Edmund Cannon Banking Crisis University of Verona Lecture 3.

28

Edmund Cannon Banking Crisis University of Verona Lecture 3

-

Upload

gladys-sutton -

Category

Documents

-

view

218 -

download

1

Transcript of Edmund Cannon Banking Crisis University of Verona Lecture 3.

Edmund Cannon

Banking CrisisUniversity of Verona

Lecture 3

Plan for today2

Review of Monday and Tuesday

Finish material from Tuesday

Opportunity for questions

I shall discuss the formative assessment tomorrow (after I have marked it).

Today’s Material: More about Risk

Measuring risk: how do they do it (VaR)?

Insuring risk: Credit Default Swaps

Systemic risk and endogeneity; housing market

REPO

How to measure risk3

Regulators interested in downside risk (things going wrong).

Variance (or standard deviation) does not measure precisely this.

Most widely used measure is Variance-at-Risk

Usually abbreviated VaR (VAR = Vector Auto Regression)

VaR = how bad things are if worst 1% (or x% happens)

≈ 1% critical value of the probability distribution

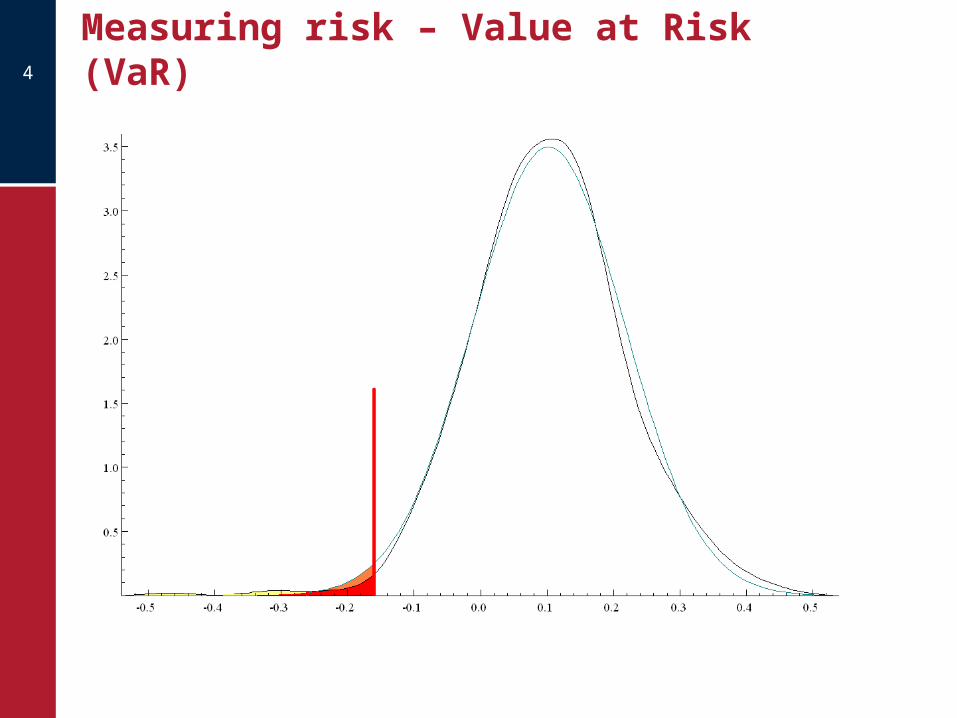

Measuring risk – Value at Risk (VaR)4

Normal or non-Normal5

If returns are Normal (= Gaussian) then:

The variance is a sufficient statistic for all measures of risk;

Estimates of the variance have a chi-squared distribution so it is easy to model how risk depends upon estimation error.

If returns are non-Normal then:

The variance cannot tell us about the risk of certain situations;

Estimates of the variance are unbiased but that is about all we can say;

Any model assuming Normality will heavily under-estimate “extreme events”.

