English

32

Money Matters NxLeveL Guide to Money Management

-

Upload

saina33 -

Category

Economy & Finance

-

view

172 -

download

0

Transcript of English

Money Matters

NxLeveL Guide toMoney Management

Getting Started

Discussion Topics

Household Budgeting Setting Financial Goals Personal Financial Statement Understanding Credit Debt ~ is it for you? Linking Personal & Business Finances Borrowing for your Business The Lender Relationship Take the First Step

Household Budgeting

Sample of Household Budget Categories

Income Salary Partner’s Salary Public Assistance Child Support/Alimony Other

Expenses Living/Housing Regular Payments Food Personal Transportation Charity, Donations Savings Other

Setting Financial Goals

The Planning Cycle

Set Goals

Create thePlan

Work the Plan

Make Changes

Analyze the Situation

What are Your Goals?

Immediate Within 1year

Short Term 2-5 years

Long Term 5+ years

U.S. Personal Savings Rate (1960-2008)

0

2

4

6

8

10

12

14

1960

1975

1990

2005

Perc

en

t o

f D

isp

osab

le In

co

me

Personal Financial Statement

Assets = Liabilities + Net Worth

Understanding Credit

Credit Report Basics

Four Types of Information

Identification Name, address(es), Social Security number, birth date,

employers, etc. Credit History

Account information, credit/loan limits, payment history, balances due

Public Records Bankruptcies, tax liens, criminal records, other

Inquiries Requests for your credit history

Elements of Credit Score

35%

30%

15%

10%

10%

Payment History

Amounts Ow ed

Length of Credit History

New Credit

Types of Credit Used

Rebuilding & Protecting Your Credit

Reduce existing debt … Stop spending! Stick to a budget Pay bills on time Make more than the minimum monthly payment Don’t carry too many credit cards Get copy of Credit Report annually Fix discrepancies ~ in writing Carefully guard your Social Security Number and

other personal information Beware of Identity Theft schemes

Debt ~ Is it for You?

Types of Debt

Short term Less than one year Personal: Consumables (restaurants, clothing, vacations, etc) Business: Working capital, supplies, seasonal inventory, lines of

credit, etc.

Intermediate term 2-10 years Personal: Auto or student loans Business: Furniture & fixtures, leasehold improvements,

equipment

Long term 10+ years Personal: Home mortgage, property Business: Real estate, large equipment, initial business purchase

Caution: Not all debt is created equal

Pay Check Loans Easy to arrange Extremely high interest rates, restrictive terms Committing future pay as a guarantee to repay the debt

Rent to Own Easy; down payment is usually not required Rent an item for a short period before returning If all payments are made, you own it; if not, it will be repossessed for as

little as one missed payment Extremely high interest rates; may pay more than double or triple the

original purchase price by the end

Layaway Making a resurgence as our economy struggles Retailer holds an item for you; no credit history is required Store keeps the money as you make payments; fee is charged Retailer may go out of business and/or you may incur extra expenses if

you later change your mind

Caution: Not all debt is created equal

Car Title Loans Similar to rent to own; easy to access Lender holds the title of vehicle until all payments are received High interest rates; vehicle repossessed if payments are missed

Pawn Shops Quick money using your valuables as collateral No questions are asked Extremely high interest rates; shop can sell your property if you

do not pay Loan is for only a small portion of the true value of your items

Quick Tax Refund Loan against your expected tax refund Quick access to money; high interest rates; refund may be

delayed An alternative is electronic filing or using a VITA (Volunteers

Income Tax Assistance) Center to assist you

Spending Choices

5-10%Savings & Investments

10-20%Debt & Obligations

10-15%Transportation

25-40%Living

20-35 % own15-20% rent

Housing

Linking Personal & Business

Why do we care?

