Liquidity Stress Testing - Pages - Australian Prudential ... Stress Testing Scenario modelling in a...

23

Liquidity Stress Testing Scenario modelling in a globally operating bank APRA Liquidity Risk Management Conference Sydney, 3-4 May 2007 Andrew Martin Head of Funding & Liquidity Risk Management, Asia/Pacific Treasury & Capital Management [email protected] +65 6423 6887

Transcript of Liquidity Stress Testing - Pages - Australian Prudential ... Stress Testing Scenario modelling in a...

Liquidity Stress Testing

Scenario modelling in a globally operating bank

APRA Liquidity Risk Management Conference Sydney, 3-4 May 2007

Andrew MartinHead of Funding & Liquidity Risk Management, Asia/PacificTreasury & Capital [email protected] +65 6423 6887

APRA Liquidity Risk Management Conference · page 2

Agenda

11

22

33

External requirements for liquidity risk management

Stress testing: risk drivers and scenarios

Integrated liquidity risk management process

APRA Liquidity Risk Management Conference · page 3

Increasing focus on Liquidity Risk Management

Basel Committee: Sound Practices (issued in Feb 2000)– Liquidity is crucial to the ongoing viability of any banking organisation

– The importance of liquidity transcends the individual bank since a liquidity shortfall at a single organisation can have systemic repercussions.

Joint Forum: Management of liquidity risk in financial groups (May 2006)– Survey on best practices across banking, securities and insurances groups

IIF Paper: Principles of Liquidity Risk Management (March 2007)– No one-size-fits-all formula for liquidity risk management

– Recommends individual risk management practices and systems to suit the institution, rather than prescriptive, quantitative requirements

– Greater harmonisation of standards and practices among regulators

Developments in the financial markets:– Declining ability to rely on core deposits and increased reliance on wholesale funding

– Technological and financial innovations provided banks with new ways of funding their activities and managing their liquidity

APRA Liquidity Risk Management Conference · page 4

Total current assets / Total current liabilities >= 25%

Liquid assets >= 30% of liabilities in “Foreign currency deposit unit” (FCDU)

Liquid assets / Liquid liabilities >= 1

3 mths assets >= 3 mths liabilities

Liquidity ratios are still common practice …

Liquid assets >= 6% of deposit & borrowing

Liquid assets >= 3-15% of 1wk-3mth deposits (cash flow based)

APRA Liquidity Risk Management Conference · page 5

… however, regulators are increasingly moving towards processes

Hong Kong Monetary Authority: New liquidity risk management framework (June 2005)

Monetary Authority of Singapore: Liquidity Supervision Framework (July 2001 / 2007)

Bangko Sentral ng Pilipinas: Guideline on Liquidity Risk Management (September 2006)

Australian Prudential Regulation Authority: APS 210 Liquidity (September 2000)

Bundesanstalt fuer Finanzdienstleistungsaufsicht: Opening clause for internal bank models under discussion

APRA Liquidity Risk Management Conference · page 6

Rating agencies place increasing emphasis on comprehensive liquidity risk management

For the measurement of banks’ liquidity risk, Moody’s does not rely solely on any numeric indicator and insists on stress-tests demonstrating the capacity of the bank to continue operating over a one year horizon under very difficult market conditions. Moody’s Methodology for Risk Management Assessments of Diversified Global Banking Groups, March 2005

“… the solid liquidity profile and management capabilities are a key determinant of, as much as a crucial prerequisite for, Deutsche Bank’s credit quality. We expect the group to retain a prudent approach to its liquidity and funding.”

