Ewald Engelen et al. - Misrule of experts? The financial crisis as elite debacle

23

Misrule of experts? The financial crisis as elite debacle Ewald Engelen, Ismail Ertu ¨rk, Julie Froud, Sukhdev Johal, Adam Leaver, Michael Moran and Karel Williams Abstract This paper is about knowledge limits and the financial crisis. It begins by examining various existing accounts of crisis which disagree about the causes, but share the belief that the crisis represents a problem of socio-technical malfunction which requires some kind of technocratic fix: the three variants on this explanation are the crisis as accident, conspiracy or calculative failure. This paper proposes an alternative explanation which frames the crisis differently as an elite political debacle. Political and technocratic elites were hubristically detached from the process of financial innovation as it took the form of ‘bricolage’, which put finance beyond technical control or management. The paper raises fundamental questions about the politicized role of technocrats after the 1980s and emphasizes the need to bring private finance and its public regulators under democratic political control whose technical precondition is a dramatic simplification of finance. Keywords: knowledge; experts; elites; financial crisis; financialization; bricolage. The financial crisis that began in August 2007 bankrupted the idea that self- regulation and a ‘light touch’ regulatory regime could check risky behaviour and prevent systemic crisis in financial markets. The period since August 2007 has been one of critical reflection by policy-makers and academics over what went wrong and what might be done to prevent future crisis. Here, marked differences have emerged. Some read the crisis as a structural phenomenon Adam Leaver, 6.04 Harold Hankins, Manchester Business School, University of Manchester, Booth St West, Manchester, M15 6PB, UK. E-mail: [email protected] Copyright # 2012 Taylor & Francis ISSN 0308-5147 print/1469-5766 online http://dx.doi.org/10.1080/03085147.2012.661634 Economy and Society Volume 41 Number 3 August 2012: 360 382 Downloaded by [Erasmus University] at 09:03 12 April 2013

-

Upload

che-brandes-tuka -

Category

Documents

-

view

52 -

download

0

description

This paper is about knowledge limits and the financial crisis. It begins by examining various existing accounts of crisis which disagree about the causes, but share the belief that the crisis represents a problem of socio-technical malfunction which requires some kind of technocratic fix: the three variants on this explanation are the crisis as accident, conspiracy or calculative failure. This paper proposes an alternative explanation which frames the crisis differently as an elite political debacle. Political and technocratic elites were hubristically detached from the process of financial innovation as it took the form of ‘bricolage’, which put finance beyond technical control or management. The paper raises fundamental questions about the politicized role of technocrats after the 1980s and emphasizes the need to bring private finance and its public regulators under democratic political control whose technical precondition is a dramatic simplification of finance.

Transcript of Ewald Engelen et al. - Misrule of experts? The financial crisis as elite debacle

Misrule of experts Thefinancial crisis as elitedebacle

Ewald Engelen Ismail Erturk Julie FroudSukhdev Johal Adam Leaver Michael Moranand Karel Williams

Abstract

This paper is about knowledge limits and the financial crisis It begins by examiningvarious existing accounts of crisis which disagree about the causes but share thebelief that the crisis represents a problem of socio-technical malfunction whichrequires some kind of technocratic fix the three variants on this explanation are thecrisis as accident conspiracy or calculative failure This paper proposes analternative explanation which frames the crisis differently as an elite politicaldebacle Political and technocratic elites were hubristically detached from theprocess of financial innovation as it took the form of lsquobricolagersquo which put financebeyond technical control or management The paper raises fundamental questionsabout the politicized role of technocrats after the 1980s and emphasizes the need tobring private finance and its public regulators under democratic political controlwhose technical precondition is a dramatic simplification of finance

Keywords knowledge experts elites financial crisis financialization bricolage

The financial crisis that began in August 2007 bankrupted the idea that self-

regulation and a lsquolight touchrsquo regulatory regime could check risky behaviour

and prevent systemic crisis in financial markets The period since August 2007

has been one of critical reflection by policy-makers and academics over what

went wrong and what might be done to prevent future crisis Here marked

differences have emerged Some read the crisis as a structural phenomenon

Adam Leaver 604 Harold Hankins Manchester Business School University of

Manchester Booth St West Manchester M15 6PB UK E-mail adamleavermbsacuk

Copyright 2012 Taylor amp Francis

ISSN 0308-5147 print1469-5766 online

httpdxdoiorg101080030851472012661634

Economy and Society Volume 41 Number 3 August 2012 360382

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

with little blame attached to individuals and greater emphasis on the

unanticipated and accidental consequences of system complexity For others

the crisis was caused by the avarice of bankers and other actors who apparently

knew what they were doing and were aided and abetted by self-interested

regulators and politicians A third set of authors emphasize institutionally and

or culturally produced calculative failures where un-knowing but active

subjects created runaway risks that they neither understood nor controlled In

many cases the analysis of crisis centres on socio-technical failures which

would be solved by new restorative interventions supervised and administered

by technocratic experts

This paper deals with two problems that emerge from this narrow framing

of the crisis as a serious but momentary malfunction in financial markets

where that malfunctioning part or feature can be fixed and thus stability

restored with new and inventive technical tools First it seeks to make the case

that the quest to restore control to financial markets is quixotic because

innovation takes the form of bricolage with instability written into its DNA

For this reason transformative rather than restorative reform is required

where the fundamental principle of action must be to downsize and simplify

finance Allied to this is a second point that the crisis was not just the result of

technical failure in financial markets but also the outcome of a political and

regulatory debacle where the hubristic detachment of elites created the space

for finance to grow and become more complex This paper therefore explores

the cultural and institutional dimensions of this elite hubris and is designed to

sound a note of caution to those who blithely recommend new tools with which

to fix finance and neglect the lsquoordinary politicsrsquo of UK financial regulation and

oversight Our contention is that if technical reforms of financial markets are to

work they must first be transformative and second be coupled to greater

democratic control and accountability at regulatory and political levels

Our paper develops this argument in four sections The first reviews current

explanations of crisis where differences are classified according to whether the

causes are located in structure or agency or in neither as part of a kind of third

way explanation In this section we argue that these explanations of the crisis

(as accident conspiracy or calculative failure) share common assumptions

about how crisis is generated within socio-technical systems amenable to

technical and mainly technocratic fixes The second section explains the

process of financial innovation as bricolage where restorative reform became an

input to strategic calculation rather than a powerful external constraint The

third section describes how bricolage produced a fragile latticework of

connections that evade technical control across four dimensions volume

complexity opacity and interconnectedness thus making the activity in-

herently ungovernable The fourth section then outlines the political

dimension of the crisis Within this frame the section focuses on the massive

failure of regulation before the crisis and argues that the crisis was then

permitted by the inaction of political and technocratic elites whose hubristic

detachment was such that they made no serious attempt to control the finance

Ewald Engelen et al Misrule of experts 361

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

sector A brief conclusion draws out some implications and makes some

recommendations The final verdict is that this financial crisis is different from

earlier credit crises because it now requires a political solution

The financial crisis in a socio-technical frame

The causes of the August 2007 financial crisis have been understood in a

variety of ways Typically authors fall into one of two camps for some it was

an accident the unanticipated product of system malfunction for others it

was unbridled individual greed Yet despite the differences that exist within

and between these perspectives both groups generally assert or assume that

stability within financial markets can be restored through technical interven-

tions which hand great responsibility to technocratic overseers This section

reviews these two perspectives before briefly summarizing other accounts

which engage with our two key observations that knowledge limits render

finance practically unmanageable in its present incarnation and that reform is

not just a question of selecting the correct socio-technical fix but rather is a

broader problem of accountability in politico-regulatory structures

The idea that the 2007 crisis was the result of a socio-technical malfunction

and could be fixed by technocrats with new tools is the basis for most official

reports on the subject This is no surprise given that their usual remit is to

identify problems and recommend solutions but what is notable is the distinct

lack of any discussion on either the limits of technocratic control in a sector

like finance or the institutional failings which led to the crisis Instead reports

like those by De Larosiere Turner and Walker all published in 2009 offer

detailed analysis of multiple and compounding system failures but then assume

that this can be rectified with the right kind of technical interventions which

return financial markets to a state of stability by restoring the defective part(s)

