ESG - Allianz · ESG matters Environmental, Social and Governance ... mobile payments, and cloud...

32

ESG matters Environmental, Social and Governance thought piece Issue 13 FinTech: Buzzing about Blockchain Understand. Act. 04 The Dao: Do nothing, and nothing is left undone by Robbie Miles 12 Methane emissions: The next frontier for the Oil & Gas industry by Marie-Sybille Connan 18 Dialogue between shareholders and the German supervisory boards by Henrike Kulmann 20 How does ESG affect the credit rating of corporate bonds? by Dr. Steffen Hörter

Transcript of ESG - Allianz · ESG matters Environmental, Social and Governance ... mobile payments, and cloud...

ESGmattersEnvironmental, Social and Governance thought piece

Issue 13

FinTech: Buzzing about Blockchain

Understand. Act.

04 The Dao: Do nothing, and nothing is left undone by Robbie Miles

12 Methane emissions: The next frontier for the Oil & Gas industry by Marie-Sybille Connan

18 Dialogue between shareholders and the German supervisory boards by Henrike Kulmann

20 How does ESG affect the credit rating of corporate bonds? by Dr. Steffen Hörter

2

The Global ESG Team

LONDON

Eugenial Jackson,Head of ESG Research

Marissa Blankenship, ESG Analyst

Robbie Miles, ESG Analyst

PARIS

Marie-Sybille Connan, ESG Analyst

Mathilde Moulin, ESG Analyst

FRANKFURT

Henrike Kulmann, ESG Analyst

Rainer Sauer, Proxy Voting Specialist

CONTACT DETAILS

For any further information please contact:

Eugenia Jackson

Head of ESG Research

+44 20 3246 7134

www.esgmatters.co.uk

Editorial

Emma-Louise Allen, Allianz Global Investors

Design and Art Direction

Susan Lane, Allianz Global Investors

Imagery

Getty Images, iStockphoto

Allianz Global Investors GmbH, UK Branch

199 Bishopsgate

London EC2M 3TY

www. allianzglobalinvestors.co.uk

+44 20 7859 9000

© 2016 Allianz Global Investors

All rights reserved

Dear reader

Welcome to the 13th edition of ESG matters. The lead article by Marissa Blankenship investigates the development and merits of Blockchain and the regulatory hurdles that this technology will have to overcome before widespread application within the financial industry is possible. Robbie Miles explores the world of the DAO: a business model that breaks all conventions about how a company works, combining the two recent major technology innovations of Blockchain and Crowdfunding.

Further to our special edition on Climate Change in November of last year, Marie-Sybille Connan in her latest article, raises awareness about Methane emissions and argues that any strategy on climate change should tackle both Carbon Dioxide and Methane emissions in order to limit global warming.

Henrike Kulmann discusses a recent initiative in Germany which aims to increase dialogue between shareholders and supervisory boards members of listed companies. While meetings with the non-executive board members are becoming business as usual in the United Kingdom, such exchanges are currently the exception rather than the rule in Germany.

Finally, this edition closes with an extract from the latest whitepaper by Dr. Steffen Hörter (Global Head of ESG) and his team, the aim of this paper is to find evidence of the material effect of ESG dimensions in the performance of listed corporate bonds. For this edition we have taken a short extract from the paper which looks at how ESG affects the credit ratings of listed companies’ bonds.

We hope you enjoy reading this edition of ESG matters.

As always we are happy to discuss any comments or address any questions that you may have about our magazine.

Eugenia Jackson

Head of ESG Research

Eugenia JacksonHead of ESG Research

3

EXECUTIVE PAY

Contents

ESG Matters | Issue 13

04

20

08

04 The DAO: Do nothing, and nothing is left undone

08 FinTech: Buzzing about Blockchain

12 Methane emissions: The next frontier for the Oil & Gas industry

18 Communication is key: dialogue between shareholders and German supervisory boards

20 How does ESG affect the credit rating of corporate bonds?

12 18

4

The DAO: Do nothing, and nothing is left undoneA leaderless collective, automated by a set of laws enshrined in its algorithms. ROBBIE MILES examines the world of the DAO and how it is inspiring a radically new type of governance structure.

The DAO/Section 1

5

The DAO, or ‘Decentralised Autonomous Organisation’, is a business model that breaks all conventions about how a company works. It combines the ideology of decentralised organisational power with two major tech innovations; blockchain (for more information please refer to our lead article ‘Blockchain: more than just Bitcoin’ by Marissa Blankenship) and crowdfunding. In doing so, it opens the door to a potentially radical new era of commerce, law and politics and with them a host of new risks. The DAO is the largest ever crowdsourcing project, yet employs no-one. It works by allocating a

Robbie MilesESG Analyst London

ESG Matters | Issue 13

digital currency called ‘Etheruem’ (invented by a coder named Vitalik Buterin when he was a mere teenager) to projects worthy of investment, a bit like an automated venture capital fund.

Insinuated by its name, parallels can be drawn between the DAO and an ancient philosophy known as Taoism. The Tao (pronounced the same) refers to the spontaneous way the universe works according to the spiritual philosophy of Taoists. While the ways of the Tao technically cannot be described with words, they are alluded to in metaphors. For example, a

6

THE DAO/SECTION 1

cherry tree, without any assertion of will, grows deep roots and its branches grow tall. As if by doing nothing, the tree silently forms cherries. Without claim or praise; it fulfils its purpose. This is ‘non-action’. The cherry tree is governed by the universal laws of nature. Similarly, the DAO is automated by its own laws; its immutable algorithms. Nothing needs to be done by the organisation, yet nothing in the DAO’s cyber universe is left undone.

When it launched, the leaderless collective raised a record-breaking USD150m via crowdfunding from 20,000 individuals who believed in the investment potential that the DAO was offering. To invest, one buys ‘Ether’ a cryptocurrency (currently trading for around USD11.76 each, as at 10/10/16) and then exchanges these for voting shares called ‘DAO tokens’. The investor can use these tokens to vote on projects on The DAO’s platform that they believe to be worthy of investment. When sufficient votes are received, the projects, which have their own unique smart contracts, fulfill their stated objectives. These objectives may be to generate a return for the DAO, create products and services the DAO can use or may simply support charitable causes. Any returns are either reinvested or distributed to token holders, depending on votes of the token holders.

Conceptually, using smart contracts enables the disintermediation of lawyers because the contracts are undisputable and enforce themselves. In reality though, this immutability can cause big problems. If the code that creates such a contract contains a defect, it can be manipulated for self-interest by a hacker with very few remedial options available to the victim(s). The DAO’s designers

were criticized for launching too hastily, without carrying out necessary security checks. The criticism was prophetic: in June 2016, two months after launch, the DAO was hacked and USD60m of Ethereum was stolen as vulnerability in the DAO’s code was exploited. This was not the only theft of a digital currency. Bitfinex, one of the largest exchanges for Bitcoin, was hacked in August 2016 with USD71 million being stolen, sending the price of a Bitcoin plunging 20%. Stealing from a DAO isn’t even necessarily illegal as some argue the DAO operates independently of legal systems. This gives investors very little security if things go wrong. The token holders in the DAO are given code name, as shown in the ownership graph on the next page, giving them complete anonymity, making it very hard for any national government to know who to prosecute.

