Dr. Colin Lawrence Director, Prudential Risk Division Financial Services Authority Improving...

24

Dr. Colin Lawrence Director, Prudential Risk Division Financial Services Authority Improving Sustainability in Banks Through Liquidity and Capital Management The Asian Banker Summit 2011 6-8 April 2011

-

Upload

gloria-watson -

Category

Documents

-

view

217 -

download

4

Transcript of Dr. Colin Lawrence Director, Prudential Risk Division Financial Services Authority Improving...

Dr. Colin LawrenceDirector, Prudential Risk Division

Financial Services Authority

Improving Sustainability in Banks Through Liquidity and Capital

Management

The Asian Banker Summit 20116-8 April 2011

Past Weaknesses – Liquidity Policy

• No clear articulation of risk tolerance and supervisory objectives

• Maintain going concern, or handle transition to gone concern?

• Took no account of the business cycle

• Underestimated potential stresses

• Cross-border issues not addressed

• Regulatory liquid assets not liquid

Past Weaknesses - Firms

Liquidity risk mismanaged

Governing Body not fully informed

Stress testing inadequate

Liquidity as a profit centre

Transfer pricing

New product approval

Implications for Firms

• Enhanced liquidity risk management capabilities in firms

• Greater use of stress testing

• Testing and improvements to contingency funding plans

• Less reliance on short-term wholesale funding, including from foreign counterparties

• Greater incentive to attract a higher proportion of retail time deposits

• A higher amount and quality of stocks of liquid assets, including a greater proportion of government debt

• A check on unsustainable expansion of lending during favourable economic times

Systems and Controls Requirements

Governing body & Senior management oversight

Comprehensive liquidity risk measurement

Pricing liquidity risk

Intra-day liquidity risk management

Managing liquidity across legal entities, business lines & currencies

Policies to control liquidity risk

Funding diversification

Management of collateral

New UK Regime- will converge into Basel 3

• Systems and Controls

• Adequate Liquidity & Self Sufficiency

• Stress Testing

• Individual Liquidity Adequacy Standards

• New Reporting

http://www.fsa.gov.uk/pubs/cp/cp09_13.pdf

http://www.fsa.gov.uk/pubs/cp/cp08_22.pdf

Sustainable Business Model is Key Starting PointBut Many Different Business Models Suffered in The Crisis

Businesses need to be well run, and the Business Model and Risk Appetite aligned

High Liquidity

Ratios

Crisis Casualties Included:

Small Building Societies

Regional Banks

Large Universal Banks

Investment Banks

Global Players

Domestic Businesses

Illustrative Impact of Cyclical Downturn on Portfolios

Credit Grade

PD LGDCredit

PremiumTransfer

Price

Branch add-on /

yearCoupon

Economic Capital

RAROCRequired

Shareholder Return (IPO)

Economic Value Added

(EVA)1 0.05% 40% 0.02% 1% 0.05% 1.07% 0.30% 16.95% 14% 0.01%2 0.50% 40% 0.20% 2% 0.20% 2.40% 1.84% 10.87% 14% -0.06%3 1.00% 40% 0.40% 3% 0.40% 3.80% 3.10% 12.90% 14% -0.03%4 5.00% 60% 3.00% 4% 2.00% 9.00% 14.45% 13.84% 14% -0.02%5 10.00% 70% 7.00% 5% 4.00% 16.00% 26.19% 15.27% 14% 0.33%

Net total EVA 0.23%

1 0.20% 60% 0.12% 1% 0.05% 1.17% 1.35% 3.70% 14% -0.14%2 2.00% 60% 1.20% 2% 0.20% 3.40% 7.69% 2.60% 14% -0.88%3 4.00% 60% 2.40% 3% 0.40% 5.80% 12.45% 3.21% 14% -1.34%4 20.00% 80% 16.00% 4% 2.00% 22.00% 44.55% 4.49% 14% -4.24%5 40.00% 90% 36.00% 5% 4.00% 45.00% 69.95% 5.72% 14% -5.79%

Net total EVA -12.39%

1 0.03% 40% 0.01% 1% 0.05% 1.06% 0.17% 30.06% 14% 0.03%2 0.25% 40% 0.10% 2% 0.20% 2.30% 1.08% 18.60% 14% 0.05%3 0.50% 40% 0.20% 3% 0.40% 3.60% 1.84% 21.75% 14% 0.14%4 2.50% 60% 1.50% 4% 2.00% 7.50% 9.01% 22.20% 14% 0.74%5 5.00% 70% 3.50% 5% 4.00% 12.50% 16.86% 23.73% 14% 1.64%

