Epic research special report of 10 dec 2015

8

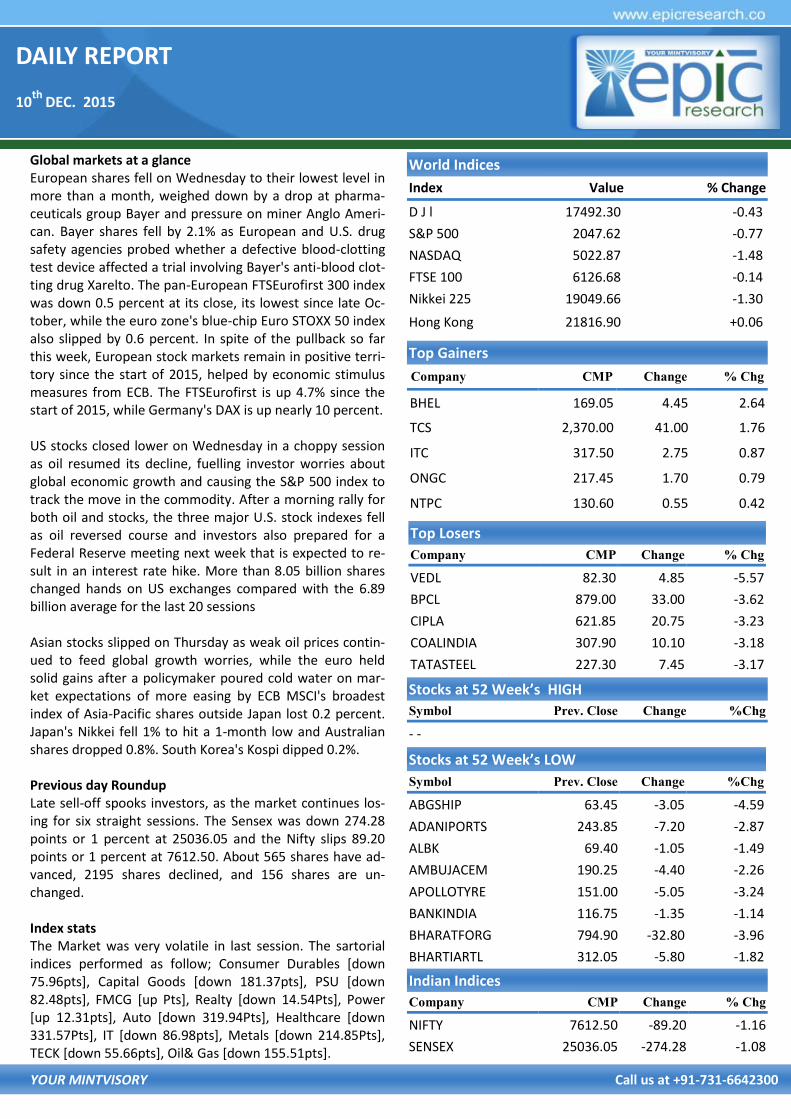

DAILY REPORT 10 th DEC. 2015 YOUR MINTVISORY Call us at +91-731-6642300 Global markets at a glance European shares fell on Wednesday to their lowest level in more than a month, weighed down by a drop at pharma- ceuticals group Bayer and pressure on miner Anglo Ameri- can. Bayer shares fell by 2.1% as European and U.S. drug safety agencies probed whether a defective blood-clotting test device affected a trial involving Bayer's anti-blood clot- ting drug Xarelto. The pan-European FTSEurofirst 300 index was down 0.5 percent at its close, its lowest since late Oc- tober, while the euro zone's blue-chip Euro STOXX 50 index also slipped by 0.6 percent. In spite of the pullback so far this week, European stock markets remain in positive terri- tory since the start of 2015, helped by economic stimulus measures from ECB. The FTSEurofirst is up 4.7% since the start of 2015, while Germany's DAX is up nearly 10 percent. US stocks closed lower on Wednesday in a choppy session as oil resumed its decline, fuelling investor worries about global economic growth and causing the S&P 500 index to track the move in the commodity. After a morning rally for both oil and stocks, the three major U.S. stock indexes fell as oil reversed course and investors also prepared for a Federal Reserve meeting next week that is expected to re- sult in an interest rate hike. More than 8.05 billion shares changed hands on US exchanges compared with the 6.89 billion average for the last 20 sessions Asian stocks slipped on Thursday as weak oil prices contin- ued to feed global growth worries, while the euro held solid gains after a policymaker poured cold water on mar- ket expectations of more easing by ECB MSCI's broadest index of Asia-Pacific shares outside Japan lost 0.2 percent. Japan's Nikkei fell 1% to hit a 1-month low and Australian shares dropped 0.8%. South Korea's Kospi dipped 0.2%. Previous day Roundup Late sell-off spooks investors, as the market continues los- ing for six straight sessions. The Sensex was down 274.28 points or 1 percent at 25036.05 and the Nifty slips 89.20 points or 1 percent at 7612.50. About 565 shares have ad- vanced, 2195 shares declined, and 156 shares are un- changed. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 75.96pts], Capital Goods [down 181.37pts], PSU [down 82.48pts], FMCG [up Pts], Realty [down 14.54Pts], Power [up 12.31pts], Auto [down 319.94Pts], Healthcare [down 331.57Pts], IT [down 86.98pts], Metals [down 214.85Pts], TECK [down 55.66pts], Oil& Gas [down 155.51pts]. World Indices Index Value % Change D J l 17492.30 -0.43 S&P 500 2047.62 -0.77 NASDAQ 5022.87 -1.48 FTSE 100 6126.68 -0.14 Nikkei 225 19049.66 -1.30 Hong Kong 21816.90 +0.06 Top Gainers Company CMP Change % Chg BHEL 169.05 4.45 2.64 TCS 2,370.00 41.00 1.76 ITC 317.50 2.75 0.87 ONGC 217.45 1.70 0.79 NTPC 130.60 0.55 0.42 Top Losers Company CMP Change % Chg VEDL 82.30 4.85 -5.57 BPCL 879.00 33.00 -3.62 CIPLA 621.85 20.75 -3.23 COALINDIA 307.90 10.10 -3.18 TATASTEEL 227.30 7.45 -3.17 Stocks at 52 Week’s HIGH Symbol Prev. Close Change %Chg - - Indian Indices Company CMP Change % Chg NIFTY 7612.50 -89.20 -1.16 SENSEX 25036.05 -274.28 -1.08 Stocks at 52 Week’s LOW Symbol Prev. Close Change %Chg ABGSHIP 63.45 -3.05 -4.59 ADANIPORTS 243.85 -7.20 -2.87 ALBK 69.40 -1.05 -1.49 AMBUJACEM 190.25 -4.40 -2.26 APOLLOTYRE 151.00 -5.05 -3.24 BANKINDIA 116.75 -1.35 -1.14 BHARATFORG 794.90 -32.80 -3.96 BHARTIARTL 312.05 -5.80 -1.82

