EFFECTS OF WORKING CAPITAL MANAGEMENT ON FINANCIAL ...

88

EFFECTS OF WORKING CAPITAL MANAGEMENT ON FINANCIAL PERFOMANCE OF ENERGY AND PETROLEUM COMPANIES LISTED ON NAIROBI SECURITIES EXCHANGE FOR THE PERIOD 2013-2017 BY MARK W. NAMASAKE UNITED STATES INTERNATIONAL UNIVERSITY- AFRICA FALL 2018

Transcript of EFFECTS OF WORKING CAPITAL MANAGEMENT ON FINANCIAL ...

EFFECTS OF WORKING CAPITAL MANAGEMENT ON

FINANCIAL PERFOMANCE OF ENERGY AND PETROLEUM

COMPANIES LISTED ON NAIROBI SECURITIES EXCHANGE

FOR THE PERIOD 2013-2017

BY

MARK W. NAMASAKE

UNITED STATES INTERNATIONAL UNIVERSITY- AFRICA

FALL 2018

EFFECTS OF WORKING CAPITAL MANAGEMENT ON

FINANCIAL PERFOMANCE OF ENERGY AND PETROLEUM

COMPANIES LISTED ON NAIROBI SECURITIES EXCHANGE

FOR THE PERIOD 2013-2017

BY

MARK W. NAMASAKE

A Research Project Report Submitted to the Chandaria School of

Business in Partial Fulfillment of the Requirements of Master in

Business Administration

UNITED STATES INTERNATIONAL UNIVERSITY- AFRICA

FALL 2018

ii

STUDENT’S DECLARATION

I declare this work has not been submitted to any other university other than United States

International University-Africa, it’s my original work which have been submitted for the

Academic purposes.

Signed: ________________________ Date: ______________________

Mark Namasake (ID NO: 639230)

The project has been submitted for the examination as the designated university

supervisor.

Signed: ________________________ Date: ______________________

Mr. Kepha M. Oyaro

Signed: ________________________ Date: ______________________

Dean, Chandaria School of Business

iii

COPYRIGHT

All rights reserved. No part of this project report may be produced or transmitted in any

form or by any means, electronic, mechanical, including photocopying, recording or any

information storage without prior written permission from the author. ©Mark W.

Namasake 2018

iv

ABSTRACT

The purpose of the study was to determine the effect working capital management on

financial performance of energy and petroleum companies listed in the Nairobi Securities

Exchange. The study used the following research questions; What is the effect of

accounts receivables on financial performance of energy and petroleum companies listed

in the NSE? What is the effect of cash conversion cycle on financial performance of

energy and petroleum companies listed in the NSE? and how do accounts payables affect

financial performance of energy and petroleum companies listed in the NSE?

The study adopted the use of descriptive research design. Descriptive was used because

the study is a non- experimental research design used to measure a variable when little

conceptual background has been developed on specific aspects of the variables under.

The population used comprised of all the Energy and Petroleum companies listed in the

Nairobi Securities Exchange as at 31st December 2017. The study adopted the use of

census technique where all listed firms were sampled.

The study collected secondary data in which quantitative data was obtained for the five

companies in the energy and petroleum firms listed in the Nairobi Securities Exchange.

The data was collected from the audited financial statements obtained from the company

websites, the Nairobi Securities Exchange from the year 2013 to 2017. With the help of

Statistical Packages for Social Sciences version 24, the study used descriptive statistics

which included the percentages, mean and standard deviation. Inferential statistics was

used in the study to establish the degree of relationship between the independent variables

and dependent variables in which correlation and regression analysis were used to test the

effects of working capital management on the financial performance of the energy and

petroleum firms listed in the Nairobi Securities Exchange.

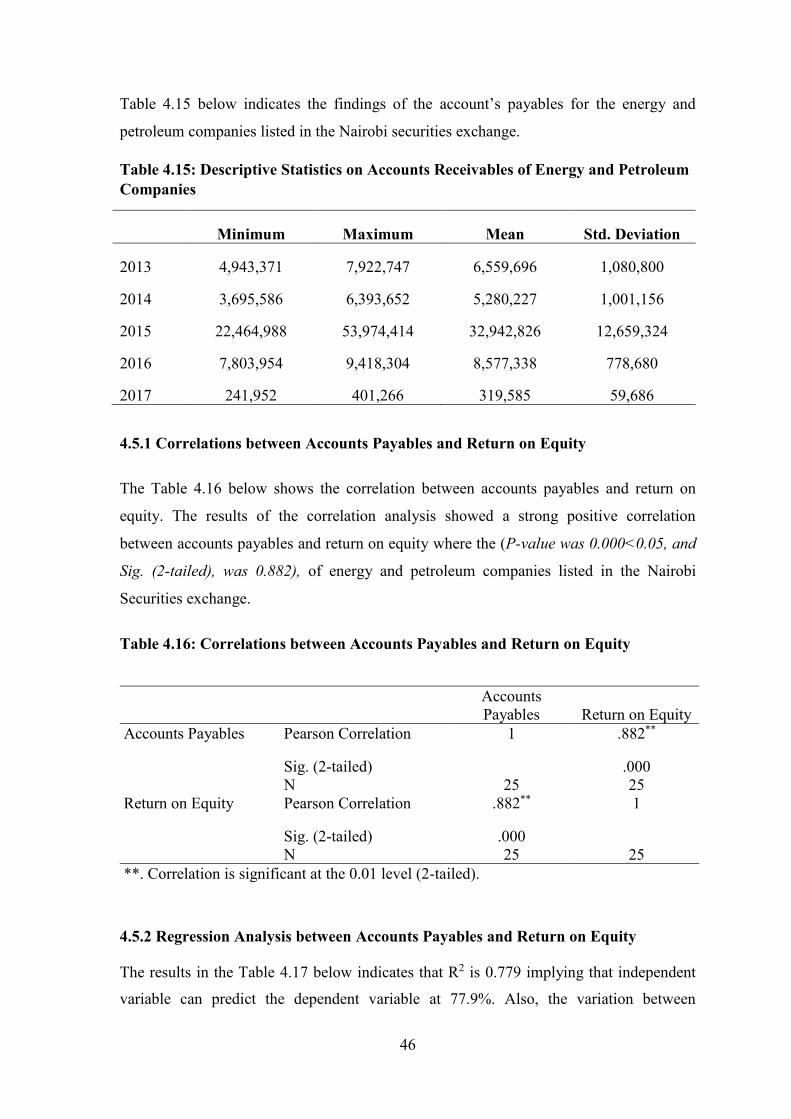

The findings of the first research questions indicated that there was a strong positive

correlation between accounts receivables and net profit where the (P-value was

0.000<0.05, and Sig. (2-tailed), was 0.931). The variations of accounts receivables on the

net profit in which the value of R-squared indicated that there was variation of 86.7% on

net profit was due to changes in accounts receivables. The results of the correlation

analysis on the second research questions indicated that there was moderate negatively

relationship between cash conversion cycle and return on assets the (P-value was

0.003<0.05, and Sig. (2-tailed), was -0.566). The variations of cash conversion cycle on

v

return on assets in which the value of R-squared indicated that there was variation of

32.0% on return on assets was due to changes in cash conversion cycle. There was a

strong positive correlation between accounts payables and return on equity for the firms

where the (P-value was 0.000<0.05, and Sig. (2-tailed), was 0.882). The variations of

accounts payables on the return on equity in which the value of R-squared indicated the

variation of 77.9% on return on equity was due to changes in cash accounts payables.

The study concludes that there was a strong positive relationship between accounts

receivables and net profit of energy and petroleum companies listed in the Nairobi

Securities exchange. Accounts receivables influences the financial performance of the

listed companies and which makes them profitable. Secondly, there was negatively

relationship between cash conversion cycle and return on assets. The results imply that

financial performance of listed energy and petroleum firms depends upon effective

working capital management. Lastly, accounts payables was found to be significant

positive association with return on equity, indicating that if time period of supplier ‘s

payment is increased then overall firm‘s financial performance also improves for the

listed firms.

From the findings the study recommends that there is need for managers to delay payment

to suppliers and take advantage of the funds as short-term credit which does not attract

interest costs to reinvest in order to generate more income for shareholders. Secondly,

managers can improve the profitability of their firms by reducing their cash conversion

cycle which is the components of days account receivable, inventory turnover in days.

