Default & Loss Rates of Structured Finance Securities ... · Special Comment Default & Loss Rates...

48

Special Comment Default & Loss Rates of Structured Finance Securities: 1993-2005 Summary Opinion This Special Comment presents Moody's fourth annual report of the default, impairment, and loss rates of global structured finance securities, covering the credit performance through year-end 2005 of all structured finance securities issued since 1993. The following are the highlights of this report: • The credit performance of structured finance securities improved sharply in 2005. The number of newly impaired tranches fell to 98 in 2005 from 213 in 2004, reflecting a large drop in the number of newly impaired US ABS and global CDO securities. Declining impairments, coupled with strong growth in the number of outstand- ing ratings, drove the one-year impairment rate – the number of newly impaired tranches as a percentage of the total tranches outstanding at the beginning of a year – down to historical lows. The one-year investment-grade impairment rate fell to 0.05% in 2005 from 0.4% in 2004, while the one-year speculative-grade impairment rate dropped to 2.7% from 5.4%. • Five-year loss rates as a percent of original balances have averaged 0.017% for Aaa-rated, 0.7% for Aa-rated, 1.8% for single-A-rated, 5.8% for Baa-rated, and 11.7% for speculative-grade-rated securities. Historical average loss rates, however, have varied substantially across asset classes, with those in the CMBS and RMBS sectors being the lowest among all structured finance sectors. • When weighted by dollar volume, the average credit loss rate across all structured finance has been very low, which should be expected since 83% (by volume) of all securities have been rated Aaa at issuance. Within five years of origination, the volume-weighted aggregate loss rate has been about 0.49%. • By the end of 2005, 1,095 securities issued since 1993 had become materially impaired. This represents roughly 2.3% of the 47,519 structured finance tranches and 4.4% of the 13,619 transactions studied. Of the $6.2 trillion worth of dollar-denominated structured finance tranches in the sample, 0.47% (by original balance) became impaired. • Final loss severity rates on impaired securities have averaged 53% as a share of original balances for the 352 impaired securities that have reached "maturity" (i.e., with no remaining principal balance) as of year-end 2005. The final loss severity rates of all impaired securities including those with balances still outstanding are expected to be lower. Final loss severity rates have historically been higher on matured ABS and CDO defaults than on matured RMBS and HEL defaults, and higher on securities rated lower at issuance than those rated higher at issuance. April 2006 New York Jian Hu 1.212.553.1653 Hadas Alexander Debjani Roy Julia Tung Richard Cantor Gus Harris Detlef Scholz Nicolas Weill Contact Phone

Transcript of Default & Loss Rates of Structured Finance Securities ... · Special Comment Default & Loss Rates...

Special CommentApril 2006

New YorkJian Hu 1.212.553.1653Hadas AlexanderDebjani RoyJulia TungRichard CantorGus HarrisDetlef ScholzNicolas Weill

Contact Phone

Default & Loss Rates of Structured Finance Securities: 1993-2005

Summary Opinion

This Special Comment presents Moody's fourth annual report of the default, impairment, and loss rates of globalstructured finance securities, covering the credit performance through year-end 2005 of all structured financesecurities issued since 1993. The following are the highlights of this report:• The credit performance of structured finance securities improved sharply in 2005. The number of newly

impaired tranches fell to 98 in 2005 from 213 in 2004, reflecting a large drop in the number of newly impaired USABS and global CDO securities. Declining impairments, coupled with strong growth in the number of outstand-ing ratings, drove the one-year impairment rate – the number of newly impaired tranches as a percentage of thetotal tranches outstanding at the beginning of a year – down to historical lows. The one-year investment-gradeimpairment rate fell to 0.05% in 2005 from 0.4% in 2004, while the one-year speculative-grade impairment ratedropped to 2.7% from 5.4%.

