Economic Outlook Central Europe - April 2014

8

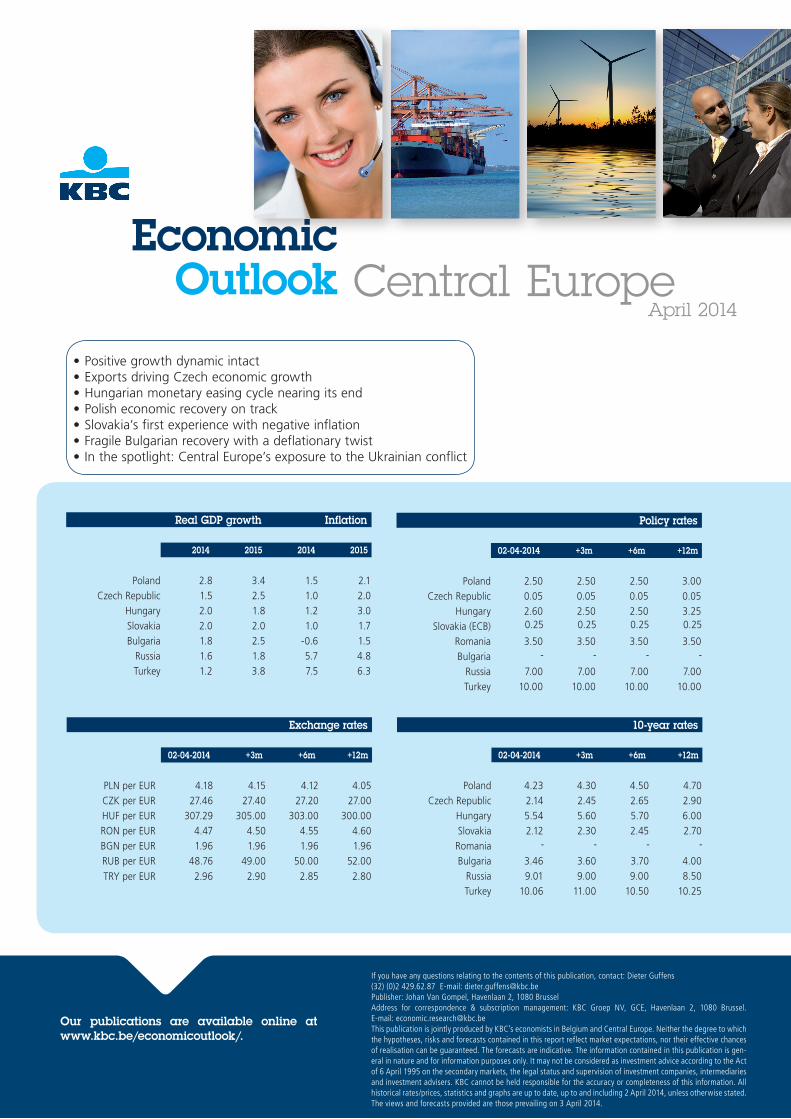

Economic Outlook Our publications are available online at www.kbc.be/economicoutlook/. If you have any questions relating to the contents of this publication, contact: Dieter Guffens (32) (0)2 429.62.87 E-mail: [email protected] Publisher: Johan Van Gompel, Havenlaan 2, 1080 Brussel Address for correspondence & subscription management: KBC Groep NV, GCE, Havenlaan 2, 1080 Brussel. E-mail: [email protected] This publication is jointly produced by KBC’s economists in Belgium and Central Europe. Neither the degree to which the hypotheses, risks and forecasts contained in this report reflect market expectations, nor their effective chances of realisation can be guaranteed. The forecasts are indicative. The information contained in this publication is gen- eral in nature and for information purposes only. It may not be considered as investment advice according to the Act of 6 April 1995 on the secondary markets, the legal status and supervision of investment companies, intermediaries and investment advisers. KBC cannot be held responsible for the accuracy or completeness of this information. All historical rates/prices, statistics and graphs are up to date, up to and including 2 April 2014, unless otherwise stated. The views and forecasts provided are those prevailing on 3 April 2014. Central Europe • Positive growth dynamic intact • Exports driving Czech economic growth • Hungarian monetary easing cycle nearing its end • Polish economic recovery on track • Slovakia’s first experience with negative inflation • Fragile Bulgarian recovery with a deflationary twist • In the spotlight: Central Europe’s exposure to the Ukrainian conflict Real GDP growth Inflation 2014 2015 2014 2015 Poland 2.8 3.4 1.5 2.1 Czech Republic 1.5 2.5 1.0 2.0 Hungary 2.0 1.8 1.2 3.0 Slovakia 2.0 2.0 1.0 1.7 Bulgaria 1.8 2.5 -0.6 1.5 Russia 1.6 1.8 5.7 4.8 Turkey 1.2 3.8 7.5 6.3 Policy rates 02-04-2014 +3m +6m +12m Poland 2.50 2.50 2.50 3.00 Czech Republic 0.05 0.05 0.05 0.05 Hungary 2.60 2.50 2.50 3.25 Slovakia (ECB) 0.25 0.25 0.25 0.25 Romania 3.50 3.50 3.50 3.50 Bulgaria - - - - Russia 7.00 7.00 7.00 7.00 Turkey 10.00 10.00 10.00 10.00 Exchange rates 02-04-2014 +3m +6m +12m PLN per EUR 4.18 4.15 4.12 4.05 CZK per EUR 27.46 27.40 27.20 27.00 HUF per EUR 307.29 305.00 303.00 300.00 RON per EUR 4.47 4.50 4.55 4.60 BGN per EUR 1.96 1.96 1.96 1.96 RUB per EUR 48.76 49.00 50.00 52.00 TRY per EUR 2.96 2.90 2.85 2.80 10-year rates 02-04-2014 +3m +6m +12m Poland 4.23 4.30 4.50 4.70 Czech Republic 2.14 2.45 2.65 2.90 Hungary 5.54 5.60 5.70 6.00 Slovakia 2.12 2.30 2.45 2.70 Romania - - - - Bulgaria 3.46 3.60 3.70 4.00 Russia 9.01 9.00 9.00 8.50 Turkey 10.06 11.00 10.50 10.25 April 2014

-

Upload

kbc-economics -

Category

Documents

-

view

214 -

download

0

Transcript of Economic Outlook Central Europe - April 2014

1

Economic Outlook

Our publications are available online at www.kbc.be/economicoutlook/.

If you have any questions relating to the contents of this publication, contact: Dieter Guffens (32) (0)2 429.62.87 E-mail: [email protected]: Johan Van Gompel, Havenlaan 2, 1080 BrusselAddress for correspondence & subscription management: KBC Groep NV, GCE, Havenlaan 2, 1080 Brussel. E-mail: [email protected] publication is jointly produced by KBC’s economists in Belgium and Central Europe. Neither the degree to which the hypotheses, risks and forecasts contained in this report reflect market expectations, nor their effective chances of realisation can be guaranteed. The forecasts are indicative. The information contained in this publication is gen-eral in nature and for information purposes only. It may not be considered as investment advice according to the Act of 6 April 1995 on the secondary markets, the legal status and supervision of investment companies, intermediaries and investment advisers. KBC cannot be held responsible for the accuracy or completeness of this information. All historical rates/prices, statistics and graphs are up to date, up to and including 2 April 2014, unless otherwise stated. The views and forecasts provided are those prevailing on 3 April 2014.

