Evolution of Mexican Financial Markets€¦ · North-to-South FAQ & Onboarding Reference Guide 3....

34

The Evolution of Mexican Financial Markets Joe Kogan Head of Emerging Markets Strategy Scotia Capital Presentation prepared for MexDer – CME Launch July 28, 2011

Transcript of Evolution of Mexican Financial Markets€¦ · North-to-South FAQ & Onboarding Reference Guide 3....

The Evolution of Mexican Financial Markets

Joe KoganHead of Emerging Markets StrategyScotia Capital

Presentation prepared for MexDer – CME Launch

July 28, 2011

Contents

2

1. Introduction

2. Fixed Income

3. FX

4. Equity

5. Mexder

6. Scotiabank

CME Group / MexDer Partnership

In March 2010, CME Group and Bolsa Mexicana de Valores announced a new strategicpartnership.

April 4, 2011South-to-North Order Routing successfully launched

August 1, 2011North-to-South Order Routing to launch

Benefits• No withholding taxes when trading in MexDer

• No local presence required in Mexico

• Remote Membership

• Omnibus Accounts: Rule 30.7 (CFTC) segregation

One for Proprietary Trading

One for Customer Trading

• With the CME Group – MexDer order routing agreement MexDer products will be available in more than 100,000 CME Globex ® screens.

3

Customers

• CFTF Approved Products

• Remote Membership

• Co-location

• DMA

• Collaterals accepted in the U.S.

• Give Ups

FIA standard agreement

CME Group / MexDer Global Partnership Page

For more information on CME Group’s partnership with MexDer, plus Order Routing Agreements and upcoming events, visit the MexDer Partnership Page at www.cmegroup.com/mexder. Available resources include:

1. List of MexDer Clearing Members

2. North-to-South FAQ & Onboarding Reference Guide

3. Client Impact Assessment Document

4. MexDer / CME Group Partnership Brochure

5. Presentation on Mexican Bond Markets and IPC Futures

4

Mexican Sovereign Bonds: Total AmountOutstanding of Mbonos and Cetes

1999-2011 (July)

5

Mexican Sovereign Bonds: OutstandingAmount and Holders

Mexican Sovereign Bonds: Holdings by Local Investors

2007-2011 (July)

Source: Banxico

Fixed Income

Source: Banxico

Pension and Mutual Funds represent a solid, stable and a long term investment in the local markets, holding about 33% of the total amount outstanding

0

50,000

100,000

150,000

200,000

250,000

300,000

1999 1999 2000 2001 2002 2003 2004 2004 2005 2006 2007 2008 2009 2009 2010 2011

U.S

. m

illion

s

Total Local Investors Foreign Investors Total Outstanding Amount

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2007 2008 2009 2009 2010 2011

US

mil

lio

n

Banking System Pension Funds Mutual Funds Insurance Co. Other Local Investors

Mexican Sovereign Bonds: Foreign Investors

Foreign Investment in Mexican Cetes and Mbonos

6Source: Banxico

Foreign holders of Mbonos are mainly Central Banks, Insurance Companies, and Sovereign Funds. As a consequence we expect lower foreign outflows during high volatility periods.

2%

18%

33%

0%

5%

10%

15%

20%

25%

30%

35%

2009 2010 Jul-11

Cetes: Foreign Investment 2009 - 2011

Mbonds: Foreign Investment2009 - 2011

23%

31%

36%

15%

20%

25%

30%

35%

40%

2009 2010 Jul-11

Fixed Income

Mexico Budget Balance (%GDP)

7

Benchmark rate and Macroeconomics

Mexico CPI 1979-2011 (Annual Rate)

M Bono 10 Yr

5

6

7

8

9

10

11

12

Jul-01 Mar-02 Nov-02 Jul-03 Mar-04 Nov-04 Jul-05 Mar-06 Nov-06 Jul-07 Mar-08 Nov-08 Jul-09 Mar-10 Nov-10

%

Investment Grade forMexico

BanxicoTightening

Mexican PresidentialElections

Lehman Bankruptcy/Comerci derivatives

default

WGTB Index: Inclusion Mbonos

Subprime Mortgagescontagion

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

Jan-70 Jan-75 Jan-80 Jan-85 Jan-90 Jan-95 Jan-00 Jan-05 Jan-10

2000-2011

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Jan-00 Nov-01 Sep-03 Jul-05 May-07 Mar-09 Jan-11

-0.54%

-0.21%

-2.17%

-2.68%

0.09%

-0.10% -0.07%

0.04%

-3%

-3%

-2%

-2%

-1%

-1%

0%

1%

2003 2004 2005 2006 2007 2008 2009 2010

Fixed Income

8

Spreads between Mexican and US interest rates have been tightening due to solid fundamentalsin Mexico.