Moody’s on Deutsche Bank, August 2006

APRA Liquidity Risk Management Conference · page 7

Agenda

11

22

33

External requirements for liquidity risk management

Stress testing: risk drivers and scenarios

Integrated liquidity risk management process

APRA Liquidity Risk Management Conference · page 8

Liquidity Risk Management framework at DB

Objectives

Balanced liquidity profile of the balance sheetAccess to Capital Markets Funding diversification Support the bank’s credit curve

Access to Wholesale funding- unsecured- securedAccess to liquid assets on the balance sheet

Funding Matrix(Liquidity profile of assets & liabilities)

Central Liquidity PoolSafeguard solvencyIntra-day liquidity Management Maintenance of collateralAccess to Central BanksDaily cash flow projections

Maximum Cash Outflow (MCO) Analysis including limit setting

Stress Testing Analysisincluding contingent liquidity risk

Funding Plan & Issuance Strategy

DB-Toolbox

Unsecured Funding Limits

TacticalLiquidity

StrategicLiquidity

Dimension

OperationalLiquidity

Asset Liquidity Analysis

APRA Liquidity Risk Management Conference · page 9

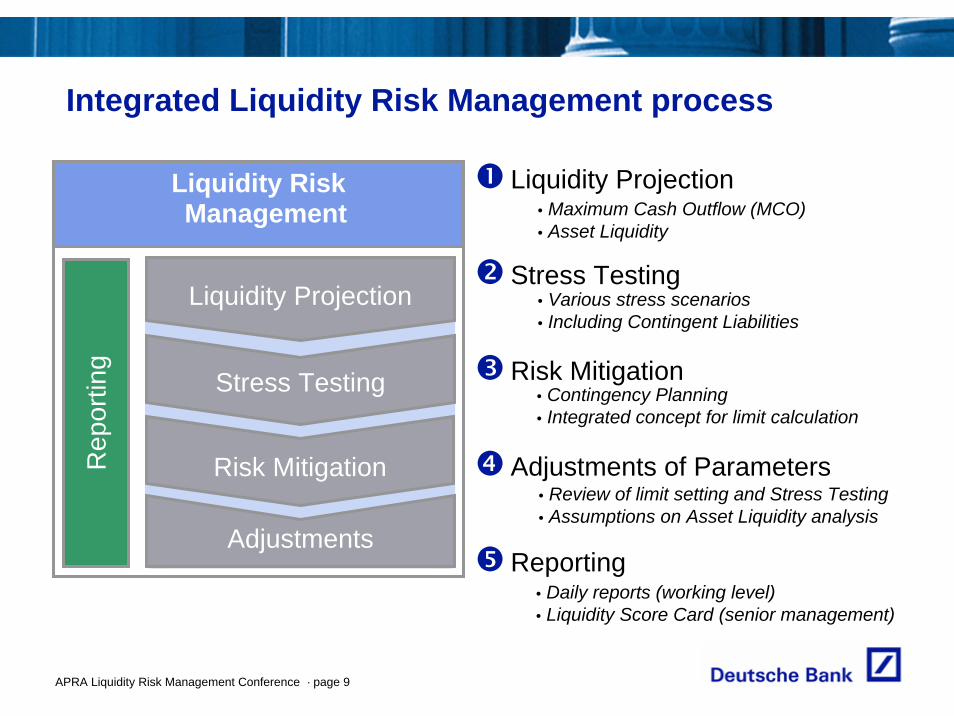

Integrated Liquidity Risk Management process

Liquidity Projection

Stress Testing

Risk Mitigation

Adjustments of Parameters

Reporting

• Maximum Cash Outflow (MCO)• Asset Liquidity

• Various stress scenarios• Including Contingent Liabilities

• Contingency Planning• Integrated concept for limit calculation

• Daily reports (working level)• Liquidity Score Card (senior management)

• Review of limit setting and Stress Testing• Assumptions on Asset Liquidity analysis

