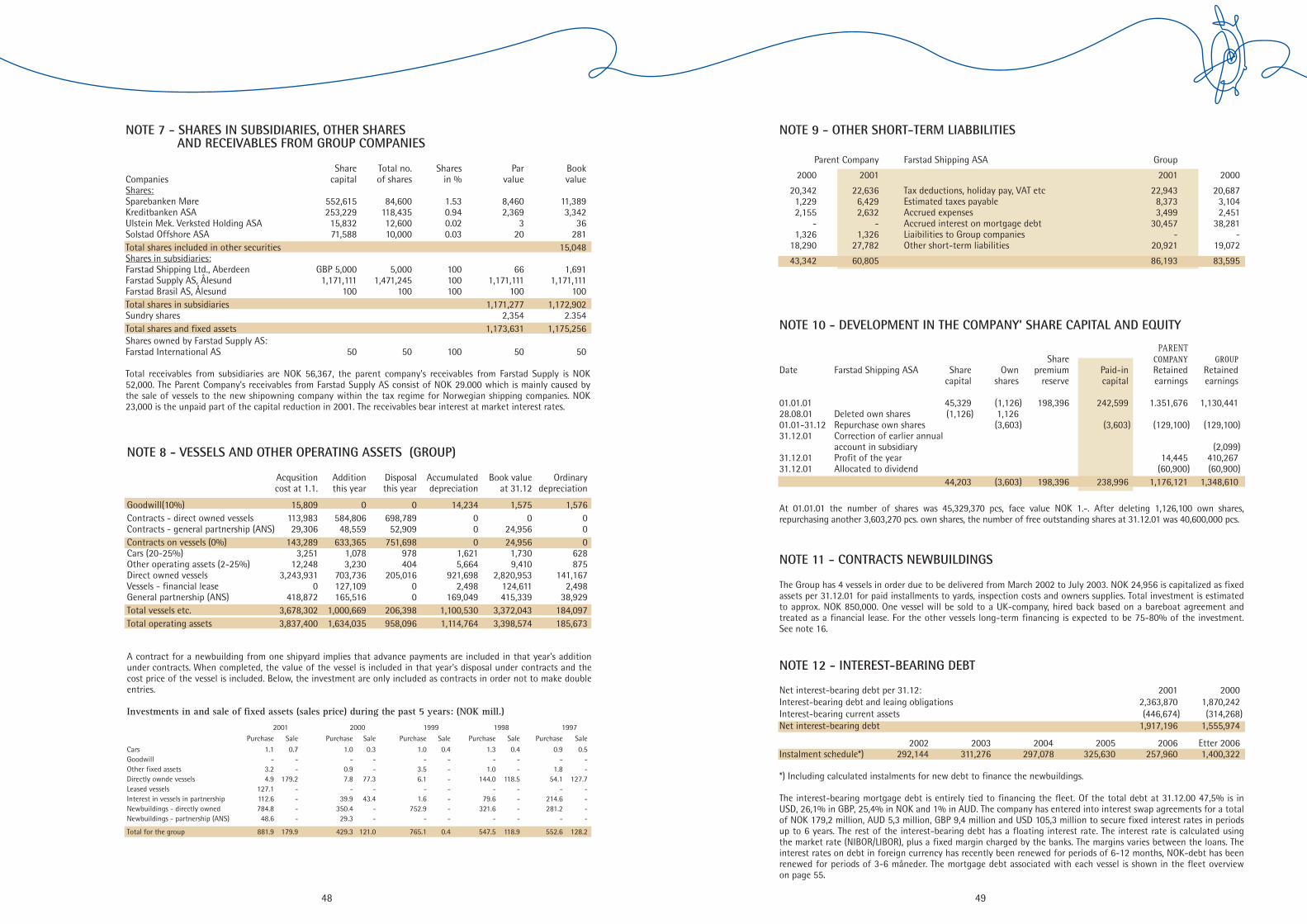

FARSTAD SHIPPING ASA ANNUAL REPORT 2001 · and 10 AHTS are owned through IOS, ... are operated in...

30

FARSTAD SHIPPING ASA ANNUAL REPORT 2001

Transcript of FARSTAD SHIPPING ASA ANNUAL REPORT 2001 · and 10 AHTS are owned through IOS, ... are operated in...

FARSTAD SHIPPING ASA

ANNUAL REPORT 2001

3

80

100

60

40

20

0

%

800

1000

600

400

200

0

(mill. NOK)

1993 1994 1995 1996 1997 1998 1999 2000 2001

1200

FINANCIAL DEVELOPMENT FARSTAD SHIPPING

Freight income Cash flow *) CF-margin

*) Cash flow (CF) is defined as result before tax and sales of operating assets + depreciation +/- unrealised disagio/agio concerning mortgage dept in foreign currency.

THIS IS FARSTAD SHIPPING ASA

Farstad Shipping’s strategy is to grow and maintain a long-term presence as a substantial operator of large and modern offshore service vessels on a world wide basis. The Company has focused its activities in the market segment that demands the largest and most advanced tonnage; anchor handling vessels (AHTS) with engine power greater than 10,000 BHP and platform supply vessels (PSV) with loading capacity greater than 2,000 DWT.

Farstad Shipping started its offshore activities in 1973 as one of the pioneers in the North Sea. At this time, the Company contracted its first supply vessel, an AHTS model UT 704. This was the first order of a UT vessel design that the Ulstein Group

received, a design that was to become standard in the industry. Since the initial order, the Company has ordered a total of 37 vessels of this type. In addition, favourable timing of trading of vessels has been instrumental in building the Company’s fleet as it remains today.

The Company has been traded on the stock exchange as a public company since 1988. In 1993, the Company was fully integrated when all its operations were consolidated. Through co-operation with P&O, Australia, and Petroserv, Brazil, Farstad Shipping has solidified its international commitment.

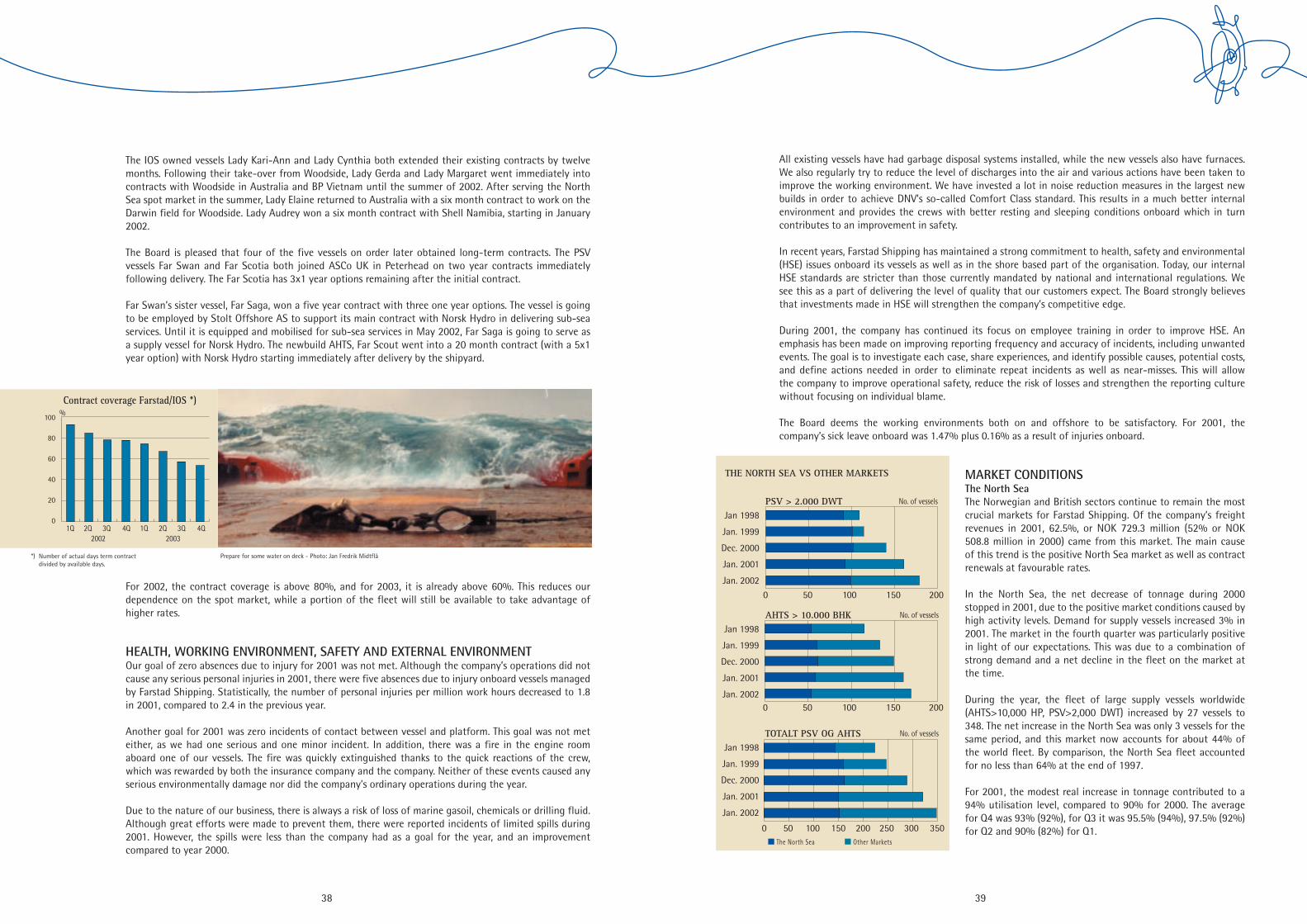

The Company’s fleet consists of 43 vessels, 21 of which are PSV’s and 22 are AHTS. Of these vessels, 4 PSV and 10 AHTS are owned through IOS, a joint venture with P&O, Australia, of which the Company owns 50%. In addition, 1 AHTS is chartered through a bare-boat agreement. The contract coverage is 83% for 2002 and 63% for 2003. The Company intends to maintain a long-term chartering profile.

Currently, Farstad Shipping has no vessels under construction. However, through its joint venture, Brazil Offshore Services (BOS), the Company is optimistic about securing 3 contracts with Petrobras, and winning these contracts would necessitate contracting new tonnage. Presently, IOS has 2 AHTS on order for delivery in March and July 2003.

The Company’s activities are managed by 55 employees in offices located in Ålesund, Aberdeen and Macae, Brazil. Vessels in the Far East/Australia are managed by our partner in Melbourne, P&O Maritime Services. At this time, 3 vessels are underway to new markets. When these are employed, 20 vessels will be located in the North Sea, 7 in Brazil, 7 in Australia, 5 in the Far East, 1 in West Africa and 1 in the Black Sea. There are a total of 950 sailing crew.

Farstad Shipping has approximately 1,700 shareholders. In the middle of March 2002, the price per share was NOK 47.00, which gives the Company a market value of approx. NOK 1.9 Bn.

