompany has 7 members of staff and 76sailors serving on our vessels in Brazil.In Asia/the Pacific Ocean region, theoperation of the vessels is handled by

P&O Maritime Services, Melbourne.Approximately 154 sailors are serving onour vessels in this region.Shareholder mattersDuring the year, the share price hasclimbed from NOK 21.00 to NOK 25.50at the end of 1999. This gives thecompany a market capitalisation ofapprox. NOK 1,156 million (NOK 951million). A dividend of NOK 1 was paidout in 1999. An equivalent amount issuggested as dividend in 2000. The company’s board has the power ofattorney to expand the share capital byissuing up to 6 million shares, withoutthe right of first refusal for presentshareholders. This authority is validuntil the shareholder’s meeting in 2000.In addition, the board has the power ofattorney to purchase up to 10% of ourown shares. This power of attorney isvalid until 30.06.2000. None of theboard’s power of attorneys have beenused in 1999.The FleetThe Farstad fleet now consists of 25vessels. In addition, 9 vessels are ownedthrough IOS, the partnership companywith P&O, Australia (Farstad’s share50%), as well as one vessel that ischartered to IOS on a bareboat charter.Kværner Govan, Glasgow, delivered theplatform vessels (PSV’s) Far Strider andFar Supplier on 12th January and 12thMarch respectively. Immediatelyfollowing delivery, both vessels started5-year charters with Amerada Hess andASCo UK respectively. In August, FarSupplier was terminated from itscontract with ASCo. The vessel entereda 2-year contract with ASCo Norwaytogether with Far Spirit to serviceBP/Amoco locations in the Norwegiansector.The contract that Far Scotsman had wasterminated in July. The vessel was laidup due to expectations about the fallingmarket, and remain laid up for the restof the year.The anchor handling vessel (AHTS) FarSovereign was delivered by LangstenSlip og Båtbyggeri AS on 25th June. Acollaboration agreement with EMC(European Marine Contractors) wassigned for this vessel. However, becauseof the market conditions the partiesagreed in September to allow the vesselto go to Brazil to start the contract that

6

Farstad Shipping ASA

From the naming ceremony of Far Star in the Geirangerfjord

with Lady Sponsor Birte Mikkelsen, flanked by representatives from yard and ship-owner.

had been signed for Far Santana(AHTS). This vessel was delivered byUlstein Verft AS on 25th February 2000and went directly to Brazil to start its7.5-year contract with Petrobras. UponFar Santana’s arrival Far Sovereignreturned to work in the North Sea.Far Star (PSV) was delivered fromBrattvaag Skipsverft AS on 19th August.The vessel then entered a 10-yearcontract with Norsk Hydro.Far Sky and Far Senior (AHTS’) left theNorth Sea in the middle of November tostart 6 months work for BP/Amoco offthe coast of Trinidad.Up to 5 of our vessels were withoutemployment for periods during thesecond and third quarter in the FarEast/Australia. In the North Sea it wasduring the third quarter in particularthat we noticed the poor market. With 3AHTS vessels on the spot market,reduced rates on three contracts and onevessel laid up, the resulting effects wereconsiderable, but not unexpected.Health, Safety and EnvironmentFarstad Shipping has maintained overthe last few years’ strong commitment tomaking people aware of health, safetyand environmental issues (HSE)onboard the vessels and in the onshoreoperational organisations. Our require-ments for vessel operation are on a levelthat exceeds the requirements innational and international regulationswith respect to safety and conservationof the environment. Furthermore, thismandatory has given our customers’expectations of high quality. The boardbelieves that the significant effort beingmade on HSE will strengthen thecompany’s competitive edge.The project that was set in motionconcerning the inspection of equipmentand systems, the millennium change-over, uncovered only a few minorproblem areas. The changeover to theyear 2000 went without problems of anykind.There has also been significant trainingactivity for staff, focusing on HSEimprovements, during 1999. Activitiesinclude the reporting of unwantedevents (including potential accidents), athorough investigation of the

circumstances, and a discussion ofexperiences that involves causes, costsand effective steps to take to preventsuch events from recurring. This is aneffective tool, and one that gives theCompany an opportunity to limit losses and improve operational safety. Inaddition, it encourages the crew toreport hazards, which in turn can helphighlight the hazards. Because thereporting now is performed in a moreobjective manner, the "individual at

fault" risk is eliminated, and the sailingcrew has a better incentive to reportpossible hazards to people, equipmentand machinery.The operation of the company during1999 has not caused serious personalinjuries, substantial equipment damageor significant pollution of the environ-ment. The board acknowlegdes that thework environment onboard and onshoreis good.In 1999, the company had an absencedue to sickness rate of 1.4% and aninjury at sea rate of 0.3%.Market conditionsThe North SeaThe Norwegian and British sectors arestill the most important markets forFarstad Shipping. About 59% of thecompany’s freight earnings in 1999 camefrom these markets. The North Sea’sshare of freight earnings has been fallingfor the last few years.The market balance for supply vessels inthe North Sea has, during 1999,experienced a decline for the first time insix years. During the first half of theyear, the demand for supply vessels wason a par with the first six months of1998. However, the average utilisationrate fell due to increased availability oftonnage. During the third quarter, theNorth Sea market was further affectedby the increasing tonnage surplus, whilst

the fourth quarter experienced asignificant drop in demand. Thisproduced a further reduction in theutilisation rate. The drop in the fourthquarter was, however, limited as a resultof the net departure of tonnage from the North Sea. While the average utilisationrate for the first half of the year wasapprox. 89% (95% in the first half of1998) it fell to approx. 85% (97%)during the third quarter and 82% (93%)in the fourth quarter.

The fact that the drop in demand hasnot been greater in the North Sea is dueto the stable demand that is associatedwith the operation and maintenance ofexisting installations. Exploration relatedactivity, which is very dependent on theoil price, makes up a steadily smallershare of the accumulated demand forsupply vessels in the North Sea, and in1999 came to just 5%.The good market conditions of the lastfew years have contributed to asignificant number of new build orders.Market developments in 1999 havecontributed to an almost full stop in thenew build order activity.

REPORT OF THE BOARD OF

DIRECTORS

7

60

80

70

100

90

%

1998 1999 E-2000

Average utilisation rateNorth Sea

J F M A M J J A S O N D

From the naming cermony of Far Supplier in Glasgow with Lady Sponsor Ruth Maxwell

8

BrazilDespite big problems in the Brazilianeconomy in the beginning of 1999,activity in this region has been stable.Brazil still has ambitions of being one ofthe pioneering countries when it comesto oil activity in deep waters. Theopening of Brazilian fields to foreign oilcompanies will underpin this further.Following Far Sovereign going toPetrobras on contract at the end ofSeptember, Farstad has 7 vessels thatoperate in this region. In 1999, approx.28% of Farstad’s freight earnings camefrom vessels that work in Brazil. FarCenturion, Far Crusader, Far Sailor, FarSea – all AHTS vessels – have, togetherwith Far Sleipner (PSV), been on

contract to Petrobras the whole year.Lochnagar, which has been on contractto DSND (Søndenfjeldske) has alsoworked for Petrobras, laying flexible oilpipelines.Farstad wishes to consolidate and deve-lop our position further in the Brazilianmarket through the establishment ofBOS.Australia and Southeast AsiaApproximately 15% of Farstad’s incomein 1999 came from freight earnings fromthis region. At the end of 1999, twoPSV’s and six AHTS vessels wereworking in this region.The drop in the oil price affected theactivity in this region as early as the lastsix months of 1998. Activity has beenlow throughout the whole of 1999. Afterthe bottom was reached in the thirdquarter, activity gradually began to riseduring the fourth quarter.