MEXICO – USA: BenchmarksRates /Spreads

Source: Bloomberg

USA – MEXICO: FED FUNDS TARGET RATE VS BANXICO OFFICIAL OVERNIGHT RAT

2005-2011

USA – MEXICO BOND YIELD SPREAD 10 YR2001-2011 (July)*

* US Generic Govt 10 Yr Yield vs GMXN10YR Index. Source:Bloomberg

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Oct-05 Jun-06 Feb-07 Oct-07 Jun-08 Feb-09 Oct-09 Jun-10 Feb-11150

250

350

450

550

650

750

2001 2002 2003 2004 2006 2007 2009 20102011

Fixed Income

9

MEXICO – Government Securities AuctionCalendar 2011

Quarterly

Instrument Bn Pesos

Cetes $25

MBonos $30 *

Udibonos $6

Source: SHCP * Syndicated

*Not includes Syndicated Auctions

The Government schedules auctions 1 month in advance of each quarter.

Primary Auction Issue Program (average data)

Fixed Income

10

Daily Market Volumes

• Bid ask spread is 1-3 bps, depends on volatily in Market

• Typical sizes are MNX$ 10-100 mm. Larger sizes would entail much larger bid-ask spread.

• Most liquid 10Y: June 20 and June 21

• Most liquid 20Y: May 29

• Most liquid overall: Dec 24

• Functioning repo market for domestic players

• No on-the-run premium as there is in US Treasuries

• 7 Market Makers approved by the Financial Authorities. They must comply with liquidity and volume standards on a monthly basis

• Qtr. Issuance schedule, sometimes new series, sometimes add to existing series.

• Security lending is available; Short selling is allowed to/through the Market Makers and/or Mexder

• Central counterparty “Indeval” clears, deposits and custodies all securities.

• Securities settlement within 96 hours

• Trade between 8:00 am and 3:00pm EST

• 4.9% withholding tax if double taxation treaty; 10% otherwise and 30% for tax havens

• No taxes in FX, Equity, and derivatives.

Up to90 days

From90 days to

1 Yr

From 1 Yr to3 Yr

From 3 Yr to5Yr

From 5Yr to10 Yr

From 10 Yrto 20 Yr

More than20 Yr

Cetes 759 1,045 0 0 0 0 0

Mbonos 234 713 1,072 1,097 2,031 3,285 820

Udibonos 0 0 26 9 71 23 34

Sources: Banxico as of Dic. 2010.

Average Daily Volume US Million

Mbonos Market

Fixed Income

USA – MEXICO Bond Curves*

11

Mexico - USA : Nominal and Swap Curves

USA Libor Curve– MEXICO TIIE Curves *

*Source: Bloomberg as of Jul, 6, 2011

The Mexican term structure offers many opportunities for trading, with tenors ranging from 1 day to 30 years.

0

1

2

3

4

5

6

7

8

9

1month

3months

6months

1 yr 2 yr 3 yr 5 yr 7 yr 10 yr 15 yr 20 yr 30 yr0

1

2

3

4

5

6

7

8

9

3months

6months

9months

1 yr 2 yr 3 yr 4 yr 5 yr 8 yr 10 yr 15 yr 20 yr 30 yr

Fixed Income

Mexder: Fixed Income Contracts

Bond Futures28-day TIIE

Futures Contracts

91-day Cetes

Futures ContractsInterest Rate

Swaps 2 yr / 10 yr

Ticker Symbol M3/M5/M10/M20/M30 TE28 CE91 SW2 /10 + Month

and Mat. Yr.

