Eurobond Press Briefing Aug 12 Press Version

17

Press Conference on 12 August 2013 1 THE GHANA 2013 EUROBOND TRANSACTION

Transcript of Eurobond Press Briefing Aug 12 Press Version

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 1/17

Press

Conference on

12 August2013

1

THE GHANA 2013

EUROBONDTRANSACTION

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 2/17

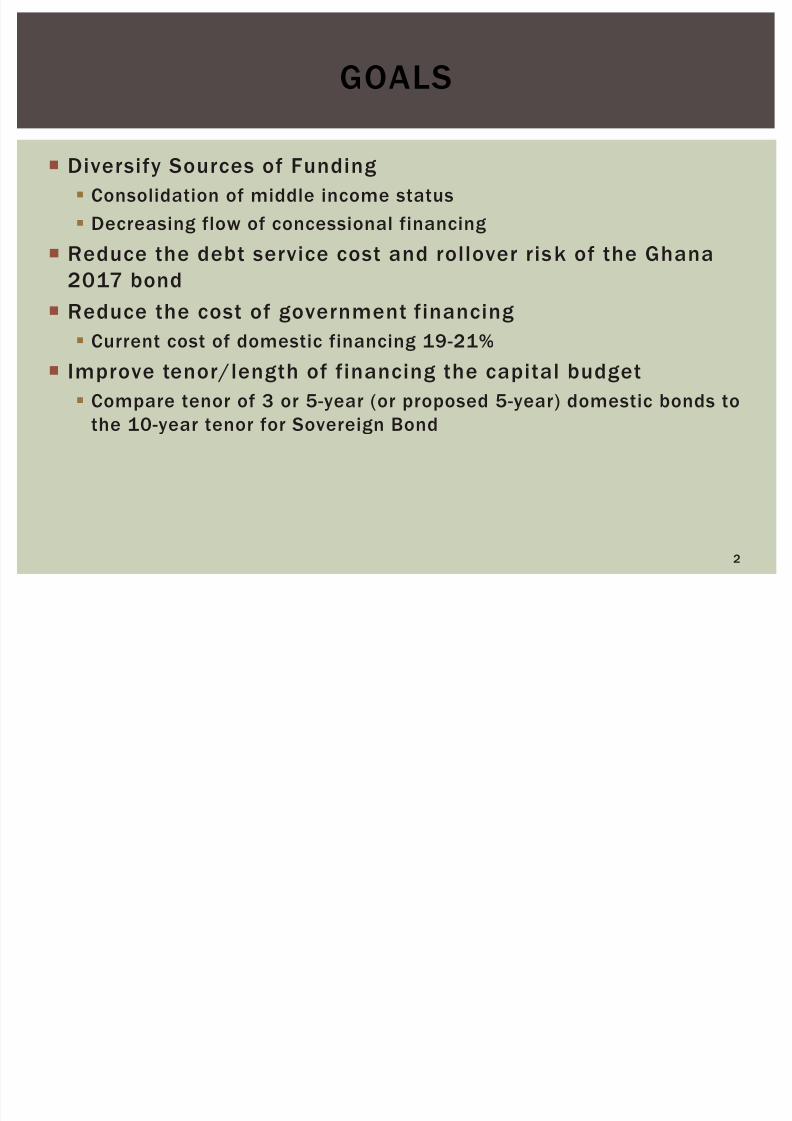

Diversify Sources of Funding

Consolidation of middle income status

Decreasing flow of concessional financing

Reduce the debt service cost and rollover risk of the Ghana

2017 bond

Reduce the cost of government financing

Current cost of domestic financing 19-21%

Improve tenor/length of financing the capital budget

Compare tenor of 3 or 5-year (or proposed 5-year) domestic bonds to

the 10-year tenor for Sovereign Bond

2

GOALS

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 3/17

3

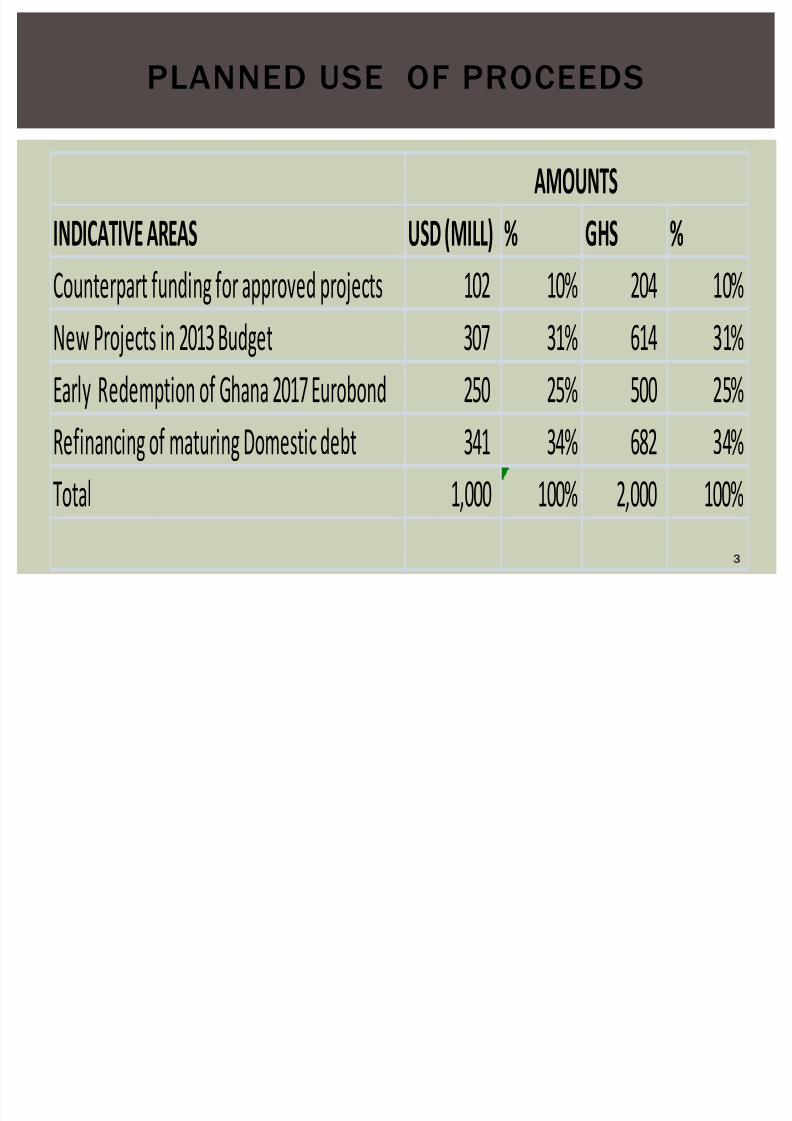

PLANNED USE OF PROCEEDS

INDICATIVE AREAS USD (MILL) % GHS %

