Epic research special report of 23 oct 2015

8

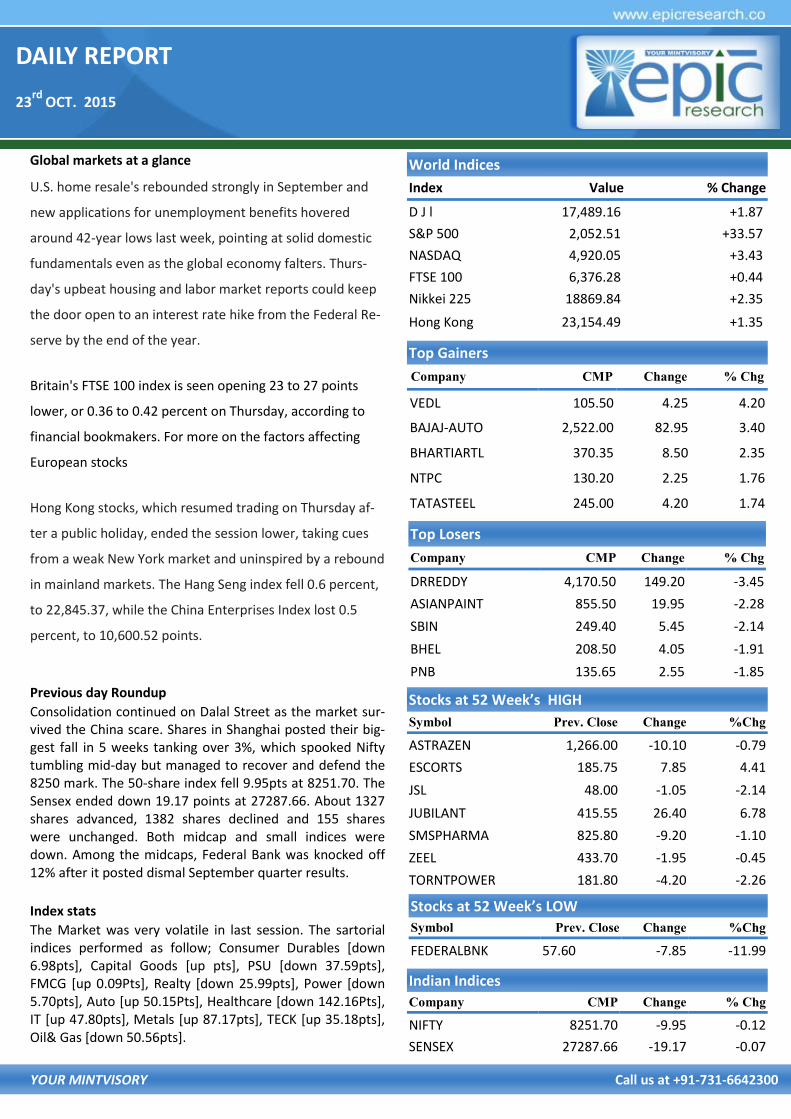

DAILY REPORT 23 rd OCT. 2015 YOUR MINTVISORY Call us at +91-731-6642300 Global markets at a glance U.S. home resale's rebounded strongly in September and new applications for unemployment benefits hovered around 42-year lows last week, pointing at solid domestic fundamentals even as the global economy falters. Thurs- day's upbeat housing and labor market reports could keep the door open to an interest rate hike from the Federal Re- serve by the end of the year. Britain's FTSE 100 index is seen opening 23 to 27 points lower, or 0.36 to 0.42 percent on Thursday, according to financial bookmakers. For more on the factors affecting European stocks Hong Kong stocks, which resumed trading on Thursday af- ter a public holiday, ended the session lower, taking cues from a weak New York market and uninspired by a rebound in mainland markets. The Hang Seng index fell 0.6 percent, to 22,845.37, while the China Enterprises Index lost 0.5 percent, to 10,600.52 points. Previous day Roundup Consolidation continued on Dalal Street as the market sur- vived the China scare. Shares in Shanghai posted their big- gest fall in 5 weeks tanking over 3%, which spooked Nifty tumbling mid-day but managed to recover and defend the 8250 mark. The 50-share index fell 9.95pts at 8251.70. The Sensex ended down 19.17 points at 27287.66. About 1327 shares advanced, 1382 shares declined and 155 shares were unchanged. Both midcap and small indices were down. Among the midcaps, Federal Bank was knocked off 12% after it posted dismal September quarter results. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 6.98pts], Capital Goods [up pts], PSU [down 37.59pts], FMCG [up 0.09Pts], Realty [down 25.99pts], Power [down 5.70pts], Auto [up 50.15Pts], Healthcare [down 142.16Pts], IT [up 47.80pts], Metals [up 87.17pts], TECK [up 35.18pts], Oil& Gas [down 50.56pts]. World Indices Index Value % Change D J l 17,489.16 +1.87 S&P 500 2,052.51 +33.57 NASDAQ 4,920.05 +3.43 FTSE 100 6,376.28 +0.44 Nikkei 225 18869.84 +2.35 Hong Kong 23,154.49 +1.35 Top Gainers Company CMP Change % Chg VEDL 105.50 4.25 4.20 BAJAJ-AUTO 2,522.00 82.95 3.40 BHARTIARTL 370.35 8.50 2.35 NTPC 130.20 2.25 1.76 TATASTEEL 245.00 