The system malfunction analysis and lsquolist and fixrsquo format also appears in a

number of academic publications on the crisis where an emphasis is placed on

the need for better regulation of mortgage originators and improved

transparency in securitization markets (for example De La Dehesa 2007

Unterman 2009) In a more theoretical development system malfunction

arguments appear in recent academic accounts inspired by Perrowrsquos (1984)

classic work on normal accidents Guillen and Suarez (2009) for example use

Perrowrsquos frame to argue that financial markets became more complex as banks

diversified and products became more opaque Similarly the system became

more tightly coupled as leverage levels and bespoke derivatives tied in the

fortunes of major banks eroding the safety buffers which might prevent

cascading losses across notionally separate financial institutions and markets

(see also Schneiberg amp Bartley 2009 p 7) From this perspective the crisis was

not caused by human venality or fraud but by anonymous interactions within a

closed system (Palmer amp Maher 2010 p 84) Restoring stability to financial

362 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

markets is therefore a technical matter of reducing system complexity and

introducing redundancies that improve robustness

If these authors view the crisis as a product of malfunction in a closed

system a second group of authors take the opposite position that the crisis was

not caused by impersonal systemic interactions but by lsquoknowing actorsrsquo Yet

despite this fundamental disagreement the idea that errors can be reversed

and stability can be restored through technical interventions alone is retained

This idea is at the heart of most lsquomoral hazardrsquo analyses which explain the

crisis as rational responses by knowing subjects to distorted incentives

Bebchuk et al (2009) argue that the boards of large banks understood the

risks they were taking but calculated that other actors (shareholders and

taxpayers) would take on the costs if the gambles failed (see also Becker 2008

Dowd 2009 Ho 2009) Elite actors therefore responded rationally to

institutionally set remuneration incentives which encouraged short termism

and increased the probability of corporate failure (Dowd 2009 p 144) Moral

hazard we are told is easily solved with a basic technical reform of

remuneration structures so that a greater portion of pay is remitted in long-

dated share options with claw-back provisions Other authors recommend

more radical cures for moral hazard such as the separation of retail and

wholesale banking activities in a bid to end too-big-to-fail incentives created by

state bailout guarantees (see for example King quoted in Halligan 2011)

It is at this point that we would emphasize the importance of a different set

of authors who continue the lsquoknowing actorsrsquo theme but recognize that

problems have a political and regulatory context primarily strong economic

andor ideological connections between financial and political elites which

may frustrate attempts to impose new technical reforms Ironically this is the

position of Charles Perrow the progenitor of normal accident theory who like

Bebchuk et al (2010) argues that the financial crisis was neither lsquoaboversquo agency

nor inevitable but rather caused by self-interested agents conscious of the

effects of their actions But it is crucial to note that Perrow (2009) argues that

malfeasance was aided and abetted by political and regulatory elites who

seduced by donations and the offer of revolving door jobs deliberately turned a

blind eye to the manifest dangers building up within financial services (see also

Blackburn 2008 pp 814) These claims are taken further by Simon Johnson

ex-chief economist at the IMF and James Kwak (2010 pp 67 ch 7) and by

those on the radical left like Gowan (2009) who in different ways argue that the

power of the major banks is systemic and that the (Anglo-American) state has

simply become an expression of prevailing class relations where finance capital

is in the ascendance (see also Wade 2008 pp 1314)

Perrow (2009) Johnson and Kwak (2010) and Gowan (2009) argue that

financial market problems are both technical and political insofar as it would be

foolhardy to expect radical reform from a political and regulatory coterie The

political dimension of the crisis is important and these authors are right to

emphasize this neglected part of the story Yet their understanding of the political

dimension does however border on the conspiratorial where politicians cut

Ewald Engelen et al Misrule of experts 363

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

shadowy deals with senior bankers with self-serving intent Such ideas presume

shared private knowledges and interests and ignore the possibility that elite

politicians and bankers might have had agency without really understanding

what they were doing and the likely outcomes of their actions

From this point of view we would emphasize the importance of a third set of

authors who propose more sophisticated institutional and cultural explana-

tions about knowledge limits Most notable here is the work of Financial Times

commentator Gillian Tett who identifies the problems created by institutional

silences and silos within banks and between banks and regulators which

meant that the arcane technical innovations within credit markets were not

well understood by bank CEOs or politicians (Tett 2010) The limits of

knowledge or lsquopracticersquo are constructed differently by MacKenzie (2010a)

whose argument is that different clusters of evaluation around asset-backed

securities (ABSs) and collateralized debt obligations (CDOs) created arbitrage

opportunities that resulted in financial catastrophe The Gaussian copula

assumptions used by CDO engineers assumed low default correlations in

mortgage-backed ABSs which boosted demand for riskier ABS tranches

which in turn allowed new mortgages to be written to riskier households

The cultural and calculative explanations of Tett and MacKenzie emphasize

the importance of human agency in the current financial crisis without

reducing everything to a conspiracy on the part of knowing actors But in

contrast to Perrow and others their reform recommendations are surprisingly

modest Tett (2010) proposes an anthropologistrsquos variant on the socio-technical

fix for finance and argues the case for a more active role for outsiders or

lsquocultural translatorsrsquo who could develop a more holistic view MacKenzie offers

different socio-technical solutions such as the need for better models which

build from the bottom up (MacKenzie 2010b) as well as for banks to pay more

attention to the gaps in evaluation cultures (MacKenzie 2009)

Nevertheless the insights of Tett on institutional blockages to knowledge

sharing and MacKenzie on the unanticipated consequences of various actors

transposing specific knowledges into different settings are crucial and raise the

central question about the limits of manageability Our analysis now explains in

more detail precisely why finance in its current form is unmanageable and

requires transformative rather than restorative intervention The third section

then follows by developing a stronger political dimension to the analysis Here

we emphasize the hubristic detachment of political and technocratic elites from

events in financial markets which ultimately proved fatal The challenge for

transformative regulation is therefore not just selecting the right technical tools

but securing greater accountability and oversight of politicians and technocrats

Bricolage and ungovernability

Some of the authors discussed in the first part of the previous section retain

the idea that the crisis is an error or aberration in a system that is normally

364 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

stable and hence stability can be restored with the right socio-technical tools to

fix the defective parts The elephant in the room is whether finance in its

current form is simply beyond this kind of palliative reform and whether

finance is a system which generates order and disorder simultaneously Our

first claim is that finance is now technically ungovernable so that any attempt

to restore finance to some kind of equilibrium or balance is futile because

instability is written into its DNA We make this case by arguing that financial

innovation takes the form of bricolage which has had four key consequences the growth of volume complexity opacity and interconnectedness With

bricolage restorative regulation ceases to be an external constraint and

becomes an input for future financial improvisation by creative bricoleurs

The fundamental problem from a technocratic perspective is that financial

innovation does not progress in a predictable and rule-bound fashion it does

not take the form of scientific experiment or grand plan but rather takes the

form of what Levi-Strauss (1966) termed lsquobricolagersquo (Engelen et al 2010)