This attack may well prove to be the death knell for The DAO, but the concept is far from dead. It would not be the first time that a ground-breaking concept has failed in its first iteration. In 1997, seven years before the launch of Facebook, a social networking site named SixDegrees.com offered its users a platform to create profiles, invite friends, view other’s profiles and organise groups. At its peak, the site attracted 3.5 million members but pushy marketing e-mails began to put off users. The site ultimately failed but the idea of social networking went on to change the world.

If the design flaws can be ironed out, decentralised autonomous organisations could have profound implications for society. Beyond being a disruptive model of venture capital, the DAO offers an example of a radically new form of corporate governance. The DAO’s

“ The DAO’s white paper outlines two fundamental problems with corporate governance: (1) people do not always follow the rules and (2) people do not always agree what the rules actually require. ”

Vitalik Buterin on day one of Devcon two in Shanghai.

7

ESG Matters | Issue 13

white paper outlines two fundamental problems with corporate governance: (1) people do not always follow the rules and (2) people do not always agree what the rules actually require. Their solution is to automate and formalize governance rules by embedding them in the code that automates the platform and also allow investors to “maintain direct real-time control of contributed funds”. With perfect financial transparency and no human decision makers to be tempted by self-interest, the agency risk between a corporation’s management and its shareholders would vanish. An entity that IPO’s as a DAO could allow shareholders to participate in organisational governance directly and regularly, rather than once a year by proxy vote or AGM attendance, improving the stewardship a company receives. It could create wealth creation opportunities for anyone with an internet connection, even those at the bottom of the pyramid. For example, a business with this DAO structure could IPO to 100 million shareholders, each contributing just a few pennies. The flexibility in the design of the decentralized structures will allow people to build entirely new applications that couldn’t have been built on top of conventional financial and legal infrastructure1. This new model, where investors vote on which contracts to fulfil, could lead to organisations that simply contract out tasks on behalf of a highly active shareholder base – no employees are needed.

The DAO was ultimately conceived with a desire to find a way of making more decentralised decisions. For example, one alternative that emerged after Brexit was a website called referendum.nl, which offers a glimpse of the benefits of direct democracy when combined with ‘range voting’, where voters can express the strength of their

conviction. Further down the line, there could come a point when artificial intelligence, such as IBM Watson, which is designed to find the best possible answers by analysing vast quantities of data, becomes a more attractive alternative to the votes of the disillusioned public. There are certainly a lot of sustainability issues created by the short-termism in policies that are inherent in a 4-year political cycle. Tweaking these models and harnessing technology to achieve long-term/bi-partisan/international agreement on intergenerational issues such as climate change would be a great way of addressing society’s toughest challenges.

What is clear is that developments in this area will be important to monitor but there are teething problems to resolve before these ideas are applied elsewhere and enjoy mass adoption. The coded design of these new structures must undergo rigorous testing to iron out the vulnerabilities that have plagued The DAO since its inception. With headlines of robbery and lawlessness, it feels more like the Wild West than a viable alternative to traditional governance but the DAO’s rapid ascension into the forefront of the tech world’s consciousness is a watershed moment for autonomous organisations. Less than a year old, this innovative model already has a rich story and imitators will follow.

1 The Future of Business: Critical Insights into a Rapidly Changing World from 60 Future Thinkers. Rohit Talwar, 2015.

87.02%

1.62%

0.87%0.71%0.69%

0.65% 0.48%0.43%

0.35%0.35%4.18%

The Dao Top 100 Token Holders

0xbf4ed7b27f1d666546e30d74d50d173d20bca754

0x0a869d79a7052c7f1b55a8ebabbea3420f0d1e13

0xfc361105dd90f9ede566499d69e9130395f12ac8

0x88bbf6f5ba896262d80dbbe3597d09c817fd1475

0x525784459b8926722b9137eddb5611ab346e8510

0xb1179589e19db9d41557bbec1cb24ccc2dec1c7f

0x5c4973d33fb982000fad5765b684d22b298b97aa

0x5816c2687777b6d7d2a2432d59a41fa059e3a406

0xdf21fa922215b1a56f5a6d6294e6e36c85a0acfb

0x17ef4acc1bf147e326749d10e677dcffd76f9e06

Token holders 11-100

Source: Etherscan.io – The Ethereum Blockchain explorer

8

FinTech: Buzzing about Blockchain

In the past two years, in terms of financial innovation, Blockchain has surged past cyber security, peer-to-peer lending, mobile payments, and cloud computing. MARISSA BLANKENSHIP investigates this new technology, examining the potential risks and rewards of its application within the financial industry.

It is impossible to follow the financial sector without being bombarded by information about distributed ledger technology (DLT) or ‘Blockchain’, as it is more widely known. Blockchain is the technology which underpins Bitcoin and allows participants to share in a single “golden record” without relying on central authorities or intermediaries. It has sprung up from almost nowhere as even as early as two years ago it was largely an absent topic from sell side research, Bloomberg Intelligence, and industry conferences. However, it is now recognized as a potential disruptive force for systems, process and infrastructure used to settle and record financial transactions. To that point, financial and technology companies are investing greater than USD 1 billion in 2016 to bring this technology to the market according to Magister Advisors, having already spent over USD 900m in the past 36 months.1

Marissa BlankenshipESG Analyst, London

FinTech/ section 2

9

ESG Matters | Issue 9

10

FINTECH/SECTION 2

In the past two years, in terms of financial innovation, blockchain has surged past cyber security, peer-to-peer lending, mobile payments, and cloud computing and is being touted as the best revolutionary idea since the Internet. What is driving such attention is that the transaction ledger database with cryptographic integrity is shared by all parties in a distribution network and every transaction that occurs in the network is recorded and stored by creating an irrevocable and auditable transaction history.

The fact that every business has a ledger means that the potential scale and application of DLT is far reaching and could easily evolve into areas that are not yet in a pilot phase. In addition to diversified financials (stock exchanges, banks, and asset managers), pilot applications of DLT include e-commerce and manufacturing, supply chain management, and healthcare. Intermediaries such as custodians, clearing houses and financial messaging services can be seen at most risk of disruption and are joining consortiums such as R3 which consists of 42 banks and Hyperledger which consists of banks, exchanges, post-trade, and other technology companies and consultants to invest in research, design, and engineering of pilot applications.

In addition to banks, venture capital is also active and growing globally. According to Outlier Ventures, there are 967 blockchain start-ups as of June 2016 with the United States and United Kingdom leading the pack, although close to 20 percent of start-up origins were not disclosed. While still dwarfed by the US and UK, financial technology investment in Asia quadruped last year with venture capital firms backing blockchain, peer-to-peer lending, online lending, cloud computing, and cyber-security.

Realistically, wide-spread adoption of DLT is ten plus years away as vested interests in legacy technology systems will make change

0

20

40

60

80

100

Sep 11 Sep 12 Sep 13 Sep 14 Sep 15

Blockchain: (Worldwide) Distributed ledger technology: (Worldwide)

Figure 1: Google Trends - Global Interest1 over 5 years in Blockchain and Distributed Ledger Technology

Source: Google Trends (www.google.com/trends). 1 A value of 100 is peak popularity for the 5-year term while a score of zero means the term was less than 1% as popular as the peak.

costly and the governance of aligning shareholder interests and developing common protocols is a key challenge in addition to data privacy, scalability and regulation.

