Exercise 1witor.biz/yahoo_site_admin/assets/docs/ACF_Exercise_Solutions... · Discuss the merits of...

18

Exercise 1 Question 1 Calculate the following values assuming a discount rate of 9%. (a) The future value of £700 invested for 5 years assuming a discount rate of 9%. (b) The present value of £700 received in 5 years’ time assuming a discount rate of 9%. (c) Assume the discount rate falls to 5%. Recalculate your answer to part (b). What do you notice about the relationship between the fall in discount rate and the change in the value of the income stream? (d) The present value of receiving £500 in 1, 2 & 3 years’ time; and £700 in 4 and 5 years’ time, assuming a discount rate of 9% (e) For a constant income stream show that the present value can be written (f) Using equation (1), or otherwise, calculate the present value of receiving £800 every year for 10 years (g) By considering what happens to equations (1) when n gets very large calculate the present value of receiving £800 every year forever

Transcript of Exercise 1witor.biz/yahoo_site_admin/assets/docs/ACF_Exercise_Solutions... · Discuss the merits of...

Exercise 1

Question 1

Calculate the following values assuming a discount rate of 9%.

(a) The future value of £700 invested for 5 years assuming a discount rate of 9%.

(b) The present value of £700 received in 5 years’ time assuming a discount rate of 9%.

(c) Assume the discount rate falls to 5%. Recalculate your answer to part (b). What do you notice

about the relationship between the fall in discount rate and the change in the value of the income

stream?

(d) The present value of receiving £500 in 1, 2 & 3 years’ time; and £700 in 4 and 5 years’ time,

assuming a discount rate of 9%

(e) For a constant income stream show that the present value can be written

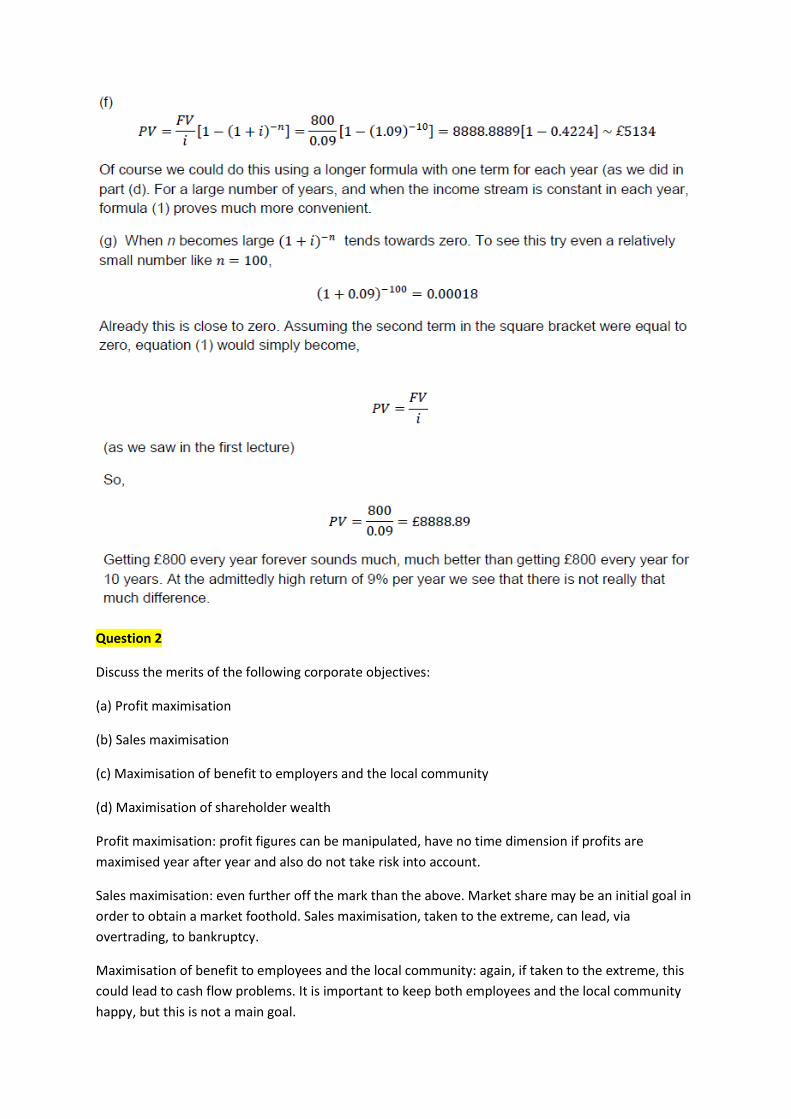

(f) Using equation (1), or otherwise, calculate the present value of receiving £800 every year for 10

years

(g) By considering what happens to equations (1) when n gets very large calculate the present value

of receiving £800 every year forever

Question 2

Discuss the merits of the following corporate objectives:

(a) Profit maximisation

(b) Sales maximisation

(c) Maximisation of benefit to employers and the local community

(d) Maximisation of shareholder wealth

Profit maximisation: profit figures can be manipulated, have no time dimension if profits are

maximised year after year and also do not take risk into account.

