Experience the Power of Fixed Index Annuities The “Yellow Pad” Presentation.

12

Experience the Power of Fixed Index Annuities The “Yellow Pad” Presentation

-

Upload

robyn-summersett -

Category

Documents

-

view

217 -

download

1

Transcript of Experience the Power of Fixed Index Annuities The “Yellow Pad” Presentation.

Experience the Power ofFixed Index Annuities

The “Yellow Pad” Presentation

Consider the advantages of a Fixed Index Annuity

Returns linked to an index Return of principal* Liquidity features Tax deferred growth Safety

* Subject to claims paying ability of issuing institution

The Strength of Tax Deferral

Earnings accumulate tax deferred No income taxes are due until

proceeds are taken outAND the Power of Triple Compounding Earn interest on your principal Earn interest on the interest Earn interest on the money you

would have paid in taxes

Help Protect Yourself

If you don’t have the recovery time that may be necessary, a Fixed Indexed Annuity may make sense for a portion of your money

If you lostthis much

It could take this long to rebuild yournest egg assuming these potential annual returns

at a 3% return at a 6% return at a 8% return

10% 3.6 years 1.8 years 1.3 years

20% 7.5 years 3.7 years 2.9 years

30% 12 years 6 years 4.6 years

40% 17 years 8.6 years 6.6 years

50% 23.2 years 11.6 years 9 years

With the safety and growthpotential of a Fixed Index Annuity

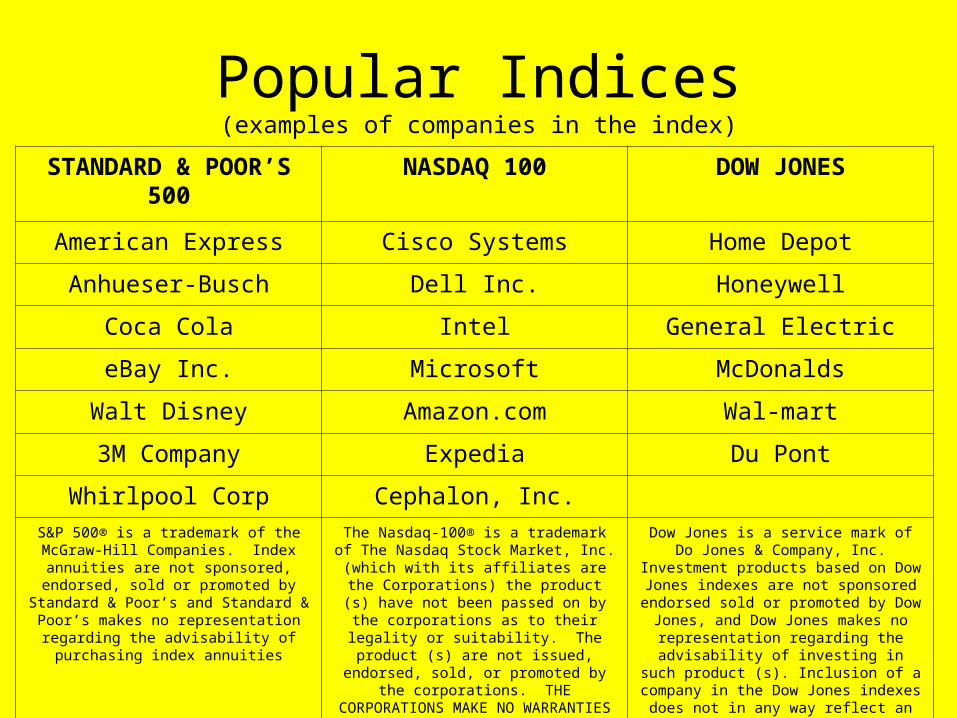

Popular Indices(examples of companies in the index)

STANDARD & POOR’S 500

NASDAQ 100 DOW JONES

American Express Cisco Systems Home Depot

Anhueser-Busch Dell Inc. Honeywell

Coca Cola Intel General Electric

eBay Inc. Microsoft McDonalds

Walt Disney Amazon.com Wal-mart

3M Company Expedia Du Pont

Whirlpool Corp Cephalon, Inc.S&P 500® is a trademark of the McGraw-Hill Companies. Index

annuities are not sponsored, endorsed, sold or promoted by

Standard & Poor’s and Standard & Poor’s makes no representation

regarding the advisability of purchasing index annuities

The Nasdaq-100® is a trademark of The Nasdaq Stock Market, Inc. (which with its affiliates are the Corporations) the product (s) have not been passed

on by the corporations as to their legality or suitability. The product (s)

are not issued, endorsed, sold, or promoted by the corporations. THE

CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE PRODUCT (S).