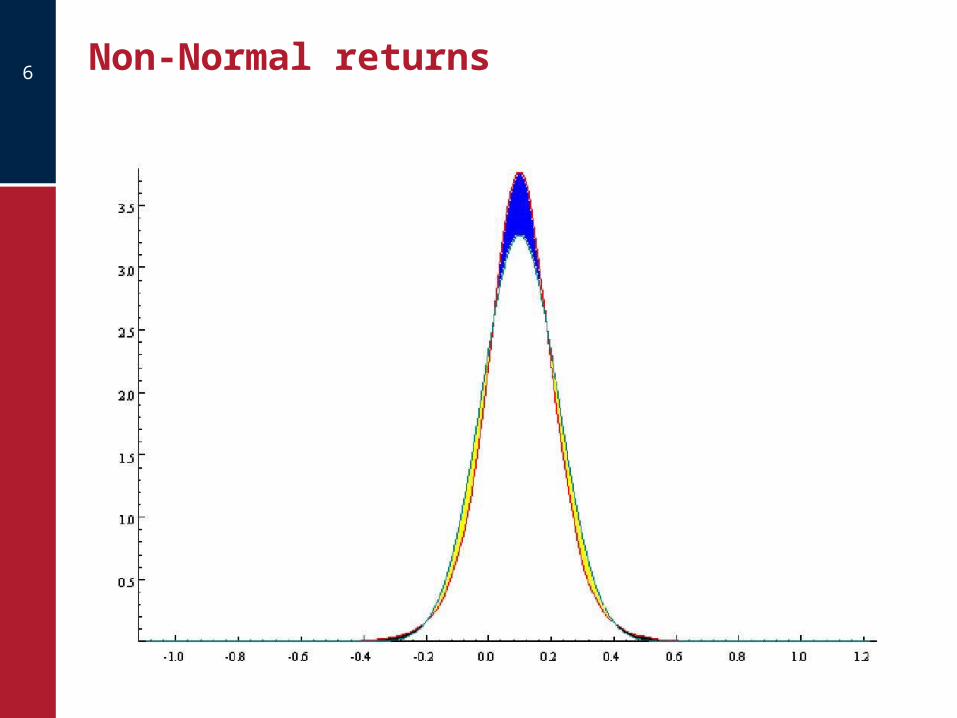

Non-Normal returns6

Statistical issues with VaR7

Statistical issues:

Expected value and Variance relatively easy to estimate;

Characteristics of “Tails” much harder to estimate.

Intuitive explanation of statistical problem:

By definition, very rare events are very rare;

Therefore there are very little data.

Possible solution:

make strong assumptions about the probability distribution (eg Normal)

Further problem: many estimates based on inadequate data (eg from last ten years: series is too short).

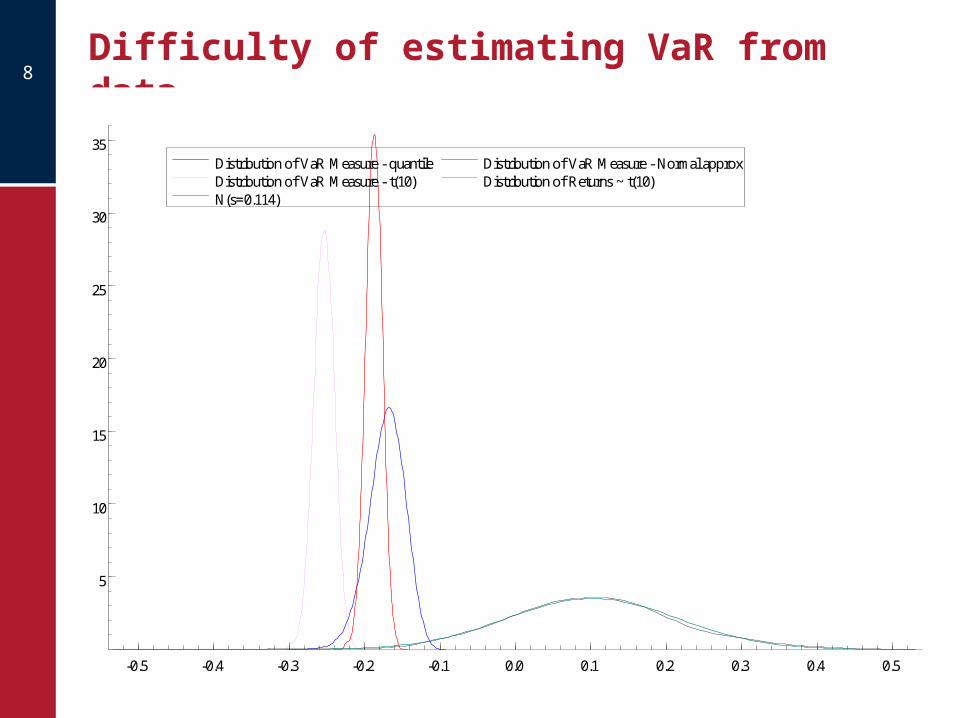

Difficulty of estimating VaR from data

8

Distribution of VaR Measure - quantile Distribution of VaR Measure - t(10) N(s=0.114)

Distribution of VaR Measure - Normal approx Distribution of Returns ~ t(10)

-0.5 -0.4 -0.3 -0.2 -0.1 0.0 0.1 0.2 0.3 0.4 0.5

5

10

15

20

25

30

35Distribution of VaR Measure - quantile Distribution of VaR Measure - t(10) N(s=0.114)

Distribution of VaR Measure - Normal approx Distribution of Returns ~ t(10)

