Energy Finance 101: Mechanisms for Financing Sustainable Energy

31

Energy Finance 101: Mechanisms for Financing Sustainable Energy Chris Lohmann U.S. Department of Energy

-

Upload

stewart-johns -

Category

Documents

-

view

40 -

download

0

description

Energy Finance 101: Mechanisms for Financing Sustainable Energy. Chris Lohmann U.S. Department of Energy. Financing is an ideal way to increase deployment of energy efficiency and renewable technologies. Financing programs are inherently sustainable whereas grants and rebates are once-and-done - PowerPoint PPT Presentation

Transcript of Energy Finance 101: Mechanisms for Financing Sustainable Energy

Energy Finance 101: Mechanisms for Financing Sustainable Energy

Chris Lohmann

U.S. Department of Energy

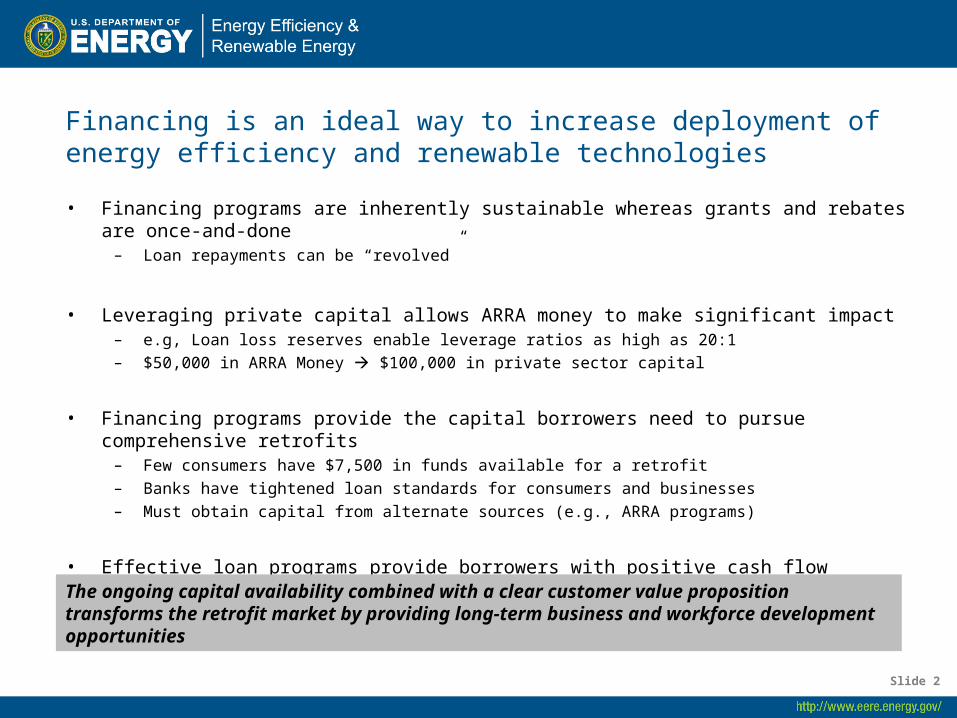

Financing is an ideal way to increase deployment of energy efficiency and renewable technologies

• Financing programs are inherently sustainable whereas grants and rebates are once-and-done– Loan repayments can be “revolved”

• Leveraging private capital allows ARRA money to make significant impact– e.g, Loan loss reserves enable leverage ratios as high as 20:1– $50,000 in ARRA Money $100,000 in private sector capital

• Financing programs provide the capital borrowers need to pursue comprehensive retrofits– Few consumers have $7,500 in funds available for a retrofit– Banks have tightened loan standards for consumers and businesses – Must obtain capital from alternate sources (e.g., ARRA programs)

• Effective loan programs provide borrowers with positive cash flow (Energy Savings > Monthly Loan Payment)

Slide 2

The ongoing capital availability combined with a clear customer value proposition transforms the retrofit market by providing long-term business and workforce development opportunities

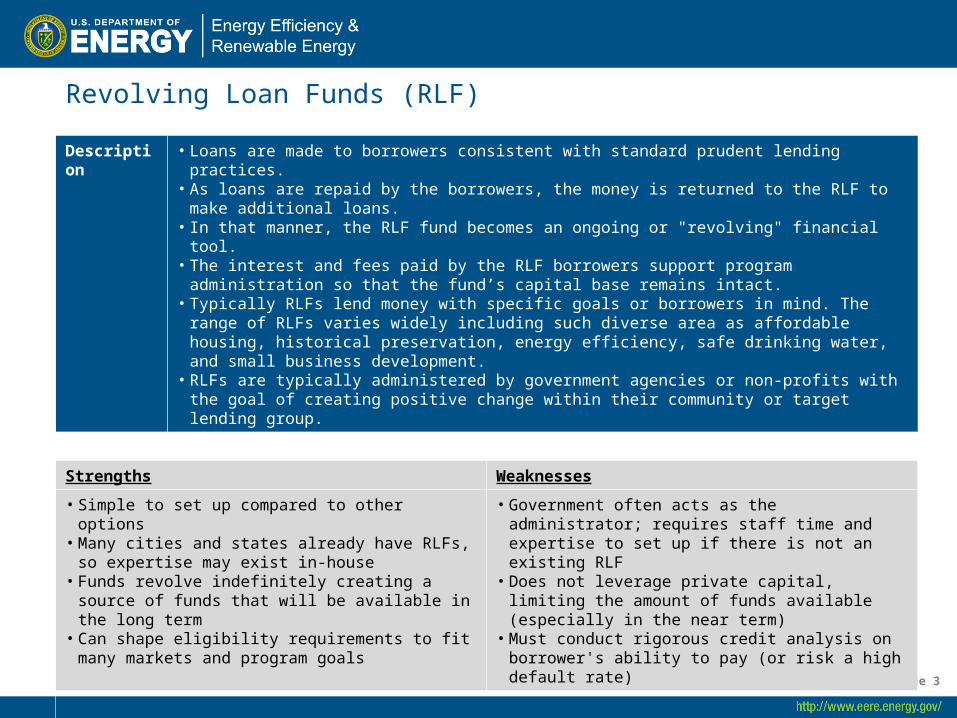

Revolving Loan Funds (RLF)

Slide 3

Description • Loans are made to borrowers consistent with standard prudent lending practices. • As loans are repaid by the borrowers, the money is returned to the RLF to make additional loans. • In that manner, the RLF fund becomes an ongoing or "revolving" financial tool. • The interest and fees paid by the RLF borrowers support program administration so that the fund’s

capital base remains intact. • Typically RLFs lend money with specific goals or borrowers in mind. The range of RLFs varies widely

including such diverse area as affordable housing, historical preservation, energy efficiency, safe drinking water, and small business development.

