Deloitte_ROI Case Study for Abu Dhabi Commercial Bank

8

Benefits from implementing BPM solution at a leading bank

-

Upload

varun-ghai -

Category

Documents

-

view

47 -

download

3

Transcript of Deloitte_ROI Case Study for Abu Dhabi Commercial Bank

Benefits from

implementing BPM solution

at a leading bank

Return on Investment of #190%

At a Glance

Abu Dhabi Commercial Bank (ADCB), with a strong

presence in Consumer and Corporate Banking, is a leading

provider of technology-enabled services. In its objective

towards complete automation of processes, the bank was

in urgent need for a solution that would enable end-to-end

automation of its key business processes and also provide

integration with its existing applications. Newgen provided

the bank with a BPM-enabled workflow platform that not

only helped the bank to automate its processes, but also

allowed seamless integration of the BPM solution with the

existing applications.

• Processing delays and low productivity

• Dependency on physical movement of documents

between branches and departments

• Difficulty in verification process and error identification

due to unavailability of documents

• Difficulty in tracking and monitoring of processes

• Major challenges in incorporating process change

requirements using the existing application

Key Challenges

# Refer “Methodology” section for details on how Return on Investments (ROI) has been calculated* As per data provided by Newgen’s client

1 of 6

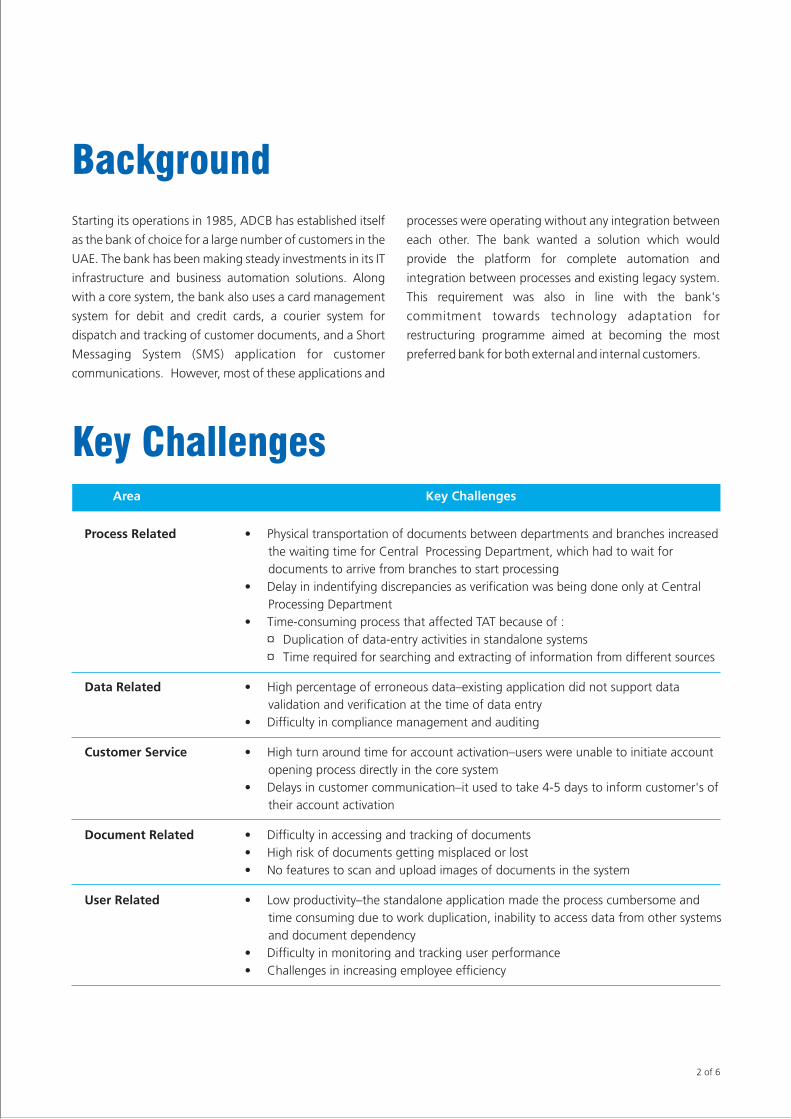

Background

Starting its operations in 1985, ADCB has established itself

as the bank of choice for a large number of customers in the

UAE. The bank has been making steady investments in its IT

infrastructure and business automation solutions. Along

with a core system, the bank also uses a card management

system for debit and credit cards, a courier system for

dispatch and tracking of customer documents, and a Short

Messaging System (SMS) application for customer

communications. However, most of these applications and

Key ChallengesArea Key Challenges

Process Related • Physical transportation of documents between departments and branches increased

the waiting time for Central Processing Department, which had to wait for

documents to arrive from branches to start processing

• Delay in indentifying discrepancies as verification was being done only at Central

