Excellence in the New Era for Construction

30

Excellence in the new era Don Ward Chief Executive constructingexc

-

Upload

clarkson-alliance -

Category

Real Estate

-

view

93 -

download

4

Transcript of Excellence in the New Era for Construction

Excellence in the new era

Don Ward

Chief Executive

constructingexc

“Constructing Excellence”

A national, regional and local (and international)

platform for industry improvement

to deliver better value

for clients, industry and users

through collaborative working

“A BETTER INDUSTRY TOGETHER”

The CE ‘movement’80 national members, 9 regional Centres35 best practice Clubs, 480 G4C members+ 7 partners in the CE International Alliance

National membersClients at the heart Clients

Acivico (Birmingham CC)

BAE Systems

Battersea Park

Crossrail

East Riding of Yorks BC

EDF Energy (NNB GenCo)

Environment Agency

Fusion 21

Heathrow Airport

Highways Agency

Igloo Regeneration

Imperial University

Kent CC

Lambeth Living

Land Securities

London Underground

Magnox

Northumbrian Water

Nu-Gen

ProCure 21

Rochdale Boroughwide

Royal Mail Group

Sandwell MBC

Consultants

Aecom

Arup

Burges Salmon

Capita

CH2M Hill

Coaction Management

CWC

DBD

FaulknerBrowns

Invennt

LCMB

Lucas Fettes

Pick Everard

Pinsent Masons

Project5

Pw2.0.com

Rider Levett Bucknall

Ryder Architecture

SmartBIM Solutions

Synaps

Temple

Thurlow Associates

Trowers & Hamlin

Turner & Townsend

Visonality

Waterman

Wragge Lawrence Graham

SCAPE

Westfield Group

Worthing Homes

Yorkshire Water

Contractors

Ashleigh (Scotland)

Balfour Beatty

Bowmer & Kirkland

Cara

Costain

Dawnus

Higgins

Interserve

ITC Concepts

Keltbray

Kier Group

Lend Lease

London & London

Mace

McGee

Morrison Galliford Try

Skanska Integrated Projects

Willmott Dixon

Manufacturers & Suppliers

4Projects

Astins

Coubari

FSI Europe

Graphisoft

Knauf Drywall

Management Process Systems

Polypipe Terrain

Tekla

UK Timber Frame Association

Waterloo Air Products

Associates

BRE

British Property Federation

Chartered Institute of Building

CL:AIRE

Glenigan

UK Green Building Council

University of Reading

UK construction improvementcan be charted by a number of key reports

1994.......1998.................2006…....2010…..2013…

Latham…….Egan………………Olympics….’Crisis’…..…’2025’…

1980s...................................................2012+

... and a number of mega-projects

£5.8 bn

£4.3 bn

£9.3 bn

Client satisfaction with the service(and the product) they receive is up

63% 63% 65%71% 74% 77% 79%

75% 77%84% 82% 80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

% 8

/10

or b

ette

r

Client Satisfaction - Service

The industry has improved its safety

13541271 1318

12171097

1172

1023901 946

865 906971 967

0

200

400

600

800

1000

1200

1400

1600

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Safety - Industry Accident Incident Rate (AIR)

Construction output in Great Britain

£0

£5,000

£10,000

£15,000

£20,000

£25,000

£30,000

£35,000

1980 1985 1990 1995 2000 2005 2010

Value of construction output in Great Britain (£M)Current prices, non seasonally adjusted - by sector

BIS May 2014

new repair & maintenance

80

90

100

110

120

1997 1999 2001 2003 2005 2007 2009 2011 2013

Construction output GB(2010 prices index, seasonally adjusted)

Construction output (index linked)

