Development Discussion Papers to the issues considered here are Ismah Afwan, Hilman Akil,...

141

Harvard Institute for International Development HARVARD UNIVERSITY Development Discussion Papers Rural Financial Intermediation: Lessons from Indonesia, Part One The Bank Rakyat Indonesia: Rural Banking, 1970-1991 Marguerite S. Robinson Development Discussion Paper No. 434 October 1992 © Copyright 1992 Marguerite S. Robinson, and President and Fellows of Harvard College

Transcript of Development Discussion Papers to the issues considered here are Ismah Afwan, Hilman Akil,...

Harvard Institute forInternational Development

HARVARD UNIVERSITY

Development Discussion Papers

Rural Financial Intermediation:Lessons from Indonesia, Part One

The Bank Rakyat Indonesia:Rural Banking, 1970-1991

Marguerite S. Robinson

Development Discussion Paper No. 434October 1992

© Copyright 1992 Marguerite S. Robinson,and President and Fellows of Harvard College

Development Discussion Paper no. 434

Rural Financial Intermediation: Lessons from Indonesia. Part One

The Bank Rakyat Indonesia: Rural Banking, 1970-91

Marguerite S. Robinson*

Abstract

Indonesia operates probably the most successful nationwide system of rural banking found in anydeveloping country; the world’s fourth largest nation achieved this result in only seven years (1984-90).The development of rural banking through the Bank Rakyat Indonesia (BRI), the Peoples’ Bank ofIndonesia, is examined here in order to show how the present system emerged and how it operates. InPart Two, theories of rural financial markets are re-examined in light of this experience and a model ofrural financial intermediation in developed. Part three analyzes policy issues relating to governmentintervention in rural financial markets, with emphasis on the relation of such intervention to economicdevelopment and equity. (Parts Two and Three are forthcoming in the HIID Development DiscussionPaper Series).

This paper, Part One of the series, examines the reasons for the remarkable turnaround in BRI’s ruralbanking system from a channeling agent for subsidized credit to a profitable nationwide system of ruralbanking. They include the following:

1. Good, consistent, macro-economic management and political stability at the national level.

2. Creation of the underlying conditions for a successful rural banking system: a) investment, in the1970s, of a significant portion of the country’s oil wealth in the rural areas, resulting insubstantial rural development and in a growing demand for banking services; and b) financialderegulations, in the 1980s, which permitted the introduction of banking instruments that couldboth meet local demand and provide institutional profitability.

3. An understanding that the supply-leading theories of rural finance and their associatedsubsidized agricultural credit programs, which became popular during the 1950s throughout thedeveloping world, generally do not promote rural development and typically serve to inhibit thedevelopment of sustainable rural financial institutions.

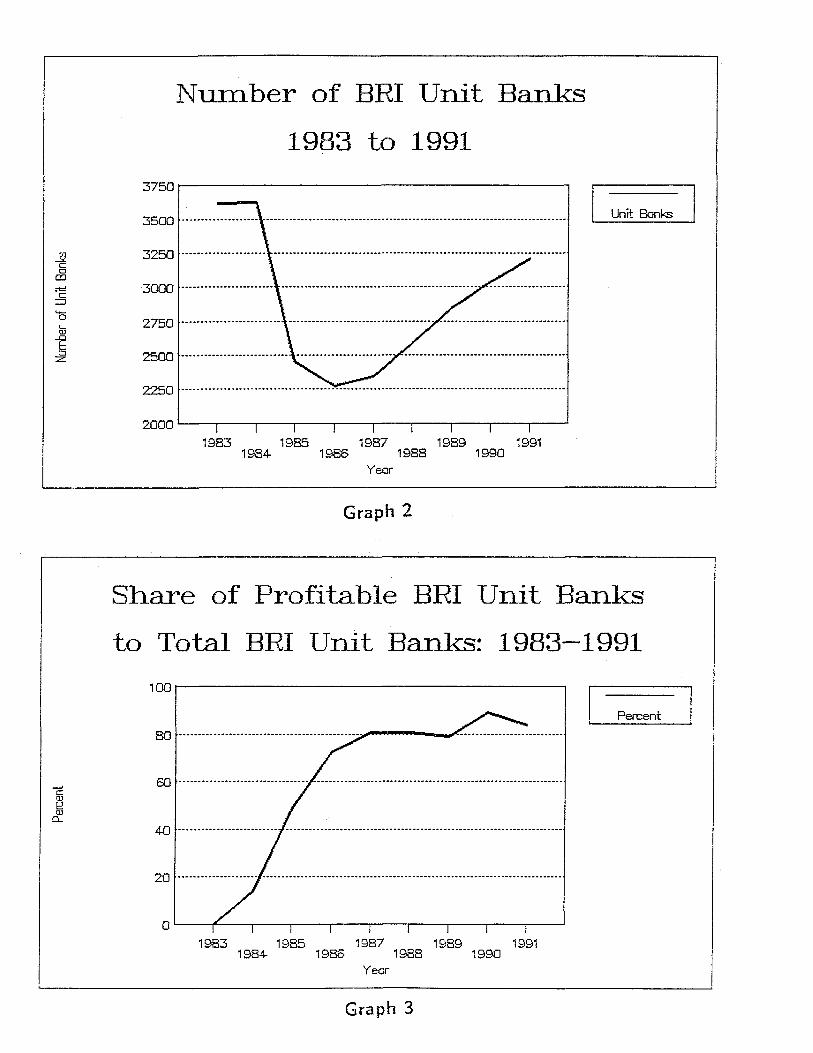

4. The introduction to BRI’s unit banks throughout the country, in 1984, of the KUPEDESprogram of general rural credit provided at commercial interest rates substantially below therates typically charged by local informal commercial lenders.

