Easy Structuring Max

68

Overview of Structured Products Maxime Poulin 2 Introduction A Structured product is a simple concept: it is a bond, which has a coupon and/or a redemption value which, rather than being fixed like a bond, is linked to an underlying price. A good example would be: a bond which does not pay any coupon throughout its life, but at maturity will be redeemed at its par value plus the best between zero and 100% of the performance of the underlying (an equity index for example) measured over the lifetime of the product. This very simple payoff can be split into two very simple financial instruments: A call option on the underlying and a zero coupon bond which will ensure the redemption at par (both instruments have the same notional amount). In this paper we will see what the manufacturing aspects of structured products are: from the pricing to the hedging as well as the distribution channel. We will try to cover the most commonly sold payoffs, their advantages on both sides: clients and sellers as well as the risks and costs they incur to the bank which issues them.

-

Upload

papalazorous -

Category

Documents

-

view

120 -

download

11

Transcript of Easy Structuring Max

Overview of Structured Products

Maxime Poulin 2

Introduction A Structured product is a simple concept: it is a bond, which has a coupon

and/or a redemption value which, rather than being fixed like a bond, is linked

to an underlying price.

A good example would be: a bond which does not pay any coupon throughout

its life, but at maturity will be redeemed at its par value plus the best between

zero and 100% of the performance of the underlying (an equity index for

example) measured over the lifetime of the product.

This very simple payoff can be split into two very simple financial instruments:

A call option on the underlying and a zero coupon bond which will ensure the

redemption at par (both instruments have the same notional amount).

In this paper we will see what the manufacturing aspects of structured

products are: from the pricing to the hedging as well as the distribution

channel. We will try to cover the most commonly sold payoffs, their

advantages on both sides: clients and sellers as well as the risks and costs

they incur to the bank which issues them.

Overview of Structured Products

Maxime Poulin 3

Index

Introduction....................................................................................................2

1. The Market Makers.................................................................................6

1.1. The Structure of the issuers (banks)..................................................6

1.2. The Profit and Loss Scheme .............................................................7

2. The Clients and the Intermediaries ......................................................9

3. Structured Products ............................................................................11

3.1. Definition..........................................................................................11

3.2. Building a Structured product ..........................................................11

3.3. Structured Products type .................................................................13

4. Derivatives used in Structured Products...........................................16

4.1. Vanilla Options ................................................................................16

4.2. Barrier Options ................................................................................18

4.3. Merging Options ..............................................................................20

5. Black-Scholes Model ...........................................................................22

5.1. Assumptions of the Black & Scholes model.....................................22

5.2. Stochastic Differential Equations (SDEs).........................................22

5.3. Lognormal returns for asset prices ..................................................23

5.4. The Black & Scholes formula...........................................................23

5.5. The Black & Scholes formulas for options .......................................23

5.6. Call – Put Parity...............................................................................24

6. The Forwards .......................................................................................26

7. The Correlation ....................................................................................27

7.1. Definition..........................................................................................27

7.2. Correlation term structure and skew................................................27

8. Volatility and Variance.........................................................................29

8.1. Definition..........................................................................................29

8.2. Implied Volatility...............................................................................29

8.3. Volatility term Structure....................................................................30

Overview of Structured Products

Maxime Poulin 4

8.4. Volatility Skew / Smile......................................................................30

9. Quanto and Compo Options ...............................................................33

10. Sensitivities of Exotic Options ...........................................................36

10.1. Time Value Relationship..................................................................36

10.2. Estimating sensitivities: Pragmatic approach...................................37

11. Models used on Trading floors (Commerzbank)...............................39

11.1. Calibration process of a model ........................................................40

11.2. How do Option pricing models operate?..........................................41

11.3. Black Vanilla Model .........................................................................46

11.4. Black Diffusion Model ......................................................................46

11.5. Local Volatility Model .......................................................................47

11.6. Stochastic Volatility Model ...............................................................47

11.6.1. The Heston Model.................................................................49

11.6.2. The Hagan Model .................................................................50

11.6.3. The Scott-Chesney Model ....................................................50

12. The risks related to structured products ...........................................51

12.1. Delta Risk ........................................................................................52

12.2. Vega Risk ........................................................................................52

12.3. Correlation Risk ...............................................................................53

12.4. Second order Risks .........................................................................53

13. Example of exotic derivative: Cliquets ..............................................55

13.1. Convexity (or Volga) ........................................................................55

13.2. Cliquets............................................................................................58

13.2.1. Classic Cliquet ......................................................................58

13.2.2. Ratchet Cliquet .....................................................................60

13.2.3. Reverse Cliquet ....................................................................62

13.2.4. Napoleon Cliquet ..................................................................65

Conclusion ...................................................................................................69

Bibliography.................................................................................................70

Overview of Structured Products

Maxime Poulin 5

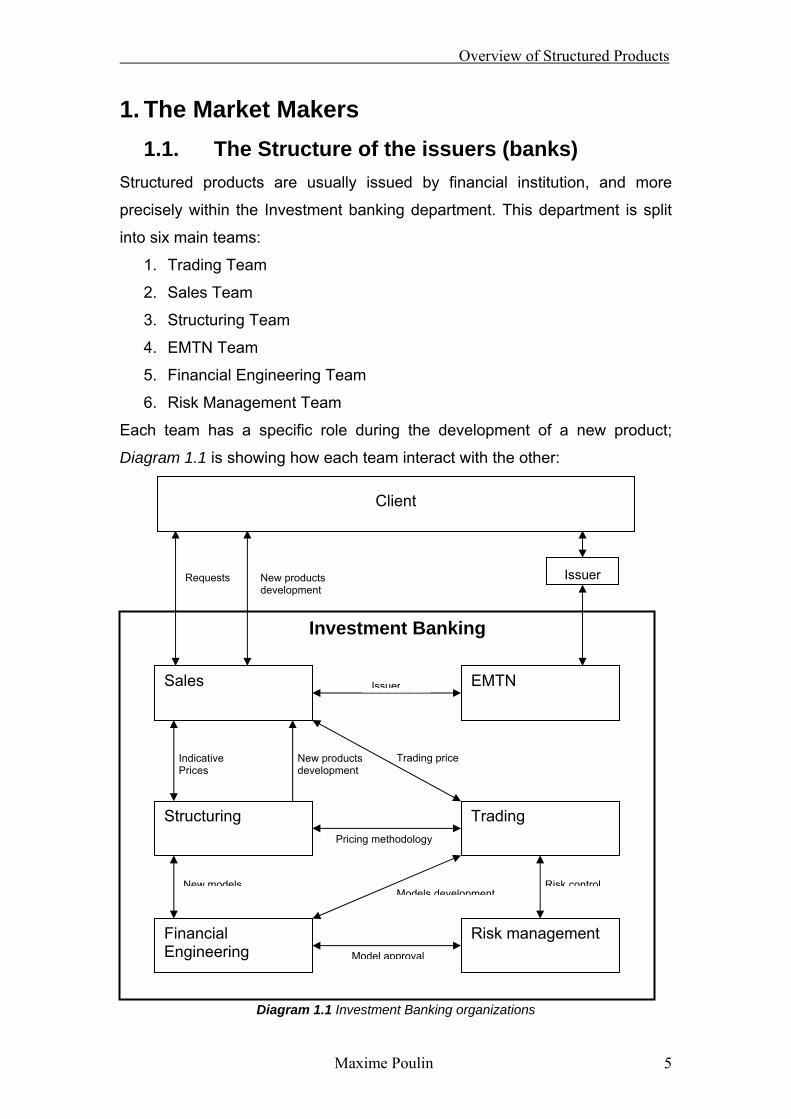

1. The Market Makers

1.1. The Structure of the issuers (banks) Structured products are usually issued by financial institution, and more

precisely within the Investment banking department. This department is split

into six main teams:

1. Trading Team

2. Sales Team

3. Structuring Team

4. EMTN Team

5. Financial Engineering Team

6. Risk Management Team

Each team has a specific role during the development of a new product;

Diagram 1.1 is showing how each team interact with the other:

Diagram 1.1 Investment Banking organizations

Pricing methodology

Model approval

Trading Structuring

Sales

Client

EMTN

Requests New products development

Indicative Prices

Trading price New products development

Issuer

Risk management

Risk control

Financial Engineering

New modelsModels development

Investment Banking

Issuer

Overview of Structured Products

Maxime Poulin 6

Each team (Trading, Sales, Structuring, etc) is also segmented into different

desks, depending on the asset class: Equity, Commodities, Fixed Income,

Currencies and Credit.

Trading will take care of the hedging and the pricing, while the sales team will

try to sell products at a fair price for the bank.

1.2. The Profit and Loss Scheme

As in every corporate group, the aim is to make profit, and mainly maximizing

those while taking as little risk as possible. Financial institutions like banks,

which offer financial products to their clients, have to bear some risk on these.

This risk taken on by the bank has to be hedged by the traders using tools

and techniques we will see further on.

But in this case, what is the value added for the bank, where does it make a

profit? In fact it works the same way than for most companies, the bank

determine a fair price for the financial product and sells it at a higher price.

This fair price is calculated using mathematical models which we will more in

detail in the “Pricing” section; represent the cost of fully hedging the product,

this assuming the pricing model is perfect.

If the Traders job is to hedge position taken by the bank when it sells financial

products, what explain the bonuses they receive each year? As we said

earlier the banks makes its profit by selling a financial product which has a

hedging cost of USD 98 at a higher price: USD 100 for example, incurring a

profit of USD 2 for the bank for each product sold with these characteristics.

But this assumes each product is fully hedged, although in facts, traders don’t

usually fully hedge their books. Meaning they keep some exposure to the

market in their books that they decide not to hedge. This is driven by the risk

aversion and the market views of each trader. By keeping a market exposure,

the traders increase the risk of their books which might lead to losses if the

Overview of Structured Products

Maxime Poulin 7

traders’ views were wrong, but on the other end might also lead to additional

earnings if they are right.

As a conclusion we can see that the total Profit and Loss of the bank will be

the sum of both the sales margin: selling at a higher price than the actual

hedging cost, and the traders profit or loss realised by not fully hedging his

position.

∑∑==

+=J

j

jTrader

I

i

iSalesLP

11PositionsMargin&

Where: “i” is the number of product sold and “j” the number of positions held

by the bank.

Overview of Structured Products

Maxime Poulin 8

2. The Clients and the Intermediaries

Structured products are sold to a wide range of clients: although very often

overpriced, structured products are very powerful tools in order to improve the

performance of a portfolio. Clients range from institutional investor to retail

investor, they are not interested in the same products: Institutional investor

usually only buy the option part of a structured product whereas retails

investor tend to go for bundles with both the option and the bond part.

The front office division (Sales Teams) cannot distribute directly these product

to all customers, moreover, it cannot tailor a product for a single retail investor

(size would be too small). On top of that the regulators do not allow them to

talk directly to retail customers due to their lack of awareness. The retail

market is maintained by companies such as: insurance companies, fund

management companies, brokers, banks (wealth management department),

financial advisors, family offices. Those companies have a very large

distribution network and an administration which allows them to speak directly

to the public.

These intermediaries are making profit by charging the client for their services

as well as receiving a commission from the product manufacturer. In this

case, the manufacturer will take this commission into account into its hedging

price.

Some intermediaries will only buy the option part of the structured product and

then manufacture the bond feature of the product themselves.

As a conclusion we can say that there are different types of product which will

be suitable for different investors:

• Fully manufactured products for small retail investors, brokers, or other

intermediary. This enables the product manufacturer to sell its product

to the general public without having to actually deal with them. These

customers / intermediaries are referred to as “Private Banks”: high

powered investors, asset managers, brokers who do not have the

capacity to manufacture structured products, but who are very lightly

regulated in regards to who they are marketing products to.

Overview of Structured Products

Maxime Poulin 9

• “Raw” Structured products: the option part of a structured product sold

to institutional investor. Very highly regulated and competitive

business.

There is a broad range of products available to each type of investors, but

most of them can be classified in to these three classes.

• Simple market access products

• Yield enhancement products

• Capital protected products

Overview of Structured Products

Maxime Poulin 10

3. Structured Products

3.1. Definition

A structured product can take the form of many different payoffs. But in

essence it is a bond (or certificate) which pays instead of the guaranteed

coupon offered by the bond, a payoff linked to the performance (either

positive or negative) of an underlying (which can be of any asset class:

commodity, equity, FX, interest rate).

A good example would be: a bond which does not pay any coupon throughout

its life, but at maturity will be redeemed at its par value plus a coupon of X% if

the performance of the underlying (an equity index for example) measured

over the lifetime of the product is positive.

This very simple payoff can be split into two very simple financial instruments:

A digitale option on the underlying and a zero coupon bond which will ensure

the redemption at par (both instruments have the same notional amount).