-

Upload

epic-research -

Category

Business

-

view

111 -

download

0

Transcript of Epic research special report of 10 dec 2015

DAILY REPORT

10th

DEC. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance European shares fell on Wednesday to their lowest level in more than a month, weighed down by a drop at pharma-ceuticals group Bayer and pressure on miner Anglo Ameri-can. Bayer shares fell by 2.1% as European and U.S. drug safety agencies probed whether a defective blood-clotting test device affected a trial involving Bayer's anti-blood clot-ting drug Xarelto. The pan-European FTSEurofirst 300 index was down 0.5 percent at its close, its lowest since late Oc-tober, while the euro zone's blue-chip Euro STOXX 50 index also slipped by 0.6 percent. In spite of the pullback so far this week, European stock markets remain in positive terri-tory since the start of 2015, helped by economic stimulus measures from ECB. The FTSEurofirst is up 4.7% since the start of 2015, while Germany's DAX is up nearly 10 percent. US stocks closed lower on Wednesday in a choppy session as oil resumed its decline, fuelling investor worries about global economic growth and causing the S&P 500 index to track the move in the commodity. After a morning rally for both oil and stocks, the three major U.S. stock indexes fell as oil reversed course and investors also prepared for a Federal Reserve meeting next week that is expected to re-sult in an interest rate hike. More than 8.05 billion shares changed hands on US exchanges compared with the 6.89 billion average for the last 20 sessions Asian stocks slipped on Thursday as weak oil prices contin-ued to feed global growth worries, while the euro held solid gains after a policymaker poured cold water on mar-ket expectations of more easing by ECB MSCI's broadest index of Asia-Pacific shares outside Japan lost 0.2 percent. Japan's Nikkei fell 1% to hit a 1-month low and Australian shares dropped 0.8%. South Korea's Kospi dipped 0.2%. Previous day Roundup Late sell-off spooks investors, as the market continues los-ing for six straight sessions. The Sensex was down 274.28 points or 1 percent at 25036.05 and the Nifty slips 89.20 points or 1 percent at 7612.50. About 565 shares have ad-vanced, 2195 shares declined, and 156 shares are un-changed. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 75.96pts], Capital Goods [down 181.37pts], PSU [down 82.48pts], FMCG [up Pts], Realty [down 14.54Pts], Power [up 12.31pts], Auto [down 319.94Pts], Healthcare [down 331.57Pts], IT [down 86.98pts], Metals [down 214.85Pts], TECK [down 55.66pts], Oil& Gas [down 155.51pts].