Counterpart funding for approved projects 102 10% 204 10%

New Projects in 2013 Budget 307 31% 614 31%

Early Redemption of Ghana 2017 Eurobond 250 25% 500 25%

Refinancing of maturing Domestic debt 341 34% 682 34%

Total 1,000 100% 2,000 100%

AMOUNTS

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 4/17

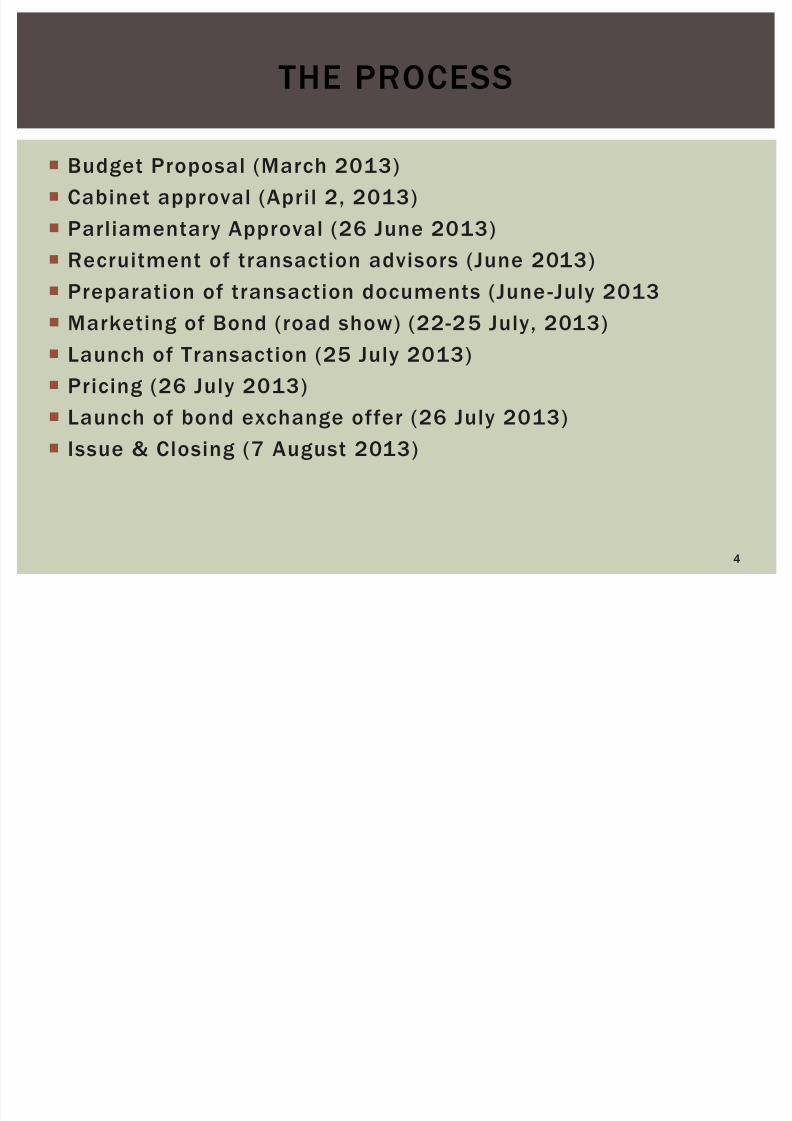

Budget Proposal (March 2013)

Cabinet approval (April 2, 2013)

Parliamentary Approval (26 June 2013)

Recruitment of transaction advisors (June 2013)

Preparation of transaction documents (June -July 2013

Marketing of Bond (road show) (22-25 July, 2013)

Launch of Transaction (25 July 2013)

Pricing (26 July 2013)

Launch of bond exchange offer (26 July 2013)

Issue & Closing (7 August 2013)

4

THE PROCESS

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 5/17

Lead Managers (Citigroup, Barclays)

Co-Managers (EDC Stockbrokers, Strategic African Securities)

International legal counsel (Denton’s)

Local legal counsel (JLD & MB)

Government of Ghana Transaction Committee (MoF, Bank of Ghana)