Adjustments

Stress Testing

Liquidity Projection

Liquidity RiskManagement

Rep

ortin

g

Risk Mitigation

APRA Liquidity Risk Management Conference · page 10

Local Liquidity Management

Guiding Principle – Liquidity Management is Local

Local Liquidity Managers

Local regulatory framework

Local Liquidity Policies

Local stress parameters

Local cash flow profiles

Local limit allocations

Global Liquidity Management

Global Liquidity Managers

Global Liquidity Policy

Development of methodology

Enhancement of toolbox

Risk appetite

Limit determination

Our global liquidity profile is the sum of local analysis

Consolidation of local analysis

Application of methodology

APRA Liquidity Risk Management Conference · page 11

Cash flows projections for forward looking liquidity management

18 month horizon8 week horizon

Cash inflows

Cash outflows

Cumulative cash flow profile

Net cash flow profile

Daily cash flow projections with 18 month horizon, cash outflow limits are set for the first 8 weeks, recalibrated at least quarterly

Central modelling tool for short-term cash flow modelling

High granularity by product, business line, location and currency

Limit incorporates stress testing through haircut on funding capacity and inclusion of contingent funding requirements

APRA Liquidity Risk Management Conference · page 12

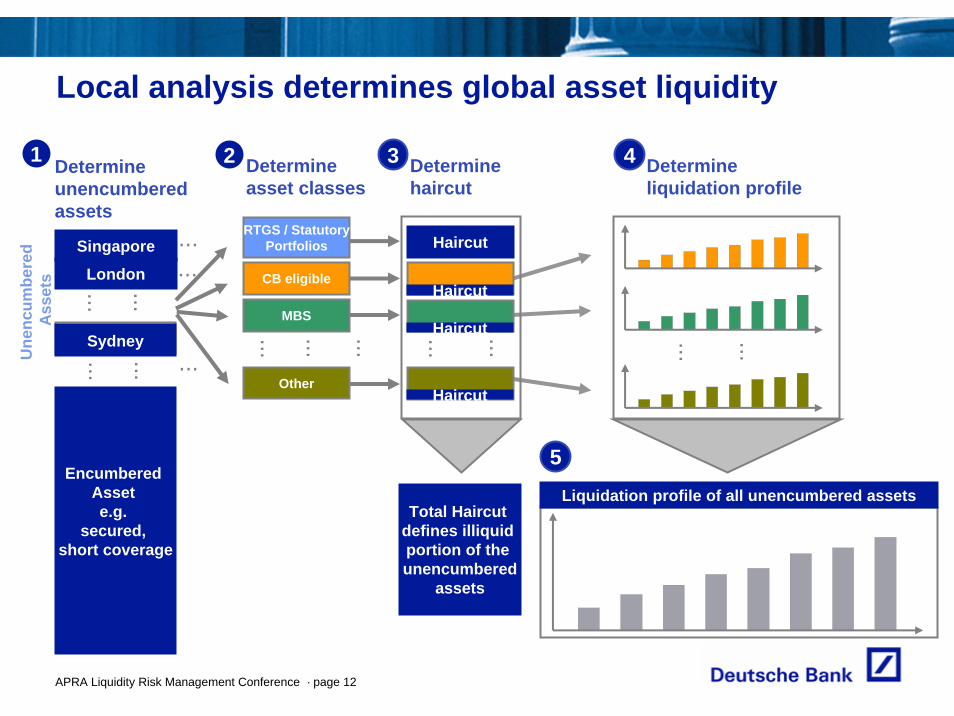

Local analysis determines global asset liquidity

Encumbered Asset e.g.

secured, short coverage

Other

RTGS / StatutoryPortfolios

MBS

CB eligible

Singapore

... ...

Haircut

... ......

Haircut

Haircut

Haircut

... ...

Total Haircut defines illiquid portion of the unencumbered

assets

Liquidation profile of all unencumbered assets

Determine unencumbered assets

Determine asset classes

Determine haircut

Determine liquidation profile

1 2 3 4

5

Une

ncum

bere

d A

sset

s London

Sydney

...

...

...... ...

... ...