• Five-year loss rates as a percent of original balances have averaged 0.017% for Aaa-rated, 0.7% for Aa-rated, 1.8%for single-A-rated, 5.8% for Baa-rated, and 11.7% for speculative-grade-rated securities. Historical average lossrates, however, have varied substantially across asset classes, with those in the CMBS and RMBS sectors being thelowest among all structured finance sectors.

• When weighted by dollar volume, the average credit loss rate across all structured finance has been very low,which should be expected since 83% (by volume) of all securities have been rated Aaa at issuance. Within fiveyears of origination, the volume-weighted aggregate loss rate has been about 0.49%.

• By the end of 2005, 1,095 securities issued since 1993 had become materially impaired. This represents roughly2.3% of the 47,519 structured finance tranches and 4.4% of the 13,619 transactions studied. Of the $6.2 trillionworth of dollar-denominated structured finance tranches in the sample, 0.47% (by original balance) becameimpaired.

• Final loss severity rates on impaired securities have averaged 53% as a share of original balances for the 352impaired securities that have reached "maturity" (i.e., with no remaining principal balance) as of year-end 2005.The final loss severity rates of all impaired securities including those with balances still outstanding are expected tobe lower. Final loss severity rates have historically been higher on matured ABS and CDO defaults than on maturedRMBS and HEL defaults, and higher on securities rated lower at issuance than those rated higher at issuance.

Figure 1 – New Impairments in 2005 and Lifetime Impairments since 19932005 1993-2005

Number of New Impairments

One-Year Impairment Rate

Number of Impairments

Lifetime Impairment Rate

Invest. Grade

Spec. Grade

Invest. Grade

Spec. Grade

Invest. Grade

Spec. Grade

Invest. Grade

Spec. Grade

US ABS 4 36 0.04% 5.6% 402 139 3.2% 22.9%US CMBS 0 32 0.00% 2.9% 15 81 0.5% 6.5%US RMBS 3 8 0.07% 1.4% 90 60 1.3% 6.0%Global CDOs 4 11 0.10% 1.7% 181 122 3.7% 19.8%European SF ex CDOs 0 0 0.00% 0.0% 1 1 0.0% 0.7%SF in Other Regions 0 0 0.00% 0.0% 2 1 0.1% 0.6%All SF 11 87 0.05% 2.7% 691 404 2.2% 10.7%

Note: The categorization of investment (invest.) grade and speculative (spec.) grade for the 2005 data is based on the security's rating at the beginning of 2005. For the overall historical totals during 1993-2005, the categorization is by their original rating. Lifetime impairment rates are computed by dividing the total number of impairments from 1993 to 2005 by all the securities issued from 1993 to 2004 (securities issued in 2005 are not included.) SF stands for "structured finance," which includes ABS (including HELs), CMBS, RMBS, and CDOs. See Appendix 1 for a description of the data sample and glossary.

2 Moody’s Special Comment

Table of ContentsPage

Summary Opinion .................................................................................................................................. 1

Overview of Global Structured Finance Material Impairments in 2005 .............................................. 4

Analysis of Material Impairments and Payment Defaults by Credit Event ......................................... 6Distribution of Material Impairments by Credit Event ......................................................................................... 6Analyzing the Cure Rate of Payment Defaults .................................................................................................... 6Comparing Reasons Underlying Uncured Payment Defaults by Sector ............................................................... 8

Analysis of Material Impairments by Sector, Rating, and Vintage ...................................................... 8US ABS: Impairment Rates Dropped Precipitously ............................................................................................. 8US HEL: Impairment Rates Edged Down .......................................................................................................... 10US CMBS: Impairment Rates Remained Low ................................................................................................... 11US RMBS: Impairment Rates Rose in the Speculative-Grade Category ............................................................. 13Global CDOs: Impairment Rates Plunged Across All Categories ....................................................................... 14

