Transisi Demografi, Bonus Demografi dan the Window of Oppoertunity

28 September 2017

Anton Hendranata

Chief Economist

+6221 80645208, ext. 8867

Dian Ayu Yustina

Economist

+6221 80645208, ext. 8875

Wisnu Wardana

Economist

+6221 80645208, ext. 8873

Economic Outlook 2018 N a v i g a t i n g T h r o u g h G l o b a l Q u a n t i t a t i v e T i g h t e n i n g

2

Rentetan krisis ekonomi dunia & pelonggaran

moneter yang agresif

Economic Crisis QE (USD) 2016 GDP Policy Rate Real IR

US 3Q08 - 4Q09 Nov 08-Oct 14 4.5 tn (24%) 18.5 tn 1.25 -0.45

Japan 2Q - 3Q11 Agt 11-Jul 17 3.5 tn (71%) 4.9 tn -0.10 -0.50

EU 1Q12 - 2Q13 Mar 15-Jul 17 2.1 tn (18%) 11.9 tn 0.0 -1.4

Japan 2Q14 - 1Q15

Russia 3Q15 - 4Q16 1.3 tn 9.0 4.6

China Slowing, 2Q11 11.1 tn 4.45 2.65

Brexit Jun-16 Mar 09-Agt16 0.7 tn (27%) 2.6 tn 0.25 -2.35

3

Wajah Perekonomian Global

4

Perekonomian dunia stagnan

China

US Japan

Euro

area

5

Demografi Menghambat Potensi Pertumbuhan

Ekonomi

Japan

Eropa

China

US

World

Indonesia

6

Proteksi Perdagangan Dunia Meningkat

7

Perdagangan Global Stagnan 10 Tahun

Terakhir

8

Ketidakpastian Tinggi: Ekspektasi > Aktual

Economic Surprise Indices

Source:Bloomberg

CNY

EUR

US

JPN

9

Kenaikan Suku Bunga di Des 2017?

Source:Bloomberg

0

10

20

30

40

50

60

70

80

Fed BoC BoE ECB

% 21-Jul 22-Aug 15-Sep

10

Source: WEO July 2017

Global Growth Forecast

Proyeksi Perekonomian Global 2018

2.6

1.62.1 2.1

2 1.81.9

1.7

1.1 11.3

0.6

6.9 6.7 6.76.4

8

7.1 7.27.7

4.9 4.9 5.1 5.2

2015 2016 2017F 2018F

India

China

ASEAN5

US

Euro Area

Japan

Global Trade Outlook

2015 2016 2017F 2018FWTV* 2.6 2.3 4 3.9

Adv. Econ 4 2.3 3.9 3.5

Emerging Econ 0.3 2.2 4.1 4.6

Commodity Price

Oil 42.8 51.9 52

Non Fuel** -17.5 -1.8 5.4 -1.4

*average growth rates of export and import volumes

**average growth based on exports weights

11

Trump: Konsisten Untuk Tidak Konsisten

Policy

Initial Stand

Post Presidency 1

Post Presidency 2

Current Position

Economic Impact

Health Care

Repeal and cover everybody

“I Like the Mandate”

Not everyone will be covered

Replace it with something

Core PCE Inflation thus Fed Fund Rate

trajectory

Low Interest Rate

Fed is keeping rates artificially low and

creates a false economy

“USD is too strong”

Prefers the Fed to keep rates low

Low interest rates are good

Market “risk-on” sentiment, IDR bond

yields dropped by 7bps on 13 Apr

+ other 32 policies(taxes, min wages, debt,

climate change, immigration, muslim ban, defeating ISIS, etc.)