Central Europe

• Positive growth dynamic intact• Exports driving Czech economic growth• Hungarian monetary easing cycle nearing its end• Polish economic recovery on track• Slovakia’s first experience with negative inflation• Fragile Bulgarian recovery with a deflationary twist• In the spotlight: Central Europe’s exposure to the Ukrainian conflict

Real GDP growth Inflation

2014 2015 2014 2015

Poland 2.8 3.4 1.5 2.1Czech Republic 1.5 2.5 1.0 2.0

Hungary 2.0 1.8 1.2 3.0Slovakia 2.0 2.0 1.0 1.7Bulgaria 1.8 2.5 -0.6 1.5

Russia 1.6 1.8 5.7 4.8Turkey 1.2 3.8 7.5 6.3

Policy rates

02-04-2014 +3m +6m +12m

Poland 2.50 2.50 2.50 3.00Czech Republic 0.05 0.05 0.05 0.05

Hungary 2.60 2.50 2.50 3.25Slovakia (ECB) 0.25 0.25 0.25 0.25

Romania 3.50 3.50 3.50 3.50Bulgaria - - - -

Russia 7.00 7.00 7.00 7.00Turkey 10.00 10.00 10.00 10.00

Exchange rates

02-04-2014 +3m +6m +12m

PLN per EUR 4.18 4.15 4.12 4.05CZK per EUR 27.46 27.40 27.20 27.00HUF per EUR 307.29 305.00 303.00 300.00RON per EUR 4.47 4.50 4.55 4.60BGN per EUR 1.96 1.96 1.96 1.96RUB per EUR 48.76 49.00 50.00 52.00TRY per EUR 2.96 2.90 2.85 2.80

10-year rates

02-04-2014 +3m +6m +12m

Poland 4.23 4.30 4.50 4.70Czech Republic 2.14 2.45 2.65 2.90

Hungary 5.54 5.60 5.70 6.00Slovakia 2.12 2.30 2.45 2.70Romania - - - -

Bulgaria 3.46 3.60 3.70 4.00Russia 9.01 9.00 9.00 8.50Turkey 10.06 11.00 10.50 10.25

April 2014

2

-6

-4

-2

0

2

4

6

8

10

Czech Republic Slovakia Hungary Poland Bulgaria

Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013

Low inflation creates room for monetary manoeuvre (year-on-year, in %)

Growth dynamic intact (annualised, quarter-on-quarter, in %)

-1

0

1

2

3

4

5

6

7

2009 10 11 12 13 14

Czech republic Slovakia Hungary Poland Q3 2012 Q2 2013 Q4 2012 Q3 2013 Q1 2013 Q4 2013

Czech Republic Hungary Slovakia Poland

Economic Outlook Central Europe

General perspective

Positive growth dynamic intact

Cyclical recovery

Economic growth is gaining strength in Central Europe in the wake of a gradual recovery in the euro area. Economic activity was up in the fourth quarter compared to the third quarter in virtually every country in the region, although real GDP growth remains relatively modest in most cases. Real fourth-quarter GDP growth of 1.6% year-on-year in Slovakia and 1.3% in Bulgaria, for instance, is still considerably lower than the pace of expansion prior to the Great Recession. In the Czech Republic, on the other hand, fourth-quarter economic activity rose by no less than 7.9% quarter-on-quarter annualised. The figure ought, however, to be treated with a degree of caution. On the one hand, it is encour-aging that the Czech economy has now been growing for three quarters in a row, indicating a sustainable recovery trend. On the other hand, we ought not to attach too much weight to this one figure. Czech GDP figures are known for their volatility, due primarily to sharp fluctuations in the inventory component. What’s more, a number of new taxes and duties came into effect on 1 January 2014, which is likely to have encouraged consumers to bring forward a certain amount of spending. All the same, the

Czech Republic has now put its longest ever recession – six successive quarters of contraction, beginning in the fourth quarter of 2011 and ending in the first quarter of 2013 – firmly behind it.

Monetary policy is supportive

We expect the positive dynamic to con-tinue this year, underpinned by accom-modating monetary policy. The excep-tionally weak inflationary dynamic leaves scope for this. Regional central banks are following the example of the ECB and holding their policy rates at historically low levels. The Polish policy rate stands at 2.50% and the country’s central bank has stated that interest rates will remain at their present low levels until the end of the third quarter at least. The Hungarian central bank has now lowered its policy rate for 20 months in a row to 2.60% at present. The Czech policy rate has been at 0.05% since November 2012, so the central bank there is now opting for currency interventions. It has pursued a maximum rate of 27 koruna to the euro since last December, and is prepared, if necessary, to sell unlimited amounts of the Czech currency in order to maintain this level.