Net total EVA 2.60%

Cyclical Downturn

Cyclical Upturn

Base Case

Gains

Losses

Cyclical

User Cost of Credit

Payable to Treasury

CRM Spread

EPS RAPM

• Risk Information• Diversification

EVA

• Growth rate• Business cycle

Fair Value Stock Price

• Investor perception• Market sentiment

Revenue Risk AdjustedRevenue

Shareholder Value

OperatingMargin

CapitalStructure

• Pricing - Spreads - Fees• Product Cost• Overhead

Market Risk

Credit Risk

Operational Risk

Diversification / Concentration

Benefits

• Portfolio div. (inside risk categories)• Strategic div. (across risk categories)

IndustryGrowth

Share ofMarket

• Market Penetration

• Product expansion

New Client

Client Retention

• Product Mng.

• Sales forces incentives

• Selling skills

Client awareness

Product Innovation

Promotion effectiveness

Liquidity Risk

The Critical Link Between Risk and Stakeholder ValueRisk Transformation is What Banks Do…

To understand risk adjusted profitability, a Board has to understand the risks being run

Historic Return on Equity for UK Banks “…as long as the music is playing, you’ve got to get up and dance. We’re still dancing” Chuck Prince 9 July 2007

Average ROE below 10% pa,

volatility low at c.2% pa

Average ROE over 20% pa, c.30%

pre-crisis and volatility much higher

Higher returns even when driven by higher risk & leverage were rewarded by the market

No Business Model is Inherently “Better”…But Some are Riskier Than Others

1. RAROC• Risk appetite• Risk strategy

2. Capital and Liquidity• Appropriate given 1.• Still appropriate under stress?

3. Risk Management & Control• First line of defence• Local level independent challenge essential• Principal agent problems

4. May show 1. does not work given 2. and 3.• Forces correct pricing• Can you create EVA under stress?

5. Complexity & Opacity• If you can’t measure and monitor risk - you should not do it• Regulators must be willing to shut down areas of business

6. Shadow Banking• Unintended consequence of more regulation?• How do we monitor and control?

Key issues to consider:

Basel 3 – More Capital & Higher Quality CapitalReflects Key Regulatory Objective of Increasing Loss Absorbency

Core(at least 50% of T1)

Non-innovative

Innovative (max 15% of T1)

Upper Tier 2

Lower Tier 2(max 50% of T1)

Upper Tier 3

Lower Tier 3(not limited)

Tie

r 1

Cap

ital

Tie

r 2

capi

tal

Tie

r 3

15%

50%

50%

100%

250%

of

Tier 1

capital

Core

Non- core

Tie

r 1

Cap

ital

Tier 2

Tie

r 2

capi

tal

Goi

ng c

once

rn c

apita

lG

one

conc

ern

capi

tal

50%

4.5% 6%

8%

FSA Current Regime Basel 3 proposal

Global minimum liquidity regime also introduced for the first time

• Sensitivity analyses– Large movement on single factor or parameter

• Scenario analyses– Used to assess model risk, effectiveness of potential hedging strategies etc.– Full representations of possible future situations to which portfolio may be subjected– Involves simultaneous, extreme moves of a set of factors– Reflects individual effects and interactions between different risk factors, assuming a certain cause for the combined adverse movements– Used to assess particular scenarios (e.g worst-case)

• Historical– Based on observed events from the past

• Hypothetical– Plausible events that are yet to be realized– Requires expert judgment and analysis – sometimes difficult to link with underlying factors

• Macroeconomic (eg changes in unemployment, cyclical downturn etc)– A shock to the entire economy – Occurs external to firm and develops over time

• Market (eg stock market crash, change in interest rates, shock to credit spreads in a sector)– A shock to the financial and capital markets– May be historical or hypothetical

• Event-driven – Based solely on a specific event independent of the portfolio characteristics– Identify risk sources/events that cause changes in market and effects of these changes on the risk parameters

• Portfolio-driven – Directly linked to the portfolio– Identify risk parameters changes that result in a portfolio change and identify events that cause the parameters to change

• Worst Case/Catastrophe (E.g. terrorist attack, change in regulations)– Event exogenous to market/economy, though impact arises through resulting changes – Often are tied to specific characteristics of portfolio or exposures

Different Types of Stress Tests RequiredForward Looking, With a Focus on Extreme Tails & Points of Weakness