• RLFs are typically administered by government agencies or non-profits with the goal of creating positive change within their community or target lending group.

Strengths Weaknesses

• Simple to set up compared to other options• Many cities and states already have RLFs, so expertise

may exist in-house• Funds revolve indefinitely creating a source of funds

that will be available in the long term• Can shape eligibility requirements to fit many markets

and program goals

• Government often acts as the administrator; requires staff time and expertise to set up if there is not an existing RLF

• Does not leverage private capital, limiting the amount of funds available (especially in the near term)

• Must conduct rigorous credit analysis on borrower's ability to pay (or risk a high default rate)

Example • Texas LoanSTAR fund finances energy efficient retrofits for state agencies, public schools, et. Al. • Borrowers repay loans through the stream of cost savings realized from the projects • • Logistics: Fund value -$125 million • 200 loans • Average payback – 6 years

Loan Loss Reserve (LLR)

Slide 4

Description • Loss reserves provide a liquid, immediately accessible source of cash to offset covered losses incurred by a participant.

• Created at the outset or over time by assessing fees and other charges based upon activity level or other metric.

• Typically protects a portfolio of loans against a limited amount of potential losses (but insufficient to cover large losses)

Strengths Weaknesses

• Excellent way to leverage third party capital• Leverage ratios can be as high as 20:1• Can be sustainable if replenished by third parties (e.g.,

contractors)• Can support secondary markets• Liability is capped at the amount of loan loss reserve

• Can be perceived (wrongly) as a subsidy to financial partners

Example • States form an agreement with lenders to set up a 10% loan loss reserve in exchange for providing residential retrofit loans

• In the event of borrower default, funds are taken from this escrow account and distributed to the investors to ensure they receive full repayment (up to the maximum covered by the loan loss reserve).

• Loans continue to be made until the loan loss reserve is exhausted or refilled from other sources (e.g., fees from contractors participating in the program)

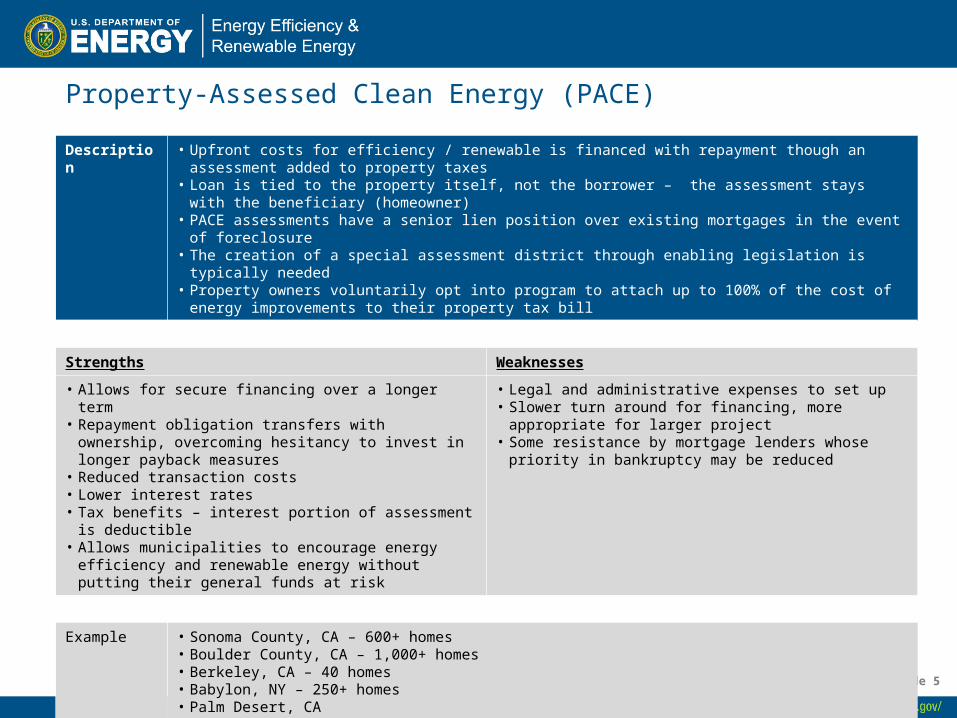

Property-Assessed Clean Energy (PACE)

Slide 5

Description • Upfront costs for efficiency / renewable is financed with repayment though an assessment added to property taxes

• Loan is tied to the property itself, not the borrower – the assessment stays with the beneficiary (homeowner)• PACE assessments have a senior lien position over existing mortgages in the event of foreclosure• The creation of a special assessment district through enabling legislation is typically needed • Property owners voluntarily opt into program to attach up to 100% of the cost of energy improvements to their

property tax bill

Strengths Weaknesses

• Allows for secure financing over a longer term• Repayment obligation transfers with ownership, overcoming

hesitancy to invest in longer payback measures• Reduced transaction costs• Lower interest rates• Tax benefits – interest portion of assessment is deductible • Allows municipalities to encourage energy efficiency and

renewable energy without putting their general funds at risk

• Legal and administrative expenses to set up• Slower turn around for financing, more appropriate for larger

project• Some resistance by mortgage lenders whose priority in

bankruptcy may be reduced

Example • Sonoma County, CA – 600+ homes• Boulder County, CA – 1,000+ homes• Berkeley, CA – 40 homes• Babylon, NY – 250+ homes• Palm Desert, CA