Far Grip - Photo: Jan Fredrik Midtflå

2

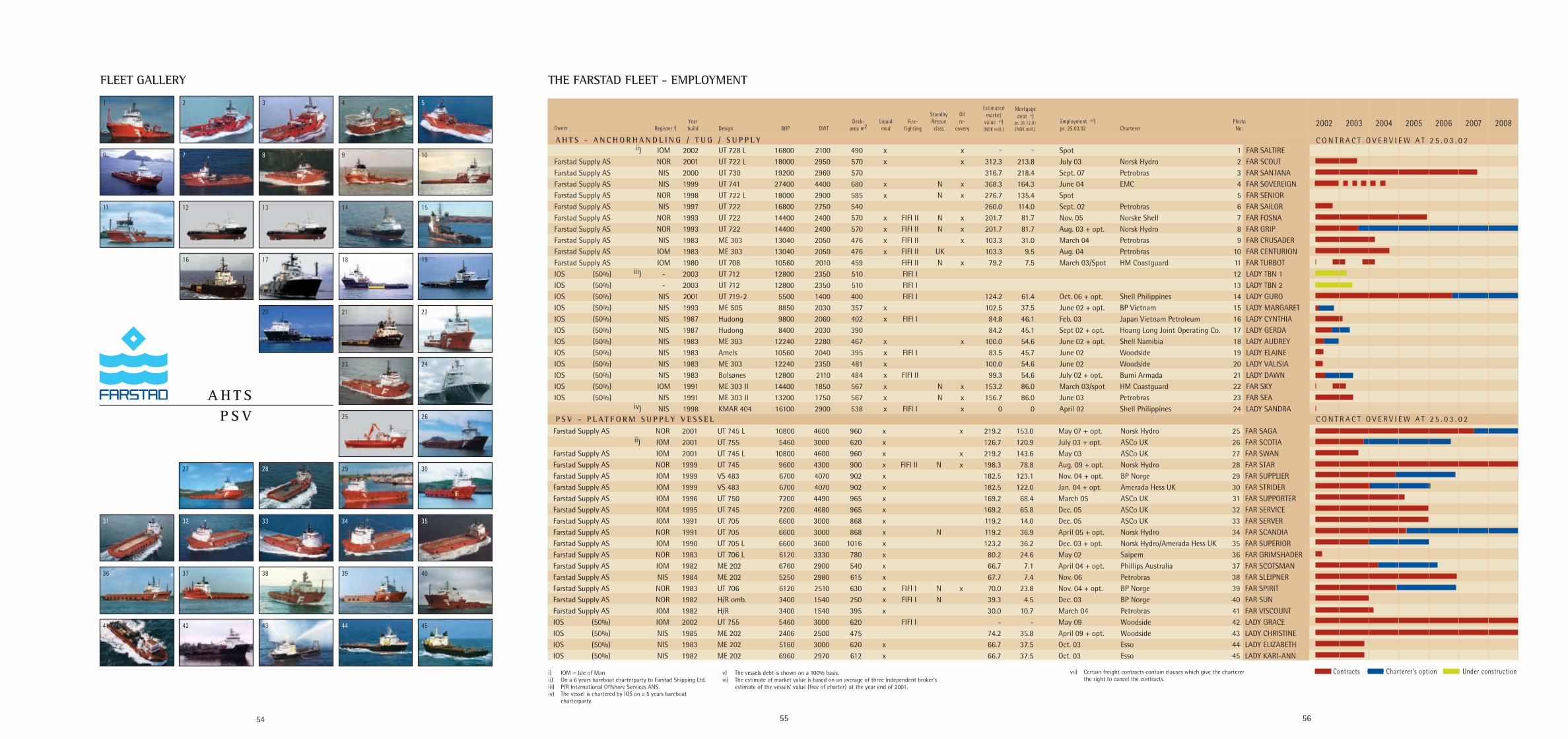

This is Farstad Shipping ASA 3Status and the road ahead 4Highlights in 2001 5Administration and organisation 6Main financial figures 8Analycal information 10Shareholder details 13Market strategy 16 The market for offshore supply vessels 17HSE-philosophy 28Helth, Safety and Environment 29Recruitment 33The Board of Directors 34Annual report 35Profit and loss account 42Balance sheet 43Cash flow statement 44 Notes to financial statement 45Auditor's report 53 Fleet gallery 54The Farstad Fleet - employment 55Glossary 57

CONTENTThe Farstad Fleet (100%):AHTS BHP> 10.000 11PSV DWT> 2.000 15PSV DWT< 2.000 2 28The IOS fleet (50%):AHTS BHP> 10.000 8AHTS newbuilds BHP> 10.000 2AHTS BHP< 10.000 3PSV DWT> 2.000 4 17

Total number of vessels 45

4 5

Last year, the American magazine Marine Money completed an analysis of profitability and solidity among 50 shipping and offshore companies. Based on fiscal 2000 results, all companies were ranked by six criteria, including net result and the balance sheet. Farstad Shipping ASA was ranked second only to Coflexip Stena Offshore.

The prize was awarded at J.P. Morgan’s offices in New York during Marine Money Week in June 2001.

We are very pleased to have maintained our profitability despite doubling our revenues since 1997.

STATUS AND THE ROAD AHEAD

Again we have put another successful year behind us. The year finished more favourable than anticipated in many areas, although there were some disappointments as well. The most significant events, either positive or negative, are summarised on the opposite page.

Despite the drama of terror and war as well as a worldwide recession, the offshore market showed strength until the end of December. Subsequently, the financial results were better than the previous year and favourable against the budget as well. With a strong result behind us, and a high contract coverage going into 2002, Farstad Shipping ASA is in an excellent position to continue its success in 2002.

In the early years, the growth strategy was to secure long-term charters prior to ordering a newbuild. During the latter part of the 90’s, we had achieved sufficient financial strength to order new vessels without securing charters in advance. Subsequently, when we envisaged market growth in 2000, we had the ability to order vessels at favourable prices and delivery dates. During the year 2000, the Company ordered 5 vessels without long-term contracts and 2 vessels (ordered through IOS - 50% owned) with contracts, representing a total investment of NOK 1,1 Bn. Today, all the vessels have been delivered, and 3 additional vessels have been purchased from Woodside and P&O. Four of the five wholly owned vessels have entered into long-term contracts.

The additional activity has put many parts of the organisation under considerable pressure. A great thanks is owed to all for great efforts throughout the year! The Company could not be successful without its motivated and skilled staff, both on and offshore. In order to continue to develop and maintain our position as one of the top performers, we need creative team members who have the drive to further improve the organisation.

We must recognise that safety and security is among the most valued aspects in life, both privately and professionally. We desire secure jobs, safety and recognition in a community, and safety for life and health. At Farstad Shipping, we want all our employees to feel secure and safe. We also want the spouses of all those who are at work either on land or at sea feel that their families are in a safe environment at work. Everyone’s support is needed in order to achieve and maintain such an environment. Safety and sound financial results are our top benchmarks for how we measure success.

We see it as a mission to include everyone in the community of our organisation and motivate employees at all levels to actively pursue improved safety at work in the time ahead.

Terje J. K. Andersen CEO

FOCUS ON PROFITABILITY

HIGHLIGHTS IN 2001

NEGATIVEOne vessel collided with an oil rig

Delay in the delivery of a new vessel to IOS by a Korean shipyard

Many new vessels under construction

High Norwegian interest rate levels

An uncertainty about the oil price

POSITIVEFocus on Health, Safety and Environment (HSE)No serious injuries to personnelExcellent and thorough work on safetyReceived Best Supplier Award from Petrobas in the large contracts category Overall high quality operations

A good year for the ownersGenerated significantly higher revenues than anticipatedMaintained the value of the Company’s tonnage (fleet)A rise in the Company’s stockA dividend increaseA buy-back of own shares equivalent to 8.2% of outstanding shares

A favourable North Sea marketNew tonnage absorbed into the marketHigh activity level in the markets outside the North SeaA good balance between demand for, and supply of tonnage

A positive development for subsidiariesEfficient and profitable operations of our subsidiaries in Aberdeen and Macae (Brazil)Significant growth experienced by IOS

Substantial increase of the fleetThe delivery of four new, wholly owned vessels on time and within budgetary constraints.The delivery of one new vessel to IOSIOS’s acquisition of the Woodside fleet (3 vessels)

Long-term employmentSolid contracts coverage for the Company’s vesselsSeveral new, long-term contracts obtained by existing tonnageSecuring long-term contracts for all five newly delivered vessels

Sale of the Lochnagar

Low interest rate levels internationally

Strong USD and GBP

Far Supplier operating in the North Sea - Photo: Espen Kvale

6 7

John R. MaxwellManaging Director

Jim WattShip Manager

Helen WilsonPersonnel Officer

Richard StablesAccountant

Mike GibbonOperation Manager

Fiona DawsonAssistant Chartering Manager

Dawn HughesAccounts Assistant

Dennis SangsterTransportation

Marilyn GibbonAdministration Manager

George GrantShip Manager

Trevor ReidShip Manager

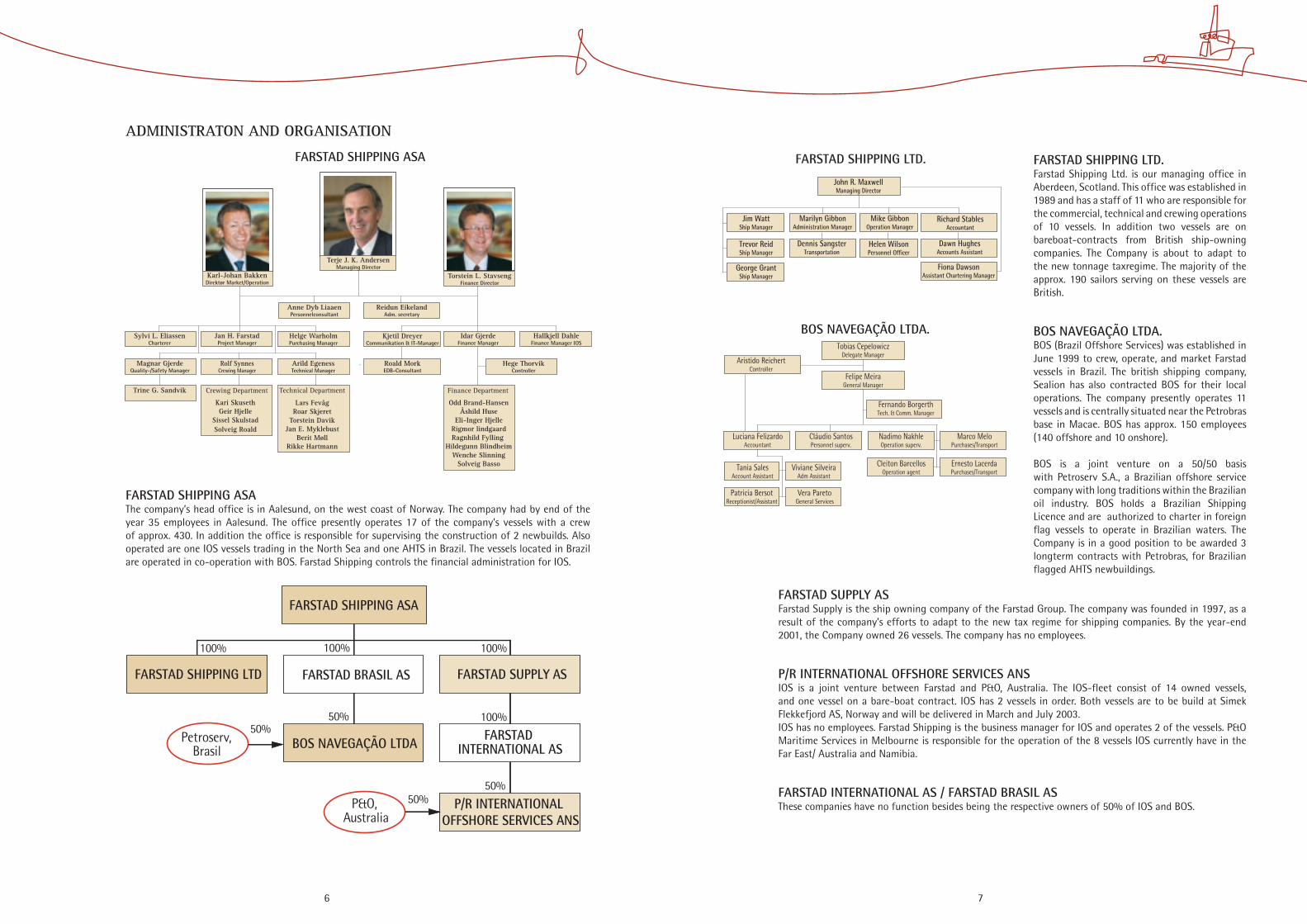

FARSTAD SHIPPING ASA

FARSTAD SHIPPING LTD FARSTAD BRASIL AS

BOS NAVEGAÇÃO LTDA

FARSTAD SUPPLY AS

FARSTAD INTERNATIONAL AS

P/R INTERNATIONAL OFFSHORE SERVICES ANS

100%

100%100%100%

50%

50%

P&O, Australia

50%

Petroserv, Brasil

50%

Felipe MeiraGeneral Manager

Tobias CepelowiczDelegate Manager

Fernando BorgerthTech. & Comm. Manager

Luciana FelizardoAccountant

Cláudio SantosPersonnel superv.

Nadimo NakhleOperation superv.

Cleiton BarcellosOperation agent

Ernesto LacerdaPurchases/Transport

Marco MeloPurchases/Transport

Aristido ReichertController

Tania SalesAccount Assistant

Viviane SilveiraAdm Assistant

Patricia BersotReceptionist/Assistant

Vera ParetoGeneral Services

FARSTAD SHIPPING ASA FARSTAD SHIPPING LTD.

