D_Fryer

21

The Political Geography of International Lending by Private Banks Author(s): Donald W. Fryer Source: Transactions of the Institute of British Geographers, New Series, Vol. 12, No. 4 (1987), pp. 413-432 Published by: The Royal Geographical Society (with the Institute of British Geographers) Stable URL: http://www.jstor.org/stable/622793 . Accessed: 09/01/2015 05:53 Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. . The Royal Geographical Society (with the Institute of British Geographers) is collaborating with JSTOR to digitize, preserve and extend access to Transactions of the Institute of British Geographers. http://www.jstor.org This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AM All use subject to JSTOR Terms and Conditions

-

Upload

hilmi-oelmez -

Category

Documents

-

view

1 -

download

0

description

D Fryer

Transcript of D_Fryer

The Political Geography of International Lending by Private BanksAuthor(s): Donald W. FryerSource: Transactions of the Institute of British Geographers, New Series, Vol. 12, No. 4 (1987),pp. 413-432Published by: The Royal Geographical Society (with the Institute of British Geographers)Stable URL: http://www.jstor.org/stable/622793 .

Accessed: 09/01/2015 05:53

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

The Royal Geographical Society (with the Institute of British Geographers) is collaborating with JSTOR todigitize, preserve and extend access to Transactions of the Institute of British Geographers.

http://www.jstor.org

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

413

The political geography of international lending by private banks DONALD W. FRYER

Professor of Geography, University of Hawaii at Manoa, Porteus Hall 445, 2424 Maile Way, Honolulu, Hawaii 96822, USA

Revised MS received 15 January, 1987

ABSTRACT Bank lending to foreign governments has long been an agent of foreign policy, and for a Less Developed Country (LDC) a private bank loan confers international respectability. After 1970 private bank loans became the largest source of financial inflows into all such countries, except the very poorest. This growth in bank lending was in part a recycling of the large surpluses of oil-exporting developing countries through the sharp increases in oil prices during the decade. More importantly, it arose from the economic and political exigencies of the United States in maintaining leadership of the non- communist world. American banks have thus dominated foreign lending throughout, but have increasingly been chal- lenged by European, Japanese, and other foreign banks. The geographical distribution of private bank loans closely reflects the economic and geopolitical interests of their domestic governments; American loans have gone mainly to Latin America and to 'newly industrailizing countries' (NICs) in Asia, 'middle-income' countries with high annual growth rates of GNP. Rival banks have broadly pursued a similar strategy, so that such borrowers have by far the largest debt service obligations among developing countries, and some are in serious danger of default. Nevertheless, the loans of non-American banks show both vestiges of older commercial or imperial interests, and new patterns unrelated to the past.

KEY WORDS: Banks, Debt, Latin America, Loans, Oil prices, United States, West Germany, Japan

Who hold the world both old and new in pain Or pleasure? Who make politics run glibber-all? The shade of Bonaparte's noble daring? Jew Rothschild and his fellow Christian Baring!

(Lord Byron, Don Juan XII, 5)

The good news is that Chase Manhattan is going to merge with the Polish National Bank. The bad is that Chase is going to run it.

(Wall St. story, 1982)

The Mexican financial crisis of August 1982 and de facto default on obligations to foreign banks marked a turning point in the post-war history of economic and financial relations between the developed and devel- oping worlds. By mid-1984 the approach of another quarterly deadline for the payment by some major debtor LDCs of its debt service was no longer recorded only in specialized technical publications, but had moved onto the pages of the developed world's popular press. In a sluggish world economy

with high unemployment and interest rates, falling commodity prices and the threat of renewed tariff wars, the possibility that a major default could trigger a world depression comparable to that of the 1930s was newsworthy. Many bankers viewed this publi- city as an impediment to accommodation with reluc- tant debtors. But they had the solid support of their own governments, and they looked to their new- found ally, the International Monetary Fund (IMF), to administer the fiscal and financial medicine to debtors to ensure that they paid up.

Yet there was nothing new in the technical default of a borrowing country, although to have a loan de- clared 'non-performing' cuts if off at once from all credit and compels cash-down payments for imports. Several LDCs had been in technical default on their loans from official creditors since the 1950s, some such as Argentina, Indonesia, Turkey and Pakistan more than once, and which had necessitated complex and difficult 'rescheduling' (Franko and Seiber, 1979; Seiber, 1982). Moreover, some of these borrowers

Trans. Inst. Br. Geogr. N.S. 12: 413-432 (1987) ISSN: 0020-2754 Printed in Great Britain

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

414 DONALD W. FRYER

had defaulted on loans in the nineteenth century, and again in the 1930s. What differentiated the crises of the 1980s was the enormous size of debtors' obli- gations to banks in relation to what has traditionally constituted the basis of bank lending, i.e. share- holders' equity, or capital, and customers' deposits. In creating an 'exposure' in which default by a single major borrower could bring down the world's largest banks, commonsense suggests that many bankers had behaved with gross irresponsibility.

While Zaire, Peru, Turkey and a string of east European countries caused the bankers repeated anxiety between 1982 and 1986, the focus of greatest concern shifted from Mexico to Brazil, then back to Mexico as falling oil prices invalidated all forecasts of the country's liquidity position and reinforced general economic mismanagement to plunge the country into the deepest crisis for half a century. Yet despite rumblings of intention to repudiate its obligations, default by Mexico or by any other major debtor at mid-1986 still seemed unlikely; in recent times default has only occurred with major political change and ideological reorientation, as in Cuba, Iran or Indonesia (Gisselquist, 1981, p. 187). Nevertheless, LDC debt to foreign bankers is beyond redemption, as the laws of mathematics operate inexorably to accelerate the interest burden beyond even the most optimistic assessment of ability to pay (Rohatyn, 1986). As it is clear that no government of the developed world can allow a major bank to fail, the real issue is how to apportion the cost of a settlement between borrower, lending banks, and the taxpayers of the banks' home country (Economist, 1986b).

LDC debt has now acquired an enormous literature at academic, official, professional and popular levels. This paper focuses on the political and economic fac- tors that motivated bankers to initiate and develop their spatial patterns of lending, how such enormous loans were made, and what they were used for. Though driven primarily by the quest for profit, bankers through their lending practices also for- warded the political and economic objectives of their domestic governments. Financial power has always supplemented political power and military capability in the struggle for hegemony. Hobson, who coined the term 'financial capitalism', i.e. the banking and broking community, saw imperialism as a conspiracy of capitalists 'to use the machinery of government to secure economic gains outside the country,' and that its necessary consequence 'was a large and ever growing domestic and foreign indebtedness to the

financiers, militarism and war' (Hobson, 1938, pp. 46, 94). From this Lenin argued that, 'finance capitalism' led inevitably to struggle among the Powers for the political division of the world into colonies and col- ony owners, in which even apparently independent countries became 'enmeshed in a network of diplo- matic and financial dependence' (Lenin, 1934). Nearly half a century later 'dependence' was implicit in the attacks of President Nkrumah of Ghana on 'neo- colonialism', in the almost identical nekolim oratory of Indonesia's President Sukarno (Sievers, 1974), and with further theoretical underpinnings became the 'dependency' theory of Latin American academics and officials (Prebisch, 1949; Frank, 1967; Furtado, 1970). The Hobson-Lenin model of financial imperi- alism still has advocates (Forbes, 1983; Trainer, 1985); however, Johnson argues that with the possible exception of Japan, the model bears little relevance to the development of any empire. His observation that 'the most consistent single characteristic of European investors throughout the colonial period was ignor- ance, based on laziness' (Johnson, 1983, pp. 153-5) finds a striking modern parallel in the incredible behaviour of American bankers in the 1984 collapse of Penn Square, an obscure Oklahoma bank that nearly brought down Continental Illinois and several other major banks (Dutcher, 1985; Singer, 1985). Every international loan or investment is a political act (Gisselquist, 1979, p. 99), but bankers pay most court to their governments when they seek rescue from the consequences of their folly.