World Indices

Index Value % Change

D J l 17492.30 -0.43

S&P 500 2047.62 -0.77

NASDAQ 5022.87 -1.48

FTSE 100 6126.68 -0.14

Nikkei 225 19049.66 -1.30

Hong Kong 21816.90 +0.06

Top Gainers

Company CMP Change % Chg

BHEL 169.05 4.45 2.64

TCS 2,370.00 41.00 1.76

ITC 317.50 2.75 0.87

ONGC 217.45 1.70 0.79

NTPC 130.60 0.55 0.42

Top Losers

Company CMP Change % Chg

VEDL 82.30 4.85 -5.57

BPCL 879.00 33.00 -3.62

CIPLA 621.85 20.75 -3.23

COALINDIA 307.90 10.10 -3.18

TATASTEEL 227.30 7.45 -3.17

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

- -

Indian Indices

Company CMP Change % Chg

NIFTY 7612.50 -89.20 -1.16

SENSEX 25036.05 -274.28 -1.08

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

ABGSHIP 63.45 -3.05 -4.59

ADANIPORTS 243.85 -7.20 -2.87

ALBK 69.40 -1.05 -1.49

AMBUJACEM 190.25 -4.40 -2.26

APOLLOTYRE 151.00 -5.05 -3.24

BANKINDIA 116.75 -1.35 -1.14

BHARATFORG 794.90 -32.80 -3.96

BHARTIARTL 312.05 -5.80 -1.82

DAILY REPORT

10th

DEC. 2015

YOUR MINTVISORY Call us at +91-731-6642300

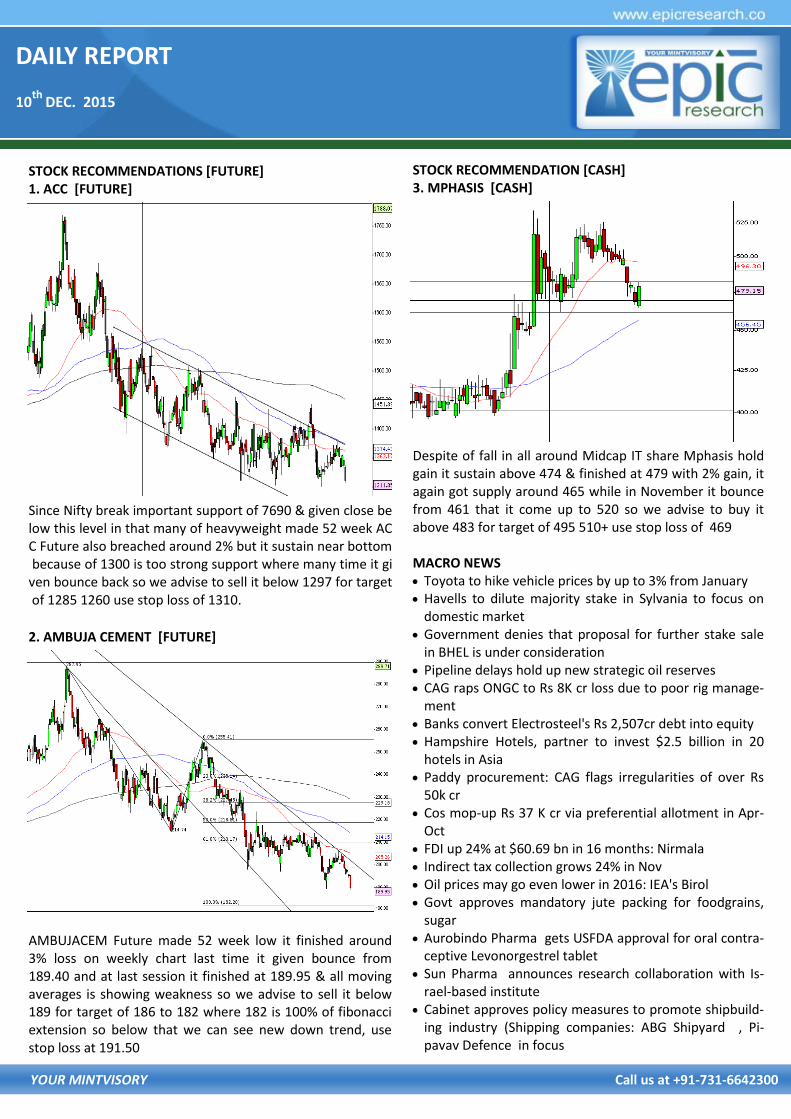

STOCK RECOMMENDATION [CASH] 3. MPHASIS [CASH]

Despite of fall in all around Midcap IT share Mphasis hold gain it sustain above 474 & finished at 479 with 2% gain, it again got supply around 465 while in November it bounce from 461 that it come up to 520 so we advise to buy it above 483 for target of 495 510+ use stop loss of 469 MACRO NEWS Toyota to hike vehicle prices by up to 3% from January Havells to dilute majority stake in Sylvania to focus on

domestic market Government denies that proposal for further stake sale

in BHEL is under consideration Pipeline delays hold up new strategic oil reserves CAG raps ONGC to Rs 8K cr loss due to poor rig manage-

ment Banks convert Electrosteel's Rs 2,507cr debt into equity Hampshire Hotels, partner to invest $2.5 billion in 20

hotels in Asia Paddy procurement: CAG flags irregularities of over Rs

50k cr Cos mop-up Rs 37 K cr via preferential allotment in Apr-

Oct FDI up 24% at $60.69 bn in 16 months: Nirmala Indirect tax collection grows 24% in Nov Oil prices may go even lower in 2016: IEA's Birol Govt approves mandatory jute packing for foodgrains,

sugar Aurobindo Pharma gets USFDA approval for oral contra-

ceptive Levonorgestrel tablet Sun Pharma announces research collaboration with Is-

rael-based institute Cabinet approves policy measures to promote shipbuild-

ing industry (Shipping companies: ABG Shipyard , Pi-pavav Defence in focus

STOCK RECOMMENDATIONS [FUTURE] 1. ACC [FUTURE]

Since Nifty break important support of 7690 & given close below this level in that many of heavyweight made 52 week ACC Future also breached around 2% but it sustain near bottom because of 1300 is too strong support where many time it given bounce back so we advise to sell it below 1297 for target of 1285 1260 use stop loss of 1310.

2. AMBUJA CEMENT [FUTURE]

AMBUJACEM Future made 52 week low it finished around 3% loss on weekly chart last time it given bounce from 189.40 and at last session it finished at 189.95 & all moving averages is showing weakness so we advise to sell it below 189 for target of 186 to 182 where 182 is 100% of fibonacci extension so below that we can see new down trend, use stop loss at 191.50

DAILY REPORT

10th

DEC. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 7,800 48.45 2,34,147 38,55,950