As the application of blockchain becomes better understood, there are trends emerging from an ESG perspective. Naturally, there will be an impact on human capital although it is too early to determine the magnitude. According to ‘Blockchain in Capital Markets: the Prize and the Journey’,2 it is estimated that IT and capital markets currently cost banks close to USD100 – 150 billion per year in addition to another USD100 billion for post-trade and other market inefficiencies. Santander estimates that about USD20 billion in costs could be reduced per year with more efficient digital ledgers. Further work needs to be done on quantifying both operational costs and savings from blockchain. Human capital would be impacted due to a reduction in operational overheads as well as cost-sharing across institutions.

The nature of blockchain is such that it is designed to enable trust and cooperation in new and innovative ways. This would be a welcome benefit for financial companies who are still suffering from mistrust post the global financial crisis. For banks, which are under pressure to cut costs due to downward pressure of net interest margin (NIM), blockchain can be used to streamline processes and reduce inefficiencies in the capital market infrastructure. Specifically, post trade settlement, custody, clearing, and international payments are the most named applications. Furthermore, DLT allows for more transparency for regulators on transaction history and can enhance monitoring; know your client (KYC) and anti-money laundering (AML) processes.

Stock exchanges are working on industry changing applications by replacing Central Depositories (CSD) and positioning themselves as

11

ESG Matters | Issue 13ESG Matters | Issue 13

Figure 2: Percentage Blockchain Start Ups by Country as of June 2016

Source Bloomberg, Outlier Ventures.

0%

10%

20%

30%

40%

Unite

d St

ates

Unite

d Ki

ngdo

m

Cana

da

Chin

a

Sing

apor

e

Germ

any

Israe

l

Aust

ralia

Fran

ce

Neth

erla

nds

Switz

erla

nd

Japa

n

Swed

en

Viet

nam

Zim

babw

ea “digital vault.” This sets them up to build applications which process data for reporting and allow for performance monitoring. Early projects involve the testing of providing real time access to issuers to their share register and using smart contracts to facilitate corporate actions.

Nasdaq Talinn (Estonia) is trialling using DLT to facilitate proxy voting and the National Settlement Depository in Russia has also developed an e-proxy voting system which allows for electronic interaction between securities holders and issuers for the purpose of exchanging information and documents. According to financial messaging service company, SWIFT, the proxy voting function has been characterised by non-standard, proprietary processes, with frequent requirements for manual intervention. Proxy voting covers about 85,000 companies each year is labour intensive for investors as well as their intermediaries, is subject to significant errors and carries a significant cost. The once manual process has moved largely to online platforms but smart contracts would help catch the large proportion of votes that go uncast each year. This was the case in 2014, where according to Broadbridge, over 22 billion retail shares went un-voted in 1,077 US company shareholder meetings from July to December.3

In addition to stock exchanges and banks, there are several examples which would be a positive from an ESG perspective including providing trade finance facilities, real estate registration facilities, databases on agricultural receivables and digital assets. Notably, it is possible to use blockchain to help make supply chains more transparent by using digital encryption to create an immutable history of a products authenticity and ownership. This is being explored in respect to conflict minerals and blood diamonds which would enable compliance with disclosure requirements under the Dodd-Frank Act in the US. In Honduras, blockchain technology is

being used to build a land title registry which will help to reduce land title fraud which is a common issue in poorer countries.

The race to production has kicked off with most large financial institutions already having 10-20 applications in prototype phase. Yet the overarching hurdle to implementation is achieving the necessary governance, regulation and compliance. This will be aided by having regulators such as International Organisation of Securities Committees (IOSCO) taking the lead to developing harmonised global standards. Assuming these barriers can be scaled, what remains to be considered from an ESG perspective is the trade-off between improved transparency, reduced fraud and corruption and better management of complex supply chains versus the implied risk to human capital. The buzz about blockchain is indeed a constant chatter and the opportunity to reduce ESG risks due through applications which increase protection and promote the efficacy of institutions across multiple sectors is needed globally.

1 http://uk.businessinsider.com/magister-advisors-report-on-bitcoin-and-blockchain-ecosystems-2015-12/#-1

2 https://www.euroclear.com/en/news-views/news/press-releases/2016/2016-MR-02.html

3 http://bravenewcoin.com/news/nasdaq-to-simplify-proxy-voting-process-for-shareholders-with-the-blockchain/

“ For banks blockchain can be used to streamline processes and reduce inefficiencies in the capital market infrastructure. ”

12

Methane Emissions/

Section 3

Methane Emissions: The next frontier for the Oil & Gas industry

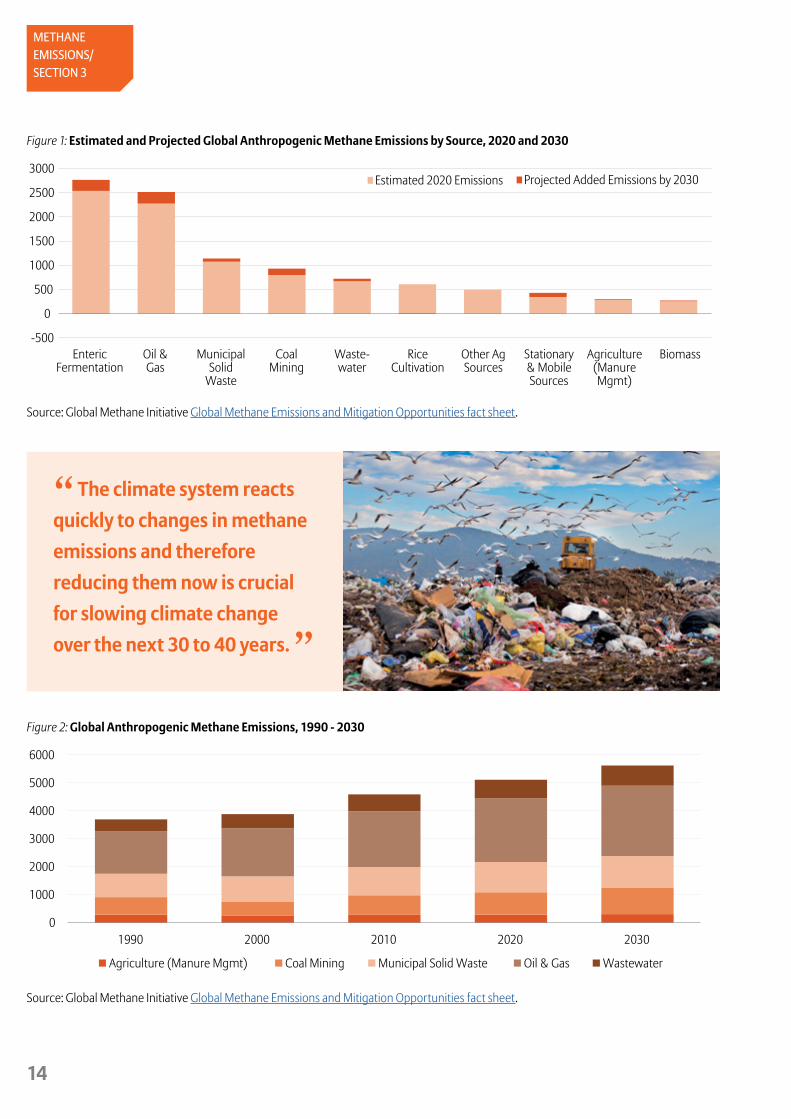

In this article MARIE-SYBILLE CONNAN highlights the need for a strategy on climate change which targets both greenhouse gas emissions (GHGs), carbon dioxide and methane. Methane emissions can be a game changer for climate change in general and for the Oil & Gas industry in particular.