Quotation Price Interest Rate Interest Rate Interest Rate

Size 100 $100,000 MXN 10,000 Cetes ( $100,000 MXP) $1 Million MXN

Tick $0.025 MXN // $0.00208 USD* One bp (0.01) One bp (0.01) 0.5 bp

Notional Value $100,000 MXN// $8.333 USD* 100,000 MxN 100,000 MxN 1000,000 MxN

Maturity Months Quarterly, up to 3 years Monthly up to 10 yr

Monthly up to 12 months. Months and quarterly, up to 24 quarters

Monthly andQuarterly

Settlement Physical Delivery Differentials Differentials Physical Deliveryand Differentials

Trading Hours 8:30 – 15:00 hrs. EST

8:30 – 15:00 hrs. EST

8:30 – 15:00 hrs. EST

8:30 – 15:00 hrs. EST

Bloomberg(MMDD) DWA (CMDTY) CT DOA (CMDTY) CT GMA (CMDTY) CT SWTA (CMDTY) CT

R.30 – ReutersMXN/FUTEX1 0#B10: 0#T11: 0#CTE: 0#SW2 and

0#SW10

Worth mentioning is the fact that MBonos Futures are very liquid and trade at tight spreads.

MEXDER and its clearing firm ASIGNA already have a 2 and 10 years swap that can be “delivered/received” once the future expires directly using ASIGNA as a counterparty.

12

Fixed Income

Latin American FX Markets Turnover

Currency distribution of global foreign exchange market turnover

1. Mexico is positioned as the 13th most traded currency in the world.

2. It is the third most traded currency of the emerging economies, just below the Hong Kong dollar and the Korean won.

3. That makes the MXN the most traded currency in Latin America

Global FX Market Turnover

Note:

The graphics show the percentage shares of

average turnover in April of 2010. The sum of the

percentage shares of all the currencies add up to a total of 200%, instead of

100% because two currencies are involved in

each transaction.

Sources: Triennial Central Bank Survey, Bank for International Settlements

Emerging Markets

FX

13

0

10

20

30

40

50

60

70

80

90

US Dollar Euro JapaneseYen

Poundsterling

Australiandollar

Swissfranc

Canadiandollar

HongKongdollar

Swedishkrona

NewZelanddollar

Koreanwon

Singaporedollar

Norwegiankrone

Mexicanpeso

Othercurrencies

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Mexican peso Brazilian real Chilean peso Colombian peso Argentine peso Peruvian nuevo sol