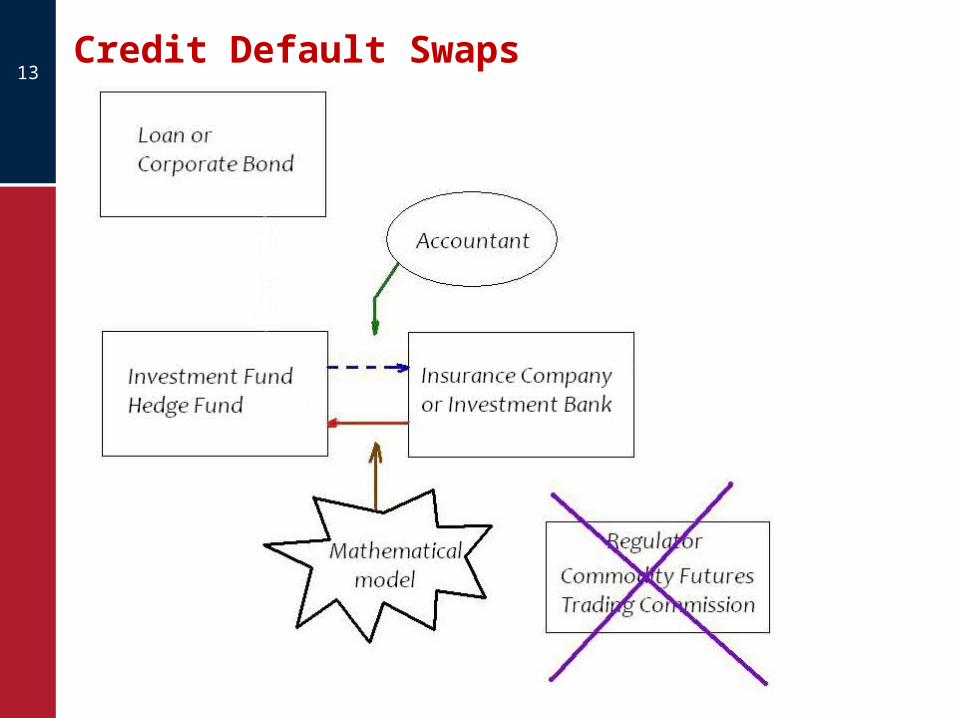

Reducing risk with insurance: Credit Default Swaps9

One way to reduce risk is to move risk off balance sheet – eg CDO.

Alternatively a bank can hold a risky asset on the balance sheet but purchase insurance through a Credit Default Swap.

The CDS insures against default. Insurance against price movements is insured through conventional future contracts (which I do not discuss).

Compare CDS with conventional insurance.

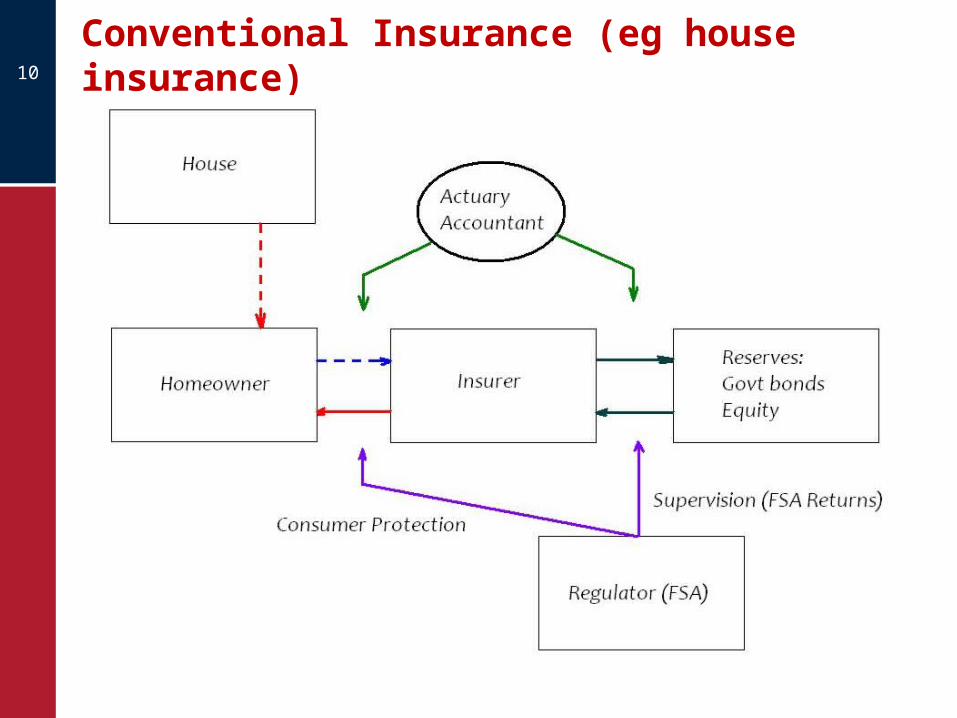

Conventional Insurance (eg house insurance)10

Characteristics of conventional insurance11

Standardised products:

Easy to have industry standards;

Straightforward to regulate;

Possibility of competition.

Purchaser must have an “insurable interest”:

Genuine insurance.

Often purchased by individuals: consumer protection.

Insurance companies are leveraged: capital regulation (Solvency I ~ Basel I).

Adverse selection and moral hazard.

Credit Default Swaps12

Pay monthly premium to provider (often a monoline).

Receive payment if bond defaults.

In problem cases: definition of default determined by ISDA.

Differentiated products – no industry standard.

Purchaser need not have an “insurable interest”:

Traded OTC not on exchange – prices difficult to observe.

Minimal regulation of reserve requirements:

Market participants impose capital requirements.

Who is the appropriate counter party for sovereign debt?

Credit Default Swaps13

“Endogenous” Risk14

Basic idea:

Economic insitutions magnify good and bad shocks.