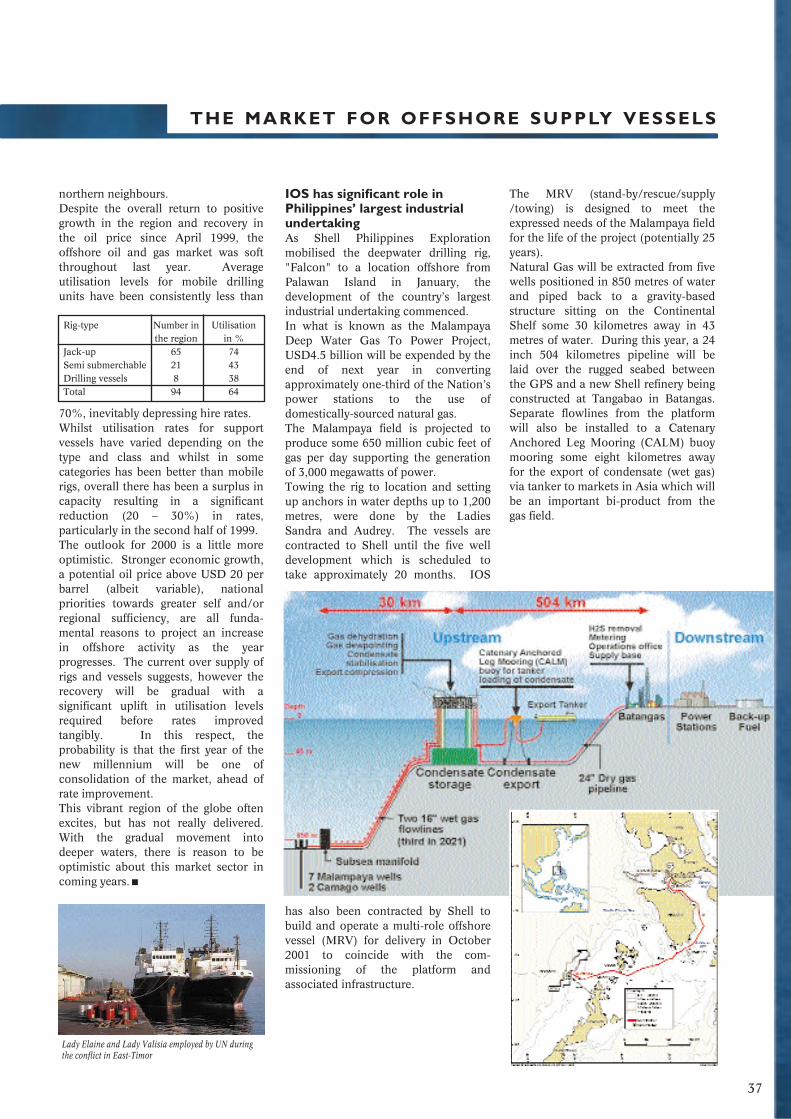

The partnership with P&O gives usposition to meet the increased activity inthe region. One example is the award ofcharter conracts from Shell to IOS inconnection with the development of theMalampaya field off the coast of thePhilippines.West Africa and Latin AmericaA co-operation agreement was signedwith Tidewater in September concerningmarket collaboration in West Africa andLatin America (except Brazil) for ourAHTS vessels. So far the collaborationhas resulted in contracts for Far Seniorand Far Sky in Trinidad & Tobago.Shipping taxationIn 1996, the Norwegian Parliament,‘Stortinget’, passed a new tax law forNorwegian Shipping Companies. Thenew taxation system gave Norwegianshipping companies satisfactory generalconditions; compared with generalconditions in countries that Norwegianshipping competes with.Unfortunately, in every budget dis-cussion since the arrangement wasintroduced, Parliament has managed tosow doubt about the stability of theindustry’s general terms by repeatedreductions in the arrangement. It is ofgreat importance that capital intenseindustries’, such as shipping havegeneral conditions that are predictableand stable. The fact that more and morenew countries have introduced generalconditions for shipping that are morecompetitive than the Norwegian onesdoes not make things better. Should thissituation continue, we must expect thatthe positive development thatNorwegian shipping has experiencedduring the last few years, will do anabout turn.

Farstad Shipping ASA

Aalesund, 13 March 2000 The Board of Farstad Shipping ASA

Per Erik Dalen

Sverre A. FarstadChairman

Terje J.K.AndersenManaging Director

Per Norvald SperreDeputy Chairman

Bjarne Sælensminde

Sigmund Borgundvåg

Bjørn Havnes

Future outlookThere is a clear correlation between theoil companies’ earnings and thecompanies’ exploration and investmentactivities. Reduced earnings, resultingfrom low oil prices, led to substantialcuts in the oil companies’ explorationactivities in 1999. This resulted in asignificant number of rigs being laid up.In addition, large cost reductioncampaigns were set in motion in the oilcompanies. Many of these weremotivated by a need to document gainsfrom collaborations and mergers.Given the background of thedevelopment of the oil price during 1999and into 2000, we have seen more andmore signs that exploration activity isundergoing an increase again. While atthe beginning of 2000 there are, on aglobal basis, 96 semis working, this isexpected to increase to about 110 nearthe end of summer. The North Sea, WestAfrica, the East/Australia and Brazil areexpected to be responsible for the

increase. Similarly, the number ofjackups is expected to increase from 265to 300. In this case, it is the Gulf ofMexico in particular that is expected tocontribute to the growth. The abovementioned development means that thedemand for supply vessels in Brazil, theFar East, Australia and West Africa mustbe expected to increase in the monthsahead.The market balance in 1999 was stronglyaffected by the many new builds thatcame out. While it is not expected thatthe demand in 2000 will be big enoughto absorb the surplus tonnage, themarkets outside of the North Sea,however, have in the last few monthstaken tonnage away from the North Seato a greater degree than was expected.When the utilisation rate in the NorthSea approaches 90%, it is usuallyreflected by a rise in rates. At the end ofthe first quarter we have experiencedutilisation rates at this level and anequivalent strong rise in rates. With

expectations of a continued net declinein the tonnage in the North Sea we areentitled to hope that the market mayrecover faster than what was expectedjust a few months ago.The Farstad fleet at the start of 2000 wascontractually covered, through signedcharter agreements, calculated atapprox. 90% during the first half of theyear and approx. 75% for the secondhalf.The going concern statementThe financial statements are presentedbased on the assumption of goingconcern. The Board of Directors confirmthat the assumption is present based onthe company’s solid equity capital andchartering position of the vessels.

9

REPORT OF THE BOARD OF

DIRECTORS

Farstad Shipping ASA

PARENT COMPANY FARSTAD SHIPPING ASA (NOK 1000) GROUP

Operating income:Freight incomeOther incomeProfit on sale of fixed assets

Total operating income

Operating expenses:Crewing expenses vesselsOther operating expenses vesselsAdministration

Total operating expenses

Operating profit before depreciation

Depreciation

Operating result

Financial items:Financial incomeFinancial expenses

Net financial items

Pre-tax profit

Taxes

Profit of the year

Profit per. share (NOK)

1999

-35,576

38

35,614

--

(38,293)

(38,293)

(2,679)

(2,355)

(5,034)

22,659(1,422)

21,237

16,203

-

16,203

0.36

1999

795,8445,492

154

801,490

(231,946)(148,423)

(46,117)

(426,486)

375,004

(159,638)

215,366

28,958(158,294)

(129,336)

86,030

(5,576)

80,454

1.77

1998

703,0523,648

62,005

768,705

(184,671)(122,528)

(40,430)

(347,629)

421,076

(118,893)

302,183

32,747(76,181)

(43,434)

258,749

(1,844)

256,905

5.67

1997

597,376907

75,117

673,400

(142,920)(99,644)(32,389)

(274,953)

398,447

(124,470)

273,977

22,076(55,634)

(33,558)

240,419

102,361

342,780

5.30

1998

-28,250

315,910

344,160

-4

(34,974)

(34,970)

309,190

(1,989)

307,201

16,878(405)

16,473

323,674

-

323,674

7.14

NOTE

17

14

20

7

17

22

11

4

12

18

5

125

10

P R O F I T A N D L O S S

A C C O U N T

Terje J.K.AndersenManaging director

Farstad Shipping ASA

1999

4,7272,583,487

39,04960,202

675

650

2,688,790

154,57751,50531,367

155,463

392,912

3,081,702

1998

6,3031,830,998

42,591206,430

675

650

2,087,647

119,18928,81721,257

112,175

281,438

2,369,085

1997

7,8791,549,407

36,589114,610

275

425

1,709,185

58,14933,56111,171

156,414

259,295

1,968,480

FARSTAD SHIPPING ASA (NOK 1000) GROUP

ASSETSFixed assets:GoodwillVessels etc.Deferred maintenance costContracts newbuildingsOther long-term receivablesReceivables from Group companiesShares

Total fixed assets

Current assets:Account receivables, freight incomeOther short-term receivables Other securitiesBank deposits

Total current assets

Total assets

PARENT COMPANY

NOTE

77

10

66

3 6

16

7

1999

45,329198,396980,023

1,223,748

1261,693,066

1,693,192

38,10245,32981,331

164,762

1,857,954

3,081,702

1998

45,329198,396944,832

1,188,557

2,0681,045,402

1,047,470

37,37445,32950,355

133,058

1,180,528

2,369,085

1997

45,329211,509720,036

976,874

1,411875,937

877,348

25,34745,32943,582

114,258

991,606

1,968,480

1998

6,3031,710

--

1,425207,156

1,473,586

1,690,180

39,0039,326

21,25762,516

132,102

1,822,282

1999

4,7272,195

--

675164,039

1,473,686

1,645,322

5,92229,10231,36771,239

137,630

1,782,952

1998

45,329198,396

1,459,583

1,703,308

2,068-

2,068

8,15445,32963,423

116,906

118,974

1,822,282

1999

45,329198,396

1,430,457

1,674,182

126-

126

27,43345,32935,882

108,644

108,770

1,782,952

EQUITY AND LIABILITIESEquity capital:Share capitalShare premium reserveOther equity

Total equity capital

Liabilities:Long-term liabilities:Other long-term liabilitiesInterest-bearing mortgage debt

Total long-term liabilities

Short-term liabilities:Debt to suppliersAllocated dividendsOther short-term liabilities

Total short-term liabilities

Total liabilities

Total equity and liabilities

NOTE

1999

1216

8

9

13

11

B A L A N C E

S H E E T

Per Erik Dalen

Sverre A. FarstadChairman

Per Norvald SperreDeputy Chairman

Bjarne Sælensminde

Sigmund Borgundvåg

Bjørn Havnes

Aalesund, 13. March 2000 The Board of Farstad Shipping ASA

Farstad Shipping ASA

1999

16,203-

(38)2,355

-33,08119,279

(1,942)-

(47,378)

21,560

186(1,415)

(36)43,867

-

42,602

---

(45,329)-

(45,329)

18,833

83,773

102,606

1999

86,030(5,204)

(154)159,638

8,252(35,388)

728

(1,942)47,257

7,120

266,337

400(764,906)

(36)--

(764,542)

724,438(127,506)

-(45,329)

-

551,603

53,398

133,432

186,830

1998

258,749(348)

(62,005)118,893

24,069(61,040)12,027

657(6,296)9,330

294,036

120,139(578,136)

(225)-

(400)

(458,622)

331,506(155,744)

-(45,329)

-

130,433

(34,153)

167,585

133,432

1998

323,674-

(315,910)1,989

-(11,012)(6,310)

657-

37,369

30,457

571,740(956)

(431,725)671,638

(400)

810,297

-(708,606)(131,128)(45,329)

-

(885,063)

(44,309)