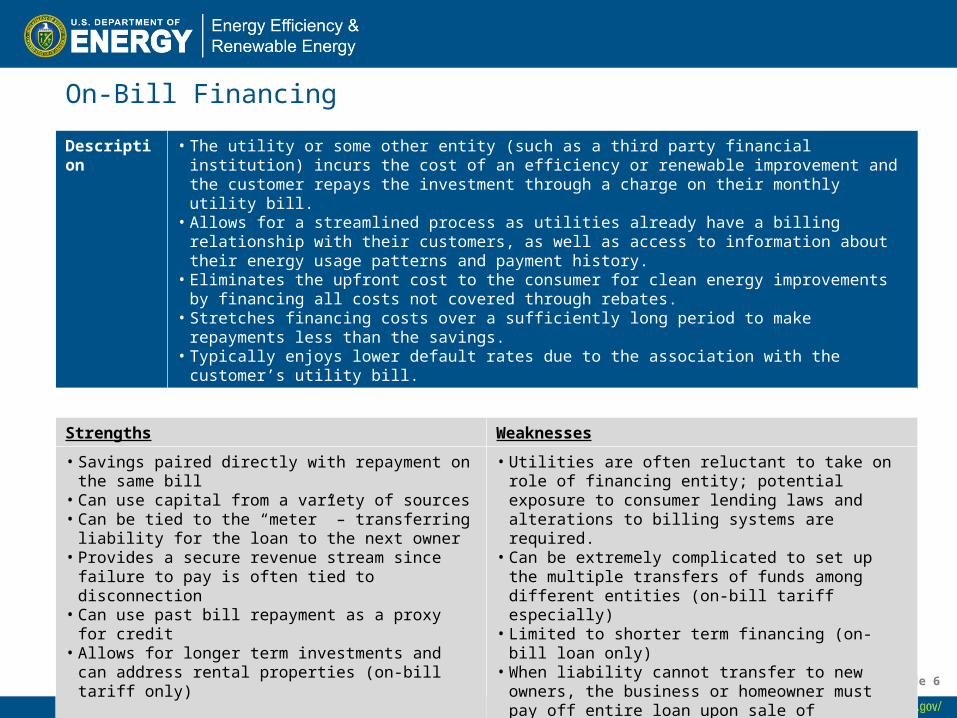

On-Bill Financing

Slide 6

Description • The utility or some other entity (such as a third party financial institution) incurs the cost of an efficiency or renewable improvement and the customer repays the investment through a charge on their monthly utility bill.

• Allows for a streamlined process as utilities already have a billing relationship with their customers, as well as access to information about their energy usage patterns and payment history.

• Eliminates the upfront cost to the consumer for clean energy improvements by financing all costs not covered through rebates.

• Stretches financing costs over a sufficiently long period to make repayments less than the savings. • Typically enjoys lower default rates due to the association with the customer’s utility bill.

Strengths Weaknesses

• Savings paired directly with repayment on the same bill• Can use capital from a variety of sources• Can be tied to the “meter” – transferring liability for the

loan to the next owner• Provides a secure revenue stream since failure to pay is

often tied to disconnection• Can use past bill repayment as a proxy for credit• Allows for longer term investments and can address

rental properties (on-bill tariff only)

• Utilities are often reluctant to take on role of financing entity; potential exposure to consumer lending laws and alterations to billing systems are required.

• Can be extremely complicated to set up the multiple transfers of funds among different entities (on-bill tariff especially)

• Limited to shorter term financing (on-bill loan only)• When liability cannot transfer to new owners, the

business or homeowner must pay off entire loan upon sale of property, which could result in not all of the energy savings being realized (on-bill loan only)

Example • Connecticut’s United Illuminating’s Small Business Energy Advantage program provides financing and then puts the finance charge directly on the utility bill

The Financial Market Development Team is providing robust technical assistance resources to support grantees with financing initiatives

• DOE has assembled a team of finance experts with key skills in:– Designing innovative financing programs – Matching appropriately structured financial products with deep capital

markets

• This group of experts is available to help develop finance programs for SEP and EECBG grantees

Slide 7

Technical Assistance Comes in Several Forms

• Education and Self-Help: Webinars, White Papers, & Online Resources

• Responsive Assistance: Requests through the Technical Assistance Center will be directed to the appropriate resources. Assistance will be tailored to help meet the specific needs of each request -- to include one-on-one sessions and site visits where appropriate.

• Pro-Active Outreach: DOE will seek to identify and reach out to grantees who are strong candidates for finance programs but who are currently unaware of their potential benefits. This may include aggregating multiple small grantees into consortiums to achieve sufficient scale to make financing programs cost-effective.

Slide 8

PACE Financing Programs: Enabling Investments in

Clean EnergyMerrian Fuller

Lawrence Berkeley National Laboratory (LBNL)

April 7, 2010

Barriers to Energy Efficiency

• “Not worth the effort” (i.e. transaction costs)

• Lack of information• Uncertainty about the energy

savings• Split incentives• High upfront costs• Others…

11

150+ Residential Energy Efficiency Financing Programs in the US…

Success!! Our work is done.

Most programs reach less than 0.5% of their potential

participants each year

Issues with Existing Financing Options

• Low Participation Rates

• Limited Applicability to

Households Most in Need

• Limited Support for

Comprehensive Retrofits

• Inability of Programs to

Cover Their Costs

Report available: http://uc-ciee.org/energyeff/documents/resfinancing.pdf

Property-Assessed Clean Energy (PACE)

• Creates financing district & approval process

• Provides upfront capital

• Attaches repayment obligation to the building

• Identifies work & chooses contractor

• Repays financing as a line item on the property tax bill

• Repayment obligation transfers with ownership

$$ Upfront

$$ Repaid on tax bill

Potential Benefits of PACE• New source of capital for EE/RE improvements

• Longer repayment period – Up to 20 years, compared to 5 to 7 years

• Repayment transfers with ownership – Property owners do not want to invest in improvements if they plan to sell their property in a few years.

• Tax benefits –The interest portion of repayments are tax deductible.

• Reduced transaction costs – Often an easier process than applying for a home equity line or second mortgage.

• Information from a trusted source – State and local govts are a trusted source of info and can enable residents and businesses to take action.

• Low interest rates – Low rates MAY be available due to the lower interest on municipal bonds and other sources of financing.