Source: NBC News

http://www.nbcnews.com/politics/2016-election/full-list-donald-trump-s-rapidly-changing-policy-positions-n547801

12

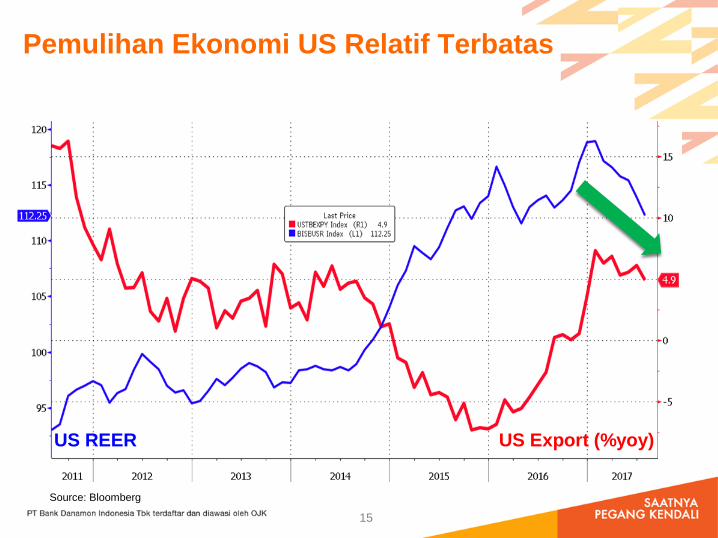

Pemulihan Ekonomi US Relatif Terbatas

Source: Bloomberg

US GDP growth (%yoy)

US Leading Economic Indicator

(%yoy)

13

Pemulihan Ekonomi US Relatif Terbatas

Source: Bloomberg

US Unemployment Rate (%)US Labor Force (%)

14

Pemulihan Ekonomi US Relatif Terbatas

Source: Bloomberg

US Average Hourly Earning (%yoy) US Inflation (%yoy)

15

Pemulihan Ekonomi US Relatif Terbatas

Source: Bloomberg

US Export (%yoy) US REER

16

Pemulihan Ekonomi EU Agak Stagnan

Source: Bloomberg

EU GDP growth (%yoy)

EU Leading Economic Indicator

(%yoy)

17

Pemulihan Ekonomi Jepang Masih Lemah

Source: Bloomberg

Japan GDP growth (%yoy)

Japan Leading Economic Indicator

(%yoy)

18

Pemulihan Ekonomi China Melambat

Source: Bloomberg

China GDP growth (%yoy)

China Leading Economic Indicator

(%yoy)

19

Perekonomian Domestik – Driver Utamanya

Konsumsi RT, Tapi Stagnan

2.8 3.0 2.9 2.8 2.7 2.7 2.7 2.7

2.72.9

1.6 1.4 1.6 1.5 1.5 1.7

6.17 6.03 5.56

5.01 4.88

5.02 5.01 5.01

-2

-1

0

1

2

3

4

5

6

7

2011 2012 2013 2014 2015 2016 1Q17 2Q17

G Net X I C GDP

%yoy

Source: BPS, CEIC, Danamon calculation

20

Perekonomian Domestik – Kontribusi Industri

Manufaktur Menurun

Source: BPS, CEIC, Danamon calculation

1.4 1.2 1.0 1.0 0.9 0.9 0.9 0.8

0.5 0.60.6 0.6 0.5 0.4

0.90.5

1.30.8

0.7 0.70.4 0.5

0.7

0.5

0.8

0.60.6 0.7

0.6 0.5

0.6

0.7

0.4

0.50.4 0.4

0.4 0.4

0.4

0.5

0.3

0.30.3 0.3

0.3 0.3

0.3

0.3

0.2

0.30.3 0.2

0.3 0.3

0.2

0.2

6.17 6.03 5.56

5.01 4.88 5.02 5.01 5.01

0

1

2

3

4

5

6

7

2011 2012 2013 2014 2015 2016 1Q17 2Q17Accommodation, Food&Bev Financial, Insurance

Transportation, Storage Information, Communication

Construction Wholesales, Retail Trade

Agriculture, Forestry, Fisheries Manufacturing

GDP

%yoy

21

Daya Saing Makin Membaik

Peringkat 54 (2007) membaik menjadi 41 (2016)