Thirdly the study recommends that managers and financial officers of companies should

establish a long-term relationship with their vendors in order to access trade credit in a

more easy and fast way, as increased use of trade credit enhances performance of

companies through increased financial performance. The study recommends on further

studies to be carried for a longer time period such as ten twenty years to establish the

effect of working capital and financial performance.

vi

TABLE OF CONTENTS

STUDENT’S DECLARATION ........................................................................................ ii

COPYRIGHT ................................................................................................................... iii

ABSTRACT ....................................................................................................................... iv

ACKNOWLEDGEMENTS ............................................................................................. ix

DEDICATION.................................................................................................................... x

LIST OF TABLES ............................................................................................................ xi

LIST OF FIGURES ......................................................................................................... xii

ABBRIEVIATIONS AND ACRONYMS .................................................................... xiii

CHAPTER ONE ................................................................................................................ 1

1.0 INTRODUCTION........................................................................................................ 1

1.1 Background of the Study ............................................................................................ 1

1.2 Statement of the Problem ........................................................................................... 4

1.3 Purpose of the Study .................................................................................................. 5

1.4 Research Questions .................................................................................................... 6

1.5 Significance of the Study ........................................................................................... 6

1.6 Scope of the Study...................................................................................................... 7

1.7 Definition of Terms .................................................................................................... 7

1.8 Chapter Summary ....................................................................................................... 8

CHAPTER TWO ............................................................................................................... 9

2.0 LITERATURE REVIEW ........................................................................................... 9

2.1 Introduction ................................................................................................................ 9

2.2 Effects of Account Receivables on Financial Performance ....................................... 9

2.3 Effects of Cash Conversion Cycle on Financial Performance ................................. 13

2.4 Effects of Accounts Payable on Financial Performance .......................................... 18

vii

2.5 Chapter Summary ..................................................................................................... 22

CHAPTER THREE ......................................................................................................... 23

3.0 RESEARCH METHODOLOGY ............................................................................. 23

3.1 Introduction .............................................................................................................. 23

3.2 Research Design ....................................................................................................... 23

3.3 Population and Sampling Design ............................................................................. 24

3.4 Data Collection Methods .......................................................................................... 26

3.5 Research Procedures ................................................................................................ 26

3.6 Data Analysis Methods ............................................................................................ 27

3.7 Chapter Summary ..................................................................................................... 28

CHAPTER FOUR ............................................................................................................ 29

4.0 RESULTS AND FINDINGS ..................................................................................... 29

4.1 Introduction .............................................................................................................. 29

4.2 General Information ................................................................................................. 29

4.3 Effects of Accounts Receivables on Financial Performance ................................... 40

4.4 Effects of Cash Conversion Cycle on Financial Performance ................................. 43

4.5 Effects of Accounts Payables on Financial Performance......................................... 45

4.6 Chapter Summary ..................................................................................................... 48

CHAPTER FIVE ............................................................................................................. 49

5.0 DISCUSSION, CONCLUSIONS, AND RECOMMENDATIONS ....................... 49

5.1 Introduction .............................................................................................................. 49

5.2 Summary of the Study .............................................................................................. 49

5.3 Discussion ................................................................................................................ 51

5.4 Conclusions .............................................................................................................. 56

viii

5.5 Recommendations .................................................................................................... 57

REFERENCES ................................................................................................................. 59

LIST OF APPENDICES ................................................................................................. 68

Appendix i: Kenya Electricity Generating Company Data Collection Sheet in Kshs.

“000” .............................................................................................................................. 68

Appendix ii: KenolKobil Data Collection Sheet in Kshs. “000” ................................... 69

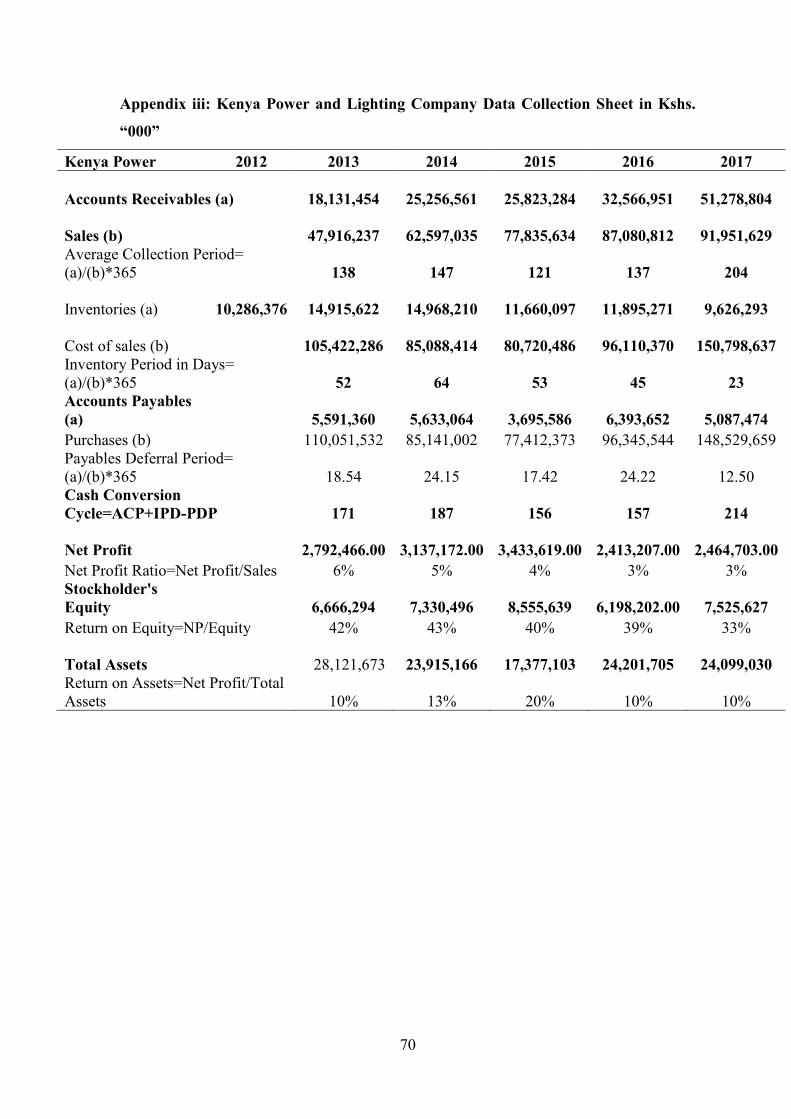

Appendix iii: Kenya Power and Lighting Company Data Collection Sheet in Kshs.

“000” .............................................................................................................................. 70

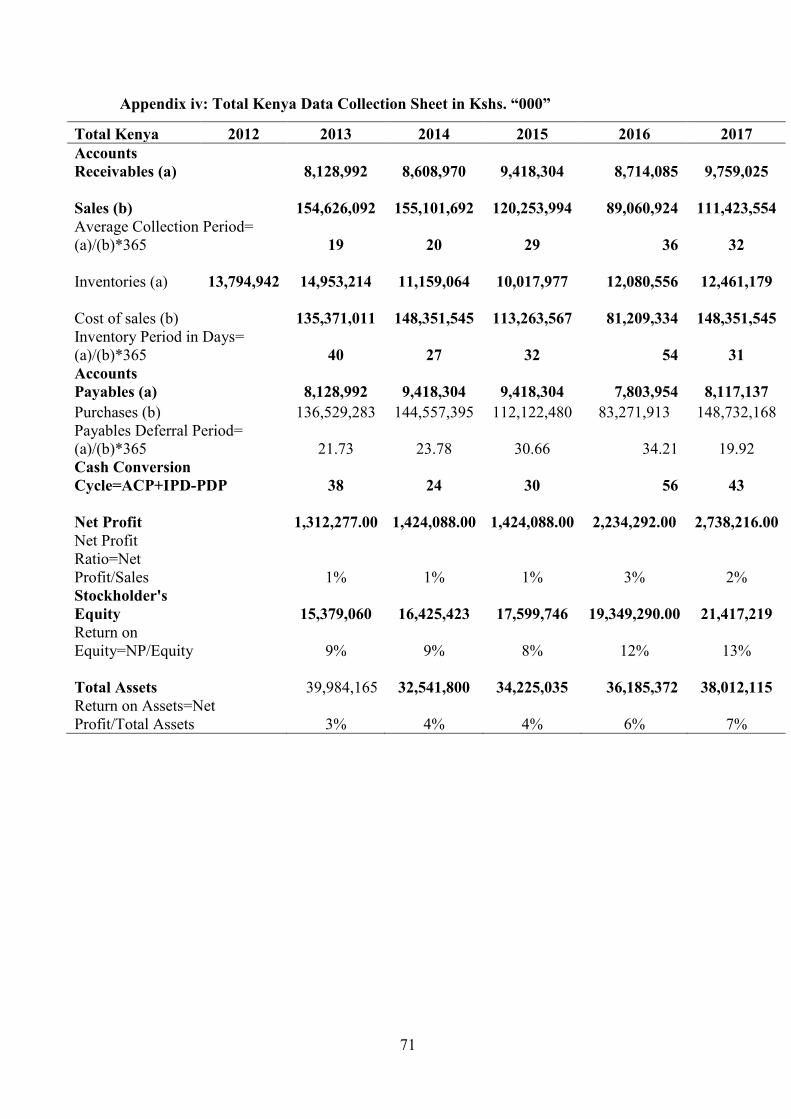

Appendix iv: Total Kenya Data Collection Sheet in Kshs. “000” ................................. 71

Appendix v: Umeme Plc Data Collection Sheet in Kshs. “000” ................................... 72

Appendix vi: Data Collection Sheet Summary for Period (2013-2017) in Kshs. “000” 73

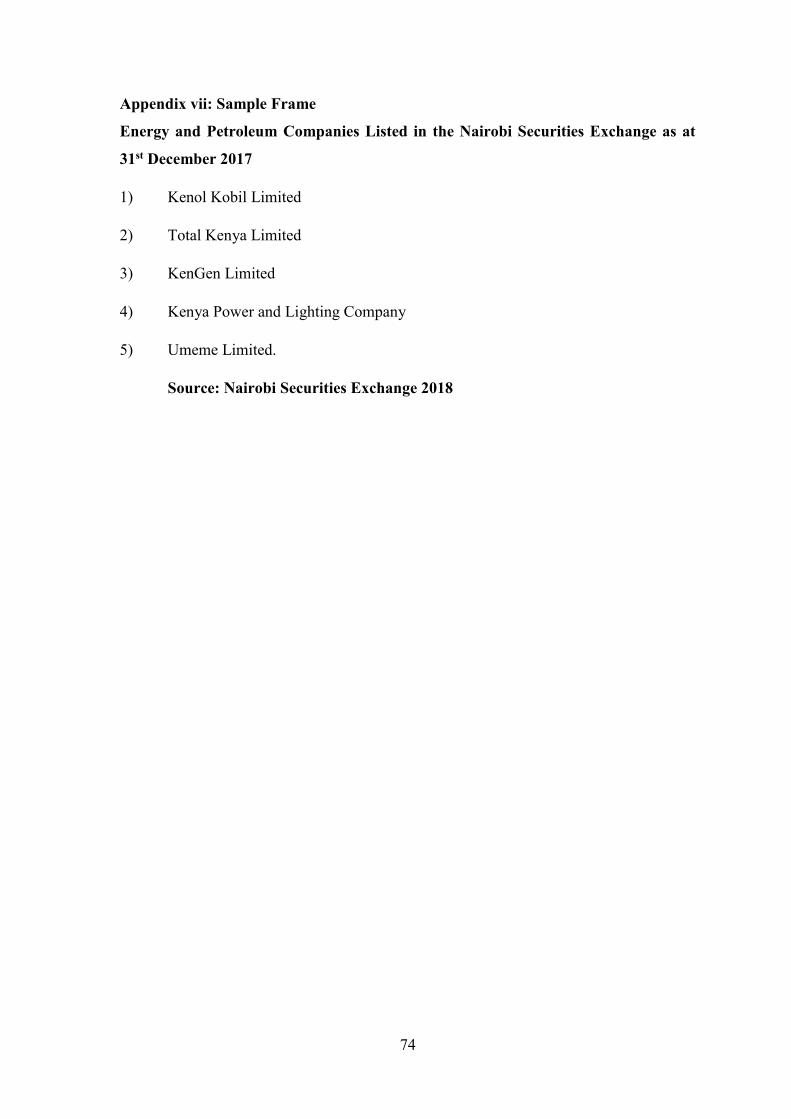

Appendix vii: Sample Frame ......................................................................................... 74