Loss Severity Rates on Impaired Tranches by Sector, Rating, and Horizon ..................................... 17Final LGD of Matured Defaults in All Structured Finance Averaged 53% .......................................................... 17Estimated Final LGD Rates on Impaired RMBS and HEL Tranches Averaged 32% ............................................ 19Estimated Final LGD Rates on Impaired CDO Tranches Averaged 72% ............................................................ 20Comparing LGD Rates by Time Horizon ........................................................................................................... 21

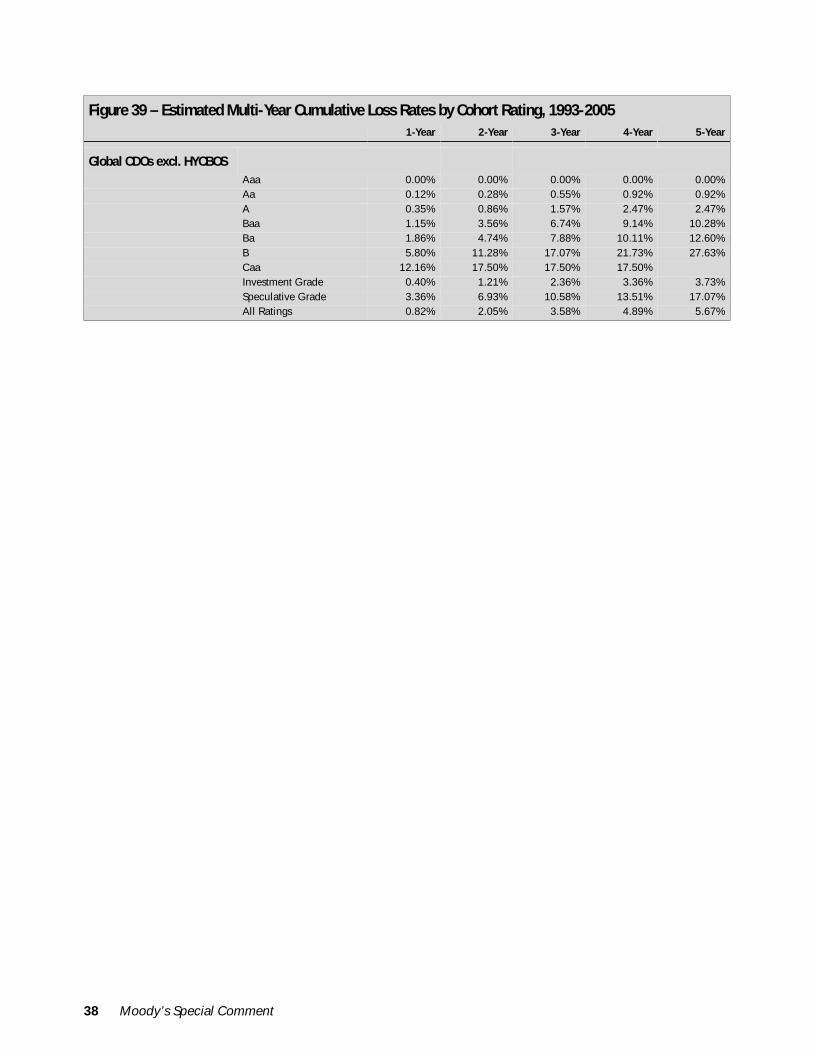

Multi-Year Cumulative Loss Rates by Rating and Sector .................................................................. 22

Appendix 1: Descriptions of Data Sample and Glossary ................................................................... 24Description of Data Sample ............................................................................................................................. 24Glossary ......................................................................................................................................................... 24

Appendix 2: How to Calculate Multi-Year Material Impairment Rate and LGD Rate ........................ 27Cumulative Impairment Rate by Cohort Rating ................................................................................................ 27Cumulative Impairment Rate by Original Rating ............................................................................................... 28Multi-Year Cumulative LGD Rates ................................................................................................................... 29

Appendix 3: Impairment Rates by Rating ........................................................................................... 30