Source: BI, World Economic Forum – The Global Competitiveness Report 2016 -2017

22

Kemudahan Berusaha (Ease of Doing Business)

Makin Membaik

Source: MOF, World Bank – Doing Business 2017 Report

23

Kepercayaan Rakyat Kepada Pemerintah

Tertinggi di Dunia

Source: BPS, CEIC, Danamon calculation

2007

2016

Source: OECD

24

Reformasi Struktural – Mendorong Daya Beli &

investasi

Source: MOF

25

Belanja Pemerintah Makin Produktif

Source: MOF

26

Indonesia Tempat Investasi Menarik

27

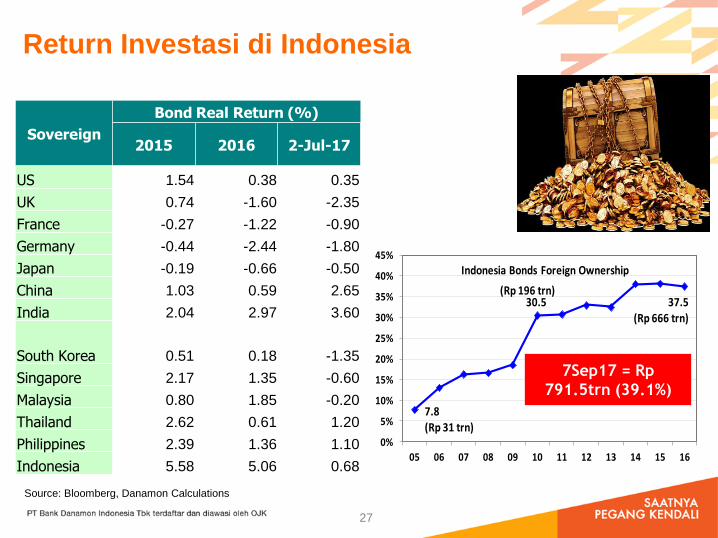

Return Investasi di Indonesia

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

05 06 07 08 09 10 11 12 13 14 15 16

7.8(Rp 31 trn)

37.530.5

Indonesia Bonds Foreign Ownership

(Rp 666 trn)

(Rp 196 trn)

7Sep17 = Rp

791.5trn (39.1%)

Sovereign

Bond Real Return (%)