“Six regions hit new house price peak…”BBC News website 16 Sept 2014

‘Economic climate change’meant companies faced a stark choice

Collaborative Working Champions ‘Survival Guide’ , 2009

Never waste a good crisis, 2009

Four ‘blockers’ have slowed the pace of change

Business and economic models

Capability

Delivery model

Industry structure

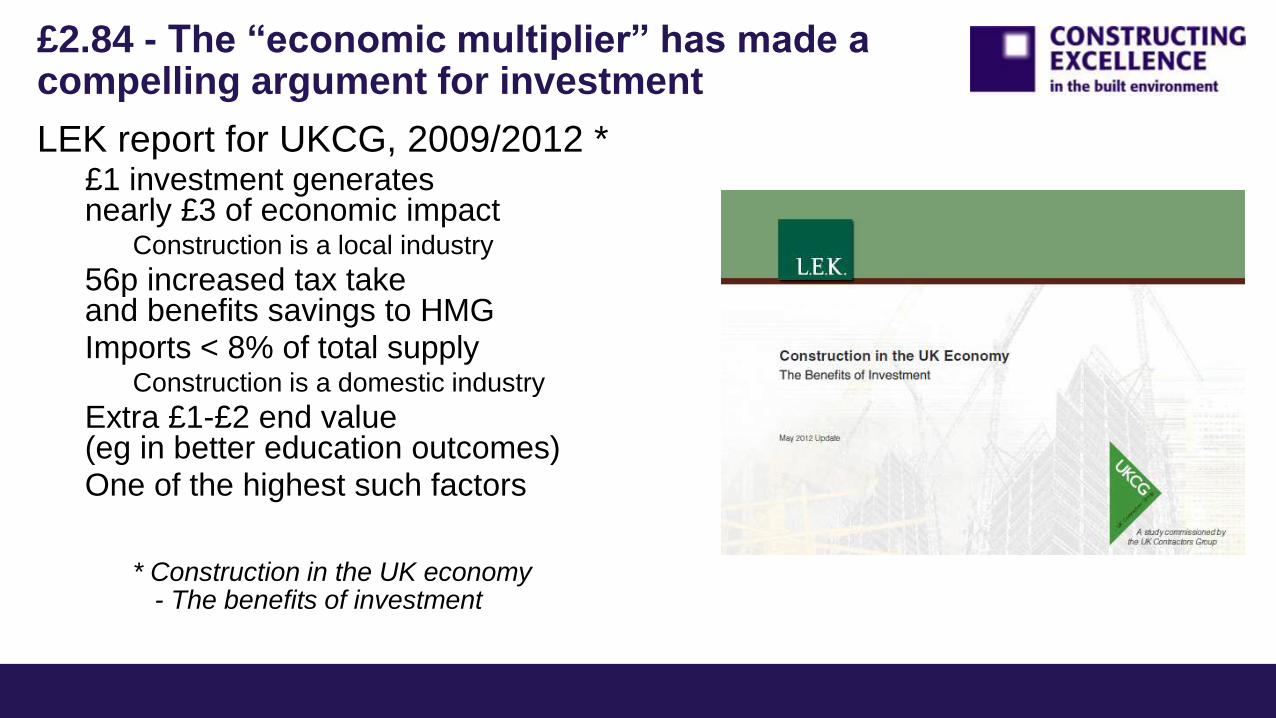

£2.84 - The “economic multiplier” has made a compelling argument for investment

LEK report for UKCG, 2009/2012 *£1 investment generates nearly £3 of economic impact

Construction is a local industry

56p increased tax take and benefits savings to HMGImports < 8% of total supply

Construction is a domestic industry

Extra £1-£2 end value (eg in better education outcomes)One of the highest such factors

* Construction in the UK economy - The benefits of investment

Plan for Growth (HM Treasury)

Government Construction Strategy (Cabinet Office)

Infrastructure Cost Review (IUK)

Industrial Strategy “Construction 2025” (BIS)

Government policies are aligned

Construction 2025, BIS, 2013

People

Smart

Sustainable

Growth

Leadership

A burning platform for transforming performance

A fit-for-purpose,

streamlined industry

by 2025

Collaborative platform:

coordinated, not fragmented

integrated, not siloed

investing, innovative

enhanced capability

rewarded for the value created

Intelligent industry

Informed intelligent client

Thinks international, long-term, programmes not projects

Demands detailed data about assets and performance

Tests new procurement methods

Builds alliances and an integrated supply chain

Incentivises teams to deliver more efficiently, predictably

Produces outcomes not outputs

Shares the rewards

The value adder

Rewarded for the value created

Collaborative

Innovative

Solution focused

Integrated capability

Strategic business relationship

High levels of investment

Data rich

Lean

The transactional

Commoditised service

Transacted engagement

Lower margins

Clearly defined role

Bought in competition

Informed clients and intelligent industry

Adding value and delivering Construction 2025

People

Smart

Sustainable

Growth

Leadership

CE Vision 2025

Construction Clients’ Group

Regional & National Awards series

Centre for Infrastructure

Development (Manchester

Business School)