128,082

83,773

1997

240,419(109)

(75,117)124,470

16,796(5,409)2,201

4043,394

(14,226)

292,823

127,415(578,886)

--

(500)

(451,971)

326,446(163,230)

--

(33,997)

129,219

(29,929)

197,514

167,585

CASH FLOW FROMOPERATING ACTIVITY:Pre-tax profitPaid taxes this periodProfit on sale of fixed assetsOrdinary depreciationsPeriodical maintenance costsChanges in debtorsChanges in creditorsDiscrepancies pension costs/paymentsfrom pension fundsUnrealised foreign exchange loss/(gain)Changes in prepayments and accruals

Net cash flow from operation activity

CASH FLOW FROMINVESTMENT ACTIVITY:Sale of fixed assets (sales price)Investments in fixed assets/ contracts newbuildingsPurchase of sharesChanges in long-term receivablesOther investments

Net cash flow from investment activity

CASH FLOW FROMFINANCE ACTIVITY:New long-term debtRepayment of debtResult 1997, transferred to subsidiariesDividendsRepayment of equity capital

Net cash flow from finance activity

Changes in liquidity over the year

Liquid assets at 01.01

Liquid assets at 31.12

FARSTAD SHIPPING ASA (NOK 1000 ) GROUP PARENT COMPANY

A

B

C

A + B + C

C A S H F L O W S TAT E M E N T

12

Accounting principles – new accounting actThe financial statement is presented in compliancewith the Norwegian Companies Act, the NorwegianAccounting Act of 1998 and Norwegian generallyaccepted accounting principles.The company has, according to the new accountingact, changed its principles for calculation of foreigncurrency mortgage debt. The debt is now calculatedto NOK using the exchange rate at the end of theyear. Previously, the mortgage debt in NOK wascalculated using the highest of the exchange rate atthe drawdown date and the exchange rate by year-end. As a result of the change, a latent currencyprofit of NOK 16,441 was added to income in 1998,and it also resulted in a corresponding increase incompany equity by the end of 1998.The former legal reserve is now transferred to sharepremium reserve. The former general reserve istransferred to other equity. The profit and lossaccount and balance sheet is restructured incompliance with the new Accounting Act of 1998.Figures for previous years are changed according tothe above mentioned change of principles.Principles of consolidationThe consolidated financial statements include theparent company Farstad Shipping ASA and thesubsidiaries specified in note 6. In the consolidatedstatements, all inter-company balances andtransactions are eliminated. The cost of acquiringshares in subsidiaries is eliminated against equity inthe subsidiary at the time of acquisition or at the timeof establishment. The cost method is used for thiselimination. The profit and loss statement (P&L) for a foreignsubsidiary is calculated to NOK at the averageexchange rate for the year. The balance sheet iscalculated to NOK according to the exchange rate atthe end of the year. Equity in foreign currency isadjusted to the exchange rate by year-end. This isposted directly to the equity.Costs- and revenue recognitionFreight income is posted when it is earned. Incomeand costs related to the operation of the vessels areentered according to the accruals principle based onthe number of days the contract lasts before and afterthe end of the accounting period.Valuation and presentation of current assetsShort-term shareholdings and other securities are nottreated as a portfolio, and are valued to the lowest ofcost price and market value. The value of tradereceivables and other short-term receivables are facevalue reduced by expected future losses.Ownership of the general partnership (ANS)Farstads share of this general company, see note 4,are entered using the principle of proportionalconsolidation (gross method). Accordingly, FarstadShipping’s share of the parent company’s assets,debts and margins are included in Farstad Shipping’sfinancial statements, respectively. Balance sheetitems, costs and income between the general

company and Farstad Shipping are eliminatedproportionally to the extent of Farstad Shippingsshare of ownership in this company.Sale of vesselsProfit from sale of vessels is included in operatingincome, due to the perception that these transactionsare part of the regular business operations.Depreciation of vesselsVessels and portion of vessels in ANS are valued inthe consolidated balance sheet at cost, lessaccumulated depreciation. The cost of the vessels orthe portion of the vessels in ANS follows a straight-line depreciation schedule over 25 years. Thisprinciple was changed in 1998. Prior years’depreciation expense of the fleet was based on auseful life of 20 years from the time ofpossession/acquisition. The effect of this change wasa reduction in depreciation expense of NOK 30million compared to the previous depreciationschedule. Smaller investments, alterations andinvestments necessitated by new charter contractsare normally depreciated in a straight line over 5years, unless there are conditions that dictate alonger or shorter useful life of that particularinvestment.GoodwillWith the acquisition of the management companiesSverre Farstad & Co AS and Farstad UK Ltd. in1993, the goodwill value of NOK 15.8 million hasbeen added to the balance sheet. This will bedepreciated by 10% annually, in that the aquisition isanticipated to have value for the Company for atleast ten years. Construction ContractsPaid instalments for newbuildings are entered asfixed assets as each payment take place. Investmentsthat are not included in the contract, such asinspection costs, and other related costs and rebatesduring construction, will be recorded as fixed assets.For details, see note 10. Pension costs and obligationsThe Company is financing its pension obligations to223 employees through two group pension plans.The Company has separate arrangements with fiveindividuals, for whom the Company pays the annualpremiums. These premiums are recorded as pensioncosts as they incur.The net present value of the future obligations of thegroup pension plans is calculated based on insuranceaccounting principles. The estimated obligation forthe employees on shore is recorded as a debt on thebalance sheet. The current year’s change in netpension obligation then becomes a pension cost inthe financial statements. Estimates of the pensionobligation to the sailing crew currently indicate over-financing. This is not included on the balance sheet.For details, please see note 12.Maintenance costsPeriodic maintenance is capitalized, and posted tooperating costs during the period until the next

Farstad Shipping ASA

N O T E S ( N O K 1 0 0 0 )

NOTE

1NOTE

1Accounting principles

13

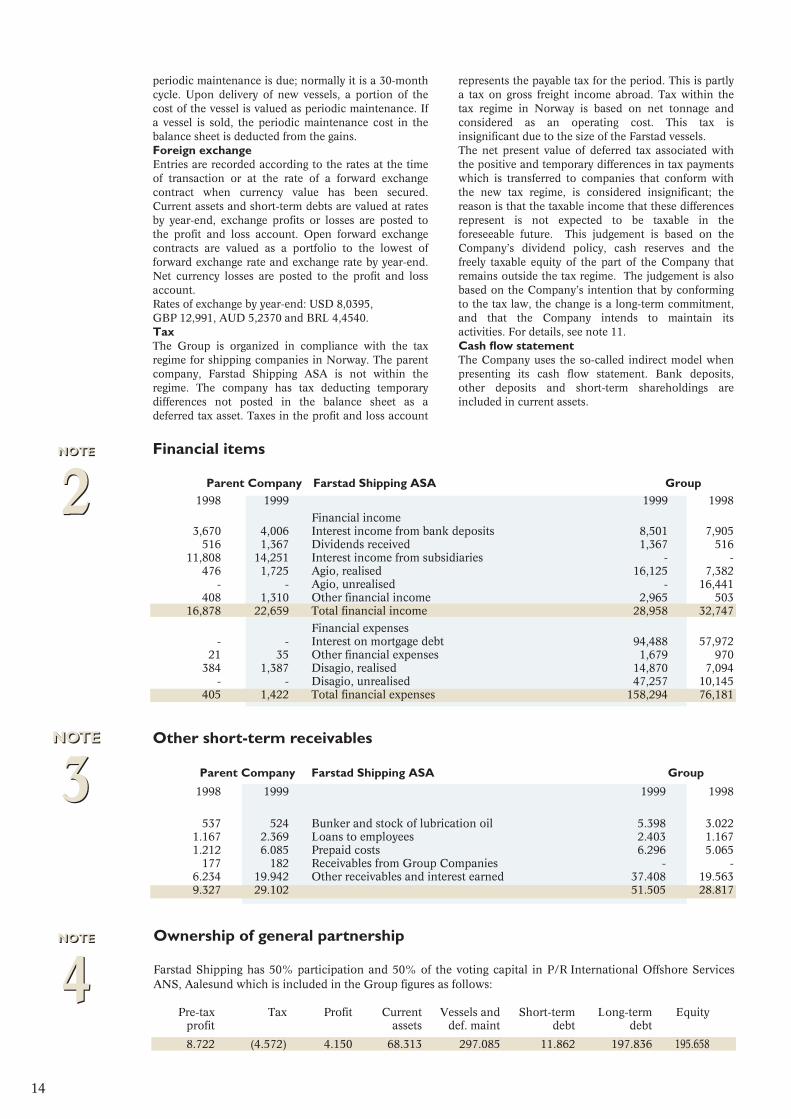

Financial items

Ownership of general partnership

NOTE

2NOTE

2

NOTE

4NOTE

4

Parent Company Farstad Shipping ASA Group1998 1999 1999 1998

Financial income 3,670 4,006 Interest income from bank deposits 8,501 7,905

516 1,367 Dividends received 1,367 51611,808 14,251 Interest income from subsidiaries - -

476 1,725 Agio, realised 16,125 7,382- - Agio, unrealised - 16,441

408 1,310 Other financial income 2,965 50316,878 22,659 Total financial income 28,958 32,747

Financial expenses - - Interest on mortgage debt 94,488 57,972

21 35 Other financial expenses 1,679 970384 1,387 Disagio, realised 14,870 7,094

- - Disagio, unrealised 47,257 10,145405 1,422 Total financial expenses 158,294 76,181

Farstad Shipping has 50% participation and 50% of the voting capital in P/R International Offshore ServicesANS, Aalesund which is included in the Group figures as follows:

Pre-tax Tax Profit Current Vessels and Short-term Long-term Equityprofit assets def. maint debt debt