4.20 1.74 Top Losers Company CMP Change % Chg DRREDDY 4,170.50 149.20 -3.45 ASIANPAINT 855.50 19.95 -2.28 SBIN 249.40 5.45 -2.14 BHEL 208.50 4.05 -1.91 PNB 135.65 2.55 -1.85 Stocks at 52 Week’s HIGH Symbol Prev. Close Change %Chg ASTRAZEN 1,266.00 -10.10 -0.79 ESCORTS 185.75 7.85 4.41 JSL 48.00 -1.05 -2.14 JUBILANT 415.55 26.40 6.78 SMSPHARMA 825.80 -9.20 -1.10 ZEEL 433.70 -1.95 -0.45 TORNTPOWER 181.80 -4.20 -2.26 Indian Indices Company CMP Change % Chg NIFTY 8251.70 -9.95 -0.12 SENSEX 27287.66 -19.17 -0.07 Stocks at 52 Week’s LOW Symbol Prev. Close Change %Chg FEDERALBNK 57.60 -7.85 -11.99

-

Upload

epic-research -

Category

Business

-

view

247 -

download

0

Transcript of Epic research special report of 23 oct 2015

DAILY REPORT

23rd

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

U.S. home resale's rebounded strongly in September and

new applications for unemployment benefits hovered

around 42-year lows last week, pointing at solid domestic

fundamentals even as the global economy falters. Thurs-

day's upbeat housing and labor market reports could keep

the door open to an interest rate hike from the Federal Re-

serve by the end of the year.

Britain's FTSE 100 index is seen opening 23 to 27 points

lower, or 0.36 to 0.42 percent on Thursday, according to

financial bookmakers. For more on the factors affecting

European stocks

Hong Kong stocks, which resumed trading on Thursday af-

ter a public holiday, ended the session lower, taking cues

from a weak New York market and uninspired by a rebound

in mainland markets. The Hang Seng index fell 0.6 percent,

to 22,845.37, while the China Enterprises Index lost 0.5

percent, to 10,600.52 points.

Previous day Roundup

Consolidation continued on Dalal Street as the market sur-vived the China scare. Shares in Shanghai posted their big-gest fall in 5 weeks tanking over 3%, which spooked Nifty tumbling mid-day but managed to recover and defend the 8250 mark. The 50-share index fell 9.95pts at 8251.70. The Sensex ended down 19.17 points at 27287.66. About 1327 shares advanced, 1382 shares declined and 155 shares were unchanged. Both midcap and small indices were down. Among the midcaps, Federal Bank was knocked off 12% after it posted dismal September quarter results.

