Economic Outlook William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of...

36

Economic Outlook William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Multi-Chamber Economic Outlook Luncheon Westmont, IL February 27, 2014

-

Upload

johnny-eakins -

Category

Documents

-

view

214 -

download

0

Transcript of Economic Outlook William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of...

Economic Outlook

William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of

Chicago

Multi-Chamber Economic Outlook LuncheonWestmont, ILFebruary 27, 2014

• The outlook is for the U.S. economy to expand at a

pace around trend in 2013

What I said last year about 2013

• Employment is expected to rise moderately with the

unemployment rate edging lower

• Slackness in the economy will lead to a relatively

contained inflation rate

• Growth in manufacturing output should be around trend in 2013

The “Great Recession” ended in June 2009 and GDP expanded by 2.7% in 2013

-10

-8

-6

-4

-2

0

2

4

6

8

1990 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Real gross domestic productpercent

Quarterly change (saar)

Percent change from a year earlier

A large share of the growth in Real GDPcame from an increase in inventories

2.7

1.6

0.3 0.2

0.9

-0.4

0.3

-1

0

1

2

3

GDP Consumption BusinessFixed

Investment

ResidentialInvestment

Change inInventories

Government Net Exports

Contributions to real GDP growth in 2013percentage points

However, real final sales(GDP less change in private inventories)

growth was far more restrained

-8

-6

-4

-2

0

2

4

6

8

1990 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Real final salespercent

Quarterly change (saar)

Percent change from a year earlier

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Liabilities of the Federal ReserveBi l lions of dollars

Treasury Balance

Currency in Circulation

2007 2008 2009 2010

Deposits of Depository Institutions

2011 2012 2013

The liabilities side of the Fed’s balance sheetshows large amount of excess reserves

$150,000

$175,000

$200,000

$225,000

$250,000

$275,000

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Real Median sales price - existing single family home3-month smoothed (2013 dollars)

Real existing home prices fell by 40%, but have begun to rise

62

64

66

68

70

72

74

76

1965 '70 '75 '80 '85 '90 '95 '00 '05 '10

United States

Homeownership ratepercent

Midwest

The forecast calls for a very gradual recovery in housing

0

500

1,000

1,500

2,000

2,500

1980 '85 '90 '95 '00 '05 '10 '15

Housing startsthousands

Blue Chip Housing StartsForecast (thousands)

Actual Forecast 2013 2014 2015928 1,106 1,311

The stock market has improved since March 2009,and has exceeded its previous peak

50

100

150

200

250

300

350

1990 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Real S&P 500 stock indexIndex: 1990 = 100

-10

-8

-6

-4

-2

0

2

4

6

8

2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Real gross domestic productpercent

Quarterly change (saar)

Percent change from a year earlierQ4-2013

Blue Chip GDP Forecast

Actual Forecast 2013 2014 2015

2.7 2.7 3.0

GDP is forecast to grow somewhatabove trend in 2014 and 2015

The FOMC expects GDP to grow somewhatabove trend over the next three years

-5-4-3-2-10123456

1990 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Real gross domestic productpercent change from a year earlier

FOMC

FOMC Central Tendency (December 2013)

2014 2.8 – 3.22015 3.0 – 3.42016 2.5 – 3.2

Longer run 2.2 – 2.4

98100102104106108110112114116118120122124126

98100102104106108110112114116118120122124126

-8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Business cycle recovery pathindex - business cycle trough = 100

1981-82

2008-09

1974-75

quarters before trough quarters after trough

The path of the current recovery is restrainedcompared with past deep recession recovery cycles

average annualized growth: 5.0%

average annualized growth: 4.6%

average annualized growth: 2.4%

-8

-6

-4

-2

0

2

4

6

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Total employmentpercent

Monthly change (saar)

Percent change from a year earlier

Employment fell by over 8.7 million jobsbetween December 2007 and February 2010,since then it has added over 7.8 million jobs,

with just over 2.2 million jobs added over the past 12 months

3

4

5

6

7

8

9

10

11

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Unemployment ratepercent

After peaking in October 2009,the unemployment rate has fallen by

3.4 percentage points

0

2

4

6

8

10

2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Unemployment ratepercent

Unemployment ratepercent

Q4-2013

Blue Chip Forecast

The unemployment rate is forecast to edge lower

3

4

5

6

7

8

9

10

11

1990 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Unemployment ratepercent