8.722 (4.572) 4.150 68.313 297.085 11.862 197.836 195.658

periodic maintenance is due; normally it is a 30-monthcycle. Upon delivery of new vessels, a portion of thecost of the vessel is valued as periodic maintenance. Ifa vessel is sold, the periodic maintenance cost in thebalance sheet is deducted from the gains.Foreign exchangeEntries are recorded according to the rates at the timeof transaction or at the rate of a forward exchangecontract when currency value has been secured.Current assets and short-term debts are valued at ratesby year-end, exchange profits or losses are posted tothe profit and loss account. Open forward exchangecontracts are valued as a portfolio to the lowest offorward exchange rate and exchange rate by year-end.Net currency losses are posted to the profit and lossaccount.Rates of exchange by year-end: USD 8,0395, GBP 12,991, AUD 5,2370 and BRL 4,4540.TaxThe Group is organized in compliance with the taxregime for shipping companies in Norway. The parentcompany, Farstad Shipping ASA is not within theregime. The company has tax deducting temporarydifferences not posted in the balance sheet as adeferred tax asset. Taxes in the profit and loss account

represents the payable tax for the period. This is partlya tax on gross freight income abroad. Tax within thetax regime in Norway is based on net tonnage andconsidered as an operating cost. This tax isinsignificant due to the size of the Farstad vessels.The net present value of deferred tax associated withthe positive and temporary differences in tax paymentswhich is transferred to companies that conform withthe new tax regime, is considered insignificant; thereason is that the taxable income that these differencesrepresent is not expected to be taxable in theforeseeable future. This judgement is based on theCompany’s dividend policy, cash reserves and thefreely taxable equity of the part of the Company thatremains outside the tax regime. The judgement is alsobased on the Company’s intention that by conformingto the tax law, the change is a long-term commitment,and that the Company intends to maintain itsactivities. For details, see note 11.Cash flow statementThe Company uses the so-called indirect model whenpresenting its cash flow statement. Bank deposits,other deposits and short-term shareholdings areincluded in current assets.

Other short-term receivablesNOTE

3NOTE

3 Parent Company Farstad Shipping ASA Group

1998 1999 1999 1998

537 524 Bunker and stock of lubrication oil 5.398 3.0221.167 2.369 Loans to employees 2.403 1.1671.212 6.085 Prepaid costs 6.296 5.065

177 182 Receivables from Group Companies - -6.234 19.942 Other receivables and interest earned 37.408 19.5639.327 29.102 51.505 28.817

14

NOTE

6NOTE

6Shares in subsidiaries and other shares

Share Total no. Share Par BookCompanies capital of shares in % value value Shares:Sparebanken Møre 552.615 84.600 1,53 8.460 11.389Kredittbanken ASA 163.517 84.200 1,03 1.684 2.315Ulstein Mek. Verksted Holding ASA 15.832 12.600 0,02 3 36Solstad Offshore ASA 71.588 10.000 0,03 20 280Total shares included in other securities 14.020Shares in subsidiaries:Farstad Shipping Ltd., Aberdeen GBP 5.000 5000 100 65 1.691Farstad Supply AS, Aalesund 1.471.245 1.471.245 100 1.471.245 1.471.245Farstad Brasil AS, Aalesund 100 100 100 100 100Total shares in subsidiaries: 1.471.410 1.473.036Sundry shares 650 650Total shares under fixed assets 1.472.060 1.473.686Shares owned by Farstad Supply AS:Farstad International AS 50 50 100 50 50

Total receivables from subsidiaries are NOK 164.039, the parent company’s receivables from Farstad Supply isNOK 162.956. This is mainly caused by the sale of vessels to the new shipowning company within the tax regimefor Norwegian shipping companies. The receivables bear interest at market interest rates.

NOTE

7NOTE

7Vessels and other operating assets (GROUP)

Acquisition Addition Disposal Accumulated Book value Ordinary cost at 1.1. this year this year depreciation at 31.12 depreciation

Goodwill(10%) 15.809 0 0 11.082 4.727 1.576Contracts on vessels(0%) 206.430 752.894 899.122 0 60.202 0Cars (20-25%) 2.584 1.017 715 1.707 1.179 739Other fixed assets (2-25%) 8.868 3.527 80 4.011 8.304 932Directly owned vessels 2.150.189 905.198 0 774.425 2.280.962 123.332General parntership (ANS) 390.227 1.552 0 98.737 293.042 33.059Total vessels etc. 2.551.868 911.294 795 878.880 2.583.487 158.062Total operating assets 2.774.107 1.664.188 899.917 889.962 2.648.416 159.638

A contract for a newbuilding from Ulstein Verft implies that advance payments are included in that year’s addition under contracts. When completed, the value of the vessel is included in that year’s disposal under contracts and the cost price of the vessel is included. Below, the investment are only included as contracts in order not to make double entries.

Investments in and sale of fixed assets (sales price) during the past 5 years: (NOK mill.)

1999 1998 1997 1996 1995 Purchase Sale Purchase Sale Purchase Sale Purchase Sale Purchase Sale

Cars 1,0 0,4 1,3 0,4 0,9 0,5 1,4 1,4 0,3 0,2Goodwill - - - - - - - - - -Other fixed assets 3,5 - 1,0 - 1,8 - 1,3 0,1 0,3 0,1Directly owned vessels 6,1 - 144,0 118,5 54,1 127,7 33,5 - 8,9 64,4Interest in vessels in partnership 1,6 - 79,6 - 214,6 - - - 138,7 - Newbuildings 752,9 - 321,6 - 281,2 - 132,4 - 142,5 -

Total for the group 765,1 0,4 547,5 118,9 552,6 128,2 168,6 1,5 290,7 64,7

Average number of employees in the administration in Aalesund, Aberdeen and Macaè, was 44. Averagenumber of crewmembers onboard the vessels in 1999 was 726. 10 of the vessels in the company’s fleet areowned by IOS which is a 50% owned company. A corresponding share of the crew costs are incorporated.Crew costs for foreign crew is difficult to divide on above mentioned groups.

NOTE

5NOTE

5Payroll expenses, number of emplotees

Parent Company Farstad Shipping ASA Group

1998 1999 1999 1998 12.141 13.137 Wages 157.931 132.111

- - Crew cost IOS vessels 48.316 36.8352.228 3.222 Social security costs 17.151 14.0751.729 1.766 Pension costs 4.044 3.404

554 1.008 Other contributions 29.578 22.363

16.652 19.133 257.020 208.788

15

Tax situationNOTE

11NOTE

11 Parent Company Farstad Shipping ASA Group

1998 1999 1999 1998Calculation of taxable profit:

323,674 16,203 Operating income before taxes1,458 (1,238) Permanent discrepancies

(315,873) - Profit sale of vessels within the Group

Changes in temporary discrepancies related to:657 (1,942) Current assets / short-term liabilities

1,571 1,684 Fixed assets / long-term liabilities(11,487) (7,935) Reversed from correction income

- (6,772) Loss to be carried forward

0 0 Taxable profit

Calculation of deferred tax. Specification of discrepancies:(2,068) (126) Current assets / short-term liabilities (126) (2,068)6,457 4,773 Fixed assets 4,773 6,457

(1,587) (2,955) Unused dividend tax credit (2,955) (1,587)(13,659) (6,887) Loss carried forward (6,887) (13,659)(7,935) - Correction income - (7,935)

(18,792) (5,195) Calculation base for deferred taxes (5,195) (18,792)

5,262 1,455 Deferred tax 1,455 5,262

Specification of taxes in profit and loss account:- - Taxes payable abroad 5,576 1,844

0 0 Total tax costs 5,576 1,844

NOTE

9NOTE

9Development in the Company’ share capital and equity (parent company)

Date Farstad Shipping ASA Number of Share- Share pre- Othershares capital mium reserve equity

01.01.1999 45.329.370 45.329 198.396 1.459.58331.12.1999 Profit of the year 16.20331.12.1999 Allocated to divedends (45.329)

Total parent company 45.329.370 45.329 198.396 1.430.457

Other short-term liabilitiesNOTE

8NOTE

8 Parent Company Farstad Shipping ASA Group

1998 1999 1999 1998

18,004 20,314 Tax deductions, holiday pay, VAT, etc 20,444 18,015- - Estimated taxes payable 2,736 1,644

4,455 2,305 Accrued expenses 4,461 6,914- - Accrued interest on mortgage debt 27,617 16,966

40,786 7,180 Liabilities to Group companies - -178 6,083 Other short-term liabilities 26,073 6,816

63,423 35,882 81,331 50,355

NOTE

10NOTE

10Contract newbuilding

The Company has 1 vessel in order due to be delivered February 2000 from Ulstein Verft. Total investmentis approximately NOK 298.000, whereof NOK 60.202 is capitalized as fixed assets per 31.12.99 for paidinstalments to Ulstein Verft, inspection costs and owners suppliers. Longterm financing is expected to be 80% of the investment.