Storm clouds to the east

Just as the euro area recovery means the region’s western trading partners are finally doing better, there are omi-nous rumbles in the east. The Turkish economy is struggling with its depend-ence on external financing and the cen-tral bank was obliged to raise its policy rate substantially. Meanwhile, the chess game about Ukraine is weighing chiefly on the Russian economy. Most Central European countries, by contrast, are pri-marily embedded in Western-European production chains. Poland, 8% of whose total exports go to Russia and Ukraine together, is therefore one of the most vulnerable economies. This illustrates that trade links are relatively small and that the danger of contagion is therefore rather limited.

Dieter Franceus ([email protected])KBC Group

3

Year-on-year Quarter-on-quarter

-6

-4

-2

0

2

4

6

2008 09 10 11 12 13

quarter-on-quarter year-on-year

Very strong real GDP growth in fourth quarter(in %)

Headline CPI inflation Housing, water, energy, fuel Food Health Other Alc. beverages, tobacco Transport

Low inflation(consumer basket decomposition, in %)

Economic Outlook Central Europe

Czech Republic

Exports driving economic growth

Petr Dufek ([email protected])CSOB Czech Republic

Eventually, the Czech economy grew even faster in the fourth quarter of 2013 than suggested by the initial flash fore-cast. Real GDP grew by 1.8% quarter-on-quarter and by 1.2% year-on-year. Economic growth was driven by exports, investment, and eventually also by house-hold consumption. However, the biggest growth contribution came from invento-ries. Therefore, given the strong effect of inventories and the increase of tobacco excise duties leading to a stocking-up of tobacco products in Q4, we should not overly rejoice at nearly 2% growth in the fourth quarter. It is certainly good that the economy emerged from the recession, as is the fact that consump-tion and investment are no longer falling. Nevertheless, the last quarter was largely exceptional, due to the above-mentioned extraordinary factors.

As far as individual sectors are concerned, particularly the manufacturing industry fared well, followed by construction, which may be seen as a surprise. However we should keep in mind the very support-ive weather conditions. Notwithstanding the latest three consecutive positive growth quarters, real GDP growth in 2013 was only -0.9%. Nevertheless, the Czech economy’s longest recession has ended and the economy has resumed

growing, mainly thanks to export growth, based on the manufacturing industry.

While economic growth has accelerated recently, inflation is not picking up. In February headline inflation was 0.3% year-on-year, owing to a significant reduc-tion in electricity and natural gas prices for households. Prices of seasonal goods such as shoes and clothing went down. Food prices, to which consumers are most sus-ceptible, only fell slightly by 0.1% month-on-month. Thus the Czech Republic is one of the EU countries with the low-est inflation, primarily due to cheaper energy, telecommunication services and mobile phones. There is no reason to be afraid of deflation, however. With the increased prices of food and certain imported goods, inflation is highly unlikely to become negative. The current low infla-tion is no reason for the Czech National Bank to change its current exchange rate regime. Owing to low inflation, the central bank can maintain the lower threshold of CZK 27 per EUR until the middle of 2015, although it originally cited the possibility of leaving the regime in early 2015.

In the beginning of 2014 there are indica-tions that export-oriented industrial firms are raising their production. Exports are clearly driving Czech economic growth

and raising the trade balance surplus. The rising exports reflect the good competi-tive position of domestic firms on the one hand and the increasing demand on the European market on the other. Trade may also show favourable figures in the months to come. We do not expect that the weak koruna will significantly boost the volume of exports soon (aside from the conver-sion of euro invoices into korunas). Czech exporters will primarily benefit from the favourable demand trend in Europe.