Index stats

The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 6.98pts], Capital Goods [up pts], PSU [down 37.59pts], FMCG [up 0.09Pts], Realty [down 25.99pts], Power [down 5.70pts], Auto [up 50.15Pts], Healthcare [down 142.16Pts], IT [up 47.80pts], Metals [up 87.17pts], TECK [up 35.18pts], Oil& Gas [down 50.56pts].

World Indices

Index Value % Change

D J l 17,489.16 +1.87

S&P 500 2,052.51 +33.57

NASDAQ 4,920.05 +3.43

FTSE 100 6,376.28 +0.44

Nikkei 225 18869.84 +2.35

Hong Kong 23,154.49 +1.35

Top Gainers

Company CMP Change % Chg

VEDL 105.50 4.25 4.20

BAJAJ-AUTO 2,522.00 82.95 3.40

BHARTIARTL 370.35 8.50 2.35

NTPC 130.20 2.25 1.76

TATASTEEL 245.00 4.20 1.74

Top Losers

Company CMP Change % Chg

DRREDDY 4,170.50 149.20 -3.45

ASIANPAINT 855.50 19.95 -2.28

SBIN 249.40 5.45 -2.14

BHEL 208.50 4.05 -1.91

PNB 135.65 2.55 -1.85

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

ASTRAZEN 1,266.00 -10.10 -0.79

ESCORTS 185.75 7.85 4.41

JSL 48.00 -1.05 -2.14

JUBILANT 415.55 26.40 6.78

SMSPHARMA 825.80 -9.20 -1.10

ZEEL 433.70 -1.95 -0.45

TORNTPOWER 181.80 -4.20 -2.26

Indian Indices

Company CMP Change % Chg

NIFTY 8251.70 -9.95 -0.12

SENSEX 27287.66 -19.17 -0.07

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

FEDERALBNK 57.60 -7.85 -11.99

DAILY REPORT

23rd

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

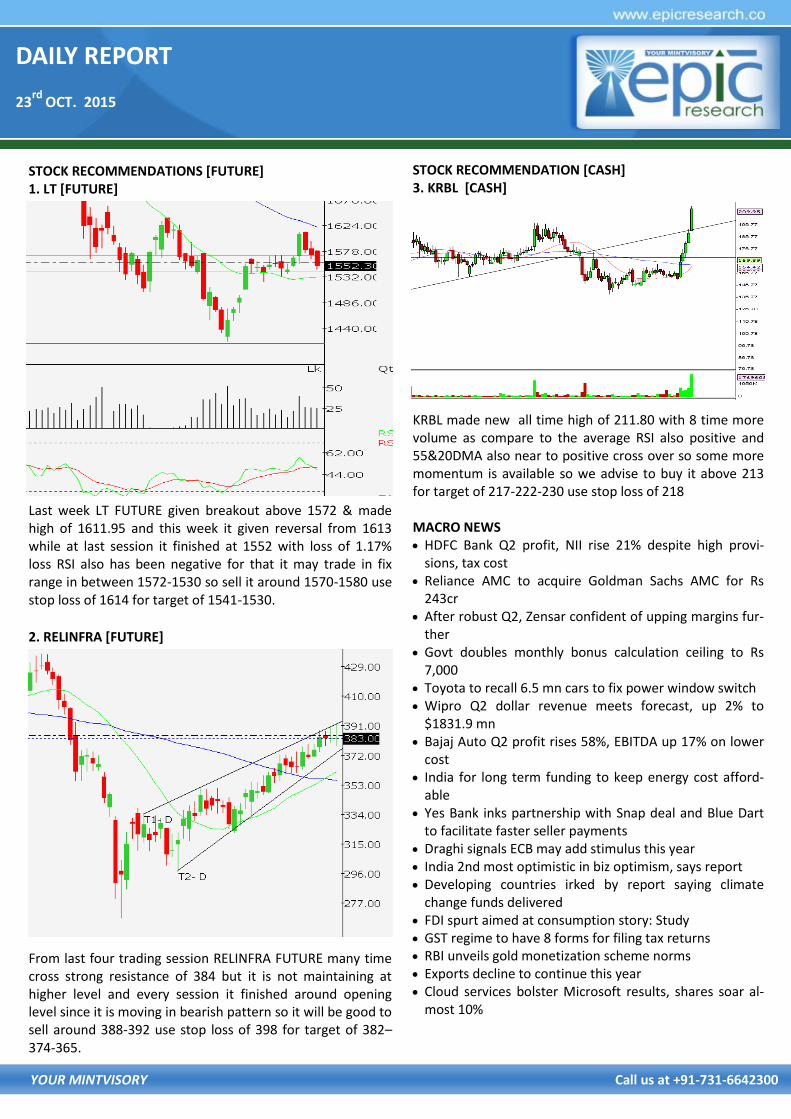

STOCK RECOMMENDATION [CASH] 3. KRBL [CASH]

KRBL made new all time high of 211.80 with 8 time more volume as compare to the average RSI also positive and 55&20DMA also near to positive cross over so some more momentum is available so we advise to buy it above 213 for target of 217-222-230 use stop loss of 218 MACRO NEWS HDFC Bank Q2 profit, NII rise 21% despite high provi-

sions, tax cost Reliance AMC to acquire Goldman Sachs AMC for Rs

243cr After robust Q2, Zensar confident of upping margins fur-

ther Govt doubles monthly bonus calculation ceiling to Rs

7,000 Toyota to recall 6.5 mn cars to fix power window switch Wipro Q2 dollar revenue meets forecast, up 2% to

$1831.9 mn Bajaj Auto Q2 profit rises 58%, EBITDA up 17% on lower