Appendix 4: Estimated Loss Rates by Rating ..................................................................................... 36

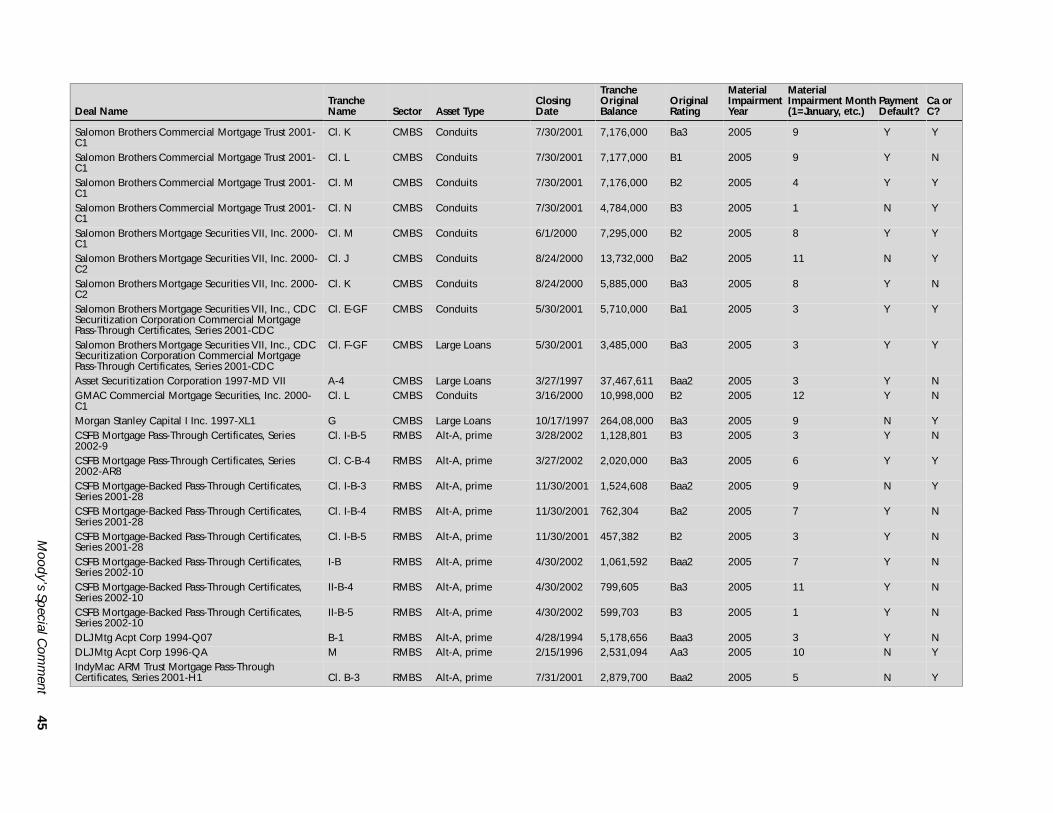

Appendix 5: List of 2005 New Impairments ....................................................................................... 41

Related Research ................................................................................................................................ 46

Moody’s Special Comment 3

Overview of Global Structured Finance Material Impairments in 2005

2005 was a year of strong growth and superb credit performance for global structured finance. The sector continued togrow at a brisk rate with traditional securitizations remaining strong and new products and new features beingintroduced into the market. The year 2005 also marked the first time asset-backed credit default swaps (ABS CDS)were introduced to the market, potentially enhancing the liquidity of ABS securities and showing that the market isbecoming increasingly mature.

With the benign corporate environment, strong real estate markets, and low interest rates, the structured financesector saw only 98 tranches become newly impaired in 2005. This number is substantially lower than those observedduring 2002-2004 and similar to the level last seen in 2001 (see Figure 2). Moreover, roughly 50 previously impairedtranches, or about 4.8% of the total 1051 impairments as of year-end 2004, were cured in 2005, as collateral assetvaluation strengthened and interest payments reverted to current.