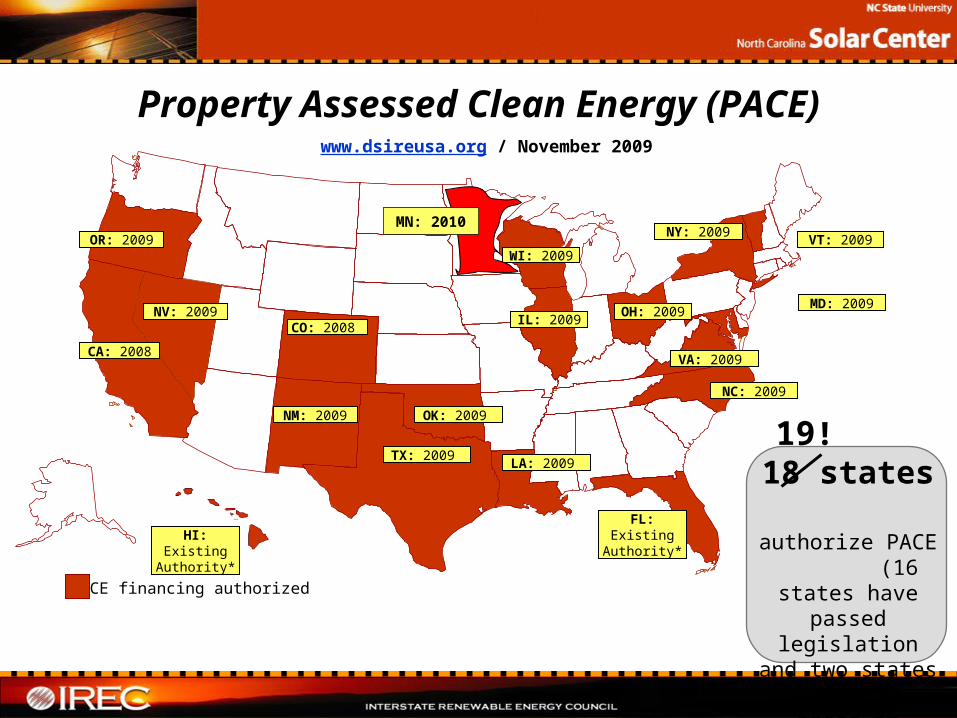

Property Assessed Clean Energy (PACE)

PACE financing authorized

www.dsireusa.org / November 2009

CA: 2008

NM: 2009

CO: 2008

WI: 2009VT: 2009

18 states authorize PACE

(16 states have passed

legislation and two states

permit it based on existing law)

MD: 2009

VA: 2009

OK: 2009

TX: 2009 LA: 2009

IL: 2009OH: 2009NV: 2009

OR: 2009NY: 2009

NC: 2009

FL: Existing Authority*HI: Existing

Authority*

15

19!

MN: 2010

Additional Legislation

Many states “in the process” of pursuing legislation: Alaska, Arizona, Connecticut, Delaware, Florida, Hawaii, Iowa, Idaho, Kansas, Maine, Massachusetts, Maine, Michigan, Missouri, Nebraska, New Hampshire, Ohio, and Pennsylvania

Efforts to amend existing legislation in: Colorado, Illinois, Maryland, Virginia and New York

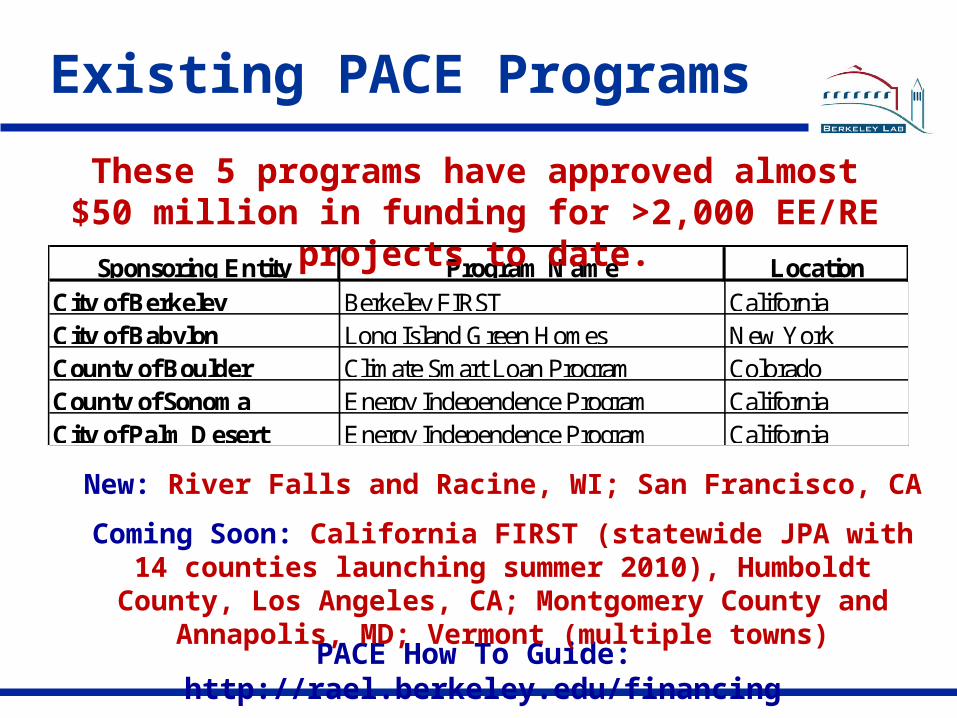

Existing PACE Programs

PACE How To Guide: http://rael.berkeley.edu/financing

Sponsoring Entity Program Name LocationCity of Berkeley Berkeley FIRST CaliforniaCity of Babylon Long Island Green Homes New YorkCounty of Boulder Climate Smart Loan Program ColoradoCounty of Sonoma Energy Independence Program CaliforniaCity of Palm Desert Energy Independence Program California

These 5 programs have approved almost$50 million in funding for >2,000 EE/RE

projects to date.