Processing Department

• Time-consuming process that affected TAT because of :

¤ Duplication of data-entry activities in standalone systems

¤ Time required for searching and extracting of information from different sources

Data Related • High percentage of erroneous data–existing application did not support data

validation and verification at the time of data entry

• Difficulty in compliance management and auditing

Customer Service • High turn around time for account activation–users were unable to initiate account

opening process directly in the core system

• Delays in customer communication–it used to take 4-5 days to inform customer's of

their account activation

Document Related • Difficulty in accessing and tracking of documents

• High risk of documents getting misplaced or lost

• No features to scan and upload images of documents in the system

User Related • Low productivity–the standalone application made the process cumbersome and

time consuming due to work duplication, inability to access data from other systems

and document dependency

• Difficulty in monitoring and tracking user performance

• Challenges in increasing employee efficiency

Key BenefitsArea Benefits*

TATs, processing time and servicing time

Customer Service Quality and Satisfaction

Dependency on physical documents

Volumes of transactions handled per day

More than 70%

For both existing & new customers

100%

100%

2 of 6

“Greater flexibility to amend and improvise processes –allowed the bank to incorporate Islamic banking norms, in a very short duration”

processes were operating without any integration between

each other. The bank wanted a solution which would

provide the platform for complete automation and

integration between processes and existing legacy system.

This requirement was also in line with the bank's

commitment towards technology adaptation for

restructuring programme aimed at becoming the most

preferred bank for both external and internal customers.

Return on Investment of #190%

At a Glance

Abu Dhabi Commercial Bank (ADCB), with a strong

presence in Consumer and Corporate Banking, is a leading

provider of technology-enabled services. In its objective

towards complete automation of processes, the bank was

in urgent need for a solution that would enable end-to-end

automation of its key business processes and also provide

integration with its existing applications. Newgen provided

the bank with a BPM-enabled workflow platform that not

only helped the bank to automate its processes, but also

allowed seamless integration of the BPM solution with the

existing applications.

• Processing delays and low productivity

• Dependency on physical movement of documents

between branches and departments

• Difficulty in verification process and error identification

due to unavailability of documents

• Difficulty in tracking and monitoring of processes

• Major challenges in incorporating process change

requirements using the existing application

Key Challenges

# Refer “Methodology” section for details on how Return on Investments (ROI) has been calculated* As per data provided by Newgen’s client

1 of 6

Background

Starting its operations in 1985, ADCB has established itself

as the bank of choice for a large number of customers in the

UAE. The bank has been making steady investments in its IT

infrastructure and business automation solutions. Along

with a core system, the bank also uses a card management

system for debit and credit cards, a courier system for

dispatch and tracking of customer documents, and a Short

Messaging System (SMS) application for customer

communications. However, most of these applications and

Key ChallengesArea Key Challenges

Process Related • Physical transportation of documents between departments and branches increased

the waiting time for Central Processing Department, which had to wait for

documents to arrive from branches to start processing

• Delay in indentifying discrepancies as verification was being done only at Central

Processing Department

• Time-consuming process that affected TAT because of :

¤ Duplication of data-entry activities in standalone systems

¤ Time required for searching and extracting of information from different sources

Data Related • High percentage of erroneous data–existing application did not support data

validation and verification at the time of data entry

• Difficulty in compliance management and auditing

Customer Service • High turn around time for account activation–users were unable to initiate account

opening process directly in the core system

• Delays in customer communication–it used to take 4-5 days to inform customer's of

their account activation

Document Related • Difficulty in accessing and tracking of documents

• High risk of documents getting misplaced or lost

• No features to scan and upload images of documents in the system

User Related • Low productivity–the standalone application made the process cumbersome and

time consuming due to work duplication, inability to access data from other systems

and document dependency

• Difficulty in monitoring and tracking user performance

• Challenges in increasing employee efficiency

Key BenefitsArea Benefits*

TATs, processing time and servicing time

Customer Service Quality and Satisfaction

Dependency on physical documents

Volumes of transactions handled per day

More than 70%

For both existing & new customers

100%

100%

2 of 6

“Greater flexibility to amend and improvise processes –allowed the bank to incorporate Islamic banking norms, in a very short duration”

processes were operating without any integration between

each other. The bank wanted a solution which would

provide the platform for complete automation and

integration between processes and existing legacy system.