3.2. Building a Structured product

A structured product is composed of several pieces: the seller of such a

product will try to replicate each individual piece and sell them in a package.

In order to do so, the issuer will create the product through legal

documentation which will state exactly the terms and conditions of the

product: the exact obligation that the issuer has in regards to the investors.

The buyer will not in general have any physical proof of ownership of the

bond, but the exchange will go trough electronic settlement systems such as

Euroclear or Clearstream, and they will keep track of all these transactions.

Such structured products can take different legal form:

Overview of Structured Products

Maxime Poulin 11

• It can be issued as an investment fund: in this case, a fund is incorporated

and buys all parts of the structured product. The investor who bought

shares of this fund gain an identical exposure to the market than if he had

bought the pieces independently. This kind of legal form is mainly used for

regulation purpose. For example in the UK, the range products that can be

offered to the public are very restricted, but it is legal to sell investment

funds to the same public.

• The most common legal form is the Medium Term Note (MTN, and more

often in Europe: Euro MTN: EMTN). This is usually used by the issuer to

finance its business activities. For this legal form, the traders enter into a

swap with the bond issuer in which they will give an amount to the bond

issuer and receive a floating coupon generally equal to Libor plus or minus

Spread. This Spread is determined by the market’s required rate of return

to take the risk of that specific bond issuer.

• The second most common form is the certificate, there is not much

difference between the MTN (or EMTN) and the certificate. Regarding the

pricing: it has no impact on the pricing of the derivative, and the impact on

the bond part is only due to the funding given by the bond issuer.

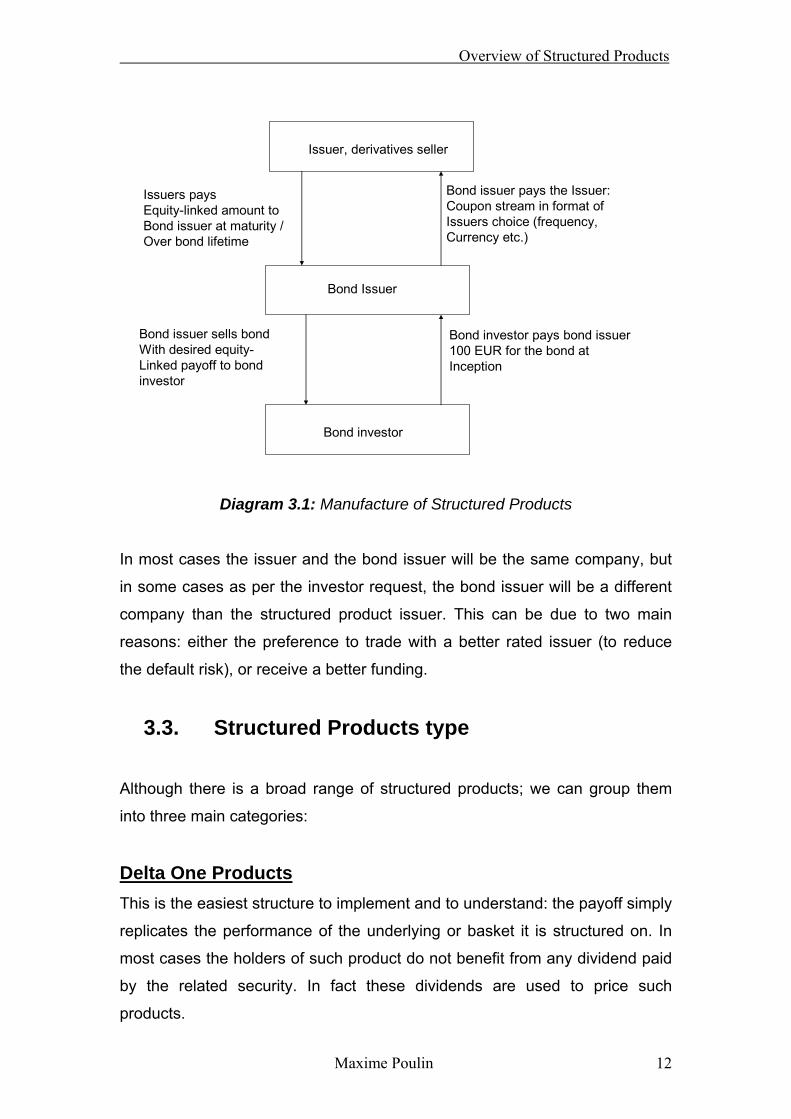

In order to take advantage of this wide range of legal form and the ability to

structure a product with a different bond issuer than the structured product

originator, most structured products are manufactured in the following way:

Overview of Structured Products

Maxime Poulin 12

Issuer, derivatives seller

Bond Issuer

Bond investor

Issuers pays Equity-linked amount to Bond issuer at maturity / Over bond lifetime

Bond issuer pays the Issuer:Coupon stream in format of Issuers choice (frequency,Currency etc.)

Bond investor pays bond issuer100 EUR for the bond atInception

Bond issuer sells bondWith desired equity-Linked payoff to bondinvestor

Diagram 3.1: Manufacture of Structured Products

In most cases the issuer and the bond issuer will be the same company, but

in some cases as per the investor request, the bond issuer will be a different

company than the structured product issuer. This can be due to two main

reasons: either the preference to trade with a better rated issuer (to reduce

the default risk), or receive a better funding.

3.3. Structured Products type

Although there is a broad range of structured products; we can group them

into three main categories:

Delta One Products This is the easiest structure to implement and to understand: the payoff simply

replicates the performance of the underlying or basket it is structured on. In

most cases the holders of such product do not benefit from any dividend paid

by the related security. In fact these dividends are used to price such

products.

Overview of Structured Products

Maxime Poulin 13

This kind of structure is attractive for investors who do not have the right or

ability to invest in certain markets or underlying. This structure, by wrapping

the securities they want to invest in, in another legal form, allows them to

invest in a more efficient way: ability to invest into indices with much smaller

size or infrastructure than it would require if the investor wanted to replicate

himself an index.

These do not offer any kind of coupon but an exposure to a security or a

basket of securities; this means that the redemption of the product will be

completely dependent on the level of the underlying (linear relation between

the two).

Yield enhancement Products Plain vanilla bonds provide a coupon dependent on the issuers credit risk, the

coupon is a premium agains the risk that the investor bears, this risk being

that the issuer might not be able to repay the principal.

To enhance this coupon, it is possible to have structured products whose

principal repayment will be indexed to an equity price. For example, for every

1% drop in the equity price, the principal repayment would be decreased by

1%, this being observed at maturity. And as a gain, the investor would receive

an increased coupon compared to the plain vanilla bond.

“Manufacturing” such a product is done by: buying (“Long”) a plain vanilla

bond which pays a fixed (or floating) coupon, and selling (“Short”) a vanilla put

option at the money on the equity. The premium received by selling the put

will be added to the coupon received from the bond which will give a

structured product that pays a higher coupon.

Yield Enhancement product regroups a wide range of payoffs, but in essence,

it involves the investor having a downside risk on equities in exchange for a

higher coupon. The most common ones are: Premium, bonus, discount (bond

or certificate), reverse convertible bond, autocallable, and sidestep note

among others.

Overview of Structured Products

Maxime Poulin 14

These are widely used by investors who have a bullish view on the market,

but still think that the performance of the underlying will be very small. This is

why they are willing to swap this potential upside performance against a

coupon while keeping all or part of the downside risk.

Capital Protected Products These are referred to as products which do not have an additional risk than

the credit risk brought by the issuer of the bond. It will be a bond with a

participation to the upside performance of an underlying (one or more).

These are used by very risk-averse investors.

Overview of Structured Products

Maxime Poulin 15

4. Derivatives used in Structured Products

“Derivatives” is the term used in order to describe investment products which

derive (which explained why they are called “Derivatives”) from an underlying

asset. The payoff, meaning the relation between the Derivative and the

Underlying is almost never linear, a variation of one dollar in the underlying’s

price will not necessarily impact the derivatives price by one dollar.

This brings us to realise that there is convexity in the price of the derivative

which depend on the volatility of the underlying (can be proven with Jensen’s

inequality). We can conclude with this information that the volatility is

fundamental when looking at such products.

4.1. Vanilla Options

These are the well known Calls and Puts. They are referred to as vanilla

options due to their “simple” payoffs compared to other more exotics options,

which have more refined payoffs and are much more complex to price as well.

A Call is a buying option: it gives the right to the investor who bought the

option at a premium P1 (but not the obligation) to buy the underlying at a fixed

price which is the strike price.

A Put is a selling option: it gives the right to the investor who bought the

option at a premium P2 but not the obligation to sell the underlying at a fixed

price which is the strike price.

The price/value of such an option is driven by: the underlying’s spot price, its

volatility, its drift rate, the strike of the option, its maturity and the market

interest rates. This gives us the following formula, where P is the price of the

option.

)),,(;;,()( µσtSrTKVtV =

In this formula, the semicolons are making the distinction between different

parameters: the first parameters are linked to the option (K, T), the second

Overview of Structured Products

Maxime Poulin 16

one is a market parameter (r), and the last one is linked to the underlying (S

(t, σ, µ)). The Strike and the maturity can be modified to suit the investor’s

requirement. The other parameters are market/underlying dependent and

cannot be modified but are dictated by the market itself.

The parameters in the formula are define as follow:

S: the spot of the asset

σ: the volatility of the asset

µ: the drift of the asset

K: the strike of the option

T: the maturity of the option

r: interest rates

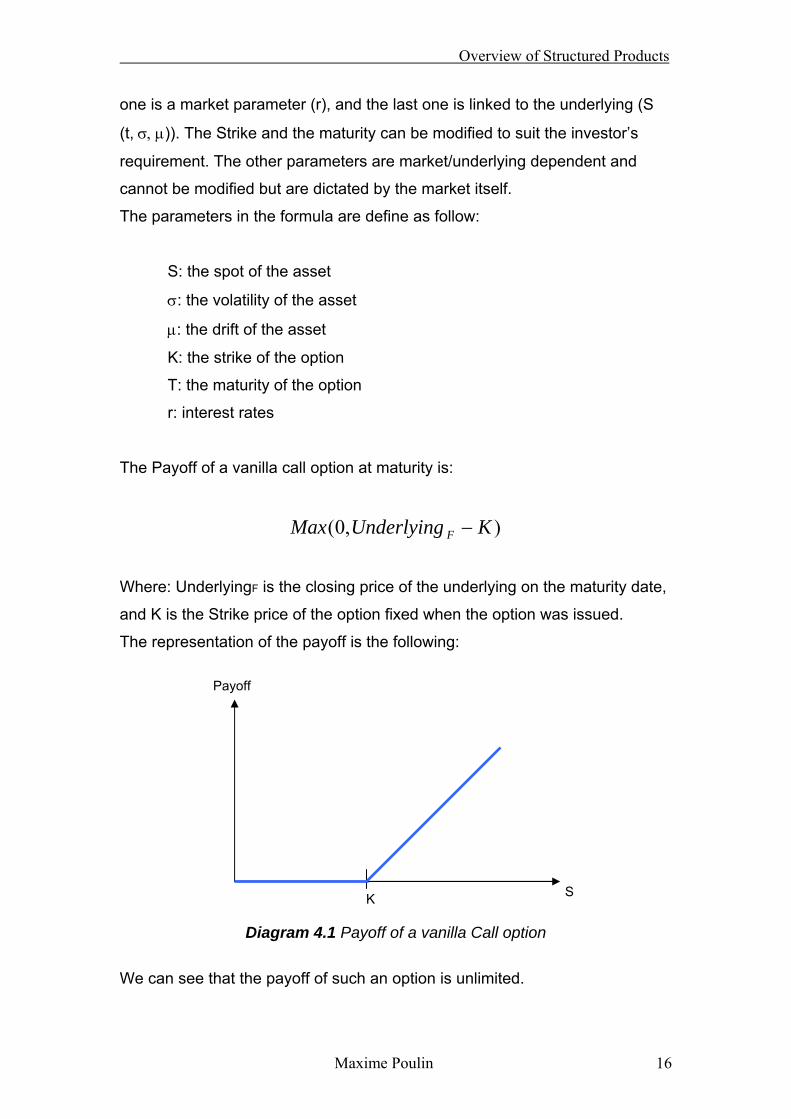

The Payoff of a vanilla call option at maturity is:

),0( KUnderlyingMax F −

Where: UnderlyingF is the closing price of the underlying on the maturity date,

and K is the Strike price of the option fixed when the option was issued.

The representation of the payoff is the following:

Diagram 4.1 Payoff of a vanilla Call option

We can see that the payoff of such an option is unlimited.