ix

ACKNOWLEDGEMENTS

First and foremost, I thank the Lord Almighty for His sufficient grace in this work. I am

also greatly indebted to my supervisor Mr. Kepha Oyaro whose invaluable advice,

support and contribution has been instrumental to me in this study.

Secondly, I am also grateful to all faculty members of Chandaria School of Business

especially Prof. Francis Wambalaba for their immense support and encouragement.

Thirdly, I thank my Dad Peter Tumen for his great help both financially and

psychologically throughout my education.

Finally, Special thanks also goes to all my friends for the peer review, moral support, and

constructive criticisms which have added value in realization of this project.

x

DEDICATION

The project is dedicated my parents, brothers and sisters for their support and

encouragement throughout this academic journey.

xi

LIST OF TABLES

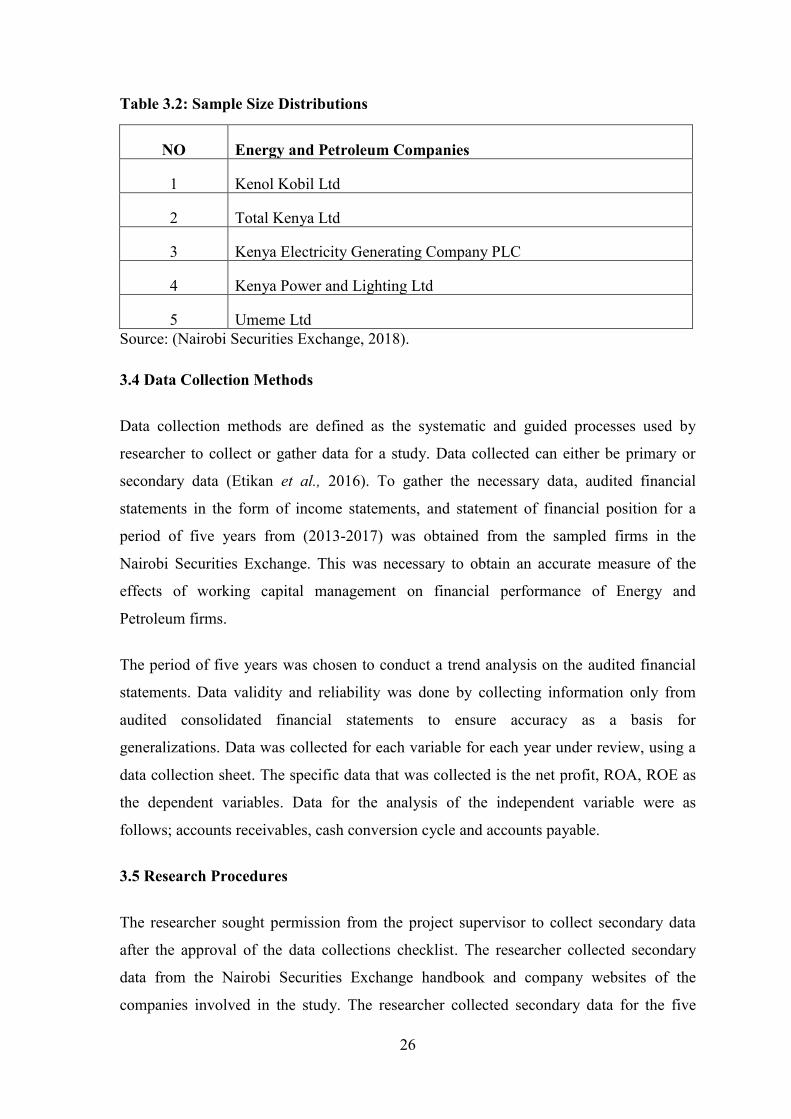

Table 3.1: Population Distribution ..................................................................................... 24

Table 3.2: Sample Size Distributions................................................................................. 26

Table 4.1: Nature of Business for Energy and Petroleum Companies listed ..................... 30

Table 4.2: Descriptive Statistics for Net Profit of Energy and Petroleum Companies ...... 38

Table 4.3: Descriptive Statistics for Total Assets of Energy and Petroleum Companies .. 39

Table 4.4: Descriptive Statistics for Return on Equity of Energy and Petroleum

Companies.......................................................................................................................... 39

Table 4.5: Descriptive Statistics on Accounts Receivables of Energy and Petroleum

Companies.......................................................................................................................... 40

Table 4.6: Correlations between Accounts Receivables and Net Profit ............................ 41

Table 4.7: Model Summary for Accounts Receivables ..................................................... 41

Table 4.8: Analysis of Variance (ANOVA) for Accounts Receivables ............................ 42

Table 4.9: Coefficients Analysis for Accounts Receivables .............................................. 43

Table 4.10: Cash Conversion Cycle and Financial Performance ...................................... 43

Table 4.11: Correlations between Cash Conversion Cycle and Return on Assets ............ 44

Table 4.12: Model Summary for Cash Conversion Cycle ................................................. 44

Table 4.13: Analysis of Variance (ANOVA) for Cash Conversion Cycle ........................ 45

Table 4.14: Coefficients Analysis for Cash Conversion Cycle ......................................... 45

Table 4.15: Descriptive Statistics on Accounts Receivables of Energy and Petroleum

Companies.......................................................................................................................... 46

Table 4.16: Correlations between Accounts Payables and Return on Equity .................... 46

Table 4.17: Model Summary for Accounts Payables ........................................................ 47

Table 4.18: Analysis of Variance (ANOVA) for Accounts Payables ............................... 47

Table 4.19: Coefficients Analysis for Accounts Payables ................................................. 48

xii

LIST OF FIGURES

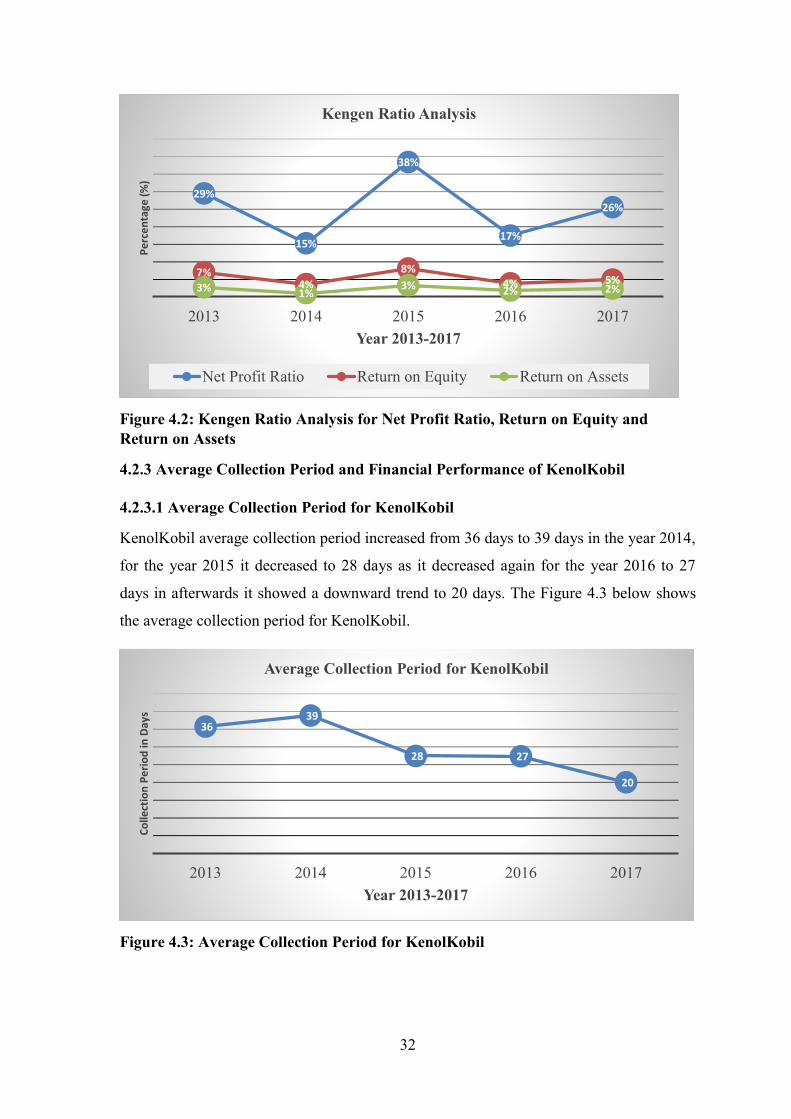

Figure 4.1: Average Collection Period for Kengen ........................................................... 31