FOMC

The FOMC forecasts that the unemployment ratewill approach the natural rate towards the end of 2016

FOMC Central Tendency (December 2013)

2014 6.3 – 6.62015 5.8 – 6.12016 5.3 – 5.8

Longer run 5.2 – 5.8

-1

0

1

2

3

4

5

6

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Personal consumption expenditure - chain price indexpercent change from a year earlier

Inflation has moderated

0

20

40

60

80

100

120

140

160

1970 '75 '80 '85 '90 '95 '00 '05 '10

Real West Texas Intermediate oil pricedol lars per barrel, 2013 dollars

Adjusted for inflation, current oil prices are belowthe levels that existed thirty years ago

Natural gas prices remain low

0

2

4

6

8

10

12

14

16

1994 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Real natural gas pricedol lars per mmbtu, 2013 dollars

Between 1994 and 2005 the natural gas to oil price ratio averaged 13.4% - it fell to average 3.8% in 2013

0

5

10

15

20

25

30

35

1994 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Natural gas price to oil price ratiopercent (dollars per mmbtu/dollars per barrel West Texas intermediate)

0

1

2

3

4

5

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Personal consumption expenditure - less food and energy -chain price indexpercent change from a year earlier

Removing the volatile food and energy components from the PCE, “core” inflation remains low

-10

-8

-6

-4

-2

0

2

4

6

8

2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Consumer price indexpercent

Quarterly change (saar)

Percent change from a year earlier

Q4-2013

Blue Chip CPI Forecast

Actual Forecast 2013 2014 20151.2 1.9 2.1

Inflation is forecast to rise 1.9 percent in 2014and 2.1 percent in 2015

The FOMC anticipates that PCE inflationwill remain below two percent through 2016

-1

0

1

2

3

4

5

6

1990 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16

Personal consumption expenditure - chain price indexpercent change from a year earlier

FOMC

FOMC Central Tendency (December 2013)

2014 1.4 – 1.62015 1.5 – 2.02016 1.7 – 2.0

Longer run 2.0

0

1

2

3

4

5

1990 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16

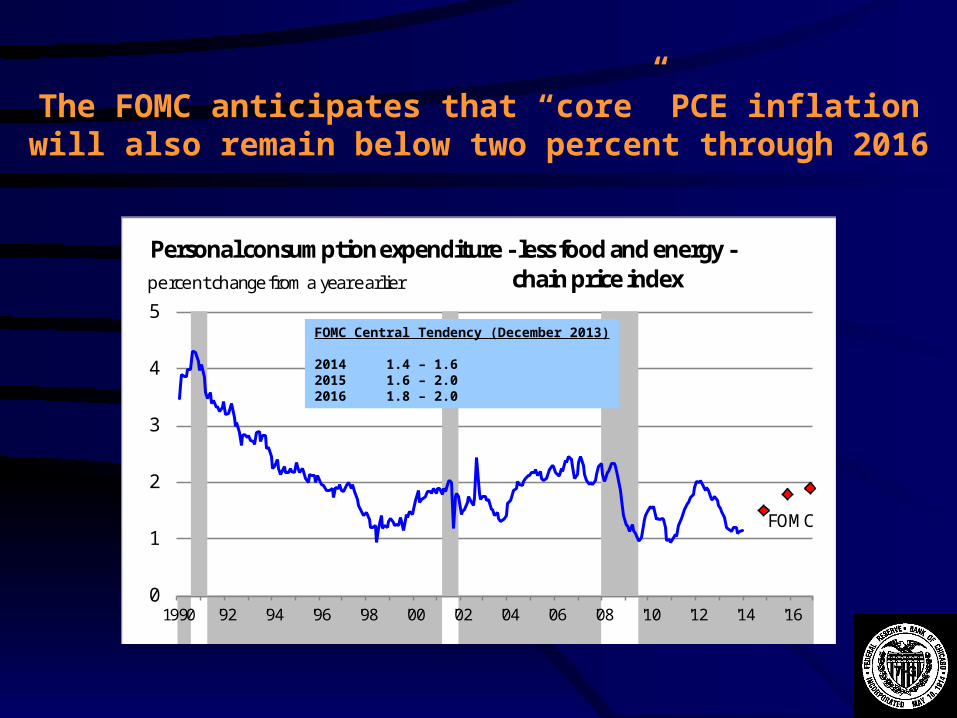

Personal consumption expenditure - less food and energy -chain price indexpercent change from a year earlier