NIFTY CE 7,900 25.60 2,13,730 41,56,450

BANKNIFTY CE 17,500 67.50 54,506 5,90,610

TCS CE 2,400 30.25 3,134 3,34,000

LT CE 1,400 6.80 2,557 10,60,500

DLF CE 120 2.10 2,227 65,20,000

LT CE 1,350 15.65 2,159 5,02,800

RELIANCE CE 960 7.20 2,094 5,93,000

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts

Open

Interest

NIFTY PE 7,600 93.50 1,80,819 38,59,925

NIFTY PE 7,500 62.05 1,67,971 65,03,375

BANKNIFTY PE 16,500 229.30 50,306 5,60,910

LT PE 1,300 28.95 1,678 3,38,100

RELIANCE PE 900 9.85 1,670 5,08,000

MARUTI PE 4,500 97.00 1,448 1,14,875

DRREDDY PE 3,000 98.00 1,444 1,08,000

BHARATFORG PE 750 13.30 1,388 1,65,000

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 33997 1902.15 35590 2024.75 265675 14836.91 -122.60

INDEX OPTIONS 330552 18583.42 325981 18556.49 1243071 70307.46 26.93

STOCK FUTURES 67610 3256.27 65893 3175.07 1001833 48247.53 81.20

STOCK OPTIONS 40946 2013.95 42217 2078.69 55590 2660.82 -64.74

TOTAL -79.21

STOCKS IN NEWS

NBCC bags projects worth Rs 192.74 crore in Novem-ber

DrReddy submits response to USFDA over warning let-ter

JLR global wholesales up 23.5 percent at 51,021 units Infosys -Company invests USD 4 million in Israeli start-

up CloudEndure Wipro Digital opens new office in London; further hir-

ing planned SBI likely sell 15% stake in NSE and has started process Bharat Forge keeps revenue target for FY 2018 NIFTY FUTURE

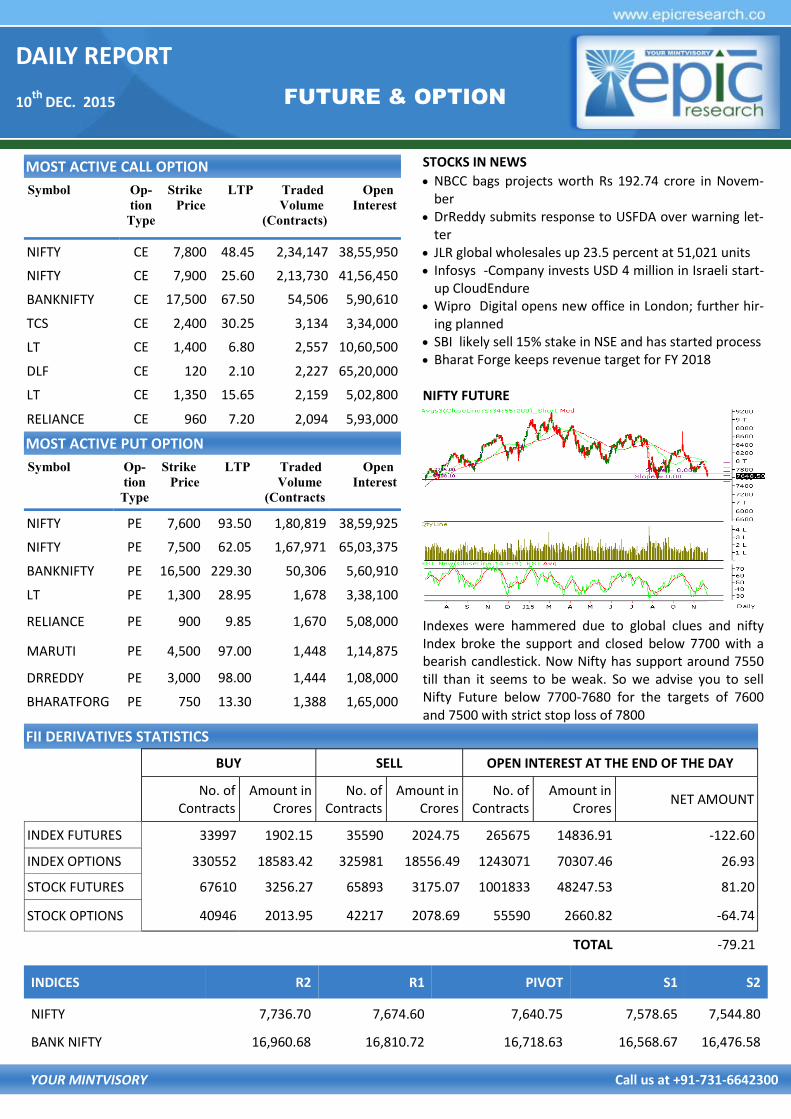

Indexes were hammered due to global clues and nifty Index broke the support and closed below 7700 with a bearish candlestick. Now Nifty has support around 7550 till than it seems to be weak. So we advise you to sell Nifty Future below 7700-7680 for the targets of 7600 and 7500 with strict stop loss of 7800

INDICES R2 R1 PIVOT S1 S2

NIFTY 7,736.70 7,674.60 7,640.75 7,578.65 7,544.80

BANK NIFTY 16,960.68 16,810.72 16,718.63 16,568.67 16,476.58

DAILY REPORT

10th

DEC. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD FEB ABOVE 25600 TGTS 25680,25770 SL BELOW

25500

SELL GOLD FEB BELOW 25400 TGTS 25320,25230 SL

ABOVE 25500

SILVER

TRADING STRATEGY:

BUY SILVER MAR ABOVE 34600 TGTS 34800,35100 SL BE-

LOW 34100

SELL SILVER MAR BELOW 34300 TGTS 34100,33800 SL

ABOVE 34600

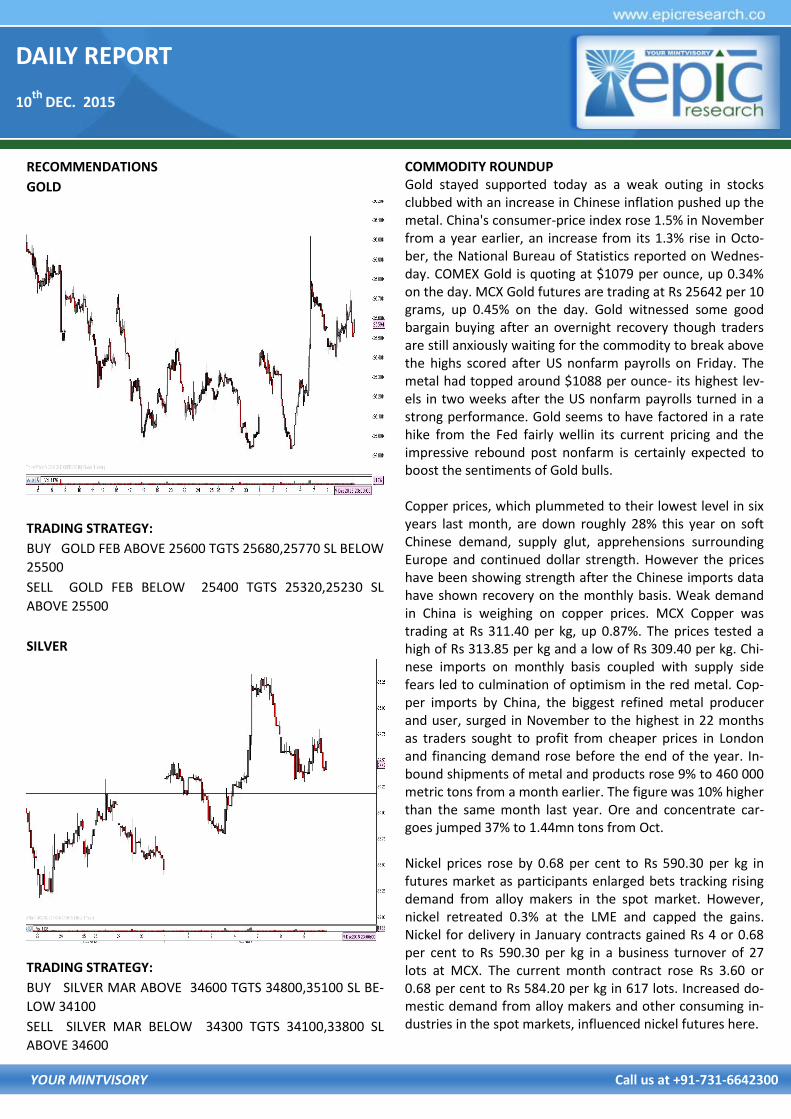

COMMODITY ROUNDUP Gold stayed supported today as a weak outing in stocks clubbed with an increase in Chinese inflation pushed up the metal. China's consumer-price index rose 1.5% in November from a year earlier, an increase from its 1.3% rise in Octo-ber, the National Bureau of Statistics reported on Wednes-day. COMEX Gold is quoting at $1079 per ounce, up 0.34% on the day. MCX Gold futures are trading at Rs 25642 per 10 grams, up 0.45% on the day. Gold witnessed some good bargain buying after an overnight recovery though traders are still anxiously waiting for the commodity to break above the highs scored after US nonfarm payrolls on Friday. The metal had topped around $1088 per ounce- its highest lev-els in two weeks after the US nonfarm payrolls turned in a strong performance. Gold seems to have factored in a rate hike from the Fed fairly wellin its current pricing and the impressive rebound post nonfarm is certainly expected to boost the sentiments of Gold bulls. Copper prices, which plummeted to their lowest level in six years last month, are down roughly 28% this year on soft Chinese demand, supply glut, apprehensions surrounding Europe and continued dollar strength. However the prices have been showing strength after the Chinese imports data have shown recovery on the monthly basis. Weak demand in China is weighing on copper prices. MCX Copper was trading at Rs 311.40 per kg, up 0.87%. The prices tested a high of Rs 313.85 per kg and a low of Rs 309.40 per kg. Chi-nese imports on monthly basis coupled with supply side fears led to culmination of optimism in the red metal. Cop-per imports by China, the biggest refined metal producer and user, surged in November to the highest in 22 months as traders sought to profit from cheaper prices in London and financing demand rose before the end of the year. In-bound shipments of metal and products rose 9% to 460 000 metric tons from a month earlier. The figure was 10% higher than the same month last year. Ore and concentrate car-goes jumped 37% to 1.44mn tons from Oct. Nickel prices rose by 0.68 per cent to Rs 590.30 per kg in futures market as participants enlarged bets tracking rising demand from alloy makers in the spot market. However, nickel retreated 0.3% at the LME and capped the gains. Nickel for delivery in January contracts gained Rs 4 or 0.68 per cent to Rs 590.30 per kg in a business turnover of 27 lots at MCX. The current month contract rose Rs 3.60 or 0.68 per cent to Rs 584.20 per kg in 617 lots. Increased do-mestic demand from alloy makers and other consuming in-dustries in the spot markets, influenced nickel futures here.