Payoff

K S

Overview of Structured Products

Maxime Poulin 17

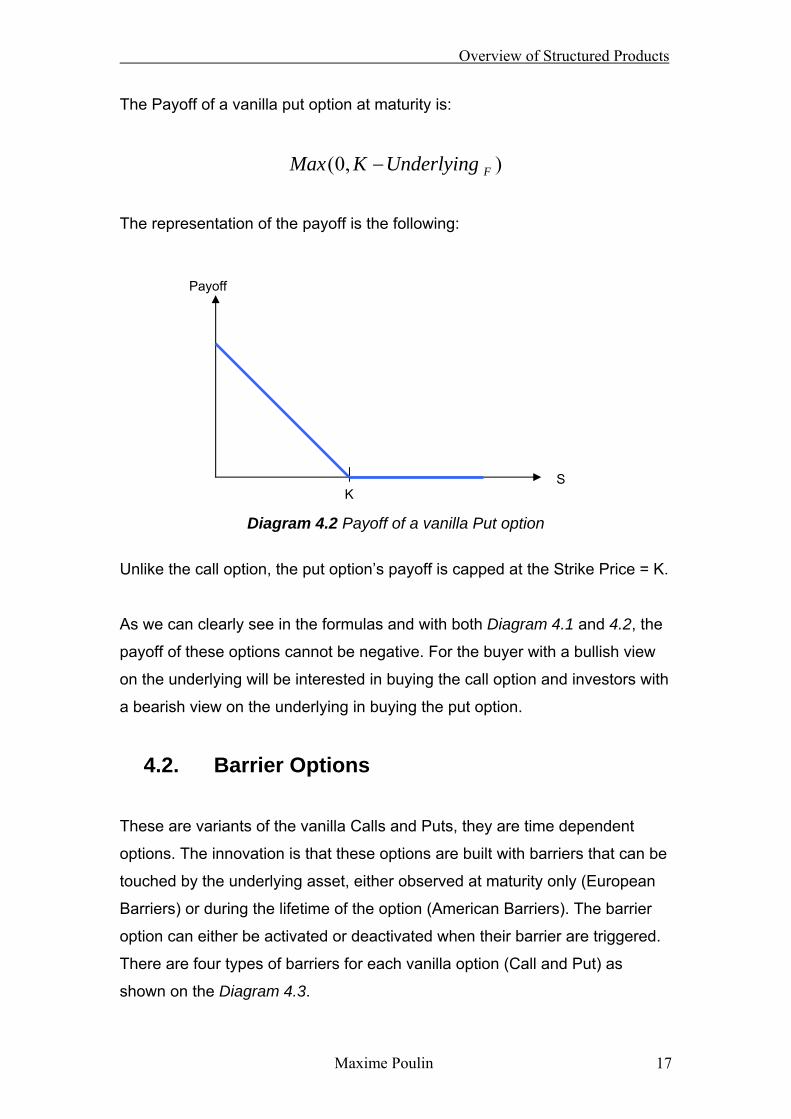

The Payoff of a vanilla put option at maturity is:

),0( FUnderlyingKMax −

The representation of the payoff is the following:

Diagram 4.2 Payoff of a vanilla Put option

Unlike the call option, the put option’s payoff is capped at the Strike Price = K.

As we can clearly see in the formulas and with both Diagram 4.1 and 4.2, the

payoff of these options cannot be negative. For the buyer with a bullish view

on the underlying will be interested in buying the call option and investors with

a bearish view on the underlying in buying the put option.

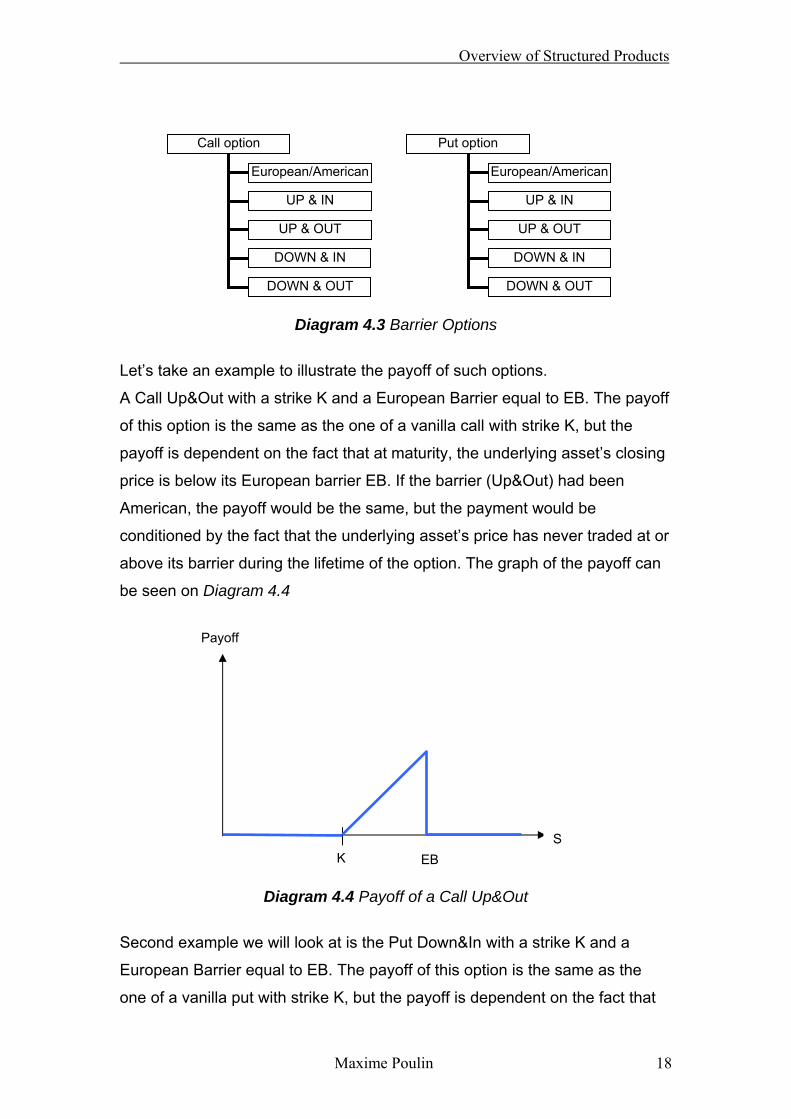

4.2. Barrier Options

These are variants of the vanilla Calls and Puts, they are time dependent

options. The innovation is that these options are built with barriers that can be

touched by the underlying asset, either observed at maturity only (European

Barriers) or during the lifetime of the option (American Barriers). The barrier

option can either be activated or deactivated when their barrier are triggered.

There are four types of barriers for each vanilla option (Call and Put) as

shown on the Diagram 4.3.

K S

Payoff

Overview of Structured Products

Maxime Poulin 18

Diagram 4.3 Barrier Options

Let’s take an example to illustrate the payoff of such options.

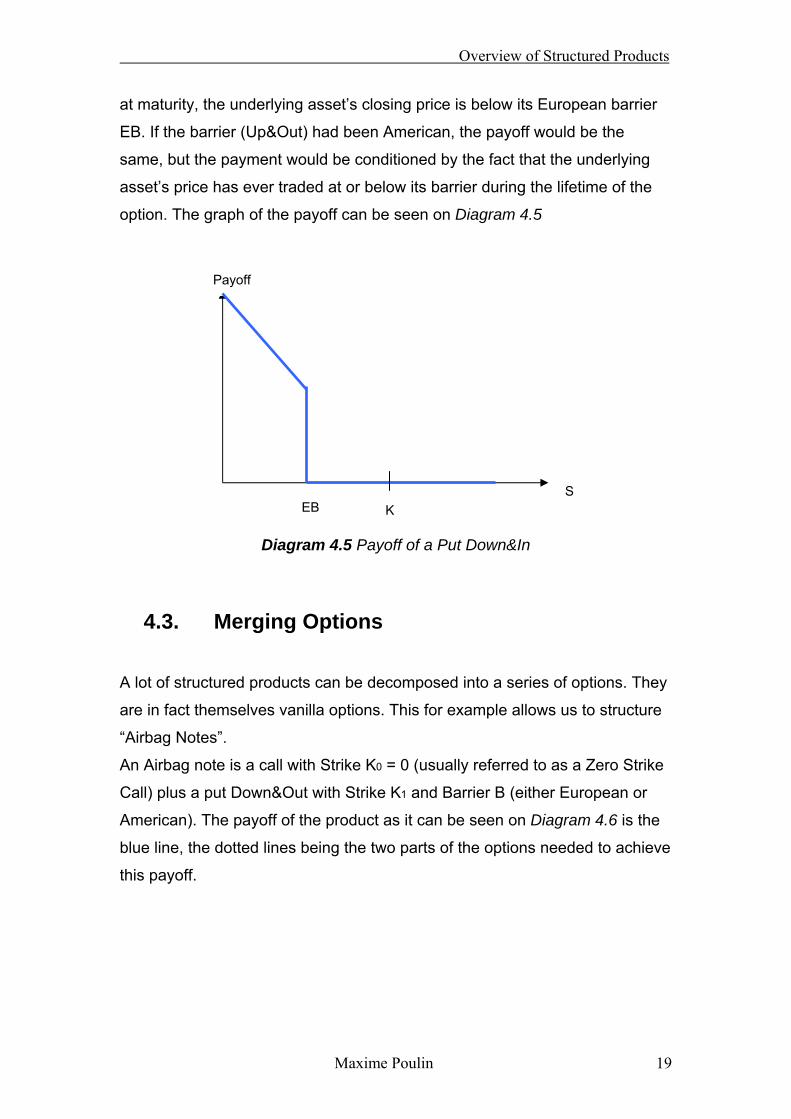

A Call Up&Out with a strike K and a European Barrier equal to EB. The payoff

of this option is the same as the one of a vanilla call with strike K, but the

payoff is dependent on the fact that at maturity, the underlying asset’s closing

price is below its European barrier EB. If the barrier (Up&Out) had been

American, the payoff would be the same, but the payment would be

conditioned by the fact that the underlying asset’s price has never traded at or

above its barrier during the lifetime of the option. The graph of the payoff can

be seen on Diagram 4.4

Diagram 4.4 Payoff of a Call Up&Out

Second example we will look at is the Put Down&In with a strike K and a

European Barrier equal to EB. The payoff of this option is the same as the

one of a vanilla put with strike K, but the payoff is dependent on the fact that

Put option

European/American

UP & IN

UP & OUT

DOWN & IN

DOWN & OUT

Call option

European/American

UP & IN

UP & OUT

DOWN & IN

DOWN & OUT

Payoff

S K EB

Overview of Structured Products

Maxime Poulin 19

at maturity, the underlying asset’s closing price is below its European barrier

EB. If the barrier (Up&Out) had been American, the payoff would be the

same, but the payment would be conditioned by the fact that the underlying

asset’s price has ever traded at or below its barrier during the lifetime of the

option. The graph of the payoff can be seen on Diagram 4.5

Diagram 4.5 Payoff of a Put Down&In

4.3. Merging Options

A lot of structured products can be decomposed into a series of options. They

are in fact themselves vanilla options. This for example allows us to structure

“Airbag Notes”.

An Airbag note is a call with Strike K0 = 0 (usually referred to as a Zero Strike

Call) plus a put Down&Out with Strike K1 and Barrier B (either European or

American). The payoff of the product as it can be seen on Diagram 4.6 is the

blue line, the dotted lines being the two parts of the options needed to achieve

this payoff.

Payoff

S K EB

Overview of Structured Products

Maxime Poulin 20

Diagram 4.5 Payoff of an Airbag Note Many other payoffs can be manufactured from combining different vanilla options.

K1 K0 S

Payoff

B

Overview of Structured Products

Maxime Poulin 21

5. Black-Scholes Model

This model is the starting point of most other models in finance. It is also the

model the most widely used for pricing structured product, and is the

foundation of more complex models such as the Local Volatility Model (LVM).

5.1. Assumptions of the Black & Scholes model

The key assumptions made for the Black & Scholes to be correct are:

• The returns of the underlying follow a lognormal distribution with constant

drift µ and constant volatility σ

• It is possible to short (sell an underlying) in the market.

• There are no arbitrage opportunities in the market.

• Ability to trade the stock continuously.

• There are no transaction costs or taxes.

• All securities are perfectly divisible (e.g. it is possible to buy 1/10th of a

share).

• It is possible to borrow and lend cash at a constant risk-free interest rate.

5.2. Stochastic Differential Equations (SDEs)

These equations are separated in two parts: the Brownian element (which is

the stochastic element) and the Newtonian element (the deterministic term).