BOS NAVEGAÇÃO LTDA.

Finance DepartmentTechnical Department

Terje J. K. AndersenManaging Director

Torstein L. StavsengFinance Director

Karl-Johan BakkenDirektør Market/Operation

Sylvi L. EliassenCharterer

Jan H. FarstadProject Manager

Helge WarholmPurchasing Manager

Magnar GjerdeQuality-/Safety Manager

Rolf SynnesCrewing Manager

Arild EgenessTechnical Manager

Idar GjerdeFinance Manager

Kjetil DreyerCommunikation & IT-Manager

Hallkjell DahleFinance Manager IOS

Odd Brand-HansenÅshild Huse

Eli-Inger HjelleRigmor lindgaardRagnhild Fylling

Hildegunn BlindheimWenche Slinning

Solveig Basso

Hege ThorvikController

Roald MorkEDB-Consultant

Trine G. Sandvik

Lars FevågRoar Skjeret

Torstein DavikJan E. Myklebust

Berit MøllRikke Hartmann

Kari SkusethGeir Hjelle

Sissel SkulstadSolveig Roald

Reidun EikelandAdm. secretary

Anne Dyb LiaaenPersonnelconsultant

Crewing Department

ADMINISTRATON AND ORGANISATION

FARSTAD SHIPPING ASAThe company’s head office is in Aalesund, on the west coast of Norway. The company had by end of the year 35 employees in Aalesund. The office presently operates 17 of the company’s vessels with a crew of approx. 430. In addition the office is responsible for supervising the construction of 2 newbuilds. Also operated are one IOS vessels trading in the North Sea and one AHTS in Brazil. The vessels located in Brazil are operated in co-operation with BOS. Farstad Shipping controls the financial administration for IOS.

FARSTAD SHIPPING LTD. Farstad Shipping Ltd. is our managing office in Aberdeen, Scotland. This office was established in 1989 and has a staff of 11 who are responsible for the commercial, technical and crewing operations of 10 vessels. In addition two vessels are on bareboat-contracts from British ship-owning companies. The Company is about to adapt to the new tonnage taxregime. The majority of the approx. 190 sailors serving on these vessels are British.

BOS NAVEGAÇÃO LTDA.BOS (Brazil Offshore Services) was established in June 1999 to crew, operate, and market Farstad vessels in Brazil. The british shipping company, Sealion has also contracted BOS for their local operations. The company presently operates 11 vessels and is centrally situated near the Petrobras base in Macae. BOS has approx. 150 employees (140 offshore and 10 onshore).

BOS is a joint venture on a 50/50 basis with Petroserv S.A., a Brazilian offshore service company with long traditions within the Brazilian oil industry. BOS holds a Brazilian Shipping Licence and are authorized to charter in foreign flag vessels to operate in Brazilian waters. The Company is in a good position to be awarded 3 longterm contracts with Petrobras, for Brazilian flagged AHTS newbuildings.

FARSTAD SUPPLY ASFarstad Supply is the ship owning company of the Farstad Group. The company was founded in 1997, as a result of the company’s efforts to adapt to the new tax regime for shipping companies. By the year-end 2001, the Company owned 26 vessels. The company has no employees.

P/R INTERNATIONAL OFFSHORE SERVICES ANSIOS is a joint venture between Farstad and P&O, Australia. The IOS-fleet consist of 14 owned vessels, and one vessel on a bare-boat contract. IOS has 2 vessels in order. Both vessels are to be build at Simek Flekkefjord AS, Norway and will be delivered in March and July 2003.IOS has no employees. Farstad Shipping is the business manager for IOS and operates 2 of the vessels. P&O Maritime Services in Melbourne is responsible for the operation of the 8 vessels IOS currently have in the Far East/ Australia and Namibia.

FARSTAD INTERNATIONAL AS / FARSTAD BRASIL ASThese companies have no function besides being the respective owners of 50% of IOS and BOS.

8 9

1996 1997 19981999 2000 2001

120

150

90

60

30

0

250

300

200

150

100

0

50

1996 1997 19981999 2000 2001

(mill. NOK)(mill. NOK)

20

60

80

100

40

01995 1997 1998 20001999

%

1996 2001

200

600

800

1200

400

0

mill. NOK

1000

1995 1997 1998 200019991996 2001

(NOK)

Share capital (NOK mill.)Market price at 31.12 Market capitalisation (4) (NOK mill.)Share price high Share price low Earnings per share including sales profit (5) Earnings per share excluding sales profit Cash flow per share including sales profit (6)Cash flow per share excluding sales profit Dividend per shareRISK-amount (7)Average number of outstanding shares

SHARE KEY FIGURES

FARSTAD SHIPPING ASA - GROUP

2001 44.2 45.00 1,827.0 49.90 28.00 9.57 8.14 13.55 12.08 1.50 -0.96 42,910,872

2000 45.3 35.40 1,564.8 40.50 23.30 5.41 3.75 10.25 8.59 1.25 -1.00 44,653,088

1999 45.3 25.50 1,155.9 26.80 19.00 1.77 1.77 6.34 6.34 1.00 -1.00 45,329,370

1998 45.3 21.00 951.9 43.00 19.80 5.67 4.30 8.15 6.78 1.00 -1.00 45,329,370

1997 45.3 42.00 1,903.8 50.50 24.00 5.30 3.65 8.12 6.47 1.00 -0.00 45,329,370

DEFINITIONS:

(1) Current assets - short-term liabilities.

(2) Pre-tax profit - taxes paid + depreciation + change in revaluation of liabilities.

(3) Equity capital as a % of total assets.

(4) Total share outstanding x share price at 31.12.

(5) Pre-tax profit - taxes paid, divided by average number of shares outstanding.

(6) (2) divided by average shares outstanding.

(7) 01.01. of the year shown in the actual column.

MAIN FINANCIAL FIGURES

1997

598.3 75.1 (275.0) 398.5 (124.5) 274.0 (33.6) 240.4

1,709.2 259.3 1,968.5 976.9 877.3 114.3

167.6 145.0 368.3

1,968.5 976.9 49.6%

1,579.0 875.9

2001

1,177.5 63.2 (509.6) 731,0 (185.7) 545.4 (119.0) 426.3

3,449,1 708.0 4,157.1 1,587.6 2,366.2 203.3

438.9 504.7 580.2

4,157.1 1,587.6 38.2%

3,408.2 2,243.0

2000

989.2 74.2 (481.0) 582.4 (182.4) 400.0 (151.7) 248.3

2,866.7 554.1 3,420.8 1,373.0 1,871.9 175.8

302.2 378.3 457.7

3,420.8 1,373.0 40.1%

2,707.7 1,870.2

PROFIT AND LOSS ACCOUNT (NOK mill.)

Operating income ex. sale of fixed assetsProfit on sale of fixed assetsOperating expensesOperating profit before depreciationDepreciationOperating profitNet financial itemsPre-tax profit

BALANCE SHEET

Fixed assetsCurrent assetsTotal assetsEquity capitalLong-term liabilitiesShort-term liabilities

LIQUIDITY

Liquid assets Working capital (1)Cash flow (2)

CAPITAL

Total assets Equity capitalEquity ratio (3)

FLEET

Book value of vessels, interest in vesselsMortgage debt

1999

801.3 0.2 (426.5) 375.0 (159.6) 215.4 (129.3) 86.0

2,688.8 392.9 3,081.7 1,223.7 1,693.2 164.8

186.8 228.2 287.3

3,081.7 1,223.7 39.7%

2,613.1 1,693.1

1998

706.7 62.0 (347.6) 421.1 (118.9) 302.2 (43.4) 258.7

2,087.7 281.4 2,369.1 1,188,6 1,047.5 133.1

133.4 148.4 369.5

2,369.1 1,188.6 50.2%

1,866.2 1,045.4

FARSTAD SHIPPING ASA - GROUP

OPERATING INCOME(excl. profit on sales)

CASH FLOW(before tax and profit on sales)

1 quarter 2 quarter 3 quarter 4 quarter 1 quarter 2 quarter 3 quarter 4 quarter

Norway UK Brazil Far East/Australia Other

FREIGHT INCOME FARSTAD SHIPPING IN % AND NOK SORTED BY SECTOR

10 11

250

200

150

100

50

0UT 745

(Far Service) UT 705

(Far Scandia)UT 722

(Far Grip)ME 303 II (Far Sea)

6000

5000

4000

3000

2000

1000

0 31.12.92 31.12.93 31.12.94 31.12.95 31.12.96 31.12.97 31.12.98 31.12.99 31.12.00 31.12.01

PSV AHTS(NOK mill.)

(NOK mill.)

1995 1996 1997 1998 1999 2000 2001

1200

1000

800

600

400

200

0

60

50

40

30

20

10

0

92 93 94 95 96 97 98 99 00 01

3500

3000

2500

2000

1500

1000

500

0

(NOK mill.)

(NOK mill.)

2000 2001

VESSELS SEGMENT2001 2000 2001 2000

OPERATING INCOME SORTED BY BUSINESS SEGMENT

AHTS PSV Norwegian sector UK sector

Brazsil Far East / Australia Others

EBIT IN % OF OPERATING INCOMESORTED BY REGION

Norwegian British Brazil Far East Australia

VALUE ADJUSTED EQUITY VS. MARKET CAPITALISATION

VAE 31.12.01 Total Per share*) (NOK mill.) (NOK)

Market value vessels 5,053.1 124.46Book value vessels 3,404.6 83.86Excess value vessels 1,648.5 40.60Book equity 1,587.4 39.10VAE 3,236.1 79.70 *) number of 40.6 mill

Value adjusted equity Market capitalisation

Total (NOK mill.)

DEVELOPMENT IN VALUE OF VESSELS

Market value Book value Mortgage

AREAS OF OPERATIONSIn note no. 19 in the financial statements, the Company’s activities are categorized by type of vessel and geography. In this footnote, a detailed account of each segment is given. A detailed account is also shown in the section describing each market segment, page 20 to 27. However, it should be noted that this breakdown does not support a complete profitability evaluation by segment. There is some degree of uncertainty associated with this type of breakdown by cost, revenues and balance sheet allocations. There are many other factors to consider; the markets’ different needs and requirement for tonnage, the vessels’ varying life cycle depending on which market they serve, the age of the tonnage, the contract terms, operational demands, tax laws, need for local partner, and the varying degree of administrative/marketing support required by each individual vessel.

VALUE ADJUSTED EQUITY (VAE)Following a 10% decrease in 1999, the value adjusted equity increased by approximately 42% in the year 2000. During the year 2001, it rose another 14%. VAE was estimated at NOK 3.2 billion at the end of year 2001 vs. NOK 2.8 billion at the end of year 2000. The market value of the Company (share price multiplied by number of shares outstanding) during the same time period increased by approximately 17%, after rising 35% in year 2001. At the end of 2000, the market value was NOK 1,827 million (vs. NOK 1,565 million at the end of year 2000).

MARKET VALUE OF VESSELSThe market value is based on estimates from three independent Norwegian brokers at the end of year 2001. An overview of estimated value for each vessel can be found in Fleet Overview on page 55. The valuations assume that the vessels are free of charter and immediately available for sale. All valuations are given in Norwegian currency.

The exhibit on the next page displays the growth in value for 2 PSV’s and 2 AHTS during recent years. After a decrease of 7% in 1998 and 12% in 1999, the year 2000 saw an increase of 17%. There was no material change in value in 2001. The recent trading of vessels in the second hand market has shown that our current value estimates are prudent.

ANALYTICAL INFORMATION

VARIATION IN BROKERS’ ESTIMATESThe brokers’ estimates use high/low intervals. Taking the average on the high end produces a fleet value of NOK 5,151 million (equivalent to VAE of NOK 82.10 per share), whereas the low end average gives a fleet value of NOK 4,955.2 million (equivalent to VAE of NOK 77.30 per share). A value appreciation of 10% would yield a change in VAE of NOK 12.45 per share, or 15.6%.

EXCESS VALUESThe calculation of value adjusted equity takes into account differences between the market value of the vessels and their book value. Any other factors that would impact value are excluded. The value estimates further assume that the vessels can and will be sold individually. No adjustments have been made for the potential value of chartering contracts nor for vessels under construction. Thus, the potential increase or decrease in value by selling the entire fleet in one piece, or the Company as a going concern is not contemplated in the calculation of value adjusted equity. However, the acquisitions seen during recent years have shown that buyers are willing to pay a significant premium in exchange for control over a company.