cost India for long term funding to keep energy cost afford-

able Yes Bank inks partnership with Snap deal and Blue Dart

to facilitate faster seller payments Draghi signals ECB may add stimulus this year India 2nd most optimistic in biz optimism, says report Developing countries irked by report saying climate

change funds delivered FDI spurt aimed at consumption story: Study GST regime to have 8 forms for filing tax returns RBI unveils gold monetization scheme norms Exports decline to continue this year Cloud services bolster Microsoft results, shares soar al-

most 10%

STOCK RECOMMENDATIONS [FUTURE] 1. LT [FUTURE]

Last week LT FUTURE given breakout above 1572 & made high of 1611.95 and this week it given reversal from 1613 while at last session it finished at 1552 with loss of 1.17% loss RSI also has been negative for that it may trade in fix range in between 1572-1530 so sell it around 1570-1580 use stop loss of 1614 for target of 1541-1530.

2. RELINFRA [FUTURE]

From last four trading session RELINFRA FUTURE many time cross strong resistance of 384 but it is not maintaining at higher level and every session it finished around opening level since it is moving in bearish pattern so it will be good to sell around 388-392 use stop loss of 398 for target of 382–374-365.

DAILY REPORT

23rd

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,300 42.75 10,16,691 60,90,450

NIFTY CE 8,200 96.60 5,58,046 48,56,875

BANKNIFTY CE 18,000 95.00 1,24,115 7,34,225

RELIANCE CE 980 4.85 12,033 7,35,500

INFY CE 1,200 2.80 5,945 33,68,250

TATASTEEL CE 250 3.95 5,454 15,01,000

LT CE 1,600 8.40 4,903 4,52,125

HDFCBANK CE 1,100 11.95 4,864 6,68,250

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 8,200 39.75 10,57,978 56,72,875

NIFTY PE 8,100 18.45 7,28,656 49,59,375

BANKNIFTY PE 17,500 137.00 99,988 4,59,150

RELIANCE PE 940 6.15 9,307 5,97,750

INFY PE 1,100 3.60 3,531 4,24,750

TATASTEEL PE 240 4.10 3,257 15,36,000

TATAMOTOR PE 370 4.20 3,229 9,61,000

BAJAJ AUTO PE 2,400 5.00 3,215 70,125

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 62898 1727.13 60921 1578.35 1000250 25833.3 148.788