16

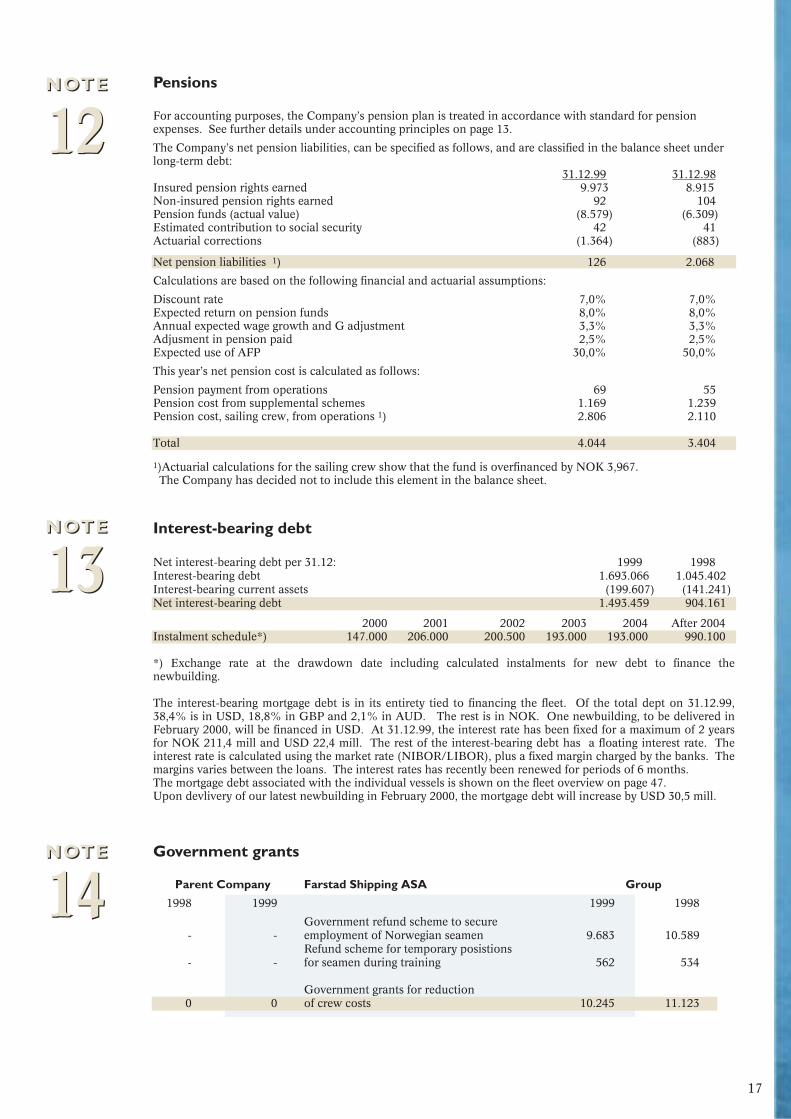

NOTE

12NOTE

12Pensions

For accounting purposes, the Company’s pension plan is treated in accordance with standard for pensionexpenses. See further details under accounting principles on page 13.

The Company’s net pension liabilities, can be specified as follows, and are classified in the balance sheet under long-term debt:

31.12.99 31.12.98Insured pension rights earned 9.973 8.915Non-insured pension rights earned 92 104Pension funds (actual value) (8.579) (6.309)Estimated contribution to social security 42 41Actuarial corrections (1.364) (883)

Net pension liabilities 1) 126 2.068

Calculations are based on the following financial and actuarial assumptions:

Discount rate 7,0% 7,0%Expected return on pension funds 8,0% 8,0%Annual expected wage growth and G adjustment 3,3% 3,3%Adjusment in pension paid 2,5% 2,5%Expected use of AFP 30,0% 50,0%

This year’s net pension cost is calculated as follows:

Pension payment from operations 69 55Pension cost from supplemental schemes 1.169 1.239Pension cost, sailing crew, from operations 1) 2.806 2.110

Total 4.044 3.404

1)Actuarial calculations for the sailing crew show that the fund is overfinanced by NOK 3,967. The Company has decided not to include this element in the balance sheet.

NOTE

13NOTE

13Interest-bearing debt

Net interest-bearing debt per 31.12: 1999 1998Interest-bearing debt 1.693.066 1.045.402Interest-bearing current assets (199.607) (141.241)Net interest-bearing debt 1.493.459 904.161

2000 2001 2002 2003 2004 After 2004Instalment schedule*) 147.000 206.000 200.500 193.000 193.000 990.100

*) Exchange rate at the drawdown date including calculated instalments for new debt to finance thenewbuilding.

The interest-bearing mortgage debt is in its entirety tied to financing the fleet. Of the total dept on 31.12.99,38,4% is in USD, 18,8% in GBP and 2,1% in AUD. The rest is in NOK. One newbuilding, to be delivered inFebruary 2000, will be financed in USD. At 31.12.99, the interest rate has been fixed for a maximum of 2 yearsfor NOK 211,4 mill and USD 22,4 mill. The rest of the interest-bearing debt has a floating interest rate. Theinterest rate is calculated using the market rate (NIBOR/LIBOR), plus a fixed margin charged by the banks. Themargins varies between the loans. The interest rates has recently been renewed for periods of 6 months.The mortgage debt associated with the individual vessels is shown on the fleet overview on page 47. Upon devlivery of our latest newbuilding in February 2000, the mortgage debt will increase by USD 30,5 mill.

NOTE

14NOTE

14Government grants

Parent Company Farstad Shipping ASA Group

1998 1999 1999 1998

Government refund scheme to secure - - employment of Norwegian seamen 9.683 10.589

Refund scheme for temporary posistions- - for seamen during training 562 534

Government grants for reduction0 0 of crew costs 10.245 11.123

17

NOTE

15NOTE

15Off-balance financial instruments

In order to secure the currency exchange rate of short-term receivables and freight income in foreign currency, at31.12.99 the Company has entered into the following agreements:

a) Forward agreements for an amount of GBP 20,8 million due from January 2000 to May 2003.Forward rates varies between NOK 12.00 and 13.42.

b) Forward agreements for an amount of USD 20.5 million due from January 2000 to March 2001.Forward rates varies between NOK 7.94 and 8.17

To secure the planned financing of a newbuilding in USD the Company has per 31.12.99 entered into forwardagreement to buy USD 30.5 million, due date 25.02.00,at an average forward rate of NOK 7,7664. For alteration ofmortgage-debt in NOK the Company has bought GBP 7.0 million through forward exchange contracts whichterminates 31.01.01 to an average exchange rate of NOK 12.5950.

Mortgages and guarantee liabilitiesNOTE

16NOTE

16 Farstad Shipping ASA Parent Company Group

Mortgages: Debt and accrued interest secured by mortgages 0 1.720.683

Security includes:Bank deposits - 23.979Account receivables - 150.138Vessels, at book value - 2.574.004

0 2.748.121

In addition the Company has assigned future freight income, and any insurance payment as security for debt. Taxesowed on behalf of employees, NOK 4.806, are commited resourced deposited into separate account, but areincluded in bank deposits.

Guarantee:Guarantee liabilities not included in the balance sheet 1.522.167 207.627

Mortgage debt has been transferred from Farstad Shipping to Farstad Supply as a part of the adaptation to the newtax regime for Shipping Companies. Farstad Shipping remains as guarantor for this debt, amounting to NOK1,521,772 at 31.12.99.

NOTE

17NOTE

17Result sorted by business segments

Freight Operating Operating Depreciation Operating Book value income costs profit I(EBDIT) profit II (EBIT) vessels*)

AHTS 398.745 213.308 185.437 78.106 107.331 1.384.075PSV incl. Lochnagar 397.099 213.178 183.921 78.285 105.636 1.228.978Total vessels 795.844 426.486 369.358 156.391 212.967 2.613.053Norwegian sector 207.231 113.629 93.602 39.657 53.945 789.576British sector 246.175 124.845 121.330 42.122 79.207 497.733Brazil 220.554 105.934 114.620 44.819 69.800 795.304Far East/Australia 117.670 77.917 39.754 28.798 10.956 244.077Other markets 4.214 4.160 54 994 (940) 286.363Total sector 795.844 426.486 369.358 156.391 212.967 2.613.053

For 1999 the investment has been NOK 317.974 in new ATHS vessels and NOK 442.637 in new PSV’s. Totalinvestment NOK 760.611. Operating profit (EBIT) for Farstad Shipping are NOK 215.366. The difference ofNOK 2.366 is divided between other revenues NOK 5.492, sales of fixed assets NOK 154 and other depreciationNOK 3.247.

In 1999, some of the vessels have had activity in more than one area. When allocating costs/ revenues for eachgeographical area, consideration has been made to actual revenues. However, the vessels’ operating costs areprorated. The depreciation is allocated using the same principle as other costs. The administration overheadcosts related to the entity as a whole are allocated equally between the vessels.

*) The book value breakdown per vessel by geographical location was determined using the end of 1999 as basis.Book value as of 31.12.99 was used, and includes the individual vessel’s accrued periodic maintenance costs asof that date.

18

NOTE

18NOTE

18Connected Companies

Tyrholm & Farstad AS, Aalesund, the Company’s largest shareholder (46%), is defined as a connected company.On 01.01.98 the Company signed a 5 year extension of an agreement with Tyrholm & Farstad AS with regard torent of office accommodation. Further agreements were made 01.01.99 for use of computers for 5 years andother office services for 3 years. All agreements are for the head office in Aalesund and represent an annual costof NOK. 3.483.

The Company has no receivables or liabilities to Tyrholm & Farstad AS at 31.12.99.