Figure 4.2: Kengen Ratio Analysis for Net Profit Ratio, Return on Equity and Return on

Assets ................................................................................................................................. 32

Figure 4.3: Average Collection Period for KenolKobil ..................................................... 32

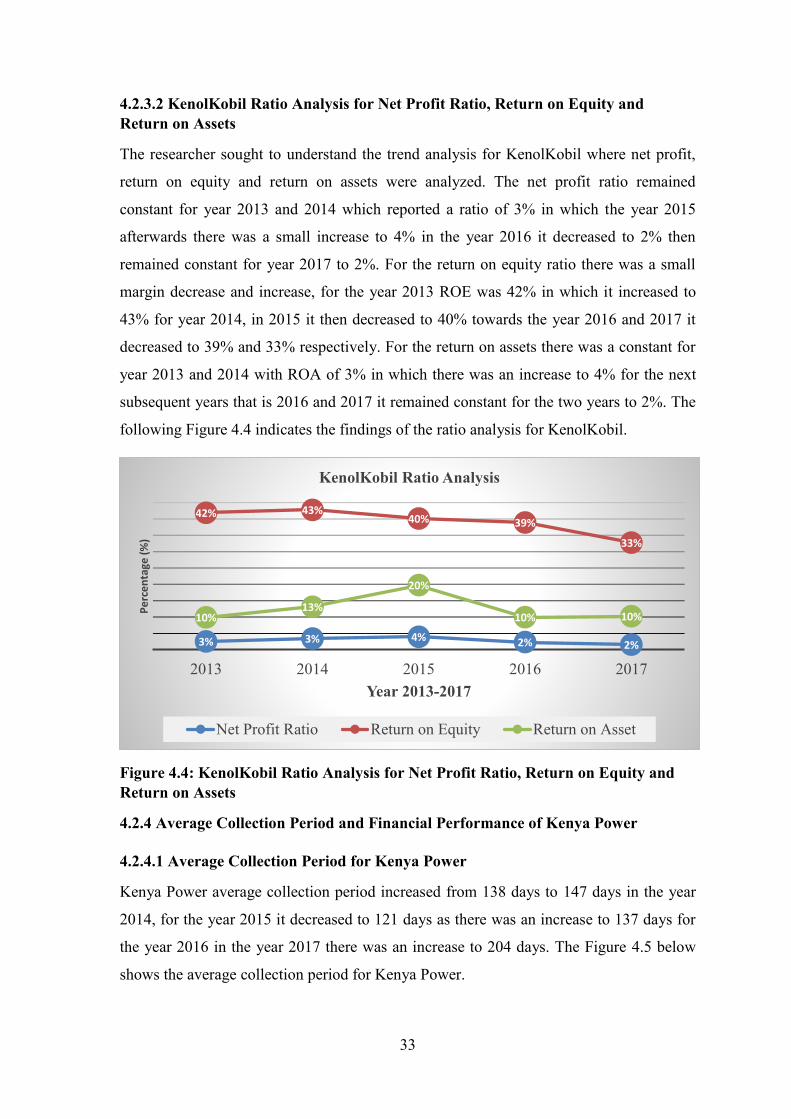

Figure 4.4: KenolKobil Ratio Analysis for Net Profit Ratio, Return on Equity and Return

on Assets ............................................................................................................................ 33

Figure 4.5: Average Collection Period for Kenya Power .................................................. 34

Figure 4.6: Kenya Power Ratio Analysis for Net Profit Ratio, Return on Equity and

Return on Assets ................................................................................................................ 35

Figure 4.7: Average Collection Period for Total Kenya .................................................... 35

Figure 4.8: Total Kenya Ratio Analysis for Net Profit Ratio, Return on Equity and Return

on Assets ............................................................................................................................ 36

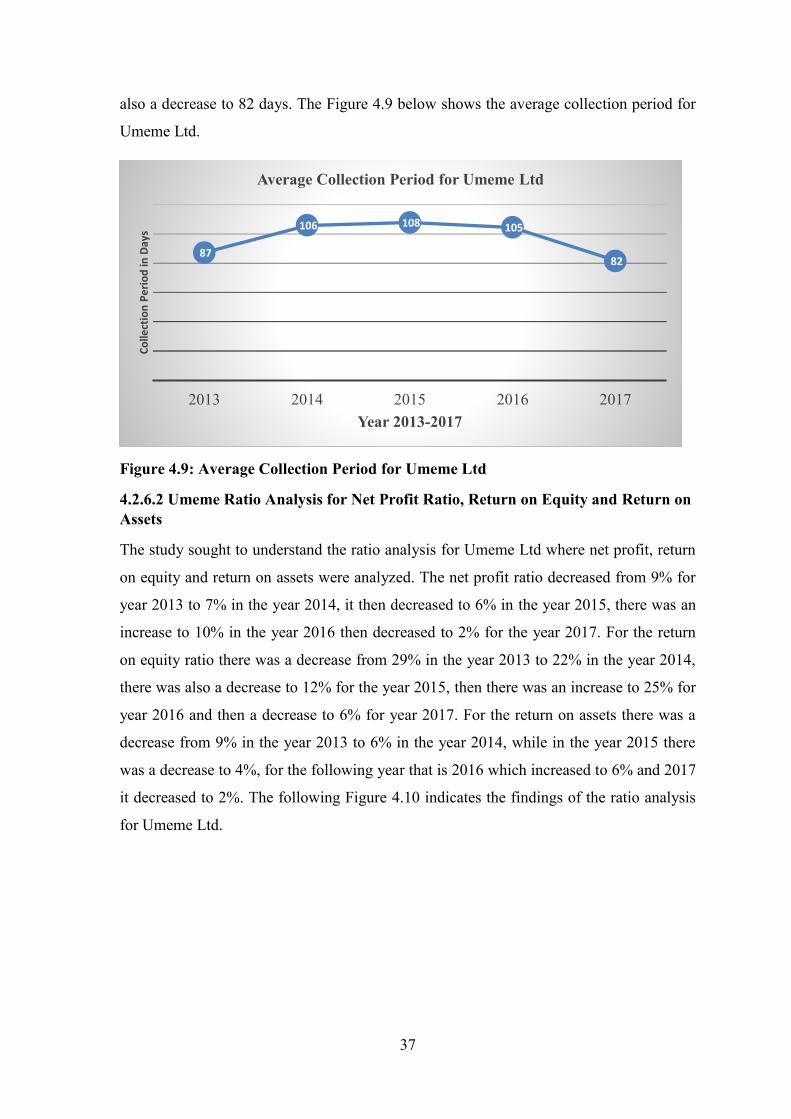

Figure 4.9: Average Collection Period for Umeme Ltd .................................................... 37

Figure 4.10: Umeme Ratio Analysis for Net Profit Ratio, Return on Equity and Return on

Assets ................................................................................................................................. 38

xiii

ABBRIEVIATIONS AND ACRONYMS

ANOVA Analysis of Variance

ACP Accounts Payables

CCC Cash Conversion Cycle

KenGen Kenya Electricity Generating Company PLC

KPLC Kenya Power and Lighting Ltd

NSE Nairobi Securities Exchange

OLS Ordinary least square

ROA Return on Assets

ROE Return on Equity

SMEs Small and Medium Enterprises

VIF Variance Inflation Factor

1

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the Study

Working capital management is a very important component of corporate finance because

it directly affects the liquidity and profitability of a company (Khalaf 2012). Ray (2012)

indicates that one of the vital issues that must be seriously considered before making

financial decision is the working capital. This is because it is an integral part of the

investment and has a direct effect on the liquidity and the financial performance of the

organization. Though, working capital encompasses short term financing and

investments, it is always overlooked when making financial decisions. Furthermore, its

lack of contribution to return on equity makes it work as a hold back for financial

performance.

Working capital management ensures a company has sufficient cash flow in order to meet

its short-term debt obligations and operating expenses. Many firms operating in different

economic sectors may have an optimal level of working capital that maximizes their

wealth (Rathiranee 2017). Ramesh, Hamad and Tammam (2017) argue that working

capital management is one of the prominent financial functions and it represents the

amount of money invested by an organization to meet the day-to-day operations. The

working capital encompasses the difference between the various current assets such as

cash, bank balances, inventories, trade and other receivables, marketable securities and

current liabilities such as trade and other payables, accrued expenses, short-term payables.

The present competitive business environment demands efficient use of resources, which

highlights the importance of working capital management. Previous researches have

concluded that the profitability of a business concern largely depends upon the manner in

which its working capital is managed (Adamu & Hussaini 2015). The inefficient

management of working capital not only reduces profitability but also may in the long run

lead to distress and financial crises in an organization. Akinyomi and Tasie (2016) argue

that the amounts invested in working capital are often high in proportion to the total

assets employed and so it is vital that these amounts are used in an efficient way.

2

Management of working capital, which aims at maintaining an optimal balance between

each of the working capital components which are, cash, receivables, inventory and

payables, is a fundamental part of the overall corporate strategy to create value and is an

important source of competitive advantage for the organization (Waema & Nasieku

2016). The crucial part in managing working capital is maintaining sufficient liquidity for

the day-to-day business operation to ensure the firm’s smooth running and meeting its

obligations.

Management of working capital necessitates short term decisions in working capital and

financing of all aspects of both firm’s short-term assets and liabilities (Nyabuti &

Mokeira 2014). They further indicate that the main objective is to ascertain that the firm

has the ability to continue operating with sufficient cash flow for payment of both

maturing short term debt and impending operational expenses. Its thus involves multiple

crucial decisions which involves managing account payables and account receivables.