2015 2016 2-Jul-17

US 1.54 0.38 0.35

UK 0.74 -1.60 -2.35

France -0.27 -1.22 -0.90

Germany -0.44 -2.44 -1.80

Japan -0.19 -0.66 -0.50

China 1.03 0.59 2.65

India 2.04 2.97 3.60

South Korea 0.51 0.18 -1.35

Singapore 2.17 1.35 -0.60

Malaysia 0.80 1.85 -0.20

Thailand 2.62 0.61 1.20

Philippines 2.39 1.36 1.10

Indonesia 5.58 5.06 0.68

Source: Bloomberg, Danamon Calculations

28

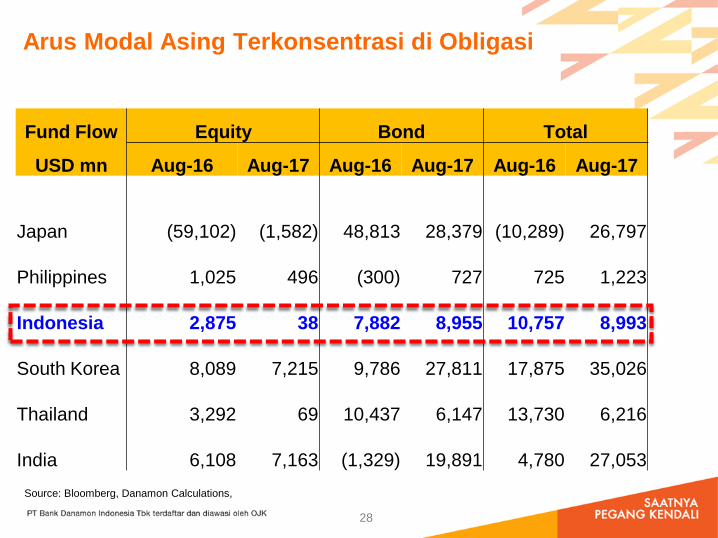

Arus Modal Asing Terkonsentrasi di Obligasi

Fund Flow Equity Bond Total

USD mn Aug-16 Aug-17 Aug-16 Aug-17 Aug-16 Aug-17

Japan

(59,102) (1,582) 48,813 28,379 (10,289) 26,797

Philippines

1,025

496

(300)

727

725

1,223

Indonesia

2,875

38

7,882

8,955 10,757

8,993

South Korea

8,089

7,215

9,786 27,811 17,875 35,026

Thailand

3,292

69 10,437

6,147 13,730

6,216

India

6,108

7,163 (1,329) 19,891

4,780 27,053

Source: Bloomberg, Danamon Calculations,

29

Rupiah Relatif Stabil

30

USD Menguat Sejak 2011, 2017 Melemah

Dollar Index IDR/USD

31

Bonds Yield Turun Signifikan, Waspada

Pembalikan

IDR/USD Bond 10yr

32

Harga Komoditas Ekspor Masih Lemah

85.6

79.5

74.9

65

70

75

80

85

90

4Q16 2017f 2018f

Coal Ric Bay $/MT

10,796

10,047 10,203

9,600

9,800

10,000

10,200

10,400

10,600

10,800

11,000

4Q16 2017f 2018f

Nickel $/MT

68.1

66.0

61.0

56

58

60

62

64

66

68

70

4Q16 2017f 2018f

Iron Ore $/MT

2,933

2,640 2,650

2400

2500

2600

2700

2800

2900

3000

4Q16 2017f 2018f

Palm Oil RM/metric ton

33

Harga Komoditas Impor Naik

51.151.4

52.5

50

51

51

52

52

53

53

4Q16 2017f 2018f

Oil - Brent $/BBl

1,217

1,253

1,268

1,180

1,200

1,220

1,240

1,260

1,280

4Q16 2017f 2018f

Gold $/t oz

525.9

622.8 628.5

450

500

550

600

650

4Q16 2017f 2018f

Steel $/ST

Pelemahan Ekonomi Mungkin Sudah di Titik Terendah

6.2% 6.0%

5.6%

5.0% 4.9%

5.0%

4%

5%

6%

7%

8%

9%

10%

4.5%

5.0%

5.5%

6.0%

6.5%

2011 2012 2013 2014 2015 2016

yoy yoy Real GDP (LHS)

Private Consumption Expenditures

Gross Fixed Capital Formation

• Ekonomi tumbuh terendah pada tahun 2015 di level 4.9%. Kemungkinan pemulihan

berbentuk U (U-shaped recovery).

• Pertumbuhan investasi diharapkan menjadi motor pendorong perekonomian, selain

konsumsi.

• Indikator Net Other Income (FDI + Exports) telah menunjukkan peningkatan (rebound),

yang dapat diikuti oleh pemulihan konsumsi (dampak memiliki lag 2 tahun).

Government’s Forecast Growth Drivers

1.8

2.2

2.6

3.0

0.2

0.6

1.0

1.4

1.8

2004 2006 2008 2010 2012 2014 2016

% bps Real Other Income

PCE Contribution 2Y Lag

34

Mendorong Investasi Bangkit

Poverty and Inequality Infrastructure Priorities Sectors Regional Funds

Rp 292.8 T Rp 409 T Rp 34.8 T Rp 761.1 T

Social Security Program

(increase from 6mn families

to 10 mn families

Health Services

Coverage of 92.4mn people

Education Program (around

20mn scholarships)

Roads (856 km)

Irrigations (781 km)

Electrification Ratio

(95.15%)