THE ORIGINS OF INTERNATIONAL BANK LENDING

'Loans have been the stuff of international politics for nearly all recorded history' (Kelley, 1978); the Medicis and the Dukes of Burgundy, the Fuggers and the Hapsburgs, Disraeli and Rothschild, and Bismarck and Bleichr6der, are but some of the better known connections between major political figures and bankers. In the latter half of the nineteenth century private loans to foreign governments played a vital role in the creation of rival imperialisms as 'lending countries gradually came to envisage the foreign investments of their citizens not as private financial transactions but as one of the instruments through which national destiny was to be achieved' (Feis, 1930). This was 'portfolio' investment; the bankers largely acted as agents in selling bonds of foreign state or undertakings to private individuals. If the

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

International bank lending 415 risk of default was sometimes high, so was the rate of return to the bondholders and the fee to the managing bankers.

The geographical distribution of foreign lending before 1914 showed a strong coincidence with the geopolitical interests of the Powers. British invest- ment, the largest and most widespread, was heavily concentrated in the United States, in the Dominions and dependencies, and in Argentina, where strong interest in railroads and export industries, and sub- stantial British immigration, promoted an image of Argentina as the 'Sixth Dominion'. French lending in contrast, was less heavily oriented towards its extensive colonial possessions. Eastern and Southern Europe, and in particular Imperial Russia, dominated French loans, where they supported diplomatic efforts to contain the rising political and economic strength of the German Empire, through building up Russia's rail network and heavy industries (Gisselquist, 1981, p. 42). Germany in turn pursued its Drang nach Osten through loans focussed mainly on Austria-Hungary, the Balkans, and Turkey. United States foreign lending, though small in comparison with that of the European powers, showed a strong orientation towards the western hemisphere, and to Mexico in particular.

The end of World War I left Europe with tremen- dous inflation, indebtedness, and conflicting financial claims as the Allies sought to collect on their loans to each other, to recoup from defeated Germany, and to restore the fixed exchanges of the gold standard that had characterized the expanding economy of the pre- ceding century. Ludendorff's Germany fought the war through a 'state socialism' derived from Imperial Russia, and later copied by Lenin, but the European Allies helped finance the war effort through US loans, which transformed the country from a debtor to the world's largest creditor. Official American loans ceased with the collapse of Wilsonism, and the new administration insisted on repayment of war debts. This policy had no chance of success. To collect from Germany as the Allies hoped, would have necessi- tated an enormous increase in German exports which no Ally was prepared to concede, while Germany itself resisted payment of reparations whose magni- tude remained indeterminate, itself a consequence of the unsatisfactory manner in which the Versailles settlement came to be signed by the German delegation (Johnson, 1983, pp. 34-5, 109-10).

The question of debts and reparations, inflamed by an unsound polemic from Keynes (Keynes, 1919; Mantoux, 1946), bedevilled world finance until the

Great Depression and the repudiation of Versailles by Hitler. In effect, private loans raised in the American market financed virtually all payments of war debt and reparations, for throughout the 1920s the Federal Reserve viewed cheap money and large foreign loans as desirable for the stability of the world economy. In addition to loans to Europe, a new field for the American bankers, large loans were also made to Latin America, -many of which were basically unsound or the subject of malfeasance. In the general abandonment of the gold standard in the financial collapse of the early 1930s and the catastrophic fall in commodity prices, virtually all Latin American deb- tors defaulted, and were promptly followed by the European debtors. These however, were prompted not by inability to pay, but through the desire to create their own autarchic trade blocs with the col- lapse of the multilateral, largely free trade, world economy (Gisselquist, 1981, p. 42).

The bankers undoubtedly shared responsibility for the onset of the Great Depression, but as with all climacterics of modern history, its causes were multi- faceted and deep seated, and will probably never be the subject of consensus (Galbraith, 1972; Kindleberger, 1973; Brunner, 1981, Garraty, 1986). The US government by its tacit approval of stock market speculation through inflation and cheap money, the Hawley-Smoot tariff of 1930, France's deep-seated fear of a German revanche which drove it to destroy Germany's credit-worthiness in 1931 (Gisselquist, 1981, pp. 67-70), the failure of Versailles and the League of Nations, all shared in the debacle. But for the greatest disaster to befall the United States since the Civil War the bankers incurred maximum odium, and their guilt seemed confirmed in mass failures which culminated in the virtual shut-down of the entire banking system in early 1933. The new Roosevelt administration determined to shift the locus of financial power from Wall St. to Washington, and to keep the bankers firmly under control through new restrictions and regulatory agencies. The political and economic standing of the bankers was destroyed for more than two decades.

After World War II the United States had both the resources and the will to create a new multilateral free-trade economic order, and under its hegemony. Europe's rehabilitation through the massive Marshall Plan set the pattern for the subsequent use of foreign aid programmes to further ideological and strategic ends, and with colonial devolution the United States extended its interests in the former dependencies of its Allies. Unfortunately, the farsighted policy of

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

416 DONALD W. FRYER

providing outright grants for European reconstruc- tion was not followed in programmes for newly inde- pendent countries, where aid was largely in the form of loans. The Mutual Security Acts, which channelled aid to countries perceived threatened by communist subversion, compounded this error.

For several years after World War II private finan- cial flows to developing countries consisted mainly of direct investment by corporations, and export credits granted by banks for financing foreign trade. Orig- inally small in relation to the official credits of trade promoting agencies of donor countries, in the 1960s private export credits at short or medium term and stiff rates of interest, grew rapidly. Export credits went largely to oil producers and middle income countries, i.e. those with a per capita GNP above $500 per annum; such credits then constituted more than a quarter of the total external debt of Argentina, Peru, South Korea, and of several West African countries (Pearson, 1969, p. 119). United States par- ticipation in private export credits was initially modest. European nations and Japan led in this new bank lending, which reflected these countries' econ- omic resurgence and their struggles with each other and the United States for new markets for their expanding industries (Gisselquist, 1981, p. 130). The United States government on the other hand, actively encouraged American corporate investment in the former colonial possessions of its Allies, and wherever possible, tailored its own aid programmes in support of large private investment, as was the case with the Volta river scheme and Kaiser Aluminum in Ghana.

Yet the share of private investment in capital inflows into newly independent countries speedily declined as so many followed Latin America in reserving more activities to national entities, or to joint ventures in which multinational corporations (MNCs) could hold only a minority equity. American and European manufacturing corporations have much

preferred to invest in each others' home territories, a

pattern that increasingly holds for those engaged in extractive industries also (McConnell, 1980; Rees, 1985; Hamilton, 1986); only Japan has steered the greater part of its foreign investment to the devel- oping world (Fuchs, in press). Better to serve traditional corporate customers, American banks hastened to extend their overseas branches, but they were also impelled by growing domestic competition and above all, by the desire to participate in the bur- geoning Eurodollar market in less regulated European financial centers.

The origins of the Eurodollar market are obscure, but its main focus has been London since it first clearly emerged in the 1950s (Einzig and Quinn, 1977; Aronson, 1977, p. 50; Delamaide, 1984, pp. 40-6). Ironically, both China and the USSR were involved since both feared blocking of their dollar holdings in the United States itself, and so chose to shift them to Paris and London banks (Lomax and Guttman, 1981; Sampson, 1981, p. 109). Meanwhile massive overseas investment by US corporations, particularly the oil companies, and the immense American aid and over- seas military expenditure, swelled prodigiously the dollar holdings of foreigners.

To finance such capital outflows required a large balance of trade surplus, but in the 1960s, through growing competition in export markets from Europe and Japan, the EEC's agricultural policy, and increasing expenditure on the Vietnam War, the large surpluses of the previous decade disappeared. To preserve the Bretton Woods system of fixed exchanges established in 1944, the United States imposed a series of measures to restrict imports and capital outflows, and to raise the cost of foreign borrowing. Ironically, this policy served only to exacerbate the drain; in their overseas branches American banks were exempt from such regulations, and could circumvent others. Simultaneously, there occurred a revolution in banking practice fraught with immense consequences for the developing world. In 1967 First National City Bank of New York became Citicorp in order to transform the traditional functions of banking into those of a financial inter- mediary, or 'money centre bank' making loans not on the basis of its own deposits and equity, but on purchased funds (Mayer, 1984; Lombardi, 1985; pp. 74, 100). Within a decade, every major world bank had adopted the Citibank model.