Both the US ABS and global CDO sectors dramatically improved with only 40 and 15 new impairments in 2005,respectively, compared to 140 for US ABS and 41 for global CDOs in 2004. In particular, manufactured housing (MH)loan-backed ABS and high-yield corporate bond-backed CDOs (HYCBOs) saw the number of new impairmentsdwindle, with just three for MH and none for HY CBOs in 2005, down from 76 and 11 in 2004, respectively.

The CMBS, HEL, and RMBS sectors, supported by the continuing strong real estate markets and the steady andlow interest rate environment, performed well and similarly in 2005 and 2004. There were 32 newly impaired tranchesin CMBS, 20 in HEL, and 11 in RMBS in 2005, up slightly from 23, 16, and 7 in the prior year. Moreover, 19 of the42 impaired CMBS tranches in 2004 were subsequently cured in 2005.

The structured finance sector outside the United States excluding CDOs did not have any newly impairedtranches in 2005. The sector's total number of impairments remains at only five for the entire sample period.

Declining impairments, coupled with strong growth in the number of outstanding ratings, drove the one-yearimpairment rate – the number of newly impaired tranches as a percentage of the total tranches outstanding at thebeginning of a year – down to historical lows. Within the speculative-grade category, which includes securities ratedBa, single-B or Caa, the one-year impairment rate fell to 2.7% in 2005 from 5.4% in 2004, and within the investment-grade category, which includes securities rated Baa or above, the impairment rate went down to 0.05% from 0.4% (seeFigure 3).

Figure 2 – Number of New Material Impairments

0

50

100

150

200

250

300

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Other SF (ex CDOs)

Europe SF (ex CDOs)

Global CDOs

US RMBS

US CMBS

US ABS

4 Moody’s Special Comment

The improvements in the impairment rates were broad-based, affecting all sectors. In the investment-gradeportion of the market, which comprises about 99% of total issuance volume or 90% of all structured finance securities,the one-year impairment rate declined across all sectors in 2005, especially in the ABS and CDOs sectors (see Figure4). In addition, the investment-grade impairment rate was almost zero in the ABS (excluding MH and HEL) sector forthe first time since 2001, and zero for the CMBS sector for the second year in a row.

Figure 3 – Investment-Grade and Speculative-Grade One-Year Impairment Rates in Structured Finance Overall

Figure 4 – Investment-Grade One-Year Impairment Rates by Sector

0.0%

0.4%

0.8%

1.2%

1.6%

2.0%

1996 1997 1998 1999 2000 2001 2002 2003 2004 20050%

2%

4%

6%

8%

10%

12%

Spec. Grade (right axis)

Invest. Grade (left axis)