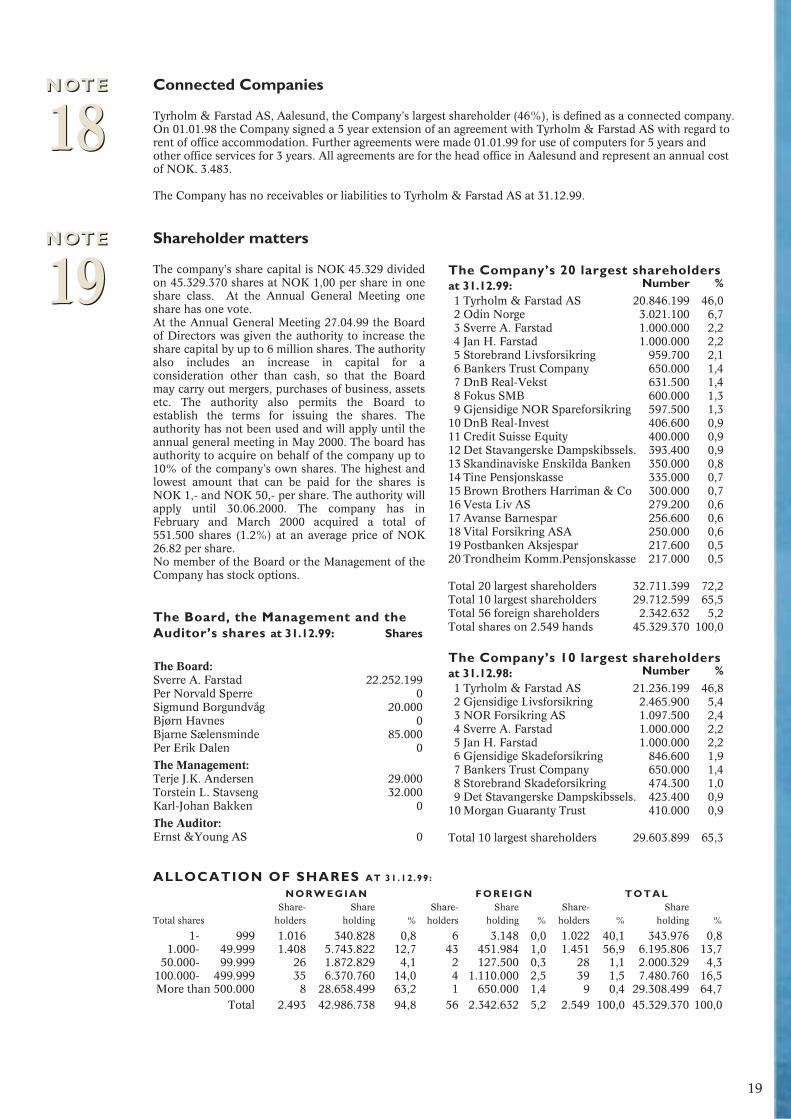

The Company’s 20 largest shareholdersat 31.12.99: Number %1 Tyrholm & Farstad AS 20.846.199 46,02 Odin Norge 3.021.100 6,73 Sverre A. Farstad 1.000.000 2,24 Jan H. Farstad 1.000.000 2,25 Storebrand Livsforsikring 959.700 2,16 Bankers Trust Company 650.000 1,47 DnB Real-Vekst 631.500 1,48 Fokus SMB 600.000 1,39 Gjensidige NOR Spareforsikring 597.500 1,3

10 DnB Real-Invest 406.600 0,911 Credit Suisse Equity 400.000 0,912 Det Stavangerske Dampskibssels. 393.400 0,913 Skandinaviske Enskilda Banken 350.000 0,814 Tine Pensjonskasse 335.000 0,715 Brown Brothers Harriman & Co 300.000 0,716 Vesta Liv AS 279.200 0,617 Avanse Barnespar 256.600 0,618 Vital Forsikring ASA 250.000 0,619 Postbanken Aksjespar 217.600 0,520 Trondheim Komm.Pensjonskasse 217.000 0,5

Total 20 largest shareholders 32.711.399 72,2Total 10 largest shareholders 29.712.599 65,5Total 56 foreign shareholders 2.342.632 5,2 Total shares on 2.549 hands 45.329.370 100,0

The Company’s 10 largest shareholdersat 31.12.98: Number %1 Tyrholm & Farstad AS 21.236.199 46,82 Gjensidige Livsforsikring 2.465.900 5,43 NOR Forsikring AS 1.097.500 2,44 Sverre A. Farstad 1.000.000 2,25 Jan H. Farstad 1.000.000 2,26 Gjensidige Skadeforsikring 846.600 1,97 Bankers Trust Company 650.000 1,48 Storebrand Skadeforsikring 474.300 1,09 Det Stavangerske Dampskibssels. 423.400 0,9

10 Morgan Guaranty Trust 410.000 0,9

Total 10 largest shareholders 29.603.899 65,3

The Board, the Management and theAuditor’s shares at 31.12.99: Shares

The Board:Sverre A. Farstad 22.252.199Per Norvald Sperre 0Sigmund Borgundvåg 20.000Bjørn Havnes 0Bjarne Sælensminde 85.000Per Erik Dalen 0

The Management:Terje J.K. Andersen 29.000Torstein L. Stavseng 32.000Karl-Johan Bakken 0

The Auditor:Ernst &Young AS 0

ALLOCATION OF SHARES AT 31.12.99:

N O R W E G I A N F O R E I G N T O T A LShare- Share Share- Share Share- Share

Total shares holders holding % holders holding % holders % holding %

1- 999 1.016 340.828 0,8 6 3.148 0,0 1.022 40,1 343.976 0,81.000- 49.999 1.408 5.743.822 12,7 43 451.984 1,0 1.451 56,9 6.195.806 13,7

50.000- 99.999 26 1.872.829 4,1 2 127.500 0,3 28 1,1 2.000.329 4,3100.000- 499.999 35 6.370.760 14,0 4 1.110.000 2,5 39 1,5 7.480.760 16,5More than 500.000 8 28.658.499 63,2 1 650.000 1,4 9 0,4 29.308.499 64,7

Total 2.493 42.986.738 94,8 56 2.342.632 5,2 2.549 100,0 45.329.370 100,0

NOTE

19NOTE

19Shareholder matters

The company’s share capital is NOK 45.329 dividedon 45.329.370 shares at NOK 1,00 per share in oneshare class. At the Annual General Meeting oneshare has one vote.At the Annual General Meeting 27.04.99 the Boardof Directors was given the authority to increase theshare capital by up to 6 million shares. The authorityalso includes an increase in capital for aconsideration other than cash, so that the Boardmay carry out mergers, purchases of business, assetsetc. The authority also permits the Board toestablish the terms for issuing the shares. Theauthority has not been used and will apply until theannual general meeting in May 2000. The board hasauthority to acquire on behalf of the company up to10% of the company’s own shares. The highest andlowest amount that can be paid for the shares isNOK 1,- and NOK 50,- per share. The authority willapply until 30.06.2000. The company has inFebruary and March 2000 acquired a total of551.500 shares (1.2%) at an average price of NOK26.82 per share.No member of the Board or the Management of theCompany has stock options.

19

NOTE

20NOTE

20Remuneration to executives, board of directors and auditor’s fee

Farstad Shipping ASA - Parent Company 1999 1998Managing DirectorWages 1.025 995 Pension liabilities 300 172 Other remuneration 585 1.007

1.910 2.174

Directors feesChairman of the Board 163 1555 members of the Board 605 575

768 730

Auditor’s feeFee for auditing 196 167Consulting fee 86 130

282 297

If the Managing Director or the Finance Director due to company takeover decides to resign or get dissmissed,they have the right to a compensation of two yearly wages. It is agreed upon that the Managing Director has anarrangement for resign remuneration, this is by 31.12.99 accumulated to NOK 133. The Managing Director has amutual agreement for early retirement by the age of 60.No member of the Board or the Management of the Company has stock options in Farstad Shipping. Themanagement (three persons) has a bonus arrangement based on company profit, limited to NOK 500 per person.The board evaluates both arrangements annualy Loan to managers and shareholders.The Company has granted loans to the Managing Director of NOK 1.440 and to the Finance Director of NOK579. The interest is fixed to the lowest non-taxable interest, this is 5 % for the time beeing. Loans are not grantedto members of the board or shareholders.

Farstad Shipping ASA

To the Annual Shareholders' Meeting of Farstad Shipping ASAWe have audited the annual financial statements of the Farstad Shipping ASA as of 31 December 1999, showinga profit of NOK 16.203.426,- for the parent company and a profit of NOK 80.454.000 for the Group. We havealso audited the information in the Board of Directors' report concerning the financial statements, the goingconcern assumption and the proposal for the allocation of the profit. The financial statements comprise thebalance sheet, the income and cash flow statements, the accompanying notes and the Group accounts. Thesefinancial statements are the responsibility of the Company’s Board of Directors and the Managing Director. Ourresponsibility is to express an opinion on the financial statements and on other information as required by theNorwegian Act on Auditing and Auditors.We conducted our audit in accordance with the Norwegian Act on Auditing and Auditors and generallyaccepted auditing principles. These principles require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free of material misstatement. An audit includesexamining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Anaudit also includes assessing the accounting principles used and the significant estimates made by Management,as well as evaluating the overall financial statement presentation. To the extent required by law and generallyaccepted auditing principles, an audit also comprises a review of the management of the Company's financialaffairs and its accounting and internal control systems. We believe that our audit provides a reasonable basis forour opinion.In our opinion,• the financial statements are prepared in accordance with Norwegian law and regulations and present fairly,

in all material respects, the financial position of the Company and of the Group as of 31 December, 1999, and the results of its operations and cash flows for the year then ended, in accordance with generally accepted accounting principles

• the company's management fulfilled its duty to properly register and document the accounting information in accordance with Norwegian law and generally accepted accounting principles

• the information in the Board of Directors' report concerning the financial statements, the going concern assumption, and the proposal for the allocation of the profit are consistent with the financial statements and comply with Norwegian law and regulations

Aalesund, 15 March 2000ERNST & YOUNG ASOdd Jarle Døving State Authorised Public Accountant (Norway)

Note: This translation from Norwegian has been prepared for information purposes only

A U D I TO R ’ S R E P O RT F O R 1999

20

II

Positive

• Major increase in the oil price

• No fatalities

• High operational quality

• Received HSE award from SAGA Petroleum

• Large percentage of term contracts

• Delivery of four new vessels in time and within budget

22

Farstad Shipping ASA

H I G H L I G H T S I N 1999

• Falling demand for supply vessels

• Cancellation of two term contracts

• One vessel laid up

• Large increase in crew costs

• Unstable working conditions- additional changes in the

taxation rules for shipping companies

• Increase in international interest rates

• Low share price

Negative

23

Mike GibbonSafety & Personnel Manager

Richard StablesAccountant

John R. MaxwellGeneral & Chartering Manager

Trevor ReidShip Manager

George GrantShip Manager

Jim WattShip Manager

Magnar GjerdeQuality/Safety Manager

Sylvi L. EliassenChartering Manager

Idar GjerdeFinance Manager

Hallkjell DahleFinance Manager IOS

Rolf SynnesCrewing Manager

Jan H. FarstadTechnical Manager

Felipe MeiraGeneral Manager

Marco MeloPurchaser

Nadimo NakhleOperations Supervisor

Carlos Temke and Aristido Reichert are employed by Petroserv, but are offering services to BOS according to a seperate agreement.