As the world moved from the post-war dollar shortage to dollar oversupply, there followed the 'failure of trilateralism' (Gisselquist, 1979), i.e., grow- ing dissension between the United States, Western Europe and Japan over trade and financial matters. Success in export markets, often at the expense of the United States, had given to West Germany and Japan large and growing balance of payments surpluses, which the United States sought anxiously to reduce by persuading its Allies to inflate their economies and to import more. In this it was largely unsuccessful, but its use, or misuse, of energy policy to further this objective precipitated a series of crises in the world economy, and greatly reinforced the consequences of the banking revolution. The price of oil was also

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

International bank lending 417

under attack from the enormous 'shut-in' surpluses of Middle East and North African fields, an erosion that the Organisation of Petroleum Exporting Countries (OPEC), created in 1960, was pledged to resist. By 1970, pressure in the American oil industry for official action to raise oil prices was also strong, and higher oil prices had many attractions for the Nixon adminis- tration. They would greatly increase the contribution to the balance of payments from the American oil companies' overseas operations. Oil prices have been nominated in dollars since the industry began; American banks could expect to be the principal depository for the swollen incomes of OPEC. Iran could finance its ambitious programme to become a major power in the Middle East and Indian Ocean, a policy that the United States actively supported to fill the power vacuum created by Prime Minister Wilson's withdrawal of British forces under the 'east of Suez' policy. Moreover, cheap Middle East oil, largely denied to the United States through the quota programme imposed by President Eisenhower to protect high-cost domestic oil producers, had greatly assisted the competitive position of European and Japanese export industries. Higher oil prices would hit commercial rivals whose dependence on imported energy was higher than that of the United States; American exports could thus regain a cost advantage, and promote the balance of payments surplus necessary for the implementation of foreign policy.

Whether or not the Nixon administration deliber- ately encouraged OPEC to raise prices, many European officials and academics had no doubts about the matter (Taki Rifai, 1972; Oppenheim, 1976; Gisselquist 1979; O'Dell, 1982). If it did, the policy also hastened the oil companies' loss of managerial control in host countries, and failed to promote greater domestic energy self-sufficiency. But over the 1970s the United States reversed the decline in its share of OECD area exports, and the gains to American banks were enormous. These however, could not save the dollar. In 1971 President Nixon cut the link between the dollar and gold, signalling the abandonment of the fixed-exchange Bretton Woods system. This 'Nixon shock', and the five-fold increase in oil prices of 1970-73 seriously impacted on Official Development Aid (ODA) as donor countries sought to minimize the charge of their aid pro- grammes on their balance of payments, and in 1972 the Nixon administration urged that aid should be restricted to the poorest group of countries; LDCs that were credit-worthy should apply to multilateral

agencies such as the World Bank, or to private sources of credit (Gisselquist, 1981, pp. 142-4).

The administration thus tacitly assured the American banks of its protection in any problems arising from foreign lending, and as their deposits swelled from the ballooning incomes of OPEC, the banks needed little further bidding. Moreover, a com- modity boom in the late 1970s assisted a general inflation prompted by the energy crisis, so that oil prices fell in real terms. Exports of 'big ticket' items financed jointly by official export credit agencies and private banks increased sharply. ODA on the other hand grew slowly, so that inflation kept its real value almost constant, and its share of financial flows to LDCs fell from nearly 40 per cent in 1970 to scarcely 30 per cent in 1981 (OECD, 1983, pp. 52-3). In the decade after 1973 commercial banks provided more than two-thirds of the inflow to Latin America, and rather less than this figure to LDCs as a whole (Kuczynski, 1983). But if the barikers had regained the status lost in the Great Depression, they had little time to enjoy it. Between 1980 and 1985 some 40 LDCs made agreements for, or had requested, rescheduling of their private debt, most of which had been contracted during the 1970s (Lombardi, 1985, p. 74).

THE NATURE OF INTERNATIONAL LENDING BY PRIVATE BANKS

The world's biggest debtors to foreign banks are the developed countries; in 1983 Britain owed almost twice as much as Mexico to American banks (FFIEC, 1983). But this is illusory as lending among devel- oped countries is largely an inter-bank matter. Essentially banks have become money brokers, 'inter- mediating' their loans, i.e. covering themselves in lending long by short term 'rollover' borrowings, and ensuring that loan commitments already made can be funded. It is an inevitable consequence of the concept of 'money centre' banking made possible by bank deregulation and an enormous volume of largely uncontrollable Eurocurrency deposits, and by vastly improved telecommunications and data processing systems, which with new 'offshore' banking centres together constitute a 24 hour world-wide market in which the daily turnover of currency dealings can attain $200 billion (Economist, 1985). Governments of OECD countries of course, can easily raise private loans whenever they please; in 1984 New Zealand, Sweden and Ireland negotiated large loans at fine

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

418 DONALD W FRYER

margins over the London three-month Eurodollar rate, or London Interbank Offer Rate (LIBOR), despite external debts that proportionately to their GNPs were equivalent to those of developing countries now of greatest concern to foreign creditors (Economist, 1984e).

Banks loans to LDCs, on the other hand, are primarily directed towards central and local govern- ments, and to other state bodies, especially oil enti- ties. This is particularly true of the largest, and mainly Latin American borrowers, for whom in 1983 such loans accounted for some 40-45 per cent of their national totals. Mexico is unique in that some 25 per cent of foreign bank loans, an unusually high pro- portion, were made to private borrowers. Lending long but borrowing short violates the canons of banking practice; hence bankers shift risk onto their sovereign borrowers by shortening maturities and charging variable rates of interest reflecting their cost of funds. This growing dominance of the short term loan at variable rates had explosive consequences.

Private bank lending to LDCs takes three principal forms. Despite the debt warnings of the Pearson Commission (Pearson, 1969, p. 120-1), official export promoting and credit agencies such as the US Exim Bank, Britain's Export Credits Guarantee Department (EGCD) and France's Comite' Francaise pour I'Assurance du Commerce Exthrieur (Coface), have continued to lead syndicates of private banks to finance the export of jet aircraft, nuclear and other power plants, refineries and oilfield equipment, steelmills and the like. Only too often these 'top of the line' items are ill-suited to local needs or human and material resources, and uncom- petitive prices are concealed in attractive financial packaging. National entities in LDCs find such wares irresistible, but their high sophistication and oper- ational difficulties often result in large losses and under-utilization. Such is the price many LDCs pay for their rejection of foreign MNCs. The failure of trilateralism greatly expanded this reckless export promotion, the most notorious offender being Japan, which has the advantage of lower domestic interest rates than its rivals, a consequence of a very high rate of saving in which tax-exempt Post Office Savings play a significant role.

Second, banks lent directly to governments for general or unspecified purposes. Some newly inde-

pendent countries such as Jamaica, released from the balanced-budget constraints of colonialism and wishing to use Keynesian deficit financing for devel- opment, used bank loans for balance of payments purposes from the beginning (Bernal, 1985). LDCs

also turned increasingly to bank loans to finance import-substitution development strategies, and in the later 1970s such lending grew enormously as banks 'recycled' the OPEC surpluses. Most loans were at first geographically restricted, but under the Citicorp concept of 'actuarial risk' or 'insur- ance banking', and soon adopted by competitors, the range of borrowers widened progressively. Sovereign countries could not disappear or go bankrupt, Citicorp argued, but as they could default or fail to generate the foreign exchange to make payment their credit-worthiness had to be evaluated, and any individual risk reduced by lending to a multiplicity of borrowers in the actuarial manner of insurance companies. Thus originated 'country risk analysis', in which numbers cranked out by social scientists unacquainted with the countries under review, replaced the deep personal knowledge and experience of the traditional banker, in order to establish country loan quotas (Nagy, 1979; Carvounis, 1985, pp. 46-51; Haner and Ewing, 1985; Krayenbuehl, 1985) which were then filled by little better than travelling salesmen who pressed their loans on Ministries of Finance (Sampson, 1981, p. 291; Delamaide, 1984, pp. 43-4). Given wide- spread and virtually institutionalized corruption in every LDC, such offerings were seldom refused, and the protestations of multilateral monitoring agencies to the contrary, malfeasance and waste were enor- mous (Lombardi, 1985, pp. 86-7). Finally, for large countries with a wide range of resources, or for major oil producers, there appeared the syndicated 'jumbo' loan, sometimes of more than $1 billion, managed by a leading commercial or investment (merchant) bank and subcontracted among a multiplicity of lenders, Eurocurrency edificies recorded in so-called 'tomb- stones' in the technical press (Abbott, 1979, p. 77, Sampson, 1981, p. 115). First made at a margin above LIBOR, in the late 1970s the American prime rate was increasingly substituted in such loans, a change that preserved the prestige of a country not deemed creditworthy for a fine margin and usually more

profitable for the banks (Seiber, 1982, p. 87). Though international lending is essentially for big banks, whose risks are offset because no home government can let a major bank fail, syndication made partici- pation possible for smaller banks, and for those in countries that possess no 'big league' banking estab- lishments. For the smaller US banks in particular, such lending was a profitable escape from growing dom- estic competition from new conglomerate financial institutions and 'non-bank' banks.