Economic growth is also starting to affect the labour market favourably. The number of unemployed fell slightly in February but still exceeds the 600,000 mark. The unemployment rate remained at 6.7% in February but it was nice to see the number of vacancies rise (to 38,300). As a result, the labour market has been stabilising in recent months. However, a return of the labour market to the condition prior to the first recession, when unemployment was below 5%, is nowhere near. A significant reduction of the unemployment rate in the 2014 is indeed unlikely. By late 2014, fixed-term employment contracts, which are increasingly popular among employers, again expire, and seasonal work ends.

-2

-1

0

1

2

3

4

5

11 12 13 14

Food Alc. beverages, tobaccoHousing, water, energy, fuel HealthTransport OtherHeadline CPI inflation

4

Economic Outlook Central Europe

Hungary

Monetary easing cycle nearing its end

Inflation trending lower(year-on-year, in %)

Composition of real GDP growth (year-on-year, in %)

Real GDP growth Construction Agriculture Services Industry

Headline CPI Inflation target Core CPI

David Nemeth ([email protected])K&H Bank ZRT

Real GDP grew by 2.7% year-on-year and by 0.5% quarter-on-quarter in the fourth quarter of 2013. This was the highest growth rate in the past 8 years. Even more surprising was the growth composition. Since 2007 net exports have been the main and almost sole driver of economic growth. In the fourth quarter, however, all GDP compo-nents contributed positively to growth. Household consumption increased by 0.5% year-on-year, government con-sumption by 5.7% year-on-year, gross capital formation by 10.4% year-on-year and net exports contributed 1.2% year-on-year. Although these figures are very impressive, especially if we take into account the poor performance of the economy in the last years, the sustain-ability is questionable. Once we filter all the one-off effects (low base effects, election spending) out of economic growth, we would have seen real GDP growth around 1.5% year-on-year in the fourth quarter. For 2014 we expect real GDP to grow by 2% after which it will slow to 1.8% in 2015.

Industrial production rose by 6.1% year-on-year in January. Vehicle production is still the main growth driver, while elec-tronic device production growth is still weak. Retail sales increased 3.9% year-

on-year in January. Beside food, dura-ble goods sales and fuel sales are also increasing. This suggests that house-holds are starting to spend their higher disposable income, which can stabilise retail sales growth around 3% year-on-year, even without an acceleration in consumption loan growth.

Surprising fall of inflation...

Inflation surprisingly slowed further from 0.8% year-on-year in January to 0.3% year-on-year in February. Market ser-vices prices decreased by 0.6% month-on-month. The limited tradable goods price increase of 0.1% month-on-month suggests that the pass-through of the exchange rate channel is weak. Nevertheless, we believe that there is definitely no deflationary risk in Hungary, as low inflation is partly explained by several one-off effects (such as the public utility cuts in 2013 and 2014). We believe inflation will return to around 3% year-on-year in six to eight quarters.

... allows central bank to further cut policy rate

Against the favourable inflation back-ground, the national bank continued its gradual rate cutting cycle. For the

twentieth consecutive month the central bank lowered its policy rate, this time by an additional 10 basis points to 2.60%. However, we believe the national bank of Hungary is nearing the end of its easing cycle, especially given the recent weakening of the HUF. The market is already pricing in a rate hike on a six months’ horizon.

No political change expected

At the time of publication the April 6 election results were not yet available. The current governing party Fidesz was the clear favourite to win these parlia-mentary elections. We therefore expect a continuation of current macroeco-nomic policy.

0

2

4

6

8

10

2006 07 08 09 10 11 12 13 14

Headline CPI (year-on-year, in %) Core CPI (year-on-year, in %)

Inflation target

-10

-8

-6

-4

-2

0

2

4

6

2006 07 08 09 10 11 12 13

Agriculture Industry Construction Services GDP growth

5

Economic Outlook Central Europe

PolandEconomic recovery on track

Real GDP growth Investments Private consumption Net exports Public consumption Inventory

Solid growth recovery(year-on-year, in %)

Headline CPI Core CPI

Low inflationary pressure(year-on-year, in %)

Jaroslaw Antonik ([email protected])KBC Towarzystwo Fund. Inwest. A.S.