Our definition of financial innovation as bricolage differs from orthodox

understandings For mainstream finance innovation and financial market

practice are driven by rationalities Financial innovation is viewed as the

application of scientific formulas inducted from experiments and applied in

markets by financial engineers Bricolage on the other hand rather than

producing events from structures of formal knowledge involves the creation of

structures out of events it is innately improvisatory and the structures built are

without a central guiding scientific rationality For Levi-Strauss lsquothe

lsquolsquobricoleurrsquorsquo builds up structures by fitting together events or rather the

remains of events while science lsquolsquoin operationrsquorsquo simply by virtue of coming

into being creates its means and results in the form of events thanks to the

structures which it is constantly elaborating and which are its hypotheses and

theoriesrsquo (1966 p 22)

On the surface the idea that financial innovation is bricolage may appear

incongruous and implausible when there is widespread use of economic models

which draw on scientific theory for example in pricing options (Black Scholes)

measuring risk exposure (value at risk) or producing structured derivative

products (Gaussian copula models) To this we would make two responses

First the models used are diverse and involve improvisation by reflexive

market actors (Beunza amp Stark 2010 Haug amp Taleb 2009 MacKenzie 2003)

Haug (2006) lists 60 models for pricing options alone while Merton (1995)

lists 11 strategies for taking the same basic leveraged long position This all

suggests that the models are not plans or blueprints which format behaviour

but more a suite of adaptable resources that can be drawn upon selectively to

meet market opportunities that present

Second if financial models are a resource not a plan then it is important to

remember that they are just one element of a broader company (or even

divisional) trading strategy It is possible that two companies integrate identical

formulas into entirely different trading strategies To take a simple example

MacKenzie (2010a) convincingly demonstrates how the low default correlation

Ewald Engelen et al Misrule of experts 365

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

assumptions that underpinned ABS CDOs created a fatal arbitrage opportu-

nity as CDOs bought risky ABS tranches from which they produced reams of

AAA-rated paper But banks responded differently to this event Some like

Merrill Lynch Citi Bear Stearns and UBS took the correlation assumptions

at face value and boughtretained this AAA paper funded by cheap repo loans

booking a profit on the spread between the lower short-term borrowing rates

on the repos and the higher yield on the securities (Gorton 2010 Milne

2009) Others like Goldman Sachs were more concerned with exploiting the

information asymmetries created by these correlation assumptions In their

$1bn sub-prime backed lsquoTimberwolf rsquo CDO Goldman allegedly went short on

the securities sold to investors which infamously included one of Bear Stearns

now defunct hedge funds (Reuters 24 April 2010) and on their Abacus CDO

Goldman allowed a client hedge fund to select the underlying collateral for the

deal but this fund subsequently shorted the securitized structure In both

cases the same models are used for different ends with different economic

outcomes because they are integrated into a variety of strategies with a range

of goals The tangible result is morphing meso-configurations of instruments

practices and market relations constructed from events which in turn become

the start point for improvisation in the next phase of bricolage (see Engelen

et al 2011 for extended discussion)

To this general point about bricolage we can add a more specific point that

technical interventions which respond to immediate problems are unlikely to

prevent future crisis because they become simply another event from which

financial institutions improvise in the next phase This is a crucial destabilizing

condition In the standard case of industry regulation the characteristics of the

activity are fixed or slow to change so that regulation can be conceived of as an

external constraint on the activity But in the case of financial regulation

innovation ensures that activity characteristics can morph through and around

events including regulation which itself becomes a primary input This was

the case with credit derivatives where Basel I and II capital adequacy accords

became intrinsic to the developments of the CDO industry In this case a credit

default swap became a legitimate instrument to remove the credit risk from the

balance sheet and thereby reduce the amount of capital that a bank needs to

hold to offset that risk This regulation became an event from which new

structures like partially funded synthetic CDO were built driven by regulatory

capital arbitrage which swelled bank revenues and enlarged the bonus pool

The challenge of volume complexity opacity and interconnectedness

The improvisatory nature of financial innovation as bricolage and the

subsequent ease with which restorative regulation is incorporated into banking

strategies created unprecedented problems for regulators by the 2000s

Bricolage has then created four new challenges in the form of volume

366 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

complexity opacity and interconnectedness which makes it ungovernable and

now requires transformative rather than restorative interventions

In terms of volume many recent innovations particularly in swaps markets

are designed to manufacture risk and leverage rather than hedge risk If risk is

tradable and leverage magnifies returns then derivatives are a key way through

which the financial sector generates its own feedstock synthetically and

provides new opportunities for volume and return This rather than risk

management was often the principal reason for banks and other financial

actorsrsquo interest in options and futures where premium and margin were used

to speculate on price movements in financial markets For example total return

swaps or credit default swaps make it possible for financial actors to gain

(levered) exposure to the return profiles (and risks) of particular securities or

indexes without necessarily dedicating the resources to buy them outright

The purchase of $100 million of ABSs would normally require the

commitment of $100 million of cash But the same result can be achieved

via a credit default swap where a trader could sell insurance on the security

and charge a premium aligned with the interest payments on the underlying

securities The CDS requires no funding other than any collateral required by

the buyer which is substantially less than the $100 million required to buy the

securities outright Thus the CDS seller has a synthetic levered position

without ever buying the underlying securities For this reason as Das (2010)

points out it was possible for CDS volumes to exceed four times the value of

the underlying bonds and loans by the end of the boom with multiples in

currency and interest rate swaps much higher

Those volumes are now so large as to be fundamentally destabilizing The

notional value of contracts outstanding on over-the-counter (OTC) derivative

markets increased 950 per cent from $72134 billion in June 1998 to a peak of

$683814 billion by June 2008 before falling back to $614673 billion by the

end of 2009 Measured comparatively OTC contracts outstanding grew from

around 24 times global GDP in 1998 to roughly 10 times by the end of 2009

according to the Bank for International Settlements At the peak in 2008 the

value of OTC derivatives outstanding was equivalent to the value of all goods

and services produced globally in the previous twenty years (Duncan 2009)

When exposures exceed multiples of global GDP as we will demonstrate later

in the argument the sheer weight of finance becomes difficult to control at

national level where regulation is primarily located

If these levels of exposure make governing finance difficult then govern-

ability is further reduced by complexity Complexity takes two forms at the

level of the product and at the level of the market relations around the product

though there is some difficulty in distinguishing the two At the level of the

product CDOs moved from relatively simple cash or lsquotrue salersquo balance sheet-

oriented structures in the late 1990s to actively managed synthetic arbitrage-

oriented structures by the mid-2000s As the models became more complex so

too did the market relations around them Figure 1 shows a fourth-generation

hybrid CDO that combines both cash and synthetic securitization It is actively

Ewald Engelen et al Misrule of experts 367

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

managed throughout its life by two special purpose vehicles (SPVs) SPV3

creates and manages a portfolio of reference assets that are not totally derived

from the originating bankrsquos balance sheet while SPV1 and possibly SPV2 buy

and sell credit default swaps to try to boost the overall arbitrage profits Total

return swaps and credit default swaps both provide protection and augment (or

preserve) returns from the reference portfolio of assets in theory diversifying

the sources of protection purchase Reference assets managed by SPV3 can

include mortgage-backed and other ABSs but may also involve both long

positions in derivatives like credit default swaps

Portfolio creation and management also necessitate a need for access to a

liquidity fund via a bank counterparty and a fund manager As early as 2001

The Economist reported that lsquo[t]he chairman of American Express Kenneth

Chenault was man enough to admit that his outfit lsquolsquodid not fully

comprehendrsquorsquo the risk underlying a portfolio of whizz-bang investments known

as CDOsrsquo (26 July 2001) If senior market actors privy to the marketing

literature of early-stage CDOs struggled to comprehend what was going on

with relatively simple CDO structures it is not hard to see why regulators

looking in from the outside might struggle in 2007 to understand the points of

vulnerability and possible risks

If these CDOs are difficult to understand in retrospect they would be

virtually impossible for regulators to understand ex ante The related opacity of

finance is therefore a third challenge to regulators The opacity of finance is

Figure 1 Partially funded synthetic CDO structureSource UK Balance of Payments The Pink Book

