E-tailing 2015

32

Indian e-tailing versus the West – What has worked, what will not work, will it increase in scale? BY - DERRICK KEITH MONIS 1

-

Upload

derrick-keith -

Category

Business

-

view

392 -

download

0

Transcript of E-tailing 2015

1

Indian e-tailing versus the West – What has worked, what will not work, will it increase in scale?

BY - DERRICK KEITH MONIS

2

What is E-tailing?

Electronic retailing (e-tailing) is a buzzword for any business-to-consumer (B2C) transactions that take place over the Internet. Simply put, e-tailing is the sale of goods online.

3

Steps involved in E-tailing•Customer Visit

•Choice of Product

•Payment Online

•Product Delivery

•Product acceptance

or return

•Customer Feedback

4

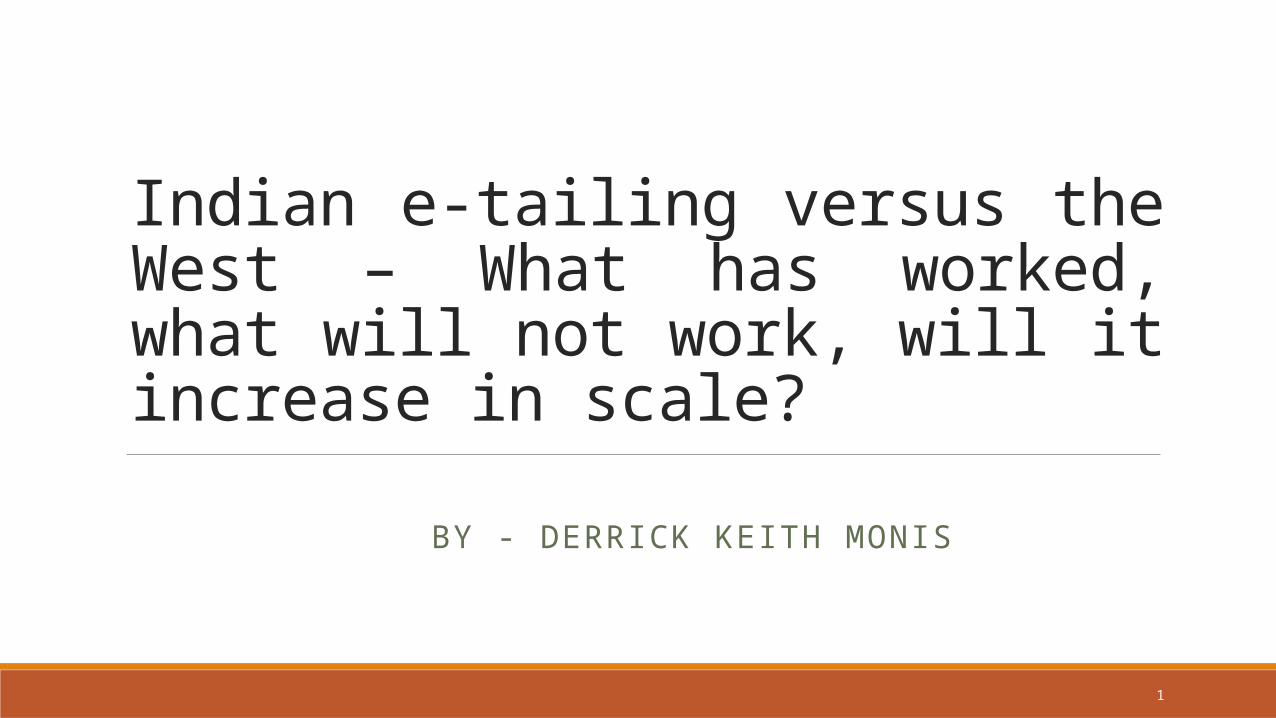

Advantages of E-tailingEliminate middlemen Secure payment

systemWorkflow automation A 24 hr. anywhere –

anytime store

Economical Unlimited market space

Collect customer info COD

Higher Margins Variety Likely to spend more(trends/ suggestion)

Deals (combo/season/sale)

Quick Comparison Shopping Better Customer Service

Cash back Send gifts

5

Disadvantages of E-tailingSecurity , System and Data Integrity

High Risk Of Internet Start–up(funding risks)

System Scalability Products People won't buy onlineLuxury/furniture etc.