Macroeconomic data published in the first quarter of 2014 indicates that the Polish economic recovery is on track. In the fourth quarter of 2013 real GDP increased 2.7% year-on-year versus 1.9% year-on-year in the third quarter. Economic growth is mainly driven by consumption and net exports. Domestic demand increased to 1.2% year-on-year in the fourth quarter from 0.5% in the third quarter with consumption increas-ing 2.1% year-on-year and investments rising to 1.3% year-on-year from 0.6% in the third quarter.

Pent-up investment demand

The high level of manufacturing producer confidence in March supports our view of a continuation of the positive trend in the coming quarters. Consumption should be driven by an increase in real wages, a more upbeat labour market, a visible improvement in consumer opti-mism and a significant drop of loan ser-vicing costs. The potential for investment growth is sizable, mainly due to supply-side constraints in the past quarters. Entrepreneurs limited their investments when the economy was slowing down. Currently, the improved situation on the domestic market as well as the recovery in the euro area, Poland’s main trading

partner, should translate into a higher willingness to invest. However, the recent political unrest sur-rounding the Ukrainian conflict is a risk factor. A deep Ukrainian recession would adversely impact trade and weigh on entrepreneurs sentiment. However, economic links should not be overesti-mated and we believe the impact on the Polish business cycle will be limited.

Low inflation

The economic recovery takes place in a context of low inflationary pressure. In February CPI inflation increased to 0.7% year-on-year. The central bank now expects a lower inflation path in the coming months with inflation remaining well below the central banks inflation target of 2.5%. The Ukrainian crisis and the Russian restrictions imposed on Polish pork exports can pull down the CPI by around 0.2% in the coming months.

Central bank communication surprised markets

After the latest monetary policy meet-ing, governor Belka declared that inter-est rates should be kept unchanged at the current level (2.5%) at least until the

end of the third quarter. This change in monetary rhetoric surprised the mar-kets, that expected the policy rate to be hiked earlier. In the short term, we believe the zloty’s exchange rate may be rather volatile as a result of the unrest on Poland’s eastern border. In the medium term, however, we believe that the zloty will resume its appreciating trend given solid economic fundamentals and the improvement of the current account balance.

0

1

2

3

4

5

2007 08 09 10 11 12 13 14

Headline CPI Core CPI

-4

-2

0

2

4

6

8

2010 11 12 13

Private Consumption Government Consumption

Investments Net exports

Inventories Real GDP Growth

6

Economic Outlook Central Europe

Slovakia

Slovakia’s first experience with negative inflation

Car production in Slovakia(number of cars)

Inflation turns negative(year-on-year, in %)

Headline CPI Food

Volkswagen Kia Motors Slovakia PSA Peugeot Citroën

-8

-6

-4

-2

0

2

4

6

8

10

12

2006 07 08 09 10 11 12 13 14

Headline CPI Food

Marek Gabris ([email protected])CSOB Slovakia

Car production supports growth

The Slovak economy expanded by 0.9% year-on-year in 2013 after it rose by 1.8% year-on-year during the previous year. Foreign demand continued to be the main engine of growth. Real export growth was 4.5% in 2013. Export growth dynamics even accelerated towards the end of the year, increasing 6.6% year-on-year in the fourth quarter as demand from Slovakia’s trading partners in the euro area strengthened somewhat. Auto production in particular was supportive for growth. The main car manufacturers were able to increase their production despite the already high capacity utilisa-tion rates of production lines. Weak consumption

Household consumption on the other hand decreased by 0.1% year-on-year in 2013. However, since the second quarter of 2013 consumption dynam-ics have improved. Government con-sumption also contributed positively to growth in 2013. This was slightly surprising as the government tried to consolidate public finances further and fulfil its obligation towards the European Commission to keep the budget deficit

below 3% of GDP. The biggest positive surprise came from gross fixed capital formation. Fourth quarter investments increased by 4.0% year-on-year after they declined almost 10% year-on-year in the third quarter. During the whole of 2013 investments declined by 4.3%.