Dow Jones is a service mark of Do Jones & Company, Inc. Investment

products based on Dow Jones indexes are not sponsored endorsed sold or promoted by Dow Jones, and Dow

Jones makes no representation regarding the advisability of investing

in such product (s). Inclusion of a company in the Dow Jones indexes

does not in any way reflect an opinion of Dow Jones on the investment merits

of the company.

Measuring the Gain

Two common methods used

Annual Point-to-Point – Annual Reset

Monthly Point-to-Point – Annual Reset

Annual Point-to-PointExamples:

Beginning index value: 1000

Ending index value on contract anniversary: 1117

Percentage of change: +11.70%

Annual Cap: 4%

X Your Return is 4%X Your Return is 4%

Beginning index value: 1000

Ending index value on contract anniversary: 900

Percentage of change: -10%

Annual Cap: 4%X Your Return is 0%

Up Year Down Year

The annual cap varies depending upon the issuing insurance company.The 4% annual cap quoted is for illustrative purposes only.

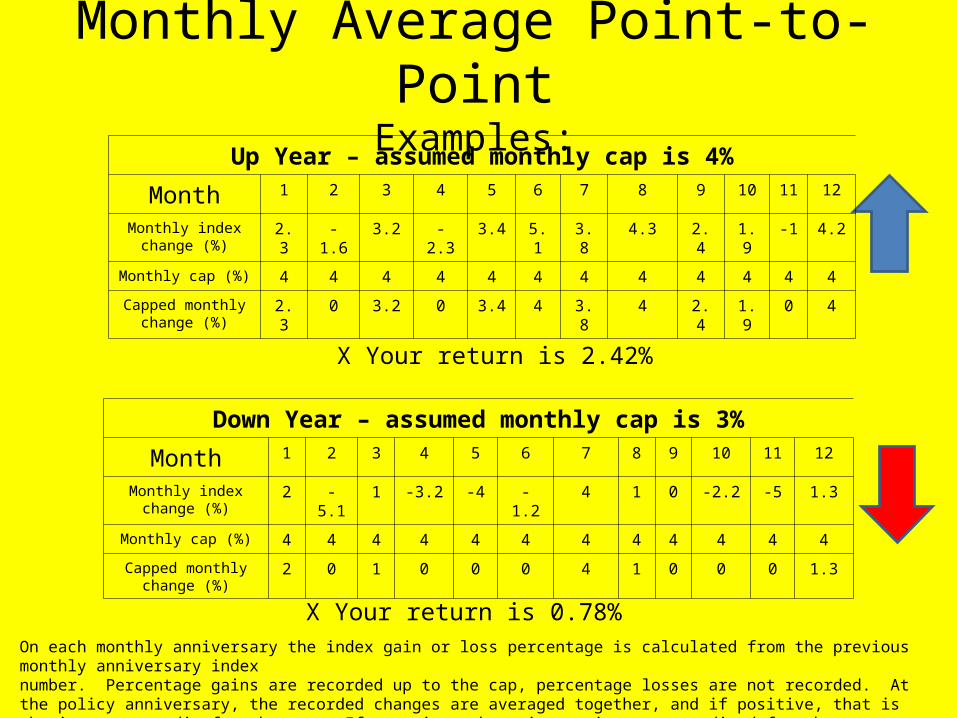

Monthly Average Point-to-PointExamples:

On each monthly anniversary the index gain or loss percentage is calculated from the previous monthly anniversary indexnumber. Percentage gains are recorded up to the cap, percentage losses are not recorded. At the policy anniversary, the recorded changes are averaged together, and if positive, that is the interest credit for the year. If negative, there is not interest credited for the year.