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

International bank lending 419

Third, the banks' overseas branches made loans in local currencies to both public and private sectors. For the largest American banks, which by the later 1970s derived some 20 per cent or more of their total earn- ings from Latin America, the magnitude of such loans unquestionably means that the total indebtedness of borrowers is still greatly underestimated. Insofar as Head Offices wish or are able to repatriate the profits of subsidiaries, such loans also generate a charge on the borrower's balance of payments.

Retribution for such prodigality was swift. Follow- ing the Iranian revolution of 1978-79, LDCs suffered a triple blow from greatly increased oil prices, from a commodity slump that within five years drove some of their export prices lower in real terms than in the Great Depression, and from a catastrophic increase in their debt service changes. By 1983, virtually all short term, and nearly half the medium (three-five year maturity) and long term debt of LDCs was at floating rates, and as astronomical American budgetary and balance of trade deficits drove the prime rate to unprecedented levels, every percentage point in- crease raised LDC service on medium and long term debt alone by some $1-2 billion (IBRD, 1983, p. xiv). The debt problems which had rumbled on for a decade as various borrowers underwent the traumatic process of rescheduling under the aegis of the IMF, usually with accompanying 'IMF riots', suddenly became a major crisis through the possible default of a major borrower, or worse as Latin American countries threatened in 1984 at a Cartagena confer- ence, by major borrowers in concert. The anxiety moreover, was essentially over the private debt, i.e. interest and amortization payments on bank loans. This not only reflected the fact that LDCs debt to private creditors greatly exceeded that to govern- ments and multilateral institutions. The bankers claimed priority in payment and their governments and the IMF supported their claim. Times had changed since President Roosevelt on learning from Dr. Schacht in 1933 of Germany's intention to default had remarked 'Serve the Wall Street bankers right!' (Schacht, 1955). Private loans were again an important adjunct to national economic and foreign policy.

The total magnitude of foreign lending by private banks can never be known exactly. Short term debt, the category that grew most quickly in the later 1970s, is particularly difficult to assess, and it was the largest borrowers that made the greatest use of such instruments. Statistics kept by multilateral monitor- ing agencies, the World Bank and IMF, the OECD,

and the Bank of International Settlements (BIS) vary widely in coverage and in definitions of the categor- ies of financial flows, as each produces what best suits its own purposes. Some LDCs still make only token efforts to collect and consolidate data of foreign bor- rowing, as did the Philippines (Economist, 1984c). Banks themselves are traditionally secretive; 'American banks have always claimed to be better judges than their governments of what the national interest mandates should be kept concealed' (Sherrill, 1983, p. 464). The central banks of the industrialized world report bank foreign lending to the BIS, which they own, and since 1974, the BIS has published pro- gressively more detailed information on such flows. Of the BIS members, however, only Britain and the United States regularly publish detailed figures of their private banks' external lending. In 1986 the World Bank published its first estimates of short-term debt, whose omission had resulted in a gross under- estimation of the gravity of LDCs' debt situation (Gisselquist, 1981, pp. 179, Dennis, 1984, p. 206). Morgan Guaranty, a leading American investment bank, also publishes from time to time its own esti- mates of bank foreign lending. Nevertheless, although there is now an enormous and bewildering amount of statistical information on international lending, 'it is difficult to gain a clear and comprehen- sive picture of total financial flows to a particular country' (Dennis, 1984, p. 319).

Since 1981 private banks have cut back sharply on their foreign lending, and new commitments have been largely in connection with rescheduling existing obligations, i.e. drawing out maturities, often with a grace period for the resumption of repayment of prin- cipal. Until the mid 1970s such negotiations were usually hosted by the finance ministries of bankers' own governments, such as the so-called Paris and London 'clubs', but increasingly this task has fallen to the IMF, an organization that initially the bankers bitterly opposed. Rescheduling is arranged through an applicant's acceptance of severe 'conditionality', essentially deflationary policies designed to reduce imports and raise exports in return for large IMF assistance, upon which the banks, albeit reluctantly, provide new funds (Carvounis, 1984, pp. 63-80). But how long the banks can, or are prepared, to pay out good money after bad is problematic in the extreme. The banking community, international agencies, and governments of the industrialized world, believe that LDCs are essentially suffering from a 'liquidity' prob- lem, and that when the developed world's rate of economic growth picks up to some 4 per cent or

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

420 DONALD W. FRYER

more, their cash flow problem will disappear (IBRD, 1982; Lombardi, 1985, pp. 93-4); only North Korea, Mozambique, Sudan, Poland and Zaire are considered really bankrupt. That such a solution is unrealistic is, however, held by a wide spectrum of writers from Marxist academics to some bankers and financiers themselves (Payer, 1974; Lever, 1982a; 1982b; Rohatyn, 1982; 1983; 1986; Lombardi, 1985, pp. 93-4) and of course, by most LDC governments.

THE DISTRIBUTION OF PRIVATE BANK LENDING

The World Bank case that the evidence does not support the conclusion that banks lent imprudently to developing countries as a whole during the 1970s and that the countries wasted the proceeds, begs the ques- tion (IBPD, 1983, pp. vii, xvi). Most poor countries continue to depend heavily on ODA for their exter- nal financing. In 1980-81, 44 LDCs received over 90 per cent, 28 from 66 to 90 per cent, and a further 33 from 33 to 66 per cent of ther inflows from this source (OECD, 1983). Yet bankers competed ferociously to place their small national quotas for poor states, and in Gabon, Ghana, Benin and Togo waste was bizarre (Lamb, 1985, pp. 109-10, 284-5). But where bankers lent very heavily, waste was on a scale to match. As a large and populous oil producer, Nigeria was a 'bankers' pet', with $1 billion jumbo loans in both 1978 and 1979 (Economist, 1982, 1986a); by 1980 $1 billion had disappeared from the National Petroleum Company, probably into numbered Swiss bank accounts (Lombardi, 1985, p. 112). The two other very populous oil producers of middle rank, Mexico and Indonesia, have an unenviable record for grandiose waste in their oil entities, which received very large private loans. And one very poor country, Zaire, with a per capita product of less than $300 in 1981, so bedazzled the bankers that it swiftly ran up a very large debt proportional to the size of the national economy; its waste in the later 1970s was on a truly spectacular scale (Aronson, 1977, pp. 169-70; Delamaide, 1984, p. 57, 60; Lamb, 1985, pp. 43-5; Callaghy, 1986).