Keeping the Books

Balance SheetPersonal Financial Statement

Cash Flow StatementProfit & Loss Statement

Balancing your Checking Account

Business BudgetHousehold Budget

BusinessPersonal

Borrowing for Your Business

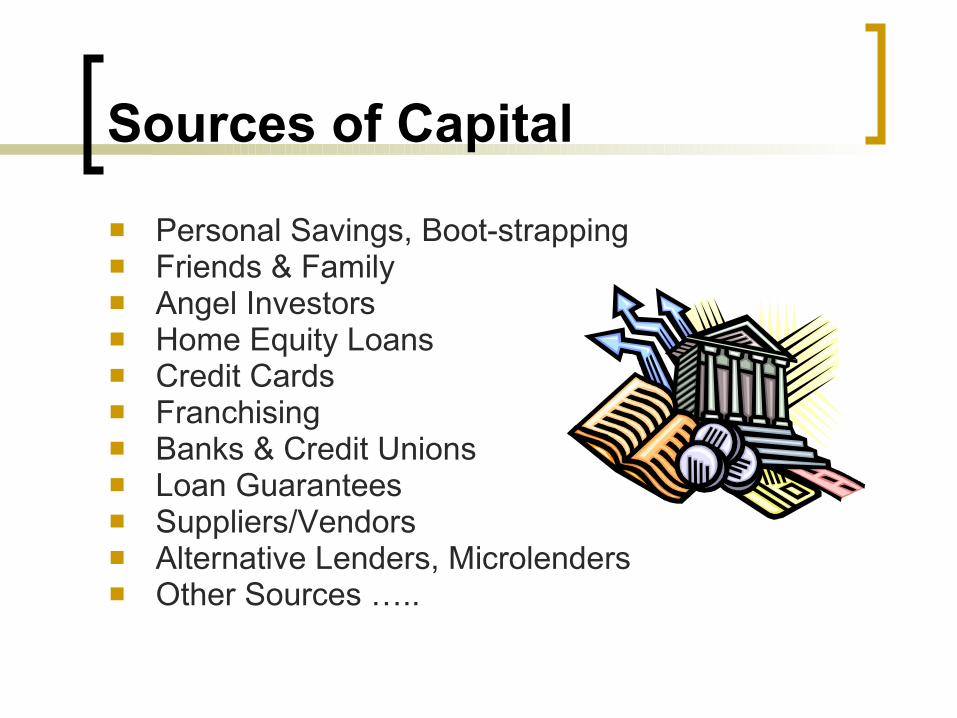

Sources of Capital

Personal Savings, Boot-strapping Friends & Family Angel Investors Home Equity Loans Credit Cards Franchising Banks & Credit Unions Loan Guarantees Suppliers/Vendors Alternative Lenders, Microlenders Other Sources …..

Business Financing

Debt Financing Money borrowed for a business A promise to pay back at a later time, with interest Payment varies on terms (amount, length of loan,

interest rate) Receive money upfront in one lump sum Repaid via a standard repayment schedule; amount

typically does not vary Common sources: Banks, Credit Unions, Alternative

Lenders

Business Financing

Equity Financing Money invested by the owner(s) Sell partial ownership of business in exchange for

financial investment Receive money upfront in one lump sum Terms vary greatly based upon owner & investor

negotiations; share risks and profits (or losses) No monthly payments, but high rate of return

expected in future

C’s of Credit

Character Credit Concept Collateral Conditions

What to Look for in a Lender

Listens Answers all questions Interested in working with you Familiar with your type of business Works with your size of $ request Explains terms & options clearly Does not talk down to you Returns all phone calls & emails Provides references, if asked Trustworthy, honest, flexible, timely Interested in a long-term relationship

Preparing for the Loan Process

Investigate multiple lenders Find lenders that regularly lend to small business Learn their preferences and requirements

Get your personal records in order Check your credit history, know your credit score Update your Personal Financial Statement

Get your business records in order Write/update your business plan Prepare financial projections for your business Know what records will be requested

Understand your commitments What is your financial investment What will you pledge as collateral Understand personal guarantee requirements

Set expectations Be prepared for “personal” questions Have patience

Next Steps

Next Steps

Know Your Baseline Household Budget Personal Financial Statement Credit Report, Credit Score

Set Financial Goals Address Credit Challenges

Rebuild & Protect your Credit Spending Plan

Prepare for Your Business Write/update a Business Plan

Take Action Today! Have fun ~ enjoy the ride!

If you don’t write it down,it doesn’t happen!

My Action Items:

1.

2.

3.

![...(EPUU) 21 I English IA] r Integrated English rintegrated English 101), rintegrated English 11 I I Is English IJ e. UT, rAdvanced English 11], English 111] r Integrated English Study](https://static.fdocuments.net/doc/165x107/5f9c0b33f8367823672ad80f/-epuu-21-i-english-ia-r-integrated-english-rintegrated-english-101-rintegrated.jpg)