Working capital management explicitly affects both financial performance and level of

desired liquidity. If a firm will invest heavily in working capital, that is, more than its

needs, then the profits which can be generated by investing these resources in fixed or

long-term assets will be diminished (Azhagaiah & Muralidharan 2017). Magudba and

Ogbonnaya (2016) conducted a study to determine the working capital management

practices and financial performance of manufacturing companies in Nigeria. The study

employed multiple regressions in analyzing the data sourced from the published financial

statement of the firms under the study. A significant outcome of the study was that

Average Payment Period and Average Collection Period impacts on both Earnings per

share and Return on capital employed. The implication is that efficient management of

working capital will improve the financial performance of the manufacturing firms.

Financial performance is a subjective measure of how well a firm can use assets from its

primary mode of business and generate revenues. The term is also used as a general

measure of a firm’s overall financial health over a given period of time and can be used to

compare similar firms across the same industry or to compare industries or sectors in

aggression (Nyabuti & Ondiek 2016). Financial performance is a subjective measure of a

firm’s overall financial health over a given period of time and can be used to compare

similar firms across the same industry According to Ganag, Kalaiselvan, and Suriya

(2015) measures of financial performance include liquidity, solvency, profitability debt

3

repayment capacity and financial efficiency of the firm. Financial performance can be

measured by the rate of return on investment. The management of a firm working capital

affects its performance. The basic purpose of managing working capital is controlling of

current financial resources of a firm in such a way that a balance is created between

profitability of the firm and risk associated with that profitability. The performance of a

firm can be measured in several ways. Brigham and Gapenski (1999) indicate that the

measures of profitability can include book value based or market value based. They

contend that accounting ratios such as return on equity, return on sales and return on

assets can be used to measure firm’s financial performance.

Management of working capital aims at maintaining an optimal balance between each of

the working capital components, that is, cash, receivables, inventory and payables is a

fundamental part of the overall corporate strategy to create value and is an important

source of competitive advantage in businesses (Abdullahi, Rahima, & Abbass, 2016). In

practice, it has become one of the most important issues in organizations with many

financial executives struggling to identify the basic working capital drivers and the

appropriate level of working capital to hold so as to minimize risk, effectively prepare for

uncertainty and improve the overall performance of their businesses (Azhagaiah &

Muralidharan 2017).

Nairobi Securities Exchange is one of the strongest capital markets in Africa. The Nairobi

Securities Exchange started in the 1920's when the country was still a British colony. The

NSE has undergone numerous transformations over the years to enhance its effectiveness

and adapt to changes in the economic environment, investors interest and leverage on

technology. The NSE has stringent rules and regulations on how accompany is to be

enlisted on the stock market. Quoted companies are divided into different sectors, namely

Agricultural, Commercial and services, Telecommunication and Technology, Automobile

and Accessories, Banking, Insurance, Investment, Manufacturing and Allied,

Construction and Energy. Different companies quoted at the NSE have adopted different

working capital management policies. The NSE as a secondary market provides listed

companies with the opportunity to benefit from improved access to capital, increased

global profile and access to liquidity. There are five listed Energy and Petroleum

Companies in the NSE. They include Kenol Kobil Limited, Total Kenya Limited,

KenGen Limited, Kenya Power and Lighting Company and Umeme Limited.

4

1.2 Statement of the Problem

Working capital management has an important role for the firm’s success or failure

because of the effect on firm’s financial performance and liquidity (Gamze, Ahmet &

Emin 2012). Tanveer, Muhammad, Khan and Sadaf (2016) indicate working capital

management is a tradeoff between risk and profitability. Risk and profitability mismatch

may increase firm’s profitability in the short run but at a risk of insolvency. Managers are

therefore coming to realization that incorrect evaluation of the liquidity implications of

the firm’s working capital needs may, in turn subject creditors and investors to an

unanticipated risk of default. Energy sector as a key foundation and one of the

infrastructural enablers upon which the economic, social and political pillars of its long-

term development strategy will be built. However, energy sector in Kenya faces

challenges such as low access to energy, high cost of energy, irregular supply and high

cost of energy investments (KIPRA, 2017).

Previous studies such as that of Gamze, Ahmet and Emin (2012), determined the effects

of working capital on firm performance in Turkey. The study was based on secondary

data collected from 75 manufacturing firms listed on Istanbul Stock Exchange. The

results demonstrate that firms can increase profitability measured by gross operating

profit by shortening collection period of accounts receivable and cash conversion cycle.

Leverage as a control variable had a significant negative relationship with firm’s financial

performance. Naeem, Malik, Muhammad and Mehboob (2014) on the effects of working

capital management on firm performance of non-financial listed firms in Pakistan. Three

performance measures namely gross profit margin return on asset and return on equity

were used to estimate the impact of working capital variables such as average age of

inventory, average collection period, and average payment period. The findings indicate

that working capital management has material effect on financial performance. A study

conducted by Irokwe and Wakoma (2017), determined how working capital management

affects firm performance of oil companies in Nigeria. The study employed Quasi-

Experimental design. The study concluded that there is an insignificant but undesirable

relationship between working capital and return on equity. The study further concluded

that working capital management impacts performance of Nigerian Oil Companies

primarily from the domain of return on assets.

5

The relationship between working capital management and financial performance of

companies quoted at Nairobi Securities Exchange, Kenya as conducted by Nyabuti and

Ondiek (2012). The study utilized secondary data obtained from the published financial

statements which were readily available at the NSE and the CMA libraries. The study

concluded that there is an existing relationship between working capital management

policy and financial performance of companies quoted at NSE. The dependent variable

which was financial performance was influenced by the independent variables which

were aggressive investment policy and aggressive financial policy. Similarly, Nduta

(2015) conducted a study to determine the effect of working capital management on

financial performance of manufacturing firms listed in the NSE. The study used

secondary data obtained from the firms published financial statements in their respective

websites for a period of 5 years, 2010-2014. Multiple regression and correlation analysis

were carried out on the data to determine the relationships between components of

working capital management and the profit after tax of the firms. The study established

that there is a positive relationship between ROA on the current liabilities to total

liabilities ratio, Current Asset to Total Asset ratio and the current ratio of manufacturing

firms evaluated.

There is scanty of studies on the effects of working capital management on financial

performance of energy and petroleum firms listed in the NSE. There is limited research

that has been done especially for the Energy and Petroleum sector as such is not

comparable to other researches done in the developed world or middle-income countries

where the empirical studies have been conducted and as a result, the researcher believes

there might be differences on the study findings. The study will seek to fill the gap by

studying the effect of working capital management of financial performance of Energy

and Petroleum companies listed in the NSE.

1.3 Purpose of the Study

The purpose of the study was to determine the effect working capital management on

financial performance of energy and petroleum companies listed in the Nairobi Securities

Exchange.

6

1.4 Research Questions

1.4.1 How do accounts receivables affect financial performance of energy and petroleum

companies listed in the NSE?

1.4.2 What is the effect of cash conversion cycle on financial performance of energy and

petroleum companies listed in the NSE?

1.4.3 What is the effect of accounts payables on financial performance of energy and

petroleum companies listed in the NSE?

1.5 Significance of the Study

1.5.1 Energy and Petroleum Companies

The study findings are of importance to energy and petroleum companies both listed and

non-listed. From the study findings, conclusions and recommendations, the companies is

able to identify effective working capital management practices with the aim of

controlling risk associated with working capital and also striking a balance between

current assets and current liabilities.

1.5.2 Policy Makers

The results of this study are significant to the policy makers and regulators such as the

capital markets to implement new set of policies and regulations regarding working

capital management for companies listed under the energy and petroleum sector of the

Nairobi Securities Exchange.

1.5.3 Financial Analysts

This study is of importance to financial and other parties whose knowledge of the

relationship between working capital management and the financial performance is

important input into investment analysis and investment decision making.

1.5.4 Future Researchers

The study findings will also be of significance to future researchers and academicians.

Through the study findings, future researchers will be able to use them as sources of

reference material for studies conducted concerning working capital management and

financial performance.

7

1.6 Scope of the Study

The study was conducted in Nairobi, Kenya with specific focus on the Energy and

Petroleum Companies listed in NSE. There are currently five energy and petroleum

companies listed in the NSE and they include Kenol Kobil Limited, Total Kenya Limited,

KenGen Limited, Kenya Power and Lighting Company and Umeme Limited. The study

analyzed financial information for all the five companies for a five-year period (2013-

2017). The information was obtained from secondary sources such as the NSE database,

the CMA database, published journals and audited company financial reports in the

company websites. However, the possible limitation that the researcher encountered

during the study was missing financial data from the reports.

1.7 Definition of Terms

1.7.1 Account Payables

An account payable is defined as an unsecured, non-interest-bearing current liability,

owed by the company to a supplier for the purchase of goods or services (Besley &

Brigham, 2007).

1.4.2 Account Receivables

Accounts Receivable is defined as the proceeds or payment which the company receives

from its customers who have purchased its goods and services on credit (Weygandt,

Kimmel and Kieso, 2015).

1.7.3 Cash Conversion Cycle

Cash conversion cycle is defined as the length of time a company’s cash is tied up in

working capital before that money is finally returned when customers pay for the

products sold or services rendered (Churchill & Mullins, 2001).

1.7.4 Working Capital

Working capital refers to the circulating capital required to meet the day to day operations

of a business firm (Besley & Brigham, 2007).

8

1.7.5 Working Capital Management

Working capital management refers to a company’s managerial accounting strategy

designed to monitor and utilize the two components of working capital, current assets and

current liabilities, to ensure the most financially efficient operation of the company

(Bhalla, 2014).

1.8 Chapter Summary

This chapter has discussed the background of the study, the problem statement, the key

research questions, the significance of the study, the scope of the study and also defined

the key study terms. Chapter two discusses the literature review based on the research

questions highlighted in chapter one. Chapter three gave a detailed explanation of the

research methodology that was adopted in the study. Chapter four reported the study

results and findings based on the data that was collected. Chapter five gave the summary,

discussion to the study and also give study recommendations.