This requirement was also in line with the bank's

commitment towards technology adaptation for

restructuring programme aimed at becoming the most

preferred bank for both external and internal customers.

The Solution

Based on the bank's requirements, Newgen developed a

customized solution, consisting of the following products:

TM • OmniFlow – workflow solution

TM• OmniDocs – document management solution

TM• OmniScan (OmniCapture) – image capture and

indexing solution

In the initial phase, Newgen helped the bank automate one

of its most critical processes, the Account Opening process.

Integrated with the bank's existing core application, the

solution provides easier and faster data exchange across

systems. Buoyed by the results achieved within a short time

of deployment, the bank also implemented and automated

a number of other key processes such as Customer and

Account Maintenance, Term Deposit Initiation and

Maintenance on the BPM platform. At present, the solution

has been implemented across 43 branches of the bank and

supports 706 users. Every month, more than 61,000

documents are scanned and imported into the workflow for

processing. For Account Opening, the system processes

approximately 245 applications every day and can be easily

scaled up to meet any future requirement of the bank.

Account Opening process: The new system allows users

to capture relevant information and customer signoff at the

branches itself before the case files move to the Central

Processing Department (CPD). Instead of customers having

to submit complex forms, the system automatically

generates the required forms. The branches update these

forms online and take customer signoff before uploading in

the system. On completion of the mandatory branch level

activities, the files move to the CPD immediately for further

processing. Through real time integration with the core

system, CPD users directly initiate the Account Opening

process from the workflow solution. Through integration

with the SMS system, the solution enabled the team to

communicate to customers within 10-15 minutes of their

account becoming operational. The solution also generates

the welcome letter within 30 minutes of account activation.

Post account activation, CPD is able to track and monitor

the dispatch of the welcome kits to customers through the

courier system, which has also been integrated with the

workflow solution.

Some of the unique features of the solution were:

Key Features:

• Real-time integration with core system and other

existing applications

• Searching for existing customer record and

comprehensive validation check at the branch level

• User friendly interface

• Direct updating of customer information in the core

banking system through real-time integration

• Generation of complete audit trail to view history of

events taken place for any record

• Display of relevant information from the core application

reducing information searching and retrieving time

• Automatic generation of relevant documents at

different worksteps of the process including the

welcome letter

• Tracking and monitoring of process and user

performance

• Scanned documents can be introduced into the

workflow from any location, providing instant access for

processing and eliminating document-arrival waiting

time

“End–to–end solution enables the bank to process applications, capture customer information, track and monitor the status of debit card generation, process cheque book request and welcome kit dispatch, more efficiently”

3 of 6

Key Benefits and ROI

Benefits accrued to the bank were both direct and indirect.

In addition to reduction in operating costs, travel and

communication expenses, office stationaries, infrastructure

usage, printing and postage costs, the bank also achieved

enhanced employee productivity and efficiency.

Key Benefits• Allowed real-time integration with the bank's core

system and other applications

• Enabled the bank to easily capture extensive customer

information as per “Know Your Customer” norms for

statutory compliance and audits

• Reduced TAT for Account opening and other processes

• Better archiving system, providing better and faster

access to documents and customer information

• Flexible solution, in terms of incorporating changes in

short durations in accordance with business

requirements

• Ease in handling complex processes having multiple if-

else-then condition

• Scalable solution that enables faster rollout of initiatives

and handle increasing business volumes

• Unified interface for all the underlying applications

providing business users with enhanced ease of usage

and perform multiple tasks through single system

access

• Enhanced performance tracking of the business users,

process and TAT

• Extended availability of the solution by providing

secured access to the bank's Direct Selling Agents

4 of 6

The Solution

Based on the bank's requirements, Newgen developed a

customized solution, consisting of the following products:

TM • OmniFlow – workflow solution

TM• OmniDocs – document management solution

TM• OmniScan (OmniCapture) – image capture and

indexing solution

In the initial phase, Newgen helped the bank automate one

of its most critical processes, the Account Opening process.

Integrated with the bank's existing core application, the

solution provides easier and faster data exchange across

systems. Buoyed by the results achieved within a short time

of deployment, the bank also implemented and automated

a number of other key processes such as Customer and

Account Maintenance, Term Deposit Initiation and

Maintenance on the BPM platform. At present, the solution

has been implemented across 43 branches of the bank and

supports 706 users. Every month, more than 61,000

documents are scanned and imported into the workflow for

processing. For Account Opening, the system processes

approximately 245 applications every day and can be easily

scaled up to meet any future requirement of the bank.