New: River Falls and Racine, WI; San Francisco, CA

Coming Soon: California FIRST (statewide JPA with 14 counties launching summer 2010), Humboldt

County, Los Angeles, CA; Montgomery County and Annapolis, MD; Vermont (multiple towns)

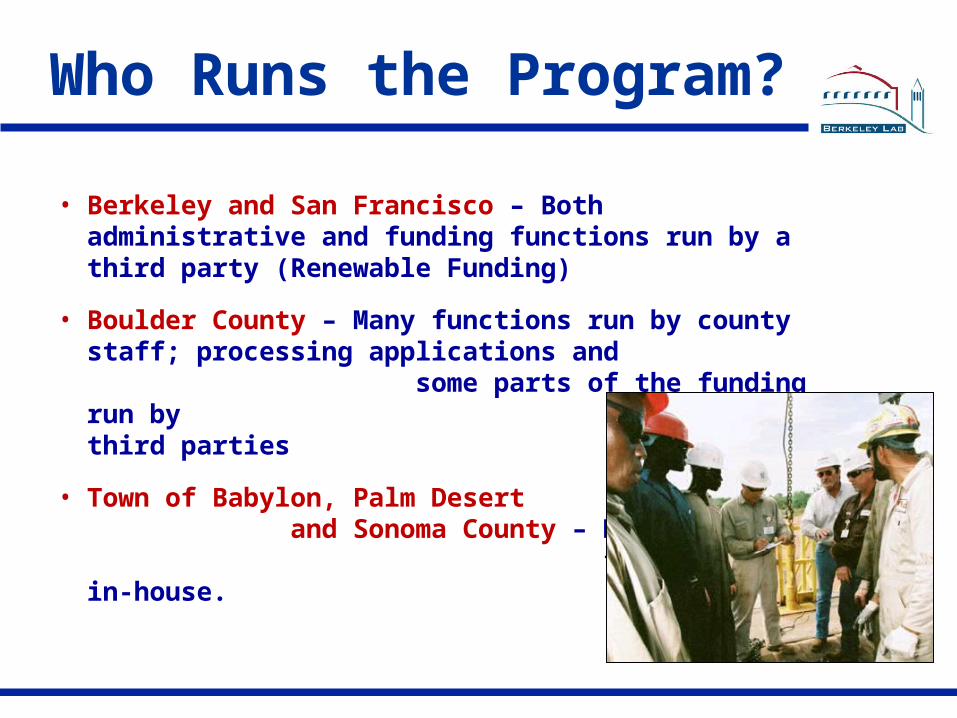

Who Runs the Program?• Berkeley and San Francisco – Both

administrative and funding functions run by a third party (Renewable Funding)

• Boulder County – Many functions run by county staff; processing applications and some parts of the funding run by third parties

• Town of Babylon, Palm Desert and Sonoma County – Most program functions run in-house.

Underwriting Criteria?

• Existing programs to date – Clear title, no involuntary liens, good property tax payment history for 2-3 years; often max assessment to property value ratio (~10%)

• San Francisco & other emerging programs – Will look at property value and outstanding mortgage to make sure the property is not currently under water

Source of Funds?

• Berkeley and San Francisco – “Mini-bonds” purchased immediately by a pre-determined investor (~7.5% interest)

• Boulder County – Aggregates demand THEN issues a bond (5.2% - 6.8%)

• Town of Babylon – Existing solid waste fund repurposed for EE/RE loans (3%)

• Palm Desert & Sonoma County – Bonds are currently held by the local govt (7%)

Eligible Measures?

• Berkeley – Pilot was solar-only

• Boulder County – Long list of measures including efficiency, solar, other renewables.

• Town of Babylon – Energy efficiency primarily with high bar to get solar.

• Sonoma – Range of efficiency, renewable energy, and water conservation measures

• San Francisco – Energy and water efficiency, plus renewables if EE is also done.