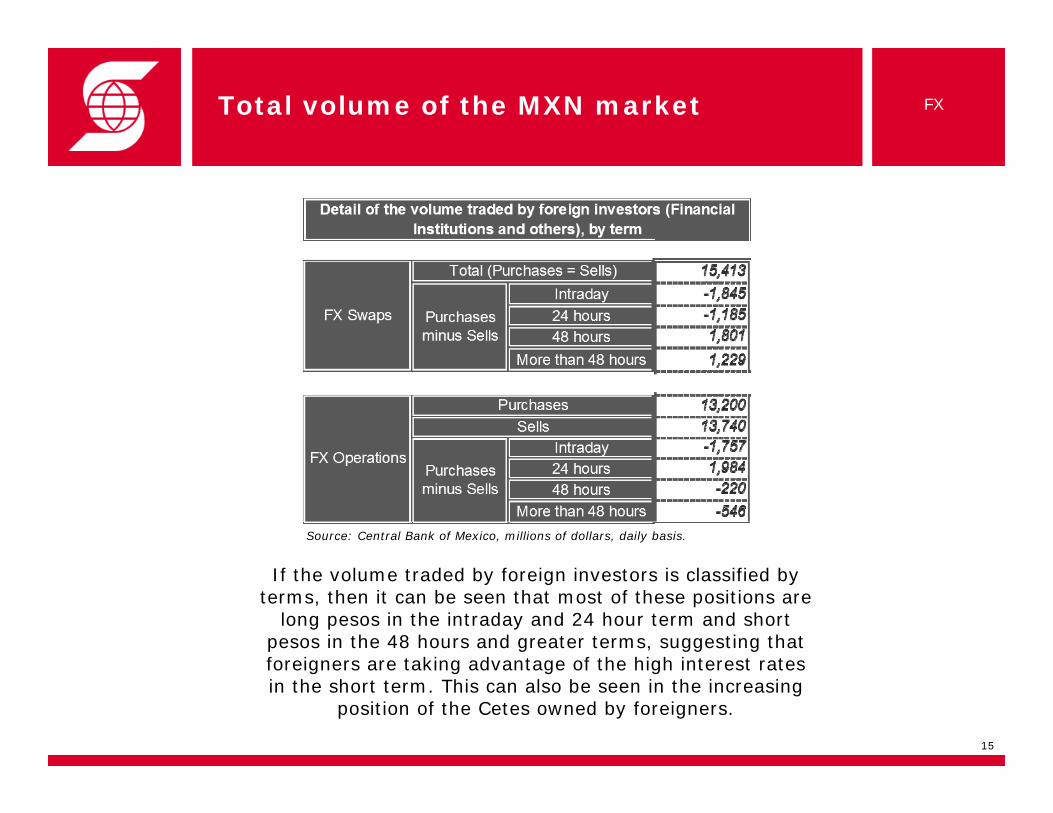

Total volume of the MXN market

The greatest amounts traded in the MXN market come fromforeign investors, who account for 95% of the volume in

swaps and 76% in cash and forward contracts.

Source: Central Bank of Mexico, millions of dollars, daily basis.

14

FX

Total volume of the MXN market

Source: Central Bank of Mexico, millions of dollars, daily basis.

If the volume traded by foreign investors is classified by terms, then it can be seen that most of these positions are

long pesos in the intraday and 24 hour term and short pesos in the 48 hours and greater terms, suggesting thatforeigners are taking advantage of the high interest ratesin the short term. This can also be seen in the increasing

position of the Cetes owned by foreigners.

15

FX

Central Bank’s monetary policy

How the Central Bank of Mexico intervenes in the FX market:• The Central Bank issues put options that can be exercised at the last day’s FIX, if this is not

greater than the average of the last 20 days’ FIX rate.

• The Central Bank auctions US$ 600 million by the end of each month, giving investors the opportunity to exercise the options throughout the next month.

• In this way, the Central Bank follows a less aggressive monetary policy than other countries in Latin America. Its policies bear some resemblance to those of Colombia.

0%

5%

10%

15%

20%

25%

30%

35%

Perú Chile Brasil Colombia México

16

International Reserves USD

Perú 46,352,600,000

Chile 34,208,100,000

Brasil 333,000,000,000

Colombia 30,420,000,000

México 129,203,000,000

International Reserves as a Percentage of the GDP

FX

MXN: Operating Factors

MXN: Operating Factors

• No Withholding Tax

• Settlement within 48hours most common; also quoted are intra-day and 24 hour settlement

• There is a very liquid futures market: OTC forward, CME Mexican Peso contract and Mexder USD contract

• Many brokers and matching systems available to trade Mexican Peso.

• Many foreign and local participants

• 24 hours trading

• Settlement should done by SWIFT

• Full delivery

MXN: Drivers

Factors that influence the MXN performance:

• High liquidity in the international economy

• Oil prices

• Economic fundamentals

• No direct intervention of the Central Bank in the FX Market

• Change in investors’ risk perception, which contributes to the daily volatility

17

FX

Mexder: Currency derivatives

MXN/USDFutures

MXN/EUROFutures

MXN/USDOptions

Ticker Symbol DA Euro DA

Quotation / Style Price Price European

Size $10,000 USD $10,000 EUROS $10,000 USD

Tick $0.0001 MXN $0.0001 MXN $0.001 MXN

Maturity Months Monthly, up to 3 years Monthly, up to 1 year Quarterly, up to 1 year

Settlement Physical delivery Non delivery, Differentials Physical delivery

Trading Hours 8:30 – 15:00 hrs. EST 8:30 – 15:00 hrs. EST 8:30 – 15:00 hrs. EST

Bloomberg (MMDD) DSA (CRNCY) CT BEA (CRCNY) CT MXX (CRCNY) OMON

R.30 – ReutersMXN/FUTEX1 0#MXP: 0 # EURO: 0 # DA:XD

Large Volume and High Open Interest are found in MXN/USD Futures.

18

FX

Returns on Emerging Market Indices

• The IPC is the benchmark equity index of the Mexican Stock Exchange (Mexbol): a capitalization-weighted index composed of the country’s 35 most liquid stocks

• Total market capitalization of the index was US$410 billion as of July 19, 2011

• Index members trade on the Mexbol between 9:30am and 4:00pm EST

• The index has posted a +17% CAGR over the prior 16 year period; the return on the MSCI index for Mexico was 12.6%.