INDEX OPTIONS 539607 14137.1 607953 15468.1 2478724 78356.4 -1331.01

STOCK FUTURES 142018 4278.99 137608 4224.56 1782558 49439.9 54.4293

STOCK OPTIONS 85377 2234.34 88142 2314.44 129858 3559.66 -80.098

TOTAL -1207.886

STOCKS IN NEWS PGCIL emerges lowest bidder for Rs 6,300-cr Vemagiri

II proj IOC sells rare Kandla cargo at small premium M&M pips Tata Motors in small commercial vehicle

sales HCL Tech to take over Volvo's IT operations, to rebadge

as many as 2600 staff Cipla gets FDA's nine observations and issues noticed

memo for Indore unit Apollo Health & Lifestyle to dilute stake raise Rs 500cr NIFTY FUTURE

In last trading session Nifty stayed volatile, after facing strong pressure in initial hours it recovered and closed flat with a Doji Candlestick. For future Nifty seems to touch at-least 8350 level, where it can face a strong re-sistance. So we advise you to buy Nifty Future at the lower levels around 8200-8240 for the targets of 8300 and 8400 with strict stop loss of 8090.

INDICES R2 R1 PIVOT S1 S2

NIFTY 8,332.00 8,291.00 8,255.00 8,213.00 8,176.00

BANK NIFTY 18,048.00 17,879.00 17,722.00 17,553.00 17,396.00

DAILY REPORT

23rd

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD DEC ABOVE 26900 TGTS 26980,27070 SL BE-

LOW 26800

SELL GOLD DEC BELOW 26700 TGTS 26620,26530 SL

ABOVE 25800

SILVER

TRADING STRATEGY:

BUY SILVER DEC ABOVE 37100 TGTS 37300,37700 SL BE-

LOW 36600

SELL SILVER DEC BELOW 36800 TGTS 36600,36300 SL

ABOVE 36900

COMMODITY ROUNDUP Copper was trading lower as prices were sliced by weaker data from China that was released third week. Chinese growth slipped to 6.9%. Meanwhile Chinese Copper produc-tion gained ground.MCX Copper was down 0.32% at Rs 341.40 per kg. The prices tested a high of Rs 343.25 per kg and a low of Rs 339.25 per kg .The latest data from China Bureau of Statistics was released showing a minor jump in refined Copper production of China. China's refined copper production rose 2.3 percent in September from the previ-ous month, hitting a three-month peak due to increasing output at some new smelters and higher supplies of raw material. Refined copper production reached 680,235 ton-nes in September, the highest since June and rising from 664,954 tonnes in August, data from the National Bureau of Statistics showed on Tuesday.

Gold stayed in a tight range today. The metal witnessed steady buying around lows under$1170 per ounce mark yesterday. Stocks stayed mostly choppy as traders stayed in awe of latest Chinese economic data though buying support continued to trickle in. Gold soared to highest levels in nearly four months last week following a break above the 100 day Exponential Moving Average (EMA) amid excellent spot market demand and rising global commodity prices. The COMEX Gold futures are trading at $1177 per ounce, down 0.04% on the day. MCX Gold futures are trading at Rs 27165 per 10 grams, up 0.20% on the day after hitting highs near Rs 27200 mark earlier in the day. The Indian Rupee weakened today, testing near its three week low of 65.20 per dollar mark. From the first oil boom in the 1970s, money sent from workers in West Asia has been a key source of dollars for India. In FY15, inward remittances were as big as IT exports and about 45 per cent of the trade deficit. Lower crude oil prices would impact inflows, as oil exporters adjust their economies to lower oil revenues. For the first time in 20 years, forex reserves of the top three oil exporters dipped in 2015. Remittances to India were stagnant in FY14 and FY15, in line with lower oil prices. Lower inflows would exert pres-sure on the current account deficit and the rupee.