Sales maximisation: even further off the mark than the above. Market share may be an initial goal in

order to obtain a market foothold. Sales maximisation, taken to the extreme, can lead, via

overtrading, to bankruptcy.

Maximisation of benefit to employees and the local community: again, if taken to the extreme, this

could lead to cash flow problems. It is important to keep both employees and the local community

happy, but this is not a main goal.

Maximise shareholder wealth: the correct goal, since as owners their wealth should be maximised

Question 3

What is the ‘agency problem’ that (large) companies potentially face?

The agency problem arises because of a divorce of ownership and control. Within a public limited

company (plc), there are a number of examples of the agency problem, the most important being

that existing between shareholders (principal) and managers (agent). The problem exists because of

divergent goals and an asymmetry of information.

Managers act to maximise their own wealth rather than the shareholders' wealth. There are various

ways to reduce the agency problem: do nothing, if the costs of divergent behaviour are low; monitor

agents, if contracting or divergent behaviour costs are high; use a reward/punishment contract, if

monitoring costs and divergent behaviour costs are high. As regards the shareholders/managers

agency problem, monitoring costs and divergent

behaviour costs are high so shareholders use contracts to reward managers for good performance

and could give managers shares in the company they manage, making them shareholders

themselves

Question 4

Show by a simple graph-theoretic procedure how linear interpolation can be used to determine the

internal rate of return of a project.

See lecture notes. The basic idea is that if we can identify a discount rate r1 which results in positive

NPV, and r2 which results in negative NPV, then IRR – which results in zero NPV – must lie between

( r1 , r2 ) . The procedure requires an assumption that NPV strictly decreases with r.

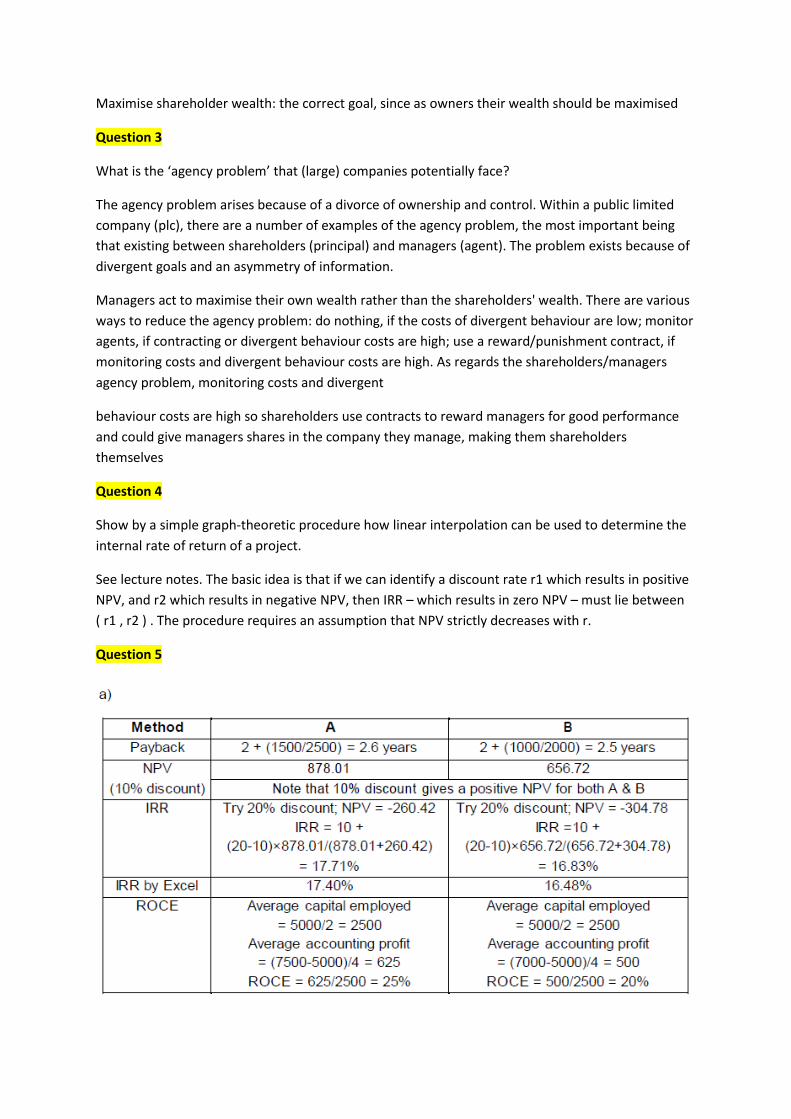

Question 5

Question 6

The expected cash flows are given below

a)

Using Excel the IRR for the project is found to be 17%.

b)

Here, we will focus on the method which is calculating the amounts by which each project variable

would have to change in order to make NPV become zero.