DAILY REPORT

10th

DEC. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX ROUNDUP Sugar prices softened 0.28% to Rs 2,830 per quintal in fu-tures market as participants reduced exposure, driven by adequate stocks at the spot market on higher supplies from mills. In futures trading at NCDEX sugar for delivery in De-cember declined by Rs 8 or 0.28% to Rs 2,830 per quintal with an OI of 48,410 lots. The sweetener for delivery in far-month March next year contracts eased by Rs 6 or 0.20 per cent to Rs 2,970 per quintal in 84,990 lots. Offloading of positions by participants triggered by ample stocks position in the physical market on higher supplies from mills, mainly kept pressure on sugar prices at futures trade. Maize has witnessed some selling due to possibility of strong supplies in the current rabi season along with antici-pation of strong imports in local mandies. Favourable rain-fall in Tamilnadu and Karantaka will encourage strong rabi supplies in the current year. However, latest USDA report is projecting weak total production of the current year. kharif corn production is estimated to decline by 2- 3 MMT over last year (16.4 MMT). While the planting for rabi corn is likely to be higher than last year, continued dry conditions (soil moisture and irrigation water availability) is likely to affect the overall yields. Consequently, MY 2015/16 produc-tion is forecast lower at 21 MMT, which includes 14 MMT kharif corn and 7 MMT rabi corn. MY 2015/16 consumption forecast is revised lower to 21.4 MMT on forecast tight do-mestic supplies, expected firm domestic prices and rela-tively stagnant growth in the consuming sectors (poultry feed and starch). MY 2015/16 export forecast is revised lower to 1.0 MMT on continued weak export demand and relatively tight domestic supplies. The NCDEX Jan futures declined by 0.17% today to trade at Rs 1547 per quintal.