APRA Liquidity Risk Management Conference · page 13

Agenda

11

22

33

External requirements for liquidity risk management

Stress testing: risk drivers and scenarios

Integrated liquidity risk management process

APRA Liquidity Risk Management Conference · page 14

Things may seem fine…

APRA Liquidity Risk Management Conference · page 15

… but are they really?

APRA Liquidity Risk Management Conference · page 16

Overview of Stress Scenario Application

Main Objective: Quantify potential liquidity gaps in specified stress scenarios and identify means of closing those gaps

Liquidity Gaps are created by:– Loss of Funding Capacity (e.g. reduction in deposits, CP and CD rollover)– Demand for Liquidity (e.g. funding contingent liabilities)

These Gaps are closed by:– Secured funding or liquidation of unencumbered assets – Reduction of external placements

Analysis of Stress Testing ResultsIf liquidity gap cannot be closed, action must be taken:– Raise term-funding or tap alternative funding sources– Change business structure: e.g. reduce exposure to contingent liabilities

APRA Liquidity Risk Management Conference · page 17

Stress Scenarios

Committed Facilities &Asset Backed Conduits

Additional collateralrequirements

Evaporation of wholesalefunding capacity

Withdrawal of retail deposits

Erosion in value of liquid assets

Liquidity Risk Driver

Externalscenarios

Internalscenarios

Emerging Markets Crisis

Systemic Shock(London / New York)

Market Risk

Operational Risk

Rating Downgrade(1 / 2+1 Notch)

E.g. Pandemic Ad hoc scenarios

Stress drivers and scenarios

Scenarios were defined top-down in co-operation with other risk areas and the Bank’s business divisionsSeveral represent real events that have occurred in the market e.g. 1 notch downgrade and emerging markets crisis Not one size fits all!

APRA Liquidity Risk Management Conference · page 18

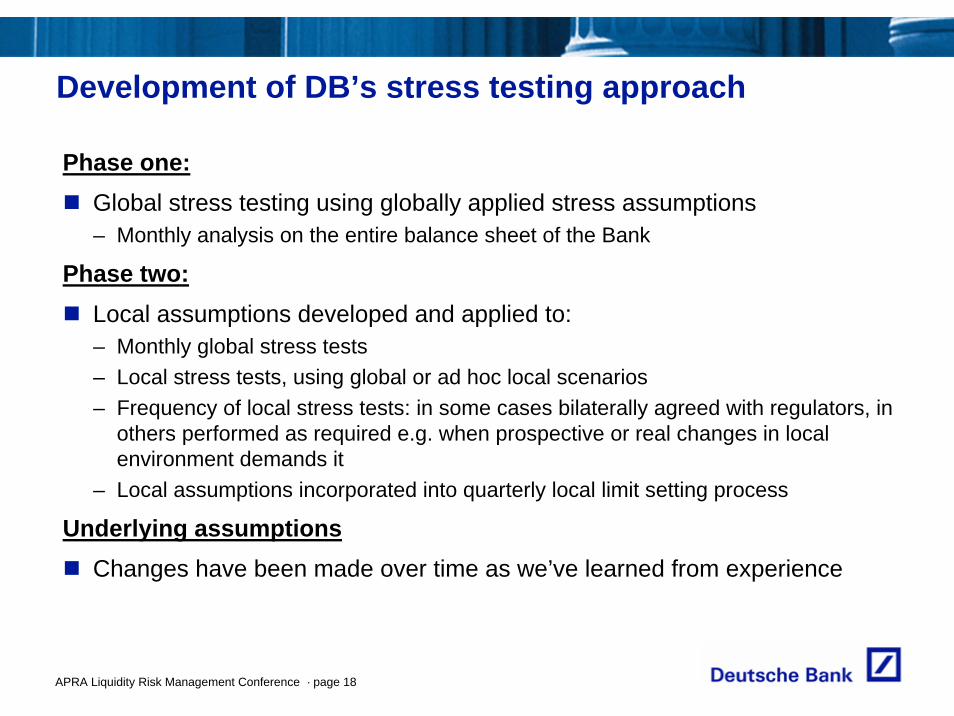

Development of DB’s stress testing approach

Phase one:Global stress testing using globally applied stress assumptions– Monthly analysis on the entire balance sheet of the Bank