368 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

not just the inevitable consequence of complexity because opacity owes much

to fair value accounting and the widespread use of off-balance sheet special

purpose vehicles domiciled in tax havens Because most derivatives are traded

lsquoover the counterrsquo and as such are effectively bespoke there is no large central

secondary market from which mark to market valuations might be inferred

For this reason paradoxically there is an over-reliance on the valuation models

of the institutions that generate the securities to price those securities (ICAEW

2009) Perversely this lsquomark to modelrsquo privilege is used to avoid taking write-

downs in the absence of market liquidity This was the case in early 2007 when

sub-prime defaults rose and banks initially refused to write-down the value of

their mortgage-backed securities because their models apparently indicated

there was no problem much to the frustration of hedge funds who had shorted

those structures (Lewis 2010) Valuations then lsquowent to zerorsquo very quickly as

the artifice of valuation disintegrated in the crunch of August 2007 (Smith

2010) If prices provide no signal to regulators of emerging risks and problems

until it is too late to make ameliorative interventions then this opacity is a

major control problem This control problem is also exacerbated by the growth

of the shadow banking system as off-balance-sheet entities domiciled in the

Cayman Islands and elsewhere mean exposures are increasingly sheltered from

the scrutiny of regulators who can follow the obligations only until they vanish

from sight

Readers up to this point might acknowledge that these developments pose

significant tests to technocrats but do not necessarily undermine the case for

restorative reform provided it is ambitious enough Our response is that the

fourth challenge interconnectedness makes technocratic responses to financial

crisis increasingly futile Interconnectedness takes two forms the concentra-

tion of relations and exposures between core financial institutions and the

exposure of national governments to their own domestic financial industry or

as we are now discovering to the financial sector of foreign sovereigns

In terms of the interconnectedness of financial institutions the combination

of higher volumes with growing industry concentration (see Crotty 2007) has

resulted in the creation of a fragile complex latticework of exposures and

obligations between systemically important banks By 2009 J P Morgan had

derivatives exposure of $78545 billion in a total market valued at $614673

billion According to the Office of the Comptroller of the Currency (2009)

bank trading and derivatives report the notional value of derivatives held by

US commercial banks was $2128 trillion (2009 p 1) Of the 1030 US

commercial banks that submitted their derivatives exposure the top five

claimed 97 per cent of this notional value Such concentration is quite

staggering An important qualification is that many industry observers argue

that the size and risks associated with such exposures are reduced by netting a

bank may have a long default risk in one market and hedge by going short if

industry conditions change But post-netting exposures are still very large

moreover the distressed conditions under which netting might take place are

precisely those under which it would be impossible to enforce regulation

Ewald Engelen et al Misrule of experts 369

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

Domino-like effects are the logical result if one counterparty does not or

cannot fulfil a sizeable contractual obligation because this would create

suspicion and fear and disrupt a sequence of payments from bank to

bank as many financial institutions found out to their cost when the

monoline insurers faced massive losses and credit downgrades in early 2008

The combination of the four challenges volume complexity opacity and

interconnectedness ties large systemically important banks together in a

compact which assures mutual self-destruction in the event that one collapses

This is now all the more serious as post-2008 events demonstrate given

bricolage a national banking system in a small open country can have

liabilities much larger than the mobilizable assets or revenue-raising powers of

their national governments This was the case in small economies like Iceland

and Ireland where banking assets to GDP ratios rose to over 800 per cent and

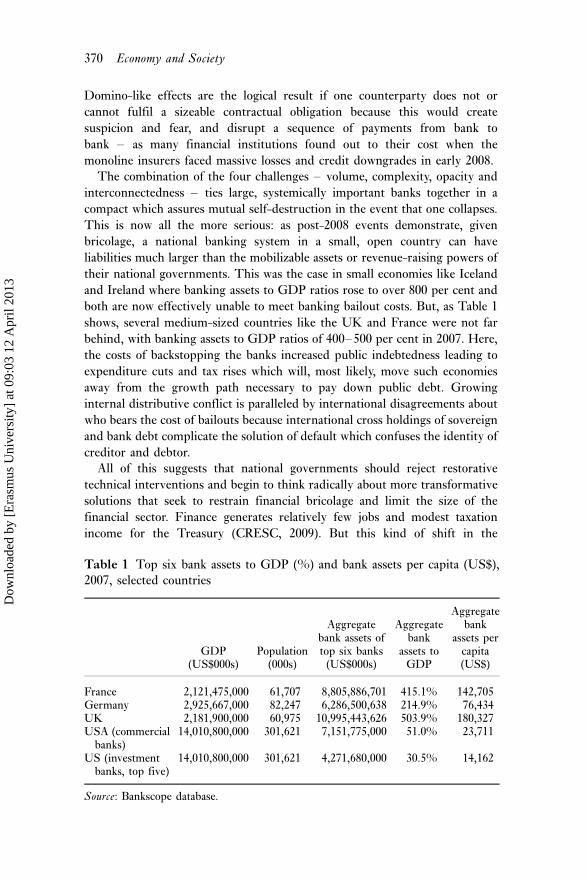

both are now effectively unable to meet banking bailout costs But as Table 1

shows several medium-sized countries like the UK and France were not far

behind with banking assets to GDP ratios of 400500 per cent in 2007 Here

the costs of backstopping the banks increased public indebtedness leading to

expenditure cuts and tax rises which will most likely move such economies

away from the growth path necessary to pay down public debt Growing

internal distributive conflict is paralleled by international disagreements about

who bears the cost of bailouts because international cross holdings of sovereign

and bank debt complicate the solution of default which confuses the identity of

creditor and debtor

All of this suggests that national governments should reject restorative

technical interventions and begin to think radically about more transformative

solutions that seek to restrain financial bricolage and limit the size of the

financial sector Finance generates relatively few jobs and modest taxation

income for the Treasury (CRESC 2009) But this kind of shift in the

Table 1 Top six bank assets to GDP () and bank assets per capita (US$)

2007 selected countries

GDP(US$000s)

Population(000s)

Aggregatebank assets oftop six banks

(US$000s)

Aggregatebank

assets toGDP

Aggregatebank

assets percapita(US$)

France 2121475000 61707 8805886701 4151 142705Germany 2925667000 82247 6286500638 2149 76434UK 2181900000 60975 10995443626 5039 180327USA (commercial

banks)14010800000 301621 7151775000 510 23711

US (investmentbanks top five)