19

Sources: Bloomberg

Ticker MSCI country indices16 YR CAGR

MEXICO 12.6%

RUSSIA 18.1%

INDIA 12.4%

BRAZIL 11.9%

CHINA 1.2%

Equity

MSCI EM vs MSCI MexicoYOY Returns

MSCI Emergent Markets MSCI Mexico

-90%

-70%

-50%

-30%

-10%

10%

30%

50%

70%

90%

110%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

IPC: Industries

20

• Members represent 17 different industries

• The largest five index members represent 56% of the index

• The main industry groups by market capitalization are Telecoms (28%), Retail (19%) and Mining (14%).

Sources: Bloomberg

Equity

Engineering & Construction

Telecommunications

Banks

Beverages

Retail

Mining

Real Estate Pharmaceuticals

Food

Building Materials

Chemicals

Diversified Financial Services

Forest Products & Paper

Holding Companies-Divers

Machinery-Diversified

Home Builders

Media

IPC: Traded Volume

• The top three stocks trade 48% of the total volume (AMX, GMEXICO and WALMEX) in the IPyC. The top ten stocks represent 76% of the index volume.

• In the LTM the index recorded an average daily trading volume of US$417 Million

21Sources: Bloomberg

2010: FIX 4.2

Aug.11: v4.4 protocol

Equity

0

100

200

300

400

500

600

700

800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

•Fully

electr

onic

tradin

g: FIX

proto

col, D

MA, rob

ots

•Sophis

ticate

d playe

rs

Daily Trading Volume (US$M)

Size of the Equity Local Market

• There are more than thirty brokerage houses in the country, including small and large firms. Fifteen of them (Scotia Capital included) account for ~80% of the traded volume.

• The International Quoting System (SIC in Spanish) trades more than 300 ETF’s and more than 280 foreign stocks.

• Among the holders of Mexican equities are foreign institutional investors such as US big pension funds, mutual funds, etc.

• The Naftrac, a local ETF which mirrors the performance of the IPC, is the most traded stock with a YTD ADTV of US$180 million.

22

Sources: Bloomberg

117

4738

3023 19 16

10 9 9

0

20

40

60

80

100

120

AmericanMovil

GroupoMexico

Walmex Cemex Gfnorte Televisa FEMSA GroupoLab

Corp GEO ALFA

Equity

Pension Funds: Equity Holdings

• Afores (Mexican pension funds) managed MXN1.46 trillion in June 2011

• As of June 2011, 18.1% of assets under management were invested in equities vs. 11.1% in November 2008.

23

87.6% 87.8%

86.7%86.1%

84.8%85.1%

85.8%85.1%

84.1%

83.3%

82.1% 82.3%82.0%

87.6%

89.1%

89.5%

89.3% 88.5%

87.7%

88.0%

87.0%

86.5%85.7%

86.0%

85.6%

84.7%84.6%

85.5%

82.7%82.9%

81.9%81.9%

% in Debt

11.5%12.0%

13.0% 13.3%13.9% 14.0%

15.3% 15.2%14.5% 14.2%

14.9%

15.9%16.7%

18.1% 17.7%18.0%18.1%17.9%

17.1%17.3%

14.9%15.4%

14.4%14.3%13.5%

12.2%12.3%

10.7%10.5%10.9%

12.4%12.4%

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Jan-10

Feb-10

Mar-10

Apr-10

May-10

Jun-10

Jul-10

Aug-10

Sep-10

Oct-10

Nov-10

Dec-10

Jan-11

Feb-11

Mar-11

Apr-11

May-11

Jun-11

% in Equity

Equity

24

Mexican ADR

Sources: Bloomberg

Ticker Short Name Shares per ADR

AMX US AMÉRICA MÓVIL 20

TMX TELMEX 20

CX US CEMEX 10

TV US GRUPO TELEVISA 5

FMX US FEMSA 10

ICA US EMPRESAS ICA 4

HXM US HOMEX 6

PAC US GAP 10

ASR US ASUR 10

OMAB US OMA 8

KOF US COCA COLA 10

SIM US GRUPO SIMEC 3

MIXT US MAXCOM 7

VITRY US VITRO 3

GMK US GRUMA 4

IBA US BACHOCO 12

Equity

Operative Factors

• Security lending is available

• Short selling is allowed to/through the Market Makers and/or Mexder

• Central counterparty “Indeval” clears, deposits and custodies all securities.