5

TRANSACTION TEAM

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 6/17

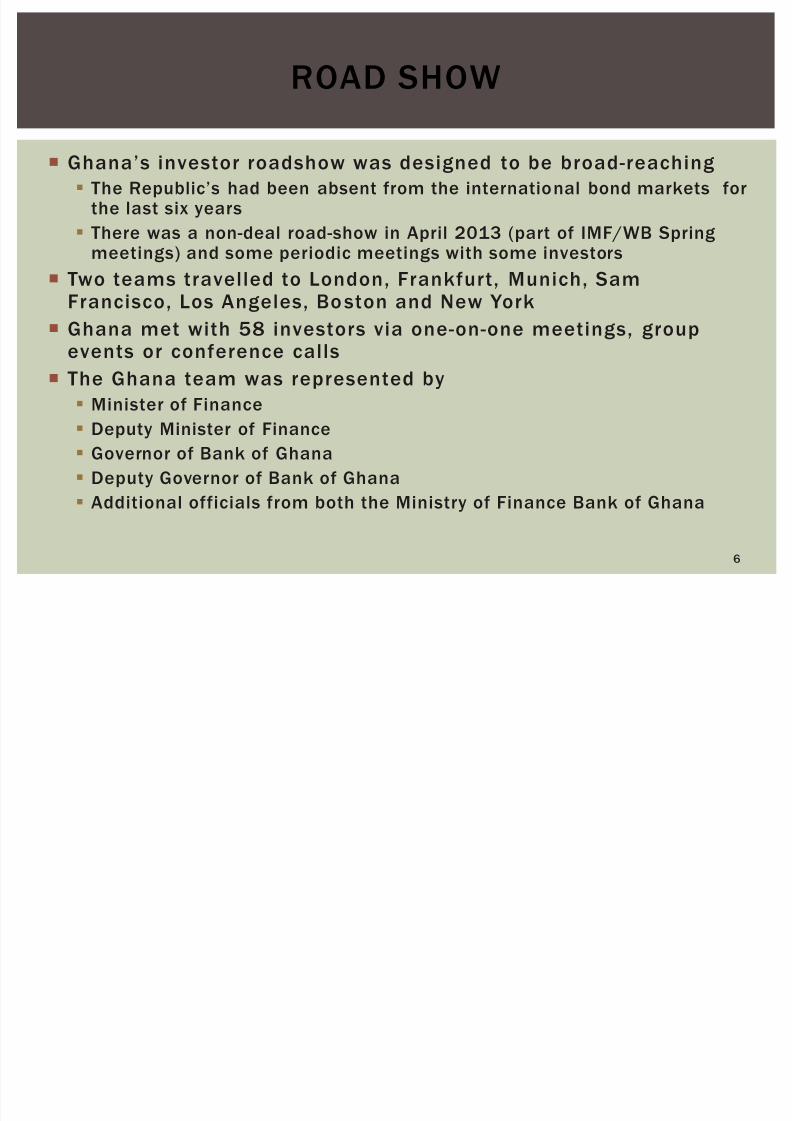

Ghana’s investor roadshow was designed to be broad-reaching

The Republic’s had been absent from the international bond markets forthe last six years

There was a non-deal road-show in April 2013 (part of IMF/WB Springmeetings) and some periodic meetings with some investors

Two teams travelled to London, Frankfurt, Munich, SamFrancisco, Los Angeles, Bo ston and New York

Ghana met with 58 investors via one-on-one meetings, groupevents or conference calls