Nickel prices dropped by Rs 3.30 to Rs 675.30 per kg in fu-tures trade today in tandem with a weakening trend at the London Metal Exchange and sluggish demand from alloy-makers in the domestic spot market. In futures trade at the Multi Commodity Exchange, nickel for delivery in current month contracts fell by Rs 3.30, or 0.49%, to Rs 675.30 per

DAILY REPORT

23rd

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX ROUNDUP

Extending its rising streak, barley prices flared up by Rs 30.50 to Rs 1,491.50 per quintal in futures trading as traders raised their bets supported by a firming trend at the spot markets on strong demand. At the NCDEX barley for delivery in far-month January contracts shot up by Rs 30.50, or 2.09 per cent, to Rs 1,491.50 per quintal, with an open interest of 300 lots. Barley for delivery in November added another Rs 24, or 1.71 per cent, to Rs 1,427 per quintal in an open interest of 16,410 lots. A firming trend at the spot markets on strong demand from consuming industries amid tight supplies from growing regions in spot markets sup-ported the upside in barley futures.

Refined soya oil prices were up by 1.09% to Rs 642.75 per 10 kg in futures trade as speculators enlarged their bets, driven by pick up in demand in the spot market. At NCDEX refined soya oil for delivery in November month went up by Rs 6.95, or 1.09% to Rs 642.75 per 10 kg with an open inter-est of 72,855 lots. The Dec contract gained Rs 6.40, or 1.01 per cent, to Rs 640 per 10 kg in 1,06,005 lots. The rise in refined soya oil futures to pick up demand in the spot mar-ket amid restricted supplies from producing regions.

Sugar prices were down 0.91 per cent to Rs 2,724 per quin-tal in futures trading as speculators trimmed positions, trig-gered by ample stocks at spot market on higher supplies from mills. At NCDEX sugar for delivery in December moved down by Rs 25, or 0.91 per cent, to Rs 2,724 per quintal with an open interest of 59,670 lots. Similarly, the sweet-ener for delivery in far-month March next year was trading lower by Rs 18, or 0.63 per cent, at Rs 2,826 per quintal in 24,720 lots. Adequate stocks position in the physical market on account of higher supplies from mills, mainly kept pres-sure on sugar prices at futures trade.