Why methane emissions matter

Ahead of COP21, the six largest European Oil & Gas companies (including Shell, BP and Total) called for a global carbon tax as a way of slowing global warming and promoting natural gas as a transition fuel to a low carbon economy. This was a welcome initiative from the European Majors which was sadly not mirrored by their US peers. However, as often, the devil is in the detail. Any carbon tax should recognize the two sides of carbon: there are two major greenhouse gases, carbon dioxide (CO2) and methane (CH4) and both are carbon gases. Targeting both is critically important if we want to

Marie-Sybille ConnanESG Analyst, Paris

13

ESG Matters | Issue 13

have a chance to limit global warming to 2°C (with an even greater ambition to reach 1.5°C) as agreed in the Paris Agreement. Identifying an upper limit in greenhouse gas emissions as soon as possible is the immediate climate concern.

One can appreciate how difficult the challenge is considering that the oil majors are currently rebalancing their portfolios towards natural gas and that the US economic recovery post Lehman Brothers is related to the shale gas boom.

Methane is the second most abundant manmade greenhouse gas after carbon dioxide: CO2 accounts for about half and CH4 for one quarter1. It is emitted during the production of coal, oil and natural gas. It also comes from solid waste stored in landfills, animal waste management systems, wastewater treatment facilities and other manmade and natural sources.

These emissions pose risks to people and the environment. Methane emitted into the atmosphere creates air pollution causing thousands of premature births every year. Methane that builds up in coal mines and oil & natural gas facilities can cause explosions that can endanger workers.

China, the US, Russia, India, Brazil, Indone-sia, Nigeria, and Mexico are estimated to be responsible for nearly half of all anthropo-genic methane emissions. However the major sources of methane emissions for these countries vary greatly. For example, a key source of methane emissions in China is coal production, whereas Russia emits most of its methane from natural gas and oil systems. In the US, oil and gas systems are the largest source methane emissions (30%) according to the US Environmental Protection Agency (EPA)2.

Global anthropogenic methane emissions are projected to increase by 19% over the period 2010 – 2030 to 10,220 million metric tons of CO2 equivalent by 20303. The relative contributions of the agriculture, coal mining and landfill sectors are

14

METHANE EMISSIONS/SECTION 3

“ The climate system reacts quickly to changes in methane emissions and therefore reducing them now is crucial for slowing climate change over the next 30 to 40 years. ”

-500

0

500

1000

1500

2000

2500

3000

EntericFermentation

Oil &Gas

MunicipalSolid

Waste

CoalMining

Waste-water

RiceCultivation

Other AgSources

Stationary& MobileSources

Agriculture(ManureMgmt)

Biomass

Estimated 2020 Emissions Projected Added Emissions by 2030

0

1000

2000

3000

4000

5000

6000

1990 2000 2010 2020 2030

Agriculture (Manure Mgmt) Coal Mining Municipal Solid Waste Oil & Gas Wastewater

Figure 1: Estimated and Projected Global Anthropogenic Methane Emissions by Source, 2020 and 2030

Source: Global Methane Initiative Global Methane Emissions and Mitigation Opportunities fact sheet.

Figure 2: Global Anthropogenic Methane Emissions, 1990 - 2030

Source: Global Methane Initiative Global Methane Emissions and Mitigation Opportunities fact sheet.

15

ESG Matters | Issue 13

projected to remain relatively constant while methane emissions from wastewater treatment systems are expected to increase by nearly 19%. Oil and gas emissions are the real issue as they are expected to increase by 26% over the same period

Methane emissions in the context of climate change

In order to address climate change, we must reduce pollution to slow the rate of climate change (notion of flows) while at the same time limiting maximum warming (notion of inventories).

But, all emissions are not equal. Like CO2, methane is a gas that warms the Earth by trapping heat. However, the way in which each gas interacts with the planetary climate is dramatically different. The climate is slow to respond to changes in carbon dioxide emissions and, as such, immediate reductions in CO2 emissions will take 30 to 40 years to slow warming but, critically, all emissions produced will have a warming effect on the climate that will last for hundreds of years. On the other hand, the climate system reacts quickly to changes in methane emissions and therefore reducing them now is crucial for slowing climate change over the next 30 to 40 years. Furthermore, the methane remains in the atmosphere for only 12 years: methane emissions don’t have any lasting influence on the planetary climate system, unlike carbon dioxide emissions.

Methane and carbon dioxide emissions have very different lifetime and impact. CH4 is 84 times more powerful than CO2 over the first two decades following its release but its only 28 times more powerful over 100 years. By contrast, CO2 remains in the atmosphere much longer. Over time, CO2 has then a greater warming potential4.

Hence, comparing them requires a metric that depends on a timeframe. Scientists measure the global warming of potential gases over two time periods: 100 and 20

years. It is scientifically proven that the Earth is predicted to warm by 1.5°C above pre-industrial baseline within the next 15 years and by 2°C within the next 35 years given current GHG emissions5. It is also scientifically proven that a combination of emissions reductions, such as curbing CO2 from coal-fired power plants and methane from oil and gas activities, is the best way to stabilize the climate in the long term while reducing warming now. That’s why, the use of a global warming potential of 84 for the 20-year time period from the IPCC Fifth Assessment is the right approach to compare the warming consequences of methane and carbon dioxide emissions.

Hence, Robert W Howarth from the Cornell University, Ithaca, NY, introduces the notion of a GHG footprint for fossil fuels and he shows that the GHG footprints of shale gas first and then conventional natural gas are higher than that of conventional oil and coal when methane emissions are considered over an appropriate timescale. As such, natural gas (and shale gas in particular) may lose its green credentials as the transition fuel to a low carbon economy.

Regulatory, investor and corporate initiatives to tackle the critical issue of methane emissions

There is an urgent need to act on methane emissions. Take the massive natural gas leak at a storage well near Los Angeles on 23rd October 2015 as an example, this resulted in thousands of nearby families having to flee their homes and be temporarily relocated. After several unsuccessful attempts to plug the leak, SoCal Gas began building a relief well to capture the leaking gas. In mid-February, the leak was fixed, over three and a half months later. The Environmental Defense Fund (EDF) estimates that the amount of methane leaked had the same 20-year climate impact as burning nearly a billion gallons of gasoline. This sole gas leak will have an impact on California’s ability to

meet its GHG targets this year. Aside from the environmental and reputational risk, SoCal Gas estimates financial costs of USD330m and 83 lawsuits have already been filed against the firm7.

From an economic standpoint, methane is valuable and lost methane is essentially wasted fuel. Because methane is the major component of natural gas, it can also be captured before it is emitted into the atmosphere and used to produce energy for heating, electricity and cooking.

When it is captured from landfills and agricultural sites, the collection systems can reduce local water contamination.

Leaked methane: Estimated impact

97,100metric tons of methane, a powerful climate pollutant, are estimated to have leaked between 23 October and 11 February.