9

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction

This chapter discusses literature review based on the purpose of the study which is to

determine the effect working capital management on financial performance of energy and

petroleum companies listed in the NSE. The literature review was based on the research

questions which were; what is the effect of account receivables on financial performance

of energy and petroleum companies listed in the NSE; what is the effect of cash

conversion cycle on financial performance of energy and petroleum companies listed in

the NSE and how does account payables affect financial performance of energy and

petroleum companies listed in the NSE?

2.2 Effects of Account Receivables on Financial Performance

2.2.1 Relationship between Account Receivables and Financial Performance

Accounts receivable as a component of cash flow has a direct effect on the profitability of

a business. A firm’s competency to synchronize cash inflows with cash outflows in

formulating a cash flow management strategy is important to a firm’s financial

performance (Gill, Bigger & Atnur 2011). Receivables are large investments in firm

assets which are like capital budgeting projects measured in terms of their net present

value. According to Ahmet and Emin (2012), accounts receivables stimulate sales

because it allows customers to assess product quality before paying but on the other hand,

debtors involve funds which an opportunity cost. Based on the characteristic of accounts

receivable; the element of risk, economic value and futurity explains the basis and need

for efficient management of receivables.

Account collection period is represented as the average collection period resulting from a

company selling its products or services on credit. This period is the average length time

form a sale on credit until the payment becomes usable funds for the firm (Sumathi,

2016). ACP involves managing the credit available to the firm’s customers, and also in

receiving, processing and collecting payments. Setting credit standards enables effective

management of credit and accounts receivable process. This process involves applying

10

techniques for determining which customer should receive credit and how much credit

should be granted. Relaxed credit standards generally yield increased sales and additional

profits, whereas tightened credit standards reduce investment in accounts receivable and

thus lowered sales and profit.

A study conducted by Divya, Simran and Vartika (2017) determined the effects of

accounts receivables management on the profitability of the commercial vehicle industry

in India. The study was based on a sample of six commercial vehicle companies. The

multicollinearity among the independent variables was determined on the basis of

Variance Inflation Factor (VIF). Autocorrelation was tested using the Durbin-Watson test.

The White test was used to test heteroscedasticity of the data. Profitability was measured

using return on capital employed. The research was conducted for the period 2009 to

2016. The findings indicated a significant positive relationship between debtor’s turnover

ratio and profitability of the firm. This implies that receivables management should be a

key focus point for improving profitability in the commercial vehicle industry.

The effects of accounts receivable management on profitability of firms during the

financial crisis in Serbia (Ksenjia 2015). A sample of 108 firms is used, which are the

most successful Serbian firms listed at the Prime and Standard Listing as well as the

Multilateral Trading Platform of the Belgrade Stock Exchange. The accounts receivables

policies were examined in the crisis period of 2008-2011. In order to explore the relation

between accounts receivables and firm’s profitability, the short-term effects were tested.

The study showed that between accounts receivables and two dependent variables on

profitability, return on total asset and operating profit margin, there was a positive but no

significant relation. The study concluded that the impact of receivables on firm’s

profitability changes in times of crisis.

A study conducted by Abdullahi, Rahima and Abass (2016) determined the effects of

trade receivables and inventory management on the performance of SMEs in Malaysia.

66 sample of SMEs involved in manufacturing covering from 2006-2012 was used for the

study. Ordinary least square (OLS) regression is used to estimate the relationship between

independent and dependent variable. The result indicated that days account receivable and

inventory turnover in days are negatively related to SME profitability substitutes which

include return on assets, return on equity and net operating profit. The result implies that

11

profitability of SME manufacturing depends upon effective of working capital

components management.

The management of accounts receivable is largely influenced by the credit policy and

collection procedure of a firm. A credit policy specifies requirements to value the worth

of customers and a collection procedure which provides guidelines to collect unpaid

invoice that will reduce delays for customers who have not yet made payment for goods

and services and outstanding receivables (Okpe & Nwakego 2015). Excessive level of

accounts receivable ratio on profitability may lead to negative effect. This is because if a

firm has so many debtors to pay, they may become short of cash which may lead to

difficulty in settling their short-term financial obligations (Sharma & Kumar, 2011).

Profit may be called real profit after receivables are turned into cash.

The relationship between working capital management and the financial performance of

brewery firms quoted on the Nigerian Stock Exchange (Aondana, Saka & Ipevnor 2017).

An Ex-post facto research involving trend analysis of eleven years (2002 to 2012) annual

reports of three brewery firms quoted on the NSE was carried out using the purposive

sampling technique. Data obtained were analyzed with the use of regression analysis. The

result indicated that each working capital components affected profitability. The findings

of the study revealed a significant negative impact of average period of debt settlement

and a statistically significant relationship between average collection period and financial

performance. The study suggested that there is need for managers to delay payment to

suppliers and take advantage of the funds as short-term credit which does not attract

interest costs to reinvest in order to generate more income for shareholders.

A study conducted by Okpe and Nwakego (2015), analyzed the effects accounts

receivable management on profitability of building materials, chemicals and paint

manufacturing firms in Nigeria. The data were collected from the Annual Reports of the

companies under study. Secondary data was used and was extracted from the Annual

report and statement of accounts and building material/chemical and paint companies in

Nigeria. The hypotheses were tested using multiple regression technique. At the end of

the study, the results showed that accounts receivable had positive and significant effects

with the profitability ratio at 1% levels of significance. This means that unit increase in

the variables brings about corresponding increase in the profitability ratio of the building,

12

chemical and paint companies in Nigeria. Both debt ratio and sales growth rate had

negative and non-significant effect on profitability.

The impact of accounts receivable management on the financial performance of Small

and Medium Firms in Mogadishu-Somalia. The target populations had 102 SMEs from

three sectors (Osman & Ayuma 2018) conducted a study to determine. The study used

both probability and non-probability sampling procedures and obtained a sample of 81

based on Slovene formula. Inferential statistics such as Pearson correlation coefficient

and coefficient correlation were used to analyze quantitative data and descriptive statistics

are employed for variables of the study. The study concluded cash flow management and

other independent variables (debt management, credit policy management and inventory

management) have positive significant effect on financial performance at 5% level of

significance.

Efficient accounts receivable management affords a firm improve on its profitability by

reducing the transaction costs of raising funds in case of liquidity crisis (Ahmet 2012). A

study conducted by Munene and Tibbs (2018) was aimed at establishing the relationship

between accounts receivable management and financial performance of Embu Water and

Sanitation Company Limited. This study adopted descriptive research to test the

relationship variables of the study. The study used secondary data which was obtained

from the accounts and finance departments. Descriptive statistics and inferential statistical

techniques were used to analyze the data and presented in tables. Average collection

period and current ratio was found to be significant positive association with return on

equities, indicating that if time period of debtor’s payment is increased then overall

financial performance increases.

A study conducted by Mathenge (2016) to determine the effect of trade receivables

management on profitability of manufacturing companies listed in the Nairobi Securities

Exchange. A descriptive research design was used in this study. The findings of the study

were arrived at using the quantitative research method. The extent and nature of

relationship between the various variables under study was identified using correlation

and regression. Relationships among the dependent and independent variables and

instances of multicolinearity were evaluated using the Pearson correlation analysis. The

study concluded that Average Collection Period, bad debt to receivables ratio and

accounts receivables turnover contribute to 24.7% of the overall profitability. The study

13

concluded that the average collection period has a significant and negative effect on

profitability.

The effects of accounts receivable on the financial performance of firms funded by

government venture capital in Kenya as conducted by Kilonzo, Memba and Njeru (2016).

The target population comprised all firms funded by government venture capital in

Kenya. The study adopted a census approach because of the small number of firms. Both

descriptive and inferential analyses were done. Analysis for variance (ANOVA) and

regression analysis were used to test the hypothesis. The results showed there is a positive

relationship between accounts receivables and financial performance of firms funded by

government venture capital in Kenya. Accounts receivable explained 25.7% of the

financial performance of firms funded by government venture capital in Kenya while the

variation of 74.3% is explained by other factors.

2.3 Effects of Cash Conversion Cycle on Financial Performance

2.3.1 Relationship between Cash Conversion Cycle and Financial Performance

A firm's performance mainly depends on the way the firm is able to manage its resources

at all times. In order to manage working capital efficiently, a firm has to be aware of how

long it takes them, on average, to convert their goods and services into cash. This length

of time is formally known as the Cash Conversion Cycle. In order to measure how well a

firm manages its working capital, a financial performance metric called cash to cash cycle

which was developed by Richards and Laughlin (1980). According to Afzar and Nazir

(2008), cash conversion cycle is a comprehensive performance measure used for

reviewing the ability of companies in managing their capital. Cash conversion cycle

indicate the efficiency of management of current assets. Shorter the time of cash

conversion allows the firms to generate more sales from the amount invested, which

shows that business utilized their resources for generating maximum profit.

The effects of cash conversion cycle on the performance of the cement industry in

Pakistan as conducted by Muhammad, Abdul and Zahid (2014). The study used the

sample of 16 firms selected from cement industry of Pakistan for the period of six years

from 2007 to 2012. The correlation and regression analysis are used to examine the

relationship between cash conversion cycle and firm’s performance i.e. return on assets.

14

The study examined the impact of different component variables of cash conversion cycle

which included receivables collection period, inventory conversion period and payables

deferral period. The findings of the study show negative relationship between firm’s cash

conversion cycle and profitability.

The effect of cash conversion cycle on the profitability of manufacturing companies listed

in the Karachi Stock Exchange Pakistan as conducted by Raheem and Qaisar (2013). The

study took into consideration five years financial statements data starting from 2007 to

2011. Results showed that manufacturing companies are have low average return on asset

and high average return on equity with reasonable average cash conversion cycle.