Phase two:Local assumptions developed and applied to:– Monthly global stress tests– Local stress tests, using global or ad hoc local scenarios– Frequency of local stress tests: in some cases bilaterally agreed with regulators, in

others performed as required e.g. when prospective or real changes in local environment demands it

– Local assumptions incorporated into quarterly local limit setting process

Underlying assumptionsChanges have been made over time as we’ve learned from experience

APRA Liquidity Risk Management Conference · page 19

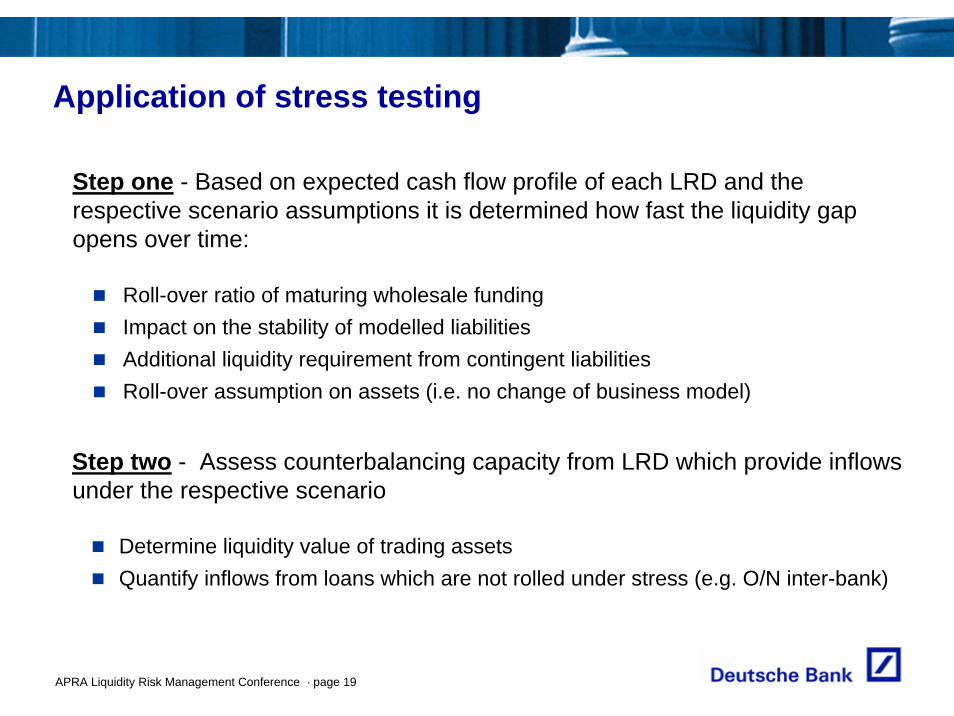

Application of stress testing

Step one - Based on expected cash flow profile of each LRD and the respective scenario assumptions it is determined how fast the liquidity gap opens over time:

Roll-over ratio of maturing wholesale fundingImpact on the stability of modelled liabilitiesAdditional liquidity requirement from contingent liabilitiesRoll-over assumption on assets (i.e. no change of business model)

Step two - Assess counterbalancing capacity from LRD which provide inflows under the respective scenario

Determine liquidity value of trading assetsQuantify inflows from loans which are not rolled under stress (e.g. O/N inter-bank)

APRA Liquidity Risk Management Conference · page 20

Stress testing results

-60,000

-40,000

-20,000

-

20,000

40,000

60,000

80,000 8

Inflows

Outflows

Net Position

Liquidity Risk Driver 1

Liquidity Risk Driver 2

Liquidity Risk Driver 3

Liquidity Risk Driver 4::::::