In finance we use the SDE with Ito’s lemma, which can be written as follow:

dWtXbdttXadX ),(),( +=

Overview of Structured Products

Maxime Poulin 22

5.3. Lognormal returns for asset prices

We assume (although it can be proved, but it is not the purpose of this paper)

that the returns of an asset are log normally distributed and answer to the

following rule:

tdWdtSdS σµ +=

Where

StXa µ=),( And

StXb σ=),(

5.4. The Black & Scholes formula

The Black & Scholes formula determines the variation of a derivative’s price

over time. It can be expressed with the following partial differential equation

(PDE).

rVSVrS

SVS

tV

−∂∂

+∂∂

=∂∂

2

222

21 σ

5.5. The Black & Scholes formulas for options

From the Black & Scholes formula, we can extract equation to express the

price of a call option and a put option. By expressing C the price of a call, P

the price of a Put, we can write the prices of each as an equation of the

Underlying price S, its volatility σ, the option strike K, its expiry T and the

interest rate r:

)()(),( 21 dNKedSNTSC rT−−=

Overview of Structured Products

Maxime Poulin 23

)()(),( 12 dSNdNKeTSP rT −−−= −

Where:

T

TrKS

dσ

σ⎟⎟⎠

⎞⎜⎜⎝

⎛++⎟

⎠⎞

⎜⎝⎛

=2

ln2

1

Tdd σ−= 12

N () is the cumulative distribution function of the standard normal distribution.

5.6. Call – Put Parity

This is a very important concept in finance; it is extracted from the Black and

Scholes formula. It gives us a linear relationship between the price of a put, a

call, a cash position and the underlying.

In order to show this relationship, we will proceed in two steps:

First we will consider the portfolio position of an investor at time T (portfolio

with Long/Short position)

Second we will take the present value of this portfolio by discounting it at the

risk free rate.

This present value will give us the Call – Put Parity.

Let’s assume the investor has the following portfolio:

a) He is long a cash position K

b) He is long a call strike K with expiry T

c) He is short a put strike K with expiry T

At maturity of the options (time T), the portfolio is worth:

Overview of Structured Products

Maxime Poulin 24

TT PCK −+=ΠT

But being long a call and short a put, means that the performance of the

Portfolio is exactly the same than the underlying. Moreover, the cash position

being equal to the strike of the option, the value of the portfolio at the expiry T

of the options is the value of the underlying.

TS=ΠT

From this, if we calculate the present value of the portfolio, we get:

0000 )()( SPCKPVPV T =−+=Π=Π

This gives us the following relation: the Call – Put Parity.

000)( PSCKPV +=+

Where:

Si is the spot price of the underlying at time “i”.

Ci is the price of call strike K with expiry T at time “i”.

Pi is the price of put strike K with expiry T at time “i”.

Πi is the value of the portfolio at time “i”.

Overview of Structured Products

Maxime Poulin 25

6. The Forwards

For all structured products, one need to understand the concept of forwards: it

is the expected value of the underlying at a point in the future.

This concept is used in most pricing of structured products.

Let’s see how to evaluate the forward of a security and how it varies over

time.

For this we will use the concept of lognormal distribution explained earlier:

tdWdtSdS σµ +=

If we assume that the Brownian term is null, we get the following equality:

dtSdS µ=

We can then easily solve this equation in order to get:

TqrT eSeSTS )(

00)( −== µ

We can see that the forward increases as interest rates increases and

decreases as dividends increases. This is a very important observation that

will be very useful when we’ll have to deal with the optimization problem.

Overview of Structured Products

Maxime Poulin 26

7. The Correlation

7.1. Definition

It is the linear relationship which exists between two random variables, or time

series. In other words a correlation ρ between a random variable X and a

random variable Y indicates the “probability” of X changing in a given direction

and in which direction for a given change in Y.

“Definition: The correlation can be seen as a strength vector between X and

Y, which expresses the intensity and the direction of their linear relationship.”

The correlation is a constant, and can be expressed as follow:

)()()()(

)()()()))(((),cov(2222 YEYEXEXE

YEXEXYEYXEYX

YX

YX

YX −×−

−=

−−==

σσµµ

σσρ

Where: ρ is the correlation between two random variables X and Y, with mean

µX and µY and standard deviation σX and σY. Cov () is the covariance and E ()

is the expected value.

Using Cauchy-Schwarz inequality we can show that the maximum value that

can take the correlation ρ is equal to 1.

7.2. Correlation term structure and skew

Empirically, it has been shown that the correlation between two assets is

mean reverting over time, and can be expressed as follow:

)(tρρ =

Overview of Structured Products

Maxime Poulin 27

It means that if we compare actual correlation to historical correlation, ρ(t)

should tend to the historical correlation over time.

Diagram 7.1 Correlation term structure

Moreover, correlation also depends on the market conditions. In a bullish

market, assets tend to have a smaller correlation whereas on a bearish

market, correlation between assets of the same asset classes tends to one.

This is referred to as the correlation skew:

)(Kρρ =

Diagram 7.2 Correlation Skew

As a conclusion, we can express the correlation as a function of time and

Strike:

),( Ktρρ =

Correlation

Maturity

Historical Correlation

Correlation

Strike

Overview of Structured Products

Maxime Poulin 28

8. Volatility and Variance

8.1. Definition

The volatility (σ the standard deviation) of an asset which return (as seen

earlier) are log normally distributed, is equal to the average change of the

value compared to its mean µ. The Volatility is defined as the square root of

the variance, where the variance of an asset A is defined as:

222 ))(()()))((()( AEAEAEAEAVar −=−=

And therefore

22 ))(()( AEAE −=σ

8.2. Implied Volatility

The implied volatility is defined as what the market thinks the volatility will be.

In order to evaluate this implied volatility, we will revert the Black & Scholes

formula. Meaning, we can get the option prices from the market, knowing

these, we will calculate the volatility implied by this option price using the

Black & Scholes formula.

But the Black & Scholes formula is very dependent on the dividends which

where used to price the option. In order to estimate the dividends traders tend

to use one of the following methodologies:

a) Using synthetic forwards (Long Call, Short Put)

Limitations: listed options are only liquid over a few years, to estimate

dividends over longer term; this method will not be accurate.

b) Extrapolate future dividends from recent dividends

Limitations: Past dividends do not always represent what will be paid in

the future.

Overview of Structured Products

Maxime Poulin 29

c) Follow analysts forecast.

Limitations: if the forecast is wrong, it will incur losses.

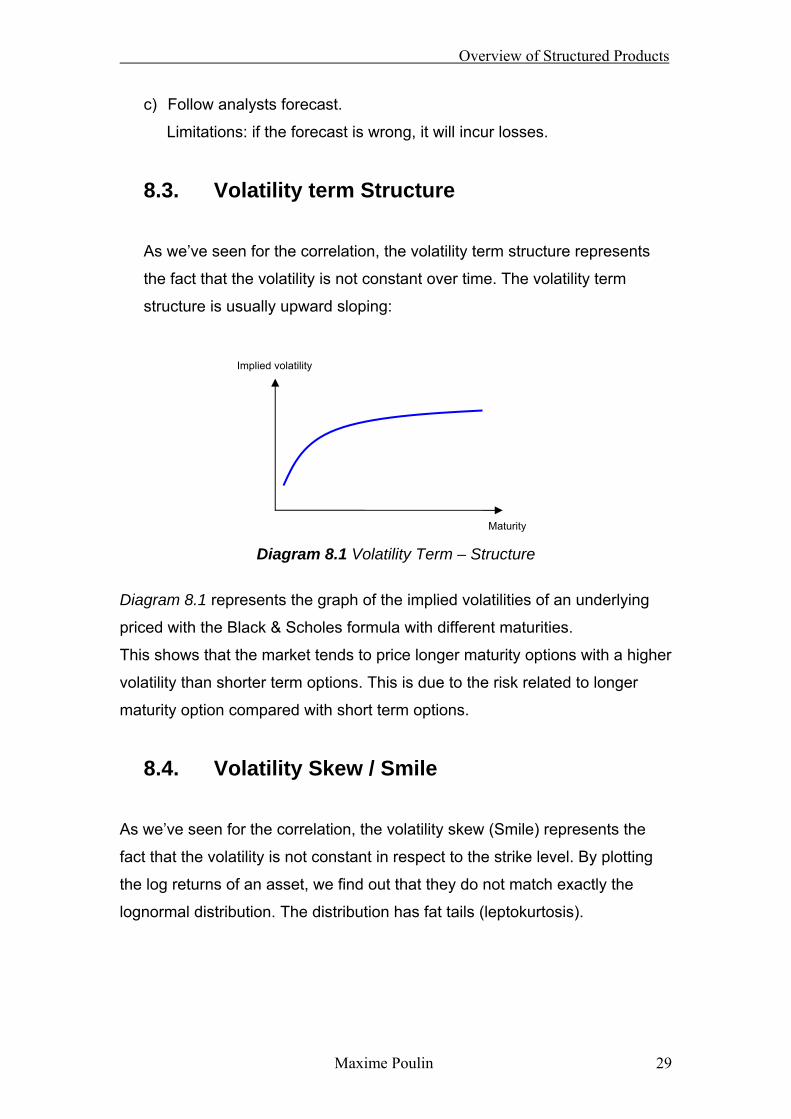

8.3. Volatility term Structure

As we’ve seen for the correlation, the volatility term structure represents

the fact that the volatility is not constant over time. The volatility term

structure is usually upward sloping:

Diagram 8.1 Volatility Term – Structure

Diagram 8.1 represents the graph of the implied volatilities of an underlying

priced with the Black & Scholes formula with different maturities.

This shows that the market tends to price longer maturity options with a higher

volatility than shorter term options. This is due to the risk related to longer

maturity option compared with short term options.

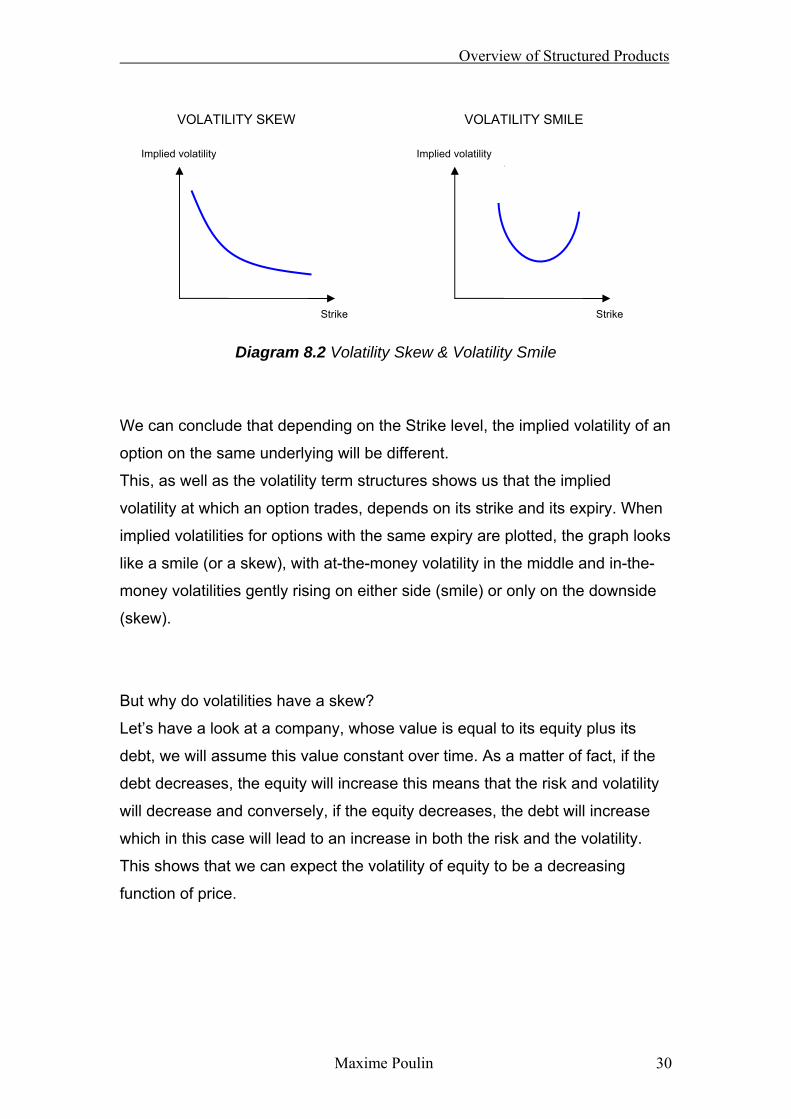

8.4. Volatility Skew / Smile

As we’ve seen for the correlation, the volatility skew (Smile) represents the

fact that the volatility is not constant in respect to the strike level. By plotting

the log returns of an asset, we find out that they do not match exactly the

lognormal distribution. The distribution has fat tails (leptokurtosis).

Implied volatility

Maturity

Overview of Structured Products

Maxime Poulin 30

Diagram 8.2 Volatility Skew & Volatility Smile

We can conclude that depending on the Strike level, the implied volatility of an

option on the same underlying will be different.