Expectation of Firm’s Stress Testing FrameworkIntegrated with Risk Appetite & Business, Capital & Liquidity Planning

Business strategy

Risk appetite

Business Plan / Operating plan / Corporate Plan

Capital Planning

Stress testing (base &

stress plan)

Mitigation plan

Stage 1

C. Taking actionManagement

actionsRegular

monitoringAmendments to business plan

B. Implementing

Second-order effects

Challenge process

Firm wide and granular

Forward looking

A. EstablishingStress testing programme

Stress testing infrastructure

Policies and procedures

Stress testing governance framework – active Board and senior management ownership and engagement in all stages

Stage 2

ECONOMETRIC / QUALITATIVE ASSESSMENT

STRESSED IMPAIRMENTS YRS 1-5

ST

RE

SS

ED

CO

RE

TIE

R 1 C

AP

ITA

L V

S. T

HR

ES

HO

LD

STRESSED PPI YRS 1-5

STRESSED PPI YRS 1-5

STRESSED PPI YRS 1-5

STRESSED PPI YRS 1-5

STRESSED VALUATIONS YRS 1-5

STRESSED ADJUSTMENTS YRS 1-5

STRESSED IMPAIRMENTS YRS 1-5

PRE-PROV INCOME(PPI)

BUSINESS UNIT 1

BUSINESS UNIT 2

BUSINESS UNIT 3

REVENUE COST

REVENUE COST

REVENUE COST

GROUP

TRADING BOOK STRUCTURED FINANCE, CREDIT, MONOLINES, MARKET RISK

OTHER STRESS PENSION, CONDUCT OF BUSINESS, ETC

IMPAIRMENTS PORTFOLIO 1

PORTFOLIO 2

PORTFOLIO 3

GROUP

LGD

PD

LGD

ELPD

PD

LGD

EL

STRESSED IMPAIRMENTS YRS 1-5

STRESSED IMPAIRMENTS YRS 1-5

CALIBRATION

GDP UNEMPLOYMENTHOUSE PRICES

COMMERCIAL PROPERTY

INTEREST RATES

MACRO ECONOMIC SCENARIO

INFLATION

REVISED CORE TIER 1 YRS 1-5

STRESSED RWAS YRS 1-5EAD, PD, CYCLICALITY FACTOR/ MARKET RISK RWASRWAS

MNGMT ACTION CAPITAL RAISING, DISPOSALS, COST CUTTING ETC

BA

NK

1

BA

NK

2

BA

NK

3

BA

NK

4

BA

NK

5

SYSTEMIC

& PEER

VIEW

EL

1: Agree the macro scenario 2: Macro to Micro

5: Management Actions

3: Stress the Firm

4: Aggregate outcome

Macro to Micro – Vicious or Virtuous Cycle?Threshold Conditions for Intervention & Management Actions Key

YEAR 1 BANK 1 BANK 2 BANK 3 BANK 4 BANK 5CT 1 START YR 1 7.10% 6.30% 8.20% 7.80% 6.20%

PORTFOLIO A -0.1% -0.1% -0.05% -0.05% -0.08%PORTFOLIO B -0.2% -0.2% -0.1% -0.15% -0.12%PORTFOLIO C -5.0% -6.0% -5.5% -4.0% -6.2%PORTFOLIO D -1.0% -0.5% -0.6% -0.4% 0.9%PORTFOLIO E -2.0% -0.5% -1.5% -0.5% -1.5%

CT 1 FINISH YR 1 7.2% 6.5% 8.5% 8.0% 6.5%

YEAR 2BANK 1 BANK 2 BANK 3 BANK 4 BANK 5

CT 1 START YR 2 7.2% 6.5% 8.5% 8.0% 6.5%PORTFOLIO A -0.7% -0.5% -0.6% -0.5% -0.5%PORTFOLIO B -1.5% -1.2% -2.0% -1.0% -1.2%PORTFOLIO C -7.5% -8.0% -8.0% -7.8% -9.0%PORTFOLIO D -2.0% -2.5% -1.8% -1.9% -2.3%PORTFOLIO E -6.0% -4.0% -6.5% -4.0% -5.0%

CT 1 FINISH YR 2 5.2% 5.4% 6.5% 7.0% 4.8%

YEAR 3BANK 1 BANK 2 BANK 3 BANK 4 BANK 5

CT 1 START YR 3 5.2% 5.4% 6.5% 7.0% 4.8%PORTFOLIO A -0.9% -0.6% -0.9% -0.7% -0.6%PORTFOLIO B -2.3% -1.7% -2.9% -1.6% -1.8%PORTFOLIO C -12.0% -9.0% -11.0% -10.0% -12.0%PORTFOLIO D -3.0% -2.2% -2.8% -2.5% -2.5%PORTFOLIO E -7.5% -4.8% -7.5% -4.9% -6.0%

