DNB GROUP Fourth quarter 2013 results update · PDF fileFourth quarter 2013 results update...

26

4 Fourth quarter 2013 results update Paris, 5 March 2014 Trond Bentestuen, Head of Personal Banking Per Sagbakken, Head of IR/Long term funding DNB GROUP

Transcript of DNB GROUP Fourth quarter 2013 results update · PDF fileFourth quarter 2013 results update...

4 Fourth quarter 2013 results update Paris, 5 March 2014 Trond Bentestuen, Head of Personal Banking

Per Sagbakken, Head of IR/Long term funding

DNB GROUP

Full year 2013 – PTP before impairment NOK 24.7bn (NOK 21.0bn)

EPS and proposed DPS (in NOK)

10.76 (8.48) and 2.70 (2.10)

Cost/income ratio (in per cent)

45.7 (49.1)

ROE (in per cent)

13.2 (11.7)

CET1- capital ratio according to transitional rules and Basel III (in per cent)

11.8 (10.7) and 13.6 (12.1) Figures in parentheses refer to 2012

2 06.02.2014

5.3 (4.6)

Leverage ratio according to Basel III (in per cent)

Stong profit trend in 2013 vs. 2012 driven by: - higher NII and fee income, lower costs and lower loan losses

06.02.2014 3

Full year Full year

Amounts in NOK million 4Q13 3Q13 2Q13 1Q13 4Q12 2013 2012

Net interest income 7 940 7 915 7 480 6 857 7 101 30 192 27 216

Net commissions and fees, core business 1 989 2 057 2 142 1 851 1 896 8 040 7 511

Net financial items 2 329 2 060 2 167 1 831 2 165 8 387 6 990

Net other operating income, total 4 318 4 117 4 310 3 682 4 061 16 427 14 501

Total income 12 258 12 032 11 790 10 539 11 162 46 619 41 717

Operating expenses 5 163 4 987 5 010 5 026 5 220 20 186 20 375

Restructuring costs and non-recurring effects (212) 236 650 8 33 682 98

Expenses relating to debt-financed structured products 0 0 0 450 0 450 0

Impairment losses for goodwill and intangible assets 557 0 0 0 202 557 287

Pre-tax operating profit before impairment 6 750 6 809 6 130 5 054 5 707 24 744 20 957

Net gains on fixed and intangible assets 153 2 (9) 4 (65) 151 (1)

Impairment of loans and guarantees 36 475 937 737 1 190 2 185 3 179

Pre-tax operating profit 6 868 6 337 5 184 4 321 4 453 22 709 17 776

Taxes 1 212 1 448 1 379 1 149 614 5 188 4 081

Profit from operations held for sale, after taxes 9 (7) (7) 10 4 4 96

Profit for the period 5 665 4 881 3 798 3 181 3 843 17 526 13 792

+11%

+7%

+6% ex BS&Nets

+7% ex BS&Nets

+9% ex BS&Nets

-0.9%

+13%exBS&Nets

-30%

+21%exBS&Nets

+27%

Development in loans and deposits

06.02.2014

NOK billion

4

1 2851 309

1 3071 298

1 3151 330 1 333 1 341

1 2851 302

1 309 1 306

1 312 1 314 1 314 1 315

31March

30June

30Sept.

31Dec.

31March

30June

30Sept.

31Dec.

2012 2013

Loans at end of period

Loans adjusted for exchange rate movements

806

854

843811

889

996

925

868

806

850

845

816

886

979

908

845

749

784 785797

810

849831

854

31March

30June

30Sept.

31Dec.

31March

30June

30Sept.

31Dec.