Adriana MonteiroAdministration Supervisor

24

Farstad Shipping ASA

Farstad Shipping ASAThe company’s headquarter is inAalesund. The company had at theyear-end 30 employees. This officeoperates 16 of the company’s vesselswith a crew of 328. In addition theoffice is responsible for supervising theconstruction and later operation of onevessel. The operation includes oneAHTS trading the North Sea and oneAHTS in Brazil, both owned by IOS.The vessels located in Brazil areoperated in coopertion with BOS.

Torstein L. StavsengFinance Director

Terje J. K. AndersenManaging Director

Karl-Johan BakkenDirector Market/Operation

Aalesund harbour

Aberdeen harbour

Macaé harbour

Farstad Shipping Ltd. The company is our managing office inAberdeen, with a total of 11 employees.The office is responsible for operating 9supply vessels and Lochnagar, whichwas reconstructed to a pipelaying vesselfor flexible pipes in 1998. The vessel isnow working in Brazil and are operatedin cooperation with DSND ConsubS.A. In total the office hasresponsibility of 193 sailors, most ofwhom is British. The office had thesupervision of construction of twoPSV’s built for Farstad in Glasgow in1998/99.BOS Navegacao LtdaBOS (Brazilian Offshore Services) wasestablished in June 1999 to operate,crew and market the Farstad vessels inBrazil. Also other shipping companies(Sealion and Solstad) have contractedBOS for their local operations. Thecompany now operates 11 vessels. The

company’s office is centrally situatednear the Petrobras base in Macae. BOShas 7 employees. 76 crew members areserving on the Farstad vessels. BOS is a joint venture company on a50/50 basis with Petroserv S.A.Petroserv is a Brazilian offshore servicecompany with long traditions withinthe Brazilian oil industry.Farstad Supply ASFarstad Supply is the ship owningcompany of the Farstad Group. Thecompany was founded in 1997, as aresult of the company’s efforts to adaptto the new tax regime for shippingcompanies. In the beginning of 2000,the Company owned 24 vessels, and 1vessel on order for delivery 25 February2000. The company has no employees.

P/R International Offshore Services ANSIOS owns 9 vessels. In addition it hasone vessel on a bare-boat contract. Thecompany was in March 2000 awarded a5-year coctract (+ 15 years options) fora vessel to be built by a South Koreanyard. The project is described on page37.The company has no employees.Farstad Shipping is the businessmanager for IOS. P&O Maritime Services in Melbourneis responsible for the operation of the 8vessels that IOS currently have in theFar East/Australia.Farstad International AS and Farstad Brasil ASThese companies have no functionbesides beeing the owner of IOS andBOS respectively.

Farstad Shipping ASA

P&O AUSTRALIA

100%

50%50%

FARSTAD SUPPLY AS

P/R INTERNATIONAL OFFSHORE SERVICES ANS

FARSTAD INTERNATIONAL AS

100%PETROSERV

50%50%

BOS NAVEGAÇÃO LTDA

FARSTAD BRASIL AS

100%

FARSTAD SHIPPING LTD.

25

A D M I N I S T R AT I O N A N D O R G A N I S AT I O N

100%

M A I N F I N A N C I A L F I G U R E S

1995

442.8

72.2

(220.0)

295.0

(116.9)

178.1

(35.2)

142.9

1,271.6

311.8

1,583.5

705.3

822.1

56,.1

238.1

255.8

248.1

1,583.5

705.3

44.5%

1,224.4

736.3

1999

801.3

0.2

(426.5)

375.0

(159.6)

215.4

(129.3)

86.0

2,688.8

392.9

3,081.7

1,223.7

1,693.2

164.8

186.8

228.2

287.3

3,081.7

1,223.7

39.7%

2,613.1

1,693.1

1998

706.7

62.0

(347.6)

421.1

(118.9)

302.2

(43.4)

258.7

2,087.7

281.4

2,369.1

1,188.6

1,047.5

133.1

133.4

148.4

369.5

2,369.1

1,188.6

50.2%

1,866.2

1,045.4

1997

598.3

75.1

(275.0)

398.5

(124.5)

274.0

(33.6)

240.4

1,709.2

259.3

1,968.5

976.9

877.3

114.3

167.6

145.0

368.3

1,968,.5

976.9

49.6%

1,579.0

875.9

1996

458.8

0.2

(242.5)

216.5

(120.1)

96.4

(37.9)

58.6

1,319.8

273.6

1,593.4

713.5

813.9

66.0

197.5

207.7

180.0

1,593.4

713.5

44.8%

1,264.7

710.8

FARSTAD SHIPPING ASA - GROUP

Farstad Shipping ASA

26

PROFIT AND LOSS ACCOUNT (NOK mill.)

Operating income ex. sale of fixed assets

Profit on sale of fixed assets

Operating expenses

Operating profit before depreciation

Depreciation

Operating profit

Net financial items

Pre-tax profit

BALANCE SHEET

Current assets

Fixed assets

Total assets

Short-term liabilities

Long-term liabilities

Equity capital

LIQUIDITY

Liquid assets

Working capital (1)

Cash flow (2)

CAPITAL

Total assets

Equity capital

Equity ratio (3)

FLEET

Book value of vessels, interest in vessels

Mortgage debt

Farstad Shipping ASA

1999

45.3

25.50

1,155.9

26.80

19.00

1.77

1.77

6.34

6.34

1.00

-1.00

1998

45.3

21.00

951.9

43.00

19.80

5.67

4.30

8.15

6.78

1.00

-1.00

1997

45.3

42.00

1,903.8

50.50

24.00

5.30

3.65

8.12

6.47

1.00

-1.00

1996

79.3

24.25

1,099.2

24.50

14.95

1.30

1.30

3.97

3.97

0.75

0.00

1995

113.3

14.95

677.7

15.50

12.30

3.14

1.54

5.47

3.88

0.75

0.00

DEFINITIONS:(1) Current assets - short-term liabilities.(2) Pre-tax profit - taxes paid + depreciation + change in revaluation of liabilities.(3) Equity capital as a % of total assets.(4) Total share outstanding x share price at 31.12.(5) Pre-tax profit - taxes paid, divided by average number of shares outstanding.(6) (2) divided by the average shares outstanding.(7) For 1995 and 1996 by write-downs of the share capital in 1996 and 1997.(8) 01.01. of the year shown in the actual column.

1. quarter 2. quarter 3. quarter 4. quarter 1. quarter 2. quarter 3. quarter 4. quarter

O P E R A T I N G I N C O M E(excl. profit on sales)

C A S H F L O W(before tax and profit on sales of vessels)

19981997

199619951994

mill. NOK mill. NOK

1999 19981997

199619951994

1999

100

80

60

40

20

0

250

200

150

100

50

0

S H A R E K E Y F I G U R E S

27

(NOK)

Share capital (NOK mill.)

Market price at 31.12

Market capitalisation (4) (NOK mill.)

Share price high

Share price low

Earning per share including sales profit (5)

Earning per share excluding sales profit

Cash flow per share including sales profit (6)

Cash flow per share excluding sales profit

Dividend per share (7)

RISK-amount (8)

31.12.9631.12.9531.12.9431.12.9331.12.92

Far ScandiaUT 705

Far ScotsmanME 202

Far SeaME 303 II

Far CrusaderME 303

Development in value of vesselsPSV AHTS

Value of vessels vs. mortgage

MortgageBook valueMarket value

mill. NOK

mill. NOK

150

120

90

60

30

0

3500

3000

2500

2000

1500

1000

500

031.12.92 31.12.93 31.12.94 31.12.95 31.12.96 31.12.97 31.12.98 31.12.99

92 93 94 95 96 97 98 99

Value adjustedequity

TOTAL PER SHARE

mill. NOK NOK2500

2000

1500

1000

500

0

50

40

30

20

10

01 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

1996 1997 1998 1999

Development inEBIT-margins

%

50

40

30

20

10

0

Total Per share(NOK mill.) (NOK)

Market value vessels 3.385,9 74,70Book value vessels 2.613,1 57,65

Excess value vessels 772,8 17,05

Book equity 1.223,8 27,00

Value adjusted equity 1.996,6 44,05

Value adjusted equity (VAE)AT 31.12.99

30.06.9931.12.9831.12.97 31.12.99

Business SegmentsNote 17 on page 18 is presentingfinancial details for the differentbusiness segments. In addition, somefinancial information is also givenwhen presenting the various marketson the pages 32 - 41. The allocation ofcosts and revenues, as well as withbalance sheet items, is associated withuncertainties. Analysis of profitabilityby business segment do not always givethe real picture of a certain segment.Other factors should be taken intoconsideration. These are; the differentneeds and requirements with respect totonnage that exist in each individualmarket, the useful financial life of eachvessel differs between markets, the ageof the fleet, the duration ofcharterparties, operational risk, taxregulations, the need for a localpartner, differences in administrativeand marketing services rendered.Value adjusted equityat 31.12.99