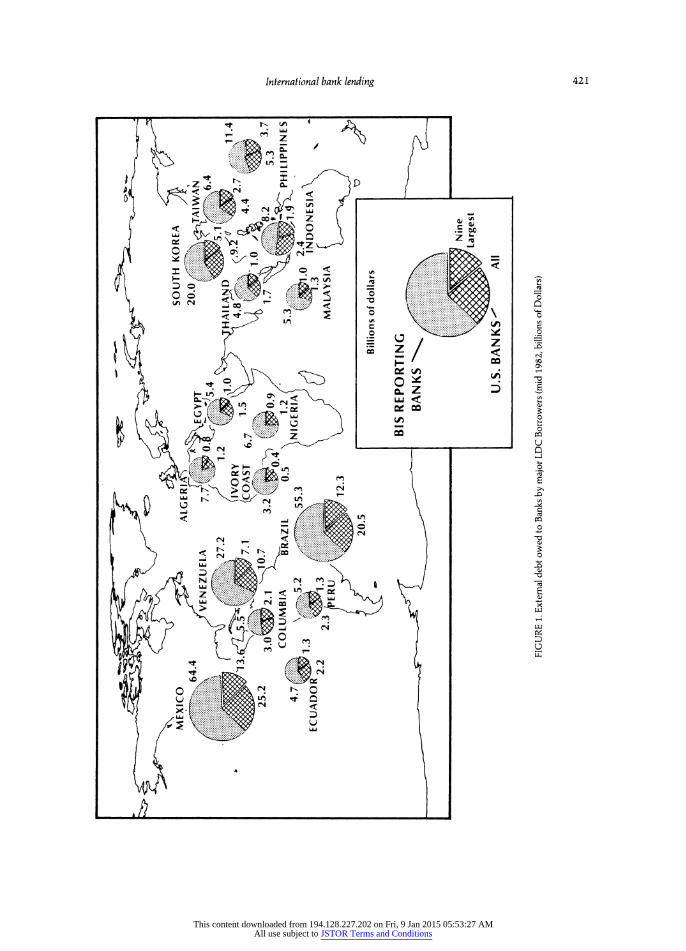

Private bank lending has been highly concentrated on relatively few developing countries. Of a total debt of $348 billion owed by all developed countries within the BIS reporting area to foreign banks in 1982, 21 countries accounted for 84 per cent of the total, the ten larger borrowers for some 70 per cent, and the five largest for no less than 55 per cent (Fig. 1).

Of the lattermost, all but one, the Republic of Korea, were Latin American countries; the five next largest included one Latin American country, and two in Southeast Asia and Africa respectively. Four of the ten, Venezuela, Indonesia, Algeria and Nigeria, were members of OPEC, and together owed almost $50 billion, over 14 per cent of all developing countries' bank indebtness.

The view that the increase in bank lending in the 1970s essentially represented the 'recycling' of the large surpluses accruing to OPEC countries and that loans to 'non-OPEC developing countries' financed their deficits and enabled them to continue to import higher cost oil, sits oddly with these facts. Banks lent mainly to middle, indeed to 'upper-middle' income countries with GNPs per capita of over $2000 and with a wide range of resources. Some were scarcely 'developing'; Argentina regards itself as essentially European, and scorns association with 'los tropicales', the nations to the north (Acoca, 1982). The USSR, Poland, Hungary and Yugoslavia, to which banks have also lent substantial sums, also fall into this income category. Two exceptions are the Philippines, with a per capita product of some $700 in 1981, and very strikingly, Indonesia with only a little over $400.

BIS data, which distinguish between US and other banks, showed that for 1982 US banks accounted for some 36 per cent of the total obligations of all devel- oping countries to private banks, and for some 40 per cent of those of Latin American countries, of which the nine largest US banks accounted for 23 per cent. Of total US bank lending to all developing countries, some 70 per cent was to Latin America (Fig. 1). The Federal Financial Institutions Examination Council (FFIEC) confirms the dominance of Latin America in US bank lending to developing countries; in 1983 of a total of nearly $108 billion in outstanding loans to all non-OPEC developing countries, Latin America, excluding the OPEC members Venezuela and Ecuador which together owed the banks some $13-5 billion, accounted for 68 per cent (Fig. 2). The principal direction of US bank loans to developing countries elsewhere was to a select group in East and South-East Asia, and to Israel.

The distribution of international lending by European, Japanese and other foreign banks is imperfectly known. But the BIS figures suggest that the direction of foreign lending by banks of other developed countries is broadly similar to that of the US banks, although each has areas of interest in which it is relatively stronger. Latin America has had a

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

MEXICO ALG SOUTH KOREA

.

64.4

2A?0. 0iiiii.T '1ii3.7.1

COAST 6.7 1.5 .

4 25.2 2.1 3.2 ~ 0.9 4. 8.2 3.7 0 .

4 .

...... .

A..S COLUMBIA BRAZIL 0.5 1.2 .

PHILIPPINES 4.7

1. N. I.NIGERIA .

ECUAO..35.3 ...1..3 . INDONESIA

2.3

ERUMALAYSIA ERU12.3 20.5 Billions of dollars

BIS REPORTING BANKS

N ine

U.S. BANKS All

FIGURE 1. External debt owed to Banks by major LDC Borrowers (mid 1982, billions of Dollars)

n =r. o x n

n x

ia x

x oc

h,

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

422 DONALD W FRYER

universal appeal; more than 500 foreign creditors were represented in the bankers' committee which in September 1984 reached outline agreement with Mexico on rescheduling some $50 billion of loans falling due by 1990 (Economist, 1984b). The belief that South America has vast potential riches is as old as the legend of El Dorado, and from the time of the South Sea Bubble, it has repeatedly bedazzled foreign investors, often with disastrous consequences (Galbraith, 1975, p. 38; Delamaide, 1984, pp. 96-8).

The success of West European countries and Japan in accumulating large balance of payments surpluses, substantially advanced the ranking of their larger banks. The world's 50 largest banks account for about two-thirds of all lending to LDCs, and within this select group in 1984 were 21 West European and sixteen Japanese banks, as against only six American (Spindler, 1984, p. 4; Banker, 1984). Because of growing competition from the large European and Japanese banks in foreign lending, the share of American banks in overall lending to developing countries has fallen since the late 1970s. Neverthe- less, American banks' exposure in those countries in which the United States has long had a special interest, remains high.

For sovereign states bank loans have the great advantage over ODA that they can be used for any purpose government wishes without external sur- veillance. Moreover, all government borrowing pro- vides budget support in that it can replace budgeted expenditures that government has already decided to make (Robichek, 1980). Loans thus strengthen a government's domestic standing and financial power, and convey a measure of international approval and respectability. Bankers argue that their lending poli- cies are politically neutral, and that any financially well-run country can obtain a loan. Nevertheless, countries falling out of political favour are apt to lose their credit-worthy status until they adopt a political orientation more acceptable to governments of big bank lenders (Aronson, 1977, p. 174).

American bank lending The American bankers earliest ventures into foreign lending were to Latin America. The American con- ception of its political role in the western hemisphere and the numerous long-established activities of American corporations, particularly in extractive industries, within the region, make the continued dominance of Latin America in US bank lending to LDCs inevitable (Fig. 2). The Monroe Doctrine, enunciated shortly after the revolt of the Spanish

colonies, was the country's first decisive foreign policy statement, and for more than a century it remained a major barrier to European governments seeking to compel payment on obligations due to bondholders by defaulting Latin American bor- rowers. Military intervention to compel payment on debts to Americans, or to support American cor- porations against host governments, was another matter. The Grenada invasion of 1984 and the pres- ent conflict in Nicaragua notwithstanding, the excesses of 'Dollar Diplomacy' and direct inter- vention have probably passed for good, and a deci- sive break in the Doctrine came with the resolution of the Cuban crisis of 1962, in which the United States tacitly accepted a USSR-oriented Cuba. But it was determined to prevent the export of Castroism to the mainland. Increased aid to military regimes implied an approval of governments that many Americans detested; private bank loans, presented as purely commercial ventures, suffered from no such political disadvantage.

Virtually all large extractive enterprises in Latin America are now under national ownership, but US strategic planning necessarily involves safeguarding the resources of the entire hemisphere for American use in a major emergency. Fundamental to this aim is the continued availability of petroleum. The close association of the fortunes of the oil industry with national economic and foreign policy is ensured by the industry's enormous contributions to the election campaigns of candidates for national office, and by the activities of its Washington lobby and its banking counterpart. The consonance of the banking and petroleum industries is seldom remarked although Chase, one of the American Big Three banks, is a Rockefeller bank and the family trusts may have a controlling interest in Exxon, Mobil and Socal (Blair, 1976). Not only do the leading banks have stock interests large enough to give decisive influence over the top US energy companies, but they are often also linked through having the same legal counsels (Sherrill, 1983, pp 492-3).