Difficulty in the return of goods

Hard to build customer relationship/loyalty

High advertisement expenses

Can’t feel the product

COD – high returns Social Media complaints Limited only to online users

Complex taxation system

Poor last-mile connectivity

Impulsive shopping reduces Lack of Skilled manpower High customer acquisition cost

6

Scenario of Western E-tailing

7

8

9

10

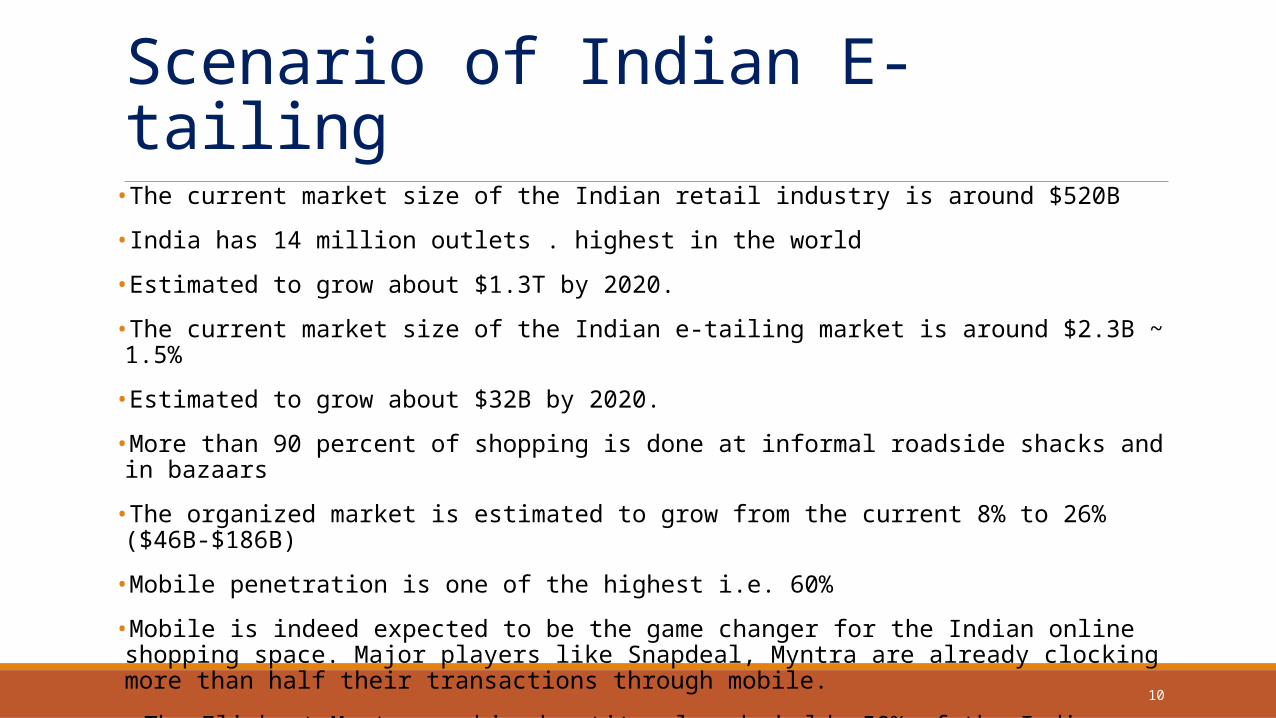

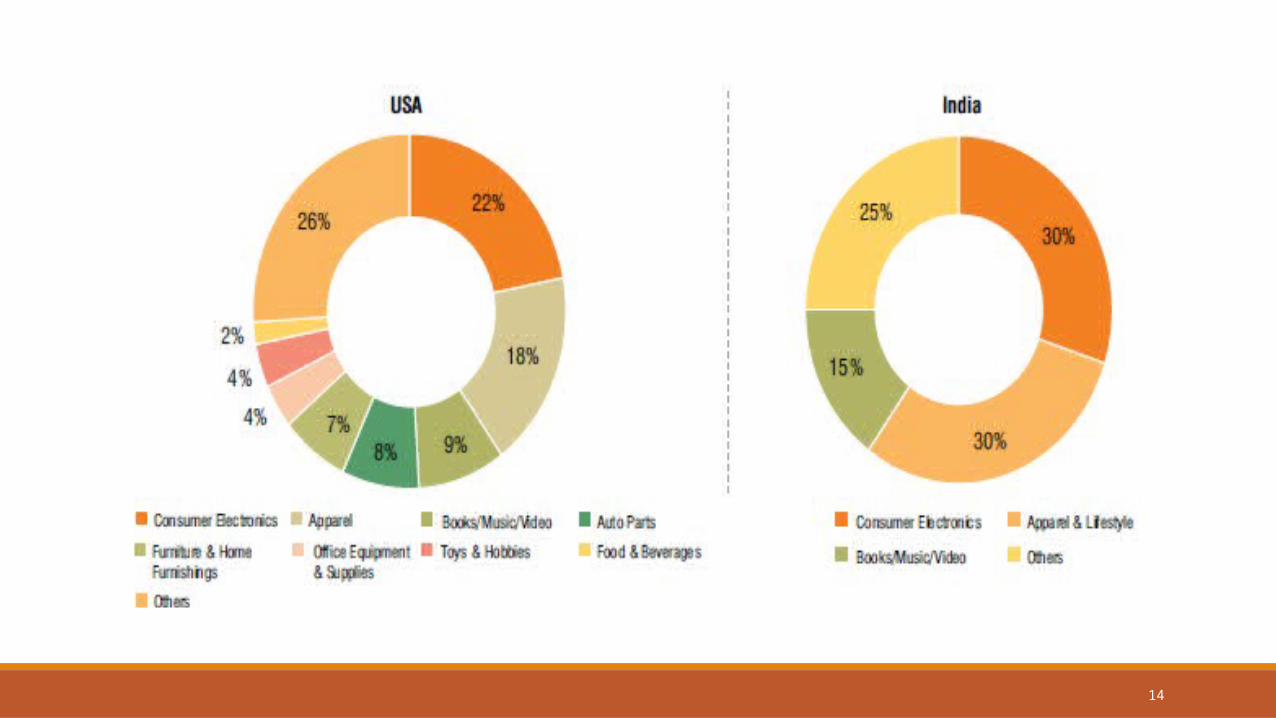

Scenario of Indian E-tailing•The current market size of the Indian retail industry is around $520B

•India has 14 million outlets . highest in the world

•Estimated to grow about $1.3T by 2020.

•The current market size of the Indian e-tailing market is around $2.3B ~ 1.5%

•Estimated to grow about $32B by 2020.

•More than 90 percent of shopping is done at informal roadside shacks and in bazaars

•The organized market is estimated to grow from the current 8% to 26% ($46B-$186B)

•Mobile penetration is one of the highest i.e. 60%

•Mobile is indeed expected to be the game changer for the Indian online shopping space. Major players like Snapdeal, Myntra are already clocking more than half their transactions through mobile.

• The Flipkart-Myntra combined entity already holds 50% of the Indian market share and is likely to capture 70% in the next two years.