The Ghana team was represented by

Minister of Finance

Deputy Minister of Finance

Governor of Bank of Ghana

Deputy Governor of Bank of Ghana

Additional officials from both the Ministry of Finance Bank of Ghana

6

ROAD SHOW

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 7/17

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 8/17

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 9/17

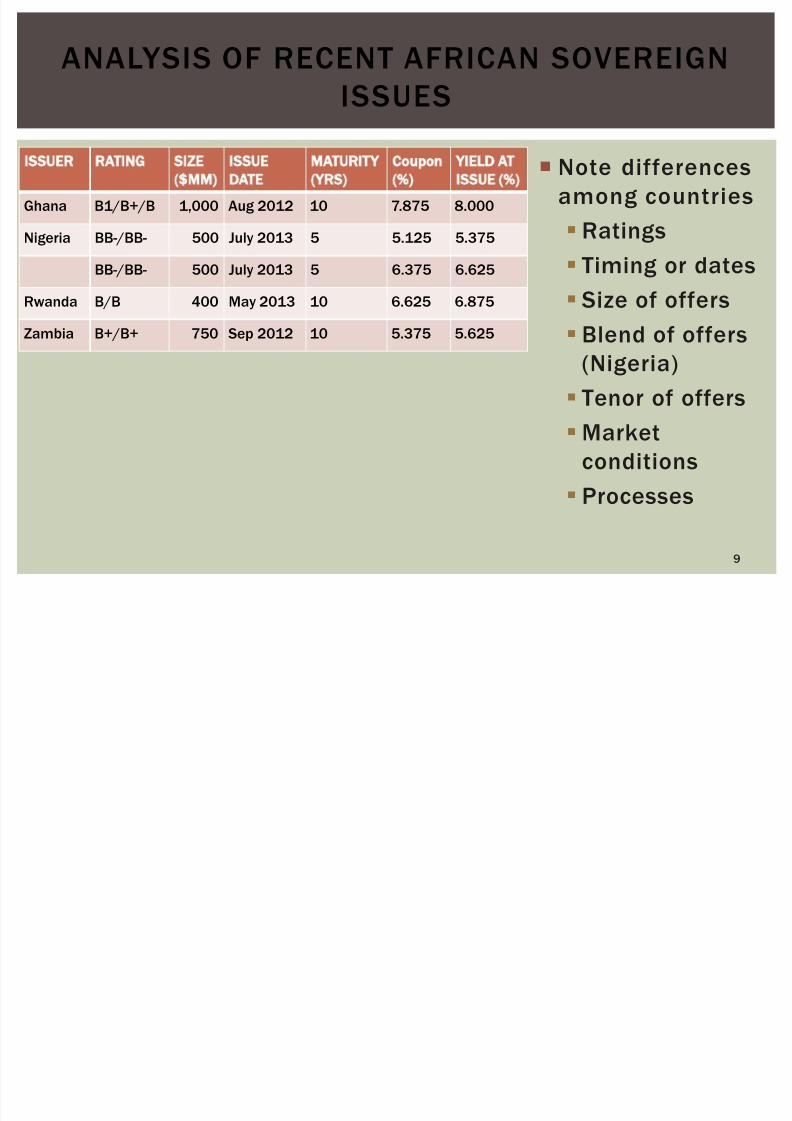

ISSUER RATING SIZE

( MM)

ISSUE

DATE

MATURITY

(YRS)

Coupon

(%)

YIELD AT

ISSUE (%)