Mechanism 1: Leverage

Unexpectedly good results increase capital (equity)

Banks lend more

Creates a bubble

Mechanism 2: Expectations / perceptions of risk

Firms only use recent data to evaluate risk

Selection bias

Too optimistic in good times; too pessimistic in bad times.

Leverage and endogenous risk (Shin)15

Leverage increases endogenous risk in all leveraged institutions, not just banks.

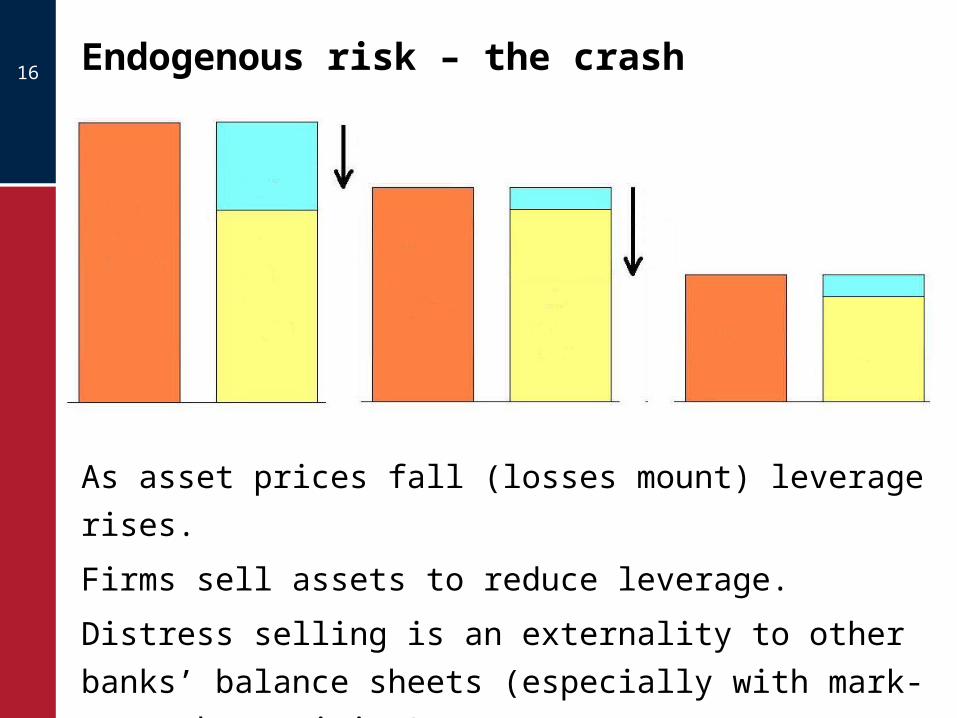

Endogenous risk – the crash16

As asset prices fall (losses mount) leverage rises.

Firms sell assets to reduce leverage.

Distress selling is an externality to other banks’

balance sheets (especially with mark-to-market

pricing).

House price bubbles17

House prices are very variable.