FOMC

The FOMC anticipates that “core” PCE inflationwill also remain below two percent through 2016

FOMC Central Tendency (December 2013)

2014 1.4 – 1.62015 1.6 – 2.02016 1.8 – 2.0

-40

-30

-20

-10

0

10

20

30

40

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Industrial production - manufacturingpercent

Monthly change (saar)

Percent change from a year earlier

Industrial output in manufacturing fell quite sharplyduring the recession, but has risen strongly over

the past fifty-four months, averaging 4.4% and hasrecovered 85.1% of the loss during the recession

While manufacturing jobs have been rising,they have only recovered 27.1% of the jobs

lost during the downturn

-25

-20

-15

-10

-5

0

5

10

15

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Manufacturing employmentpercent

Monthly change (saar)

Percent change from a year earlier

Industrial production is forecast to riseat a pace slightly above trend in 2014 and 2015

-20

-15

-10

-5

0

5

10

2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Total industrial productionpercent

Quarterly change (saar)

Percent change from a year earlier

Q4-2013

Blue Chip IP Forecast

Actual Forecast 2013 2014 20153.6 3.4 3.5

After rising by 13% in 2012, vehicle sales rose 7% in 2013and are forecast to rise around 3% this year and next year

10

11

12

13

14

15

16

17

18

1980 '85 '90 '95 '00 '05 '10

Vehicle salesmil lions of units

Blue Chip Light-VehicleSales Forecast

Actual Forecast 2013 2014 201515.5 16.0 16.4

0

2

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012 2013 2014

Credit spreads between Corporate High Yield and Corporate Aaapercent

Credit spread between Corporate High Yield securitiesand Corporate Aaa securities has remained low

0

1

2

3

4

5

6

7

8

9

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Fed Funds ratepercent

Monetary policy has been very aggressive,keeping the Fed Funds near zero since December 2008

The Federal Funds Rate is anticipated to remainlow over the forecast horizon

0

1

2

3

4

5

6

7

8

9

1990 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Target Federal Funds Ratepercent

FOMC

FOMC Midpoint Value(December 2013)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Assets of the Federal ReserveBi l lions of dollars

Term Auction CreditSecurities Held Outright

Central Bank Swaps

Maiden Lane II & III

Commercial Paper Facility

2007 2008 2009

Term Asset-Backed SecuritiesLoan Facility

AIG Support

Maiden Lane

2010 2011 2012 2013

The asset side of the Fed’s balance sheethas expanded in size and in composition

The money supply (M2) is nearly 4 timesbigger than the monetary base

0

2,000

4,000

6,000

8,000

10,000

12,000

2007 '08 '09 '10 '11 '12 '13 '14

Monetary expansion 2007-current periodbi l lions of dollars

monetary base

M2

50

100

150

200

250

300

350

400

450

1929 '30 '31 '32 '33 '34 '35 '36

Monetary expansion 2007-current periodindex: Jan 2007 = 100

monetary base

M2

CPI

50

100

150

200

250

300

350

400

450

1929 '30 '31 '32 '33 '34 '35 '36

Monetary expansion 1929-1936index: Jan 1929 = 100

monetary base

M2 CPI

The Fed’s expansion of the monetary base has allowed the money supply to continue rising,compared with what took place during the 1930s

• The outlook is for the U.S. economy to expand at a

pace somewhat above trend in 2014

Summary

• Employment is expected to rise moderately with the

unemployment rate edging lower

• Slackness in the economy will lead to a relatively

contained inflation rate

• Growth in manufacturing output should be somewhat above

trend this year

www.chicagofed.org www.federalreserve.gov