Estimated VAE has declined byapproximately 10% compared to thevalue on Dec. 31 1998. At the end of1999, VAE was estimated at NOK 2.0Bn. The market value of the Company(share price multiplied by number ofshares outstanding) increased duringthe same period by approx. 20%. Themarket value declined in 1998 by 50%.At the end of 1999, market value wasNOK 1,156 million.The market value of vessels The market value of the fleet iscalculated by averaging estimates from3 independent Norwegian ship brokersat the end of 1999. For a detailed tableof the value estimates for each vessel,

28

Farstad Shipping ASA

please turn to page 47. The brokers’assessments assume that the vessels arewithout charter and available forimmediate sale. Values are presentedin NOK by the brokers. The development of vessels’ valuesduring the last few years are shown onpage 28, represented by two vesselsbuilt in 1983 (Far Scotsman and FarCrusader) and two vessels built in 1991.While the market value for the Farstadfleet fell in 1998 by 7% on average, themarket values given at the end of 1999indicate a further decrease of 12%.Due to the current market outlook,market values are not expected todecline any further.Variation in brokers’ estimates The brokers have submitted their valueestimates using a high-low range. Theaverage of the high end of the estimatesgives a fleet market value of NOK3,483.8 million, equivalent to NOK46.20 per share. The average of the lowend of the range gives values of NOK3,288.1 million for the fleet and NOK41.90 per share. A 10% change in fleet valuecorresponds to a change in VAE ofNOK 7.50 per share.Excess valueEstimates of the value adjusted equitydoes not take into consideration otheradditional values in the company thanthe excess values of the vessels. Thevalue estimates assume that vessels canbe sold individually. There are noadjustments for excess values that arederived from charter contracts alreadyin service. There are no adjustmentsfor excess values tied to vessels underconstruction. Thus, no adjustments aremade for changes in value which couldderive from a sale of the fleet, or a saleof the whole company as a goingconcern. Goodwill is valued at NOK 4.7 million.This balance comes from the 1993acquisition of Sverre Farstad & Co.A/S and Farstad Shipping Ltd. Noadjustments of this goodwill is includedin the valuation of Farstad Shipping.The last years’ acquisition trend hasclearly demonstrated that buyers are

willing to pay a considerable premiumabove fair market value of the fleetwhen gaining control of an entirecompany.TaxesValue adjusted equity after tax is notcalculated. Farstad Shipping has, fromthe tax year 1997 and onward, adaptedto the new tax regime for Norwegianshipping companies. Anyhow, thecompany would not have reached anormal tax position for many years dueto a substantial investment program.However, the transitional regulationsmade it advantageous to adopt to thenew tax law as of 1997. The companyviews this adaptation as a long-termeffort.Farstad Shipping’s tax position in thefuture depends upon the resultsachieved in those subsidiaries that arenot included in the new regulations, theextent of activities on the Australiancontinental shelves and continentalshelves having a withholding taxsystem. For details on the company’stax position at the end of 1999, pleaserefer to note 11 in the financialstatements.Interest and exchange rateFor further details we refer to note 13on page 17. To the right you will find afigure presenting the company’s mainlenders and the estimated mortgagesorted by currency at the end of year2000. The interest risk exposure at thebeginning of 2000 is estimated to beNOK 0.13 per share for every 1.0% p.a.change in US interest rates. Theequivalent effect for 1.0% p.a. changein Norwegian rates is NOK 0.09 pershare. For a similar change in Britishrates, the effect would be NOK 0.06 pershare. Interest rate exposure is reducedon a continuous basis through hedgingactivities. The company expects the followingbreakdown in its estimated freightrevenues for 2000, sorted by currency:NOK approximately 25%, GBP approx-imately 30%, USD approximately 38%,and AUD approximately 7%. Anincreasing part of the total freightincome is in foreign currencies. To

hedge this development a larger part ofthe company’s debt has been swoppedto corresponding currencies during thelatest years. The currency riskassociated with the portion of revenuesthat does not have an offsetting cost, isreduced through the use of hedginginstruments. The effect on the cashflow of currency fluctuations is at anytime depending on the actual forwardagreements entered into. On generelterms, strong foreign currencies (USD,AUD, GBP) are positive for thecompanies activities. Note 15 on page18 presents the forward agreementsentered into at the year end.

Mortgage sorted by currencyEstimate at 31.12.2000

*)incl. 50% of the debt in IOS, based onexchangerates at 31.12.99

Mortgage*) sorted by lender

Sp. Møre MeesPierson

CBK/IOS DNB CBK

USD AUD

GBP NOK

A N A LY T I C A L I N F O R M AT I O N

29

33,3% 35,1%

7,3%9,6%

14,7%

31,5%

47,8%

1,8%18,9%

Farstad Shipping ASA

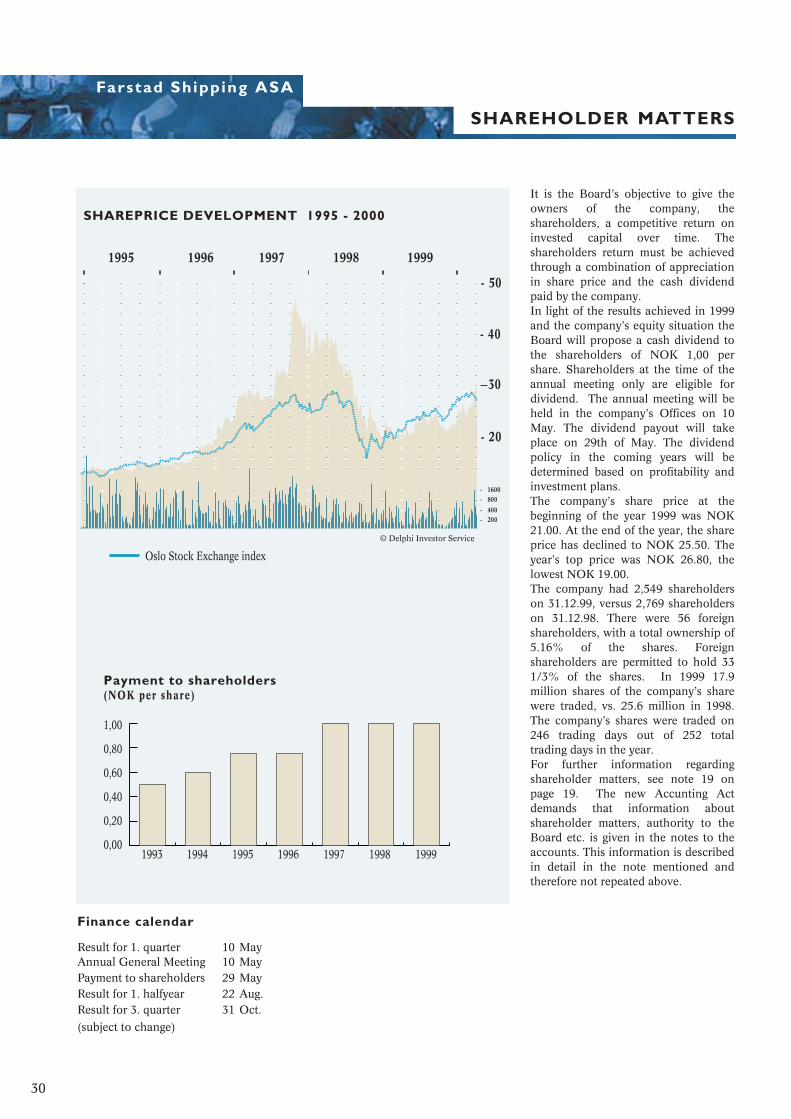

Payment to shareholders(NOK per share)

1993 1994 1995 1996 1997 1998 1999

Oslo Stock Exchange index

1,00

0,80

0,60

0,40

0,20

0,00

It is the Board’s objective to give theowners of the company, theshareholders, a competitive return oninvested capital over time. Theshareholders return must be achievedthrough a combination of appreciationin share price and the cash dividendpaid by the company.In light of the results achieved in 1999and the company’s equity situation theBoard will propose a cash dividend tothe shareholders of NOK 1,00 pershare. Shareholders at the time of theannual meeting only are eligible fordividend. The annual meeting will beheld in the company’s Offices on 10May. The dividend payout will takeplace on 29th of May. The dividendpolicy in the coming years will bedetermined based on profitability andinvestment plans.The company’s share price at thebeginning of the year 1999 was NOK21.00. At the end of the year, the shareprice has declined to NOK 25.50. Theyear’s top price was NOK 26.80, thelowest NOK 19.00.The company had 2,549 shareholderson 31.12.99, versus 2,769 shareholderson 31.12.98. There were 56 foreignshareholders, with a total ownership of5.16% of the shares. Foreignshareholders are permitted to hold 331/3% of the shares. In 1999 17.9million shares of the company’s sharewere traded, vs. 25.6 million in 1998.The company’s shares were traded on246 trading days out of 252 totaltrading days in the year. For further information regardingshareholder matters, see note 19 onpage 19. The new Accunting Actdemands that information aboutshareholder matters, authority to theBoard etc. is given in the notes to theaccounts. This information is describedin detail in the note mentioned andtherefore not repeated above.

SHAREHOLDER MATTERS

Finance calendar

Result for 1. quarter 10 May Annual General Meeting 10 MayPayment to shareholders 29 May Result for 1. halfyear 22 Aug.Result for 3. quarter 31 Oct.

(subject to change)

30