Housing

(7,062 unit)

Agriculture

Tourism

Fisheries

Share Allocation Fund

(Rp 87.7 T)

General Allocation Fund

Rp398 T

Specific Allocation Fund

Rp185.9 T

Village Funds Rp 60T

2017 2018

RAPBNP APBN

Private Consumption 5.1 5.1

Government Consumption 4.6 3.8

Investment 5.4 6.3

Exports 4.8 5.1

Imports 3.9 4.5

GDP 5.2 5.4

Component

Government’s Forecast

Focus of Government’s Budget

• Pemulihan ekonomi tahun-tahun ke depan

diharapkan lebih didorong oleh bangkitnya

investasi, namun perlu peranan dari pemerintah,

seperti :

Mempercepat distribusi Bansos, meningkatkan

belanja terutama pada infrastruktur

Paket kebijakan ke-16 yang diumumkan pada

31 Aug terfokus pada kemudahan dan

perampingan birokrasi untuk proses realisasi

investasi. Namun pemulihan investasi akan

bertahap dan butuh waktu, tidak secepat

perkiraan semula.

35

36

Source: BPS, BI, Danamon Calculation

Notes: Trend Aug-17 vs 3Q16

• Sebagian indikator ekonomi menunjukkan perbaikan di 2H17

Indicators Unit 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 Jul-17 Aug-17 Trend

Consumption

Domestic Car Sales yoy -5% 11% -1% 18% 9% -28% 37% 0%

Domestic Motorcycle Sales yoy 3% -10% -8% -16% -16% -27% 76% 5%

Retail Sales Index yoy 11% 16% 11% 10% 4% 7% -3% 5%

Consumer Confidence Index yoy -6% 2% 13% 7% 11% 8% 8% 8%

Real M2 yoy 3% 5% 2% 7% 6% 7% 5% N/A

Fixed Investment

PMI bps 50.6 51.9 50.9 49.0 50.5 49.5 48.6 50.7

Cement Sales yoy 2% 2% -3% -3% 4% -27% 56% 9%

Imported Capital Goods yoy -28% -8% -11% -1% 19% -27% 61% 8%

Government Spending yoy 6% 12% 5% 4% 18% 3% 20% N/A

Trade Volume yoy -6% 9% 6% 3% 9% -14% 12% -20%

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Gross Domestic Product yoy 4.9% 5.2% 5.0% 4.9% 5.0% 5.0% 5.1%

Leading Economic Ind icators - Indonesia

Proyeksi Perekonomian 2018

Ekonomi Global:

• Ketidakpastian pada kebijakan fiskal AS

dapat berdampak pada pertumbuhan

ekonomi yang lebih moderat.

• Fed kemungkinan akan melanjutkan

rencana pengurangan neraca moneternya,

diikuti oleh kebijakan pengetatan moneter

namun dengan skala yang lebih moderat.

• Ekonomi China mungkin akan terus

melambat

Ekonomi Domestik:

• Pertumbuhan ekonomi akan bergantung

pada pemulihan investasi dan belanja

pemerintah.

• Belanja pemerintah dapat meningkat akibat

penyelenggaraan Pilkada di 2017 dan

Pemilu di 2018 dan 2019.

• Inflasi terkendali dan respon suku bunga

minimal.

• Pemulihan ekonomi mungkin berimbas

tekanan pada defisit transaksi berjalan

(CAD) dan nilai tukar Rupiah.