NCDEX INDICES

Index Value % Change

CAETOR SEED 3663 -3.98

CHANA 5090 +1.70

CORIANDER 10360 +1.99

COTTON SEED 1774 +0.97

GUAR SEED 3188 -2.33

JEERA 15100 -1.31

MUSTARDSEED 4608 -1.50

REF. SOY OIL 632.95 +0.05

SUGAR M GRADE 2874 +1.27

TURMERIC 9250 -0.77

RECOMMENDATIONS

DHANIYA

BUY CORIANDER JAN ABOVE 10240 TARGET 10285 10435

SL BELOW 10175

SELL CORIANDER JAN BELOW 10100 TARGET 10055 9905 SL

ABOVE 10165

GUARSGUM

BUY GUARGUM JAN ABOVE 6200 TARGET 6250 6320 SL BE-

LOW 6140

SELL GUARGUM JAN BELOW 6070 TARGET 6020 5950 SL

ABOVE 6130

DAILY REPORT

10th

DEC. 2015

YOUR MINTVISORY Call us at +91-731-6642300

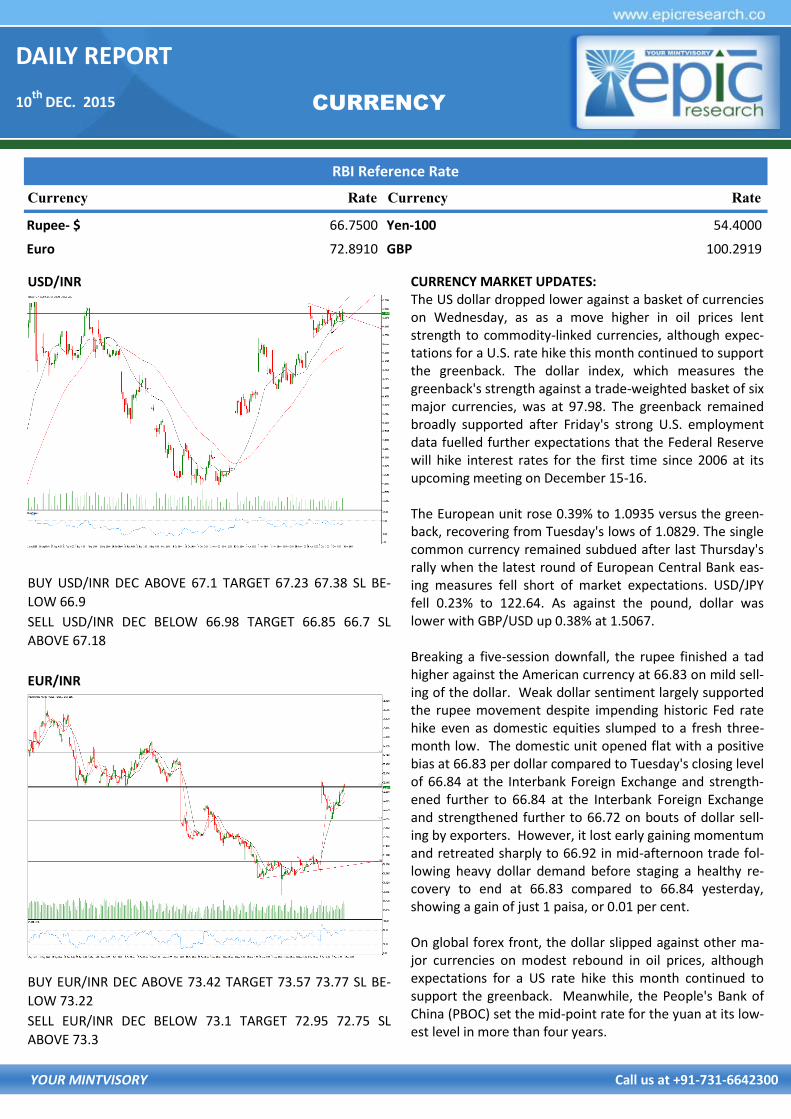

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 66.7500 Yen-100 54.4000

Euro 72.8910 GBP 100.2919

CURRENCY

USD/INR

BUY USD/INR DEC ABOVE 67.1 TARGET 67.23 67.38 SL BE-

LOW 66.9

SELL USD/INR DEC BELOW 66.98 TARGET 66.85 66.7 SL

ABOVE 67.18

EUR/INR

BUY EUR/INR DEC ABOVE 73.42 TARGET 73.57 73.77 SL BE-

LOW 73.22

SELL EUR/INR DEC BELOW 73.1 TARGET 72.95 72.75 SL

ABOVE 73.3

CURRENCY MARKET UPDATES: The US dollar dropped lower against a basket of currencies on Wednesday, as as a move higher in oil prices lent strength to commodity-linked currencies, although expec-tations for a U.S. rate hike this month continued to support the greenback. The dollar index, which measures the greenback's strength against a trade-weighted basket of six major currencies, was at 97.98. The greenback remained broadly supported after Friday's strong U.S. employment data fuelled further expectations that the Federal Reserve will hike interest rates for the first time since 2006 at its upcoming meeting on December 15-16. The European unit rose 0.39% to 1.0935 versus the green-back, recovering from Tuesday's lows of 1.0829. The single common currency remained subdued after last Thursday's rally when the latest round of European Central Bank eas-ing measures fell short of market expectations. USD/JPY fell 0.23% to 122.64. As against the pound, dollar was lower with GBP/USD up 0.38% at 1.5067. Breaking a five-session downfall, the rupee finished a tad higher against the American currency at 66.83 on mild sell-ing of the dollar. Weak dollar sentiment largely supported the rupee movement despite impending historic Fed rate hike even as domestic equities slumped to a fresh three-month low. The domestic unit opened flat with a positive bias at 66.83 per dollar compared to Tuesday's closing level of 66.84 at the Interbank Foreign Exchange and strength-ened further to 66.84 at the Interbank Foreign Exchange and strengthened further to 66.72 on bouts of dollar sell-ing by exporters. However, it lost early gaining momentum and retreated sharply to 66.92 in mid-afternoon trade fol-lowing heavy dollar demand before staging a healthy re-covery to end at 66.83 compared to 66.84 yesterday, showing a gain of just 1 paisa, or 0.01 per cent. On global forex front, the dollar slipped against other ma-jor currencies on modest rebound in oil prices, although expectations for a US rate hike this month continued to support the greenback. Meanwhile, the People's Bank of China (PBOC) set the mid-point rate for the yuan at its low-est level in more than four years.