Ghana B1/B+/B 1,000 Aug 2012 10 7.875 8.000

Nigeria BB-/BB- 500 July 2013 5 5.125 5.375

BB-/BB- 500 July 2013 5 6.375 6.625

Rwanda B/B 400 May 2013 10 6.625 6.875

Zambia B+/B+ 750 Sep 2012 10 5.375 5.625

Note differences

among countries

Ratings

Timing or dates Size of offers

Blend of offers

(Nigeria)

Tenor of offers

Market

conditions

Processes

9

ANALYSIS OF RECENT AFRICAN SOVEREIGN

ISSUES

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 10/17

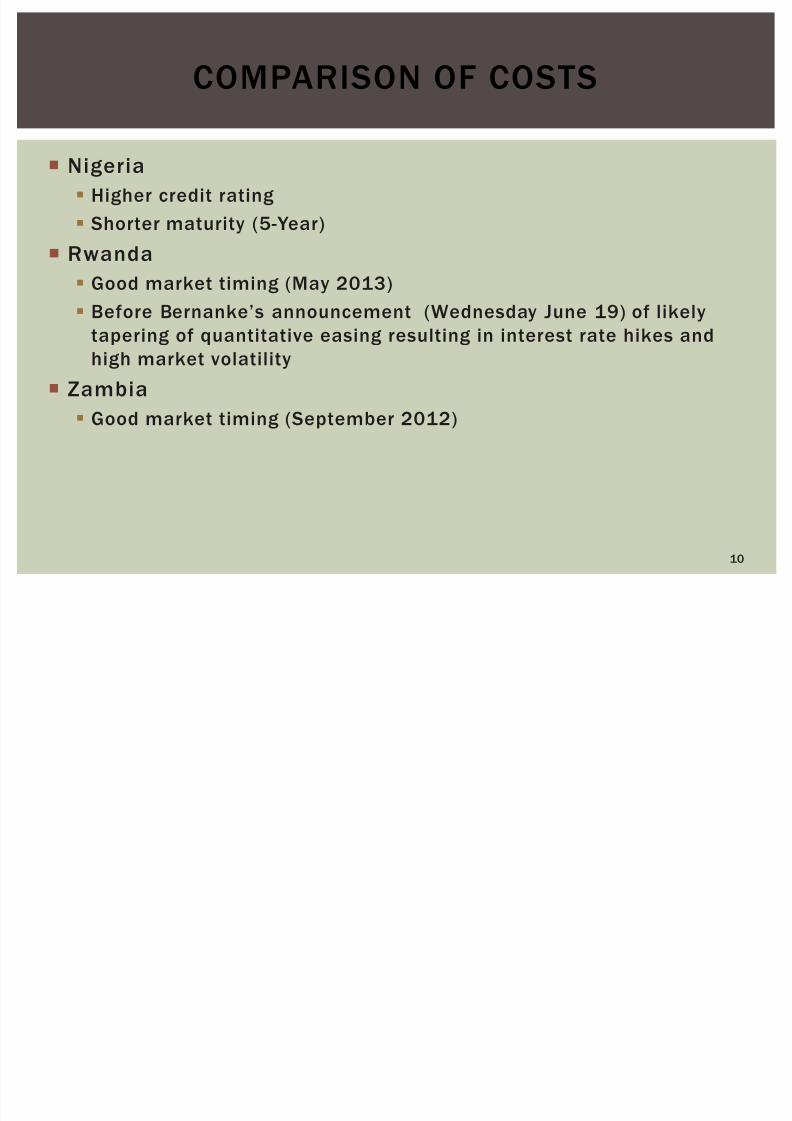

Nigeria

Higher credit rating

Shorter maturity (5-Year)