37

Real GDP Growth (%) 2016 2017F 2018F

China 6.70 6.70 6.40

US 1.50 2.10 2.30

EU 1.90 2.00 1.80

Japan 1.00 1.40 1.00

Source: Bloomberg

US - O/N policy rate (% p.a.) 0.75 1.50 2.00

Indonesia

Real GDP Growth (% yoy) 5.02 5.04 5.27

Consumer Price Index (% yoy) 3.02 3.65 3.43

BI 7D RR (% p.a.) 4.75 4.25 4.00

O/N Deposit Facility rate 4.00 3.50 3.25

FX Rate (IDR/USD) – Average 13,309 13,349 13,514

FX Rate (IDR/USD) – Year End 13,417 13,430 13,536

LPS Rate 6.25 5.75 5.50

Loan Growth (% yoy) 7.90 9.71 11.07

Third Party Fund Growth (% yoy) 9.60 8.90 10.89

Tahun

APPENDIX

38

2018

APBNP Outlook RAPBN

I. Economic Infrastructure 390.3 377.8 395.1

through Ministries 157.1 146.9 161.2

1. Ministry of Public Works and Housing (toll roads, bridges ) 101.5 100 104.2

2. Ministry of Transportation (rail tracks, airports, seaports, LRT Jakarta, Palembang) 40.8 33.5 44.2

3. Ministry of Agriculture (irrigations and dams) 2.5 2.5 1.4

4. Ministry of Human Resource 3.1 2.3 2.8

through non Ministries 6 6 3

1. Viability Gap Fund 0.5 0.5 1.2

2. Grant 5.4 5.4 1.4

through transfers to regions and village funds 180.9 178.6 182.8

1. Specific Allocated Funds 32.3 30.6 33.9

2. Village Funds for Infrastructure 24 23.3 24

3. Regional Transfer Funds for Infrastructure 121.2 121.2 120.9

through Financing Scheme 46.2 46.2 48.1

1. Housing facility (i.e. one million house program/interest rate subsidy) 3.1 3.1 2.2

2. Capital Injection to SoE 9.6 9.6 6.1

3. Fund to Public Services Institutions (Hospitals, 32.1 32.1 35.4

II. Social Infrastructure 8.2 8.1 9

1. Ministry of Education and Cultural 5.6 5.6 5.8

2. Ministry of Religion 2.6 2.5 2.9

3. Ministry of Health 0.3

III. Infrastructure Support 2.6 2.4 4.9

1. Ministry of Land (BPN) 0.2 0.2 2.8

2. Ministry of Industry 0.4 0.4 0.2

Total 401.1 388.3 409

2017Items

Pembiayaan Infrastruktur

39

40

Referensi artikel – Anton Hendranata

41

1) Kompas, 21 Nov 13: “Suku Bunga”

2) Kompas, 26 Jun 14: “Rupiah dan Pertumbuhan”

3) Tempo, 14 Nov 14: “Relying on Invesment For Growth”

4) Kompas, 13 Dec 14: “Mewujudkan Pertumbuhan 7 Persen”

5) Kompas, 27 Dec 14: “Ancaman Utang Luar Negeri Swasta”

6) Kompas, 16 Jan 15: “Minyak dan Era Perekonomian Baru”

7) Kompas, 28 Feb 15: “Optimisme APBN Perubahan 2015”

8) Kompas, 13 Mar 15: “Psikologis Rupiah”

9) The Jakarta Post, 31 Mar 15: “Additional Oxygen from the FED Rate Policy”

10) Kompas, 30 May 15: “Mengapa Kita Pesimistis”

11) Kompas, 23 Jul 15: “Dilema Suku Bunga”

12) Kompas, 24 Aug 15: “Ancaman Tiongkok”

13) Tabloid Kontan Mingguan, 14 Sep 15: “Membalikkan Sentimen”

14) Kompas, 15 Sep 15: “Persepsi Negatif dan Kekuatan Komunikasi”

15) Kompas, 26 Nov 15: “Harapan Rupiah Stabil”

Referensi artikel – Anton Hendranata

42

16) Kompas, 2 Mei 16: “Embrio Suku Bunga Rendah”

17) Kompas, 13 Juni 16: ”Melarikan Diri dari S&P”

18) Kompas, 4 Juli 16: ”Pasca Brexit”

19) Kompas, 30 Juli 16: ”Pergantian Kabinet Jilid II”

20) Kompas, 13 Sep 16: ”Untungnya Pengampunan Pajak”