11

12

13

Comparison – Maturity vs Introduction stage

WEST (US)- 2015 JULY INDIA- 2015 JULYPopulation 322M 1.26BInternet users 86.75% i.e. 279M 27% i.e. 354M Mobile penetration among Internet users

26% i.e. 72.5M 60% i.e. 213M

Growth rate (Internet Usage) 7% 14% (25% since past 4 months)Ecommerce Sales $280B $7.7B

14

15

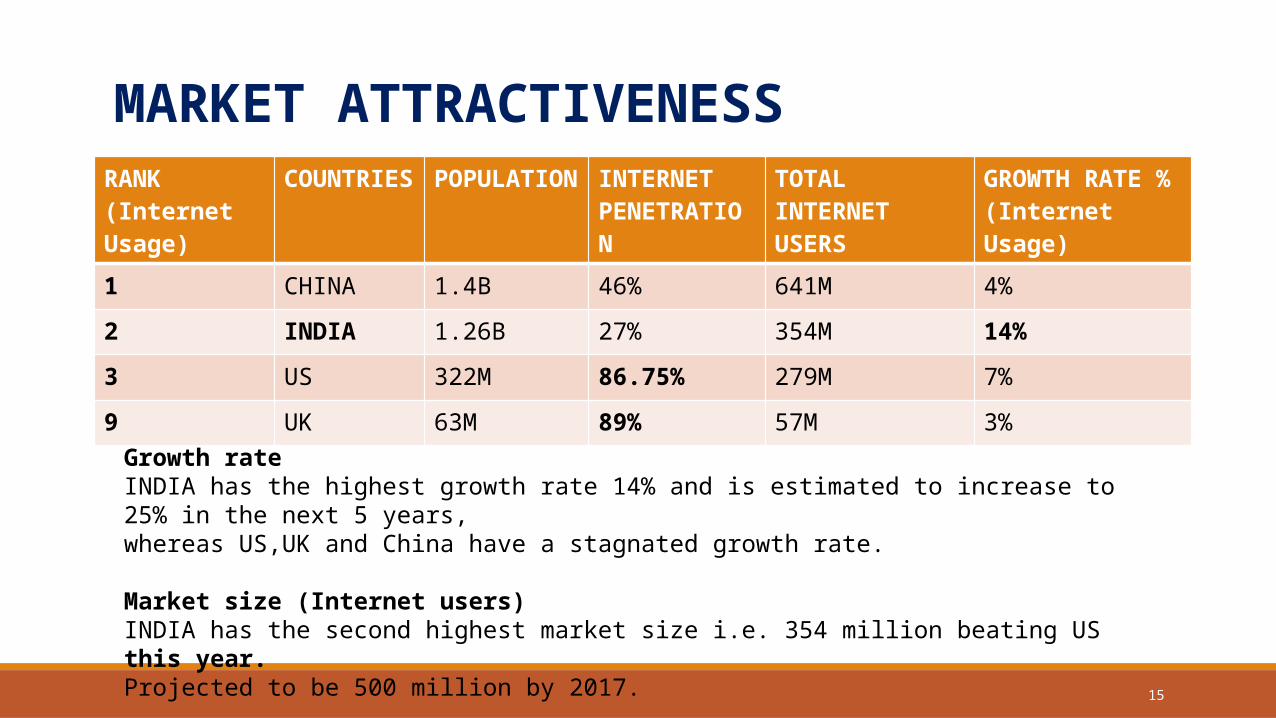

RANK(Internet Usage)

COUNTRIES POPULATION INTERNET PENETRATION

TOTAL INTERNET USERS

GROWTH RATE % (Internet Usage)

1 CHINA 1.4B 46% 641M 4%

2 INDIA 1.26B 27% 354M 14%

3 US 322M 86.75% 279M 7%

9 UK 63M 89% 57M 3%

Growth rateINDIA has the highest growth rate 14% and is estimated to increase to 25% in the next 5 years, whereas US,UK and China have a stagnated growth rate.