19961997

19981999

20002001

20022003

20042005

US RMBS

US CMBS

US HEL

US ABS ex MH HELCDOs ex HY CBO

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

Moody’s Special Comment 5

Analysis of Material Impairments and Payment Defaults by Credit Event

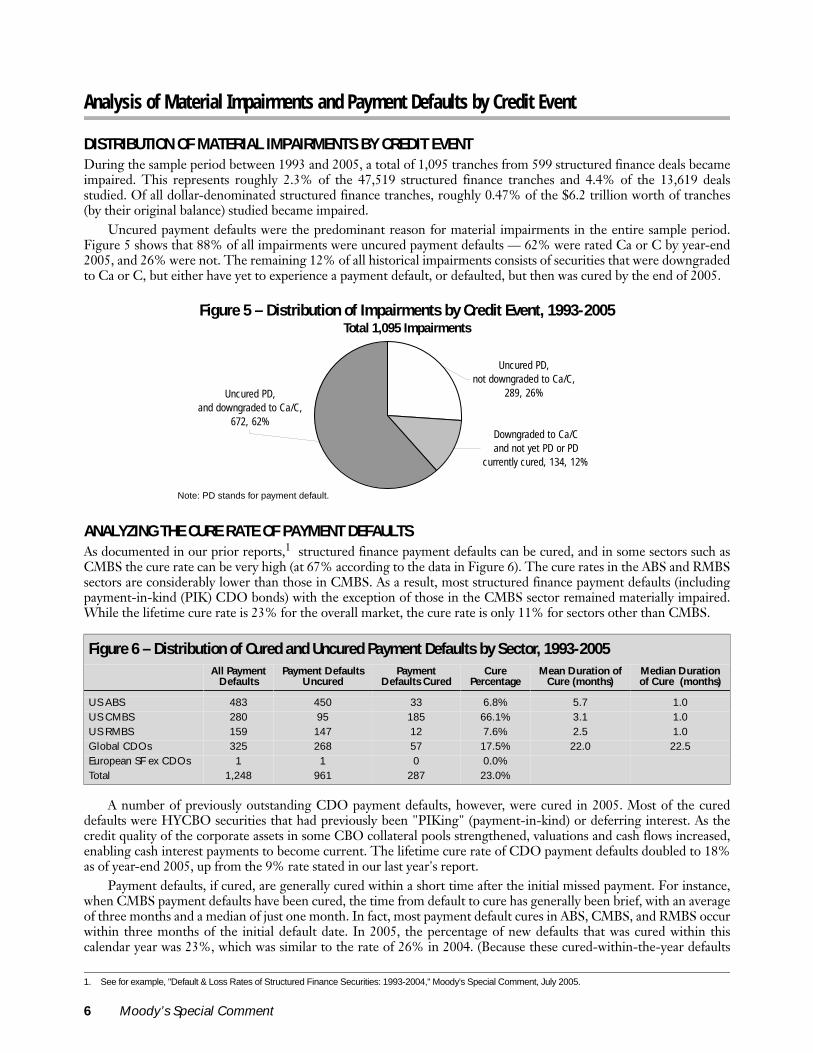

DISTRIBUTION OF MATERIAL IMPAIRMENTS BY CREDIT EVENTDuring the sample period between 1993 and 2005, a total of 1,095 tranches from 599 structured finance deals becameimpaired. This represents roughly 2.3% of the 47,519 structured finance tranches and 4.4% of the 13,619 dealsstudied. Of all dollar-denominated structured finance tranches, roughly 0.47% of the $6.2 trillion worth of tranches(by their original balance) studied became impaired.

Uncured payment defaults were the predominant reason for material impairments in the entire sample period.Figure 5 shows that 88% of all impairments were uncured payment defaults — 62% were rated Ca or C by year-end2005, and 26% were not. The remaining 12% of all historical impairments consists of securities that were downgradedto Ca or C, but either have yet to experience a payment default, or defaulted, but then was cured by the end of 2005.

ANALYZING THE CURE RATE OF PAYMENT DEFAULTSAs documented in our prior reports,1 structured finance payment defaults can be cured, and in some sectors such asCMBS the cure rate can be very high (at 67% according to the data in Figure 6). The cure rates in the ABS and RMBSsectors are considerably lower than those in CMBS. As a result, most structured finance payment defaults (includingpayment-in-kind (PIK) CDO bonds) with the exception of those in the CMBS sector remained materially impaired.While the lifetime cure rate is 23% for the overall market, the cure rate is only 11% for sectors other than CMBS.

A number of previously outstanding CDO payment defaults, however, were cured in 2005. Most of the cureddefaults were HYCBO securities that had previously been "PIKing" (payment-in-kind) or deferring interest. As thecredit quality of the corporate assets in some CBO collateral pools strengthened, valuations and cash flows increased,enabling cash interest payments to become current. The lifetime cure rate of CDO payment defaults doubled to 18%as of year-end 2005, up from the 9% rate stated in our last year's report.