CT 1 FINISH YR 3 2.5% 4.1% 4.5% 5.5% 2.4%

IMPAIRMENTS UNDER STRESSED CONDITIONS

IMPAIRMENTS UNDER STRESSED CONDITIONS

IMPAIRMENTS

PORTFOLIO C

Systemic Risk KPI

Firms to focus on

Micro to Macro - Illustrative Portfolio AnalysisEarly Signalling of Risk via Leading Indicators Key

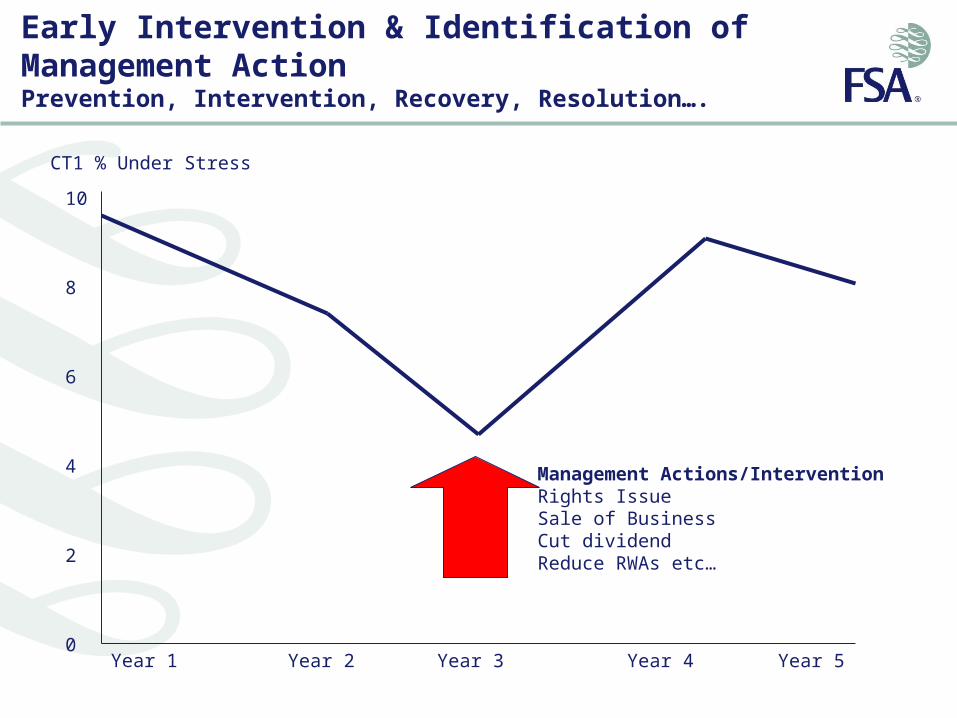

Early Intervention & Identification of Management ActionPrevention, Intervention, Recovery, Resolution….

Year 1 Year 4Year 2 Year 3 Year 5

CT1 % Under Stress

10

8

6

4

2

0

Management Actions/InterventionRights IssueSale of BusinessCut dividendReduce RWAs etc…

Liquidity Stress TestingNeed to Ensure Time For Remedial Action

Cash Flows

Liquidity Position

Profitability

Solvency

Idiosyncratic Stress

Market Wide

Stress

Combination

Stress

Wholesale funding risk

Retail funding risk

Intra-day liquidity risk

Funding diversification risk

Intra-group liquidity risk

Cross-currency liquidity risk

Off-balance sheet liquidity risk

Franchise-viability liquidity risk

Marketable asset risk

Non-marketable asset risk

Short Term & Protracted

Short Term & Protracted

Basel 3 new focus on liquidity, UK regime already implemented

Stress Testing

Cash Flows

Liquidity Position

Profitability

Solvency

Idiosyncratic Stress

Market WideStress

CombinationStress

Wholesale funding risk

Retail funding risk

Intra-day liquidity risk

Funding diversification risk

Intra-group liquidity risk

Cross-currency liquidity risk

Off-balance sheet liquidity risk

Franchise-viability liquidity risk Marketable asset risk

Non-marketable asset risk

Short Term & Protracted

Short Term & Protracted

Includes stress to failure

Hypothetical Comparison of Liquidity Mismatch by Type

Lock Out From Unsecured

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

Lock Out From Unsecured Plus Immediate 20% Outflow of Withdrawable Retail and Corporate Funds