2012 2013

Deposits at end of period Deposits adjusted for exchange rate movements

Deposits adjusted for short-term money market investments

Lending growth YOY +3.3%, FX adj. +0.6% Deposits growth YOY +7.2%

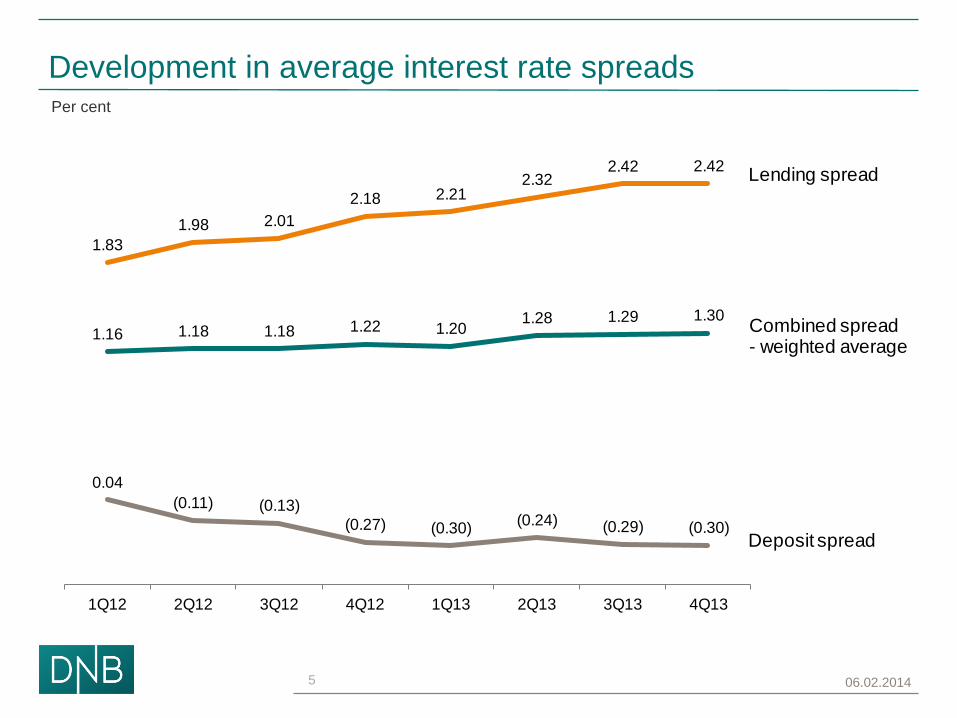

Development in average interest rate spreads

06.02.2014

Per cent

5

1.83

1.98 2.01

2.18 2.212.32

2.42 2.42

0.04

(0.11) (0.13)

(0.27) (0.30)(0.24) (0.29) (0.30)

1.16 1.18 1.18 1.22 1.201.28 1.29 1.30

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

Lending spread

Deposit spread

Combined spread- weighted average

Local access for

> 75% of Norwegian

population

Real-time

response from

our customers

Easy access to

basic banking

services

Over 80% of all

new home-

buyers

Only Norwegian

bank with 24/7

customer service

Extensive customer reach – A foundation for future growth

Online & mobile Call centres Branches Real estate

Points of entry

Weekly visits

Customer reach per channel

In-store banking

6

2.2

2.4

2.5

DNB Nordic upper quartile DNB target

Great potential in leveraging our existing customer base – Key profitability driver