Payment defaults, if cured, are generally cured within a short time after the initial missed payment. For instance,when CMBS payment defaults have been cured, the time from default to cure has generally been brief, with an averageof three months and a median of just one month. In fact, most payment default cures in ABS, CMBS, and RMBS occurwithin three months of the initial default date. In 2005, the percentage of new defaults that was cured within thiscalendar year was 23%, which was similar to the rate of 26% in 2004. (Because these cured-within-the-year defaults

Figure 5 – Distribution of Impairments by Credit Event, 1993-2005Total 1,095 Impairments

Note: PD stands for payment default.

1. See for example, "Default & Loss Rates of Structured Finance Securities: 1993-2004," Moody's Special Comment, July 2005.

Figure 6 – Distribution of Cured and Uncured Payment Defaults by Sector, 1993-2005All Payment

DefaultsPayment Defaults

UncuredPayment

Defaults CuredCure

PercentageMean Duration of

Cure (months)Median Duration of Cure (months)

US ABS 483 450 33 6.8% 5.7 1.0US CMBS 280 95 185 66.1% 3.1 1.0US RMBS 159 147 12 7.6% 2.5 1.0Global CDOs 325 268 57 17.5% 22.0 22.5European SF ex CDOs 1 1 0 0.0%Total 1,248 961 287 23.0%

Uncured PD, not downgraded to Ca/C,

289, 26%

Downgraded to Ca/C and not yet PD or PD

currently cured, 134, 12%

Uncured PD, and downgraded to Ca/C,

672, 62%

6 Moody’s Special Comment

are not outstanding at year-end, they are not included in the total number of new material impairments regularlyreported for each year-end.)