TAXATIONTax adjusted equity has not been estimated. The Company has, since 1997, conformed to the new taxation laws for the offshore industry. Due to substantial investments in new tonnage, the Company nonetheless would not be liable for income tax in Norway for several years. The transition regulations made it advantageous to conform to the new tax laws starting in 1997 and onward.

VALUE OF VESSELS VS. MORTGAGE DEBT

12 13

500

400

300

200

1,601,401,201,000,800,600,40 0,200,00

93 94 95 96 97 98 99 00 01

100

0

50

45

40

35

30

25

20

15

10

5

0

50

40

30

20

10

0 1997 1998 1999 2000 2001

%

600

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Farstad Shipping ASA

Farstad Shipping ASA

MORTGAGE SORTED BY CURRENCY

DEVELOPMENT IN EBIT MARGINS(Operating result divided by Operating income)

MORTGAGE SORTED BY LENDER

Mortgage is inclusive UK-lease and Farstad Shipping’s share of the mortgage in IOS

PAYMENT TO SHAREHOLDERS(NOK per share)

SHAREPRICE DEVELOPMENT 1992 - 2002(NOK per share)

DEVELOPMENT IN SHAREPRICE VS. OSLO EXCHANGE BENCHMARK INDEX 1992 - 2002

Oslo Stock Exchange Index

The consolidated Company’s total tax liability in the future is dependent upon the results in those subsidiaries that are excluded from the special offshore taxation laws, as well as the size of operations on the Australian continent and operations on those continents subject to withholding tax. Please see Note 13 in the financial statements for additional details

KEY FIGURESWhen calculating key figures, the average number of own shares held by the Company was subtracted from the total number of shares outstanding. The entire holding is subtracted from estimates made as of 31.12. For definitions of key figures, please see page 9.

OPERATING MARGINS When calculating operating margins, any profit made on a sale of a vessel has been subtracted. Other companies in the industry may practice different accounting principles, possibly preventing margins from being comparable between the various companies.

INTEREST AND FOREIGN EXCHANGE EXPOSURES (see note 12 on page 49)At the beginning of year 2001, the interest exposure was estimated to impact cash flow by NOK 0.05 per share for every percentage point change in US interest rates. A similar change in the NOK and GBP rates would yield a cash flow impact of NOK 0.10 and NOK 0.075 per share, respectively. The interest exposure is sought reduced on an ongoing basis through hedging.

The Company expects the following currency distribution for its 2002 freight revenues: GBP, 38%, USD, 36%, NOK, 20%, AUD, 6%. For the portion of revenues that is not matched by a corresponding operating cost or finance expenses or principal payments in same currency, foreign exchange exposure is sought reduced on an ongoing basis through various types of derivatives. The effect from currency fluctuations will depend upon what trading position the Company has taken at any given moment. Generally, a strong USD, GBP and AUD is favourable. Note 16 on page 51 displays our trading positions as of 31.12.01.

The exhibit to the left displays an overview of the Company’s largest lenders and mortgage debt by currency. Payments made on long term debt totalled NOK 282 million in year 2001. In 2002, payments are expected to reach NOK 285 million. Additionally, in conjunction with the deliveries of new vessels in 2002, the Company expects to increase its debt/leasing obligations by NOK 335 million.

USD (47,5%)

GBP (26,1%)

NOK (25,4%)

AUD (1,0%)

Sparebanken Moere (23,9%)

Nordea - Farstad Supply (22,2%)

Fokus Bank (15,0%)

Nordea - IOS (14,0%)

DnB - other (10,0%)

Gjensidige NOR (5,9%)

DnB - lease (5,0%)

Fortis Bank (4,0%)

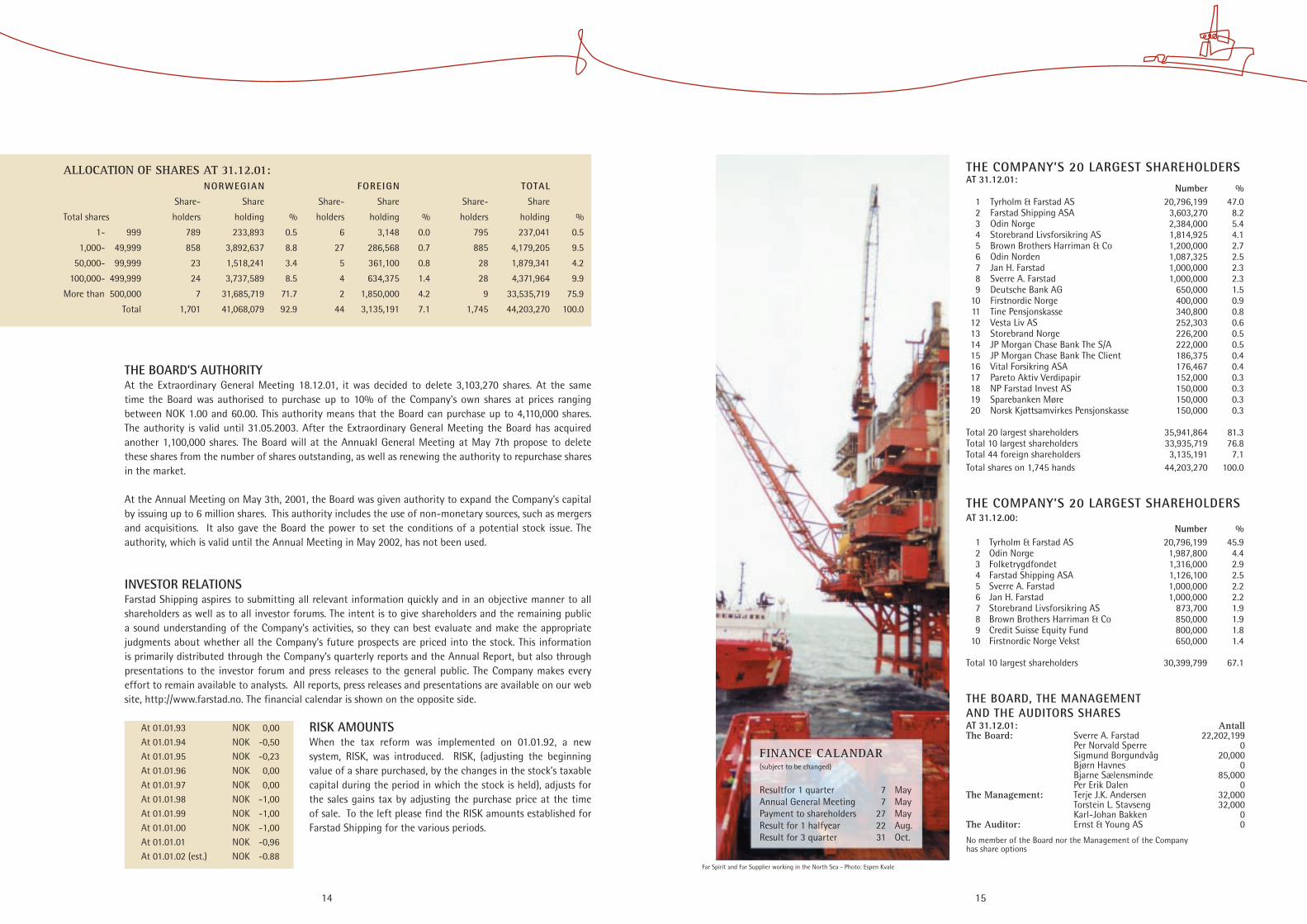

SHAREHOLDER DETAILS

DIVIDENDThe aim of the Board of Directors is to give the Company’s shareholders a competitive return on invested capital over time. This return must be realized through a combination of an increase in the Company’s share price as well as dividend payments.

In the light of 2001 and the Company’s equity position, the Board has proposed a dividend of NOK 1.50 per share. Only those who are shareholders at the time of the Annual Meeting are entitled to receive a dividend. The Annual Meeting is held on the Company’s premises on May 7th, 2002 and the dividend to be approved at this meeting will be paid on May 27th. The Company intends to continue the policy of dividend payments in the future. The size of the dividend will be subject to consideration based on factors such as profits, investments and our stock buyback program.

STOCK BUYBACKBy the end of February 2002, the Company had purchased 5,326,370 of its own shares. The total investment is NOK 193.7 million, an average of NOK 36.35 per share.

SHARE PRICE AND MARKET VALUEAt the beginning of 2001, the Company’s share price was NOK 35.40. At the end of the year, it had increased to NOK 45.00. The 27% growth in share price, paid dividends of NOK 1.25 per share (paid in May 2001) and a 24% increase in the Company’s value adjusted equity made 2001 an overall excellent year for the shareholders.

At the end of 2001, the Company’s market value was NOK 1.83 Bn. compared to NOK 1.56 Bn. in the previous year. The high/low share price in 2001 was NOK 49.90 and NOK 28.00, respectively.

SHAREHOLDER COMPOSITIONOn 31.12.01, there were 1,745 shareholders, compared to 2,031 at the end of 2000. 44 foreign shareholders owned 7,1% of shares outstanding. By law, foreign investors can own up to 33 1/3% of the shares. In 2001, 23,2 million shares were traded, vs. 16.4 million shares in 2000. The stock was traded on 241 out of a total of 251 trading days.

Year Number Price Average of shares mill. NOK NOK2000: 1) 1,126,100 35.8 31.83 2001: 2) 3,103,270 113.3 36.502001/02: 3) 1,100,000 44.6 40.53

1)are deleted. 2)will be deleted in April 2002.3)will be aproved deleted in May 2002.

14 15

FINANCE CALANDAR (subject to be changed)

Resultfor 1 quarter 7 May Annual General Meeting 7 MayPayment to shareholders 27 May Result for 1 halfyear 22 Aug.Result for 3 quarter 31 Oct.

ALLOCATION OF SHARES AT 31.12.01: NORWEGIAN FOREIGN TOTAL

Share- Share Share- Share Share- Share

Total shares holders holding % holders holding % holders holding %

1- 999 789 233,893 0.5 6 3,148 0.0 795 237,041 0.5

1,000- 49,999 858 3,892,637 8.8 27 286,568 0.7 885 4,179,205 9.5

50,000- 99,999 23 1,518,241 3.4 5 361,100 0.8 28 1,879,341 4.2

100,000- 499,999 24 3,737,589 8.5 4 634,375 1.4 28 4,371,964 9.9

More than 500,000 7 31,685,719 71.7 2 1,850,000 4.2 9 33,535,719 75.9

Total 1,701 41,068,079 92.9 44 3,135,191 7.1 1,745 44,203,270 100.0

THE COMPANY’S 20 LARGEST SHAREHOLDERS AT 31.12.01: Number % 1 Tyrholm & Farstad AS 20,796,199 47.0 2 Farstad Shipping ASA 3,603,270 8.2 3 Odin Norge 2,384,000 5.4 4 Storebrand Livsforsikring AS 1,814,925 4.1 5 Brown Brothers Harriman & Co 1,200,000 2.7 6 Odin Norden 1,087,325 2.5 7 Jan H. Farstad 1,000,000 2.3 8 Sverre A. Farstad 1,000,000 2.3 9 Deutsche Bank AG 650,000 1.5 10 Firstnordic Norge 400,000 0.9 11 Tine Pensjonskasse 340,800 0.8 12 Vesta Liv AS 252,303 0.6 13 Storebrand Norge 226,200 0.5 14 JP Morgan Chase Bank The S/A 222,000 0.5 15 JP Morgan Chase Bank The Client 186,375 0.4 16 Vital Forsikring ASA 176,467 0.4 17 Pareto Aktiv Verdipapir 152,000 0.3 18 NP Farstad Invest AS 150,000 0.3 19 Sparebanken Møre 150,000 0.3 20 Norsk Kjøttsamvirkes Pensjonskasse 150,000 0.3 Total 20 largest shareholders 35,941,864 81.3Total 10 largest shareholders 33,935,719 76.8Total 44 foreign shareholders 3,135,191 7.1 Total shares on 1,745 hands 44,203,270 100.0

THE COMPANY’S 20 LARGEST SHAREHOLDERS AT 31.12.00: Number % 1 Tyrholm & Farstad AS 20,796,199 45.9 2 Odin Norge 1,987,800 4.4 3 Folketrygdfondet 1,316,000 2.9 4 Farstad Shipping ASA 1,126,100 2.5 5 Sverre A. Farstad 1,000,000 2.2 6 Jan H. Farstad 1,000,000 2.2 7 Storebrand Livsforsikring AS 873,700 1.9 8 Brown Brothers Harriman & Co 850,000 1.9 9 Credit Suisse Equity Fund 800,000 1.8 10 Firstnordic Norge Vekst 650,000 1.4 Total 10 largest shareholders 30,399,799 67.1

THE BOARD, THE MANAGEMENT AND THE AUDITORS SHARESAT 31.12.01: Antall The Board: Sverre A. Farstad 22,202,199 Per Norvald Sperre 0 Sigmund Borgundvåg 20,000 Bjørn Havnes 0 Bjarne Sælensminde 85,000 Per Erik Dalen 0The Management: Terje J.K. Andersen 32,000 Torstein L. Stavseng 32,000 Karl-Johan Bakken 0The Auditor: Ernst & Young AS 0

No member of the Board nor the Management of the Company has share options

THE BOARD’S AUTHORITYAt the Extraordinary General Meeting 18.12.01, it was decided to delete 3,103,270 shares. At the same time the Board was authorised to purchase up to 10% of the Company’s own shares at prices ranging between NOK 1.00 and 60.00. This authority means that the Board can purchase up to 4,110,000 shares. The authority is valid until 31.05.2003. After the Extraordinary General Meeting the Board has acquired another 1,100,000 shares. The Board will at the Annuakl General Meeting at May 7th propose to delete these shares from the number of shares outstanding, as well as renewing the authority to repurchase shares in the market.