This, as well as the volatility term structures shows us that the implied

volatility at which an option trades, depends on its strike and its expiry. When

implied volatilities for options with the same expiry are plotted, the graph looks

like a smile (or a skew), with at-the-money volatility in the middle and in-the-

money volatilities gently rising on either side (smile) or only on the downside

(skew).

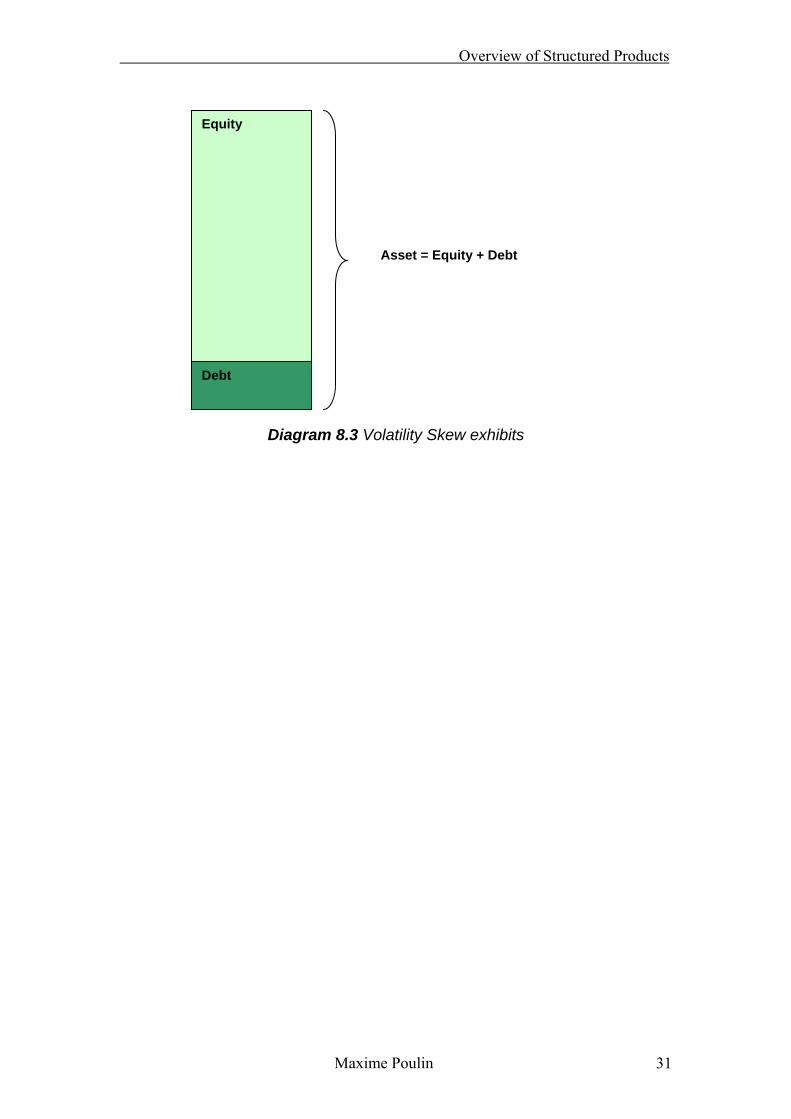

But why do volatilities have a skew?

Let’s have a look at a company, whose value is equal to its equity plus its

debt, we will assume this value constant over time. As a matter of fact, if the

debt decreases, the equity will increase this means that the risk and volatility

will decrease and conversely, if the equity decreases, the debt will increase

which in this case will lead to an increase in both the risk and the volatility.

This shows that we can expect the volatility of equity to be a decreasing

function of price.

Implied volatility

Strike

Implied volatility

Strike

VOLATILITY SKEW VOLATILITY SMILE

Overview of Structured Products

Maxime Poulin 31

Diagram 8.3 Volatility Skew exhibits

Equity

Debt

Asset = Equity + Debt

Overview of Structured Products

Maxime Poulin 32

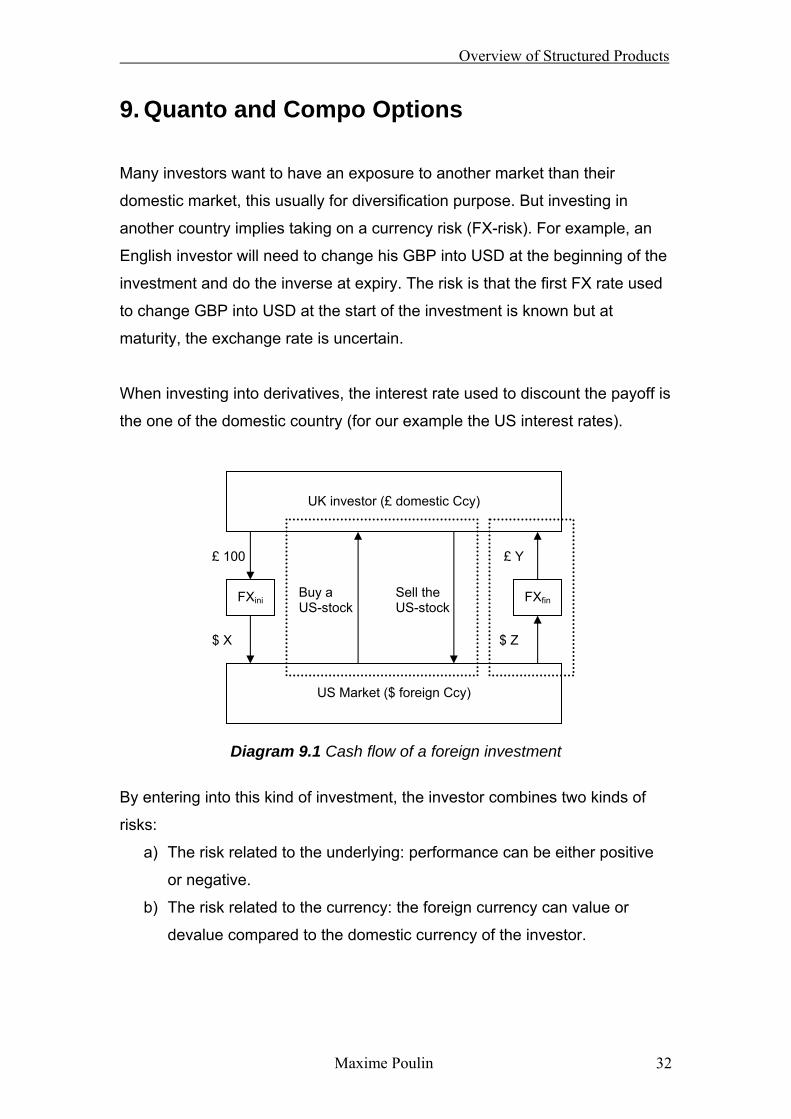

9. Quanto and Compo Options

Many investors want to have an exposure to another market than their

domestic market, this usually for diversification purpose. But investing in

another country implies taking on a currency risk (FX-risk). For example, an

English investor will need to change his GBP into USD at the beginning of the

investment and do the inverse at expiry. The risk is that the first FX rate used

to change GBP into USD at the start of the investment is known but at

maturity, the exchange rate is uncertain.

When investing into derivatives, the interest rate used to discount the payoff is

the one of the domestic country (for our example the US interest rates).

Diagram 9.1 Cash flow of a foreign investment

By entering into this kind of investment, the investor combines two kinds of

risks:

a) The risk related to the underlying: performance can be either positive

or negative.

b) The risk related to the currency: the foreign currency can value or

devalue compared to the domestic currency of the investor.

UK investor (£ domestic Ccy)

US Market ($ foreign Ccy)

£ 100

Buy a US-stock

FXini

$ X

Sell the US-stock

£ Y

FXfin

$ Z

Overview of Structured Products

Maxime Poulin 33

Compo Options “Definition: Derivatives where the payoff (expressed in foreign currency) is

converted back into the domestic currency with the exchange rate at maturity

and discounted with the domestic discount factor.”

Compo option transfer all the FX-risk to the investor, but some investors might

have a conflicting view between the Underlying and its currency.

An alternative to these options are the Quanto Options.

Quanto Options “Definition: Derivatives where the payoff (expressed in foreign currency) is

converted back into the domestic currency with a pre-specified exchange rate

at maturity and discounted with the domestic discount factor.”

Pricing quanto options:

If we assume that the exchange rate (FXt exchange rate at time t) log-normal

distributed stochastic process, we have:

FXFXfdt

t dWdtrrFXdFX

σ+−= )(

Where rd is the risk free rate of the domestic country, rf is the risk free rate of

the foreign country, σ is the volatility and dW is the Wiener process.

As we’ve seen earlier we have the same relation for the underlying’s price in

its home currency:

SSdt

t dWdtdrSdS σ+−= )(

Where d is the dividend rate of the underlying.

Overview of Structured Products

Maxime Poulin 34

The actual forward will be written as follow:

TdrrTdrT SFXfdd eSeSeSTS )(

0)'(

00)( σσρµ ⋅⋅−−−− ===

The option will then be price as seen earlier with this adjusted forward.

Overview of Structured Products

Maxime Poulin 35

10. Sensitivities of Exotic Options

This is used by all traders in the pricing stages to evaluate risks: there are two

ways to find these sensitivities; both are to be used simultaneously in order to

allow crosschecks:

a) Pragmatic approach: Estimating how the probability of being in or out

of the money will vary.

b) Mathematical approach: by isolating each parameter and looking at

the impact of a small change in this on the price of the derivatives.

10.1. Time Value Relationship

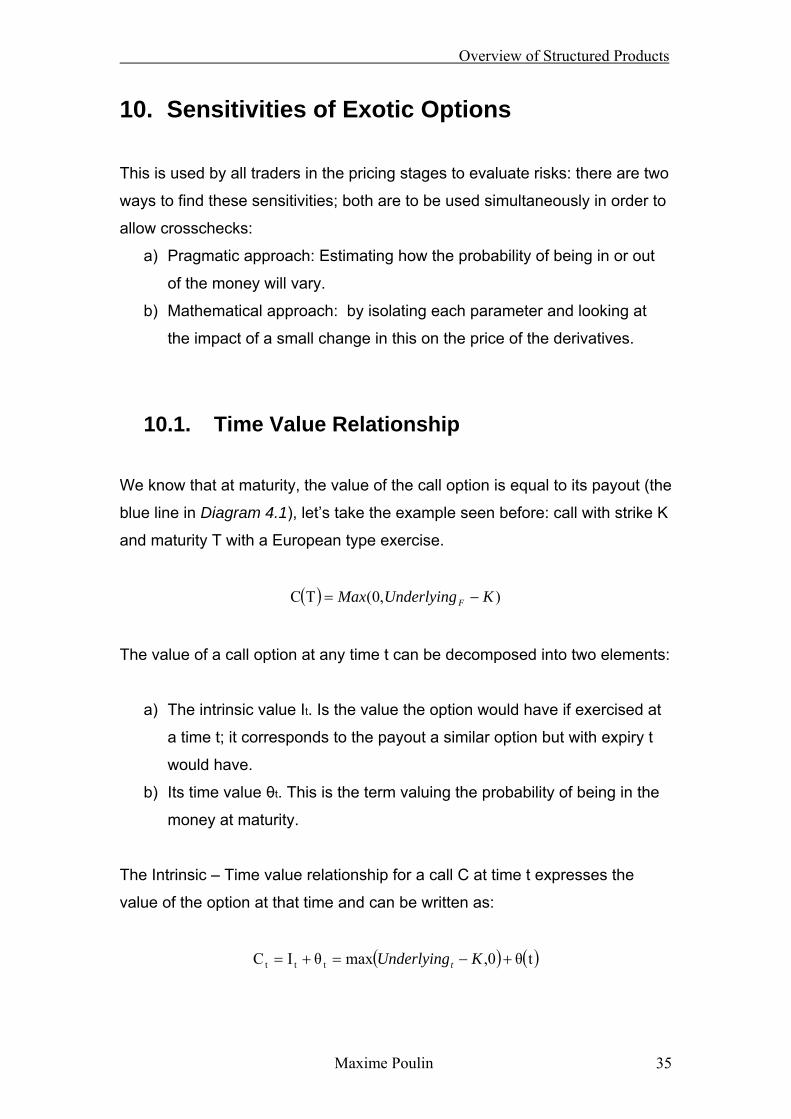

We know that at maturity, the value of the call option is equal to its payout (the

blue line in Diagram 4.1), let’s take the example seen before: call with strike K

and maturity T with a European type exercise.

( ) ),0(TC KUnderlyingMax F −=

The value of a call option at any time t can be decomposed into two elements:

a) The intrinsic value It. Is the value the option would have if exercised at

a time t; it corresponds to the payout a similar option but with expiry t

would have.

b) Its time value θt. This is the term valuing the probability of being in the

money at maturity.