That‘s the same as:

8,156,400metric tons of carbon dioxide released

Source: Environmental Defense Fund

16

METHANE EMISSIONS/SECTION 3

As such, all stakeholders have a vested interest in managing actively methane emissions. There are practical and cost effective solutions to minimize methane emissions, many of which can increase the ‘bottom line’ of the Oil & Gas industry.

Since 2004, countries around the world have been working in partnership with the Global Methane Initiative on projects to reduce emissions worldwide and to use methane emissions as a source energy source. These projects are also helping to reduce air pollution, protect people’s health and improve local economies.

In particular in the US, where financial and environmental stakes are high, the White House announced in January 2015 an ambitious national strategy to reduce oil and gas methane emissions to 40-45% below 2012 levels by 2025. However, in order to meet this target, new regulations are required that go beyond the EPA proposed methane emissions standards for

new and modified oil and gas facilities (August 2015). Indeed, circa 90% of emissions in 2018 are expected to come from existing facilities8. The outcome of the US presidential polls may weigh on the implementation of further regulations.

The Environmental Pension Fund (EDF) has done great work in increasing awareness across the Civil Society, corporate and the investor sphere. In a recent study, they show that global oil and gas methane emissions represented USD 30bn in wasted resources worldwide, which proves that there is a financial benefit for Oil & Gas companies to identify and manage methane emissions9. They also found that the disclosure on methane emissions is not up to the challenge. 28% of the 65 companies (out of which 40 Oil Majors and 25 large midstream companies) surveyed report methane emissions in investor facing channels. No company provides quantitative reduction targets. Only one company provided detailed information on

its leak detection and repair (LDAR) program. Information provided is generally vague, qualitative and non-actionable. The EDF calls for corporate action to measure and report methane emissions in order to manage the impact on global warming.

In the wake of EDF, investors are increasingly pushing for action on methane after having targeted companies for releasing sustainability reports and disclosing their carbon dioxide emissions. They want more information on the extent of the issue and how companies are tackling it. Hence, they have filed 10 shareholder resolutions to press US energy companies before their annual meetings this year to detail plans for limiting methane leakage from wells, pipelines and other energy equipment10.

Lastly, investors representing USD3.6trn commended the joint US and Canadian March 10th announcement that both countries take steps to seriously address methane emissions from the Oil & Gas

Benefits attributed to Methane Projects

Greenhouse gasesReduces emissions to

the atmosphere

Economic growthUses captured methane directly

or to generate electricity

Source: Global Methane Initiative Accomplishments Infographic.

Energy securityCreates local, reliable

energy source

17

ESG Matters | Issue 13

sector11. As widely diversified, long-term investors with holdings in the Oil & Gas industry, they share a vested interest in the industry’s long-term success and think that natural gas can play a significant role in the North American energy mix, has demonstrated the potential to reduce greenhouse gas emissions while supporting economic growth. However, they are concerned that methane emissions pose a risk to their investments. They urge companies to minimize methane emissions in a transparent manner and provide investors and the public with better methane reporting.

Methane emissions: the next frontier

Methane disclosure has become the new challenge for investors in Oil & Gas companies after the good progress achieved on carbon disclosure and stranded assets stress-testing. For the gas industry to really be part of the solution in

the transition to a low-carbon economy, methane emissions must be actively and transparently managed. Investor scrutiny will only but increase.

1 https://www.edf.org/methane-other-important-greenhouse-gas

2 https://www3.epa.gov/climatechange/Downloads/ghgemissions/US-GHG-Inventory-2016-Chapter-Executive-Summary.pdf

3 http://www.globalmethane.org/documents/analysis_fs_en.pdf

4, 5 https://www.ipcc.ch/pdf/assessment-report/ar5/syr/SYR_AR5_FINAL_ full.pdf

6 http://www.eeb.cornell.edu/howarth/publications/f_EECT-61539-perspectives-on-air-emissions-of-methane-and-climatic-warmin_100815_27470.pdf

7 http://www.latimes.com/business/hiltzik/la-fi-socal-gas-ceo-20160328-snap-htmlstory.html

8, 9 https://www.edf.org/sites/default/files/content/rising_risk_full_ report.pdf

10 https://www.edf.org/sites/default/files/content/rising_risk_full_ report.pdf

11 https://www.ceres.org/files/investor-support-of-the-joint-u.s.-and-canadian-announcement-on-methane-emissions

Local environmental qualityReduces air pollution and surface/

groundwater contamination

Worker safetyMinimizes explosive methane

levels or fires

Human healthReduces respiratory impacts

associated with high ozone levels

18

Communication is key: dialogue between shareholders and German supervisory boards

HENRIKE KULMANN discusses a recent initiative in Germany to increase dialogue between institutional shareholders and the supervisory boards of listed companies. The working group of the initiative has developed a set of guidelines to encourage such engagement with the aim of increasing transparency and trust amongst both parties.

While meetings with the non-executive board members are becoming business as usual in markets such as the United Kingdom or France, such exchange is currently rather the exception than the rule in Germany. At the same time, the planned amendments to the EU Shareholder Rights Directive expect institutional investors to become more active in monitoring listed corporates. Regular communication with the supervisory board, as the core oversight body in

Germany’s two-tier corporate governance structure, would support investors to adequately adapt to enhanced expectations. In order to stipulate convergence for better shareholder access to supervisory boards in Germany, a group of high profile representatives of investors, academics and corporates developed the “Guiding principles for the dialogue between investors and German supervisory boards” .1

German Supervisory

Board /section 4

Henrike KulmannESG Analyst, Frankfurt

19

What is it all about?

The eight guiding principles are designed as a practical tool to frame the topics of such dialogue and its participants, with the aim of establishing high quality dialogue practices. Key focus areas include:

• Supervisory board composition and nomination• Management appointment and removal• Remuneration structure of management and supervisory

boards • Strategy development and implementation• Auditor appointment

Importantly, the guidelines clarify that communication should only focus on topics within scope of the supervisory boards competencies as outlined in the German company and capital markets laws. Currently, the legal framework for supervisory board engagement is not clearly defined which creates uncertainty amongst corporates on how to handle investor requests for corporate governance engagements with supervisory board members. As such exchange is not excluded by German regulation and already practiced by some Germany corporates, the guidelines help to provide more clarity to all participants. They fit within the existing legal structures and the German Corporate Governance Code, including the equal treatment principle.

What are the benefits for investors and corpo-rates to engage in a dialogue?

A fruitful exchange between supervisory boards and institutional investors is beneficial for all participants. From a shareholder perspective, dialogue contributes to investor confidence and better investment decisions. It enables investors to evaluate supervisory board composition and the supervisory board’s ability to oversee and constructively challenge management action in the interest of all shareholders. The first-hand information from supervisory board members also helps to form a view how well management

remuneration is aligned with long term shareholder interests. Findings can be incorporated into voting decisions at annual general meetings enabling investors to make well-informed choices as part of their fiduciary duty towards clients.

From a company perspective, it gives the supervisory board the chance to explain, for example, the rationale for proposed changes to remuneration policies, how supervisory board collaborates or how succession planning is organized. Therefore, meetings between investors and supervisory boards could also increase investor support at annual general meetings. Moreover, given the German two-tier corporate governance system as well as the employee co-determination system, German supervisory boards get an opportunity to foster an understanding of the country specific corporate governance approach amongst foreign investors. Corporates would also get the chance to better understand their investors’ expectation on corporate governance and could enhance their practices, making them more attractive investments to the market.

