Eng. Osama Al-Mobarak Director of Kafalah Financing Guarantee Program, SIDF (K.S.A)

24

Eng. Osama Al-Mobarak Director of Kafalah Financing Guarantee Program, SIDF (K.S.A)

-

Upload

cathleen-porter -

Category

Documents

-

view

219 -

download

0

Transcript of Eng. Osama Al-Mobarak Director of Kafalah Financing Guarantee Program, SIDF (K.S.A)

Eng. Osama Al-Mobarak Director of Kafalah Financing Guarantee Program, SIDF (K.S.A)

1. The Role of Kafalah in Supporting SMEs

2. Kafalah’s Achievements Since its Inception (2006 – 2014)

3. Challenges Facing Kafalah & Kafalah’s Responsive

Actions

2

The Role of Kafalah in Supporting

SMEs

4

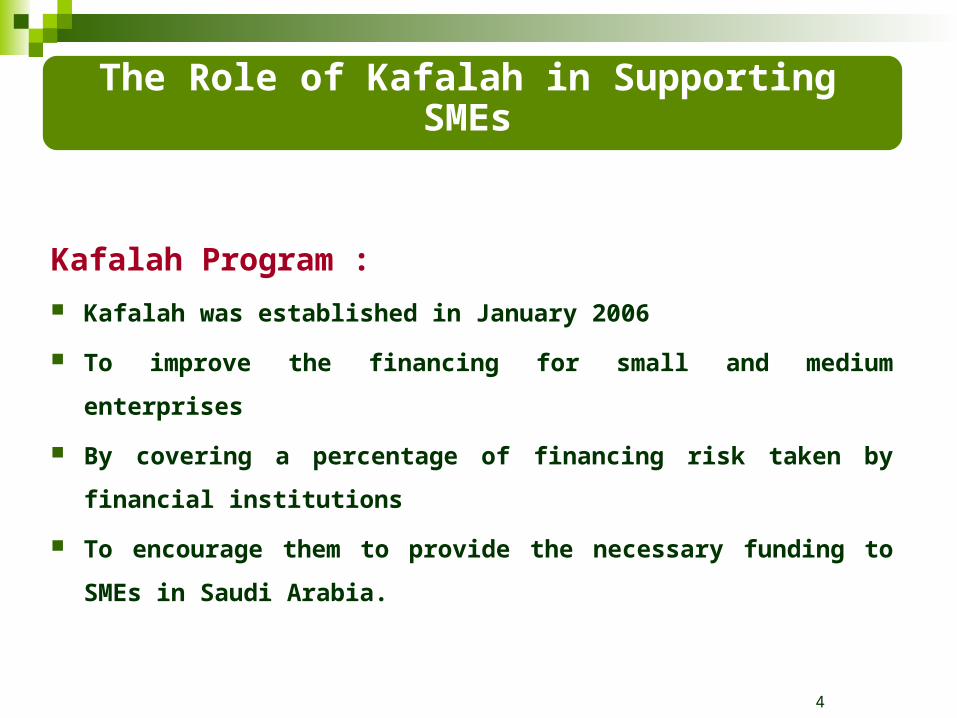

Kafalah Program :

Kafalah was established in January 2006

To improve the financing for small and medium enterprises

By covering a percentage of financing risk taken by financial

institutions

To encourage them to provide the necessary funding to SMEs

in Saudi Arabia.