With a real GDP growth of 1.5% year-on-year in the fourth quarter, Slovakia belonged to the better half of the EU economies. According to the Slovak cen-tral bank and the Ministry of Finance, growth is set to accelerate in 2014. We think growth close to 2% is possible although the recent Crimean crisis might weigh on sentiment in Western Europe. Real GDP growth of 1.5% should be achieved without any significant prob-lems. The main driver will continue to be foreign demand with strong growth of auto exports and an increasing share of local sub-contractors resulting from capacity constraints. Moreover, the recent revival of consumer confidence and the stabilization of the unemploy-ment rate should support household consumption. Furthermore, with the low inflation environment continuing in 2014, real wage growth is set to con-tinue. Real wages started growing again in 2013 after they declined in the two previous years.

Falling inflation

In January 2013 headline inflation was 2.5% year-on-year and it has gradually declined throughout the year to reach 0.4% year-on-year in December. This year the downward trend is continuing with inflation reaching 0.0% year-on-year in January and even turned nega-tive in February (-0.1% year-on-year). We do not think negative inflation will persist, although we do expect inflation to be very low during the remainder of the year.

0

200000

400000

600000

800000

1000000

1200000

1993 94 95 96 97 98 99

2000 01 02 03 04 05 06 07 08 09 10 11 12 13

Volkswagen PSA Peugeot Citroën Kia Motors Slovakia

7

Economic Outlook

Bulgaria

Fragile recovery with a deflationary twist

Deflationary environment(year-on-year, in %)

Labour market remains weak (unemployment rate, in %)

Consumer price inflation Producer price inflation

4

6

8

10

12

14

16

18

20

2000 02 04 06 08 10 12 14

Unemployment rate (in %)

Exports lead the way

Prior to the Great Recession of 2008-2009 Bulgaria enjoyed spectacular growth rates. Between 2000 and 2008 real GDP growth averaged 5.8%. The shock of the global economic crisis on the Bulgarian economy was severe. Today, output is still below its pre-crisis level as the recovery is proving to be very slow and fragile. Full year real GDP growth in 2013 was 0.9%, only margin-ally above the real GDP growth rate of 0.8% in 2012. This was disappointing as fiscal policy in 2013 was more support-ive than in previous years. The general government deficit increased from 0.8% of GDP in 2012 to 1.9% of GDP in 2013 with the structural budget deficit widen-ing.

The subdued recovery in 2013 can partly be explained by the fact that last year was marked by a high degree of social and political unrest, which depressed the investment climate. However, as the political environment calmed somewhat towards the end of the year investments already picked up somewhat. Exports remain the main engine of growth, increasing by 8.9% in 2013. As economic growth in Bulgaria’s key trading partners in the euro area is also strengthening,

we expect exports to continue leading the way in 2014. Labour market weakness

The export-led economic recovery will continue to be slow and gradual as domestic demand remains subdued. Household consumption in particular is unlikely to rebound substantially in the short term as the labour market remains in very bad shape. In January the unemployment rate increased further to 13.1%, the highest level since August 2003. Furthermore, over half of the unemployed are long-term unemployed and therefore at risk of becoming struc-turally unemployed. On a positive note, consumer confidence has been improv-ing steadily in recent months, suggesting that some improvement lies ahead.

Deflation deepens

Moreover, households purchasing power actually has increased in the past year due to a combination of positive nomi-nal wage growth and negative inflation. Average monthly gross wage increased by 2.2% year-on-year while headline inflation in December was -0.9% year-on-year. Since then deflation has deep-ened even further. In February headline

inflation was -2.1% year-on-year. Core inflation is also firmly negative (-1.6% year-on-year in February). First of all, deflation is driven by the still significant slack in the economy. Secondly, this dynamic was further exacerbated by some administratively-set price cuts in the energy sector. In the last 12 months the electricity price was cut three times (in March and August 2013 and in January 2014). In February electricity price inflation was -13.5% year-on-year. Thirdly, credit dynamics are very weak. Fourthly, as a consequence of a strong harvests, food price inflation is also negative. In Bulgaria the share of food in the CPI basket is relatively large. We therefore revised downward our full-year inflation forecasts for 2014 and 2015 to -0.6% and 1.5% respectively. We only expect inflation to turn positive again in the last quarter of this year.