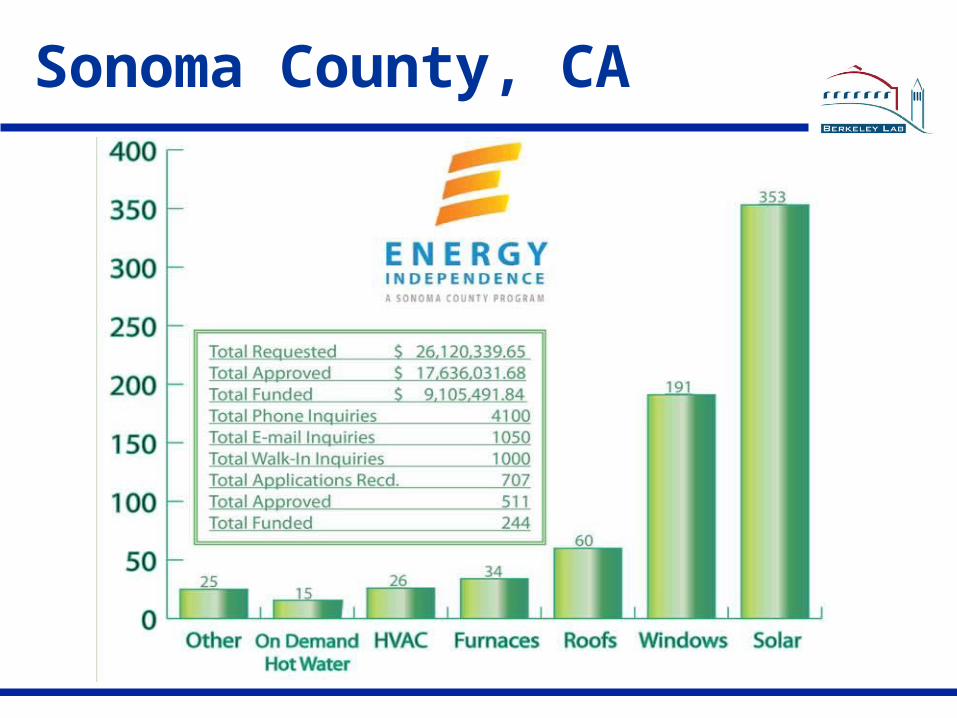

Sonoma County, CA

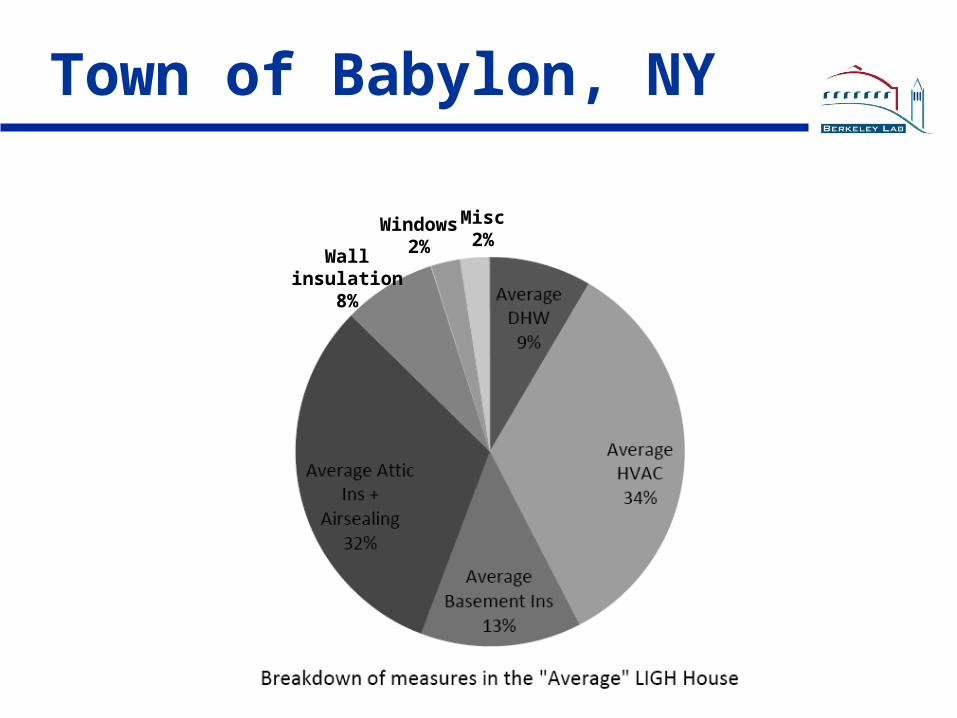

Town of Babylon, NY

Wall insulation8%

Windows2%

Misc2%

Quality Control?

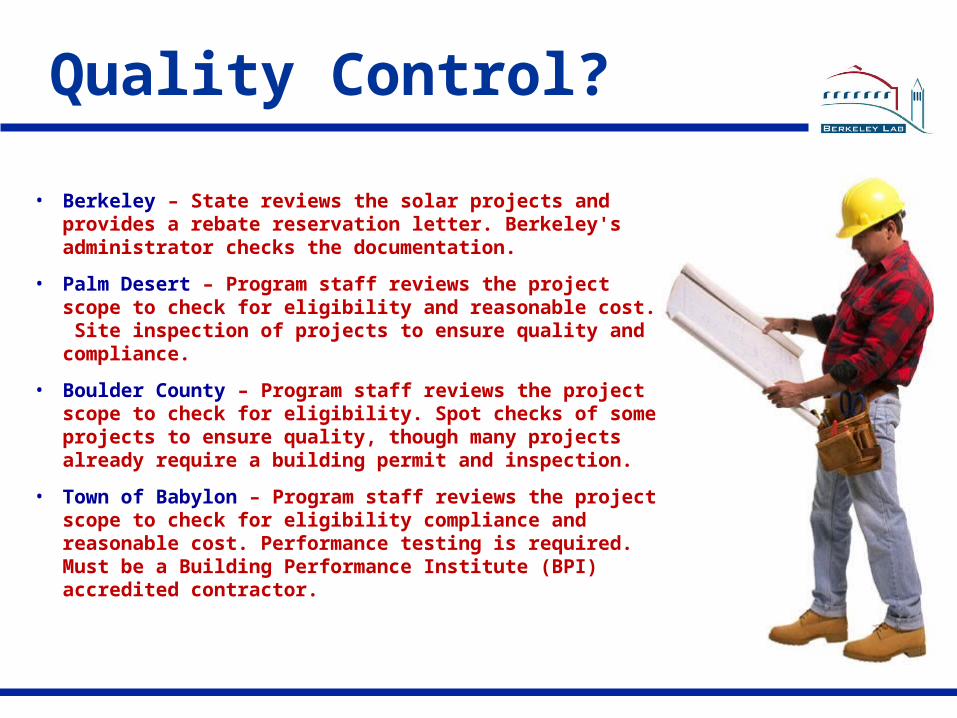

• Berkeley – State reviews the solar projects and provides a rebate reservation letter. Berkeley's administrator checks the documentation.

• Palm Desert – Program staff reviews the project scope to check for eligibility and reasonable cost. Site inspection of projects to ensure quality and compliance.

• Boulder County – Program staff reviews the project scope to check for eligibility. Spot checks of some projects to ensure quality, though many projects already require a building permit and inspection.

• Town of Babylon – Program staff reviews the project scope to check for eligibility compliance and reasonable cost. Performance testing is required. Must be a Building Performance Institute (BPI) accredited contractor.

Potential Issues

• Limits on What Can Be Funded – Must be fixed to property and last at least as long at the financing term; potential limitations if required to be “cash flow positive”.

• Cost of Setup – Often administratively difficult to set up, especially for limited local government staff; however it is easier/cheaper as trail blazers develop templates.

• Scale – A city, town, or small county is probably too small to bring down costs; fix costs need to be spread over hundreds or thousands of assessments each year.

• Access to Cheap $ – Need volume and standardization to bring down cost of capital; “on demand” funding important but more expensive.

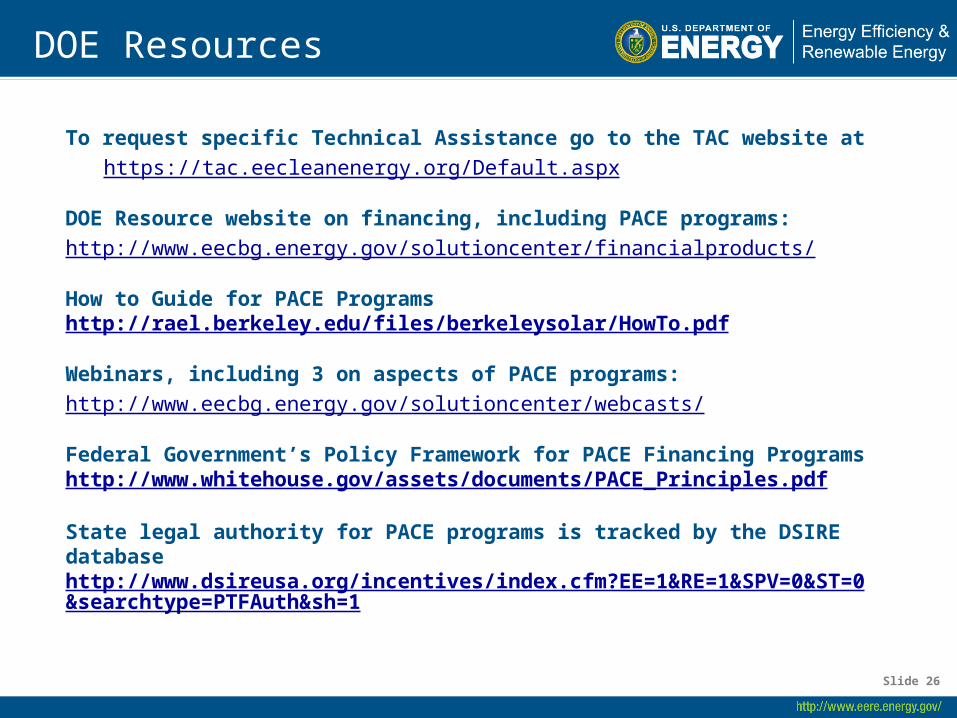

DOE Resources

To request specific Technical Assistance go to the TAC website at

https://tac.eecleanenergy.org/Default.aspx

DOE Resource website on financing, including PACE programs:

http://www.eecbg.energy.gov/solutioncenter/financialproducts/

How to Guide for PACE Programs http://rael.berkeley.edu/files/berkeleysolar/HowTo.pdf

Webinars, including 3 on aspects of PACE programs:

http://www.eecbg.energy.gov/solutioncenter/webcasts/

Federal Government’s Policy Framework for PACE Financing Programs http://www.whitehouse.gov/assets/documents/PACE_Principles.pdf

State legal authority for PACE programs is tracked by the DSIRE database http://www.dsireusa.org/incentives/index.cfm?EE=1&RE=1&SPV=0&ST=0&searchtype=PTFAuth&sh=1

Slide 26

Contact Info

Merrian FullerLawrence Berkeley National

LaboratoryEmail: [email protected]

Phone: 510-486-4482

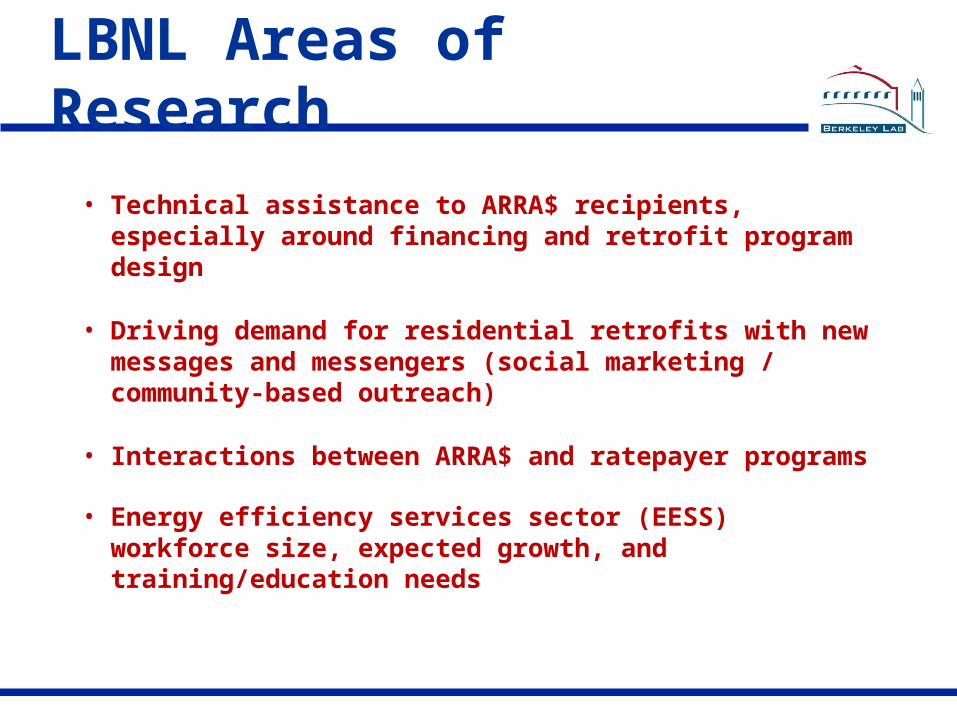

LBNL Areas of Research

• Technical assistance to ARRA$ recipients, especially around financing and retrofit program design

• Driving demand for residential retrofits with new messages and messengers (social marketing / community-based outreach)

• Interactions between ARRA$ and ratepayer programs

• Energy efficiency services sector (EESS) workforce size, expected growth, and training/education needs