G4C

CELL qualifications and training

CCG Health & Safety theme group

CEHE network

BRE Academy

Collaborative Working Champions

BIM theme group

G4C big data theme

Procurement trials for Cabinet Office

Procurement for value

Asset management theme group

CEHE

Sustainability theme group

Funding & Finance theme group

Social value – CE Clubs & Regions

CE International – 8 Alliance partners

Nuclear theme group

SMEs

• CE Regional Network

• local CE Best Practice Clubs

Environmental excellence

End user delight

Client/customer

satisfaction

Sustainable profitability

Attractive industry,

positive profile

Overarching improvement themes 2014+

Sustainability

Housing

Nuclear

BIM

Funding& Finance

Asset management

Generation4 Change

National theme groups

PLUS

Universities (#CEHE)

Procurement

Big data

Collaborative

Working

Champions

Clientshealth &safety

Construction

Clients’

Group

Three overriding principlesof collaborative working

Common vision

and leadership

Processes

and tools

Culture and

behaviours

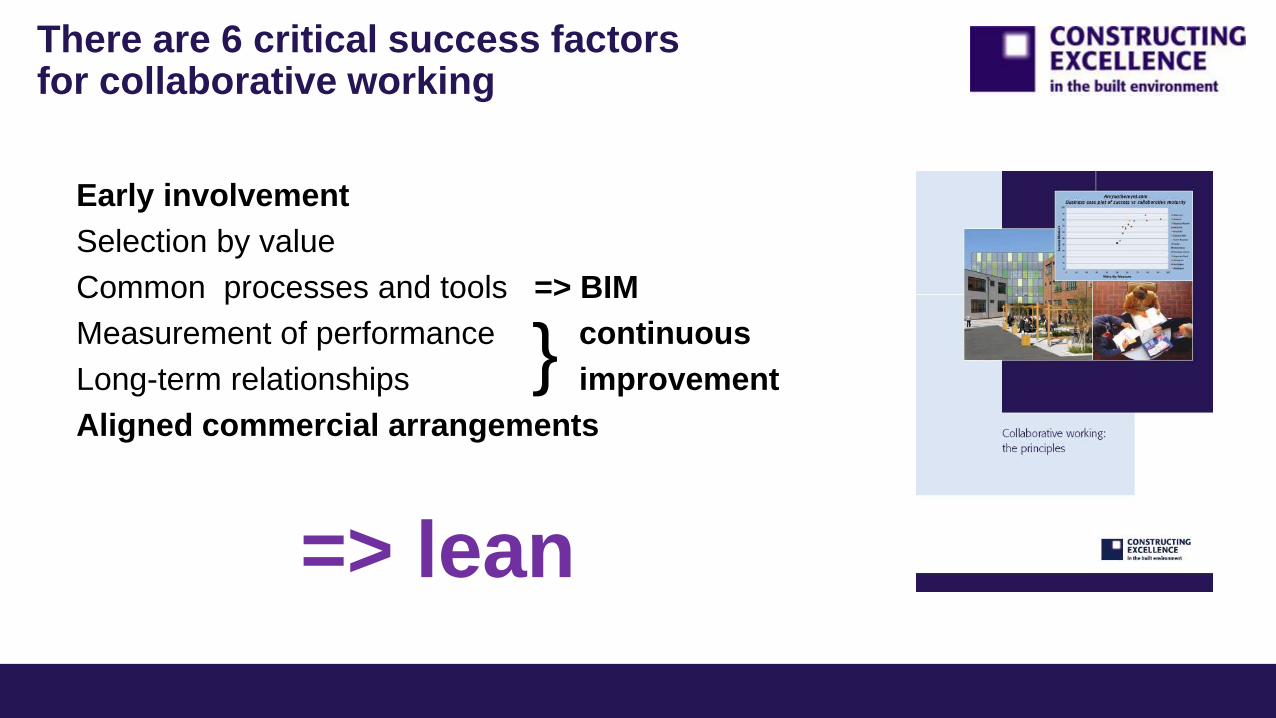

There are 6 critical success factors for collaborative working

Early involvement

Selection by value

Common processes and tools => BIM

Measurement of performance continuous

Long-term relationships improvement

Aligned commercial arrangements

=> lean

}

Above all, customers want value and we need to understand how clients and users measure it (£, happy residents, CO2, time, social value etc)

Value =

Benefit

___________

Cost

WHOLE

LIFE

Pressures on clients – what can you offer?