DAILY REPORT

10th

DEC. 2015

YOUR MINTVISORY Call us at +91-731-6642300

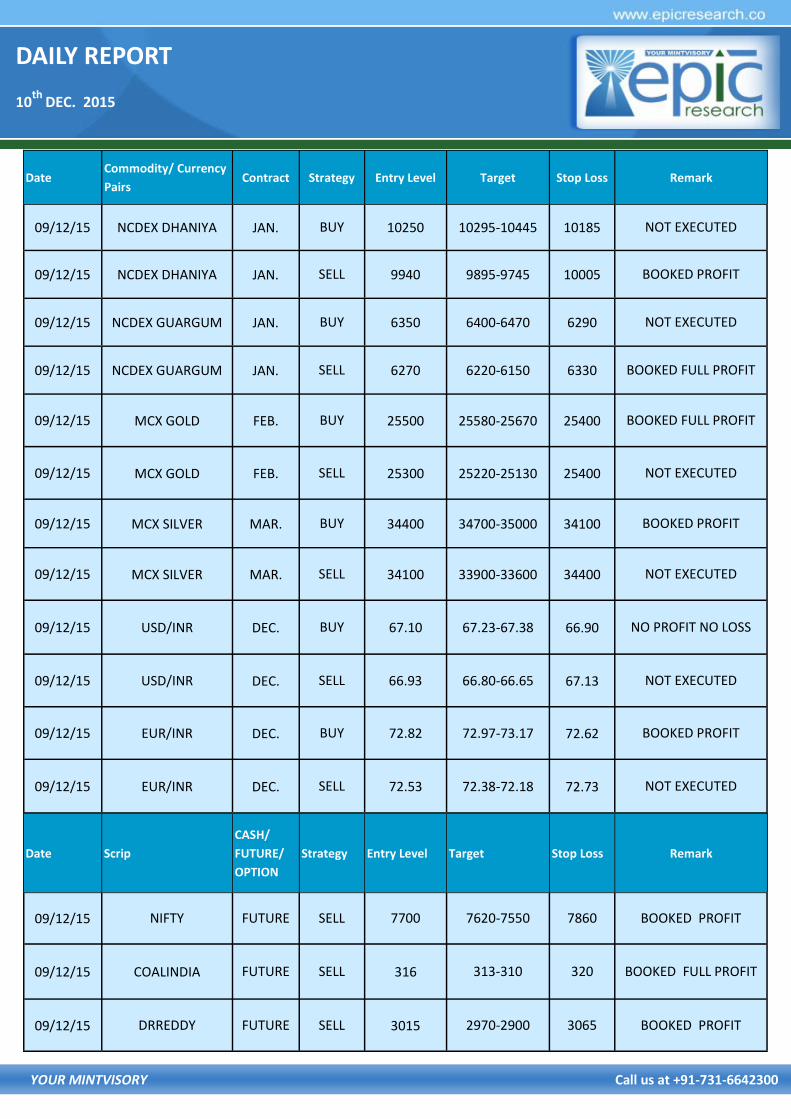

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

09/12/15 NCDEX DHANIYA JAN. BUY 10250 10295-10445 10185 NOT EXECUTED

09/12/15 NCDEX DHANIYA JAN. SELL 9940 9895-9745 10005 BOOKED PROFIT

09/12/15 NCDEX GUARGUM JAN. BUY 6350 6400-6470 6290 NOT EXECUTED

09/12/15 NCDEX GUARGUM JAN. SELL 6270 6220-6150 6330 BOOKED FULL PROFIT

09/12/15 MCX GOLD FEB. BUY 25500 25580-25670 25400 BOOKED FULL PROFIT

09/12/15 MCX GOLD FEB. SELL 25300 25220-25130 25400 NOT EXECUTED

09/12/15 MCX SILVER MAR. BUY 34400 34700-35000 34100 BOOKED PROFIT

09/12/15 MCX SILVER MAR. SELL 34100 33900-33600 34400 NOT EXECUTED

09/12/15 USD/INR DEC. BUY 67.10 67.23-67.38 66.90 NO PROFIT NO LOSS

09/12/15 USD/INR DEC. SELL 66.93 66.80-66.65 67.13 NOT EXECUTED

09/12/15 EUR/INR DEC. BUY 72.82 72.97-73.17 72.62 BOOKED PROFIT

09/12/15 EUR/INR DEC. SELL 72.53 72.38-72.18 72.73 NOT EXECUTED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

09/12/15 NIFTY FUTURE SELL 7700 7620-7550 7860 BOOKED PROFIT

09/12/15 COALINDIA FUTURE SELL 316 313-310 320 BOOKED FULL PROFIT

09/12/15 DRREDDY FUTURE SELL 3015 2970-2900 3065 BOOKED PROFIT

DAILY REPORT

10th

DEC. 2015

YOUR MINTVISORY Call us at +91-731-6642300

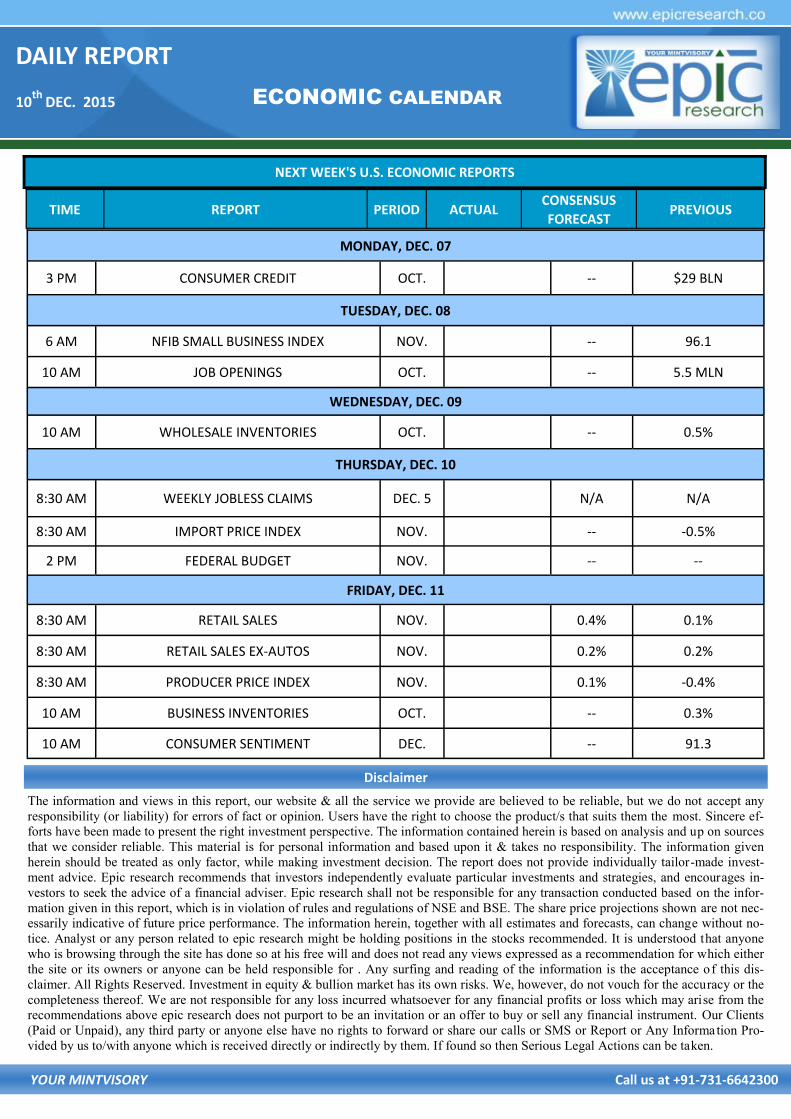

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, DEC. 07

3 PM CONSUMER CREDIT OCT. -- $29 BLN

TUESDAY, DEC. 08

6 AM NFIB SMALL BUSINESS INDEX NOV. -- 96.1

10 AM JOB OPENINGS OCT. -- 5.5 MLN

WEDNESDAY, DEC. 09

10 AM WHOLESALE INVENTORIES OCT. -- 0.5%

THURSDAY, DEC. 10

8:30 AM WEEKLY JOBLESS CLAIMS DEC. 5 N/A N/A

8:30 AM IMPORT PRICE INDEX NOV. -- -0.5%

2 PM FEDERAL BUDGET NOV. -- --

FRIDAY, DEC. 11

8:30 AM RETAIL SALES NOV. 0.4% 0.1%

8:30 AM RETAIL SALES EX-AUTOS NOV. 0.2% 0.2%

8:30 AM PRODUCER PRICE INDEX NOV. 0.1% -0.4%

10 AM BUSINESS INVENTORIES OCT. -- 0.3%

10 AM CONSUMER SENTIMENT DEC. -- 91.3