Rwanda

Good market timing (May 2013)

Before Bernanke’s announcement (Wednesday June 19) of likely

tapering of quantitative easing resulting in interest rate hikes and

high market volatility

Zambia

Good market timing (September 2012)

10

COMPARISON OF COSTS

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 11/17

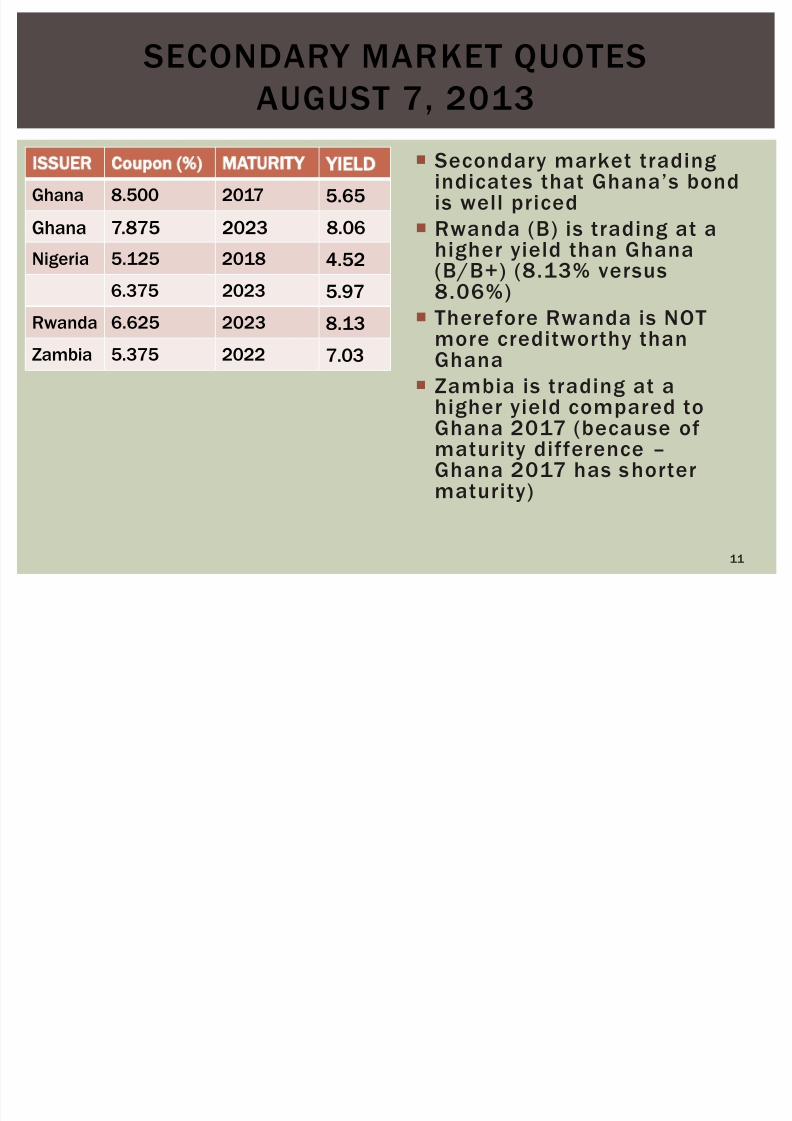

ISSUER Coupon (%) MATURITY YIELD

Ghana 8.500 2017 5.65

Ghana 7.875 2023 8.06

Nigeria 5.125 2018 4.52

6.375 2023 5.97

Rwanda 6.625 2023 8.13

Zambia 5.375 2022 7.03

Secondary market tradingindicates that Ghana’s bondis well priced

Rwanda (B) is trading at ahigher yield than Ghana

(B/B+) (8.13% versus8.06%)

Therefore Rwanda is NOTmore creditworthy thanGhana

Zambia is trading at a

higher yield compared toGhana 2017 (because ofmaturity difference – Ghana 2017 has shortermaturity)