House prices rise

Fewer defaults

Mortgage banks make high profits and increase equity

Under-estimate default risk

Lend more money on easier terms

House prices rise further

18

01.0

3.19

99

01.0

8.19

99

01.0

1.20

00

01.0

6.20

00

01.1

1.20

00

01.0

4.20

01

01.0

9.20

01

01.0

2.20

02

01.0

7.20

02

01.1

2.20

02

01.0

5.20

03

01.1

0.20

03

01.0

3.20

04

01.0

8.20

04

01.0

1.20

05

01.0

6.20

05

01.1

1.20

05

01.0

4.20

06

01.0

9.20

06

01.0

2.20

07

01.0

7.20

07

01.1

2.20

07

01.0

5.20

08

01.1

0.20

08

01.0

3.20

09

01.0

8.20

09€0

€100,000

€200,000

€300,000

€400,000

€500,000

€600,000

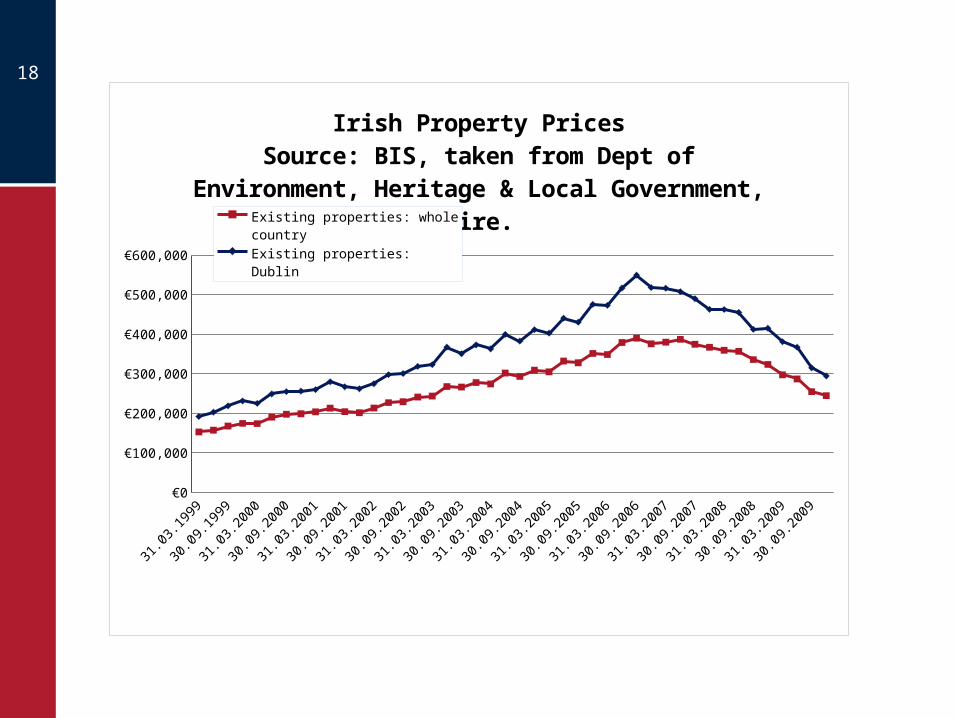

Irish Property PricesSource: BIS, taken from Dept of Environ-ment, Heritage & Local Government, Eire.