Value for money } “more

Economic recession } for

Legislation and regulation } less”

Safety – and health & welfare

Capital costs (capex) vs operation (opex)

Funding and finance

Environmental sustainability – “future proof”

Local employment in the supply chain (SMEs and social value)

Delivering in ‘live’ environments

Pressure to open on time

Growth

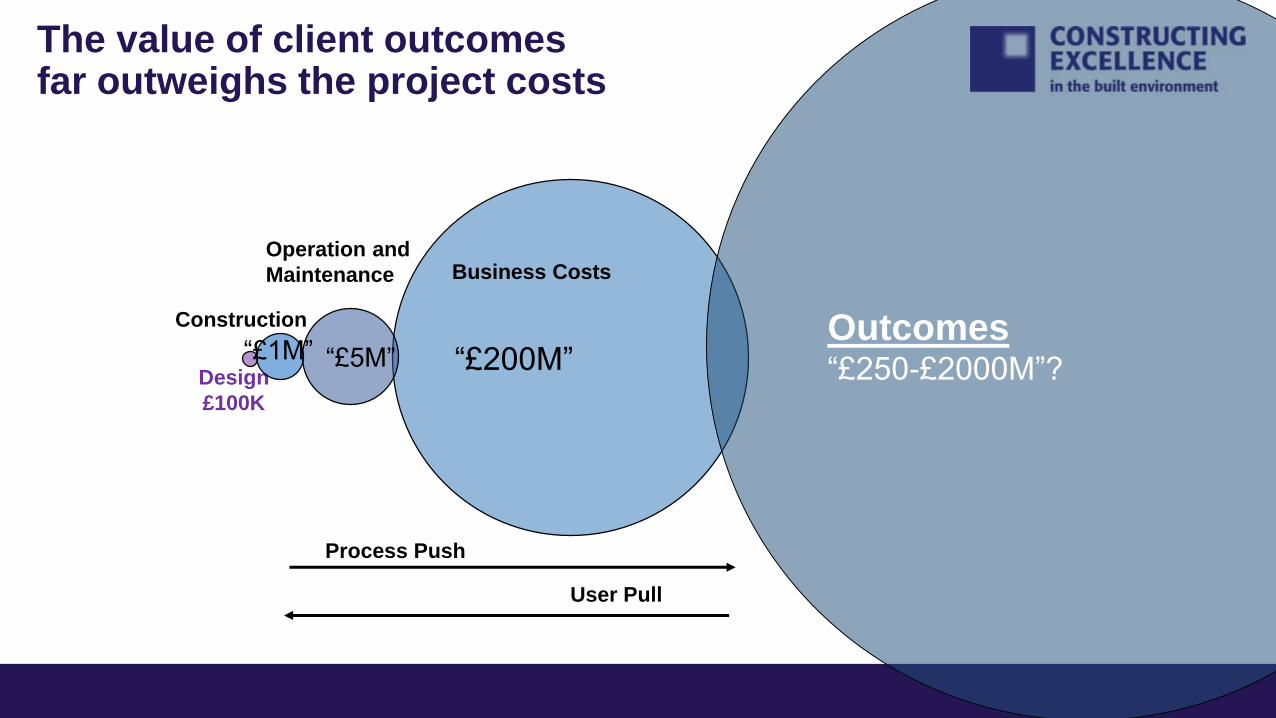

Design

£100K

Construction

The value of client outcomes far outweighs the project costs

“£200M”

Business Costs

“£5M”

Operation and

Maintenance

Process Push

User Pull

Outcomes“£250-£2000M”?

“£1M”

Design

Construction

The value of client outcomes far outweighs the project costs

Business Costs

Operation and

Maintenance

Process Push

User Pull

Outcomes

“Better together”

Better ideas and inspiration

Better evidence and intelligence

Better conversations and connections

Better influence and leadership

www.constructingexcellence.org.uk

For further informationwww.constructingexcellence.org.uk

or contact [email protected]

constructingexc