-6

-4

-2

0

2

4

6

8

10

12

14

2011 12 13 14

Consumer price inflation Producer price inflation

Central Europe

Dieter Franceus ([email protected])KBC Group

8

In the spotlightCentral Europe’s exposure to the Ukrainian conflict

Economic Outlook Central Europe

Share of Ukraine and Russia in total exports (2012, in %)

Energy imports from Russia (% of total energy imports)

The ongoing crisis in Ukraine and the mounting tensions between the EU and Russia have been at the centre of atten-tion for a few months now. Given their proximity to Ukraine, Central European economies are at the geographical heart of this conflict. Remarkably, market reac-tion so far has been relatively muted. Only at the height of the Crimean con-flict, there was a noticeable reaction in some CEE currencies and bond yields but this movement has been mostly reversed since.

We briefly discuss the two main chan-nels by which an escalation of the Ukrainian conflict could adversely affect Central Europe, namely the trade chan-nel and the energy supply channel. We focus our attention on Poland, the Czech Republic, Slovakia, Hungary and Bulgaria. Germany is also included because of the large trade links with Central European economies in what the IMF recently labelled the German-Central European supply chain.

Limited trade links

The most obvious channel by which Central European economies could be hit is via the direct trade links with Ukraine and Russia. These trade links

should not be overestimated however. Of the five Central European economies we discuss here Poland is the most heav-ily exposed with a combined share of Russia and Ukraine in its total exports of 8.0%, equivalent to 3.7% of GDP. Although this certainly is not negligible, Central European economies direct trade links with Russia and Ukraine are mod-est. This is also the case for Germany with a combined share of only 3.8% in its total exports.

Very high energy dependence

Germany’s high dependence on Russian energy supply has received the most attention (35% for gas, 29% for petro-leum). However, the energy depend-ence of Central European countries is more than twice as high as the German dependence. The energy dependence is mutual, however, as Russian energy exports to the EU account for 38% of Russia’s total exports.

Another aspect is related to the trans-portation of Russian gas. Several supply routes exist between Russia and the EU. One of these routes runs via Ukraine. This route is particularly crucial for Hungary and Bulgaria as for these countries no immediate alternative exists.

If a scenario unfolded where Russian energy to the EU is disrupted Central European economies would be hit severely worse than the rest of the EU. Obviously different possibilities exist here and the impact varies on the energy intensity of the economy, the access to alternative sources and the length of the interruption. If only the share of Russian gas supply transiting via Ukraine is cut off as part of the ongoing conflict, this would pose a problem for Hungary and Bulgaria. Germany, Poland, the Czech Republic and Slovakia have either alter-native suppliers or alternative supply routes from Russia not running through Ukraine. If a scenario unfolded where all Russian energy to the EU is cut off, Central European economies would be hit severely worse than the rest of the EU and be thrown into deep recessions. However, we deem the chance of this risk materializing to be very small as Russia would suffer the most under this scenario. Indeed, oil and gas exports generate about half of its federal budget revenue. After all, even at the height of the cold war, Russia never stopped sup-plying energy to the West.

Russia Ukraïne

Gas, natural and manufactured Petroleum, petroleum products and related materials

Dieter Franceus ([email protected])KBC Group

0

20

40

60

80

100

Germany Poland CzechRepublic

Hungary Slovakia Bulgaria

Gas, natural and manufactured

Petroleum, petroleum products and related materials

0

1

2

3

4

5

6

Germany Poland CzechRepublic Hungary Slovakia Bulgaria

Russia Ukraïne