• Securities settlement in 72 hours

• Omnibus account allows non-disclosure of customer name

• Foreign investors settle stocks through Euroclear, Clearstream or DTC vs Indeval in Mexico.

• Foreigners and local customers must trade in local market through Mexican Brokerage Houses.

• Fully electronic exchange

• Electronic access should be negotiated with a Mexican Brokerage House

• Specific rules govern electronic access to the Exchange

• CBNV (The Mexican Sec) performs extensive audits to verify compliance with these rules

• Market makers exist for the less liquid stocks

25

Equity

Mexder: IPC

IPC

Futures

IPC

Options

Ticker Symbol IPC IP

Quotation/Style IPC points European

Size IPC*10 IPC x $10 MXN

Tick 5 points 1 point

Maturity Months Quarterly, up to 1 year Quarterly, up to 1 year

Trading Hours 8:30 – 15:00 hrs. EST 8:30 – 15:00 hrs. EST

Bloomberg (MMDD) ISA (INDEX) CT ISA (INDEX) OMON

R.30 – ReutersMXN/FUTEX1 0#IPC: 0#IPC:XD

Futures and Options for IPC and some individual stocks and Traccs.

IPC non action letter was issued by the CFTC.

The IPC futures and Options are the most active.

26

Equity

Mexder

MexDer, The Mexican Derivatives Exchange was launched in December 1998. It is fully electronic, and provides listings for financial futures and options on Mexican securities and indices.

In recent years, Mexder had the following important achievements:

MEXDERMarket Makers.

IPC contracts No actions letter.

Fix Connectivity

Remote Trading Membership

No Withholding tax

Order Routing Agreement with CME Group.

Non customer disclosure Omnibus accounts.

IRS Full Delivery Futures Available (Dodd-Frank Regulation).

Regulation Segregation between House trading and Customer trading (30.7)

Give ups.27

Dic99

Ago00

Abr01

Dic01

Ago02

Abr03

Dic03

Ago04

Abr05

Dic05

Dic07

Ago06

Abr07

Ago08

Ago10

Abr09

Dic09

Abr11

0

5

10

15

20

25

30

35

40

45

50

Vo

lum

e O

pera

do

/ V

olu

me T

rad

ed

0

5

10

15

20

25

30

35

40

45

50

55

60

Ineré

s A

bie

rto

/ O

pen

In

tere

st

Clearing House

28

• Asigna is the counterparty for all transactions performed on the market. It is evaluated and rated each year by three leading international rating agencies.

• Asigna is the best counterparty in Mexico.

Local Rating Global Rating

Fitch Rating AAA (mex)