NCDEX INDICES

Index Value % Change

CAETOR SEED 4120 -0.84

CHANA 4907 -3.39

CORIANDER 11599 -4.00

COTTON SEED 1685 -0.82

GUAR SEED 4085 +1.62

JEERA 15990 -1.63

MUSTARDSEED 5049 +0.28

REF. SOY OIL 641 +0.82

TURMERIC 2742 -0.25

WHEAT 8310 +0.65

RECOMMENDATIONS

DHANIYA

BUY CORIANDER NOV ABOVE 11700 TARGET 11728 11808

SL BELOW 11673

SELL CORIANDER NOV BELOW 11600 TARGET 11572 11492

SL ABOVE 11627

GUARSGUM

BUY GUARGUM NOV ABOVE 8580 TARGET 8630 8700 SL

BELOW 8520

SELL GUARGUM NOV BELOW 8380 TARGET 8330 8260 SL

ABOVE 8440

DAILY REPORT

23rd

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 65.1513 Yen-100 54.3100

Euro 73.9728 GBP 100.5350

CURRENCY

USD/INR

BUY USD/INR OCT ABOVE 65.27 TARGET 65.4 65.55 SL BE-

LOW 65.07

SELL USD/INR OCT BELOW 65.16 TARGET 65.03 64.88 SL

ABOVE 65.36

EUR/INR

BUY EUR/INR OCT ABOVE 74.2 TARGET 74.35 74.55 SL BE-

LOW 74

SELL EUR/INR OCT BELOW 73.88 TARGET 73.73 73.53 SL

ABOVE 74.08

CURRENCY MARKET UPDATES: Most emerging Asian currencies eased on Thursday as a sharp fall in Chinese equities over the previous session deepened fears of a slump in the world's second-largest economy Indonesia's rupiah resisted the regional trend, jumping 1.6 per cent as share-buying inflows broke a four-day losing streakThe rupiah was helped by the finance min-ister saying Indonesia will hold its 2015 budget deficit esti-mate below 2.5 per cent despite an expected shortfall in tax revenue. The dollar edged slightly down against the euro on Thurs-day, but its losses were limited ahead of a European Cen-tral Bank meeting later in the day that could pave the way for further quantitative easing The ECB is likely to stop short of actually taking new policy steps at the meeting as it awaits fresh indications about the outlook for flagging euro zone inflation The rupee dropped 4 paise to 65.09 against the US dollar in early trade on Wednesday. The domestic currency had fallen 25 paise to settle above the psychological mark of 65 at 65.05 led by dollar buying by exporters and banks. While US Fed chair Janet Yellen's speech at the US Department of Labor in Washington overnight was expected to drop some cues on the possible outcome of the US Fed's October 27-28 policy review, she neither commented on the outlook for the US economy.

The dollar continued to climb against the other major cur-

rencies on Thursday, as dovish comments by European

Central Bank President Mario Draghi continued to domi-

nate investors' attention. The single currency was hit after

ECB President Mario Draghi said it will "reexamine" its

monetary policy in December, hinting at the possibility for

further easing measures. Speaking at the ECB's monthly press conference, Mr. Draghi added that the ECB's quantitative easing program is set to run until 2016 or beyond if necessary. .

DAILY REPORT

23rd

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

CALL REPORT

S T O

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

20/10/15 NCDEX DHANIYA NOV. BUY 12132 12160-12240 12105 SL TRIGGERED

20/10/15 NCDEX DHANIYA NOV. SELL 11930 11902-11822 11957 BOOKED FULL PROFIT

20/10/15 NCDEX GUARGUM NOV. BUY 8310 8360-8430 8250 BOOKED FULL PROFIT

20/10/15 NCDEX GUARGUM NOV. SELL 8150 8100-8030 8210 NOT EXECUTED

20/10/15 MCX GOLD DEC. BUY 26250 26330-26420 26150 NOT EXECUTED

20/10/15 MCX GOLD DEC. SELL 26100 26020-25930 26200 NOT EXECUTED

20/10/15 MCX SILVER DEC. BUY 37100 37300-37600 36800 NOT EXECUTED

20/10/15 MCX SILVER DEC. SELL 36800 36600-36300 37100 NOT EXECUTED

20/10/15 USD/INR OCT. BUY 65.15 65.28-65.43 64.95 BOOKED PROFIT

20/10/15 USD/INR OCT. SELL 64.90 64.77-64.62 65.10 NOT EXECUTED

20/10/15 EUR/INR OCT. BUY 74.15 74.30-74.5 73.95 SL TRIGGERED

20/10/15 EUR/INR OCT. SELL 73.98 73.83-73.63 74.18 NO PROFIT NO LOSS

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

20/10/15 NIFTY FUTURE BUY 8240 8340-8450 8090 CALL OPEN

20/10/15 AJANTA PHARMA FUTURE SELL 1582 1565-1545 1507 CALL OPEN

20/10/15 ARVIND FUTURE SELL 293-295 288-282 300 NOT EXECUTED

20/10/15 KWALITY CASH BUY 109 112-115 106 SL TRIGGERED

20/10/15 NIFTY FUTURE BUY 8240 8340-8450 8090 CALL OPEN

20/10/15 HCLTECH FUTURE BUY 858 860-875 836 CALL OPEN

09/10/15 NIFTY FUTURE SELL 8190 8070-7950 8380 CALL OPEN

09/10/15 NIFTY FUTURE SELL 8180 8100-7050 8350 CALL OPEN

DAILY REPORT

23rd

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, OCT. 19

10 AM HOME BUILDERS' INDEX OCT. 62 62

TUESDAY, OCT. 20

8:30 AM HOUSING STARTS SEPT. 1.131 MLN 1.126 MLN

WEDNESDAY, OCT. 21

NONE SCHEDULED

THURSDAY, OCT. 22

8:30 AM WEEKLY JOBLESS CLAIMS OCT. 10 N/A N/A

10 AM EXISTING HOME SALES SEPT. 5.31 MLN 5.31 MLN

FRIDAY, OCT. 23

NONE SCHEDULED