First of all, we can show the status quo (using Excel),

NPV = £377,034.99 - £350,000 = £27,035

Trying some educated guesses in Excel (it is quite obvious that the project needs to run for most of

the 10 yr period) it is easily seen that the project needs to run for between 8 and 9 years for the NPV

to enter positive territory.

This is a decrease of between 1-2 years, i.e. up to 20% in relative terms compared with the original

project life. We therefore conclude that if there is a reduction of approaching 20% in project life, this

project will no longer be attractive. If we were being cautious we might even base a decision to

proceed with the project on the likelihood that project life were even to fall by one year.

c)

Start by investigating the fall in NPV if the sales price were to drop by £1. [Cash flow in periods 1-10

drops to (7.5-3.5 )*20 000-24 875=55 125 .]

(Using Excel) for a £1 drop in sales price the PV the cash flow of £55,125 in each of the 10 periods is

found to be £276,659.62. Comparing cash flows a £1 drop in sales price would lead to a fall in NPV

of:

377 034.99 – 276 659.62 = 100 375.37

Consequently, for a reduction of £27,035 (such that the original NPV becomes zero), the price must

drop by 27,035/100,375 = £0.2693.

Check in Excel: (8.2307-3.5 )* 20 000-24 875=69 739 . Using this in the NPV calculation gives an NPV

of £3.91, which is close to zero.

[You may have approximated the price drop to simply 27 pence. Just how sensitive this project is to

price is demonstrated by the difference even this small rounding makes to the potential profitability

of the project.]

Hence, a reduction of 0.27/8.50 = 3.18% or more in sales price would make this project unattractive.

Therefore, the sensitivity of this project with respect to sales price is high, and definitely higher than

that of the project’s life.

Exercise 2

Question 1

A company is financed by bonds and ordinary shares.

The 12% bonds are redeemable in 5 years’ time at par. Annual interest has just been paid. The

current ex-interest market price of the bond is £114. Corporation tax is 28%.

The ex-dividend ordinary share price is £3.14 and the most recent dividend was 35 pence per share.

Both dividend and share price are expected to increase by 7% per year for the foreseeable future.

The company has 5,000 redeemable bonds (par value £100) and 225,000 ordinary shares (par value

£1).