Existing properties: whole coun-try

Existing properties: Dublin

19

01/1

991

01/1

992

01/1

993

01/1

994

01/1

995

01/1

996

01/1

997

01/1

998

01/1

999

01/2

000

01/2

001

01/2

002

01/2

003

01/2

004

01/2

005

01/2

006

01/2

007

01/2

008

01/2

009

01/2

010

01/2

011£0

£20,000

£40,000

£60,000

£80,000

£100,000

£120,000

£140,000

£160,000

£180,000

£200,000

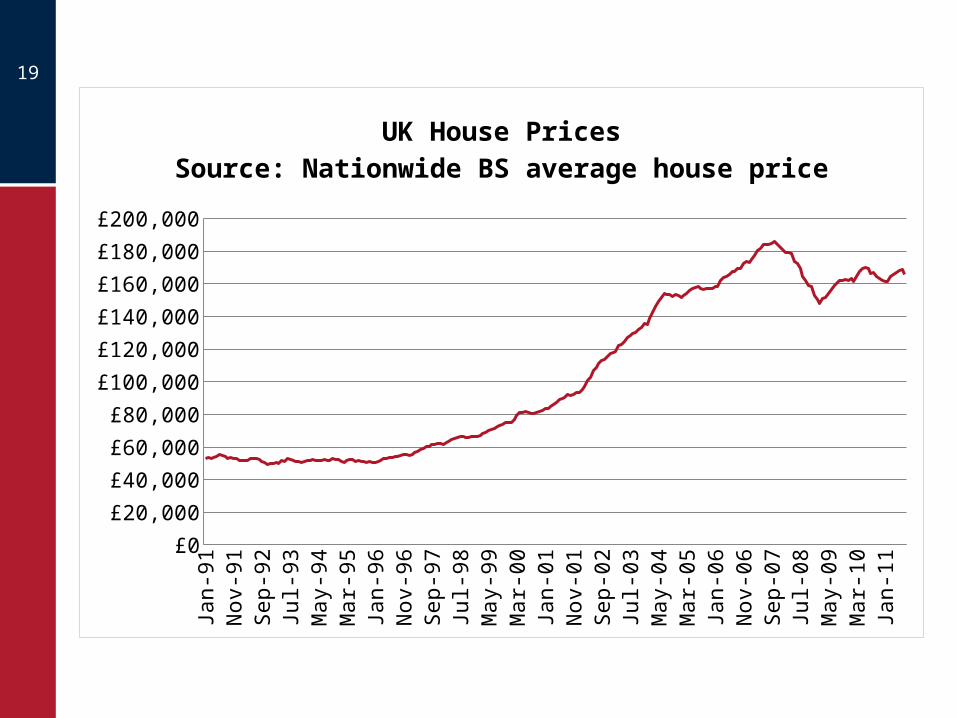

UK House PricesSource: Nationwide BS average house price

20

01

/03

/19

70

01

/03

/19

72

01

/03

/19

74

01

/03

/19

76

01

/03

/19

78

01

/03

/19

80

01

/03

/19

82

01

/03

/19

84

01

/03

/19

86

01

/03

/19

88

01

/03

/19

90

01

/03

/19

92

01

/03

/19

94

01

/03

/19

96

01

/03

/19

98

01

/03

/20

00

01

/03

/20

02

01

/03

/20

04

01

/03

/20

06

01

/03

/20

08

01

/03

/20

1010

100

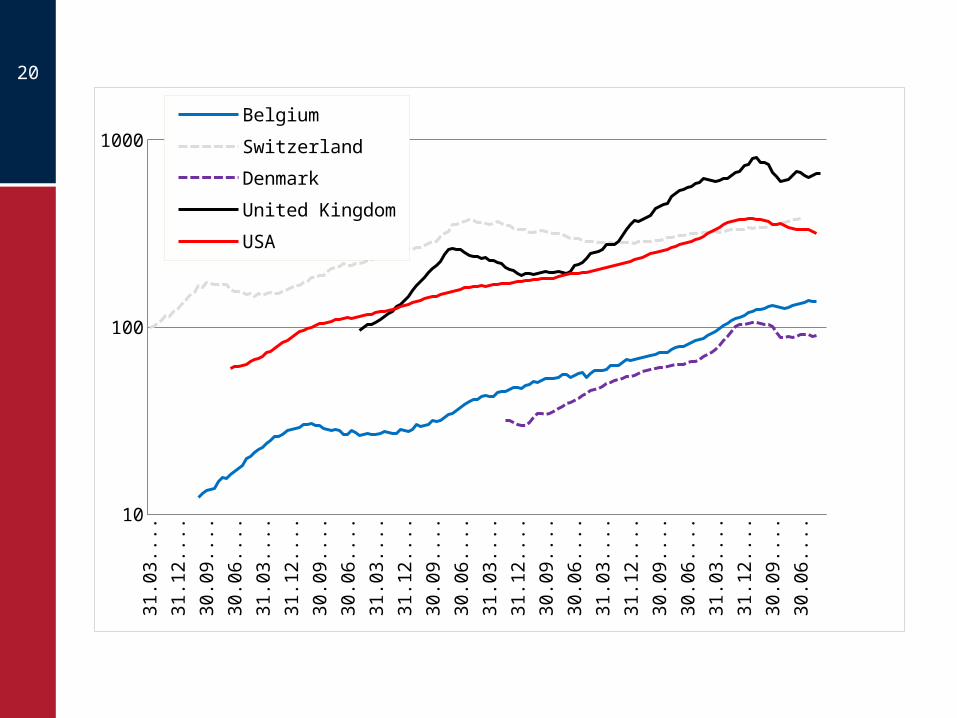

1000Belgium

Switzerland

Denmark

United Kingdom

USA

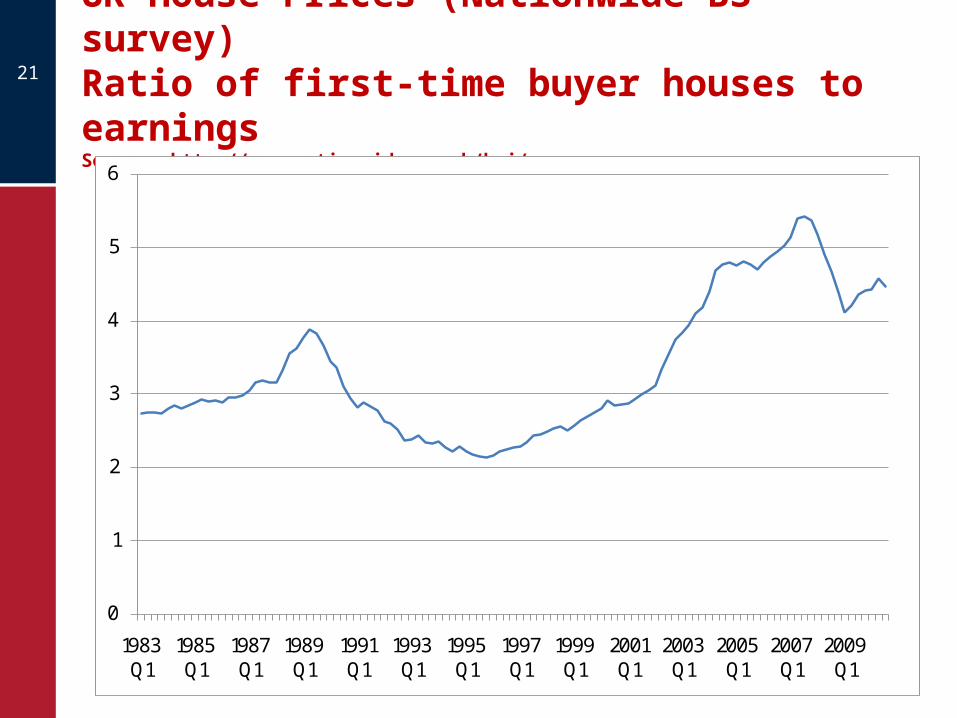

UK House Prices (Nationwide BS survey)Ratio of first-time buyer houses to earningsSource: http://www.nationwide.co.uk/hpi/