The Role of Kafalah in Supporting SMEs

5

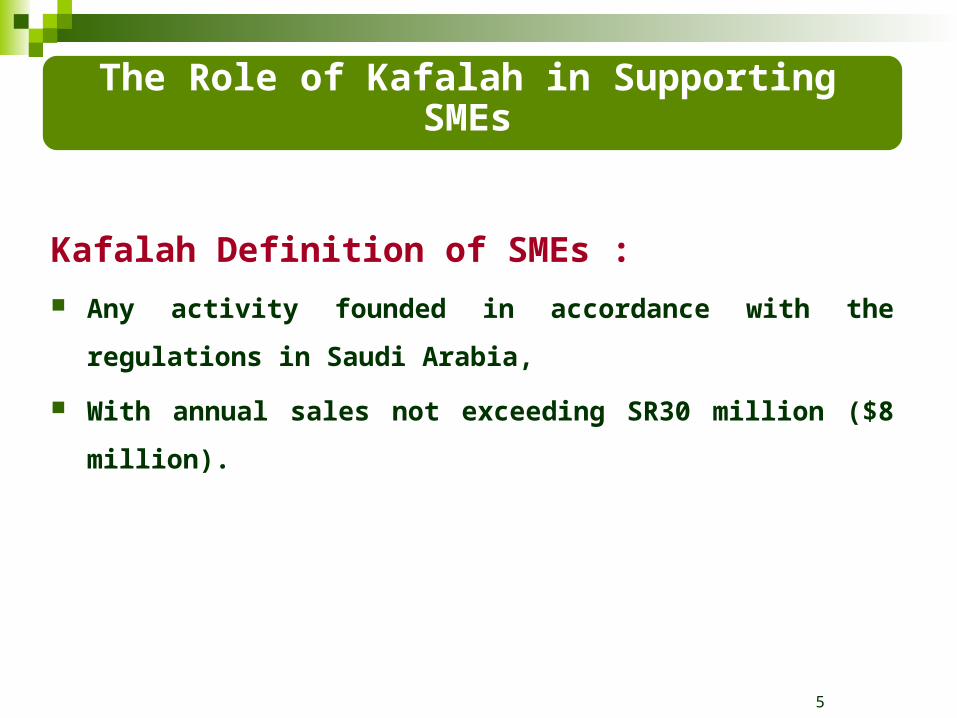

Kafalah Definition of SMEs :

Any activity founded in accordance with the regulations in

Saudi Arabia,

With annual sales not exceeding SR30 million ($8 million).

The Role of Kafalah in Supporting SMEs

Program Vision :

The Program aims to foster, support and develop SMEs to

enable them to contribute positively to the social and economic

development.

The Program seeks to increase the level of financing provided

by local financial institutions to SMEs through provision of

guarantee services.

6

The Role of Kafalah in Supporting SMEs

The Program’s capital is about SR 200 million :

SR 100 million granted by the Ministry of Finance

Around SR 100 million granted by Saudi commercial banks

7

The Role of Kafalah in Supporting SMEs

SME• Seeks

funding

Banks• Require additional

security to provide loans

Kafalah• Issues guarantee

to bank max 80% of funding value

8

Kafalah Process :