14010800000 301621 4271680000 305 14162

Source Bankscope database

370 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

principles of financial reform remains politically unattractive for national

governments like that in the UK which takes the finance sectorrsquos public

relations story at its own estimation and is hostile to a more hands-on approach

to industrial policy despite the rhetoric about rebalancing the economy There

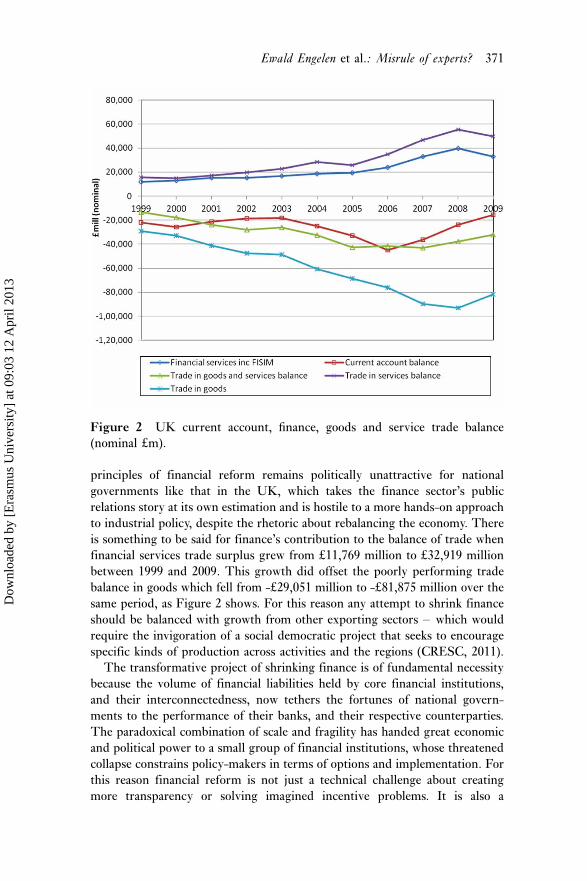

is something to be said for financersquos contribution to the balance of trade when

financial services trade surplus grew from pound11769 million to pound32919 million

between 1999 and 2009 This growth did offset the poorly performing trade

balance in goods which fell from -pound29051 million to -pound81875 million over the

same period as Figure 2 shows For this reason any attempt to shrink finance

should be balanced with growth from other exporting sectors which would

require the invigoration of a social democratic project that seeks to encourage

specific kinds of production across activities and the regions (CRESC 2011)

The transformative project of shrinking finance is of fundamental necessity

because the volume of financial liabilities held by core financial institutions

and their interconnectedness now tethers the fortunes of national govern-

ments to the performance of their banks and their respective counterparties

The paradoxical combination of scale and fragility has handed great economic

and political power to a small group of financial institutions whose threatened

collapse constrains policy-makers in terms of options and implementation For

this reason financial reform is not just a technical challenge about creating

more transparency or solving imagined incentive problems It is also a

Figure 2 UK current account finance goods and service trade balance

(nominal poundm)

Ewald Engelen et al Misrule of experts 371

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

democratic challenge of reducing the size of financial markets and institutions

so that their activities are not so damaging to the national economies and by

dint of their linked exposures they are less able to exert their will against that

of the electorate On this basis the 2007 crisis should be understood as an elite

debacle driven by improvising bankers and allowed by permissive regulators

thus reform should focus on improving the democratic accountability of

political and technocratic elites

The financial crisis as elite debacle

If the 2007 crisis was an elite debacle we can turn to the politics literatures on

policy disasters which provide us with various general perspectives of limited

relevance to the specific case of finance Hence we present a different kind of

argument about how elite debacle in finance is rooted in a distinctive and

detached post-1980s mode of governance after deregulation In the UK case

the rhetoric of neoliberalism and the long history of trust between finance and

its public regulators were reinvented as politically sponsored lsquolight touchrsquo

regulation Hubristic detachment was then encouraged by new modes of

governance driven by organizational developments The resulting financial

crisis was then a debacle of policy elites who failed to understand finance as

ramshackle bricolage which was bound to go wrong (in unpredictable ways)

The politics literature on disasters divides into three broad streams which

take different epistemological and ontological positions The first may be called

fatalistic insofar as the dominant theme is simply that lsquoaccidents will happenrsquo

This account often unites some high theorists of catastrophe with lsquocommon-

sensersquo accounts and of course echoes Perrowrsquos classic 1984 position on

lsquonormal accidentsrsquo which under some technological and social conditions

must be expected Practitioners faced with the problem of making sense of

fiascos post hoc commonly stress the complexity of the world and the

inevitability of things going wrong (for examples ranging from BSE to

financial failure see Moran 2001)

A second may be referred to as constructivist where the emphasis is on the

absence of a stable lsquoobjectiversquo understanding of a fiasco or disaster Shifting

value criteria or even the passage of time can change our understandings of a

particular fiasco and its extent A commonly cited example is the Sydney

Opera House which began as a disaster and ended as a triumphant icon The

most extended statement of this account is Bovens and rsquotHart (1996 see also

Bovens et al 2001) where the dominant message is that fiasco cannot be

explained objectively and so the aim is to explore the different meanings

assigned to specific fiascos

A third stream is the modernist stream epitomized in the sub-title of

Scottrsquos (1998) classic study lsquoHow certain schemes to improve the human

condition have failedrsquo Here disasters are the result of a particular historical

conjuncture in the modern world a toxic combination of modern state power

372 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

and the Enlightenment legacy of an obsession with legibility simplification

and measurement The result is high modernist disasters in arenas as

diverse as the modern city economic planning and the management of nature

lsquoThin simplificationrsquo knowledge derived from standardized measurement

systems overrides metis the practical knowledge derived from everyday

experience and the result is disaster The argument uncannily echoes

Oakeshottrsquos (1962) case for the primacy of tacit knowledge over expertise and

data in the practice of government

The specific debacle which led to the events of August 2007 differed in a

number of respects from these general accounts Interestingly the fatalistic

view has been forcefully attacked by Perrow (2009) and is untenable if we wish

to locate causes and avoid teleology Indeed the fatalistic lsquoaccidents will happenrsquo

account is probably most useful to policy-makers attempting blame avoidance

in the inquests that follow fiasco (this excuse was tried for example in earlier

fiascos like the Baring collapse of the mid-1990s and the UK banking crisis of

the mid-1970s see Moran 1986 2001)

A constructivist understanding of the debacle is equally inappropriate

because while there may be competing explanations of the crisis its scale and

negative consequences are inescapable as sovereign defaults beckon What

culminated in the 20078 crisis is not like the Sydney Opera House a blessing

in disguise Equally it is hard to argue that the crisis is caused by an obsessive

modernist concern with control monitoring and surveillance at the expense of

metis While this trend is observable in a number of public- and private-sector

examples often with contradictory results (see Dunleavy 1995 Power 1994)

it would be hard to picture what happened in financial regulation in the run up

to the crisis as exhibiting a modernist mania for control On the contrary the

main thrust of policy was in the opposite direction with the dismantling of

monitoring and control under regimes that placed excessive faith in market

operators and too heavy a reliance on the tacit practical knowledge of those

with expertise in markets In this sense it was deference to metis not its

extinction that gave us the crisis

This observation provides us with a starting point why was there such

deference to the practical knowledge within financial markets and the supposed

capacity of market actors and institutions to recognize package and manage

risk In the UK case we can begin by recognizing that deference to the markets

went with the grain of long-established habits of British financial regulation

and with the rhetorics of the current neoliberal project

The pattern of financial regulation and oversight in the UK was

characterized by high levels of trust between regulators and those regulated

within an enclosed interconnected policy-making community around finance

that has resisted the audit and evaluation imperatives so well described by

Power (1994) This resulted in a particular form of regulation that relies

heavily on shared interpersonal knowledges with evaluation and decision

making often informal ie driven by the lsquoimponderables of personal

judgementrsquo (Moran 2001 p 421) rather than the strict routinized

Ewald Engelen et al Misrule of experts 373

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

indicator-driven regimes of oversight and control that characterize other

sectors Financial regulation was initially reinvented after the 1986 Big Bang of

deregulation and then again when New Labour in office re-regulated finance

with the merger of banking supervision and investment services regulation

under the auspices of the Financial Services Authority (FSA) But finance was

never subject to the more adversarial forms of regulation typical under new

public management regimes in the public sector or the more proactive hands-

on approach of regulators in the privatized utilities sector like telecoms where

reducing costs to the consumer was the fundamental principle of action

The peculiar regulatory privilege of finance reflects the endurance of what

other authors have termed lsquoclub governmentrsquo (Marquand 1988) In numerous

areas of public policy the Thatcher revolution consolidated under New

Labour destroyed the club system replacing it with more transparent

centralized and low trust systems of control (Moran 2003) It seemed

superficially that the centralization of regulatory authority in the FSA in 1997

had accomplished something similar But the FSA was an imposing Potemkin

village behind its impressive facade it deferred club fashion to the elites in the

market This system has persisted in part because of the close reciprocal ties

between financial elites and high public office which provide ample

opportunities for financial reward to senior politicians and bureaucrats who

leave public service via lsquothe revolving doorrsquo to enter into lucrative directorship

or advisory roles in industry (see Gonzalez-Bailon et al 2010 Hood amp Lodge

2006) Tony Blair for example currently makes pound35 million per year as a

senior advisor to JP Morgan on top of the pound500000 per year as an advisor to

Zurich Financial another six figure sum as advisor to private equity firm

Khosla Ventures and pound1 million per year as a lsquogovernance advisorrsquo to Kuwait