Market size (Internet users)INDIA has the second highest market size i.e. 354 million beating US this year. Projected to be 500 million by 2017.

MARKET ATTRACTIVENESS

16

What has worked ?(Growth Drivers adopting etailing)Low pricing Increasing penetration of technology

Flexibility in delivery and payment Increase in social media

Connectivity Increasing disposable income

Opportunities – growing market Multiple payment options

Low operation cost Variety of brands

globalization Changing demographics

High real estate cost for Brick & Mortar Economy

17

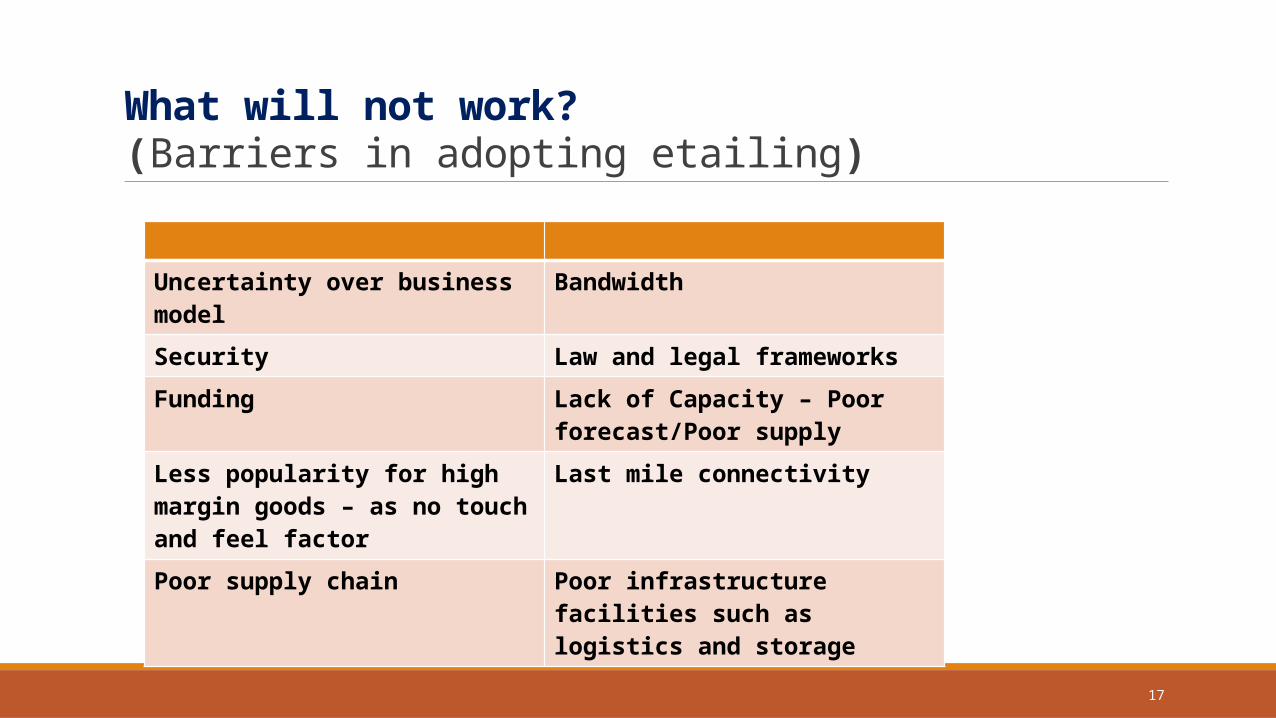

What will not work?(Barriers in adopting etailing)

Uncertainty over business model Bandwidth

Security Law and legal frameworks

Funding Lack of Capacity – Poor forecast/Poor supply

Less popularity for high margin goods – as no touch and feel factor

Last mile connectivity

Poor supply chain Poor infrastructure facilities such as logistics and storage

18

Will it increase in scale? Indian markets are currently operating in quadrant 1 and 4 mainly. Challenge going forward is to add more and more product categories in these quadrants and also to sell categories in other quadrants

•Internet penetration

•Increasing broadband Internet usages (growing at 35% MoM) and 3G penetration.