The Role of Kafalah in Supporting SMEs

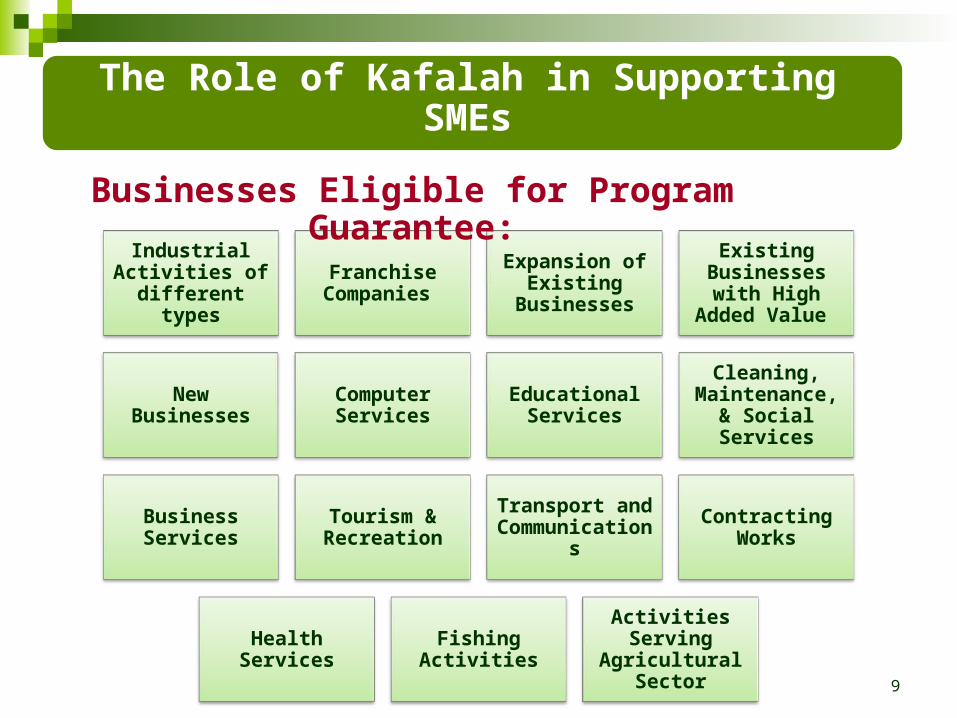

Industrial Activities of

different types

Franchise Companies

Expansion of Existing

Businesses

Existing Businesses with

High Added Value

New Businesses Computer Services

Educational Services

Cleaning, Maintenance, & Social Services

Business Services

Tourism & Recreation

Transport and Communications

Contracting Works

Health Services Fishing Activities

Activities Serving

Agricultural Sector 9

Businesses Eligible for Program Guarantee:

The Role of Kafalah in Supporting SMEs

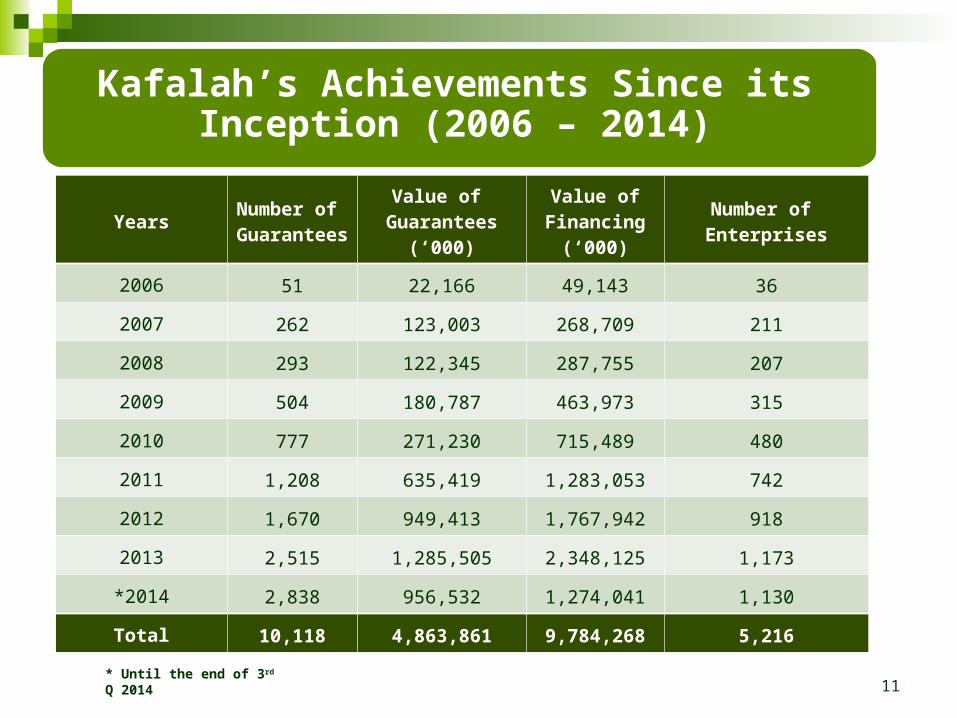

Kafalah’s Achievements Since its Inception (2006 – 2014)

YearsNumber of Guarantees

Value of Guarantees

(‘000)

Value ofFinancing

(‘000)