21

0

1

2

3

4

5

6

1983 Q1

1985 Q1

1987 Q1

1989 Q1

1991 Q1

1993 Q1

1995 Q1

1997 Q1

1999 Q1

2001 Q1

2003 Q1

2005 Q1

2007 Q1

2009 Q1

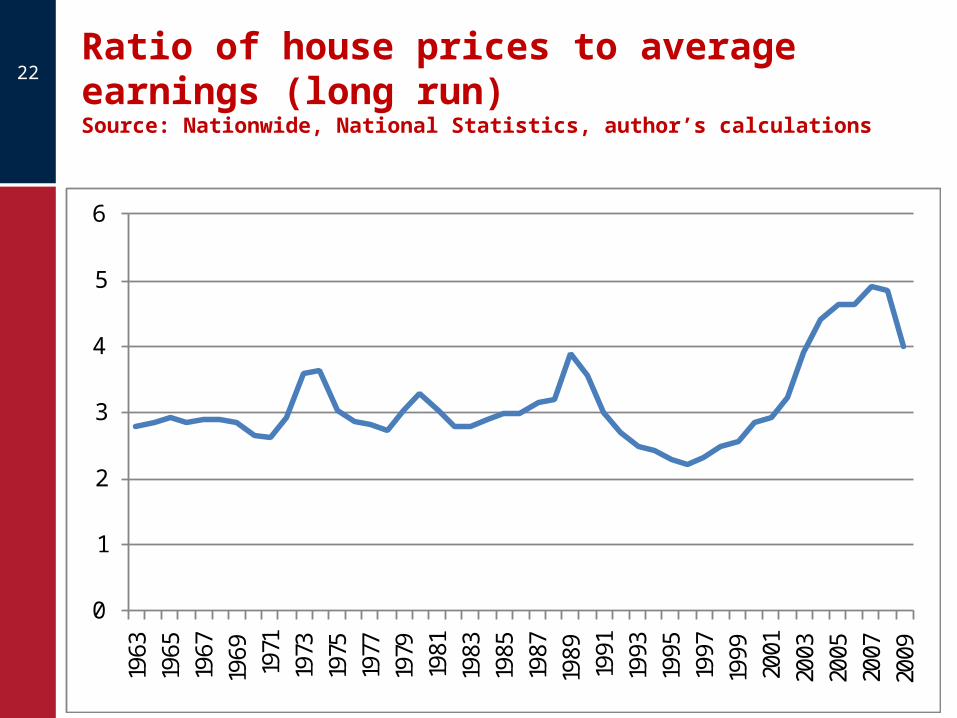

Ratio of house prices to average earnings (long run)Source: Nationwide, National Statistics, author’s calculations