Regression results after adjusting for heteroskedasticity of data to minimize the effects of

outliers showed that cash conversion cycle has significantly inverse association with both

return on assets and equity indicating that lesser the cash conversion cycle, the greater

would be the profitability measured through return on assets and equity.

The relationship between cash conversion and profitability of firms as conducted by

Majeed, Aziz, Saleem and Makki (2013). The study used the sample of 32 companies

selected randomly from three manufacturing sectors which included chemical,

automobiles and construction and material for the period of five years ranging from 2006

to 2010. Correlation and regression analyses were used to examine the relationship of

Cash Conversion Cycle with performance of the firms using profitability measures such

as return on assets, return on equity and operating profit. The study examined the impact

of different variables of cash conversion cycle on firm’s performance. Similar to the

findings by Muhammad et al., (2014), the study found that the average collection period

of accounts receivables, inventory conversion period and cash conversion cycle have

negative relationship with firm’s performance.

The impact of cash conversion cycle on the profitability of listed hotels and travels

companies in Sri Lanka (Nimal & Anandasayanan 2015). The study used the sample of

10 companies selected randomly from hotels and travels sectors for the period of five

years ranging from 2008 to 2012. This study was based on secondary quantitative data

and the data related to cash conversion cycle and profitability was collected for the period

of 5 years starting from 2008 to 2012 using the annual reports of the selected companies

which were listed in Colombo Stock Exchange. Secondary data was also obtained from

the annual handbook published by Colombo Stock Exchange. Correlation and regression

15

analyses were used to examine the relationship of CCC with performance of the firms

with profitability measures of return on assets, return on equity and net profit margin. The

study found that the cash conversion cycle (CCC) has significantly negative association

with firm’s performance.

The relationship between cash conversion cycle and the profitability of cement

manufacturing companies in India (Panigrahi 2013). Firm size and debt ratio are taken as

control variables. The study took into consideration top five Indian cement companies for

a period of 10 years starting from 2001 to 2010. Results showed that the selected

companies had low average return on asset and return on equity with significantly

negative cash conversion cycle. Regression results after adjusting for heteroskedasticity

of data to minimize the effects of outliers showed that cash conversion cycle has a

significant positive association with both return on assets and equity indicating that it is

not necessary that always the lesser the cash conversion cycle the greater would be the

profitability measured through return on assets and equity.

A study conducted by Murtala and Sani (2016), aimed to determine the impact of

conversion cycle on the profitability of listed telecommunication companies in Nigeria.

Data was collected from all the listed ICT firms from 2010 to 2014. The data was

analyzed using multiple linear regression analysis and the robustness check shows that the

data was normal. The annual reports and accounts of the companies under study, as well

as the Nigerian Stock Exchange Fact Books were used in constructing the data required

for the study. The R2 value means that 26% proportion of variation in the ROA was

explained by the independent variables. The findings confirmed that cash conversion

cycle is a good in influencing firm performance of the firms in ICT sector in the Nigeria.

The study also concluded that decrease in one day for conversion of inventory to sales

can lead to increase in return on assets.

The effect of cash conversion cycle on the profitability of Industrial and Domestic

product firms in Nigeria as conducted by Madubuko and Anastasia (2016). Receivable

ratio, payable ratio and inventory ratio were the variables studied in the study. The

research design used in the study was Ex-post facto research design. The study used only

secondary data extracted from annual report and statement of accounts of the companies

under study. Data was sourced from the annual reports of the selected Industrial and

Domestic companies in Nigeria. Generalized least square multiple regression analytical

16

tools were used to test the Hypotheses. The findings show that, accounts receivables and

accounts payable had significant positive effect on the industries’ profitability ratio at 1%

level of significance.

The effect of cash conversion cycle on the financial performance of public listed

insurance companies (Chuke, Agbo & Christian 2018). Data were collected from the

annual financial reports of sampled insurance companies. Multiple regression technique

was used in analyzing the model for testing the hypotheses. Return on assets was used as

the dependent variable. While cash conversion cycle was presented as the explanatory

variable, current ratio, debt asset ratio, fixed financial total asset ratio, Growth and Size

were all incorporated in the model as control variables. The results indicated that CCC

had negative and significant effect on profitability. Based on the findings, the study

recommended that insurance companies should endeavor to reduce their number of days

in CCC always in order to enhance their profitability.

A study conducted by Ikechukwu and Duru (2016) was aimed at determining the impact

of cash conversion cycle on the financial performance of Building materials, chemical

and paint manufacturing companies in Nigeria. Cash conversion cycle, receivable ratio,

payable ratio, and inventory ratio are the variables studied in this study. Data were

sourced from the annual reports of Health care companies in Nigeria. Generalized least

square multiple regression analytical tools were used to test the hypotheses. The findings

show that, inventory ratio and accounts receivable ratio had significant and positive effect

on firms’ profitability, accounts payable ratio and Cash conversion cycle had positive and

non- significant effect on firms’ profitability.

The effect of cash to cash cycle on profitability of basic material firms listed on the

Nigerian Stock Exchange for the period of ten years spanning 2007 to 2016 (Orjinta &

Okpalaukeje, 2018). The study employed ex-post facto research design and used

secondary data collected from the annual report of selected firms for the analysis. Simple

regression analysis (Pearson Correlation and Ordinary Least Square regression) were

employed to analyze the collected data. The results revealed that cash cover ratio was

found to have negative and insignificant effect on profitability proxy using return on asset

while quick ratio was found to have a positive and significant influence on profitability of

basic material firms at 5% level of significance. The study recommended that

management of basic material firms should reduce the magnitude at which they use up

17

cash and its equivalent in settling their short-term obligations in order to improve their

profitability.

Smilarly in Kenya, Mathuva (2014) conducted a study on the determinants of cash

conversion cycle in Kenyan listed non-financial firms. The study also examines the speed

of adjustment to the target CCC and the factors that influence corporate decisions on the

optimum length of the CCC. Based on a sample of 33 publicly traded firms on the NSE

for the period between 1993 and 2008, cross-sectional and time series analyses were

carried out on the data comprising 468 firm-years. A target adjustment model was

developed to examine the significant determinants of the CCC. Various regression

approaches including ordinary least squares, fixed effects and two-stage least squares

estimation models were used in data analysis. The study established that older firms and

firms with more internal resources maintain longer CCC. Moreover, higher returns on

assets, investment in capital expenditure and growth opportunities have a significant

negative association with the CCC.

A study by Muturi (2015) aimed at determining the effects of cash conversion cycle on

profitability of tea factories in Meru County. The study used primary method of data

collection. Census method was used to collect primary data from all the seven tea

factories in the county for a period of five years starting from 2009 to 2013. The

correlation and regression analyses were used to analyze and describe the nature of the

relationship between CCC and the firm’s profitability. A lot of literature has pointed out

that efficient management of cash has significantly influenced the firm’s profitability.

This study found out that the CCC significantly negatively affects firm’s profitability.

The study thus recommended that there is need therefore for the finance managers to

shorten the net cash conversion cycle to improve profitability.

The effect of cash conversion cycle on the profitability of companies listed in the Nairobi

Securities Exchange as conducted by Mohamed (2013). The relation between the firm’s

cash conversion cycle and its profitability was examined using dynamic panel data

analysis for a sample of firms listed on the Nairobi Securities Exchange for the period

from 2008 to 2012. The results indicated that there is a significant and negative

relationship between the cash conversion cycle and return on asset. The firms with shorter

cash conversion cycles were more likely to be profitable than firms with longer cash

conversion cycles. This is when the cash conversion cycle is relatively shorter; the firm

18

may not need external financing, which results in incurring less borrowing cost and

interest expense, hence increasing profitability.

Cash conversion cycle (CCC) has been considered a useful measure of firm’s effective

working capital management and especially the cash management (Muneeb & Kashif

2012). To explain this, they conducted a study to establish the optimal relationship of

cash conversion cycle with firm size and profitability. The data was collected from the

annual reports of 31 sampled firms out of the total firms in the related sectors i.e. 143

covering the period of 2006-2010. The data analysis was conducted by using One-Way

ANOVA and Pearson correlation techniques. From previous researches and findings, the

study also found that there was found a significant negative correlation between the CCC

and the firm size in terms of total assets and was found a negative correlation between

CCC and profitability in terms of return on total assets with the values of - 0.415 and -

0.131 respectively.

2.4 Effects of Accounts Payable on Financial Performance

2.4.1 Relationship between Accounts Payable and Financial Performance

Accounts payable is defined as the supplier whose payment for goods or services has

been processed but who has not yet been paid. Accounts payable includes trade credit and

accrued expenses which together provide finance to the operations of a business on an on-

going basis (Naeem et al., 2014). Firms would rather sell for cash than on credit, but

competitive pressure forces most companies to offer credits. Unlike credit from financial

institutions, accounts payables do not rely on formal collateral but on trust and reputation.

According to Singh (2004) the liquidity position of a firm mainly depends upon accounts

receivable and payable deferred policy as well as inventories conversion period of firm.

Firms often regard the amount owing to creditors as a source of free credit. It is one of the

major sources of secured short-term financing. Utilizing the value of relationship with

payee is a sound objective that should be highlighting as important as having the optimal

level of preventions (Gitman & Smith 2010). As a consequence, strong alliance between

company and its suppliers will strategically improve production lines and strengthen

credit record for future expansion. Singh (2004) argues that creditor is a vital part of

19

effective cash position. Purchasing initiates cash outflows and overzealous purchasing

function can create liquidity problem.

The impact of accounts payable use on profitability of SMEs in Sweden. A large cross-

sectional panel data set covering 15,897 Swedish SMEs in five industry sectors from

2009 to 2012 was analyzed using several statistical techniques (Darush & Öhman 2016).