Number of Enterprises

2006 51 22,166 49,143 36

2007 262 123,003 268,709 211

2008 293 122,345 287,755 207

2009 504 180,787 463,973 315

2010 777 271,230 715,489 480

2011 1,208 635,419 1,283,053 742

2012 1,670 949,413 1,767,942 918

2013 2,515 1,285,505 2,348,125 1,173

*2014 2,838 956,532 1,274,041 1,130

Total 10,118 4,863,861 9,784,268 5,216

11* Until the end of 3rd Q 2014

Kafalah’s Achievements Since its Inception (2006 – 2014)

12

Kafalah’s Achievements Since its Inception (2006 – 2014)

* Until the end of 3rd Q 2014

Number of Guarantees

13

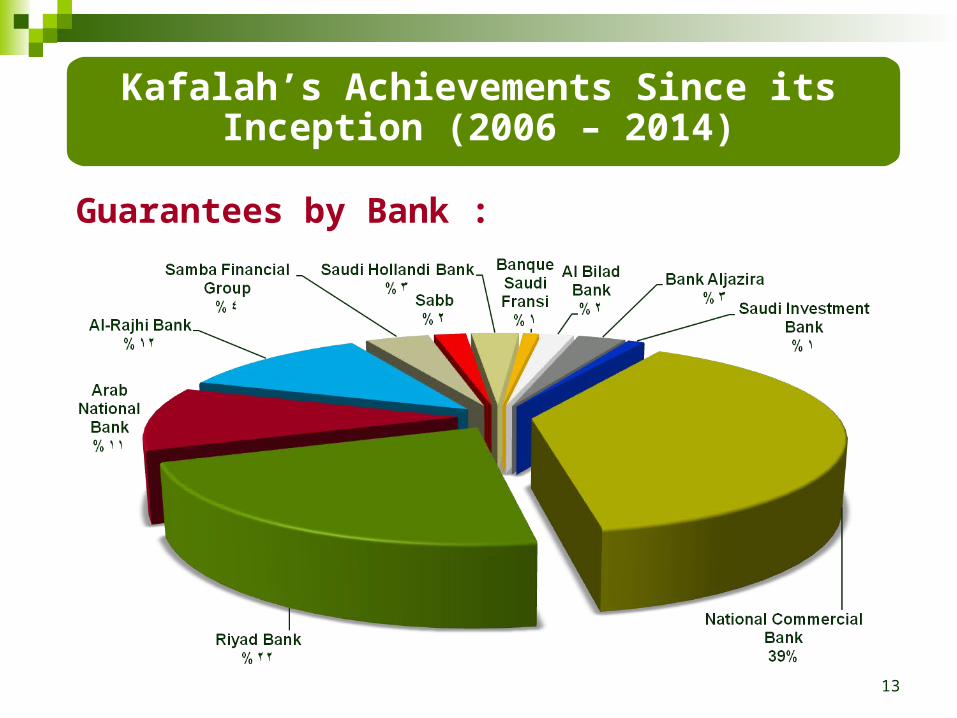

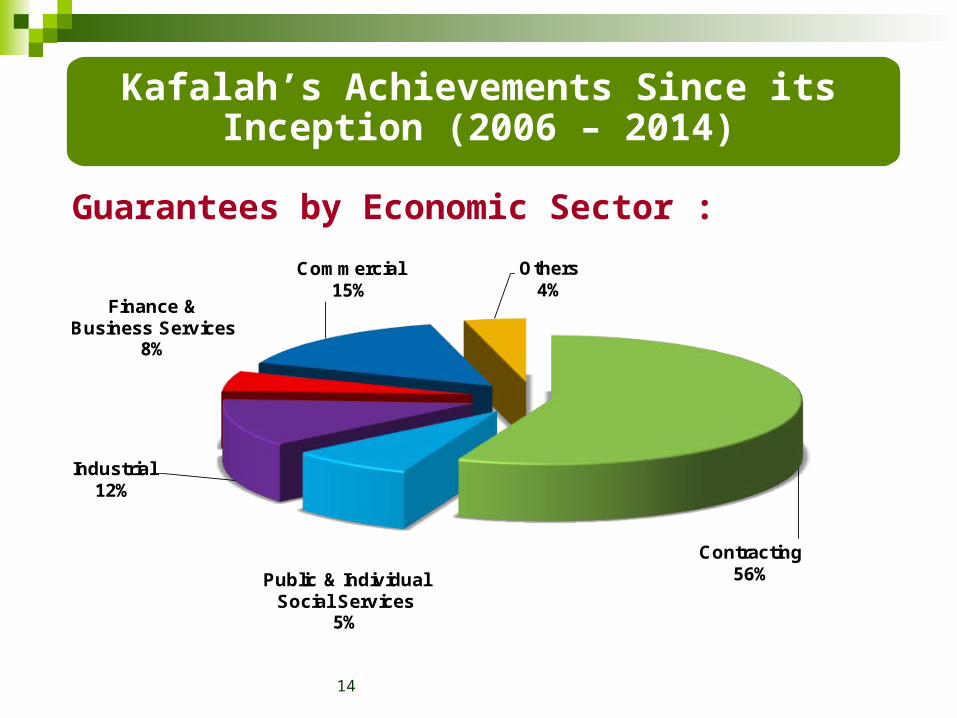

Guarantees by Bank :

Kafalah’s Achievements Since its Inception (2006 – 2014)

14

Contracting56%

Finance & Business Services

8%

Industrial12%

Public & Individual Social Services

5%

Commercial15%

Others4%

Guarantees by Economic Sector :

Kafalah’s Achievements Since its Inception (2006 – 2014)

15

The Program held training sessions for various segments of

the SME sector in cooperation with entities such as:

The World Bank & International Finance Corporation (IFC)

The Saudi Institute of Banking

Private sector training providers

Kafalah’s Achievements Since its Inception (2006 – 2014)

Non-Guarantee Services (Training):

16

Targeted trainees:

Ambitious young people who want self-employment.

Owners of existing SMEs.

SME banking staff of commercial banks.

Training contents:

Operations, marketing and financial management of SMEs.

Banks loan procedures and conditions.

Kafalah procedures and conditions.

Kafalah’s Achievements Since its Inception (2006 – 2014)

Kafalah has trained more than 1,400 trainees :

17

Kafalah’s Achievements Since its Inception (2006 – 2014)

Challenges Facing Kafalah &

Kafalah’s Responsive Actions

19

Challenge:

Slow progression in the cooperation & activity of participant

banks.

Banks’ centralization in decision making & focus on central

branches.

Kafalah’s Responsive Actions:

Regular meetings with banks’ executives to encourage the

increase of activity and encourage the distribution of focus

and decision making to all bank branches.

Challenges Facing Kafalah & Kafalah’s Responsive Actions

20

Challenge:

Stakeholders absence of knowledge about the role of credit

guarantee schemes and Kafalah’s procedures.

Kafalah’s Responsive Actions:

Training sessions for banks staff, in cooperation with the

Institute of Banking.

Training sessions for chambers of commerce staff.

Challenges Facing Kafalah & Kafalah’s Responsive Actions

21

Challenge:

Lack of SMEs awareness with regards to banks processes

and requirements.

Misunderstanding Kafalah’s role.

Kafalah’s Responsive Actions:

Several workshops and presentations around the kingdom to

improve awareness.

Kafalah promotion campaigns.

Challenges and Obstacles Facing KafalahChallenges Facing Kafalah & Kafalah’s Responsive Actions

22

Challenge:

Lack of the following skills within SMEs, leading to failure in

meeting acceptable credit standards, and to loan rejection :

Business planning skills.

Skills in preparing loan requests.

Kafalah’s Responsive Actions:

Numerous training sessions and presentations around the

kingdom to improve business planning skills.

Challenges Facing Kafalah & Kafalah’s Responsive Actions

23

Challenge:

High average levels of :

Collaterals required by banks

Loan fees

Kafalah’s Responsive Actions:

Increased Kafalah guarantee levels from 50% to 75% to 80%

to encourage banks to lower collateral conditions and loan

fees.

Challenges Facing Kafalah & Kafalah’s Responsive Actions

24

Thank you for listeningThank you for listening