22

0

1

2

3

4

5

6

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

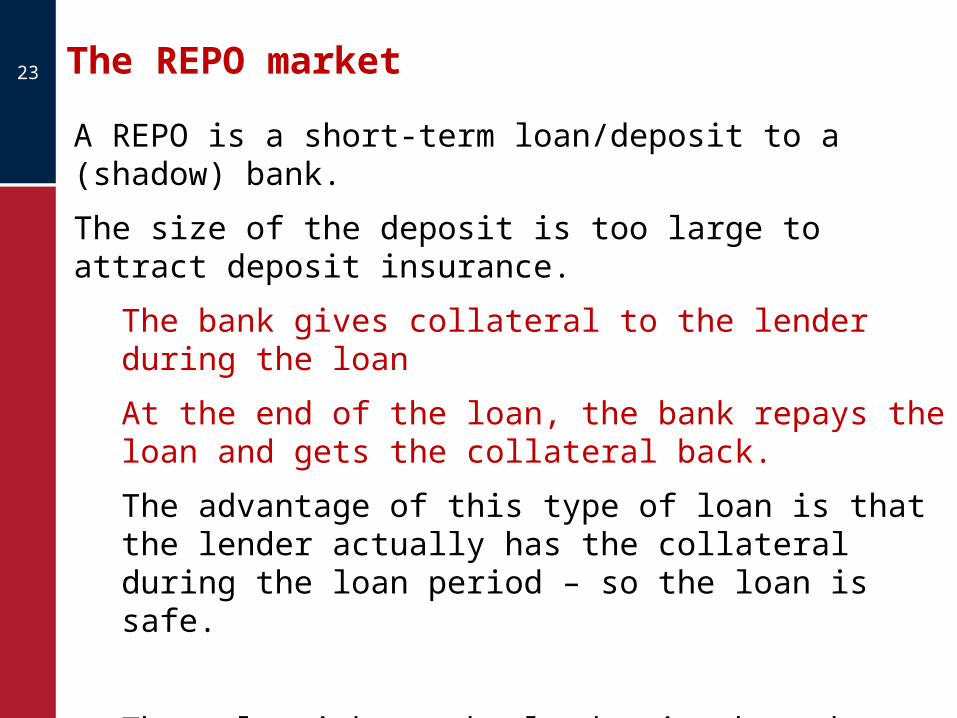

The REPO market23

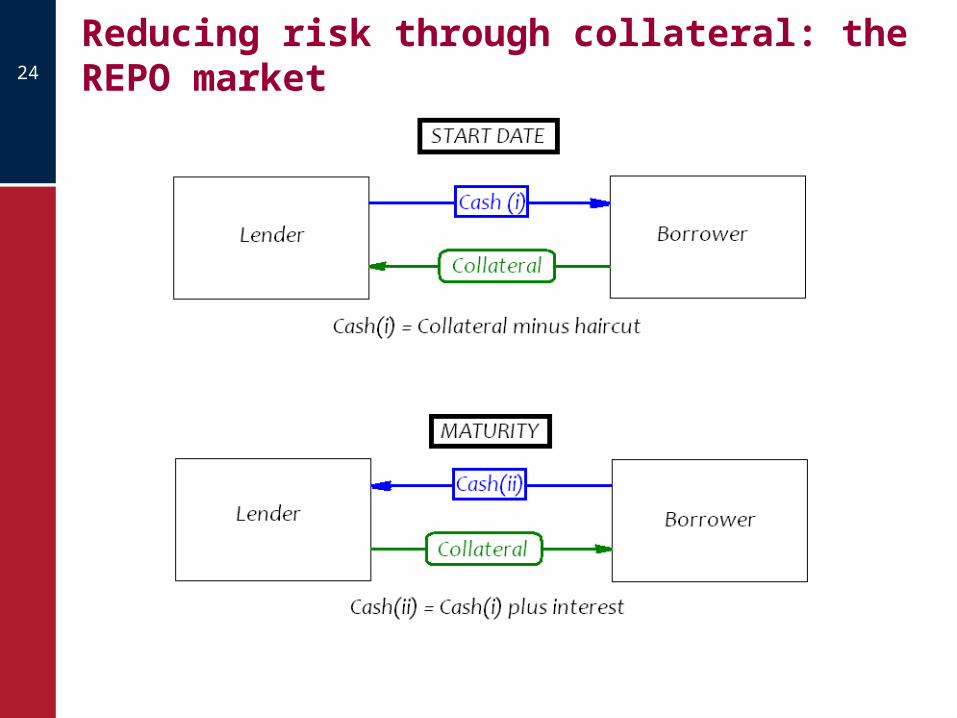

A REPO is a short-term loan/deposit to a (shadow) bank.

The size of the deposit is too large to attract deposit insurance.

The bank gives collateral to the lender during the loan

At the end of the loan, the bank repays the loan and gets the collateral back.

The advantage of this type of loan is that the lender actually has the collateral during the loan period – so the loan is safe.

The only risk to the lender is that the collateral itself may lose value or default.

Reducing risk through collateral: the REPO market24

Haircuts in REPO25

Because the collaterial may lose value, the lender lends less cash than the value of the collateral.

The difference is called the “haircut”

The word haircut is also used to describe any loss made by the lender.

Example:

The lender/depositor lends €98 of cash to the bank

The bank gives an asset worth €100 to the lender/depositor

One day later:

The lender returns the asset to the bank

The bank repays €100 cash

Haircuts and leverage26

With a haircut of 1%, the bank gets €99 of cash in exchange for €100 of collateral.

The bank can create €100 of additional credit for only €1 of equity (the bank’s own stake).

With a haircut of 10%, the bank gets €90 of cash in exchange for €100 of collateral.

The bank can create €100 of additional credit only by providing €10 of equity. So as the haircut rises, for a given amount of equity, the bank creates less credit.

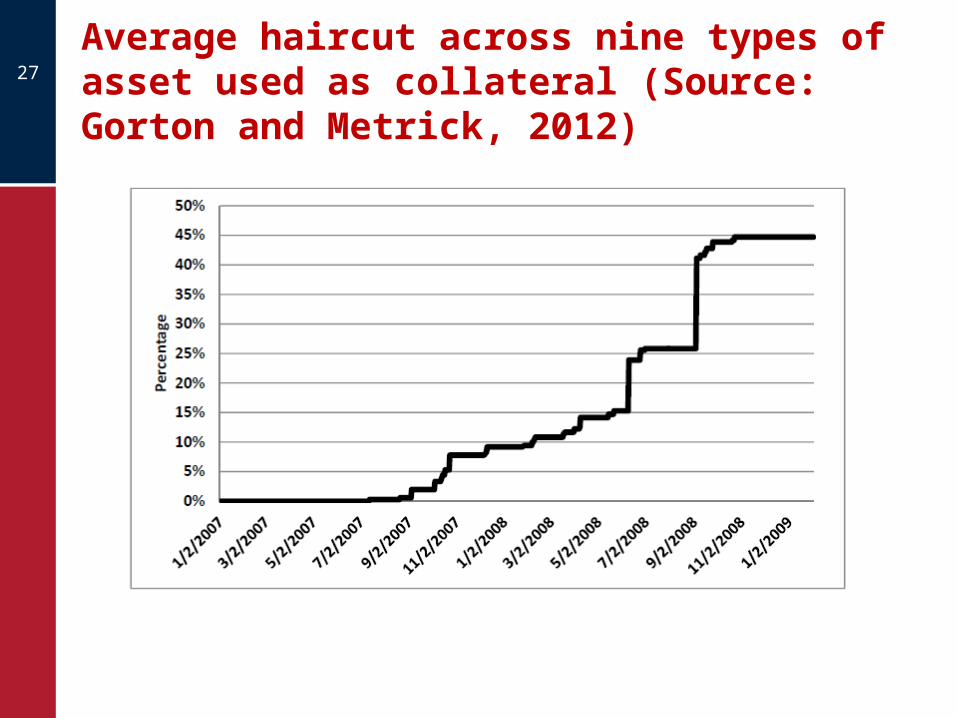

Average haircut across nine types of asset used as collateral (Source: Gorton and Metrick, 2012)

27

Haircuts and pro-cyclicity28

Perceptions of higher risk lead to higher haircuts.

Less credit is created because banks’ equity is fixed in the short run.

The bank must reduce its assets by selling them: but since everyone else is selling too, prices fall.

The falls in price lead perceptions of risk to rise further and so haircuts continue to rise.