•Smartphone sales growth

•Fall in smartphone prices.

19

•Increase in organized retail from 8 % to 26 % . Surveys predict that it will have a phenomenon growth by 2020

•Poor penetration of Organized Retail leading to a gap in the market due to unfulfilled needs of consumers, especially in lower tier cities

•Rising consumer confidence in online business

•Rising standards of living with high disposable incomes

•Busy lifestyles, urban traffic congestion and lack of time for offline shopping.

•The enhanced security measures introduced by the Reserve Bank of India

•Winning in India will probably mean Indian companies have to evade the paths where the large US players are Who are deep pocketed and are not investors driven, and build new ones.

•But we now see strategic M&A and VC funding

1. Future group- Amazon

2. Croma- Tata group.

3. Flipkart- Myntra

20

Indian Scenario

21

Trends•Many of the current brick & mortar retailers (both traditional and corporatized) will succeed in viewing e-tailing not as an extension but as an important business growth driver

•Ambient intelligence

•Omni channel

•Increase in organized retail.

•India has the 3rd largest number of Facebook subscribers (fb selling and end to end selling)

• Mobile wallet is gaining prominence

• Similarly, many consumer brands will also build e-tailing businesses as a direct go-to-market approach

•Rising internet connectivity and IOT

22

•Cluster the greater income places and also highly populated places and understand the trends and behavior

•There is going to be less of breakthrough innovation but more of incremental change

•Integrative boxes

•Pay to neighbor

•Click and collect

•Gift wrap

•Amazon dash , prime

CONT…

23

24

Why burn cash?Most b2c ebusiness models have relied initially on an intensive effort to generate a large enough customer base (market share) – Michael porter

E.g. Flipkart – They have actually not made any money – but valuation is huge (unicorn company)

They lose Rs1.7 for every rupee earned

Tradeoff between Growth and Profitability

Why app only ?•Dedicated app

•No third party cookies or ads – focused shopping

•No quick comparison

•Push notification

•Customized offers

•ios 9 has ad blockers

25

Critical factorsSICCustomer experience etailers have to come up with a completely localized strategy-Dilligrocery.com

Tapping the potential of Indian villages (infra , connectivity , transport )

Collaborative model – etailers must collaborate with the best reputed manufactures , suppliers , vendors (probably those who have reached EOS)

People are less forgiving – Flipkart BBDCustomized promotions for certain groups40% of digital advertising is consolidated with two big players - Google and Facebook. Retaining the e-customer ( 80% comes from repeat customer)•convenience,•customization, •selections, •service and delivery•pricing.

26

27

Research to understand whether etailing importance differs across product categories or across countries

Hypothesis

H1 ; etailing importance differs across countries.

H2 ; etailing importance differs across product categories.