The Intrinsic – Time value relationship for a call C at time t expresses the

value of the option at that time and can be written as:

( ) ( )tθ0,maxθIC ttt +−=+= KUnderlyingt

Overview of Structured Products

Maxime Poulin 36

Diagram 10.1 Intrinsic – Time value relationship

Generally speaking we can say that, for vanilla options, the intrinsic value is

directly a function of the forward and therefore will be sensitive to interest

rates and dividends and of the strike of the option. The time value on the other

side is a function of time and of the volatility. In case of a vanilla call it grows

asymptotically to volatility multiplied by square root of time.

10.2. Estimating sensitivities: Pragmatic approach

As seen earlier, the forward is proportional to the intrinsic value, which means

that when the dividends decrease, the intrinsic value increases. The same

way, when interest rates increase, the intrinsic value increases.

We can also see that if the strike is smaller, the option will be in the money

(assuming initial strike was at the money) and so, the intrinsic value will be

higher.

Finally, greater volatilities or longer maturities have both the same impact on

the time value of a call option (with strike at the money and European

execution): in both cases, the time value increases due to the fact that these

two points increase the probabilities of the option being in the money at

maturity.

We have now seen what where the sensitivity of the option price to the

following parameters:

S

Price

K

θt

It

Overview of Structured Products

Maxime Poulin 37

a) Dividends

b) Interest Rates

c) Strike

d) Volatility

e) Maturity

Overview of Structured Products

Maxime Poulin 38

11. Models used on Trading floors (Commerzbank)

There is a great variety of models used in finance in order to price derivatives.

They range from the Black & Scholes model to the stochastic volatility model.

But why do we need so many different models to price structured products?

How should we be able to choose which model will be the most accurate for a

specific structure?

Models in finance are mathematical tools and in the same way than

mathematical models are used in finance, each one has been implemented

for a specific purpose and to work on specific element (whether on a finance

or physics related subject).

What is a model?

A model is a series of laws which have been derived from empirical

observations and which have to describe and predict a given process in the

best possible way.

The options prices do not have a linear behavior; their first order derivative

with respect to a given parameter is not equal to zero. This has an important

impact on the option pricing.

When the second order derivative is negligible, a simple model will be enough

to price the option: in most case, a vanilla product (for example, the Black &

Scholes model will suffice).

When the first order is not enough and we have to take into consideration the

second order derivative because its impact on the option price is important.

As we’ve seen in part 5, the Black and Scholes model assumes that volatility

is constant. But like we said in part 8, it is not the case for assets in the

market, there is a skewed behavior of lognormal returns. Since skew does not

affect vanilla options with strike at the money and European execution, they

Overview of Structured Products

Maxime Poulin 39

can be priced with the Black & Scholes model. But if the strike of the option is

not at the money, we will need to use a model which estimates correctly the

impact of the skew.

This leads us to the conclusion that before choosing which model to use to

price an option, we need to check what parameter will have an impact on the

value of the option in order to have a model which will model correctly the

relevant parameter, so that the value of the option will be correct.

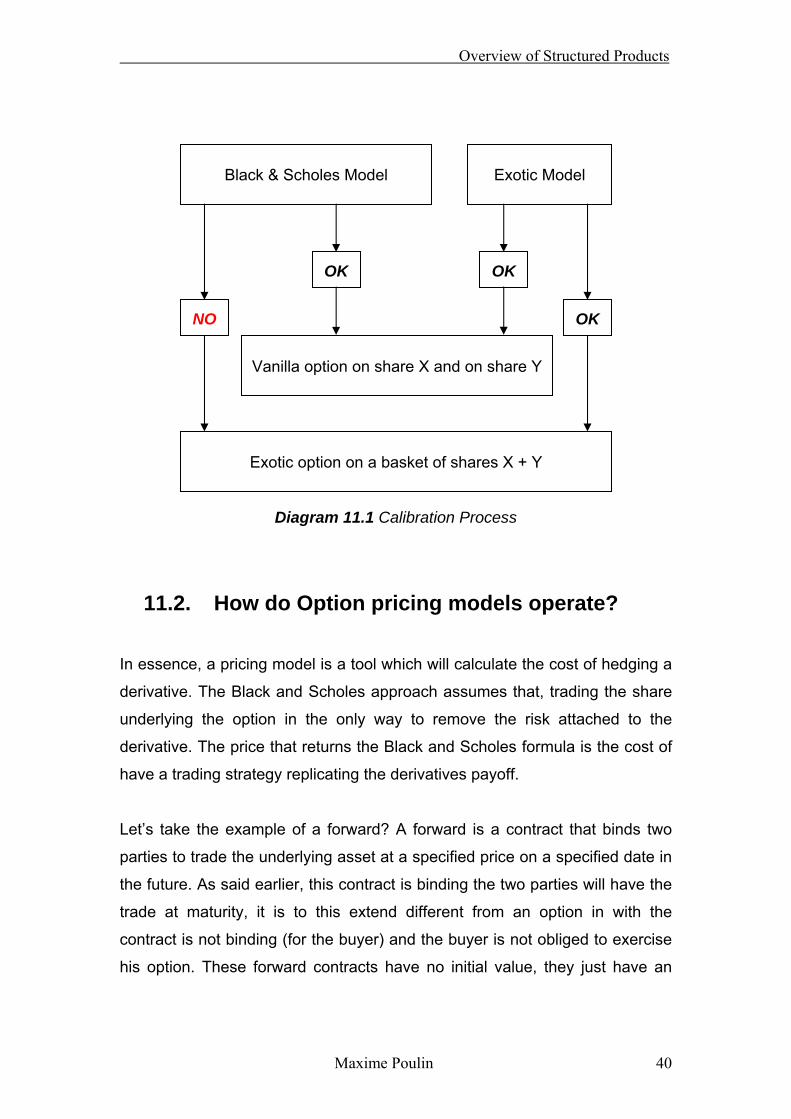

11.1. Calibration process of a model

This process is essential in order to get a correct price for an option.

We will focus our explanation around an example.

If we had to price an exotic barrier option, where the underlying is a basket of

shares (X and Y). As we’ve seen earlier, the Black & Scholes model won’t be

suitable for such an option; therefore, we’ll need to use a more complex

model. This model has to give the exact same price than the Black & Scholes

model for the individual at the money vanilla options. Adapting the parameters

of the model so that these points are matched is known as the “calibration

process”.

Overview of Structured Products

Maxime Poulin 40

Diagram 11.1 Calibration Process

11.2. How do Option pricing models operate?

In essence, a pricing model is a tool which will calculate the cost of hedging a

derivative. The Black and Scholes approach assumes that, trading the share

underlying the option in the only way to remove the risk attached to the

derivative. The price that returns the Black and Scholes formula is the cost of

have a trading strategy replicating the derivatives payoff.

Let’s take the example of a forward? A forward is a contract that binds two

parties to trade the underlying asset at a specified price on a specified date in

the future. As said earlier, this contract is binding the two parties will have the

trade at maturity, it is to this extend different from an option in with the

contract is not binding (for the buyer) and the buyer is not obliged to exercise

his option. These forward contracts have no initial value, they just have an

Black & Scholes Model

Vanilla option on share X and on share Y

OK

Exotic Model

Exotic option on a basket of shares X + Y

OK

OK NO

Overview of Structured Products

Maxime Poulin 41

execution price, price at which the underlying asset will be exchange at

maturity, and there is no upfront payment.

In order to hedge his risk, the seller of this kind of contract can for example

buy the underlying asset right now and hold it until the delivery date of the

contract, in this case the hedge is perfect, there is no more risk, and the

outcome is known with certainty.

From that, how can we estimate the settlement price, in other words the fair

price of this contract to buy / sell the underlying asset in the future, so that no

upfront is needed for the transaction? As we’ve seen in order to hedge this

position, we would need to buy the underlying asset now at a known price.

But there is a cost of financing, borrowing the cash in order to buy the

underlying asset is worth the interest rate paid during the holding period. The

full hedging cost in then equal to the price of the underlying asset plus the

borrowing cost incurred to buy the share and hold it until maturity.

As an example, assume that the underlying asset’s price is GBP 100, the

contract’s maturity is 1 year, and the interest rates are at 2%p.a. The one year

forward selling price of the underlying asset is GBP 102, which is as explained

earlier, the price of the asset (i.e. GBP 100) + the cost of borrowing GBP 100

over one year (i.e. GBP 2). At the end of the period, the seller of the contract

will have a flat position: no profits and no losses will impact him wherever the

underlying asset’s price goes.

If the agreed settlement price for the forward contract (referred to as the Strike

price) is not exactly equal to GBP 102, one of the parties will have to pay an

amount upfront to the other in order to compensate the difference.

The GBP 102 is not an arbitrary number but is the actual cost of delivering a

share worth GBP 100 today in one year knowing that the interest rates are at

2.00%, meaning that the holding cost will be of GBP 2.00.

Overview of Structured Products

Maxime Poulin 42

If the buyer has a right to cancel the contract, the pricing of such a contract

becomes entirely different. The simple hedging strategy described above

won’t be possible anymore, because if at maturity the underlying asset’s price

is below the strike price, the buyer of the contract won’t be willing to settle the

transaction as he would be better of buying the stock directly in the market at

the current market price. This would leave the seller short cash (GBP 102)

and long the stock (worth less than GBP 102), which would incur a loss. This

would not be acceptable. One possible strategy would be to sell the

underlying asset when its price falls below the strike price of the contract, and

buy it when its price goes back above the strike price. Another would be to

“smooth” the trading, by buying half a share initially, assuming that it is about

equally likely that the share is going to go up as down, and buying or selling

another half share at some point in the future depending on the way in which

the price moves.

If we consider a simplified market, with a binomial tree for the share price at

maturity: it can be GBP 95 or GBP 105. In this market, interest rates are

assumed to be equal to 0. The strike price of the option is GBP 100. In order

to hedge, the seller of the contract buys half a share on the start date of the

contract. At maturity, if the underlying’s price is GBP 105, then, the seller is

long half a share worth GBP 52.50 for which he spent GBP 50, but he will

need to buy another 50% of a share has he has to deliver one share. Buying

another 50% of a share worth GBP 105, will cost him GBP 52.50. In the end

the seller will have lost GBP 2.50.

If the share price drops, the seller of the option is left holding half a share,

worth GBP 47.50, for which he paid GBP 50. The buyer is not interested in

the option has the strike price is above the spot price. So the seller will have

to liquidate his position at a loss of GBP 2.50.

We can see that this hedge as a fixed cost of GBP 2.50 for the seller

whatever the scenario is. By charging GBP 2.50 upfront to the buyer, the

seller hedges his risk and has a flat position again. We can conclude that with

these market conditions, the fair price for this option is GBP 2.50.

Overview of Structured Products

Maxime Poulin 43

But with the actual market conditions, there are a much more possible

outcome than a simple binomial tree, which is why we need more complicated

model in order to take into account all these parameters with assumed

negligible the simplified explanation given previously.

An important point about the hedging strategy in the simplified market model

is that it involves buying shares at a higher price than they are sold. This is

what incurs a loss for the seller, and this is why an option is not worth zero. In

other words, all models will estimate the loss incurred by the hedge which will

require of the seller to buy high and sell low. This also implies that the seller

when he gives an estimation of the hedging cost does not care where the

stock price will eventually go, his concern is to cover the potential outcome

regardless of their probability with the model.

Black & Scholes option pricing is therefore just a complicated way of working

out the loss from running a hedging strategy like the ones described above,

which systematically buys shares at a higher price than they are sold. The

model makes assumptions about how the share price behaves in the very

short term, and then adds up the effect of these very short term moves,

combined with the hedging strategy which specifies how many shares are

actually being held at any time, to calculate the losses that arise from the buy

and sell strategy. The borrowing cost: financing cost is also taken into

consideration in all financial models.

The innovation that Black & Scholes brought was that it offered an accurate

representation of the market movements. Moreover, it includes a hedging

strategy which offer a perfect solution for the option seller if the market

behaves as the model expect it to behave in it representation. In other words,

the person doing the hedge will be completely indifferent to the direction the

underlying asset price takes. But one of the draw backs is that the Black &

Scholes model will only model the short term movements of an underlying

asset price but will not make any assumption over the long term.

Overview of Structured Products

Maxime Poulin 44

For highly volatile underlyings, the losses incurred by the Buy High Sell Low

strategy are much higher than what they would be with less volatile

underlyings. This explains why the price of vanilla option is highly dependent

on the volatility of the underlying asset.

As we’ve just seen, simple derivative pricing tools assume that the

underlying’s price is continuously moving, the models are representing this

movement over a short tem period. For the particular case of the Black &

Scholes model, the distribution of the underlying price and the size of the

spread is dependent on two factors: the volatility of the stock (a constant), and

the time over which the changes are observed (the exact relation is with the

square root of this duration). This model also assumes that upward movement

are as probable and are of the same size than downward movement of the

stock price. One of the problems of this model is that it considers the volatility

is constant over time which as we’ve seen earlier is not the case.