Account Opening process: The new system allows users

to capture relevant information and customer signoff at the

branches itself before the case files move to the Central

Processing Department (CPD). Instead of customers having

to submit complex forms, the system automatically

generates the required forms. The branches update these

forms online and take customer signoff before uploading in

the system. On completion of the mandatory branch level

activities, the files move to the CPD immediately for further

processing. Through real time integration with the core

system, CPD users directly initiate the Account Opening

process from the workflow solution. Through integration

with the SMS system, the solution enabled the team to

communicate to customers within 10-15 minutes of their

account becoming operational. The solution also generates

the welcome letter within 30 minutes of account activation.

Post account activation, CPD is able to track and monitor

the dispatch of the welcome kits to customers through the

courier system, which has also been integrated with the

workflow solution.

Some of the unique features of the solution were:

Key Features:

• Real-time integration with core system and other

existing applications

• Searching for existing customer record and

comprehensive validation check at the branch level

• User friendly interface

• Direct updating of customer information in the core

banking system through real-time integration

• Generation of complete audit trail to view history of

events taken place for any record

• Display of relevant information from the core application

reducing information searching and retrieving time

• Automatic generation of relevant documents at

different worksteps of the process including the

welcome letter

• Tracking and monitoring of process and user

performance

• Scanned documents can be introduced into the

workflow from any location, providing instant access for

processing and eliminating document-arrival waiting

time

“End–to–end solution enables the bank to process applications, capture customer information, track and monitor the status of debit card generation, process cheque book request and welcome kit dispatch, more efficiently”

3 of 6

Key Benefits and ROI

Benefits accrued to the bank were both direct and indirect.

In addition to reduction in operating costs, travel and

communication expenses, office stationaries, infrastructure

usage, printing and postage costs, the bank also achieved

enhanced employee productivity and efficiency.

Key Benefits• Allowed real-time integration with the bank's core

system and other applications

• Enabled the bank to easily capture extensive customer

information as per “Know Your Customer” norms for

statutory compliance and audits

• Reduced TAT for Account opening and other processes

• Better archiving system, providing better and faster

access to documents and customer information

• Flexible solution, in terms of incorporating changes in

short durations in accordance with business

requirements

• Ease in handling complex processes having multiple if-

else-then condition

• Scalable solution that enables faster rollout of initiatives

and handle increasing business volumes

• Unified interface for all the underlying applications

providing business users with enhanced ease of usage

and perform multiple tasks through single system

access

• Enhanced performance tracking of the business users,

process and TAT

• Extended availability of the solution by providing

secured access to the bank's Direct Selling Agents

4 of 6

Other Benefits

• Improved productivity and efficiency of employees –

with reduction in non-core activities, branch executives

are able to cross-sell other products

• Improved quality of data being captured through in-

built validations and checks

• Removal of work duplication by restricting data entry at

the branch operations only

• Identification of discrepancies at an earlier stage and

their faster resolution through checking and validation

utilities while doing data entry at the branch level

• Scaling up of operational activities, enabling the bank

to keep pace with business growth and demands

• Improved customer satisfaction through quicker and

better servicing, reduction in the requirement of

physical forms, and reduced customer response

timelines

#ROI of 190% has been achieved by the Abu Dhabi Commercial Bank over one year

7 of 8

# Refer “Methodology” section for details on how Return on Investments (ROI) has been calculated

* As per data provided by Newgen’s client

5 of 6

Methodology

The ROI calculation represents the relative value of a

project's cumulative net benefits over the analysis period,

divided by the project's cumulative costs, expressed as a

percentage. In a formula, this can be represented as:

ROI = cumulative net benefit / total costs. For Abu Dhabi

Commercial Bank, the ROI it achieved from the

implementation of Newgen's BPM solution was derived on

the basis of total benefits achieved and investments made

by the company over a period of one year.

Investments include both one time and annual recurring

costs incurred by the bank, for components like:

• Hardware and software

• Implementation and initial license cost,

• Maintenance and production support

• User training

Benefits were calculated by quantifying the returns

achieved through TAT improvements, higher employee

productivity and reduction in various cost heads. In case of

Abu Dhabi Commercial Bank, some of the benefit areas

evaluated were:

• Resource savings – from reduced hirings

• Time savings – reduction in processing time

• Capital expense reductions – savings in expenses such

as facilities, workstations, rentals

• Productivity benefits – increase in volumes of

transactions processed per day

The above mentioned data and information was sourced

through the following:

• Primary Research (customized questionnaire)

• Secondary Research (Third Party Industry Reports and

Deloitte Global Benchmarks and Survey Reports)