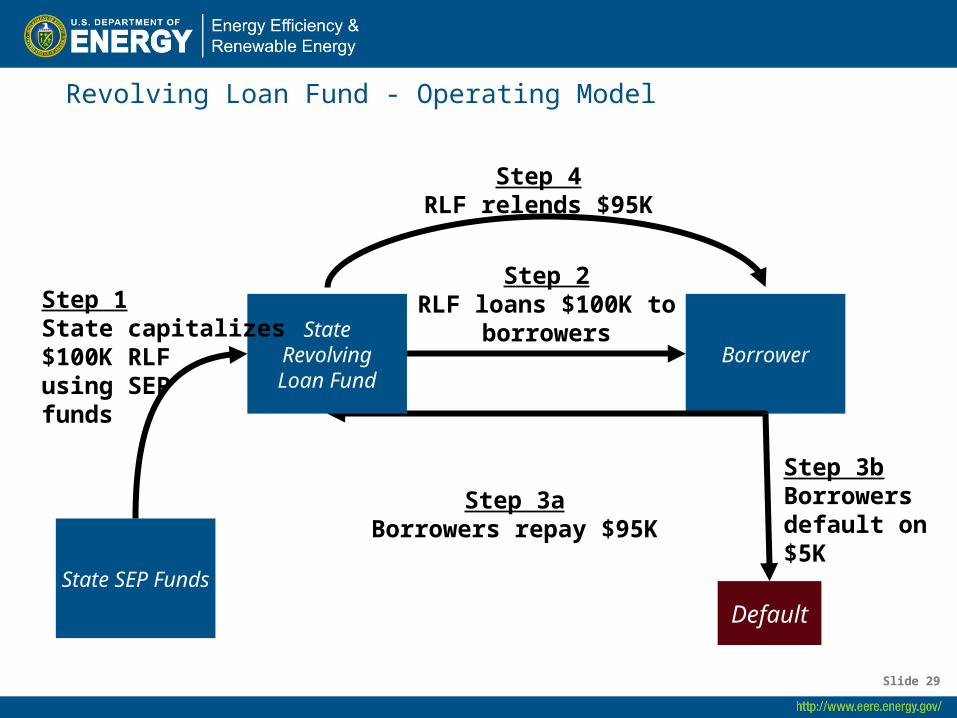

Revolving Loan Fund - Operating Model

Slide 29Slide 29

Default

Borrower

Step 3bBorrowers default on $5K

Step 3aBorrowers repay $95K

Step 4RLF relends $95K

Step 2RLF loans $100K to

borrowersStateRevolvingLoan Fund

State SEP Funds

Step 1State capitalizes$100K RLFusing SEPfunds

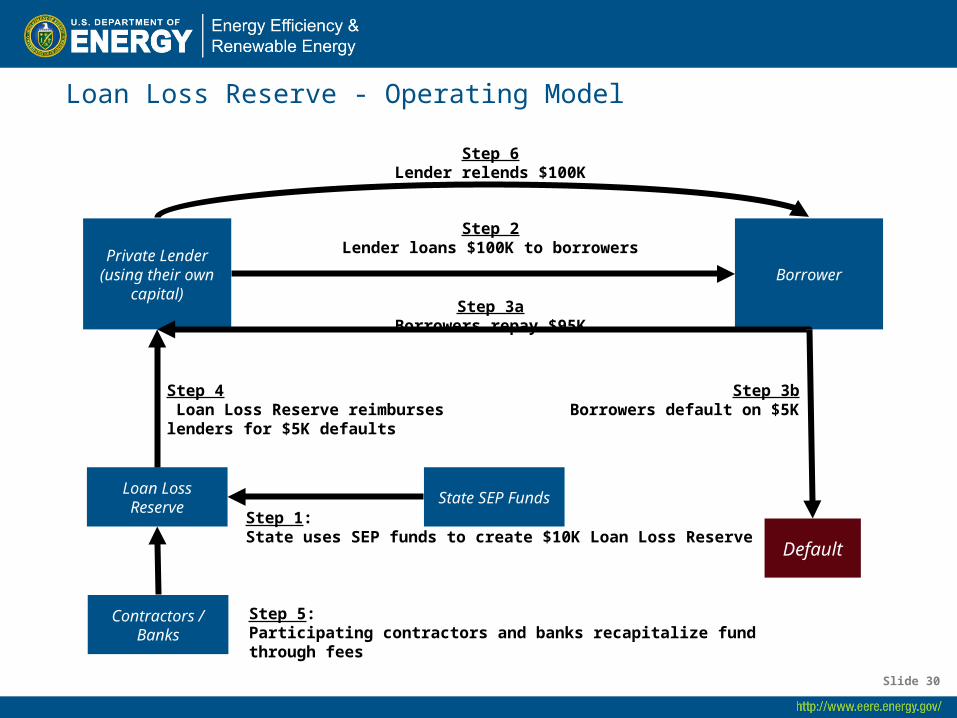

Loan Loss Reserve - Operating Model

Slide 30

Step 2Lender loans $100K to borrowers

Default

BorrowerPrivate Lender (using their own

capital)

Step 3bBorrowers default on $5K

Step 3aBorrowers repay $95K

Step 6Lender relends $100K

State SEP Funds

Step 1: State uses SEP funds to create $10K Loan Loss Reserve

Loan Loss Reserve

Step 4 Loan Loss Reserve reimburses lenders for $5K defaults

Contractors / Banks

Step 5: Participating contractors and banks recapitalize fund through fees

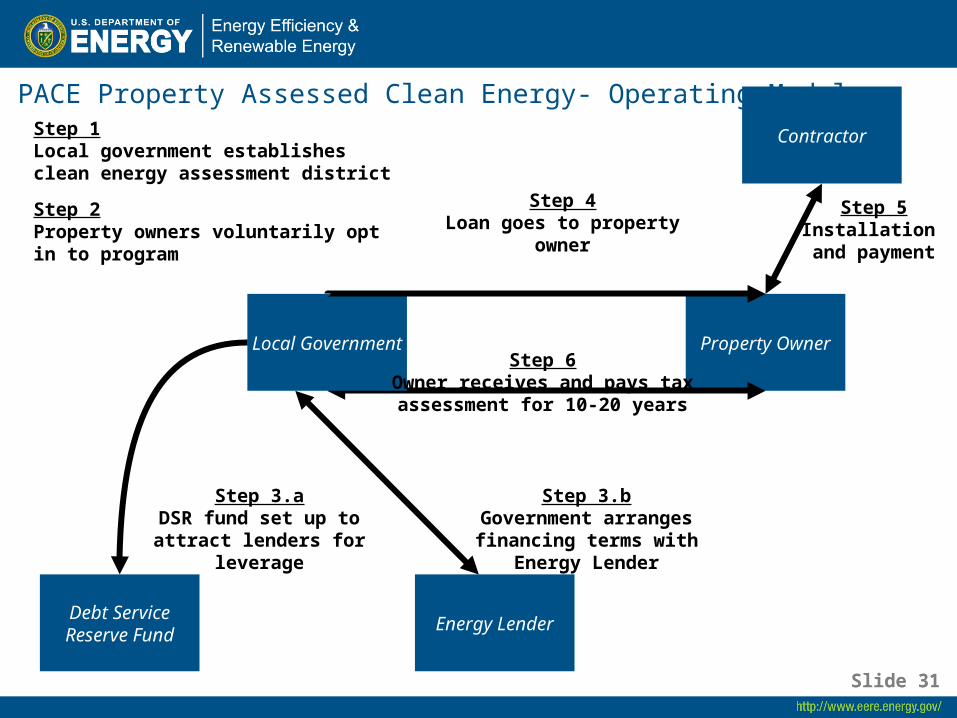

PACE Property Assessed Clean Energy- Operating Model

Slide 31Slide 31

Property Owner

Step 4Loan goes to property owner

Local Government

Debt Service Reserve Fund

Step 1Local government establishes clean energy assessment district

Contractor

Energy Lender

Step 6Owner receives and pays tax assessment for 10-20 years

Step 5Installation

and payment

Step 2Property owners voluntarily opt in to program

Step 3.bGovernment arranges

financing terms with Energy Lender

Step 3.aDSR fund set up to attract

lenders for leverage