What could be the way forward?

The initiative has started a discussion on the topic of investor – supervisory board communication which will hopefully lead to increased transparency and mutual trust amongst contributing parties. As the Government Commission on the German Corporate Governance Code is expected to incorporate a general recommendation for supervisory board and investor communication in the Code, chances are good that more German corporates will start to engage in an active dialogue with institutional shareholders.

1 http://www.esgmatters.co.uk/en/ThoughtLeadership/ExternalArticles/Pages/default.aspx

ESG Matters | Issue 13

Prof. Dr. Alexander Bassen University of Hamburg

Dr. Jürgen Hambrecht BASF, Daimler, Fuchs Petrolub Dr. Hans-Christoph Hirt Hermes Investment Management

Prof. Dr. Dr. Dr. h.c. mult. Klaus J. Hopt Director (Emeritus) of the Max Planck Institute for Comparative and International Private Law Hamburg

Prof. Dr. Ulrich Lehner E.ON, Henkel, Deutsche Telekom, Porsche Automobil Holding, ThyssenKrupp

Dr. Stephan Lowis RWE

Ingo R. Mainert Allianz Global Investors

Daniela Mattheus EY

Prof. Christian Strenger Deutsche Asset Management

Dr. Paul Achleitner Deutsche Bank, Bayer, Daimler

Kay Bommer Deutscher Investor Relations Verband Dr. Christine Bortenlänger Deutsches Aktieninstitut

Dr. Werner Brandt RWE, Deutsche Lufthansa, OSRAM Licht, ProSiebenSat. 1 Media

Dr. Joachim Faber Deutsche Börse

Dr. Dr. h.c. Manfred Gentz Government Commission on the German Corporate Governance Code

Thomas Richter German Investment Funds Association BVI

Members of the Working Group

Members of the Stakeholder Advisory Group (selected)

2020

Corporate Bonds/

Section 5

21

ESG Matters | Issue 13

How does ESG affect the credit rating of corporate bonds?

Similar to the ‘ESG in Equities’ and ‘ESG in Real Estate’ whitepapers produced in 2015, DR. STEFFEN HÖRTER and his team have performed a meta-analysis evaluating recent, selected, high-quality industry and academic research on ESG in investment grade corporate bonds. The format of a meta-analysis provides a diversified research view and aims to avoid research bias.

Dr. Steffen HörterGlobal Head of ESG,Munich

This article is an extract from our white paper called “ESG in Investment Grade Corporate Bonds”. The paper aims to find evidence of the materiality of ESG dimensions and ESG criteria within financial performance and risk for listed, publically traded corporate bonds. The paper analysed Investment Grade Bonds in European and Global markets and evaluated recent, selected and high quality industry and academic research.

ESG integration into credit risk analysis

Most recently, Moody’s and S&P, two authorities in the area of credit risk analysis, have started to incorporate ESG factors into their credit rating methodologies. By signing the UN PRI Statement on “ESG in Credit Ratings”, Moody’s, S&P and four other rating agencies affirmed their commitment towards a more systematic and

22

CORPORATE BONDS/SECTION 5

transparent consideration of sustainability and governance factors in credit analyses and ratings.

ESG analysis is focused on issuer, industry sector and country specific key credit factors. Next to an explicit focus on selected high-risk ESG factors, ESG risk is indirectly scored through the analysis of the business environment and financial strength of a corporate. While ESG factors can be material to the credit rating, other criteria such as financial strength are generally perceived to be of more importance – not only because they may facilitate an issuer to adjust to ESG risks over-time through enterprise risk-management, but also because they already may be a good proxy on the corporate management of ESG risks.

How does ESG affect the credit rating of corporate bonds?

Corporate bond performance is generally determined by a multitude of factors. These include a bond’s payment structure and duration, market risks such as interest rates and liquidity fluctuations, as well as credit risk. On a portfolio level, issuer selection and diversification are relevant factors. We investigated the financial materiality of ESG for corporate bonds and portfolios in some of these factors by analysing several selected research studies and methodologies. We investigated how and to what extent ESG ratings can complement credit ratings.

23

ESG Matters | Issue 13

The link between ESG and corporate credit risk

For Investment Grade Corporate Bond portfolios it is important to identify issuers with high credit quality. Credit risk may be measured in various ways: credit ratings and rating migrations, bond price volatility, credit default swap prices, credit spreads etc. Since many bond portfolio managers use the credit opinions of rating agencies it is important to understand if and how ESG is incorporated in their credit assessment. In May 2016, the UN PRI launched an initiative to develop practical solutions for more systemic and transparent incorporation of ESG in credit ratings and analyses. A statement was produced on ‘ESG in credit ratings and analyses’ which was signed

by over 100 investors and six of the leading credit rating agencies. In our analysis we focus on the evidence of ESG integration by the ‘big three’ agencies, namely S&P, Moody’s and Fitch ratings.

Standard & Poor’s approach to ESG

In its 2015 report “ESG Risks In Corporate Credit ratings — An Overview” Standard & Poor’s (S&P) documents their ESG methodology for credit assessment. ESG risks are seen as an essential element in their credit analysis and are already incorporated into their corporate credit criteria framework. While the main focus of S&P’s ESG intake is to identify downside credit risk, any

24

CORPORATE BONDS/SECTION 5

favourable environmental or social factors that may contribute to an improved credit rating outlook are considered. Although governance is only scored on a neutral or negative scale ESG risks are incorporated throughout their credit rating research process. Factors that are assessed in the analysis include climate change policies, environmental pollution, resource depletion, employee-, customer- and community relations, adherence to legal and regulatory requirements etc.

As mentioned, ESG factors do not receive an explicit score but are incorporated into the overall credit rating analysis to provide a holistic view of an issuer’s profile. Governance is the most frequent and material factor for rating changes.3 It is the only ESG dimension that is explicitly and exhaustively examined. Observed changes in Management & Governance can substantially influence the credit rating. This is especially true for lower rated issuers. Yet, S&P argues that environmental and social factors are implicitly covered by their assessment of a company’s management of other credit factors.

In the S&P report “How Environmental and Climate Risks Factors Into Global Corporate Ratings” the rating agency documents how material environmental and climate factors (E&C) impact their credit ratings. The analysis identifies 299 E&C cases in which these factors either contributed to a rating revision or were a determining factor in the rating analysis. 56 of these cases resulted in direct rating actions with the majority of it being in the negative direction in the energy sector (oil refining and marketing, regulated utilities, and unregulated power and gas subsectors).

Moody’s approach to ESG risks in credit ratings

In the report “Moody’s Approach to Assessing ESG risks in Rating and Research” the rating agency illustrates through which direct and indirect paths ESG risks are incorporated into their credit risk research and ratings. ESG considerations are captured in Moody’s long-term credit risk analyses when the agency believes they will materially affect the primary focus of their ratings systems – to assess the probability of default of a debt issuer and expected credit loss in the event of default. Consequently, Moody’s credit research and ratings consider material ESG factors with potentially large impact on credit default risk or size of loss in case of default.

ESG risks are differentiated along industries, sectors and single issuers. In some of Moody’s credit rating methodologies ESG risks are even explicitly scored, e.g. governance risk for sovereign bond issuers and banks. For the ultimate credit risk assessment, Moody’s puts ESG risks into the overall credit risk analysis picture. In doing so, factors like high financial strength of an issuer may, however, off-set ESG risk concerns.