(McSmith 2010)

But ideas were also important in Britain and the United States as part of a

rhetorical commitment to a neoliberal project of social and economic

reconstruction in the image of a deregulated system of free market capitalism

This rhetoric was not always faithfully implemented (see Konings 2008) and

could not be implemented in finance where state withdrawal was not an option

But is it too much to assert that this rhetoric was fundamentally lsquoideologicalrsquo in

its orthodox Marxist sense articulated by knowing political elites to empower

finance capital It is more prudent to view neoliberal thought as the ideational

centre of gravity which influenced and encouraged lsquolight touchrsquo regulation as

the most likely model of achieving sustainable economic growth lsquoLight touchrsquo

for example was personally championed by New Labourrsquos Chancellor Brown

for whom it was governmentrsquos positive contribution to the success of London

as an international financial centre

And just as two years ago we promoted the action plan for liberalising financial

services across Europe I can tell you that the Treasury is now working to

ensure that the forthcoming European financial services white paper signals a

new wave of liberalisation In 2003 just at the time of a previous

374 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

Mansion House speech the Worldcom accounting scandal broke And I will be

honest with you many who advised me including not a few newspapers

favoured a regulatory crackdown I believe that we were right not to go down

that road which in the United States led to Sarbanes-Oxley and we were right to

build upon our light touch system fair proportionate predictable and

increasingly risk based

(Brown 2006)

The policy of lsquolight touchrsquo was empowered by the short-term success of the

debt-fuelled boom of the mid-2000s which reinforced the neoliberal consensus

and encouraged optimism about an emergent new epoch For technocrats like

Mervyn King this was the Great Moderation the NICE decade the

Goldilocks economy for Chancellor Brown the growth rates confirmed his

conviction that policy-makers had effectively abolished boom and bust In

retrospect these claims and assumptions are deeply hubristic in the more or less

exact meaning of that word an overbearing self-confidence that led to ruin

And with hubris comes post hoc denial as events and onersquos personal role

within them are rewritten to accommodate emerging realities as was the case

with Gordon Brown

As I said in Harvard ten years ago we need an early warning system so that

international financial flows are properly monitored We must create a

framework for the international governance that we currently lack We must

consider at a global level the regulatory deficit For a decade I have said that the

current patchwork arrangement is inadequate

(Brown quoted in Booth 2009)

The role of hubris in modern politics is closely documented in studies of

foreign policy disasters such as the Afghanistan and Iraq conflicts (see Beinart

2010 Owen 2007 2008 Scheuer 2007) The public case for intervention in

Iraq involved the hurried manipulation of intelligence evidence to defend a

decision previously agreed with President Bush that the UK would support

the US in their quest to remove Saddam depriving the cabinet and parliament

of key information in the meantime (Sands 2011) The Butler inquiryrsquos verdict

on New Labourrsquos style of sofa government is understated but nevertheless

devastating lsquowe are concerned that the informality and circumscribed

character of the Governmentrsquos procedures which we saw in the context of

policy-making towards Iraq risks reducing the scope for informed collective

political judgementrsquo (Butler 2004 para 611) The decision processes which

led to the Iraq war as detailed by Lord Butlerrsquos inquiry show a pattern of

casualness and bravado characteristic of what Owen (2008) calls lsquohubristic

incompetencersquo a situation where elite political leaders have the self-perception

that they are missionaries or heroes endowed with powers to do good and take

the correct decision without necessarily engaging with the intricacies of policy

detail Policy on financial market oversight by way of contrast was marked by

Ewald Engelen et al Misrule of experts 375

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

lsquohubristic detachmentrsquo a cavalier lack of interest in the detail of financial

market operations and a faith that everything was probably all right This may

have been due to a perception that the lsquoright kind of peoplersquo were in charge of

key banking institutions and so it is important not to forget the lessons of

Milibandrsquos (1969) classic study of the UK capitalist state which emphasized the

importance of social ties But perhaps more pertinent is the growth of a

broader culture of government in an organizational and institutional setting

which weakened political control and democratic accountability

It is possible to identify two key institutional developments which

empowered hubristic modes of leadership after the 1980s at a political and

regulatory level and which contributed significantly to the crisis in the late

2000s First senior politicians became increasingly detached from events in

financial markets due to the dual process of centralization and devolution that

allowed political leaders to concentrate on big picture lsquostrategyrsquo leaving

tedious evidence and detail to subordinate technicians The delegation of

economic policy decisions such as interest rate setting financial regulation and

trade policy to a newly empowered technocratic elite had the effect (super-

ficially at least) of depoliticizing economic decision-making by moving it

beyond the reach of democratic control (Peck amp Tickell 2002) The result was

a political elite naıve to the developments in financial markets but happy to ride

the bubble while technocrats pondered the detail but lacked the will and

initiative to intervene without any political steer

Second the emphasis on controlling inflation as the principal concern of

economic management removed checks and balances and encouraged

hubristic detachment at the top of key regulatory institutions Gordon

Brownrsquos 1997 decision to devolve interest rate setting to the Bank of England

with a remit to keep inflation below 2 per cent empowered the Bankrsquos

Monetary Policy division at the expense of the Financial Stability division

who also ceded banking and securities oversight duties to the newly created

FSA This unbalanced the Bank of England by recalibrating internal status

hierarchies around monetary concerns and expertise within the institution

(see also Pomerleano 2010) and also encouraged stronger divisions between

what following Dunleavy (1980) we might term lsquoorganizationalrsquo elites and

lsquoprofessionalrsquo experts The new monetary policy remits drew the Governor

Mervyn King and other senior Bank employees into elite policy-making

circles in Whitehall producing a new cadre of senior organizational operators

connected to key opinion formers politicians and their advisors This led to

increasing hubris as Kingrsquos speeches adopted the trite reassuring language

and bland generalities that are normally the preserve of a front bench

politician

Securitisation is transforming banking from the traditional model in which

banks originate and retain credit risk on their balance sheets into a new model in

which credit risk is distributed around a much wider range of investors As a

result risks are no longer so concentrated in a small number of regulated

376 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

institutions but are spread across the financial system That is a positive

development because it has reduced the market failure associated with traditional

banking the mismatch between illiquid assets and liquid liabilities that led

Henry Thornton and later Walter Bagehot to promote the role of the Bank of

England as the lsquolender of last resortrsquo in a financial crisis

(King 2007)