21) Kompas, 7 Okt 16: ”Amnesti Pajak vs Utang Swasta”

22) Kompas, 16 Nov 16: ”Meredam Ketidakpastian”

23) Kompas, 8 Mar 17: ”Proteksionisme Trump”

24) Kompas, 22 Mar 17: “Ketimpangan Perekonomian”

25) Kompas, 31 Mei17: ”Menata Perekonomian Indonesia”

26) Kompas, 27 Jul 17: ”Utang: Tabu vs Solusi”

27) Kompas, 9 Sep 17: ”Antibiotik Daya Beli”

43

Biodata Singkat

Kepala Ekonom Bank Danamon, 2014 - sekarang

Ekonom dan Ekonometrisi Bank Danamon, 2008 - 2014

Dosen Fakultas Ekonomi dan Bisnis, Universitas Indonesia, 1995 – sekarang. Beberapa kali sebagai

dosen terbaik di FEUI

Asisten Pimpinan Magister Perencanaan dan Kebijakan Publik, FEUI, 2004 – 2008

Peneliti di Lembaga Penyelidikan Ekonomi dan Masyarakat, FEUI, 1992 – 2008

Pengajar di diklat Bank Indonesia, Kementerian Keuangan, dan kursus profesi pasar finansial, seperti:

Certified Securities Analyst (CSA) dan Chartered Financial Analyst (CFA).

Penulis di koran: Kompas, Bisnis Indonesia, Kontan, Tempo, Investor Daily, The Jakarta Post dll.

Nara sumber di instansi pemerintah (BI, OJK, LPS, Kemenkeu, Menko Perekonomian), swasta, & TV

The top 3 of FX Forecaster, FocusEconomics Analyst Forecast Awards 2017

The best of FX Research and Market Coverage, Asiamoney FX Poll, 2014, bersama Tim Riset Ekonomi

Bank Danamon

Research - Commended by the Assets Magazine 2014, bersama Tim Riset Ekonomi Bank Danamon di

Indonesia

The Best Economist Forecasters bersama Tim Riset Ekonomi Bank Danamon di Indonesia, yang

dilakukan oleh Bloomberg Markets, 2012 – 2013

Sarjana Statistika dan Magister Ilmu Ekonomi Pertanian IPB, serta Doktor Ilmu Ekonomi FEUI

PT Bank Danamon Indonesia, Tbk.

Terdaftar dan diawasi oleh Otoritas Jasa

Keuangan

44

DISCLAIMER

The information contained in this report has been taken from sources which we deem reliable. However, none of P.T. Bank Danamon Indonesia Tbk. and/or its affiliated companies

and/or their respective employees and/or agents makes any representation or warranty (express or implied) or accepts any responsibility or liability as to, or in relation to, the

accuracy or completeness of the information and opinions contained in this report or as to any information contained in this report or any other such information or opinions

remaining unchanged after the issue thereof. We expressly disclaim any responsibility or liability (express or implied) of P.T. Bank Danamon Indonesia Tbk., its affiliated

companies and their respective employees and agents whatsoever and howsoever arising (including, without limitation for any claims, proceedings, action , suits, losses,

expenses, damages or costs) which may be brought against or suffered by any person as a result of acting in reliance upon the whole or any part of the contents of this report and

neither P.T. Bank Danamon Indonesia Tbk., its affiliated companies or their respective employees or agents accepts liability for any errors, omissions or mis-statements, negligent

or otherwise, in the report and any liability in respect of the report or any inaccuracy therein or omission there from which might otherwise arise is hereby expressly disclaimed. The

information contained in this report is not be taken as any recommendation made by P.T. Bank Danamon Indonesia Tbk. or any other person to enter into any agreement with

regard to any investment mentioned in this document. This report is prepared for general circulation. It does not have regards to the specific person who may receive this report. In

considering any investments you should make your own independent assessment and seek your own professional financial and legal advice.

THANK YOU