Standard & Poor’s mxAAA/mxA-1+ local currency

BBB/A-3 foreign currency BBB/A-2 local currency

Moody’s AAA.MX A1

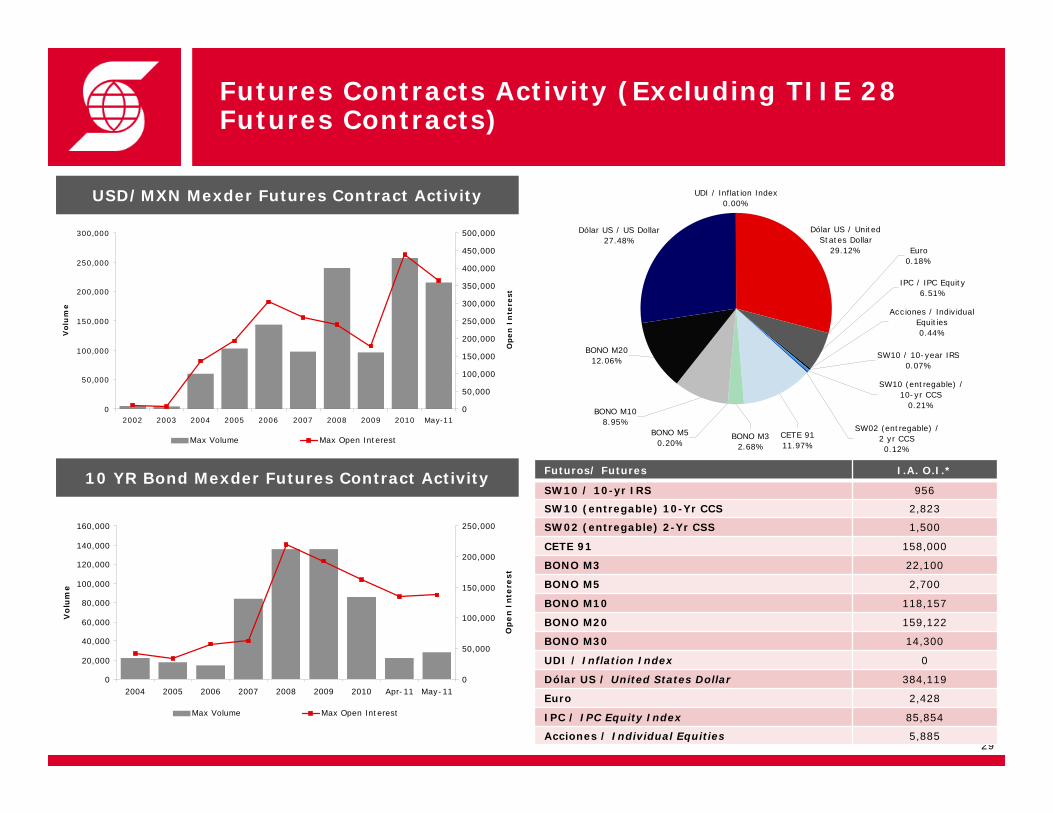

USD/MXN Mexder Futures Contract Activity

Futures Contracts Activity (Excluding TIIE 28 Futures Contracts)

10 YR Bond Mexder Futures Contract Activity

29

0

50,000

100,000

150,000

200,000

250,000

300,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 May-11

Volu

me

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

Open

In

tere

st

Max Volume Max Open Interest

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2004 2005 2006 2007 2008 2009 2010 Apr-11 May-11

Vo

lum

e

0

50,000

100,000

150,000

200,000

250,000

Op

en

Inte

rest

Max Volume Max Open Interest

UDI / Inflation Index0.00%

Dólar US / US Dollar27.48%

Acciones / Individual Equities0.44%

CETE 9111.97%

SW10 (entregable) / 10-yr CCS

0.21%

BONO M32.68%

BONO M50.20%

BONO M108.95%

SW10 / 10-year IRS0.07%

Euro0.18%

IPC / IPC Equity6.51%

SW02 (entregable) / 2 yr CCS0.12%

BONO M2012.06%

Dólar US / United States Dollar

29.12%

Futuros/ Futures I.A. O.I.*

SW10 / 10-yr IRS 956

SW10 (entregable) 10-Yr CCS 2,823

SW02 (entregable) 2-Yr CSS 1,500

CETE 91 158,000

BONO M3 22,100

BONO M5 2,700

BONO M10 118,157

BONO M20 159,122

BONO M30 14,300

UDI / Inflation Index 0

Dólar US / United States Dollar 384,119

Euro 2,428

IPC / IPC Equity Index 85,854

Acciones / Individual Equities 5,885

Why Scotia for MexDer?

• Scotia Capital, the corporate and investment banking, and capital markets, businesses of the Scotiabank Group, is a full service clearing and execution provider in Mexico for all Futures and Options products listed on the Mexican Derivatives Exchange (MexDer).

• As one of the most technologically advanced clearing members in Mexico, Scotia provides its clients with access to a wide range of services including Direct Electronic Access to the Mexican derivatives market through our broker, Scotia Derivados, and STP solution.

Some Clearing Services:

A committed team of professionals focused on customized solutions for our clients.

Excellent execution and B/O systems.

On-line information and end-of the day reports via internet.

Opening an account takes a short time.

Competitive Commissions.

Effective, fast and safe client acceptance methodology.

Compliance and Anti Money Laundering Culture

Local Flavor and Research Reports.

WE WILL BE GLAD TO ATTEND TO YOUR NEEDS AS YOUR CLEARING MEMBER IN MEXDER.

30

Scotiabank Group: Products, Services and Credit Ratings

BANK• Personal, Commerical and Corporate Banking• Wealth and Cash Management Services

INVESTMENT BANK (SCOTIA CAPITAL)• Equities• Custody Services• Technical and Fundamental Research• Corporate Finance ( Active in IPO Deals)• Money Market• Capital Markets• OTC Derivatives• Equity Derivatives• Securities Lending / Borrowing

31

SCOTIABANK Long Term CREDIT RATING:The Bank of Nova Scotia (Scotiabank)is AA-.Scotiabank Inverlat Mexico MA AAA.