28

H1 COUNTRY WISE 1. Country characteristic influencing etailing

It penetration

GDP

Education level

Age

Unemployment

E commerce regulation

Credit card holders

Trade liberalization

2. Categories by countries

BRIC

Developed

Transition counties

Asian countries

29

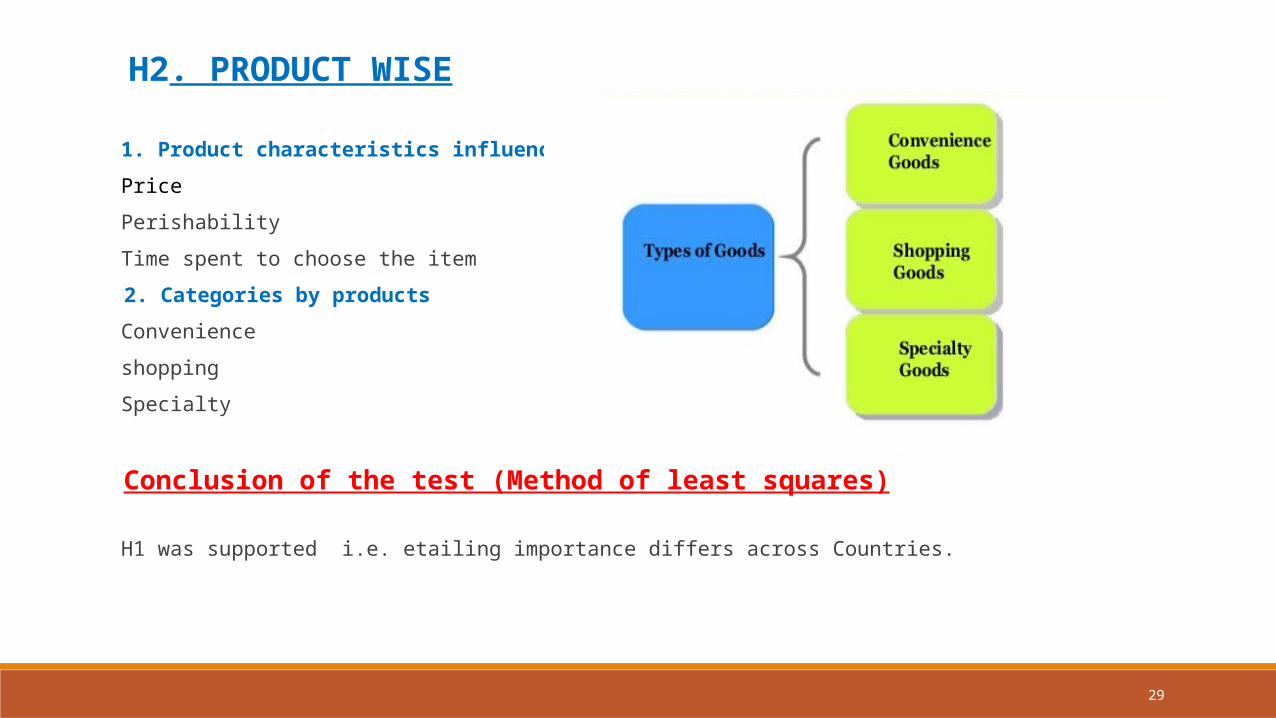

H2. PRODUCT WISE

1. Product characteristics influencing etailing

Price

Perishability

Time spent to choose the item

2. Categories by products

Convenience

shopping

Specialty

Conclusion of the test (Method of least squares)

H1 was supported i.e. etailing importance differs across Countries.

30

Conclusion Success Factors Removing Barriers, focusing on Critical factors, adapting to trends, Pest Analysis along with

•EOB

•GST

•Digital India

•Better regulatory framework

•Analytics (Homeshop18, Jabong, Wipro use Hadoop, SEO, Market basket analysis effectively)

“There is nothing permanent in this world except change”

- Heraclitus

31

Bibliography Journal of Academy of Marketing Science, 30(4), pg.no:296-312.

Michel Levy, Barton A Weitz & Ajay Pandit - Retailing Management, sixth edition(2008), Tata McGraw

Hill, New Delhi.

Zeithaml V.A (2002), “Service excellent in electronic channels”, Managing Service Quality, vol. 12, no.3,

pg no:135-138.

http://www.e-tailing.com/content/?p=1465

http://www.mergers.net/index.php?id=1833&tx_ttnews[tt_news]=2171&cHash=a1551c9cc3cd14bca7c63

05611375dc7

http://www.indiaonestop.com/retailing

http://indianecommercestory.blogspot.in/2010/01/etailing-market-in-india.html (accessed on 10.03.2012, 9.10 pm)

http://www.24dunia.com/english/search/Bata-stores.html