If hubris dominated Bank of England decision-making examples of ineptitude

casualness and a more general lack of professional scepticism are reported

about the operations at the FSA (eg Financial Times 11 October 2007 12

November 2008 and see also FSA 2008) Such ineptitude is conservatively

understood as the result of the low levels of remuneration and poor

recruitment at the FSA but the lack of rigorous oversight cannot be entirely

divorced from the general political pressures that emanated from the practice

of lsquolight touchrsquo regulation and the confidence of key operators like King about

the benefits of market self-regulation In many ways the assertive connection in

elite policy circles between non-inflationary growth and laissez faire financial

markets meant the Bank and the FSA while often organizationally divorced

were ideologically united in deferring to the metis of the markets

The paradox is that hubristic detachment is in part the result of a division of

labour between politicians and technocrats which empowered a new style of

organizational expert like Mervyn King who failed to engage with the detail of

financial innovation But this is not to imply that lsquore-engagementrsquo would have

prevented crisis though arguably it may have made us more prepared as credit

markets faltered The more fundamental problem is not knowledge gaps which

can be solved through reorganization or socio-technical interventions but

knowledge limits which are written into the DNA of financial innovation when

it takes the form of bricolage The nature of financial innovation sets practical

limits on the capacity of outside experts to understand and manage finance

even with new data or different conceptual approaches The aim of reform

should be to render finance amenable to technical controls but that in turn

requires a fundamentally new compact between civil society and its politicians

and regulators and a transformative technical agenda which seeks to shrink

finance and bring it back under democratic control

Conclusion

Our argument is that we are not living through a financial crisis caused by

some isolated socio-technical malfunction which experts can identify and fix

We are living through compounding political disasters the product of an elite

debacle that come after a massive misjudgement about the character and

consequences of financial innovation Technocratic elites and their political

sponsors have failed in their first duty as public servants to protect the

citizenry from predatory capitalist business which privatizes its gains and

Ewald Engelen et al Misrule of experts 377

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

socializes its losses The interim result is public expenditure cuts that are

beginning to bite in countries like the UK and bailouts of Greece and Ireland

that have failed to stabilize the Eurozone The future may be one of

intensifying intra-national and international distributive conflict with un-

predictable political consequences

But if such grand harm was permitted by detached politicians and

regulators it is too much to suppose that they can now make things better

by improving their technical capacity to monitor understand and steer

financial activity Their earlier hubristic misjudgements have had semi-

permanent hard to reverse consequences The political belief in the social

value of growth in financial services will not disappear overnight nor will the

blind faith in free markets because they are deeply engrained culturally and

ideologically Institutionally the triangular relation between finance technoc-

racy and elected politicians is one where the ostensibly independent

technocrats and politicians are hostages of a financial sector that produces

valuable exports but also dangerous liabilities Under such conditions the issue

is not a technical one about preventing future crises but a democratic issue

about public control of our economic and social futures

Against this background the analysis in this paper should be read more as an

attempt to clarify the problem and open out debate That debate must begin by

asking a different question from the one that currently dominates current

academic and policy documents lsquohow do we fix finance and prevent future

crisisrsquo Instead we should begin by debating how to bring finance under

democratic control This would require at least three levels of intervention At

a basic level it would involve greater public accountability of politicians and

regulators and new structures put in place for more effective checks and

balances Certainly this might include the use of cultural translators working

within the banks as Tett (2010) proposes but more importantly it would mean

greater public engagement and representation on those bodies with oversight

responsibilities For example if tradesrsquo union members working within the

retail banks had been asked about the kinds of mortgages they were offering to

clients and their possible downsides alarm bells might have sounded earlier

Second the principle of shrinking finance would require some socio-

technical interventions The logic of our analysis of financial innovation as

bricolage and of the problems associated with volume opacity and inter-

connectedness suggests policies that limit the volume of financial transactions

which bind bank exposures together in unpredictable ways To do this we

would like to see a greater proportion of all financial transactions brought onto

an exchange with onerous regulations about margin requirement and also for a

Tobin-style tax to be applied to each transaction This would not only render

many of the speculative transactions unprofitable and thus reduce volume but

would also build up a fund from which more productive investments could be

used This has advantages over the often-mooted partition or separation of

retail and wholesale activities which rests on the double misconception that

wholesale markets can be allowed to seize or blow up and that wholesale traders

378 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

know what they are doing Knowledge failure in densely interconnected

wholesale markets caused the last crisis not moral hazard An appropriate

response to the crisis must therefore be radical both in developing

knowledges that can challenge orthodoxies and embedded elite groups and

in facilitating control of finance in ways that reduce the possible impact of

future crises as well as their likelihood These ambitions underline that this is

above all a democratic issue

References

Bebchuk L Cohen A amp SpamannH (2010) The wages of failure Executivecompensation at Bear Sterns and Lehman20008 Yale Journal on Regulation 2725782Becker G (2008) Wersquore not headed for adepression No this isnrsquot the crisis thatkills capitalism Wall Street Journal 7OctoberBeinart P (2010) The Icarus syndromeA history of American hubris New YorkHarperBeunza D amp Stark D (2010) Backingout locking in Financial models and thesocial dynamics of arbitrage disasters NewYork University Working Paper March2010Blackburn K (2008) The sub-primecrisis New Left Review 50 63106Booth J (2009) Gordon Brown lsquoIcalled for global financial reform tenyears agorsquo The Times 26 JanuaryBovens M amp rsquotHart P (1996)Understanding policy fiascoes LondonTransaction PublishersBovens M rsquotHart P amp Peters G

(Eds) (2001) Success and failure in publicgovernance A comparative analysisCheltenham ElgarBrown G (2006) Mansion Housespeech 21 June Retrieved fromhttpwwwguardiancoukbusiness2006jun22politicseconomicpolicyButler R (2004) Review of intelligence onweapons of mass destruction Report of aCommittee of Privy Counsellors ChairmanThe Rt Hon Lord Butler of BrockwellHC898 20034 Retrieved from httpwwwbutlerrevieworguk

CRESC (2009) An alternative report onUK banking reform University ofManchester Centre for Research inSocio-Cultural Change Retrieved fromhttpwwwcrescacukpublicationsan-alternative-report-on-uk-banking-reformCRESC (2011) Rebalancing the economy(or buyerrsquos remorse) CRESC WorkingPaper 87 University of ManchesterCentre for Research in Socio-CulturalChange Retrieved from httpwwwcrescacukpublicationsrebalancing-the-economy-or-buyers-remorseCrotty J (2007) If financial competition isso intense why are financial firm profits sohigh Reflections on the current Golden Ageof finance Working Paper 134 PoliticalEconomy Research Institute Universityof Massachusetts Amherst AprilDas S (2010) Swap tangoEurointelligence 2 March Retrieved fromhttpwwweurointelligencecomindexphpid581amptx_ttnews[tt_news]2712amptx_ttnews[backPid]752amp-752ampcHashb9a5fa817bDe La Dehesa G (2007) How to avoidfurther credit and liquidity confidencecrises In A Felton amp C Reinhart (Eds)The first global financial crisis of the 21stcentury Centre for Economic PolicyResearch (CEPR)VoxEUDe Larosiere J (2009) The High-LevelGroup on Financial Supervision in the EU(p 86) Retrieved from httpeceuropaeuinternal_marketfinancesdocsde_larosiere_report_enpdfDowd K (2009) Moral hazard and thefinancial crisis Cato Journal 29(1) 14166Duncan R (2009) The corruption ofcapitalism A strategy to rebalance the global