SCOTIABANK Short Term CREDIT RATING:The Bank of Nova Scotia (Scotiabank)is A-1+.Scotiabank Inverlat Mexico A-3

*Not all services are available in all jurisdictions.

Scotia Capital Mexico Contacts

Head Markets, Scotia Capital Mexico

Carlos Kretschmer+52 55 [email protected]

Derivatives Sales (Mexder)

Guillermo Camou+52 55 [email protected]

Lorena Pichardo+52 55 [email protected]

Angélica Aguilar+52 55 [email protected]

Fixed Income Sales

Jorge González+52 55 [email protected]

José González Funes+52 55 [email protected]

Equity Sales

Bond Snodgrass+52 55 [email protected]

Fixed Income and Derivatives Trading

Carlos HernándezHead Fixed Income and Derivatives +52 55 [email protected]

Alejandro MoralesFixed Income+52 55 [email protected]

Miguel MartínezFixed Income Derivatives+52 55 [email protected]

Equity and Derivatives Trading

Gabriel VegaHead Equity+52 55 [email protected]

FX Trading

Lorena Nuñez Director Head FXome+52 55 [email protected]

FX Sales

Manuel RosalesFX+52 55 9179.51 [email protected]

FX Sales

Emerging Markets Strategy

Joe Kogan, Head of [email protected]

Araceli [email protected]

Leonor [email protected]

Rebeca Lizá[email protected]

Equity Research

Marcos Durá[email protected]

Rodrigo EchagarayRetail+52.55.9179.5236rodrigo_echagaray@scotiacapital.com

Andrés [email protected]

32

Scotia Capital Emerging Markets NY Contacts

Emerging Markets Sales

Tarik [email protected]

Ralph [email protected]

Percy [email protected]

Wendy [email protected]

Emerging Markets Trading

Bill [email protected]

Ryan [email protected]

Drew [email protected]

Fredrik [email protected]

Patrick O’[email protected]

Emerging Markets Strategy

Joe Kogan, Head of [email protected]

33

Disclaimer

This publication has been prepared for Institutional Investors by Fixed Income Strategists of Scotia Capital (USA) Inc. (“Scotia Capital”). Fixed Income Strategists are employees of Scotia Capital’s Fixed Income Credit Sales & Trading Desk and support the trading desk through the preparation of market commentary, including specific trading ideas, and other materials, both written and verbal, which may or may not be made publicly available, and which may or may not be made publicly available at the same time it is made available to the Fixed Income Credit Sales & Trading Desk. Fixed Income Strategists are not research analysts, and this report was not reviewed by the Research Departments of Scotia Capital. Fixed Income Strategist publications are not research reports and the views expressed by Fixed Income Strategists in this and other reports may differ from the views expressed by other departments, including the Research Department, of Scotia Capital. The securities laws and regulations, and the policies of Scotia Capital that are applicable to Research Analysts may not be applicable to Fixed Income Strategists.

This publication is provided to you for informational purposes only. Prices shown in this publication are indicative and Scotia Capital is not offering to buy or sell, or soliciting offers to buy or sell any financial instrument. Scotia Capital may engage in transactions in a manner inconsistent with the views discussed herein. Scotia Capital may have positions, or be in the process of acquiring or disposing of positions, referred to in this publication. Other than the disclosures related to Scotia Capital, the information contained in this publication has been obtained from sources that Scotia Capital knows to be reliable, however we do not represent or warrant that such information is accurate and complete. The views expressed herein are the views of the Fixed Income Strategists of Scotia Capital and are subject to change, and Scotia Capital has no obligation to update its opinions or information in this publication. Scotia Capital and any of its officers, directors and employees, including any persons involved in the preparation or issuance of this document, may from time to time act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market-makers or advisors, brokers or commercial and/or investment bankers in relation to the securities or related derivatives which are the subject of this publication.

Neither Scotia Capital nor any of its officers, directors, partners, or employees accepts any liability for any direct or consequential loss arising from this publication or its contents. The securities discussed in this publication may not be suitable for all investors. Scotia Capital recommends that investors independently evaluate each issuer and security discussed in this publication, and consult with any advisors they deem necessary prior to making any investment. 34