7 Source: Finalta – Nordic Sales Effectiveness Benchmarking 2013

Products per customer Benchmarking Study, average number of products

Opportunities to improve other income

• Non-life insurance products: ~10 per cent of customer base

• Mutual funds: ~ 20 per cent of customer base

• Life insurance/pension funds: ~ 20 per cent of customer base

• Credit cards: ~ 45 per cent of customer base

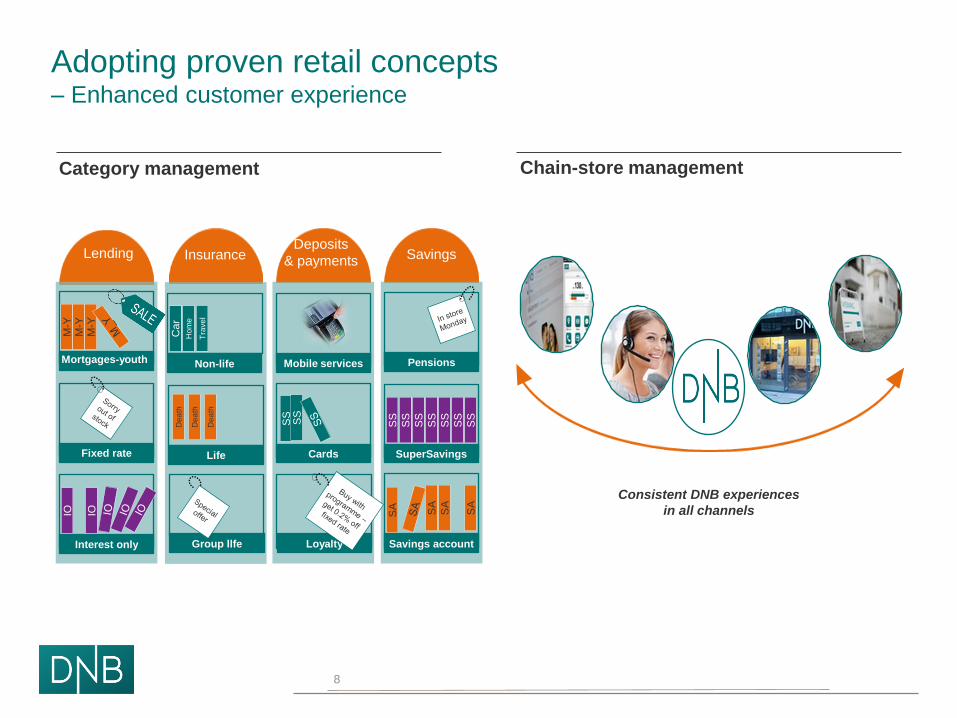

Adopting proven retail concepts – Enhanced customer experience

Category management Chain-store management

Deposits

& payments Lending Savings Insurance

Mortgages-youth

Fixed rate

Interest only

M-Y

M

-Y

M-Y

IO

IO

SuperSavings

SS

SS

SS

SS

SS

SS

SS

Pensions

Savings account

SA

SA

SA

SA

Mobile services

Cards

Loyalty

SS

S

S

Non-life

Life

Group llfe

Dea

th

Car

Hom

e

Tra

ve

l D

ea

th

Dea

th

Consistent DNB experiences

in all channels

8

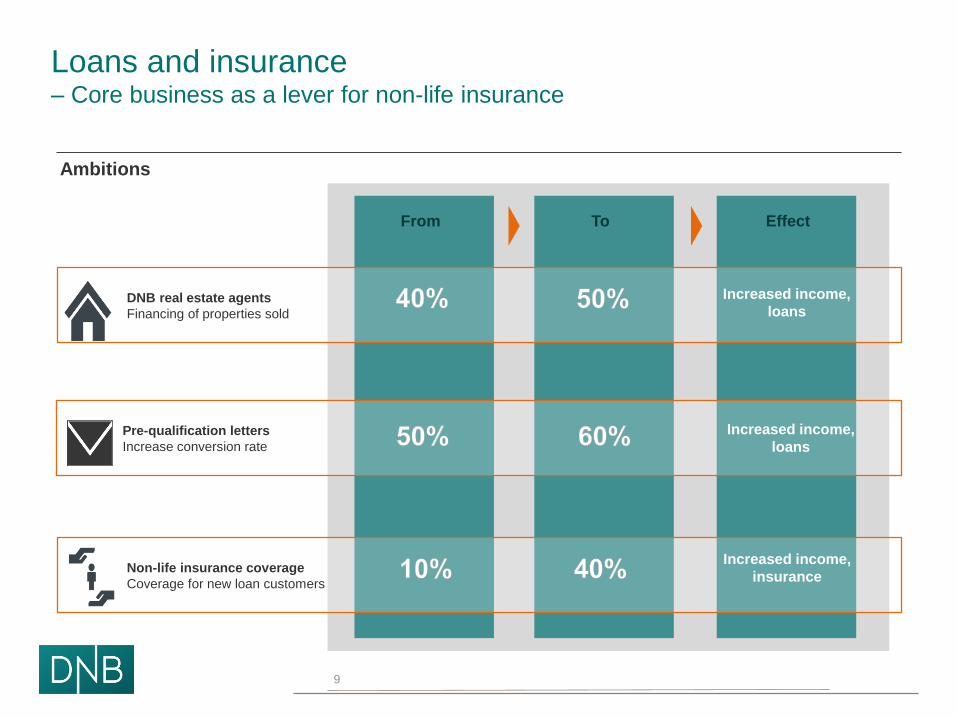

Loans and insurance – Core business as a lever for non-life insurance

Ambitions

Ambitions

To Effect From

Increased income,

insurance

Increased income,

loans

Increased income,

loans

Non-life insurance coverage

Coverage for new loan customers

9

DNB real estate agents

Financing of properties sold

Pre-qualification letters

Increase conversion rate

Savings – Growth driven by the national pension reform

Ambitions

To Effect From

Increased income,

savings

Increased income,

deposits/savings

Cost reductions

& efficient sales

10

Pension schemes

Percentage of customers

with pension schemes

Monthly savings schemes

Percentage of customers

with savings schemes

Consolidation

Number of savings products

Banking services – Focus on efficiency and loyalty programmes

Ambitions

To Effect From

Customer

satisfaction &

effectiveness

Payment cards Loyalty cards

with added value Customer loyalty

Cost reductions

11

Loyalty programmes

Consolidation

Number of products and services

Active mobile bank users

In % of active customers

30

35

40

45

50

55

60

2600

3100

3600

4100

4600

5100

5600

6100

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 2015guiding

2016

Total operating expenses excluding non-recurring effects Non-recurring effects Cost/income ratio - trailing 12 months

Total operating expenses excluding non-recurring effects NOK million, per cent

< 45

Flat average nominal cost (excluding restructuring costs) towards 2016

Cost/income ratio below 45 per cent towards 2016

Continued cost focus to stay

in line with guiding

Cost guiding maintained

12

Reduction in number of FTEs ahead of schedule

13

1) The estimate presented on the CMD was 12 000 full-time positions at year-end 2014.

13,592

12 016