At the Annual Meeting on May 3th, 2001, the Board was given authority to expand the Company’s capital by issuing up to 6 million shares. This authority includes the use of non-monetary sources, such as mergers and acquisitions. It also gave the Board the power to set the conditions of a potential stock issue. The authority, which is valid until the Annual Meeting in May 2002, has not been used.

INVESTOR RELATIONSFarstad Shipping aspires to submitting all relevant information quickly and in an objective manner to all shareholders as well as to all investor forums. The intent is to give shareholders and the remaining public a sound understanding of the Company’s activities, so they can best evaluate and make the appropriate judgments about whether all the Company’s future prospects are priced into the stock. This information is primarily distributed through the Company’s quarterly reports and the Annual Report, but also through presentations to the investor forum and press releases to the general public. The Company makes every effort to remain available to analysts. All reports, press releases and presentations are available on our web site, http://www.farstad.no. The financial calendar is shown on the opposite side.

RISK AMOUNTSWhen the tax reform was implemented on 01.01.92, a new system, RISK, was introduced. RISK, (adjusting the beginning value of a share purchased, by the changes in the stock’s taxable capital during the period in which the stock is held), adjusts for the sales gains tax by adjusting the purchase price at the time of sale. To the left please find the RISK amounts established for Farstad Shipping for the various periods.

At 01.01.93 NOK 0,00 At 01.01.94 NOK -0,50 At 01.01.95 NOK -0,23 At 01.01.96 NOK 0,00 At 01.01.97 NOK 0,00 At 01.01.98 NOK -1,00 At 01.01.99 NOK -1,00 At 01.01.00 NOK -1,00 At 01.01.01 NOK -0,96At 01.01.02 (est.) NOK -0.88

Far Spirit and Far Supplier working in the North Sea - Photo: Espen Kvale

1716

20%

Approx.1.800 vessels worldwide

PSV>2.000 DWT

161 + 57*)AHTS>10.000 BHP

160 + 31*)

DWT BHP

Farstad Shipping’s strategy is to grow and maintain a long-term presence as a substantial operator of large and modern offshore service vessels worldwide. The Company is focused on the market segment that demands the largest and most advanced tonnage; anchor handling vessels (AHTS) > 10,000 BHP and platform supply vessels (PSV) > 2,000 DWT.

In order to solidify the Company’s financial position to fund future growth, it intends to maintain its profile of long term chartering, and combine this with trading older vessels. Also, Farstad will prioritise international growth. In 2001, 73% of the Company’s revenues came from markets outside Norway. This share is expected to grow in the time ahead. Farstad’s established operations infrastructure in Aberdeen, Macae, Brazil

and Melbourne gives the Company a high degree of flexibility to move vessels between the various markets.

In recent years, several of the established supply vessel operators have chosen to invest heavily to take advantage of opportunities in the areas of seismic, sub-sea and cable laying activities. Instead, Farstad has chosen to continue its investments within supply and anchor handling vessels. However, a portion of our newer and larger tonnage could be considered for other types of activities, provided that contractual obligations can be fulfilled without permanent alterations to the vessels. Such permanent alterations could, in addition to reducing the versatility of the vessel, also lower its resale value.

MARKET STRATEGY

THE MARKET FOR OFFSHORE SUPPLY VESSELS

GENERAL MARKET DEVELOPMENTHistorically, the oil industry has migrated from land to sea, and from shallow waters to deep sea. This has generated a completely different set of demands for technology. In our industry, activity in deeper waters has increased the demand for engine capacity, manoeuvrability, and winch capacity for AHTS. It is necessary that the vessels are able to operate safely and effectively in the tough weather conditions that often characterises deep-sea oil installations. The increased focus on safe operations has significantly contributed to the use of technology onboard our vessels.

The oil companies have increased their focus on cost, causing rationalisation efforts in transportation to and from oil field installations. The result is an increasing trend to use fewer, but larger PSV’s with large deck areas and substantial

tank capacities, allowing simultaneous transportation of various types of cargo. In the North Sea, this has been standard practice for years, and other markets are now following this trend.

The increased number of floating production units (FPSO/FPU) have significantly increased the demand for high levels of station keeping and manoeuvrability for the supply vessels. This is one of the causes of the increased number of large platform vessels in markets outside the North Sea.

The supply vessel fleet totals approximately 1,700-1,800 units worldwide, depending on the definition of “supply vessel”. About 20% of the world tonnage is found in our target market, AHTS with engine power greater than 10,000 BHP and PSV’s with loading capacity greater than 2,000 DWT.

Of today’s total fleet, about 850 units are in excess of 20 years old. By the end of 2003, an additional 400 vessels will be over 20 years old. These numbers signal an inherent need for fleet renewal, and with the help of market forces, the most outdated tonnage will be replaced by newer and more modern tonnage. Excess tonnage will either disappear from the market, or seek employment in other, less developed markets. In the short term, we do not expect the market to be impacted by this development.

Far Grip, Far Scandia and Far Star at the base of Mongstad - Photo: Jarle Furset

*) Number of vessels + number of vessels in order per January -02

20

15

10

5

0

18 19

80

60

40

20

0

100

80

60

40

20

0

0 10 20 30 40 50 60

35302520151050

2002 2003 2004

Jan. 2002 Jan. 1998

AHTS>10.000 HK and PSV>2.000 DWT Sorted by owners worldwide per January 02

Sanko

Stirling

Moekster

Olympic

Eidesvik

Surf

DOF

Swire

Havila

Solstad

Trico Marine

Seacor

Edison Chouest

Gulf Offshore

Farstad/IOS

Tidewater

Maersk

No. of vessels

1.Q 2.Q 3.Q 4.Q 1.Q 2.Q 3.Q 4.Q 1.Q

NEWBUILDS SORTED BY DELIVERY TIME

AHTS PSV - UT 755 PSV - Others

No. of vessels per January 02 excl. vessels built for US-Gulf

NEWBUILDS SORTED BY REGION per January 02

No. of vessels

Europe US Gulf Brazil Canada

AHTS >10.000 BHP PER REGION

PSV > 2.000 DWT PER REGION

Sailing fleet Newbuilds Total

Jan. 1998 115 42 157 Jan. 2001 160 31 191 Jun. 2001 166 33 201 Jan. 2002 169 38 207

Sailing fleet Newbuilds Total

Jan. 1998 106 55 164 Jan. 2001 161 57 218 Jun. 2001 164 62 226 Jan. 2002 179 54 233

NS Brazil FE-A WA GoM Canada China M SA-O

NS GoM SA FE-A WA M Canada

NS = North SeaFØ-A = Far East / AustraliaVA = West-Africa

GoM = Gulf of MexixoM = MediterraneanSA (-O) = South-Amerika (Others)

THE MOST IMPORTANT MARKETSThe North Sea remains the most important market for large supply vessels, although its share of the total fleet has decreased. In the beginning of 1998, 90 of a total of 109 large PSV (82.5%) and 54 of 115 large AHTS (47%) were employed in the North Sea. The corresponding numbers for 2002 were 99 of 179 large PSV (55%) and 54 of 169 large AHTS (32%). The number of large supply vessels has increased by 124 units during this period. Of this increase, the North Sea absorbed only 9 units, leaving a 115-unit increase in

markets outside the North Sea, an average of 30 units per year. The numbers for 2001 continued this trend.

The market for large PSV’s showed the strongest increase in demand. The market with the highest growth was the Gulf of Mexico, due to fleet renewals and increased deep-sea activities. The US built vessels dominate the market in the American part of the Gulf.

Increased focus on efficient transportation to oil platforms has caused the markets for large PSV to expand in Brazil, West Africa and the Far East/Australia. Additionally, many PSV’s have been converted for sub-sea service, cable laying and seismic activities, and have thus disappeared from the traditional supply market. However, some of these could relatively easily be converted back to serve the supply market.

During the last four years, there has been an increase in demand for large AHTS in markets outside the North Sea as well. The markets in West Africa, Brazil, the Mediterranean and Canada have been particularly strong. The growth in the Gulf of Mexico is a result of American exploration activity.

NEWBUILDING ACTIVITYIn recent years, significant construction activities have taken place, especially for large AHTS and PSV’s. Developments in the offshore industry have caused much of the construction activities during the last 10 years to focus on large vessels.

As of January 2002, orders for 92 large supply vessels had been placed; 38 AHTS and 54 PSV’s. Sixty percent of these orders are represented by European shipyards, mainly Norwegian. Most of the new vessels are currently unemployed. There are orders for 3 AHTS and 5 PSV’s placed with Brazilian shipyards. These are already on long-term contracts with Petrobas for use in Brazilian territory. Shipyards in the Far East, including China, have orders to build 11 AHTS and 4 PSV’s. In addition, there are 2 AHTS under construction in Canada. They will be in a position to compete for work in the North Sea. American companies currently have orders to build 10 PSV’s at American shipyards. With the current market outlook, these are expected to remain in the Gulf of

Mexico. Of the vessels under construction, 65 are scheduled for delivery by the end of March 2003, many of them during the fourth quarter of 2002. As always, possible delays in deliveries could dilute much of the market impact that multiple deliveries over such a short period of time is likely to cause. The demand in the various markets at the time of new deliveries will determine how these will affect the rates. If the trend from the past continues, it will take approximately two years to absorb the new vessels. The number of new vessels to be delivered in subsequent quarters, as well as new contracts awarded, can prolong this period.

Based on projections for a high oil price, the market outlook for supply vessels is very positive. Despite the number of vessels under construction, there are reasons to believe that the market will be able to absorb them. How long this would take remains a question. Only the North Sea has an active spot market for supply vessels. Should the markets outside the North Sea need a longer time period to absorb the new tonnage, this would have a negative impact on the North Sea market from the fourth quarter of 2002 and through the year 2003.

After all vessels currently on order have been delivered, the total fleet in this market segment will be double that of 1997.

RESTRUCTURING IN THE INDUSTRYWhereas the years 1997 and 1998 were marked by many changes in ownership, the three years since have seen little restructuring.

Easy access to capital, a very favourable supply market and a high valuation of supply stocks were factors that led to many changes in ownership during 1997 and 1998. American companies were particularly active, making companies such as Trico Marine, Gulf Offshore, Seacor and Tidewater significant players in the North Sea market. Also, the favourable market conditions caused many new orders for vessels to be built, a substantial portion of these by American companies to be constructed in the United States. Edison Chouest, among others, has established itself as a large competitor during this period. The American built vessels have had no significant impact on markets outside the Gulf of Mexico.

In year 2000, the biggest change in the market came from Tidewater, a company that through acquiring tonnage as well as building new vessels became a prominent competitor for large supply vessels world-wide. In 2001, Tidewater further consolidated its position. In March 2001, the American supply company Seacor announced that it had acquired Stirling, a significant British competitor in the North Sea market. During 2001, Gulf Offshore acquired Seatruck, a Norwegian company. With this exception, Norwegian companies have had little involvement in the restructuring process. Instead, there is a strong trend among Norwegian companies to enter into limited agreements within specific applications or markets. Examples include Solstad and Østensjø for the sub-sea segment, District Offshore and Solstad in the Brazilian market, and Eidesvik and Surf in the West African market.