Solving the Black & Scholes formula tells us that the fair price of an option is

the weighted (by their probabilities) average of all the possible payoffs of the

option at maturity. With this method, the option fair value is the same when

calculating the losses incurred by the hedge over the life of the option and

calculating the average option price given the final distribution of the returns of

the underlying at maturity obtained through the model which return a short

term representation of the underlying asset price evolution.

In order to avoid having to simulate the entire path of an underlying from the

issue date to the maturity date, Monte-Carlo simulations are taking advantage

of this point, by only simulating changes from issue date and maturity date

and not looking at the changes in between. This gives us the distribution of

the prices at the end of the period which is the same than the one of the

prices we would get if the underlying asset price follows the exact path

modelled with the Black and Scholes equation. The model will estimate the

payoff of each path simulated with the Monte-Carlo. The fair value of the

option can be calculated by taking the weighted (by their probabilities)

average of all these payoffs (discount with the actual interest rates).

Overview of Structured Products

Maxime Poulin 45

But in the market, we can observe that option have a skew / smile, which are

not taken into consideration by the Black & Scholes model as explained

earlier on, this, implies that the price give by this model is not completely

accurate. The conclusion we can take out from this is that due to the skew

and smile, the returns are not log-normally distributed.

But as we said for Monte-Carlo simulation, the path followed by the underlying

asset between the issue date and the maturity date is not relevant for the

evaluation of the option price. As a matter of fact, the return not being log-

normally distributed is not important. If the distribution of returns can be

estimated, a Monte-Carlo simulation accounting for the skew will be possible.

For path dependent option, this pricing method will not work (for example an

American barrier option or an Asian option).

11.3. Black Vanilla Model

It is considered as one of the simplest models, but can only be used for

analytic pricing of vanilla options.

It cannot be used to price more complex structures in which a splife of the

payoff would be needed (Monte-Carlo simulations are not possible with this

model).

11.4. Black Diffusion Model

This model is the simplest model which can be used with a Monte-Carlo

simulation. It takes into account the term-structure for each underlying but

does not account for the skew.

Products which require a splife for their payoff can be priced with this model,

but the impact of the skew will not be taken in to account. As the impact is

very significant on a number of structured products, this model is not the one

which is the most often used.

Overview of Structured Products

Maxime Poulin 46

11.5. Local Volatility Model

Local volatility is a simple concept which says that the instantaneous volatility

of the process which drives share price changes is a fixed function of time and

the actual share price. If we assume the Local Volatility rules apply, we should

be able to know the volatility of a stock at any point in the future for any given

point time and underlying share price.

By looking at the options (vanilla) quoted on the market, we can create a

matrix of the short term volatilities (a volatility surface) depending on the time

and the underlying’s share price. With this matrix Monte-Carlo simulation can

easily by done as short term variations of the price can be evaluated with the

matrix. But regarding longer term variations, the model is much slower as the

calibration process takes a long time, and the need to calculate paths with

many intermediate observation dates and not just the actual ones impacting

directly the payoff of the derivative.

Although used in Commerzbank, the Local Volatility model is widely used in

finance to price options: either with an immediate starting point but also with

forward starting date. There are some known problems with the so-called

“dynamics” of the implied volatility with this model, but it is a very powerful and

widely used model which is the benchmark for most pricing.

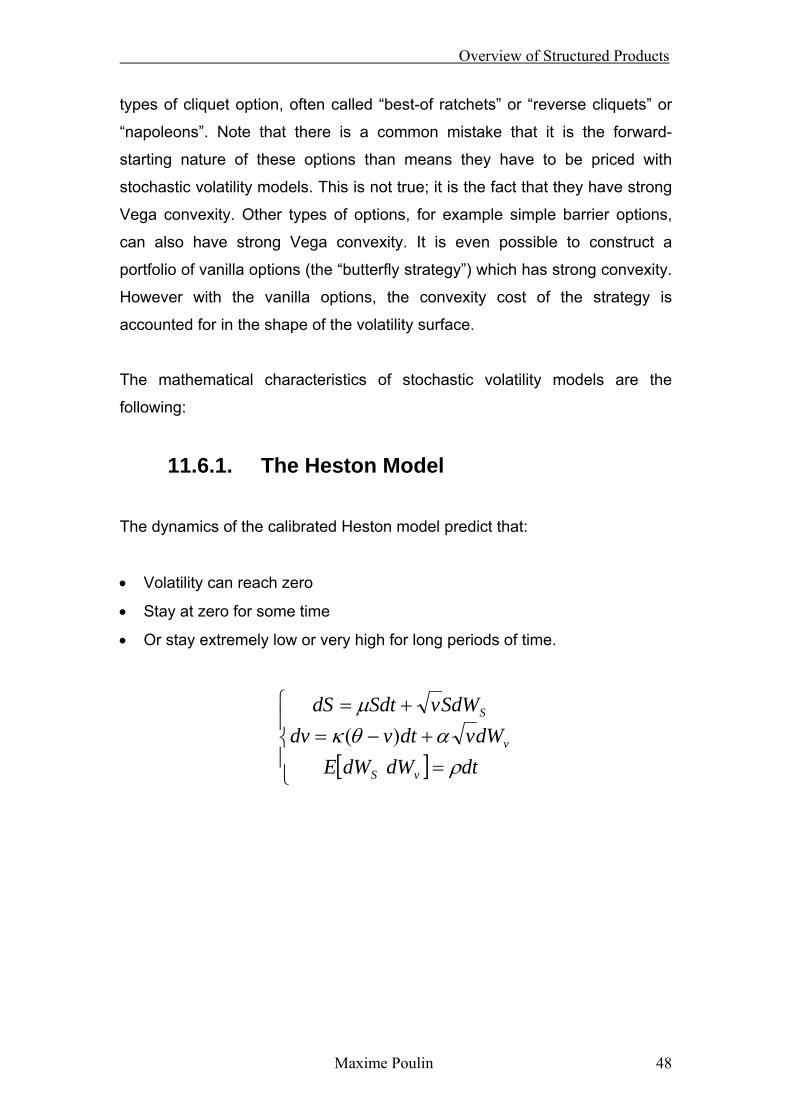

11.6. Stochastic Volatility Model

This model is a variation of the Local Volatility model which attempts to

reduce the problems of the implied volatilities “dynamics” as well as the

limitation due to the assumptions that volatility is only a function of the spot

price of the underlying and the time. But as it can easily be observed in the

market, this assumption is erroneous.

Overview of Structured Products

Maxime Poulin 47

This can be very important in pricing certain types of option which have “Vega

convexity”. This means that their sensitivity to implied volatility is not constant,

and as implied volatility goes up and down, so will the sensitivity to this

parameter. Imagine a situation where an exotic option which has a positive

sensitivity to implied volatility is Vega-hedged with a vanilla option. If the

exotic option has “positive” convexity of Vega, then its sensitivity to implied

volatility increases as implied volatility increases. So the total position will no

longer be hedged if implied volatility goes up, as the exotic option will have

become more sensitive. The hedger will need to sell some more vanilla

options in order to have a hedged position again. If implied volatility then

drops, the hedger will have to unwind the vanilla option trade. They will make

money on this unwind, as they are buying back the vanilla option at a lower

level of implied volatility compared to the level at which they bought it. So a

positive Vega convexity position will consistently make the holder money

when implied volatility varies itself.

The problem arises where an exotic option position has negative Vega

convexity. The holder of such a position will systematically lose money if

implied volatility changes, and this clearly happens on a daily basis in the

market. So they need a model to calculate the cost of these changes, in just

the same way that the basic Black & Scholes model calculates the cost of re-

heding the delta of an option.

Stochastic volatility models generally have five components. The average

level of the basic volatility of the share price, the volatility of this volatility

(which can be seen as the acceleration), the correlation between the basic

volatility and the “acceleration”, and the speed to which the basic volatility

reverts to its mean level. (This mean reversion is necessary as it is clear that,

unlike a share price, implied volatility does not increase without limit. A share

price can double, triple, quadruple or even more, whereas volatility cannot

increase above a certain level, except for very short periods.)

This is why stochastic volatility models are used to price options with Vega

convexity. The classic example of an options with Vega convexity are certain

Overview of Structured Products

Maxime Poulin 48

types of cliquet option, often called “best-of ratchets” or “reverse cliquets” or

“napoleons”. Note that there is a common mistake that it is the forward-

starting nature of these options than means they have to be priced with

stochastic volatility models. This is not true; it is the fact that they have strong

Vega convexity. Other types of options, for example simple barrier options,

can also have strong Vega convexity. It is even possible to construct a

portfolio of vanilla options (the “butterfly strategy”) which has strong convexity.

However with the vanilla options, the convexity cost of the strategy is

accounted for in the shape of the volatility surface.

The mathematical characteristics of stochastic volatility models are the

following:

11.6.1. The Heston Model

The dynamics of the calibrated Heston model predict that:

• Volatility can reach zero

• Stay at zero for some time

• Or stay extremely low or very high for long periods of time.

[ ]⎪⎩

⎪⎨

⎧

=+−=

+=

dtdWdWEdWvdtvdv

SdWvSdtdS

vS

v

S

ραθκ

µ)(

Overview of Structured Products

Maxime Poulin 49

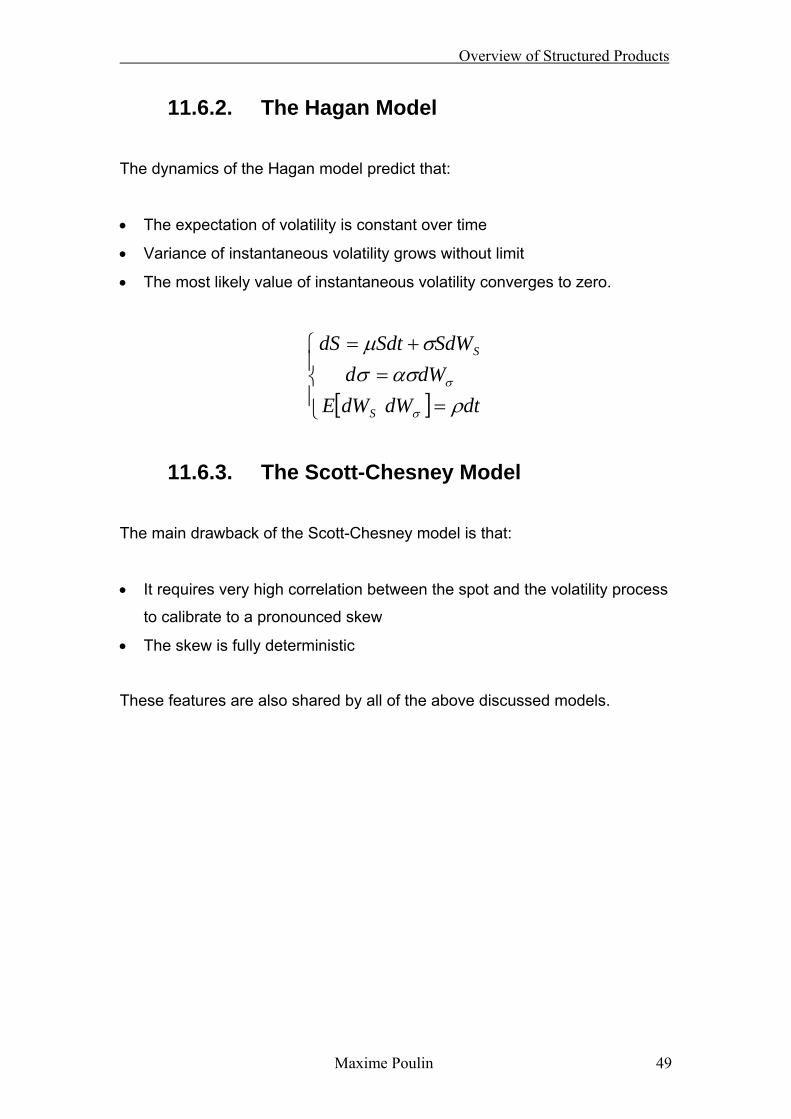

11.6.2. The Hagan Model

The dynamics of the Hagan model predict that:

• The expectation of volatility is constant over time

• Variance of instantaneous volatility grows without limit

• The most likely value of instantaneous volatility converges to zero.

[ ]⎪⎩

⎪⎨

⎧

==

+=

dtdWdWEdWd

SdWSdtdS

S

S

ρασσ

σµ

σ

σ

11.6.3. The Scott-Chesney Model

The main drawback of the Scott-Chesney model is that:

• It requires very high correlation between the spot and the volatility process

to calibrate to a pronounced skew

• The skew is fully deterministic

These features are also shared by all of the above discussed models.