30 June 12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 31 Dec. 13

Full-time positions Reduction in full-time positions

1)

NPLs1) down with sale of shipping assets

14

19.118.4 18.9

16.114.5

19.520.3

19.3 19.6 19.7 19.9

23.3 22.9

20.7

1.711.55 1.56

1.311.14

1.50 1.561.45 1.47 1.50 1.48

1.71 1.70

1.38

1.050.88 0.93

0.69 0.63

1.10 1.181.09 1.09 1.16 1.10

1.37 1.39

1.10

31 Dec. 31 Dec. 31 March 30 June 30 Sept. 31 Dec. 31 March 30 June 30 Sept. 31 Dec. 31 March 30 June 30 Sept. 31 Dec.

2009 2010 2011 2012 2013

Baltics and Poland

DNB Group excl. Baltics and Poland

As a percentage of net loans

As a percentage of net loans excl. Baltics and Poland

Per cent

NOK billion

1) Includes non-performing commitments and commitments subjectto individual impairment. Accumulated individual impairment is deducted.

Impairment of loans and guarantees

15

Full year Full year

Amounts in NOK million 4Q13 3Q13 2Q13 1Q13 4Q12 2013 2012

Individual impairment:

Personal customers

- Mortgage loans 36 15 17 9 7 77 111

- Consumer finance 1) 37 38 121 88 74 284 332

Small and medium-sized enterprises 1) 207 119 156 82 221 564 540

Large corporates and international customers

- Nordic Corporates Division 67 32 61 (24) 27 136 (21)

- International Corporates Divison 86 51 82 8 (18) 228 142

- Shipping, Offshore and Logistics Division (271) 225 198 347 315 500 945

- Energy Division 1) (17) 2 66 1 192 52 230

- Baltics, Russia and Poland 93 189 83 105 133 471 635

- Other units (3) 1 6 0 (2) 4 0

Total individual impairment 236 674 791 616 949 2 318 2 915

Collective impairment:

DNB excl. Baltics, Russia and Poland (171) (174) 173 159 280 (13) 436

Baltics, Russia and Poland (29) (25) (27) (38) (39) (119) (171)

Total collective impairment of loans (200) (199) 146 121 241 (133) 265

Impairment of loans and guarantees 36 475 937 737 1 190 2 185 3 179

1) Impairment for the fourth quarter of 2013 reflects redistributions between the segments in previous quarters in 2013. Impairment figures for Personal

customers, Small and medium-sized enterprises and Large corporates and international customers segments have thus been reduced by NOK 54 million,

increased by NOK 70 million and reduced by NOK 16 million, respectively, in the fourth quarter

50

100

150

200

250

300

1985 1990 1995 2000 2005 2010

Norwegian Real Home Prices, 1985=100 Selected deflators

CPI Disp. Income

Source: EFF/finn.no/EV/SN/DNB Markets

House price growth can be explained by fundamentals

16

* Disposible income per capita deflated house prices

*

Nominal house prices 2000-2013

Norway Sweden UK US Denmark

2000 2002 2004 2006 2008 2010 2012 2013

Housing market: Real demand exceeding supply for several years Annual Figures. 2002-2013 1)