China/Far East

20 21

1994 1995 1996 1997 1998 1999 2000 2001 E-2002

200

150

100

50

0

200

150

100

50

0 1994 1995 1996 1997 1998 1999 2000 2001 E-2002

300

250

200

150

100

50

0 92 93 94 95 96 97 98 99 00 01 E-02

100

80

60

40

20

0

%

0 5 10 15 20 25 30

0 5 10 15 20

Jan. 2001 Jan. 2002

Jan. 2001 Jan. 2002

CoastguardMaersk O+G

TeamBP Amoco

PhillipsSeaforth

Norsk HydroShellAsco

Statoil

EidesvikTFDS OffshoreMaersk Supply

District OffshoreSolstad RederiHavila Supply

SeacorTrico Supply

Gulf OffshoreFarstad Shipping

TERM DEMAND SORTED BY SECTOR

UK sectorNorwegian sector North Sea others

Boat-years

Production Construction Drilling Other Spot

TERM DEMAND SORTED BY ACTIVITY

TERM DEMAND SORTED BY OWNERS

Boat-years

TERM DEMAND SORTED BY OPERATOR

Boat-years

Boat-years

Boat-years

Supply Demand Utilisation

DEVELOPMENT IN DEMAND FOROFFSHORE SERVICE VESSELS

THE MARKET BALANCEThe average utilisation of the available fleet indicates the market balance. If the utilisation is above 90%, rates will be significantly impacted, although the top rates are achieved at 95% or higher.

The North Sea Market outlook for 2001 was positive. At the beginning of the year, utilisation rates were projected at around 91%. The actual average for the year came in at 94%, vs. 90% in the previous year. The utilisation was at or above 95% for all months during the second and third quarter in 2001. Only January came in below 90%. As a result, all supply vessels experienced excellent rates throughout the year.

For the fourth quarter, the utilisation degree was projected at 84%, but instead it came in at 93%, thus contributing to making 2001 an excellent year overall. In this quarter, the positive market was caused by a combination of high activity and the shift of vessels from the North Sea to other markets. The actual utilisation degree by quarter was: Q1 - 90% (82% in year 2000), Q2 - 97.5% (92%), Q3 - 95.5 (94%), and Q4 - 93% (92).

The demand side in the North Sea market has remained relatively stable in recent years. The supply side has therefore played a pivotal role in creating the market conditions. An extensive expansion program has contributed to a considerable increase in the size of the fleet, but the potential impact of this build-up has been partially offset by the strength of other markets world wide. During 2001, the number of supply vessels increased by 27 units to 348 units worldwide. During the same period, the North Sea market increased by only 3, to 153 units.

For 2002, the average utilisation percentage is projected to be 92%, assuming that all vessels under construction (except those built in the U.S. and Brazil) are being added to the North Sea fleet. However, projections for demand in other markets indicate that the trend of net decrease in the North Sea fleet is going to continue in 2002 as well. The second and third quarter in particular are expected to yield a positive spot market in the North Sea.

THE NORTH SEA MARKET

DEMAND FOR SUPPLY VESSELSFollowing a relatively weak first quarter, demand really picked up in the second quarter, and stayed strong during the remainder of the year. On average, the demand in the North Sea increased by six boat-years in 2001, but remained eight boat-years lower than the record-breaking year 1998.

Average demand for supply vessels is projected to increase in 2002. A demand for 199 boat-years would be the best market since 1993.

MARKET FOR SHORT-TERM CONTRACTSAfter declining by 16 boat-years for 1999 and 2000 combined (or 10%), the market for short-term contracts came back in 2001 to a level comparable to 1998. The growth has been particularly strong in the British sector. For 2002, the market is projected to remain flat.

Farstad Shipping is the largest supplier of short-term contracts in the North Sea market, with the number of contracts increasing in 2001. Despite this, the largest competitor, Gulf Offshore, almost closed the gap in 2001. On the demand side, Statoil is the operator with the most vessels contracted on a short-term basis, with ASCO in second place. Currently, Farstad has no short-term contracts with Statoil, but ended last year with six contracts with ASCO. With only one contract less, Norsk Hydro is Farstad Shipping’s second largest client.

Periods of favourable market conditions typically cause a shift towards short-term contracts. While this market represented 81% of total demand in both 1997 and 1998, it fell to 76.8% in 1999, and to 76% in year 2000. It rose again during 2001 and ended at 82%. For 2002, it is expected to remain stable. Projections for the delivery of new tonnage are the major driver in the market for short-term contracts as well as for the spot market.

SUPPORTING OIL-PRODUCING FIELDS AND STANDBY DUTIESFields in the production phase represent the largest component of the short-term market. In 2001, the demand totalled 115 boat-years, 6 boat-years higher than in the previous year. All production related activities represented 72% of short-term demand in 2001. For 2002, this number is projected to remain stable. Comparable numbers for previous years are 77% in 2000, 78% in 1999, and 73% in 1998. In 1991/1992, this number was as low as 50%.

Far Supplier - Photo: Jan Fredrik Midtflå

22 23

0 5 10 15 20 25

Jan. 2002Jan. 1996

VESSELS IN THE NORTH SEA SORTED BY OWNERS

OIL

Stirling

Smith Loyd

Viking

Olympic

Toisa

TFDS

Oestensjoe

Moekster

Eidesvik

Broevig

DOF

Tidewater

Solstad

Havila/Saevik

Maersk

Trico Marine

Seacor

Farstad/IOS

Gulf

No. of vessels

In spite of the Brazilian currency (Real) fluctuation, the domestic power supply shortage during the second half of the year and the close Argentinean crisis, the Brazilian economy performed reasonably well during 2001. The year closed with a trade balance surplus of USD 1.2 billion, the first in years, setting the pace for a sustainable growth in the surplus for the coming years. Inflation (consumer price index) closed the year at 7.7% against a governmental inflation target of 6%. The country’s economic outlook for 2002 is generally good. The economy is expected to grow between 2.5% and 3%. Governmental inflation target for 2002 is set for 3.5% .

In June 2001 the Brazilian Petroleum Board (ANP) promoted its third round of licensing for E&P blocks in Brazil. The round attracted newcomers, such as Phillips, Wintershall, Maersk and Ocean Energy. Petrobras was once more the dominant winner with 13 blocks awarded out of the 53 offered.

In August, the three-year exploration period set by the Law 9478/97 for the first partnership contracts awarded to Petrobras and other international operators expired. As a result, 57 exploration areas were relinquished back to ANP and, under the contract terms, as amended in 1999, 28 blocks with oil and/or gas discoveries made were granted an extension of additional two years in the exploration phase. Of these, three important discoveries in offshore blocks were confirmed; BC-2 (Campos Basin; operator Total, Fina and Elf), BS-4 (Santos Basin; operator Shell) and BCAM-40 (Camamú Basin; operator Petrobras).

Petrobras is still the largest oil and natural gas producer in Brazil, and closed 2001 with a record crude production peaking at 1,568,000 bopd, of which 1,274,000 bopd from the Campos Basin.

At Campos Basin, the coming into production of platforms P-40 and P-38 contributed significantly to offset the production loss resulted from the P-36 accident. The exceptional performance of P-40 subsea wells, like the record breaker MLS-42 (1,212 meters water depth) which is producing about 40,000 bopd, has to be mentioned as an important event.

Other operators like Enterprise Oil and Chevron-Texaco have also started the development of oilfields in the Campos Basin where first production from a non-PETROBRAS operated field, Enterprise’s Bijupirá and Salema, is expected to begin in mid 2003.

RESULT PER SECTOR Norwegian sector British sector

2001 2000 2001 2000

Freight income 315.397 309.292 413.936 199.455

Operation- and administration cost 157.641 133.109 146.775 106.664

Operating result before depreciation (EDBIT) 157.756 176.183 267.161 92.791

Depreciation 56.323 57.831 56.135 30.791

Operating result vessels (EBIT) 101.433 118.352 211.026 62.000

EDBIT % 50,0% 57,0% 64,5% 46,5%

EBIT % 32,2% 38,3% 51,0% 31,1%

Supplying fields in production mostly consists of containerised deck cargo. A modern supply vessel can transport many other products as well; Methanol, mixed drill fluids, brine, water and oil. In addition, there is dry bulk such as cement, barite and bentonite.

Large AHTS are used for standby services in production fields because they, in addition to their tow and anchor handling capabilities, are equipped to fight fires, perform rescue services and anti-pollution duties.

DEVELOPMENT ACTIVITIES AND OTHER ACTIVITIESThe demand for service associated with field development activities, such as new fields and infrastructure, pipelines, pumping stations and loading buoys, only made up 12 boat-years in 2001. In addition, 12 supply vessels have been involved with sub-sea, cable laying activities and rescue/coast guard duties. The record year for this segment was in 1998, when 26 boat-years were contracted for in development related activities. For 2002, no increases are projected.

EXPLORATION ACTIVITIESAs a result of significant improvement in productivity and logistics, the number of offshore service vessels contracted to support exploration activities has decreased in recent years. This trend was amplified in 1999, due to cost cutting activities by oil companies, which resulted in a reduction of rig activities. Sometime during 2000, this trend turned around. In 1992, the demand for supply vessels for this type of activity was 61 boat-years. In 1999 and 2000, the demand totalled 10 and 13 boat-years, respectively. In 2001, demand increased to 20 boat-years and is projected to remain at this level in 2002.

SPOT MARKETHistorically, the spot market has represented 20-25% of total demand. During boom years, such as 1997 and 1998, this share fell to under 20%. This happened again in 2001. The tightening in the spot market is a result of favourable market projections that causes the oil companies to attempt to secure supply by signing up for more vessels on short-term contracts, leaving fewer vessels available in the spot market. For 2002, the spot market’s share of the total is projected to be 20%. A substantial portion of the spot activity comes from Aberdeen and on British sector, and is directed towards all the activities described above.