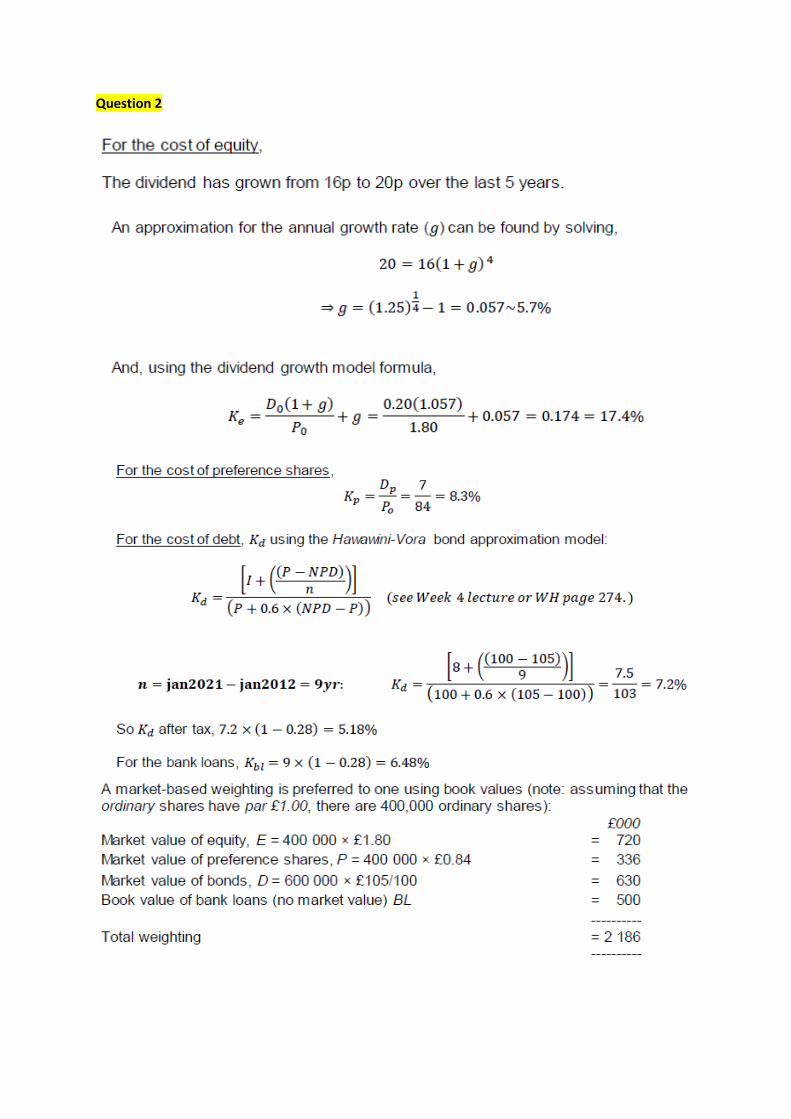

(a) Calculate the cost of debt. [Hint: remember the ‘tax-shield’.]

For the cost of debt, Kd using the Hawawini-Vora bond approximation model:

Question 2

Question 3

Explain the term diversification in finance, and give a few examples.

Diversification means spreading a portfolio over many investments to avoid excessive exposure to a

few sources of risk (Levy & Post, 2005, Investments).

Investing in stocks from different industries is one way to diversify your portfolio. Studies have

shown that maintaining a well-diversified portfolio of 25 to 30 stocks will yield the most cost-

effective level of risk reduction. Further diversification benefits can be gained by investing in foreign

securities. Buying shares in a mutual fund can also provide investors with an inexpensive source of

diversification

Question 4

Asset Y shows relatively high variation. While a return of 30% is most likely, there is also a significant

chance that the return is going to be either lower or higher by 20 percentage points. Asset X, on the

other hand, has possible returns which are clustered around 25%. Consequently, we may say that Y

is riskier than X.

b)

E[X] = 25%

E[Y] = 30%

c)

V[X] = 15

V[Y] = 160

S.D.[X] = 3.87%

S.D.[Y] =12.65%

The expected risk for X and Y are thus 3.87% and 12.65% respectively.

Question 5

Question 6

Question 7

Question 8

Question 9

Question 10

Question 11

Exercise 3

Question 1

Question 2

Question 3

Question 4

Question 5

Question 6

Question 7

Question 8

Question 9

a. Cost of Equity = 6.50% + 1.47 (5.5%) = 14.59%

Cost of Capital = 14.59% (24.27/(24.27+ 2.8)) + 6.8% (1-0.4) (2.8/(24.27+2.8)) = 13.50%

b. If Pfizer moves to a 30% debt ratio, New debt/equity ratio = 30/70 = 42.86%

Unlevered Beta = 1.47/(1+0.6*(2.8/24.27)) = 1.37

Unlevered Beta= beta1/(1+(1-Tc)(D1/E1))

New Beta = 1.37 (1+0.6*0.4286) = 1.72

New Beta = unleveler beta * (1+ (1-Tc)(D2/E2)

New Cost of Equity = 6.5% + 1.72 (5.5%) = 15.96%

New Cost of Capital = 15.96% (0.7) + 8.5% (1-.4) (0.3) = 12.70% c. If the savings grow at 6% a year in perpetuity, the change in firm value can be computed as follows – Savings each year = (.1350-.1270) (24.27 + 2.8) = 0.21656 ! $ 216.56 million PV of Savings with 6% growth = (216.56*1.06)/(.127-.06) = $3,426 ! $ 3.4 billion Increase in Stock Price = 3426/24270 = 14.12% ! Stock Price will increas by 14.12% d. The need for R& D increases the need for flexibility; therefore, Pfizer may not go to this higher optimal debt ratio, the cost of capital notwithstanding.

Question 10

(a) Current Cost of Equity = 8% + 1.06 (5.5%) = 13.83% Current Cost of Debt = 10% (1-0.4) = 6.00% Current Cost of Capital = 13.83% (250/275) + 6.00% (25/275) = 13.12% (b) If the firm borrows $ 100 million and buys back $ 100 million of stock New Debt/Equity Ratio = 125/150 = 0.833333333 Unlevered Beta = 1.06/(1+0.6*.10) = 1.00 New Beta = 1 (1 + 0.6*0.8333) = 1.50 Cost of Equity = 8% + 1.50 (5.5%) = 16.25% Cost of Capital = 16.25% (150/275) + 13% (1-.4) (125/275) = 12.41%

Question 11

See lecture notes

Exercise 4

Question 1

a. P = DIV (r-g) 20= 0.8/(r-0.06) 20r-1.2=0.8 20r=2 r=10

Value after merger =0.8/(0.1-0.08)=40

b. 25* 600 000= 15 000 000

c. (600 000/3)*90=18 000 000

d. Would not change

Question 2

a. 2.67; 34.3286 ;262172; 700 000 ; 9 000 000

b. 162172/200000=0.8109

Question 3

a. False

b. False

c. True

d. False

e. It depends.