That the State Department approved the activities of the bankers in Latin America is beyond question, for they were forwarding both short term economic and long term strategic interests of the United States. Despite, or perhaps because of, profound suspicion of the American oil companies and their Washington supporters, national oil entities borrowed heavily to finance expansion; by 1982 Mexico's Pemex owed foreign banks some $24 billion, and raising domestic production involved Brazil's Petrobras in some $10

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

PO LAND ,0.6 m=0. 5 0.5 0.4 0.7

YUGOSLA4t0 0.4 0.3 0.8 ISRAEL :::::

2.8 :.:: VENEZUELA 0.46 1.2 "

0.2 0.3 0.9 2.3 :.:3 4.9

,9 3. 0 .4 1.6 1.7 1.2 6.4 8.3 6.6

7.5 2 .7 SOUTH KOREAA 61.3 1.2 C2LU 2.5O 8.3 7.6 0.2 1.1 0.6

0.9 0.5 1.1 .6 Z .2 !!" 0 TAIWAN

4.4 13.3 14.1 j i60li 7 -"0.7 0.3 0.8-1.5

- MEXICO 1.4 2.1 2.2.. IGERIA THAIL NO NDONESIA .4.2

5.1 2.0 0.8 0.6 2.1 0.6

0.4 0.2 0.9 74 2.8 22 1.21 . 0 6

f 1.3 jiO.6 8.3 I7.4 9

0.4 2.0 3.0

0.4 1.3 1.2 , 13 3... ... .9

0.5 0.4 1.3 1.2

04 0.3 72 ECUADOR 1.6 9 133

01.3 0.9 _

__._2.6 1,06 3..

1.82.8 6 5.4

REGIONAL DISTRIBUTIONS CHILE ARGENTINA

13.57.8 6.5 10.2

LEGEND 20.0

S29.1 11.4 18.3 17.9 22.3 Non-OPEC LDCs, SOver Asia

Private Ovr : 31.2 5 Years All Others 31.2

Public 1-5 Years '' 20.5 35.9 42.6 Non-OPEC LDCs, 7.2 ans1

Year Nine Largest Latin America, Caribbean 8.5 6.4 7.2 Banks er10.7 &Under E 0.4 0.6 1.9 6.9 17.9 18.9

2.4 2.7 2.3 2.6 3.6 BORROWER MATURITY SIZE Eastern Europe OPEC

FIGURE 2. Foreign loans by major US Banks (Gross Outstanding claims, US$ billions, end 1983)

-t X zs ?r

X a

zs X fi- h, X A, X Do

cP 13 k

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

424 DONALD W. FRYER

billion of debt between 1973 and 1985 (Hartland- Thunberg and Ebinger, 1986, pp. 62, 141). Despite what Washington believed to be an excessive Mexican sensitivity in negotiations over the price for its oil and gas exports to the United States, the rise of a new petroleum producer potentially of the first magnitude, on the US southern borders, was clearly a major strategic gain.

Despite a higher degree of self-sufficiency in pet- roleum, Brazil's oil imports nevertheless increaed in absolute magnitude over the 1970s. Yet only about a fifth of bank lending was used to meet the higher cost of energy imports. By far the greater part was dis- bursed by heavily protected state entities pursuing an import-substitution and subsidized-exports develop- ment strategy, which by the early 1980s had made the public sector of the Brazilian economy the largest outside the communist world (Hartland-Thunberg and Ebinger, 1986, pp. 105-7). Among the most costly of these bloated state entities were those engaged in other energy projects to reduce the national dependence on petroleum viz., a nuclear reactor programme that by 1984 had involved some $40 billions of cost over-runs, an overly ambitious hydro-electricity plan whose excessive costs and long gestation have so far had a negative impact on the economy, and the synthesis of ethanol from sugar cane, which was barely competitive even at the height of the oil crisis of the late 1970s (Ebinger, 1986). In retrospect, the Brazilian 'economic miracle' from the early 1960s seems merely another in the country's long series of speculative cycles; it col- lapsed in the post-1980 world depression as all such previous cycles had collapsed, and after nearly two decades of opulence, Brazilians again began talking of their country as part of the 'Third World' (James, 1942, Sampson, 1981, pp. 146-7, 240-1).

The other large Latin American borrowers, Mexico and Argentina, have followed broadly similar strategies; Mexico consistently refused to sign the General Agreement on Tariffs and Trade (GATT) to protect its heavily cosseted economy until forced to do so in mid-1986. As with Nigeria and Indonesia, its greatly enhanced borrowings in the 1970s rested on the assumption that high oil prices had become a permanent feature of the world economy. While some authorities had forecast prices of $80-$100 a barrel for the later 1980s (Fesheraki, 1981), spot prices for North Sea crude by mid-1986 had fallen below $10, a fall far steeper than that of interest rates, and the Mexican economy and polity was in deep crisis. Argentina in contrast, had broken with its traditional

economic liberalism in the inter-war period, and forced draught industrialization and state ownership of natural resources intensified in the Per6n regime. In consequence Argentina, in 1914 one of the world's most affluent states with real wages only exceeded by those in the United States and Britain, had slipped to fiftieth rank by 1985 (Fernandez, 1985). While short term borrowing increased after the military coup of 1976 to ease the pressing balance of payments crisis inherited from the Peron administration (Carvounis, 1985, pp. 139-5 1; Diamond and Naszewski, 1985), to one authority the debt problem of Argentina reflects less the indiscretions of the foreign bankers than 'a lack of faith of Argentina entrepreneurs in a country where properly rights are not granted by law but by the will of a government bureaucracy' (Fernandez, 1985).

The Latin American industrial boom and its after- math of debt had two important consequences for the United States. Although competition from European and Japanese banks drove down the US share of pri- vate claims on Latin America from some 60 per cent in 1975 to 45 per cent in 1983, the United States nevertheless improved significantly its trading pos- ition vis-a-vis its industrial rivals. By 1979, the United States was supplying over 40 per cent of Latin America's imports, two-thirds of which went to the six most deeply indebted states, Brazil, Mexico, Argentina, Venezuela, Chile, and Peru. Excluding trade with OPEC countries, the share of Latin America in US trade turnover grew from a little over 10 per cent in 1973 to nearly 14 per cent in 1981 (Economist, 1984a, World Financial Markets, 1984).

The political consequence was unforeseen; Latin America's military governments were unable and unwilling to confront the exigencies of the debt crisis with its mandated deflation, declining GNPs, mount- ing unemployment and severe social distress. By 1985 Brazil had joined Uruguay, Peru, Ecuador, and Argentina in restoring elected democratic govern- ments, and only Chile of the major debtors remained under military rule. Another long-acclaimed objec- tive of US foreign policy for the hemisphere had apparently been realized, but appearances were deceptive. In Argentina the military was discredited by the disastrous 1982 Falklands/Malvinas war and by responsibility for the thousands of desparecidos, the missing victims of the generals' ferocious onslaught in the 1970s against urban leftists and alleged sup- porters. But in Argentina, Peru and Brazil alike, the new civilian administrations appeared fragile, unable and unwilling to initiate basic structural changes in

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

International bank lending 425 the economy for fear of the return of the generals, and strongly resistant to the deflationary pressures of the IMF. For Argentina, which had borrowed largely to meet balance of payments deficits rather than for infrastructural investment, this pressure was particu- larly irksome. In resisting the Fund and the bankers, Argentina was again stressing its separation from the rest of Latin America and acclaiming its European affinities. Britain's IMF credit of 1976 had involved no such 'conditionally (Gisselquist, 1981, p. 223); Argentina felt it merited no less favourable treatment than that accorded to the privileged Europeans.

Within the United States, increasing trade and financial connections with Latin America have had a remarkable impact on south Florida where burgeon- ing Miami is becoming 'the northernmost city of Latin America' (Neil, 1982, p. 3). Miami's transform- ation began during the 1950s with the immigration of skilled refugees from Castro's Cuba, but by 1980 its Hispanic population included elements from all parts of Latin America. The city has attracted a substantial, and perhaps increasing proportion of the flight capital of rich Latin Americans, 'the cowardice of money' as President Peron once called it, which has repeatedly prevented the region from capturing the maximum benefits of periods of high prices for its export products. Unlike the poor immigrants into the Southwest, Miami's wealthy and educated Hispanics maintain a multiplicity of economic and political connections with their homelands. Through these links Miami become an attractive centre for lending to Latin America, and has now become a major focus of international banking in its own right, in which virtually all the world's major banks are represented.