17

The Norwegian residential mortgage market

Source: Finance Norway - FNO

18

Housing market in Norway – turnover and forecast

Estimated for house price inflation

* Norway Statistics. ** Estimate DNB Markets

Year Growth

2011 * +9,0%

2012 * +7,7%

2013 * +4,9%

2014E ** -4,0%

2015E ** -2,5%

2016E ** -1,0%

Residential Properties turnover for DNB

0

500

1000

1500

2000

2500

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

Q406 Q308 Q210 Q112 Q413

Turnover per month (rhs) Growth YoY (lhs)

19

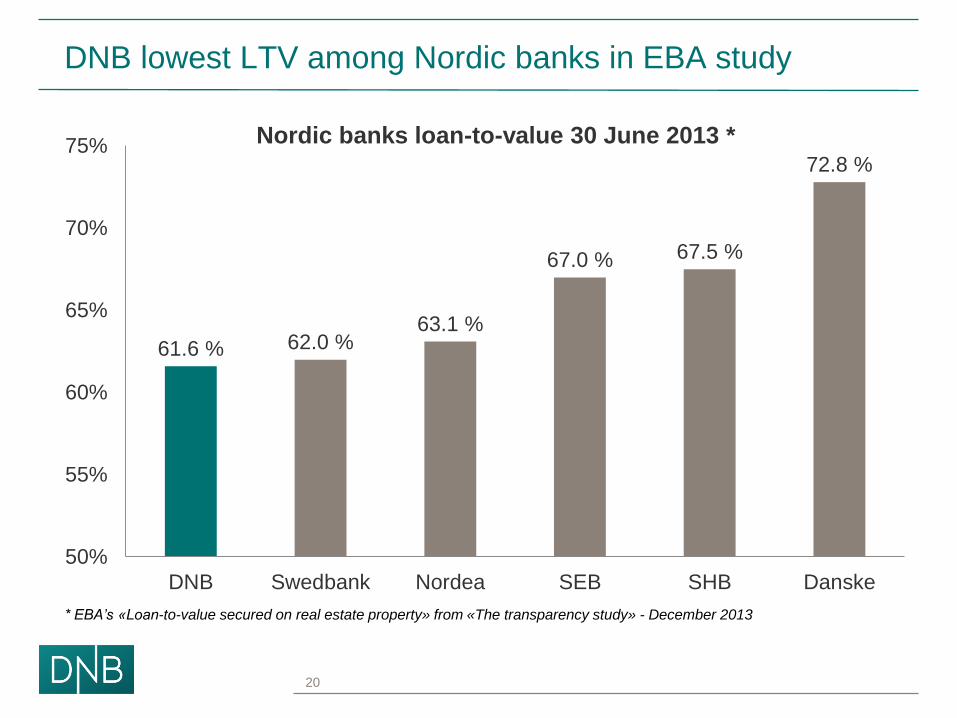

DNB lowest LTV among Nordic banks in EBA study

61.6 % 62.0 % 63.1 %

67.0 % 67.5 %

72.8 %

50%

55%

60%

65%

70%

75%

DNB Swedbank Nordea SEB SHB Danske

Nordic banks loan-to-value 30 June 2013 *

* EBA’s «Loan-to-value secured on real estate property» from «The transparency study» - December 2013