Ewald Engelen et al Misrule of experts 379

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

economy and restore sustainable growthHong Kong CLSADunleavy P (1980) Urban politicalanalysis London MacmillanDunleavy P (1995) Policy disastersExplaining the UKrsquos record Public Policyand Administration 10(2) 5270Engelen E Erturk I Froud JLeaver A amp Williams K (2010)Reconceptualizing financial innovationFrame conjuncture and bricolageEconomy and Society 39(1) 3363Engelen E Erturk I Froud JLeaver A Moran M amp Williams K(2011) After the great complacenceFinancial innovation and the politics ofreform Oxford Oxford University PressFSA (2008) The supervision of NorthernRock A lesson learned review FSAInternal Audit Division MarchGonzalez-Bailon S Jennings W ampLodge M (2010) The private gains ofpublic office Corporate rewards of formerhigh public officials in Britain Workingpaper Retrieved from httpmanchesteracademiaeduwilljenningsPapers136700The_Private_Gains_of_Public_Office_Corporate_Networks_and_Rewards_of_Former_High_Public_Officials_in_BritainGorton G (2010) Slapped by the invisiblehand The panic of 2007 Oxford OxfordUniversity PressGowan P (2009) Crisis in the heartlandConsequences of the new Wall Streetsystem New Left Review 55 529Guillen M amp Suarez S (2010) Theglobal crisis of 20072009 Marketspolitics and organizations In MLounsbury (Ed) Markets on trial Theeconomic sociology of the US financialcrisis Part A (pp 25779) Research inthe Sociology of Organizations Vol 30Bingley Emerald GroupHalligan L (2011) Historyrsquos lesson isthat investment and retail banking mustbe separate The Telegraph Comment 12MarchHaug E (2006) The complete guide tooptions pricing formulas New YorkMcGraw-HillHaug E amp Taleb N (2009) Why wehave never used the Black-Scholes-Mertonoption pricing formula Working Paper

February Retrieved from httppapersssrncomsol3paperscfmabstract_id1012075amprec1ampsrcabs283308Ho K (2009) Liquidated An ethnographyof Wall Street Durham NC DukeUniversity PressHood C amp Lodge M (2006) Politics ofpublic service bargains Oxford OxfordUniversity PressICAEW (2009) Evolutions Changes infinancial reporting and audit practiceICAEW Audit and Assurance FacultyMarchJohnson S amp Kwak J (2010) 13bankers The Wall Street takeover and thenext financial meltdown New YorkPantheonKing M (2007) Speech given at theMansion House 20 June Retrieved fromhttpwwwbankofenglandcoukpubli-cationsspeeches2007speech313pdfKonings M (2008) Rethinkingneoliberalism and the subprime crisisBeyond the re-regulation agendaCompetition and Change 13(2) 10827Levi-Strauss C (1966) The savagemind Chicago IL University of ChicagoPress (Translated from La Pensee sauvage1962 Paris Plon)Lewis M (2010) The big short Inside thedoomsday machine London Allen LaneMacKenzie D (2003) An equation andits worlds Bricolage exemplars disunityand performativity in financial economicsSocial Studies of Science 33(6) 83168MacKenzie D (2009) Culture gap lettoxic instruments thrive Financial Times25 NovemberMacKenzie D (2010a) The crisis as aproblem in the sociology of knowledgeUnpublished manuscript Retrieved fromhttpwwwspsedacuk__dataassetspdf_file001936082CrisisRevisedpdfMacKenzie D (2010b) Unlocking thelanguage of structured securitiesFinancial Times 18 AugustMarquand D (1988) The unprincipledsociety New demands and old politicsLondon CapeMcSmith A (2010) Tony Blair getsanother new job in Silicon Valley TheIndependent 26 MayMerton R (1995) Financial innovationand the management and regulation of

380 Economy and Society

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

financial institutions Journal of Bankingamp Finance 19(34) 46181Miliband R (1969) The state incapitalist society New York Basic BooksMilne A (2009) The fall of the house ofcredit What went wrong in banking andwhat can be done to repair the damageCambridge Cambridge University PressMoran M (1986) The politics of banking(2nd edn) London MacmillanMoran M (2001) Not steering butdrowning Policy catastrophes and theregulatory state Political Quarterly 72(4)41427Moran M (2003) The British regulatorystate High modernism and hyper-innovationOxford Oxford University PressOakeshott M (1962) Rationalism inpolitics and other essays LondonMethuenOffice of the Comptroller of theCurrency (2009) OCCrsquos QuarterlyReport on Bank Trading and DerivativesActivities Fourth Quarter 2009 [online]httpwwwoccgovtopicscapital-marketsfinancial-marketstradingderivativesdq409pdfOwen D (2007) The hubris syndromeBush Blair and the intoxication of powerLondon PoliticorsquosOwen D (2008) Hubris syndromeClinical Medicine 8(4) 42832Palmer D amp Maher M (2010) Themortgage meltdown as normal accidentalwrongdoing Strategic Organization 8(1)8391Peck J amp Tickell A (2002)Neoliberalizing space Antipode 34(3)380404Perrow C (1984) Normal accidentsLiving with high-risk technologies NewYork Basic BooksPerrow C (2009) The meltdown wasnot an accident In M Lounsbury ampP M Hirsch (Eds) Markets on trialThe economic sociology of the US financialcrisis Part A Research in the Sociology ofOrganizations Vol 30 Bingley EmeraldGroup (pp 309330)

Pomerleano M (2010) Are centralbanks up to the stability task FinancialTimes 8 DecemberPower M (1994) The audit societyRituals of verification Oxford OxfordUniversity PressSands P (2011) The questions TonyBlair should face at the Chilcot InquiryThe Guardian 21 JanuaryScheuer M (2007) Imperial hubris Whythe West is losing the war on terrorWashington DC Potomac BooksSchneiberg M amp Bartley T (2009)Regulating and redesigning financeObservations from organizationalsociology In M Lounsbury amp P MHirsch (Eds) Markets on trial Theeconomic sociology of the US financial crisisPart A Research in the Sociology ofOrganizations Vol 30 Bingley EmeraldGroup (pp 281308)Scott J (1998) Seeing like a state Howcertain schemes to improve the humancondition have failed New Haven CT andLondon Yale University PressSmith Y (2010) Econned Howunenlightened self interest undermineddemocracy and corrupted capitalism NewYork Palgrave MacmillanTett G (2010) Silos and silences Whyso few people spotted the problems incomplex credit and what that implies forthe future Banque de France FinancialStability Review 14 1219 Retrievedfrom httpwwwbanque-francefrgbpublicationstelecharrsf2010etude14_rsf_1007pdfTurner A (2009) A regulatory response tothe global banking crisis London FinancialServices AuthorityUnterman A (2009) Innovativedestruction Structured finance and creditmarket reform in the bubble era HastingsBusiness Law Journal 5(1) 53108Wade R (2008) Financial regimechange New Left Review 53 521Walker D (2009) A review of corporategovernance in UK banks and other financialindustry entities Final recommendationsRetrieved from httpwwwaccacoukdocumentscdr898pdf

Ewald Engelen is Professor of Financial Geography at the University of

Amsterdam His interests range from migration and the welfare state to

Ewald Engelen et al Misrule of experts 381

Dow

nloa

ded

by [

Era

smus

Uni

vers

ity]

at 0

903

12

Apr

il 20

13

shareholder value and corporate governance He is currently directing a

research project on the decline of the Amsterdam financial centre after

financialization

Ismail Erturk is Senior Lecturer in Banking at Manchester Business School

and a member of the Centre for Research in Socio-Cultural Change (CRESC) at

the University of Manchester His current research interests include corporate

governance emerging markets and the reinvention of banking Recent books

include Financialization at Work (2008) and CRESCrsquos Alternative BankingReport (2009)

Julie Froud is Professor of Financial Innovation at Manchester Business

School and a member of the Centre for Research in Socio-Cultural Change

(CRESC) at the University of Manchester Her current research interests

include elites and financialization Recent books include Financialization at

Work (2008) with Ismail Erturk et al and Financialization and Strategy (2006)

with Adam Leaver et al

Sukhdev Johal is a Reader in the Management School at Royal Holloway His

expertise is in social and economic statistics He is currently working on British

manufacturing and the national business model and was responsible for

argument and exhibits in CRESCrsquos Alternative Banking Report and Working

Paper 75 on the national business model

Adam Leaver is Senior Lecturer at Manchester Business School and a

member of the Centre for Research in Socio-Cultural Change (CRESC) at the