That this development is also related to the 'laundering' by the banks of an annual inflow into south Florida of some $7-10 billion from drug traffic, is beyond question (Neil, 1982, p. 21). Florida has a long history of lawlessness (Rothschild, 1985); the facts of geography make complete suppression of drug smuggling impossible, however thorough federal surveillance of the air, the coasts and the banks. The wholesale value of illegal drug exports to the United States from Jamaica and Colombia alone is estimated respectively at more than $2 billion annu- ally (Economist, 1984d); that from Mexico must be very much more. Virtually all discussion of the debt burden ignores the obvious, that the annual earnings of Latin America from the drug trade are probably larger than payments of its debt obligations. True, much of these earnings remains within the United

States, but eventually it gets into the banking system and is available for further lending. The proceeds also are distributed in a highly inegalitarian manner; nevertheless, 'the US huge imports of dope are people-to-people assistance of the most direct kind- in Jamaica, Colombia, Bolivia, and Peru... thousands, if not millions of farmers, rural people and entrepre- neurs are getting income from the drug business' (Stein, 1984). There is thus a strong presumption that policies for suppressing drug smuggling will achieve minimal success until a comparable financial flow is substituted. Meanwhile, US military assistance to the ambivalent governments of Mexico, Colombia and Bolivia in half-hearted efforts to destroy plantings and processing facilities, has brought renewed charges of 'Yankee imperialism' within the region.

In the second major area of American bank lending, East and South-East Asia, US political and economic interest are also of long-standing, dating back before the 1853 Perry expedition to Japan. Since the end of World War II the region's island and peninsular states have played a key role in US strategy for resisting the spread of communism in Asia, and in particular, in constraining the large Russian air and naval forces in the Pacific. Most such states have de jure (South Korea, the Philippines), or de facto (Japan, Taiwan) alliances, or tacit understandings (Thailand, Indonesia) with the United States for major US assistance in meeting external attack. The strategy necessarily involves a heavy US commitment to economic development, and sparked off by imposed land reform in the defeated Japanese empire and large official aid, the contrast in economic performance with that of the faltering communist economies of the mainland has been remarkable; following the Japanese 'economic miracle' came the success of the newly industrializing states (NICS), South Korea, Taiwan, and the two city states of British origin, Hong Kong and Singapore. These four have consti- tuted the largest destination of US corporate invest- ment in the developing world, and the first two, together with the Philippines and Thailand, a major focus of American bank lending. This reached its apogee in the mid 1970s, when US banks held over 80 per cent of total claims due to foreign banks from the four states. By 1982 this share had fallen to 46 per cent, while that due to European banks increased three-fold to some 34 per cent, and to Japanese banks increased ten-fold to 23 per cent (Spindler, 1984, p. 6, De Vries, 1983); significantly, the decline was greatest in Thailand, where an American defence commitment is equivocal.

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

426 DONALD W. FRYER

The pattern of bank lending by origin to the region thus now broadly resembles that to Latin America, in that banks of a large number of countries have sub- stantial claims. Nevertheless, the Philippines apart, a debt service problem has not so far arisen. Loans have been used in support of an alternative development strategy, usually termed 'export-led', although both South Korea and Taiwan have large domestic mar- kets; only about one-third of the value of Taiwanese manufactures is exported (Kuo, 1983). Industrial development received little protection, but it fol- lowed and did not precede agricultural reform and a great increase in productivity, which provided farmers with the income to buy new products. MNC investment and joint ventures with local private con- cerns helped to ensure a high degree of competitive efficiency from the start. True, the east Asian NICS have enjoyed a somewhat privileged access to the large US market. But the fact remains that the NICS are highly competitive in quality as well as in price; with few exceptions, Indian industrial exports are neither.

The striking exception to this success is the Philippines, which in its development strategy as in so much of its socio-economic structure, more closely resembles Latin America than its Asian neighbours. Though the United States grappled with the prob- lems of a defective agrarian organization almost from the commencement of its administration, it was unable at the end of World War II to impose on its Ally and former possession, its policy for land reform in the Japanese empire. Nor has any administration of the Philippine Republic made any real commitment to the issue; all hoped that technological change could make such action unnecessary. Failure to solve the land problem is the primary reason for the Philippine's lacklustre economic performance, and its consequences have been regional insurrections, widespread urban and rural discontent arising from underemployment and malnutrition, and intense dissatisfaction with the largely window-dressing programme of land reform which characterized the former Marcos' regime (Kerkvliet, 1974).

The disunited opposition in the Philippines was at one in viewing the loans made by foreign bankers as buttressing the Marcos regime and furthering the extension of its 'crony capitalism', through which large chunks of the economy passed to the President's close personal friends. Debt service in relation to export earnings is the equivalent of that of the largest Latin American borrowers, and the proportion of short term to total debt in 1982-some 47 per cent--

far exceeded the 27 per cent for Mexico or the 16 per cent for Brazil. Payments to foreign banks became in virtual default in October 1983, and lack of agree- ment with the banks still held up in 1986 an IMF 615 million Special Drawing Rights (SDR) stand-by credit, for which such agreement was a pre-requisite (Economist, 1984f).

In lending large sums to a country whose dismal economic performance appears to make it a poor risk, the bankers were confident that in the last resort Washington would always come to the rescue because of the supreme importance of the Subic Bay and Clark Field bases. It remains to be seen whether the new Aquino administration, which came to power with dramatic suddenness in early 1986, can thwart a communist revolutionary triumph, in which case debt repudiation would follow, as with the Russian, Chinese, Cuban and Iranian revolutions.

The non-American lenders West European states have a long tradition of private foreign lending, but Japan has only become a large creditor since 1960. The areal lending of European and Japanese banks preserves traces of former imperial interests, but these fossils coexist with new positions, for which the absence of a colonial connec- tion, or more correctly, one lost long enough to be conveniently forgotten, has been advantageous.

In sharp contrast to pre-World War II practice, non-American bank lending has been denominated largely in Eurodollars, and not in national currencies. True, some loans are now made in Deutsche mark and yen, but no country is willing to allow foreigners to acquire large quantities of its currency as none wishes to risk the costly experience of Britain in operating a major reserve (Strange, 1971). Attempts to create new reserve units such as the SDR or ECU (European Currency Unit), a unit of account between EEC mem- bers, have not significantly reduced the role of the dollar and the financial hegemony of the United States, which is buttressed by the location of both the IMF and World Bank in Washington.

As the oldest hands in the business, British banks have the widest geographical range in their lending, and in total obligations are second to those of the United States. In 1984 some 45 per cent of all loans outstanding were to Latin America, about the same proportion as that of American bank loans. Former imperial interest, however was visible in the commit- ments to Commonwealth countries, those to Nigeria for whom British banks were the largest lenders,

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

International bank lending 427

being of a magnitude to give major concern (World Financial Markets, 1985). In contrast with that of the other populous oil producers of middle rank, Mexico and Indonesia, Nigeria's debt problem is of very recent origin, and both debt per capita and debt service as proportion of export earnings are very low in comparison with those of other major debtors (Nunnenkamp, 1986). Nigeria's obligations arise mainly from private export credits granted in connec- tion with the grandiose national development plan based on the high oil prices of the 1970s. In theory, Nigeria should to be able to pay its way without major difficulty. But doing so exacerbates the immanent divisions among its very diverse peoples, as the trauma of the sudden descent from affluence to parsimony and the bitter legacy of colossal cor- ruption even at the highest levels of government, poison society. The flight of key figures in the Buhari administration and the oil industry caused serious diplomatic difficulties with Britain, and whether Nigeria could survive at all appeared at mid 1986 a matter of substantial doubt (Economist, 1986a).