6 of 6

Other Benefits

• Improved productivity and efficiency of employees –

with reduction in non-core activities, branch executives

are able to cross-sell other products

• Improved quality of data being captured through in-

built validations and checks

• Removal of work duplication by restricting data entry at

the branch operations only

• Identification of discrepancies at an earlier stage and

their faster resolution through checking and validation

utilities while doing data entry at the branch level

• Scaling up of operational activities, enabling the bank

to keep pace with business growth and demands

• Improved customer satisfaction through quicker and

better servicing, reduction in the requirement of

physical forms, and reduced customer response

timelines

#ROI of 190% has been achieved by the Abu Dhabi Commercial Bank over one year

7 of 8

# Refer “Methodology” section for details on how Return on Investments (ROI) has been calculated

* As per data provided by Newgen’s client

5 of 6

Methodology

The ROI calculation represents the relative value of a

project's cumulative net benefits over the analysis period,

divided by the project's cumulative costs, expressed as a

percentage. In a formula, this can be represented as:

ROI = cumulative net benefit / total costs. For Abu Dhabi

Commercial Bank, the ROI it achieved from the

implementation of Newgen's BPM solution was derived on

the basis of total benefits achieved and investments made

by the company over a period of one year.

Investments include both one time and annual recurring

costs incurred by the bank, for components like:

• Hardware and software

• Implementation and initial license cost,

• Maintenance and production support

• User training

Benefits were calculated by quantifying the returns

achieved through TAT improvements, higher employee

productivity and reduction in various cost heads. In case of

Abu Dhabi Commercial Bank, some of the benefit areas

evaluated were:

• Resource savings – from reduced hirings

• Time savings – reduction in processing time

• Capital expense reductions – savings in expenses such

as facilities, workstations, rentals

• Productivity benefits – increase in volumes of

transactions processed per day

The above mentioned data and information was sourced

through the following:

• Primary Research (customized questionnaire)

• Secondary Research (Third Party Industry Reports and

Deloitte Global Benchmarks and Survey Reports)

6 of 6

The ROI analysis was commissioned by Newgen and has been done by Deloitte for the the clients provided by Newgen. The analysis was done based

on data provided by Newgen and its client and Deloitte makes no assertions on the potential ROI that other organizations might receive by using

Newgen's solutions. Deloitte has verified the data but due to nature of the study and solution implementation timelines involved certain

assumptions have been made to derive the potential ROI therefore it can impact the accuracy of the data and analysis. This case study is a validation

of the benefits that one of the leading Middle East bank, derived from implementing Newgen solutions in its operational and business scenario and

is not meant to be used for competitive product analysis. The study was commissioned only for calculation of the ROI derived from implementing

Newgen's solutions and not to endorse its solutions by Deloitte.

This document contains general information only and Deloitte Touché Tohmatsu India Pvt. Ltd is not, by means of this publication, rendering

accounting, business, financial, investment, legal, tax or other professional advice or services. This publication is not a substitute for such

professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or

taking any action that may affect your business, you are advised to consult a qualified professional advisor. Deloitte, its affiliates and related entities

shall not be responsible for any loss sustained by any person who makes decisions based solely on the information present in this publication.

Deloitte, its affiliates and related entities shall not be responsible for any future changes or modifications done to the signed off published

document.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member firms, each of which is a legally separate and

independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu and its

member firms.

About Newgen

Newgen Software Technologies Limited is the market leader in Business Process Management (BPM) and Enterprise Content Management (ECM),

with a global footprint of about 750 installations in over 35 countries. More than 100 of these implementations are large, mission-critical solutions

deployed at world's leading BFSI, BPO and Fortune Global 500 companies.

Newgen is recognized by distinguished analyst firms like Frost and Sullivan as A 'Hot Company to Watch for' in their global ECM Market report,

2009 and by IDC in its exclusive report “Newgen Software: Global Leader in Business Process Management and Document Management

Solutions”. Newgen is a winner of prestigious award, such as CNBC-TV18, “Emerging India Award 2008”.

With HSBC and SAP investment, Newgen is one of the rare product companies to have backing of both leading financial and technology companies

of the world. Newgen’s Quality Systems are certified against ISO 9001:2008 and Information Security Standard, ISO 27001:2005. Newgen has been

assessed at CMMI Level3.

Disclaimer

Newgen Software Inc.

1364 Beverly Road, Suite 300

McLean, VA 22101

Tel: +1-703-439-0703

Email: [email protected]

Corporate Office

Newgen Software Technologies Ltd.

A-6, Satsang Vihar Marg,

Qutab Institutional Area,

New Delhi - 110 067 INDIA

Tel: +91-11-4077 0100, 2696 3571, 2696 4733

Fax: +91-11-2685 6936

Email: [email protected]