5. Realization that a general rural credit program at commercial interest rates, in conjunction withappropriate deposit instruments, can be successfully implemented in rural areas concurrentlywith subsidized credit programs (if continuation of the subsidies is considered politicallynecessary); because of the capital constraints of the latter, the former will gain a larger share ofthe market.

6. Introduction of a set of deposit instruments with different mixes of liquidity and returnsappropriate for the varied demand of local credit markets.

7. A spread between lending and savings interest rates which permits bank profitability, whileoffering loans at interest rates significantly below those of informal commercial lenders andproviding savers with generally positive real rates of return on their deposits.

8. Successful leadership at BRI’s head office, resulting in major organizational reformsimplemented throughout the institution, and in the development of a ‘new BRI culture’

emphasizing professionalism, accountability, incentives, training, and knowledge of localmarkets.

9. Expansion, in the late 1980s, of the unit bank concept and its instruments, with somemodification, to urban neighborhoods.

10. A well-chosen selection of complementary priorities.

Part One reviews the development of BRI’s unit banking system and analyzes the reasons for itssuccess. The theoretical and policy-related implications of the Indonesian experience for rural financialmarkets are summarized; these are then explored further in Parts Two and Three.

The conclusion is drawn that because of local-level politics and associated information flows in ruralareas of developing countries, informal commercial interest rates are typically far higher than is necessaryfor the provision of profitable institutional rural financial intermediation. Contrary to much conventionalwisdom, the Indonesian experience has demonstrated that financial institutions can operate extensivelyand profitably in rural areas, and that a nationwide rural banking system can be politically feasible andcan be economically and socially profitable.

Parts Two and Three consider, from theoretical and policy perspectives respectively, lessons whichcan be learned from the Indonesian experience in rural financial intermediation and their possibleadaptations to other developing countries.

Marguerite S. Robinson, author of the series and a social anthropologist, is an Institute fellow at HIID.She served as consultant to the Ministry of Finance, Government of Indonesia, and to the DevelopmentStudies Implementation Project and its successor, the Center for Policy and Implementation Studies(CPIS) in Jakarta, from 1979-92. She worked with the Bank Rakyat Indonesia during the period 1982-90.

*The research on which these papers are based was supported by the Ministry of Finance, Government of Indonesia.The author is grateful to the Ministry of Finance and the Coordinating Minister for Economy, Finance, and Industryfor the support provided and for the extensive information made available on rural development, banking, andgovernment policy. She would like to thank the Center for Policy and Implementation Studies and the many peoplewith whom she worked there as coordinator of the rural banking group. Those whose work has been of most directrelevance to the issues considered here are Ismah Afwan, Hilman Akil, Christopher P.A. Bennett, Kwan HwieLiong, R.J. Moermanto, Ilyas Saad, L. Hudi Sartono, Bambang Soelaksono, and Sudarno Sumarto; their help isgratefully acknowledged. Much of what the author has learned about successful rural banking has been fromdiscussions with I. G. Made Oka, President of the Bank Dagang Bali, and through observation of the operations ofthis bank. She is also grateful to Louis Eman of the Bank Pinasaan for insights into rural financial markets. Helpfulcomments on the manuscript were provided by James J. Fox, Philip N. Jefferson, Dharma Kumar, Dwight H.Perkins, Laura O. Robinson, Michael Roemer, Peter Rosendorff, Chiranjib Sen, Parker M. Shipton, Donald R. Snod-grass, and Norman T. Uphoff. The author is grateful to Satriyo Purnomo and Noor Rachmah for assistance inproviding and checking BRI data; to Gretchen O'Connor for editorial assistance; and to Elyse Wilson Foote, StevenHolmes, Carol Grotrian, and Rietje Koentjoro for help in preparation of the manuscript. She would like to thank theWorld Bank for permission to quote from the draft manuscript, Agricultural Development Policies and theEconomics of Rural Organization (Karla Hoff, Avishay Braverman, and Joseph E. Stiglitz, eds.), forthcoming 1992.

To Mr. Kamardy Arief, President-Director of the Bank Rakyat Indonesia (1983-1992); Mr. Sugianto, BRI'sDirector responsible for the rural banking system; and thousands of BRI staff from the head office to the unit banksthroughout the country, the author is indebted in a special way. Throughout the many years of this work, they notonly made available continued and extensive assistance, they also set the example. It has been a privilege to observein detail the development of BRI's nationwide system of rural banking; the author is grateful for the help and themany opportunities provided her.