Moreover, Moody’s rating outlooks are enriched by important ESG risk trends identified by Moody’s credit research. A 2015 example is the analysis of the potential impact of the ongoing Californian drought on public Californian finance.

Recent reports include: Global anti-bribery and corruption enforcement efforts, upcoming regulations on Europe’s electricity markets, and the rising impact of carbon reduction policies.

Figure 2: Rating actions related to environmental and climate risk: S&P

Outlook revised to negative 23

Downgrade 19

Upgrade 8

Outlook revised to stable from negative 3

Creditwatch negative placement 2

Outlook revised to positive 1

E&C Risk Impact on credit analysis and ratings

Contributed to general analysis 243

Source: Allianz Global Investors based on S&P Global (2015) “ESG Risks in Corporate Ratings - An Overview” and “How environmental and climate risks factor into global corporate ratings”.

25

ESG Matters | Issue 13

In summary, Moody’s does not see ESG as a main determinant of credit outcomes but rather as one of the several elements they consider through their holistic credit risk assessment for rated entities. Moody’s argues that compared to ESG other credit factors are deemed more relevant in analyses of creditworthiness. Further, Moody’s estimates the direct impact of ESG risks to be felt only over a longer time horizon. Hence, rated entities have more flexibility to adjust for these risks in advance, which is why Moody’s argues that they capture ESG risks in other, more immediate credit issues – such as is the case in the prospective evaluation of capital requirements.

Moody’s has developed a heat map (figure 3) that scores 86 sectors in terms of materiality and timing of any likely environmental risks with possible credit risk impact. The purpose of this map is to identify sectors which are more prone to environmental hazards. Environmental risks are broadly divided into two categories: effects of environmental hazards (pollution, drought, severe natural and

man-made disaster, etc.) and the consequences of regulation designed to prevent or reduce those hazards.

The heat map represents a relative assessment of potential risks. Each sector’s exposure is divided into five sub-categories: Air pollution, soil and water pollution and land use restrictions, carbon regulation, water shortages as well as natural and man-made disasters. Carbon regulations and air pollution are the two subcategories which are deemed to pose the biggest environmental threats in the future.

Fitch ratings

The report “Evaluating Corporate Governance” by Fitch outlines their approach. Within the ESG domains, Fitch focuses mostly on corporate governance. As Fitch states: “poor governance practices, including country-specific and issuer-specific corporate

Figure 3: Moody’s heat map: assesses overal sector credit risk exposure to five subcategories of environmental risks

Source: Moody’s (2015). Environmental Risks: Heat map shows wide variations in credit impact across sectors.

Overall Sector Environmental Risk Scoring

Immediate, Elevated Risk

Sectors scored “immediately/elevated” overall are already experiencing material credit implications as a result of environmental risk. Therefore, rating changes have either already been occurring for a substantial number of issuers or we believe such rating changes are likely within the next three years.

Emerging, Elevated Risk

Sectors scored “emerging/elevated” overall have clear exposure to environmental risks that, in aggregate, could be material to credit quality over the medium term (three to five years), but are less likely in the next three years.

Emerging, Moderate Risk

Sectors in this category have a clear exposure to environmental risks that could be material to credit quality in the medium to long term (five or more years) for a substantial number of issuers. However, in contrast to emerging/elevated sectors, it is less than the identified risks will develop in a way that is material to ratings for most issuers.

Low RiskSectors in this category have either no sector-wide exposure to meaningful environmental risks or, if they do, the consequences are not likely to be material to credit quality.

ICON KEYIcon colour indicates weight of each environmental exposure for the sector

VERY HIGH

HIGH

SOMEWHAT ELEVATED

CONSISTENTLY LOW

Air Pollution

Soil/Water Pollution & Land Use Restrictions

Carbon Regulations

Water Shortages

Natural & Man-made Disasters

26

CORPORATE BONDS/SECTION 5

governance matters, can result in lower ratings than typical quantitative and qualitative credit factors may otherwise imply”. Corporate governance is identified through key analytics along two dimensions: country- and issuer-specific factors. When evaluating corporate governance on a country level, Fitch will focus on systematic characteristics such as jurisdictional considerations, the quality and quantity of financial information available in the market and whether the regulatory and operational environment supports or undermines the overall transparency. Issuer-specific governance characteristics are for instance board effectiveness, management effectiveness, transparency of financial information and related-party transactions. Governance characteristics are respectively divided into three impact categories: ratings neutral, those that may constrain ratings and ratings negative. Fitch states that good governance will not, in isolation, positively affect a credit rating.

Results

When rating agencies perceive ESG risks to be material for changes in ratings or rating outlooks, we have found that they are increasingly considered as part of the credit rating process.

Rating agencies do not usually explicitly score companies or sovereigns with regards to ESG risks or strengths as is done by ESG research providers, to construct dedicated ESG issuer ratings. Material ESG factors are considered part of the standard credit risk assessment model. Credit risk materiality of ESG is subject to industry sector, company and time horizon. Previously rating agencies seem to have considered ‘governance/management strength’ as part of their standard credit risk assessment framework.

Figure 1: Credit Rating Agencies (CRA) and ESG: Peer group comparison

Key criteria S&P Moody’s Fitch

Environmental factors

Mentioned in document Evidence Evidence -

Explicitly mentioned as credit criteria Evidence Evidence -

Extent of E in credit risk analysis Considerable evidence Evidence -

Social factors

Mentioned in document Evidence Evidence -

Explicitly mentioned as credit criteria Evidence Evidence -

Extent of S in credit risk analysis - Evidence -

Governance factors

Mentioned in document Considerable evidence Evidence Evidence

Explicitly mentioned as credit criteria Considerable evidence Evidence Evidence

Extent of G in credit risk analysis Considerable evidence Considerable evidence Evidence

Methodology

Level of considerationIncorporates country and industry risk and an assessment of the competitive position

Individual industry and entity specific ESG considerations

Assessment of jurisdictional environment and entity specific factors

Approach• Risk based approach• Opportunity-based approach for E&S• Downside-scale for governance

• Risk and downside based approach• Industry/sector differences

• Risk and downside based approach• No consideration of good governance

Time horizon Long-term Long-term n/a

Integration• E&S considered when deemed material• G is a part of the “management” assessment in the credit rating process

• E&S considered when deemed material• G is a fixed component of CR assessments

G: considered on individual basis

Which factor is most important?Governance, E&S will receive more prominence in the future

Governance, E will receive more prominence in the future

Governance

Additional informationRegular publications on environmental & social event risks

• Dedicated environmental risks and developments topic section page• Social performance group (Moody’s SRI research platform)

n/a

Source: Allianz Global Investors based on selected publications of credit rating agencies.

27

ESG Matters | Issue 13

Corporate governance is perceived to be the strongest credit risk contributor when considering ESG dimensions. Whereas, environmental risks, such as climate change or industry regulations are perceived to be more of a long term macro/industry risk. In conclusion, it appears that rating agencies seem to assess environmental issues indirectly through other factors, such as solvency or liquidity.

As ESG issues and ESG trends such as demographic change, corporate transparency, carbon regulations etc. increasingly gain public attention, it is likely that the number of ESG-related rating incidents will rise. Materiality and corporate exposure towards these risks will become more important than ever.