Up Year – assumed monthly cap is 4%

Month 1 2 3 4 5 6 7 8 9 10 11

12

Monthly index change (%)

2.3 -1.6 3.2 -2.3 3.4 5.1 3.8 4.3 2.4 1.9 -1 4.2

Monthly cap (%) 4 4 4 4 4 4 4 4 4 4 4 4

Capped monthly change (%)

2.3 0 3.2 0 3.4 4 3.8 4 2.4 1.9 0 4

Down Year – assumed monthly cap is 3%

Month 1 2 3 4 5 6 7 8 9 10 11 12

Monthly index change (%)

2 -5.1 1 -3.2 -4 -1.2 4 1 0 -2.2 -5 1.3

Monthly cap (%) 4 4 4 4 4 4 4 4 4 4 4 4

Capped monthly change (%)

2 0 1 0 0 0 4 1 0 0 0 1.3

X Your return is 2.42%

X Your return is 0.78%

Monthly Sum Point-to-PointExamples:

On each monthly anniversary the index gain or loss percentage is calculated from the previous monthly anniversary indexnumber. Percentage gains are recorded up to the cap, percentage losses are recorded with no cap. At the policy anniversary, the recorded changes are added together, and if positive, that is the interest credit for the year. If negative, there is not interest credited for the year.

Up Year – assumed monthly cap is 2.5%

Month 1 2 3 4 5 6 7 8 9 10 11

12

Monthly index change (%)

2.3 1.6 -3.2 -2.3 0.4 2.1 3.8 -3.3 2.4 1.9 -1 4.2

Monthly cap (%) 3 3 3 3 3 3 3 3 3 3 3 3

Capped monthly change (%)

2.3 1.6 -3.2 -2.3 0.4 2.1 3 -3.3 2.4 1.9 -1 3

Down Year – assumed monthly cap is 3%

Month 1 2 3 4 5 6 7 8 9 10 11 12

Monthly index change (%)

2 -5.1 1 -3.2 -4 -1.2 4 1 0 -2.2 -5 1.3

Monthly cap (%) 3 3 3 3 3 3 3 3 3 3 3 3

Capped monthly change (%)

2 -5.1 1 -3.2 -4 -1.2 3 1 0 -2.2 -5 1.3

X Your return is 8.5%

X Your return is 0%

The Power of Annual ResetYou may reduce your risk during the down years!

$100,000 PAYMENT

MarketFluctuatio

n

S&P 500Index Fund

Fixed IndexAnnuity

VALUE $100,000 $100,000

Year 1 26.7% $126,700 $108,000

Year 2 19.5% $151,407 $116,640

Year 3 -12.7 $132,178 $116,640

Year 4 -10.5% $118,300 $116,640

Year 5 -23.4% $90,618 $116,640

Year 6 26.4% $114,451 $125,971

Year 7 9.0% $124,850 $136,049

Year 8 4.7% $130,718 $142,443

Year 9 11.6% $145,881 $153,839100% Participation Rate 8% Cap No Fee

Participation rate is defined ashow much of the increase in the index will be used to calculate the index-linked interest.

Annual Reset is defined as the index-linked interest, if any, is determined each year by comparing the index value at the end of the contract with the index value at the start of the contract year. Interest is added to your annuity each year during the term.

The annual cap varies depending upon the issuing insurance company.The 8% annual cap quoted is for illustrative purposes only.

Annual Point-to-Point -Annual Reset

The Power of Annual ResetYou may reduce your risk during the down years!

$100,000 PAYMENT

MarketFluctuatio

n

S&P 500Index Fund

Fixed IndexAnnuity

VALUE $100,000 $100,000

Year 1 26.7% $126,700 $109,184

Year 2 19.5% $151,407 $117,141

Year 3 -12.7 $132,178 $117,141

Year 4 -10.5% $118,300 $117,141

Year 5 -23.4% $90,618 $117,141

Year 6 26.4% $114,451 $134,059

Year 7 9.0% $124,850 $143,005

Year 8 4.7% $130,718 $143,005

Year 9 11.6% $145,881 $159,312100% Participation Rate 2.45% Monthly Cap No Fee

Participation rate is defined ashow much of the increase in the index will be used to calculate the index-linked interest.

Annual Reset is defined as the index-linked interest, if any, is determined each year by comparing the index value at the end of the contract with the index value at the start of the contract year. Interest is added to your annuity each year during the term.

The monthly cap varies depending upon the issuing insurance company.The 2.45% monthly cap quoted is for illustrative purposes only.

Monthly Point-to-Point -Annual Reset

The Safety of Fixed Indexed Annuities

All fixed annuities are backed by the claims paying ability of the insurance company offering them. The insurance companies are subject to strict guidelines established by the National Association of Insurance Commissioners and must strive to conservatively invest the premium funds to provide a minimum return.

Additionally individual states may require insurance companies doing business in their state to contribute to the Life and Health Guarantee Association, which may help should an insurance company fail to meet the obligations of their contract holders, up to the guidelines published by the state.