THE MARKET IN BRASIL

Far Santana participate at the towing of “PETROBRAS P-40” outside Rio de Janeiro

24 25

0 2 4 6 8 10 12

0 10 20 30 40

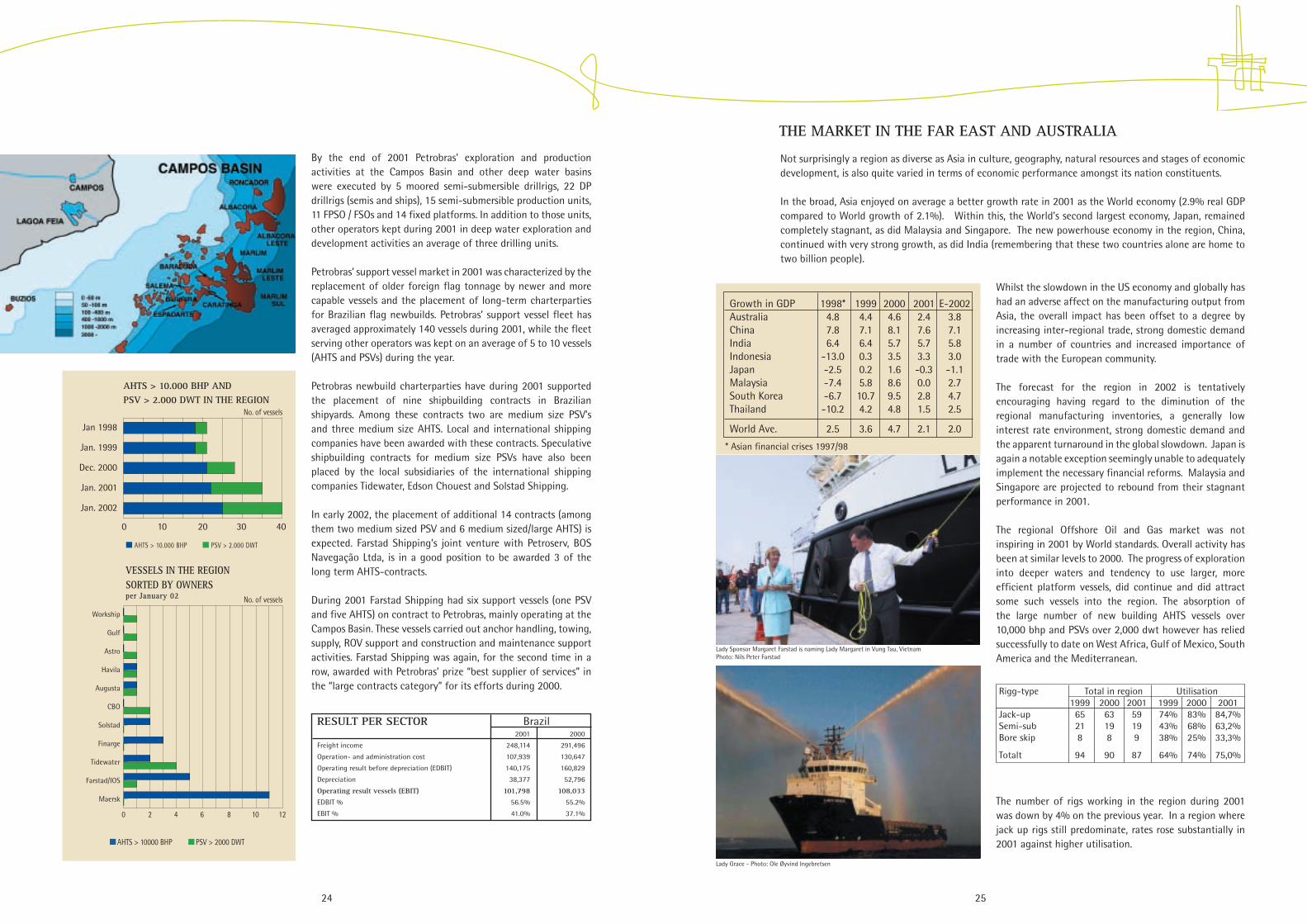

Not surprisingly a region as diverse as Asia in culture, geography, natural resources and stages of economic development, is also quite varied in terms of economic performance amongst its nation constituents.

In the broad, Asia enjoyed on average a better growth rate in 2001 as the World economy (2.9% real GDP compared to World growth of 2.1%). Within this, the World’s second largest economy, Japan, remained completely stagnant, as did Malaysia and Singapore. The new powerhouse economy in the region, China, continued with very strong growth, as did India (remembering that these two countries alone are home to two billion people).

Whilst the slowdown in the US economy and globally has had an adverse affect on the manufacturing output from Asia, the overall impact has been offset to a degree by increasing inter-regional trade, strong domestic demand in a number of countries and increased importance of trade with the European community.

The forecast for the region in 2002 is tentatively encouraging having regard to the diminution of the regional manufacturing inventories, a generally low interest rate environment, strong domestic demand and the apparent turnaround in the global slowdown. Japan is again a notable exception seemingly unable to adequately implement the necessary financial reforms. Malaysia and Singapore are projected to rebound from their stagnant performance in 2001.

The regional Offshore Oil and Gas market was not inspiring in 2001 by World standards. Overall activity has been at similar levels to 2000. The progress of exploration into deeper waters and tendency to use larger, more efficient platform vessels, did continue and did attract some such vessels into the region. The absorption of the large number of new building AHTS vessels over 10,000 bhp and PSVs over 2,000 dwt however has relied successfully to date on West Africa, Gulf of Mexico, South America and the Mediterranean.

The number of rigs working in the region during 2001 was down by 4% on the previous year. In a region where jack up rigs still predominate, rates rose substantially in 2001 against higher utilisation.

Rigg-type Total in region Utilisation 1999 2000 2001 1999 2000 2001Jack-up 65 63 59 74% 83% 84,7%Semi-sub 21 19 19 43% 68% 63,2%Bore skip 8 8 9 38% 25% 33,3%

Totalt 94 90 87 64% 74% 75,0%

* Asian financial crises 1997/98

Growth in GDP 1998* 1999 2000 2001 E-2002Australia 4.8 4.4 4.6 2.4 3.8China 7.8 7.1 8.1 7.6 7.1India 6.4 6.4 5.7 5.7 5.8Indonesia -13.0 0.3 3.5 3.3 3.0Japan -2.5 0.2 1.6 -0.3 -1.1Malaysia -7.4 5.8 8.6 0.0 2.7South Korea -6.7 10.7 9.5 2.8 4.7Thailand -10.2 4.2 4.8 1.5 2.5

World Ave. 2.5 3.6 4.7 2.1 2.0

RESULT PER SECTOR Brazil 2001 2000

Freight income 248,114 291,496

Operation- and administration cost 107,939 130,647

Operating result before depreciation (EDBIT) 140,175 160,829

Depreciation 38,377 52,796

Operating result vessels (EBIT) 101,798 108,033

EDBIT % 56.5% 55.2%

EBIT % 41.0% 37.1%

By the end of 2001 Petrobras’ exploration and production activities at the Campos Basin and other deep water basins were executed by 5 moored semi-submersible drillrigs, 22 DP drillrigs (semis and ships), 15 semi-submersible production units, 11 FPSO / FSOs and 14 fixed platforms. In addition to those units, other operators kept during 2001 in deep water exploration and development activities an average of three drilling units.

Petrobras’ support vessel market in 2001 was characterized by the replacement of older foreign flag tonnage by newer and more capable vessels and the placement of long-term charterparties for Brazilian flag newbuilds. Petrobras’ support vessel fleet has averaged approximately 140 vessels during 2001, while the fleet serving other operators was kept on an average of 5 to 10 vessels (AHTS and PSVs) during the year.

Petrobras newbuild charterparties have during 2001 supported the placement of nine shipbuilding contracts in Brazilian shipyards. Among these contracts two are medium size PSV’s and three medium size AHTS. Local and international shipping companies have been awarded with these contracts. Speculative shipbuilding contracts for medium size PSVs have also been placed by the local subsidiaries of the international shipping companies Tidewater, Edson Chouest and Solstad Shipping.

In early 2002, the placement of additional 14 contracts (among them two medium sized PSV and 6 medium sized/large AHTS) is expected. Farstad Shipping’s joint venture with Petroserv, BOS Navegação Ltda, is in a good position to be awarded 3 of the long term AHTS-contracts.

During 2001 Farstad Shipping had six support vessels (one PSV and five AHTS) on contract to Petrobras, mainly operating at the Campos Basin. These vessels carried out anchor handling, towing, supply, ROV support and construction and maintenance support activities. Farstad Shipping was again, for the second time in a row, awarded with Petrobras’ prize “best supplier of services” in the “large contracts category” for its efforts during 2000.

PSV > 2000 DWT AHTS > 10000 BHP

VESSELS IN THE REGION SORTED BY OWNERS per January 02

AHTS > 10.000 BHP AND PSV > 2.000 DWT IN THE REGION

AHTS > 10.000 BHP PSV > 2.000 DWT

No. of vessels

No. of vessels

Workship

Gulf

Astro

Havila

Augusta

CBO

Solstad

Finarge

Tidewater

Farstad/IOS

Maersk

Jan 1998

Jan. 1999

Dec. 2000

Jan. 2001

Jan. 2002

THE MARKET IN THE FAR EAST AND AUSTRALIA

Lady Sponsor Margaret Farstad is naming Lady Margaret in Vung Tau, Vietnam Photo: Nils Peter Farstad

Lady Grace - Photo: Ole Øyvind Ingebretsen

26 27

0 2 4 6 8 10 12

0 10 20 30 40

0 3 6 9 12 15

0 10 20 30 40 50

0 10 20 30 40

0 3 6 9 12 15

Vessel owners enjoyed good trading due, to the fine balance between supply and demand. Vessel utilisation, whilst hard to provide an exact figure, was estimated to be around 93% for the over 8,000 bhp AHTS vessels and close to 100% on the PSV’s. Whilst the outlook for 2002 gives owners confidence in being able to maintain high utilisation and satisfactory rate levels, the region continues to be characterised by multiple well programs. The sprinkling of these programs throughout the region and their timing is such as to maintain a sensitivity in the market to the balance between supply and demand. In essence, the market remains a sound one for owners, providing the migration of vessels from the North Sea and US Gulf is against an incremental expansion in the market and this will only be incremental in 2002.

Both IOS and other shipowners will within shortly bring other vessels into the region to meet the gradual increase in demand. Tidewater will bring another PSV to the region for term work. Similarly, BOA has recently moved their two Chinese new build AHTS vessels back from the North Sea against a specific drilling program in Malaysia and Farstad will also move a vessel in for the BP Vietnam Lan Tay field development.

IOS will introduce two more PSV’s early in 2002 One of the vessels is the newbuild Lady Grace, UT 755, delivered from Aker Brevik in March 2002, and which will enter into a 7 year contract to Woodside, working out of Dampier, Australia. The other PSV is Far Scotsman, which has achieved a two year time charter with Phillips in Australia commencing April 2002. The PSV is in turn being bareboat chartered from Farstad Shipping ASA for a minimum of two years. In August IOS took delivery of the 3 Woodside vessels, Lady Margaret, Lady Gerda and Lady Christine. The last one is a PSV which at the delivery entered into a 7 year contract to Woodside. At the end of October, Lady Guro, a UT 719-2 design multipurpose vessel, was delivered from the the Korean shipyard INP Heavy Industries Co Ltd and entered into a long-term contract with Shell Phillippines. Of the company’s vessels in the region for the time being 3 AHTS and 3 PSV are in Australia, 1 AHTS in Malaysia, 2 AHTS in Vietnam and 2 AHTS Philippines. Lady Audrey was fixed for 2 wells + 2x1 well options to Shell Namibia from early January 2002. The vessel had been working for Shell in the Philippines up till december when she mobilized for Namibia.

In November IOS has contracted two anchor handling support vessels at the Simek AS yard in Norway. Delivery of the vessels will take place in March and July 2003. The vessels are a new type of UT 712 of 12,240 bhp with DP and a double drum 370 tonne winch for employment in international markets.

PSV > 2000 DWT AHTS > 10000 BHP

Algosaibi

Seaworks

Rovde

Gulf

Tidewater

BOA

Workship

Swire

Maersk

Seacor

Farstad/IOS

Chinese

VESSELS IN THE REGIONSORTED BY OWNERS per January 02

AHTS > 10.000 BHP ANDPSV > 2.000 DWT IN THE REGION

Jan 1998

Jan. 1999

Dec. 2000

Jan. 2001

Jan. 2002

AHTS > 10.000 BHP PSV > 2.000 DWT

No. of vessels

No. of vessels

AHTS > 10.000 BHP AND PSV > 2.000 DWT

Jan 1998

Jan. 1999

Dec. 2000

Jan. 2001

Jan. 2002

No. of vessels

IN THE GULF OF MEXICO

Jan 1998

Jan. 1999

Dec. 2000

Jan. 2001

Jan. 2002

IN WEST-AFRICA Jan 1998

Jan. 1999

Dec. 2000

Jan. 2001

Jan. 2002

AHTS > 10.000 BHP PSV > 2.000 DWT

IN THE MEDITERRANEAN

Jan 1998

Jan. 1999

Dec. 2000

Jan. 2001

Jan. 2002

IN CANADA

No. of vessels No. of vessels

No. of vessels

OTHER MARKETS

RESULT PER SECTOR Far East/Australia 2001 2000

Freight income 151.229 134.127

Operation- and administration cost 84.922 78.151

Operation profit before depreciation (EDBIT) 66.922 55.976

Depreciation 30.475 29.123

Operating result vessels (EBIT) 35.832 26.853

EDBIT % 44,3% 41,7%

EBIT % 23,7% 29,0%

This is a short presentation of emerging markets that have an increasing need for large units. A positive development in these markets could play a role in the North Sea market conditions as well. There are large expectations to activities in West Africa in particular. Today, IOS has one vessel, Lady Audrey employed on a contract in Namibia. Demand for tonnage has also increased significantly in the Mediterranean. Currently, the Far Grimshader, a platform supply vessel, is transporting pipes in the Black Sea as part of a project to lay a 2 x 380 km. long pipeline, and the Far Sovereign has been employed for 3 months in the US Gulf.

Lady Audrey in Namibia - Photo: Karl Johan Bakken

28 29

The Company’s HSE-philosophy was formulated in this declaration in 1993:“The focus on Health and Safety for our employees, offshore and onshore, and the concern for the Environment is given the highest priority in the daily operation of our vessels. The operations are based on the company policy which was established in 1993 and is distributed to all employees:"Farstad Shipping has undertaken to offer and maintain a safe working environment. The Company expects that all individuals will contribute to enhance safety, regardless of their position, rank offshore or onshore. Every individual should have an understanding of responsibility towards themselves, their family, their colleagues and the company in all matters concerning health and safety.