Please note: the conclusions from the research studies analysed and summarised in this report do not necessarily reflect Allianz Global

Investors’ investment opinion. The research does not imply investment advice or investment performance related forecasts.

1 It has to be noted that evidence for ESG portfolio strategies in corporate bonds to date seems modest, though the number of publications has increased substantially in the recent years.

2 Moody’s: “Moody’s Approach to Assessing ESG Risks in Ratings and Research” and “Environmental Risks and Developments”.

3 See ”Standard & Poor’s (2012). Methodology: Management and Governance credit factors for corporate entities and insurers.

Figure 1: Credit Rating Agencies (CRA) and ESG: Peer group comparison

Key criteria S&P Moody’s Fitch

Environmental factors

Mentioned in document Evidence Evidence -

Explicitly mentioned as credit criteria Evidence Evidence -

Extent of E in credit risk analysis Considerable evidence Evidence -

Social factors

Mentioned in document Evidence Evidence -

Explicitly mentioned as credit criteria Evidence Evidence -

Extent of S in credit risk analysis - Evidence -

Governance factors

Mentioned in document Considerable evidence Evidence Evidence

Explicitly mentioned as credit criteria Considerable evidence Evidence Evidence

Extent of G in credit risk analysis Considerable evidence Considerable evidence Evidence

Methodology

Level of considerationIncorporates country and industry risk and an assessment of the competitive position

Individual industry and entity specific ESG considerations

Assessment of jurisdictional environment and entity specific factors

Approach• Risk based approach• Opportunity-based approach for E&S• Downside-scale for governance

• Risk and downside based approach• Industry/sector differences

• Risk and downside based approach• No consideration of good governance

Time horizon Long-term Long-term n/a

Integration• E&S considered when deemed material• G is a part of the “management” assessment in the credit rating process

• E&S considered when deemed material• G is a fixed component of CR assessments

G: considered on individual basis

Which factor is most important?Governance, E&S will receive more prominence in the future

Governance, E will receive more prominence in the future

Governance

Additional informationRegular publications on environmental & social event risks

• Dedicated environmental risks and developments topic section page• Social performance group (Moody’s SRI research platform)

n/a

Source: Allianz Global Investors based on selected publications of credit rating agencies.

Biographies28

ALLIANZGI AND ESG/SECTION 6

Eugenia Jackson Head of ESG Research

Eugenia Unanyants-Jackson is a Director and Head of ESG Research at Allianz Global Investors, which she joined in 2016. Eugenia is responsible for directing ESG research, guiding and overseeing AllianzGI’s stewardship activities, including corporate governance, engagement and proxy voting, and supporting integration of ESG factors into AllianzGI’s investment process for different strategies. Prior to joining AllianzGI, Eugenia was a Director, Governance and Sustainable Investment and Head of Corporate Governance at BMO Global Asset Management (formerly F&C Investments), a Stewardship Services Manager at Governance for Owners LLP, a Policy Analyst at Manifest Information Services, a Researcher at Pension Investments Research Consultants (PIRC). Eugenia co-chairs ICGN’s Shareholder Rights Committee and represents AllianzGI on the Governance and Engagement Committee of the Investment Association and other professional associations and networks. Eugenia has written on corporate governance matters, covering issues related to shareholder rights, listing standards, board diversity, directors’ liabilities, cross-border voting issues, and director remuneration. Eugenia has a M.P.A. from the Georgian Institute of Public Affairs in partnership with the National Academy of Public Administration (USA). She holds the IMC designation.

Dr. Steffen Hörter Global Head of ESG

Dr Steffen Hörter is Global Head of ESG. He advises institutional investorsin Europe on investment strategy, risk management and sustainability. In recent years he has published various studies about incorporating sustainability into investment strategy. Prior to joining Allianz Global Investors, Dr Hoerter worked as a Management Consultant for banks and risk management at an international consultancy firm. Dr Hoerter studied Business Administration in Regensburg, Edinburgh and Ingolstadt/Eichstätt. He holds a doctorate from the Catholic University of Eichstätt-Ingolstadt, where he worked as a lecturer at the Department of Finance and Banking at WFI – Ingolstadt School of Management.

Robbie Miles, ACA ESG Analyst

Robbie is an ESG analyst with Allianz Global Investors, which he joined in 2014. He has analytical responsibilities on the Environmental, Social and Governance (ESG) Research team for the utilities and industrials sectors. He has three years of sustainable finance experience. Robbie qualified as a chartered accountant with PwC and holds a BA in Environment and Business from the University of Leeds.

Please find below biographies of the contributors to this edition of ESG Matters:

Marissa Blankenship ESG Analyst

Marissa Blankenship is a Senior ESG analyst with Allianz Global Investors, which she joined in 2011. As a member of the firm’s Environmental, Social and Governance (ESG) team, she is responsible for conducting research on the financial and real estate sectors and covering the cross-sectorial themes of business ethics, taxation, and ESG disclosure and reporting. She is also responsible for corporate governance and proxy voting for the UK, Spain and Latin American markets. Prior work experience in the sustainability field includes launching an impact investment fund of funds and serving as an advisor to a microfinance fund. Ms. Blankenship started her investment career as an associate in the equity-strategies group at Hall Capital Management in San Francisco. She has a BS in Economics from the University of California, Davis, an MSc in Latin American Economic Development from the University of London and is currently completing a Master’s in Sustainability Leadership from the University of Cambridge. Marissa holds the IMC designation.

Marie-Sybille Connan ESG Analyst

Ms. Connan is an ESG analyst with Allianz Global Investors, which she joined in 2008. As a member of the firm’s Environmental, Social and Governance (ESG) team, she is responsible for the energy, media and telecom sectors. Ms. Connan was previously a fund manager and credit analyst with the firm. She has 16 years of investment-industry experience. Before joining the firm, Ms. Connan was a senior credit analyst at Fortis Investments and Aviva Investors; before that, she worked at Natixis AM as a fund manager and equity analyst, focusing on IT and software. Ms. Connan has a master’s in finance from the ESC Montpellier Business School. She is a member of the French Society of Financial Analysts and a graduate of the Centre de Formation des Analystes Financiers.

Henrike Kulmann ESG Analyst

Ms. Kulmann is an ESG analyst with Allianz Global Investors, which she joined in 2011. She is a member of the Environmental, Social and Governance (ESG) research team and is responsible for ESG stock analysis, engagement and proxy voting. Ms. Kulmann has two years of investment-industry experience and five years of overall experience in the ESG field. She previously worked at Deutsche Post DHL in environmental-strategy management and corporate-responsibility evaluation. Ms. Kulmann has an M.A. in political science, with a focus on business communication and economics, from Friedrich Schiller University of Jena, Germany.

29

ESG Matters | Issue 13

30

Disclaimer

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission (SEC); Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; and Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator; Allianz Global Investors Korea Ltd., licensed by the Korea Financial Services Commission; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

31

For more ESG related articles please visit our website: www.ESGmatters.co.uk

Allianz Global Investors GmbH, UK Branch • 199 Bishopsgate • London • EC2M 3TYwww. allianzglobalinvestors.co.uk • Telephone: + 44 20 7859 9000

Allianz Global Investors GmbH, UK Branch199 BishopsgateLondon EC2M 3TYwww. allianzgi.co.uk

Telephone: 020 7859 9000

16-1

810

| Sep

tem

ber 2

016