Overview of Structured Products

Maxime Poulin 50

12. The risks related to structured products

When a bank issues a structured product to a client, it is in fact selling a

contract (under form of swap, note or certificate) that ensures the holder

receives a given percentage of the notional invested back, depending on the

performance of the underlying asset(s). The role of the trader is to ensure that

the right amount of risk is always hedged away in order to be able to fulfil the

conditions stated in the contract.

Due to the complexity of the financial world, and especially that of exotic

products, the hedges are far from being completely accurate. This is often not

related to the ability of the trader but rather to the nature of risk which has to

be hedged away.

It is possible to categorize the main risks into the following sub-categories:

a) Delta risk

b) Vega risk

c) Correlation risk

d) Second order risks

The value of an option can vary over time because of several market

parameters. The trader has to have an opposite position in the market (with

respect to the issued products) in order to reflect the change in value of the

derivative instruments. The main components which have to be hedged away

are the so-called first-order risk indicated above (Delta, Vega and

Correlation). Once these have been hedged, the trader has still to verify the

presence of second order risk like Volga or Vanna. Usually their effect is

negligible for vanilla options and most of the commonly traded exotic options.

But this is not the case for cliquets and other unusual exotic payoffs.

Overview of Structured Products

Maxime Poulin 51

12.1. Delta Risk

The Delta represents for the trader, without any doubt, the most important risk

to be hedged. This is achieved by buying (or selling) the right amount of

shares (futures contracts in case of indices) in order to have at all time (or as

many time as possible) a flat delta position. In other words the trader has to

be long (or be short) at any time an amount of the underlying asset so that if

added to its delta position, resulting from the products issued, equals zero.

Liquidity is in this case a very important aspect which has to be analyzed

when checking if a given underlying can be hedged or not. It is important to

verify that the amount of shares traded per day corresponds to the delta of the

product which has been sold since the trader, as stated previously, has to buy

(or sell) exactly that amount of shares.

12.2. Vega Risk

Once the Delta component is hedged away, the trader still has the risk

associated with the volatility of the underlying.

Suppose that a bank sells an at the money call option on one underlying

today to one of its clients. This option has a value A which can be estimated

with the Black & Scholes equation as previously seen.

Suppose that after a period t, the market has not moved compared to the

issue date, meaning that all the market parameters have remained constant

over time. The value of the option has therefore not changed (if we neglect

the time decay) and the call is still worth A. Suppose now that after the period

t, all the market parameters have not seen any change but the volatility of the

underlying (on which the option is based) has increased. The option is now

worth B (where B is greater than A since a call is long Vega). In order to be

hedged, the trader has, therefore, to buy volatility, i.e. he will buy option on

this underlying.

Overview of Structured Products

Maxime Poulin 52

12.3. Correlation Risk

Correlation risk is one of the most important and dangerous component to

which banks are exposed. Due to the nature of the products sold over the

past decade, banks are generally short on correlation. This is because of the

attractiveness nature of low correlation. Let’s have a look at a generic product:

the “worst of”, meaning that the payoff, usually represented by a big coupon

or the capital protection, depends on event that one (or more) of the N

underlyings has touched a barrier or not. The lower the correlation the more

attractive the final payoff will be for the investor.

Consider a reverse convertible worst of where, at maturity, the investor is long

a bond, receives a coupon X and is short a put down and in (with barrier B) on

the worst performing stock. He receives therefore his notional back plus the

coupon X if none of the underlying stocks ever traded below B. In case the

condition is not verified, and therefore one or more stocks did trade below the

barrier B, the client still receives the coupon X, but the notional invested is

reduced by an amount corresponding to the highest drop among the stocks at

maturity. In order to have an attractive coupon it is in the investor’s interest to

choose stocks with as low correlation as possible. By reducing the correlation

we increase the probability of one of the shares touching the barrier B. This

will, in turn, increase the probability of losing the capital protection at maturity,

leaving more to spend for the coupon X.

12.4. Second order Risks

Modelling risk refers to the model used to evaluate the price of the derivative

instrument. Due to the complexity of exotic products it is crucial to take into

account all the effects that could affect their value. There are products for

which second order effects (second order derivatives with respect to a given

market parameter) do not have to be taken into account. This is especially the

case for simple products like vanilla options or even simple exotic options.

Overview of Structured Products

Maxime Poulin 53

Consider, for example, an at-the-money call option on a given underlying

asset. This option can be valued with the Black-Scholes model or with the

more “sophisticated” Local Volatility Model and the price we would get would

be exactly the same. Skew effects have, in fact, no influence when valuating

an at-the-money vanilla call option.

Consider now a barrier option, like a down-and-out put option with barrier at

60%. The model used in this case assumes a very important role. The Black-

Scholes model would use the same volatility for the strike and for the barrier,

whereas the Local Volatility Model would consider two different volatilities

because of presence of skew.

Overview of Structured Products

Maxime Poulin 54

13. Example of exotic derivative: Cliquets

A cliquet, ratchet option or strip of forward start options is a derivative where

the strike is reset on each observation date at the then current spot level. The

profit can be accumulated until final maturity, or paid out at each observation

date.

Cliquets are complex exotic products where second order effects can

significantly affect the pricing. There are two main effects which have to be

considered:

a) Volatility of volatility effects (Vega convexity)

b) Forward skew effects

Not all cliquets are sensitive to volatility of volatility (“acceleration”) and

forward skew. We’ll see what the impact is on the main types of re-striking

options.

13.1. Convexity (or Volga)

Let’s consider an ATM European call option. We have seen that its price can

be written as

TC **4.0 σ≈

If we draw the price of this option with respect to the volatility we can see that

it is a straight line with positive slope, as shown in Diagram 13.1.

Overview of Structured Products

Maxime Poulin 55

Diagram 13.1 A call option price as a function of volatility

It is easy to verify that the Vega in this case is equal to a constant, because

we have a linear relationship; it is therefore independent from the level of the

volatility. The Vega is a constant line as shown in Diagram 13.2.

Diagram 13.2 A call option’s Vega as a function of volatility

So for an ATM call

0Volga 2

2

=∂∂

=σV

Sigma

Price

Sigma

Price

Overview of Structured Products

Maxime Poulin 56

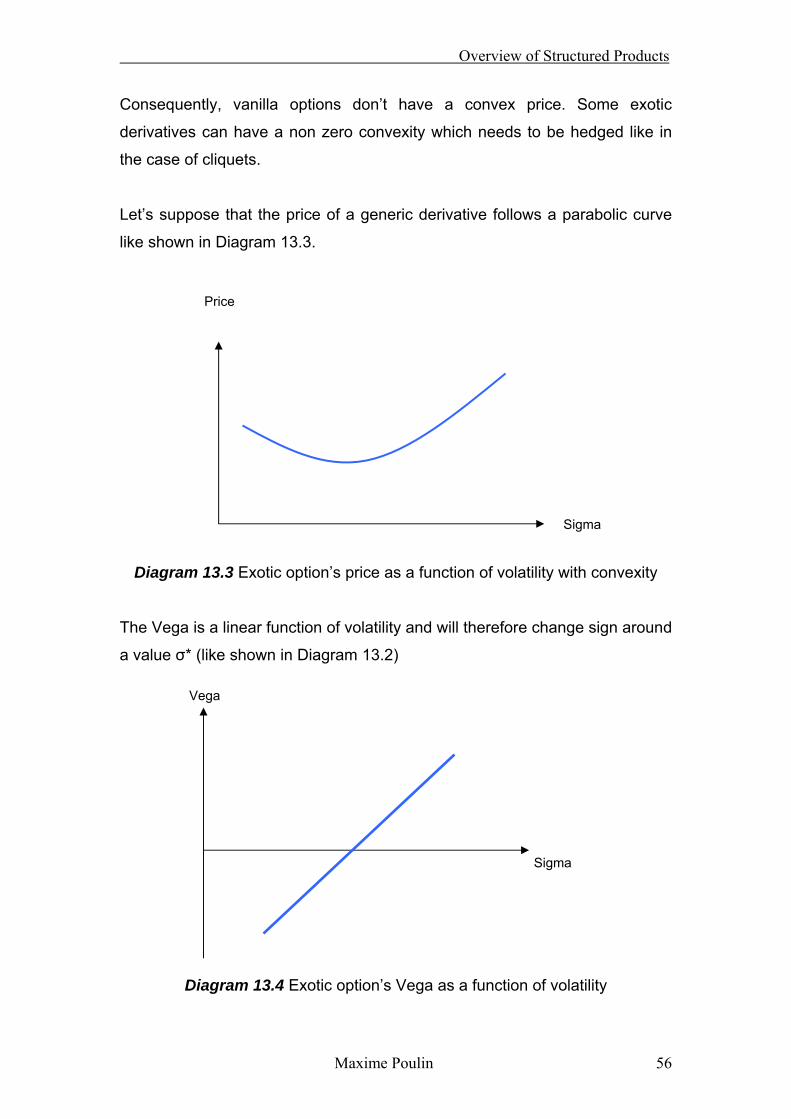

Consequently, vanilla options don’t have a convex price. Some exotic

derivatives can have a non zero convexity which needs to be hedged like in

the case of cliquets.

Let’s suppose that the price of a generic derivative follows a parabolic curve

like shown in Diagram 13.3.

Diagram 13.3 Exotic option’s price as a function of volatility with convexity

The Vega is a linear function of volatility and will therefore change sign around

a value σ* (like shown in Diagram 13.2)

Diagram 13.4 Exotic option’s Vega as a function of volatility

Sigma

Price

Sigma

Vega

Overview of Structured Products

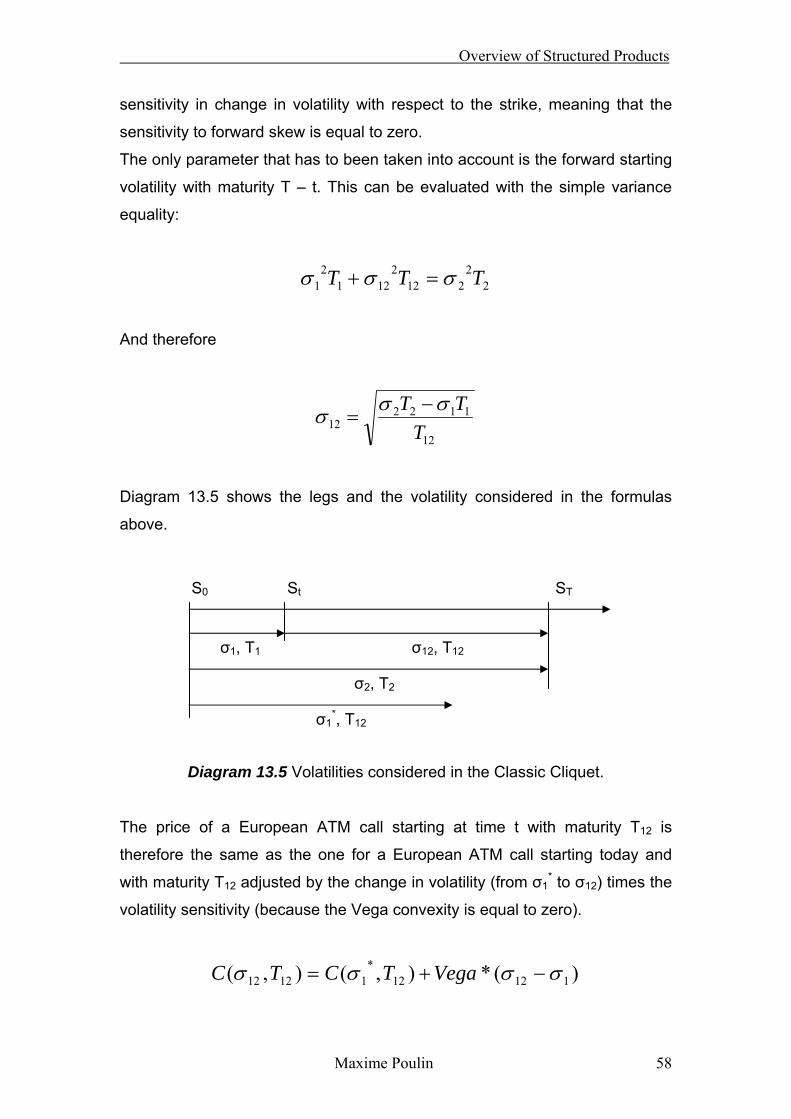

Maxime Poulin 57

As you can see in this case, the Vega is not constant with respect to volatility

but is a linear function of the volatility. We call σ* the volatility where the Vega

is equal to zero and change sign. If we are buying volatility, the more σ

increases, the smaller the Vega is. In order to hedge our position, we need to

buy the volatility, therefore we buy the volatility when it increases and we sell