The study findings indicated that the use of trade credit significantly and negatively

affects firm profitability, indicating that SMEs with lower accounts payable are more

profitable. Furthermore, liquidity level and firm size are positively related to profitability,

while firm age is negatively related to profitability. If firms rely, or are forced to rely, too

heavily on accounts payable as a funding source, their long-term profitability could be

jeopardized. According to Yazdanfar (2012), an efficient financing policy should make

the costs related to the use of trade credit more transparent. Thus, firm managers could

explicitly use trade credit agreements with their suppliers to control the costs related to

this particular financial source.

A study conducted by Doan, Bui and Hoang (2016) aimed at establishing the impact of

working capital on financial performance of the small and medium-sized enterprises in

Vietnam. Using panel data for 1,209 enterprises in the period from 2008 to 2015, with

ordinary least square method, random effects model and fixed effects model. The findings

showed that receivables and working-capital turnover impact negatively on financial

performance of enterprises. In line with accounts payable, the accounts payable period

and inventory conversion period have a direct relationship with corporate financial

performance. In addition, the results of the study also found that the growth rate, size, and

age of enterprises also affect financial performance directly.

The impact of account payables and account receivables on the financial performance the

Indian telecom industry (Jyoti & Uday 2017). Variables that were used in the study

included return on assets, average collection period, average payment period and cash

conversion cycle. The data analysis was carried out for eight telecom industry listed in

National Stock Exchange of India. The study was based on secondary data and data taken

for a period of five years in order to calculate all the variables. The research methodology

used in the study was descriptive statistics, correlation analysis and ordinary square least

regression analysis in order to know the impact of these variables on profitability. The

result of correlation analysis shows the ROA has negative relationship with average

20

collection period, cash conversion cycle while ROA has positive relationship with

average payment period.

Previous studies have established that changes in working capital have a strong positive

correlation to profitability and that whilst changes to receivables and inventory have a

positive correlation to profitability; changes in payables have an inverse relationship (Ani,

Okwo, & Ugwunta, 2013). The inverse correlation between payables and profitability is

contrary to the theory that advocates extending payment terms as a means of managing

working capital and improving liquidity. Moodley, Ward and Muller (2017) conducted a

study to determine the relationship between accounts payables and financial performance/

return on investors. The study applied a buy-and-hold portfolio methodology to an

extensive database of Johannesburg Stock Exchange over the period 1986 to 2014. The

study findings indicate that companies in industries that have a significant investment in

payables, there is a significant positive association between changes in payable days

return to investors and financial performance.

The effect of accounts payable settlement and accounts receivable on the financial

performance as conducted by Angahar, Rose and Mnena (2017). Average period of debt

settlement and average collection period of receivable were the explanatory variables of

the study while return on assets was the dependent variable. The study adopted an Ex-

post facto research involving trend analysis of eleven years using annual reports of three

brewery firms in Nigeria Securities Exchange. The result indicated that each working

capital components affected the company’s level of profitability at varying rates. The

findings of the study reveal a significant negative impact of APDS and a statistically

significant relationship between ACRP on the financial performance of these brewery

firms quoted on NSE. The study recommended that managers can delay payment to

suppliers and take advantage of the funds as short-term credit which does not attract

interest costs to reinvest in order to generate more income for shareholders.

A study conducted by Duru and Okpe (2015) was aimed at establishing the effect of

accounts payable management on corporate profitability of Brewery Manufacturing

Companies in Nigeria. The variables include, accounts payable, debt ratio and sales

growth rate. Secondary sources of data were used for the period 2000-2011. The results

show that accounts payable had negative but non-significant relationship with

profitability ratio of the companies under Brewery manufacturing companies in Nigeria.

21

Debt ratio had positive and significant relationship, while sales growth rate was negative

and significant with the profitability ratio of Brewery companies in Nigeria.

The relationship between accounts payable management policy and corporate profitability

in Nigerian quoted companies based on the data of 107 quoted companies spread across

23 sectors for the period 2006-2013 (Adolphus 2014). The study found that all the sectors

adopted an aggressive accounts payable management strategy by relying heavily on

current liabilities for financing their working capital needs. The findings also indicated

the adoption of this strategy produced negative profitability in most of the sectors. The

results also showed a strong positive correlation between net current assets ratio and

selected measures of profitability. The study recommended that companies would

maximize profitability and add value by adopting the conservative accounts payable

management strategy provided the operating environment and money markets are strong.

The study of Achode and Malingu (2016) on the effects of accounts payable as a source

of financing on the performance of listed manufacturing firms at the Nairobi Securities

Exchange. Census sampling technique was used, and the study used secondary data,

which was obtained from the companies’ statistics and journals at the Nairobi Securities

Exchange. SPSS was used to carry out the descriptive analysis of the variables, requisite

analysis and advanced analysis of the data. A multiple regression model was used to test

the relationship between the Accounts payable and firm performance. The results from

this research suggested that in most of the manufacturing firms listed at the NSE, there

was a direct positive relationship between Accounts Payable and the firm performance.

The relationship between accounts payable and SME financial performance for a sample

of 50 audited Kenyan SMEs as conducted by Kapkiyai and Mugo (2015). The study

aimed at finding how trade credit affects three measures of financial performance;

liquidity, profit margin and return on assets. Documentary guide was used in the study to

collect secondary data. Analysis was conducted using both inferential and descriptive

statistics specifically mean and standard deviation. Inferential statistics where Pearson

correlation coefficient to determine the degree of relationship while Multiple regression

model was used to test the hypotheses. Findings indicated that accounts payable

positively affected liquidity, profit margin and return on assets. The researchers

concluded that their findings are consistent with pecking order theory by SMEs in pattern

of using accounts payable as a finance source instead of other external sources of finance.

22

Management of accounts payables is very critical in ensuring that there is efficient

management of working capital (Bougheas, Mateut, & Mizen 2009). Firms should avoid

delays in paying for their supplies because of the disadvantages associated with these

delays. A study conducted by Kung’u (2015) was aimed at establishing the effects of

working capital management on the profitability of manufacturing firms in Kenya. A

questionnaire was used to collect primary data for the independent variables and a record

survey sheet was used to collect secondary data for the dependent variable. The results of

the study showed that there was positive linear relationship between accounts payable and

the profitability of manufacturing firms in Kenya. The study recommended that

manufacturing firms to regularly review their credit policies make early payments to their

suppliers in order to enjoy good relationship with their suppliers.

2.5 Chapter Summary

This chapter has presented discussed literature based on the three research questions. It

has discussed in detailed how the components of working capital; accounts receivable,

cash conversion cycle and accounts payable, influence financial performance. The next

chapter will discuss the research methodology that was used and adopted in the study.

This will include the research design, the population and sampling design, the methods of

data collection and data analysis.

23

CHAPTER THREE

3.0 RESEARCH METHODOLOGY

3.1 Introduction

This chapter gives the methodology that was used in the study. It describes the planning

of this research that undertakes to establish the effects of working capital management on

financial performance of Energy and Petroleum companies listed on Nairobi Securities

Exchange. The chapter discusses the research design, the population and sampling design,

the sampling technique that was used in the study, data collection methods, research

procedures, data analysis methods, and lastly the chapter summary.

3.2 Research Design

Research design as a plan for a study, providing the overall framework for collecting data

(Ricchie & Klein 2014). MacMillan and Schumacher (2001) define it as a plan for

selecting subjects, research sites, and data collection procedures to answer the research

questions. They further indicate that the goal of a sound research design is to provide

results that are judged to be credible. According to Saunder, Lewis and Thornhill (2007)

research design is a strategic framework for action that serves as a bridge between

research questions and the execution, or implementation of the research strategy. A

research design is a systematic plan to study a scientific problem. The design of a study

defines the study type research question, hypotheses, independent and dependent

variables, experimental design, data collection methods and a statistical analysis plan.

Research design is the framework that has been created to seek answers to research

questions or objectives (Mugenda & Mugenda, 2003).

This study adopted the use of descriptive research design. Descriptive research refers to

research studies that have as their main objective the accurate portrayal of the

characteristics of persons, situations or groups. Roberts and Burke (1989) define

descriptive research as a non-experimental research design used to observe (and measure)

a variable when little conceptual background has been developed on specific aspects of

the variables under study. This approach is used to describe variables rather than to test a

predicted relationship between variables.

24

3.3 Population and Sampling Design

3.3.1 Population

The population is the entire set of individuals (or objects) having some common

characteristics as defined by the sampling criteria established for the study (Cooper &

Schindler, 2011). In this study, the population of study comprised the listed Energy and

Petroleum companies. There are currently five companies from the energy and petroleum

sector that have been listed in the NSE. The population used comprised of all the Energy

and Petroleum companies listed in the Nairobi Securities Exchange as at 31st December

2017 namely; Kenol Kobil Ltd, Total Kenya Ltd, Kenya Electricity Generating Company

PLC, Kenya Power and Lighting Ltd and Umeme Ltd.

Table 3.1: Population Distribution

NO Energy and Petroleum Companies

1 Kenol Kobil Ltd

2 Total Kenya Ltd

3 Kenya Electricity Generating Company PLC

4 Kenya Power and Lighting Ltd

5 Umeme Ltd

Source: (Nairobi Securities Exchange, 2018).

3.3.2 Sampling Design

Sampling is a process of selecting samples from a group or population to become the

foundation for estimating and predicting the outcome of the population (Mugenda &

Mugenda, 2003). Some previous studies and research, the population may be small

enough thus bring out the need to include the entire population in the study. There also

exists studies which the population may be large and thus no the entire population can be

studied. The proportion of the population that is studied is identified as the sample of the

population. Sampling design in this study involved major procedures which include