-20%

-15%

-10%

-5%

0%

5%

10%

15%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

Lock Out From Unsecured Plus Immediate 20% Outflow of Withdrawable Retail and Corporate Funds, 75% Free Client & 15% Off Balance Sheet

Lock Out From Secured & Unsecured

-30%

-20%

-10%

0%

10%

20%

30%

40%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

Lock Out From Non Eligible Secured and Unsecured

-20%

-10%

0%

10%

20%

30%

40%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

Lock Out From Unsecured Plus 20% Outflow of Withdrawable Retail

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

Hypothetical Comparison of Liquidity Mismatch by TypeLink to Liquidity Stress Tests and Funds Transfer Pricing is Key

Increasing Stress (1 - 3)

Lock Out From Unsecured

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

Lock Out From Unsecured Plus Immediate 20% Outflow of Withdrawable Retail and Corporate Funds

-20%

-15%

-10%

-5%

0%

5%

10%

15%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

Lock Out From Unsecured Plus Immediate 20% Outflow of Withdrawable Retail and Corporate Funds, 75% Free Client & 15% Off Balance Sheet

Lock Out From Secured & Unsecured

-30%

-20%

-10%

0%

10%

20%

30%

40%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

Lock Out From Non Eligible Secured and Unsecured

-20%

-10%

0%

10%

20%

30%

40%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

Lock Out From Unsecured Plus 20% Outflow of Withdrawable Retail

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

8 Day Mismatch 1 Month Mismatch 3 Month Mismatch

6 Month Mismatch 12 Month Mismatch > 12 Months Mismatch

Bank A Bank B Bank C Bank D

A B C

1 2 3

Decreasing Stress (A - C)

Recovery and Resolution Plans “Living Wills”Regulator Actively Involved Through Supervision & Specialist Reviews

1. Key triggers Breached

2. Key triggers breached

Resolution Plan

OPTIONS• Wind-downs and

disposals• Early equity

injection• Deposit transfer/

Bridge Bank• Liquidation/

Deposit pay off• Share transfer

(Temporary Public Ownership)

Regulator Owns & Executes

Gone ConcernKey elements of Recovery Plan also feature in Resolution Plan

CRISIS

DATA

Going Concern

Bank Owns & Executes

Operational & Legal Structure

CURRENT

• Hold-Co vs. Branches• Segregation of accounts• Single customer view• Booking practices• Infrastructure issues• Local liquidity• Collateral (aggregation,

hypothecation…)• Off-balance sheet items• Cross border complications

TIME

Recovery Plan

Recovery Capital Plan

Recovery Liquidity Plan

Reduce / stop activities

Plan to wind down/liquidate trading book

Bank Owns & Executes

Going Concern

RECOVERY

Plan to sell Businesses/Subsidiaries

Speed MattersMarket May Allow Little Time Between Recovery and Resolution

Mar 16

Bear Stearns, acquired by JP Morgan

Sep 14

Merril Lynch is sold to Bank of America

Goldman Sachs receives support of $5Bn from B. Hathaway Investment

Sep 23Sep 07

Fannie Mae & Freddie Mac are rescued by the FED

Oct 12

Wachovia is acquired by Wells Fargo

2008Sep 25

JP Morgan buys Washington Mutual

Lehman Brothers declares bankruptcy

Sep 15Aug 07

Nothern Rock nationalization

2007

Lloyds take-over HBOS

Sep 17 Oct 13

UK Government rescues RBS

The next crisis will be different – together we are building a global framework that is robust and forward looking

Better Macro & Micro Prudential SupervisionData + Analytics + Judgement Key

• WHAT- Ensure financial stability– Monitor, identify and prioritise systemic risk– Link micro-supervision and macro-economic risks– Consider unregulated parts of the market– Ensure it is somebody’s job to remove the “punchbowl”

• HOW - By getting ahead of the curve – Create counter-cyclical buffers – capital/liquidity in the system should rise as risk rises – Identify leading indicators (data + analytics + judgement)– Clear thresholds for intervention

• ACTIONS - Resolve if necessary– Early action when thresholds breached

• Firm specific (Management actions)• Market wide levers (eg LTV ratios)

– Contingency plans in place – Living Wills– Bail–out to Bail-in– Resolution

Monetary Policy

Macro Prudential Supervision

Micro Prudential Supervision