11

SECONDARY MARKET QUOTES

AUGUST 7, 2013

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 12/17

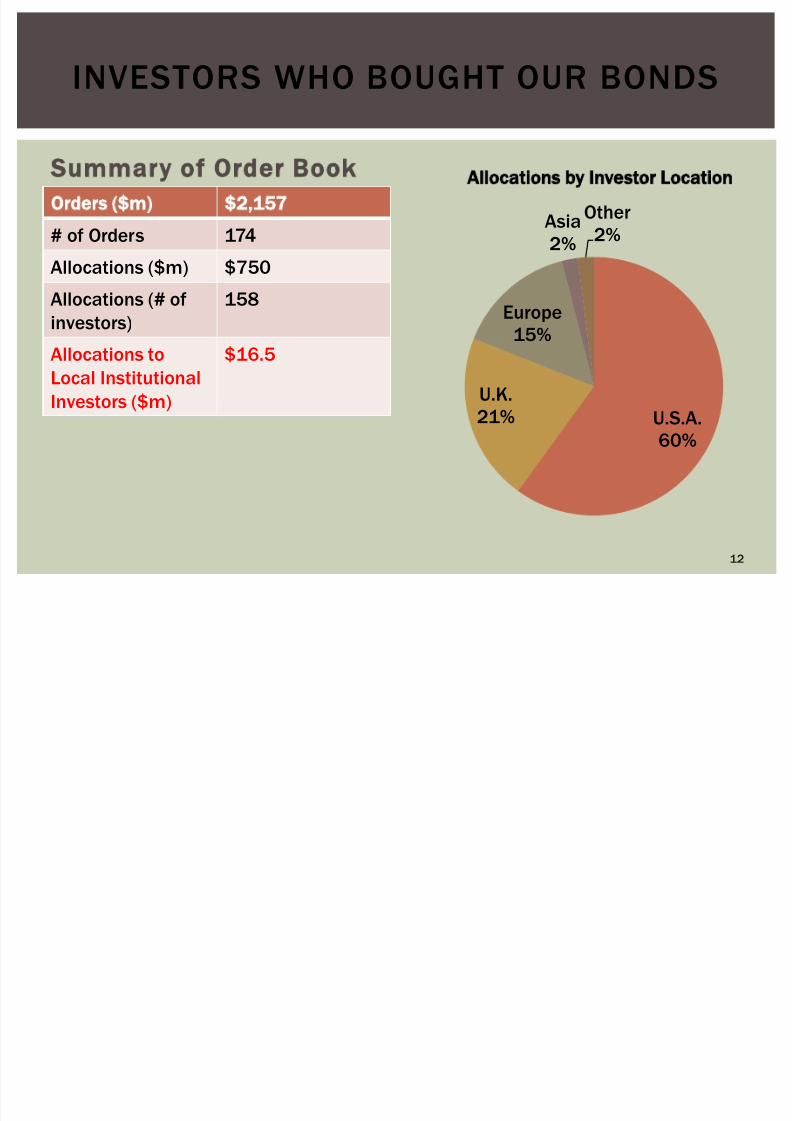

INVESTORS WHO BOUGHT OUR BONDS

Summary of Order Book

Orders ( m) 2,157

# of Orders 174

Allocations ($m) $750

Allocations (# of

investors)

158

Allocations to

Local Institutional

Investors ($m)

$16.5

U.S.A.60%

U.K.

21%

Europe15%

Asia

2%

Other

2%

Allocations by Investor Location

12

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 13/17

Ghana became the first Sub-Saharan African country

(excluding South Africa) to use the Eurobond market to

manage its overall debt by:

Reducing cost

Reducing the risk of rollover Ghana 2017 is a bullet bond repayable in October 2017