Each individual's attitude and actions, as others see and observe them, will be setting standards, and this can serve the purpose to encourage others to perform their job in a way that can contribute to the achievement of an accident free, healthy and environmentally friendly work place.We have common responsibility for protecting and improving the environment, onshore and offshore, and accordingly, we should use all means to work towards reducing any risk of damaging the environment by waste, pollutants or unnecessary use of nonenvironmentally friendly substances.Farstad Shipping invites each employees suggestions towards promoting health, safety and environmental issues, and the Company will offer the necessary resources to reach the goals set forth in this policy."

HSE-PHILOSOPHY

DEVELOPMENT IN HSE AT FARSTAD SHIPPINGThe Company has, trough its focus on helth, safety and environment been among the leading actors in our business for many years. The Implementation of our efforts can be summarised like this: 1988: Farstad Shipping began to systematically record all unwanted events.1990: All vessels began to systematically record and report non-conformance incidents (NCR).1993: A comprehensive HSE policy was developed and the Company has since complied with this policy.1994: The Company was ISO 9002 certified.1997: The offices and two vessels were ISM D.O.C. approved (Document of Compliance).2000: The North Sea and the Australian fleet were ISM certified.2001: The Brazilian fleet was ISM certified, with the exception of three vessels.

Today, Farstad Shipping employs a complete quality assurance system that focuses on the operational procedures and programs for the development of all human resources. The quality assurance standards are maintained at the same elevated level for all operations throughout the Company. In order to maintain and continue to raise this standard, an active focus and participation is needed from all parts of the organization. The Company’s HSE philosophy is based upon international laws, regulations and standard practices.

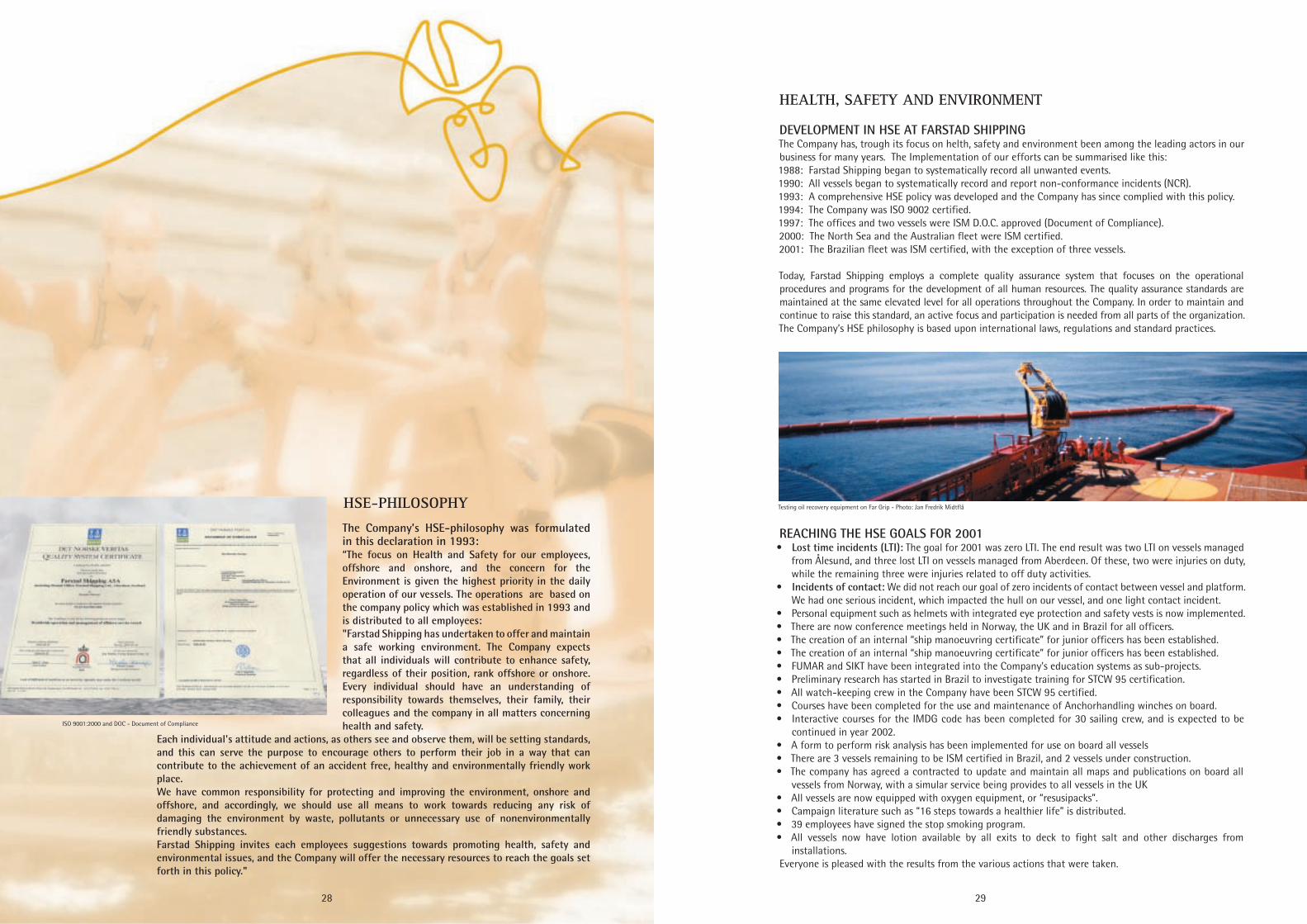

REACHING THE HSE GOALS FOR 2001• Lost time incidents (LTI): The goal for 2001 was zero LTI. The end result was two LTI on vessels managed from Ålesund, and three lost LTI on vessels managed from Aberdeen. Of these, two were injuries on duty, while the remaining three were injuries related to off duty activities.• Incidents of contact: We did not reach our goal of zero incidents of contact between vessel and platform. We had one serious incident, which impacted the hull on our vessel, and one light contact incident.• Personal equipment such as helmets with integrated eye protection and safety vests is now implemented.• There are now conference meetings held in Norway, the UK and in Brazil for all officers. • The creation of an internal “ship manoeuvring certificate” for junior officers has been established. • The creation of an internal “ship manoeuvring certificate” for junior officers has been established. • FUMAR and SIKT have been integrated into the Company’s education systems as sub-projects. • Preliminary research has started in Brazil to investigate training for STCW 95 certification. • All watch-keeping crew in the Company have been STCW 95 certified.• Courses have been completed for the use and maintenance of Anchorhandling winches on board. • Interactive courses for the IMDG code has been completed for 30 sailing crew, and is expected to be continued in year 2002. • A form to perform risk analysis has been implemented for use on board all vessels• There are 3 vessels remaining to be ISM certified in Brazil, and 2 vessels under construction. • The company has agreed a contracted to update and maintain all maps and publications on board all vessels from Norway, with a simular service being provides to all vessels in the UK• All vessels are now equipped with oxygen equipment, or “resusipacks”.• Campaign literature such as “16 steps towards a healthier life” is distributed. • 39 employees have signed the stop smoking program. • All vessels now have lotion available by all exits to deck to fight salt and other discharges from installations. Everyone is pleased with the results from the various actions that were taken.

HEALTH, SAFETY AND ENVIRONMENT

Testing oil recovery equipment on Far Grip - Photo: Jan Fredrik Midtflå

ISO 9001:2000 and DOC - Document of Compliance

30 31

88 89 90 91 92 93 94 95 96 97 98 99 00 01

15

12

9

6

3

0 90 91 92 93 94 95 96 97 98 99 00 01

1200

1000

800

600

400

200

0

UNWANTED EVENTS AND NON-CONFORMANCE REPORTS (NCR)For the fleet managed from Ålesund and Aberdeen there were 58 NCR in 2001 vs. 73 NCR in 2000. NCR reports deviances as a result of disruptions in operations and/or internal audits and inspections in accordance with the Company’s quality assurance system.

There were a total of 1054 unwanted events in 2001 compared to 1004 in 2000 (317 in 1999). The explosive increase from 1999 to 2000 is caused by incentives given to encourage correct reporting. A modest increase in 2001 should be considered an excellent result. Personal injuries gave an LTI number of 1.8 in 2001 compared to 2.4 in year 2000 and 1999 (see exhibit). The percentage of sick time for 660 sailing crew (Norway, UK and Brazil) was 1.85% in 2001, down from 2.82% in 2000.

ACTIONS TO IMPROVE HSEFarstad Shipping has taken initiative to and participate in several HSE related projects. Several of these projects has been possible due to the maritime environment in the North-western Norway. Based on our HSE policy, many activities have taken place to provide the development of new equipment to improve the working conditions and to strengthen the training of our crew.

For 2001 we will highlight the following actions:Installaton of garbage disposal units on all vessels in Norway.

Monitoring equipment for watch-keeping personnel.Should something happen to the watch-keeper; the system will sound after a pre-defined period of time. The alarm will sound on the bridge, in the Captains cabin, Mate’s cabin and recreational rooms. Integrated training infrastructure for Farstad Shipping.

The training program is developed in cooperation with the College of Engineering in Ålesund (HIA), Marintek, NTNU and Norsk Sjøoffisersforbund (Norwegian Association of Naval Officers). The goal is to increase the competency for personnel on offshore vessels by applying modern technology in a structured program.Utviklet rederistandard for utforming av bropult.

Emergency manoeuvring: Worked out simplyfied procedure by change-over from standard to emergency situation, and also integrating other functions.

Clean Ship, “Clean” is a Class Notation by DNV, founded on environmental motivated efforts related to pollution’s from ships towards the marine and the air environment. It define standards and requirements to the installed equipment and systems management related to handling of any waste produced onboard. The company have during 2001 built two vessels complying to the Class Notation, and further one vessel will be converted in 2002, in order to achieve the same standard. In addition founds made available for the coming year to implement some of the said requirements onboard sailing ships.

“Comfort Class” is a Class Notation by DNV, founded in order to improve the work environment onboard, all based upon approved standards for the indoor climate, noise and vibrations. Farstad have for several of the newbulidings delivered to the company in 2001, taken extensive investments to improve the standard and life quality onboard our vessels. In 2001 we built four vessels with flexible mounted main engines, where off two vessels installed with supersilent thrusters. One vessel was delivered in 2001 with the Class Notation

“Comfort” and further one more vessel will be converted in 2002 complying to the same standard.

In earlier years the following measures have been implemented to improve HSE:

1987: Two-step generator adopted to improve fuel efficiency.1992: Installed the first VAR-generator to improve fuel efficiency.1996: Took the initiative to develop a ship bridge simulator in Trondheim for supply vessels.1996: Improved existing VAR-generator with variable frequency.1996: Developed system for self-cleaning mud-tanks.1997: Development of integrated manoeuvring chair.1998: Development of remote controlled deck mani- pulator.1999: Contributed to development and installation of simulator for dynamic positioning at the College of Engineering in Ålesund.1999: Installed integrated manoeuvring chair as the co-pilot chair for training navigators on board.1999: Railmounted deck-crane on Far Santana.2000: Hands free loading/unloading in cooperation with Munchloaders.2000: Acoustic alarm to warn of movement of tow-pins and sharkjaws.

The intention behind actions taken by the Company every year during the last 10-15 years has been to improve safety as well as the working conditions on board, and on a broader scale, keep our vessels and personnel competitive in a market that continues to demand modern vessels manned by qualified people.

BEST SUPPLIER IN 2000In 2001, the Campos Basin Contract Department (E&P - BC/GETRAT) of Petrobras awarded Farstad Shipping the award for Best Service Supplier in 2000 in the large contracts category. This is the second time the Company received this award, after first winning it in 1999. The award was given to Farstad Shipping following a selection process, which included a careful evaluation in the areas of service performance, health, safety and environment.

The DP-simulator at HIAa, and the manoeuvring bridge on Far Scotia

RUE (number of reported unwanted events)

LTI - Tall (Lost Time Incidents)(number of incidents per million of hours worked)

3332

0

0 200 400 600 800 1000

0 200 400 600 800 1000

0 200 400 600 800 1000

0 20 40 60 80 100