Liquidity Risk Driver XY

APRA Liquidity Risk Management Conference · page 21

Stress testing output –Matrix of drivers and scenarios

Downgrade to A A2

Systemic Shock

Emerging Markets

Operational Risk

Downgrade to A1

Market Risk

Wholesale funding (excl. O/N funding) - - - - - -Overnight funding - - - - - -ABCP conduit liquidity facilities - - - - - -Clearing balances - - - - - -Fiduciary deposits - - - - - -Collateral requirements from derivative contracts - - - - - -Calls on structured notes - - - - - -Committed facilities - - - - - -Retail funding - - - - - -Small Mid-Cap Deposits - - - - - -

TOTAL 0 0 0 0 0 0

Debt Asset Liquidity - - - - - -Equity Asset Liquidity - - - - - -Maturing Loans - - - - - -TOTAL 0 0 0 0 0 0

Net Liquidity Position 0 0 0 0 0 0

Out

flow

sIn

flow

s

Liqu

idity

Ris

k D

river

s

Stress ScenariosDowngrade

to A A2Systemic

ShockEmerging Markets

Operational Risk

Downgrade to A1

Market Risk

Wholesale funding (excl. O/N funding) - - - - - -Overnight funding - - - - - -ABCP conduit liquidity facilities - - - - - -Clearing balances - - - - - -Fiduciary deposits - - - - - -Collateral requirements from derivative contracts - - - - - -Calls on structured notes - - - - - -Committed facilities - - - - - -Retail funding - - - - - -

- - - - - -

TOTAL 0 0 0 0 0 0

Debt Asset Liquidity - - - - - -Equity Asset Liquidity - - - - - -Maturing Loans - - - - - -TOTAL 0 0 0 0 0 0

Net Liquidity Position 0 0 0 0 0 0

Out

flow

sIn

flow

s

Liqu

idity

Ris

k D

river

s

Stress Scenarios

APRA Liquidity Risk Management Conference · page 22

Contingency Plans

Definition of contingency levels: – no check-list approach, but assessment based on combination of factors

– DB specific or market-wide (currency fluctuations, investment outflow)

Contingency plans incorporate:– different scenarios– liquidity management tools– sources of contingent assets and liabilities– measures to increase liquidity of assets and stability of liabilities

Clear assignment of responsibilities and authorities is required

APRA Liquidity Risk Management Conference · page 23

Cautionary statement regarding forward-looking statements and non-U.S. GAAP financial measuresThis presentation contains forward-looking statements. Forward-looking statements are statements that are not historical facts; they include statements about our beliefs and expectations. Any statement in this presentation that states our intentions, beliefs, expectations or predictions (and the assumptions underlying them) is a forward-looking statement. These statements are based on plans, estimates and projections as they are currently available to the management of Deutsche Bank. Forward-looking statements therefore speak only as of the date they are made, and we undertake no obligation to update publicly any of them in light of new information or future events.

By their very nature, forward-looking statements involve risks and uncertainties. A number of important factors could therefore cause actual results to differ materially from those contained in any forward-looking statement. Such factors include the conditions in the financial markets in Germany, in Europe, in the United States and elsewhere from which we derive a substantial portion of our trading revenues, potential defaults of borrowers or trading counterparties, the implementation of our management agenda, the reliability of our risk management policies, procedures and methods, and other risks referenced in our filings with the U.S. Securities and Exchange Commission. Such factors are described in detail in our SEC Form 20-F of 27 March 2007 under the heading "Risk Factors." Copies of this document are available upon request or can be downloaded from www.deutsche-bank.com/ir.

This presentation contains non-U.S. GAAP financial measures. For a reconciliation to directly comparable figures reported under U.S. GAAP refer to the 4Q2006 Financial Data Supplement, which is accompanying this presentation and available on our Investor Relations website at www.deutsche-bank.com/ir.