Risk of high interest rate or uncertain market access

Prudent to initiate an orderly retirement to reduce market

risks of rollover

13

MANAGING OUR DEBT MORE EFFICIENTLY

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 14/17

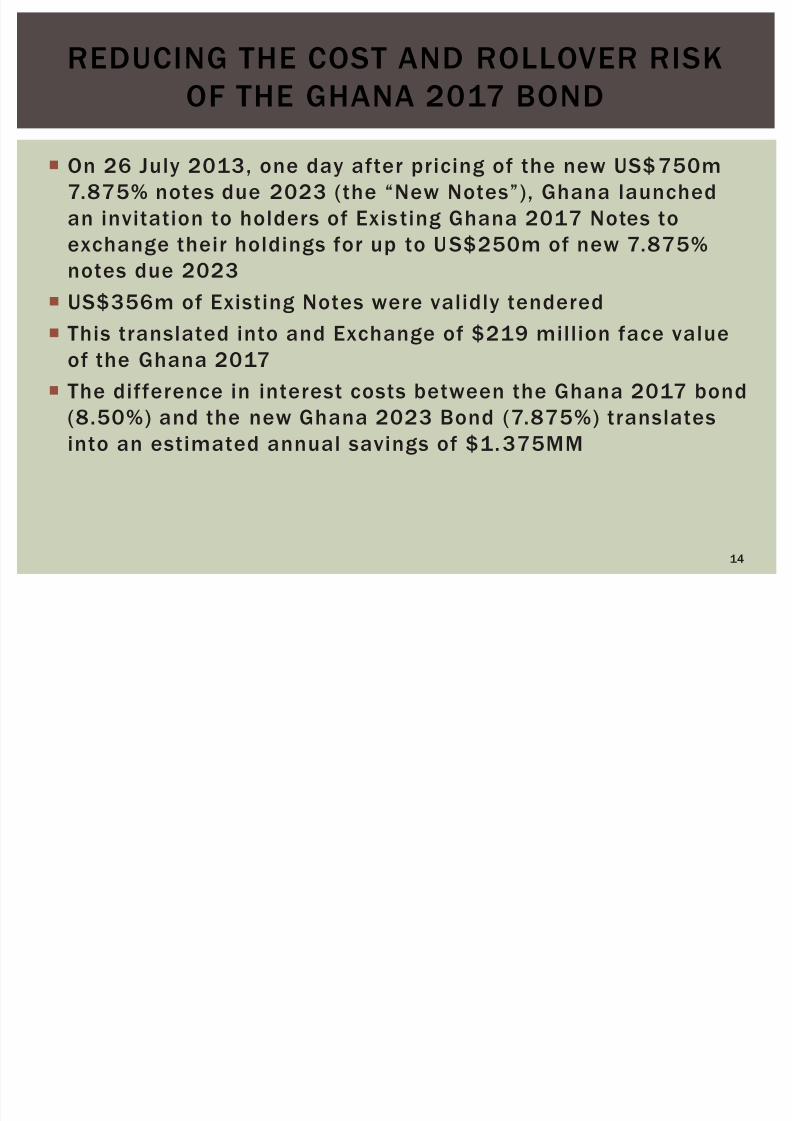

On 26 July 2013, one day after pricing of the new US$750m

7.875% notes due 2023 (the “New Notes”), Ghana launched

an invitation to holders of Exis ting Ghana 2017 Notes to

exchange their holdings for up to US$250m of new 7.875%

notes due 2023 US$356m of Existing Notes were validly tendered

This translated into and Exchange of $219 million face value

of the Ghana 2017

The difference in interest costs between the Ghana 2017 bond

(8.50%) and the new Ghana 2023 Bond (7.875%) translatesinto an estimated annual savings of $1.375MM

14

REDUCING THE COST AND ROLLOVER RISK

OF THE GHANA 2017 BOND

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 15/17

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 16/17

Ghana achieved its financing objectives with the transaction

Extended Ghana’s maturity profile

Reduced the rollover risk of the Ghana 2017 bond

Raised cost effective funds to refinance high-cost domestic term debt

Set a new benchmark and achieved a lower coupon than Ghana’sdebut 10-year USD bond

Listing of notes on the Ghana Stock Exchange, facilitating access for

local investors.

First sub-Saharan African country (excluding South Africa) to listed its

Eurobond on the local stock Exchange

Ghanaian institutional investors (banks, insurance companies, pension

funds) participated in the offer.

16

CONCLUSION

8/12/2019 Eurobond Press Briefing Aug 12 Press Version

http://slidepdf.com/reader/full/eurobond-press-briefing-aug-12-press-version 17/17

Debt policy will be guided by the principle of financing capital

expenditures with domestic and international long-term debt

(the upcoming debut issue of a domestic seven -year bond

reflects this policy)

Project specific bonds will be raised for self -financing projectswhile general conventional bonds will be raised for other

capital expenditures

Ghana will continue to source concessional financing for

social infrastructure.

17

LOOKING AHEAD