German bank loans in contrast, show old and new patterns. Freedom from the taint of colonialism helped German banks in enlarging business with some developing countries, notably with the politi- cally highly sensitive oil producers, Indonesia and Iran (Spindler, 1984, p. 68). On the other hand, in loans to Turkey and to east European countries, the banks mirrored their imperial predecessors. Lending to the countries of the Council of Mutual Economic Assistance (COMECON/CEMA), which release limited statistics of their national accounts and most of which are not members of the IMF, is fraught with risk, but such loans forward Bonn's Ostpolitik of reconciliation with states occupied by Germany dur- ing World War, and, though under Soviet hegemony, avid for western currencies for their national develop- ment. While this mandates accommodation with the USSR, its crux is relations with Poland, the most populous of the Soviet satellites, and with the sharpest cleavage between government and people. Poland commands the route to East Germany, the USSR's most valuable 'colony', but its instability and intractable economic problems, which arise from the Poles' fierce pride in their national identity, make it not only a drain on the USSR but also a threat to Bonn's Deutschlandpolitik. This set of understandings and observances between the two Germanies makes daily life more comfortable for both states, and preserves a common German identity despite the minimal prospect of political reunification.

Poland, in Bonn's view, should abandon its roman- tic attachment to freedom, concentrate on economic reform and raise living standards to those of Hungary or East Germany. It is a policy most Poles emphati- cally reject (Ash, 1985, pp. 38-9). Serious social discontent in Poland, triggered by economic short- comings, compels Bonn to provide large credits, and if necessary, to pressure its banks to support beyond their own volition, as occurred in both the early 1970s, and in 1979-80, when the German banks supplied $500 million to help Poland meet a major financial crisis (Spindler, 1984, p. 80).

Lending 'to a nation like Poland is to enter uncharted water without the conventional lifeboat on board' (Carvounis, 1984, p. 151). But the bankers believed that the USSR, which despite its repudiation of Imperial bonds became credit-worthy through prompt payment of its own bills, would rescue any client state in serious difficulties. The 1976 default of North Korea on obligations of almost $2 billion due mainly to Japan, Sweden and Finland punctured this optimism, but as few big Western banks were involved, the danger signal went unheeded. The USSR did indeed attempt to assist Poland in 1981, but the claims of other satellites for similar help and its own mounting financial problems compelled it to abandon Poland to its own devices. Poland's effective default, followed shortly by that of Romania destroyed the bankers' optimism; they were then owed some $80 billion by COMECON countries (Rohatyn, 1983). Poland has since unilaterally deter- mined what it will pay, if anything, and progress with debt rescheduling has been slow. While German banks were the major sufferers in these defaults, some American banks also burnt their fingers. Yet, the Germans still perceive the USSR itself as a good risk; Bonn mobilized large credits for the Yamal gas pipeline against strong American opposition, and in mid-1986, the Deutsche Bank announced a $250 million consortium loan for accelerating Soviet economic growth (Wall Street Journal, 1986).

That East Germany, with some $12 billion of debt, much at short term, did not become another defaulter in 1982, probably owes much to the covert support of the West German banks, acting with Bonn's tacit approval (Delamaide, 1984, pp. 94-5). East Germany can, in effect, apply a financial pressure on Bonn that is little short of blackmail. It enjoys a surrogate mem- bership of the EEC as the Federal Republic treats its exports as 'German', and in many other ways subsi- dizes its neighbour so that it enjoys the highest living standards in the COMECON bloc. Bonn's gain from

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

428 DONALD W. FRYER

this outflow may appear meagre, but the policy has strong popular support which it would be dangerous for other NATO countries to underrate (Ash, 1985, p. 34).

The close identification of national foreign and economic policy with private bank lending visible in West Germany, is even more marked in the case of Japan. Export promotion is a cornerstone of national economic policy, for though foreign trade is only a small proportion of GNP, exports are vital to meet the cost of imported raw materials and particularly energy sources, in which Japan is more dependent on outside suppliers than is any other major power. Japan's panic in 1978 was a major factor in the oil price increase sparked by the Iranian revolution, and in that year oil imports absorbed over 26 per cent of export earnings (Siddayao, 1982).

Post-war reorganization has made the banking units of the great manufacturing complexes of Mitsui, Mitsubishi and Sumitomo even more important in overall corporate policy than was the case with the banks of the old zaibatsu. Aggressive foreign lending forwarded corporate growth, and the largest loans were for ensuring or enlarging the supply to Japan of key raw materials; with a multiplicity of suppliers, the country is not hostage to any one. Typically, large loans are made by consortia headed by the Bank of Tokyo, which though no longer partly state-owned as before World War II, has such close ties with the Ministries of Finance, and Trade and Industry (MITI), that in practice it acts as a government agent (Spindler, 1984, p. 111). Loans to reduce dependence on Persian Gulf petroleum have gone to China, Mexico and Indonesia, and for the expansion of liquified natural gas (LNG) production to Brunei, Malaysia and Indonesia, which Japan intends to sub- stitute for oil in electricity generation to the fullest extent possible (FEER, 1982). The banks have also financed joint ventures with host governments for the exploitation of coal, iron ore, bauxite and aluminium, and other non-ferrous metals, and tied to the supply of Japanese machinery and processing equipment.

Yet much of Japanese bank lending mirrors former imperial interests (Fisher, 1950). Of Bank of Tokyo loans in 1979-80 of over $500 million, one-third was to countries of East and South-East Asia; oil exporters also accounted for around one-third (Spindler, 1984, pp. 140-5). Japanese foreign lending, unlike that of American and European banks which lend mainly to each other, is thus largely directed to developing countries, a situation that parallels that of Japanese

corporate investment overseas. This pattern of finan- cial penetration has disturbing overtones. Japan is the principal trade partner of every country of East and South-East Asia except Hong Kong, in some cases by a substantial margin, and also of Australia. The situ- ation of South-East Asia, which is deeply in debt to Japan, appears in danger of approaching that of pre- war south-east Europe in relation to the Third Reich, when massive German barter deals in the autarchic world economy of the 1930s, created an imperium even before the Wehrmacht began to march. By mandating greater use of countertrade, or barter, Indonesia and other South-East Asian countries resurrect a painful reminder of the 1930s, when the danger of a relapse into the protectionism of that era appear to be increasing. Barter, and its corollary, smuggling, have long thrived in the region, are encouraged by a unique geographic interdigitation of land and sea, and always increase when times are hard. The growing use of barter also by large debtors such as Brazil and Argentina, by OPEC members to defeat the organization's quotas, and by many LDCs, testifies to growing dissatisfaction with the world monetary system, and augurs ill for future debt service.

PROSPECT How to resolve LDCs' debt problems lies beyond the scope of this paper. Academics, officials and poli- ticians, bankers and financial specialists, have suggested a multiplicity of schemes for remedial action, but none has so far possessed political feasibility; most aim at trying to keep loan payments going or preventing banks from recording obvious losses, i.e., essentially ways of preserving legal fictions (Delamaide, 1984, pp. 232-51). Many writers, and LDCs themselves, see the debt problem as indicative of major dislocation in the world economy, and evidence of substantial and perhaps growing instability is very clear (Thrift, 1986). But there is substantial disagreement on the degree of restructuring necessary, and the more fundamental the changes to the world monetary and economic system posited, the greater of course, the political difficulties in implementing them. For Lombardi, a banker, the problem essentially arises from a false theory of development by multilateral agencies, based on patterns of thinking derived from the Enlightment (Lombardi, 1985). Whatever the theory, practice has been miserable; LDC debt represents a flow of resources larger than that of Marshall aid, but

This content downloaded from 194.128.227.202 on Fri, 9 Jan 2015 05:53:27 AMAll use subject to JSTOR Terms and Conditions

International bank lending 429

the return has been far from comparable. Several writers focus on a long overdue reform of the world monetary system, the need for a restoration of an equivalent to the Bretton Woods system, and the creation of new reserve units (Delamaide, 1984, pp. 213-31; Feito, 1985; D'Arista, 1986). Others single out the erosion of the barriers erected after the excesses of the Great Depression to separate commercial banking from investment banking, and both from broking (Kaufman, 1986). Still others see the debt problem, and most other socio-economic ills, as arising from fundamental defects of modem capitalism, always the view of Marxists but shared by those stressing 'paper entrepreneurship' (Reich, 1983) or 'casino capitalism' (Strange, 1986), i.e., a growing preference for the speculative manipulation of pieces of paper over making quality products or providing quality services. Yet Braudel, in sharp contrast with Marx, Lenin and Wallerstein, is emphatic that the full panoply of capitalism, including speculation and the drive to monopoly, was there from its very begin- nings in thirteenth century Florence, and is confident that the system will stay (Wallerstein, 1974; Braudel, 1982, 1984).