20

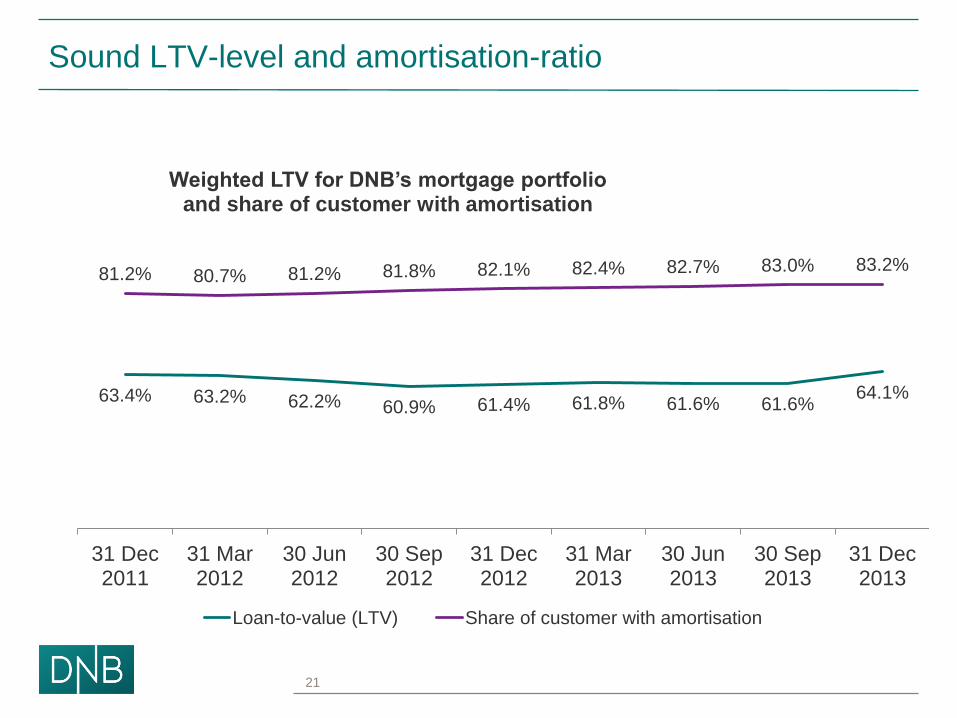

Sound LTV-level and amortisation-ratio

63.4% 63.2% 62.2% 60.9% 61.4% 61.8% 61.6% 61.6% 64.1%

81.2% 80.7% 81.2% 81.8% 82.1% 82.4% 82.7% 83.0% 83.2%

31 Dec2011

31 Mar2012

30 Jun2012

30 Sep2012

31 Dec2012

31 Mar2013

30 Jun2013

30 Sep2013

31 Dec2013

Weighted LTV for DNB’s mortgage portfolio and share of customer with amortisation

Loan-to-value (LTV) Share of customer with amortisation

21

22

DNB is well prepared for a potential negative house price correction

Mortgages are solid:

• All mortgage lending based on cash flow

Low unemployment and good social

benefit schemes makes cash flows robust

LTV levels are robust, average LTV in Cover

pool was 56.3% as of 31 December

Norway has the willingness and ability to

implement counter cyclical policies:

• A Norwegian recession would be softer due

to a likely fiscal stimulus by the Norwegian

Government (as in 2009)

Norway has net financial assets of above

180% of GDP

0.0 %

5.0 %

10.0 %

15.0 %

20.0 %

25.0 %

30.0 %

35.0 %

40.0 %

0-40 40-60 60-75 75-85 >85

LTV

Loan to value bucket

Percentage of

Mortgage book

31 Dec 2013

56.3%

62% 70%

79%

Sensitivity in DNB Boligkreditt for lower house prices

Loan-to-value Stress-scenario (LTV)Potential negative development

in house prices and potential

impact on LTV

Loan-to-value DNB Boligkreditt 2010 - 2013

Robust portfolio in DNB Boligkreditt

37% 33% 27%

17%

30-Nov-10

31-May-11

30-Nov-11

30-Jun-12

31-Dec-12

30-Jun-13

31-Dec-13

-10% -20% -30%

Regulatory overcollateralization (OC) 2010-2013

Potential negative impact

house prices and development

in regulatory OC

23

Expected capital requirements: - CET1=13.5%-14% and Total Capital=17%-18%

24

CET 1 ratio requirements

Per cent

11.8

14.0

12.5

17.0 – 18.0

Total Capital Ratio

31 Dec 2013

Transitional rules

CET1 11.8

Total capital ratio requirements

Per cent

89.6

128.1

8.5% 9.2% 9.4% 10.7% 11.8%

2009 2010 2011 2012 2013

Annual capital accumulationCET 1 capitalCET 1 capital ratio

On track towards reaching our above 12% ROE-target

above 12 per cent

Return on equity

CET1 capital ratio

13.5-14.0 per cent

Requirement

Target

Return on equity Per cent

Capital accumulation and

CET 1 capital ratio (trans.rules) NOK billion

10.6

13.6

11.4 11.7 13.2

2009 2010 2011 2012 2013

25

4 Q&A

DNB GROUP