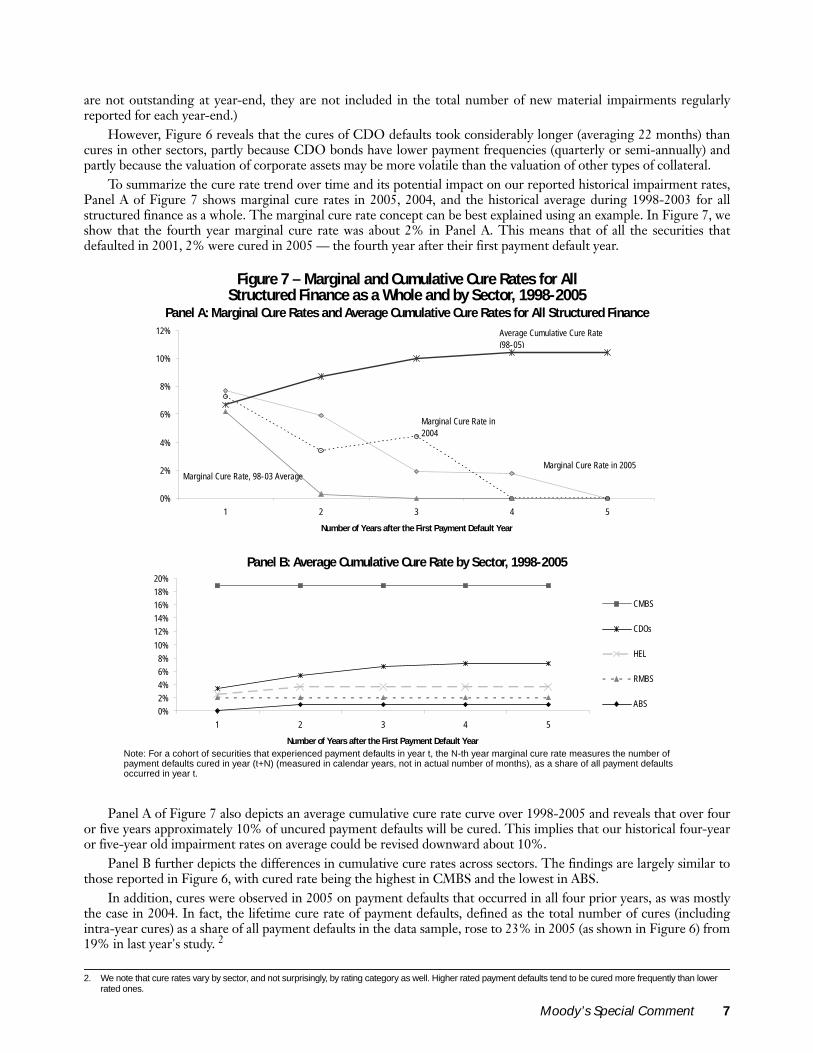

However, Figure 6 reveals that the cures of CDO defaults took considerably longer (averaging 22 months) thancures in other sectors, partly because CDO bonds have lower payment frequencies (quarterly or semi-annually) andpartly because the valuation of corporate assets may be more volatile than the valuation of other types of collateral.

To summarize the cure rate trend over time and its potential impact on our reported historical impairment rates,Panel A of Figure 7 shows marginal cure rates in 2005, 2004, and the historical average during 1998-2003 for allstructured finance as a whole. The marginal cure rate concept can be best explained using an example. In Figure 7, weshow that the fourth year marginal cure rate was about 2% in Panel A. This means that of all the securities thatdefaulted in 2001, 2% were cured in 2005 — the fourth year after their first payment default year.

Panel A of Figure 7 also depicts an average cumulative cure rate curve over 1998-2005 and reveals that over fouror five years approximately 10% of uncured payment defaults will be cured. This implies that our historical four-yearor five-year old impairment rates on average could be revised downward about 10%.

Panel B further depicts the differences in cumulative cure rates across sectors. The findings are largely similar tothose reported in Figure 6, with cured rate being the highest in CMBS and the lowest in ABS.

In addition, cures were observed in 2005 on payment defaults that occurred in all four prior years, as was mostlythe case in 2004. In fact, the lifetime cure rate of payment defaults, defined as the total number of cures (includingintra-year cures) as a share of all payment defaults in the data sample, rose to 23% in 2005 (as shown in Figure 6) from19% in last year's study. 2

Figure 7 – Marginal and Cumulative Cure Rates for All Structured Finance as a Whole and by Sector, 1998-2005

Panel A: Marginal Cure Rates and Average Cumulative Cure Rates for All Structured Finance

Panel B: Average Cumulative Cure Rate by Sector, 1998-2005

Note: For a cohort of securities that experienced payment defaults in year t, the N-th year marginal cure rate measures the number of payment defaults cured in year (t+N) (measured in calendar years, not in actual number of months), as a share of all payment defaults occurred in year t.

2. We note that cure rates vary by sector, and not surprisingly, by rating category as well. Higher rated payment defaults tend to be cured more frequently than lower rated ones.

0%

2%

4%

6%

8%

10%

12%

1 2 3 4 5

Number of Years after the First Payment Default Year

Average Cumulative Cure Rate(98-05)

Marginal Cure Rate in 2004

Marginal Cure Rate in 2005Marginal Cure Rate, 98-03 Average

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1 2 3 4 5

Number of Years after the First Payment Default Year

CMBS

CDOs

HEL

RMBS

ABS

Moody’s Special Comment 7

COMPARING REASONS UNDERLYING UNCURED PAYMENT DEFAULTS BY SECTOR For payment defaults that remained uncured, the underlying reasons have varied by sector. In the CMBS sector, 41tranches have suffered principal losses as of year-end 2005, compared with 50 tranches experiencing uncured interestshortfalls (see Figure 8). Historically, a total of 185 CMBS securities recorded some interest shortfalls, but most ofthem were cured.

In the CDO sector, 44 or about 17% of the 257 payment defaults had suffered principal losses. Most of the CDOdefaults were PIKing or simply deferring interests. By contrast, in the ABS and RMBS sectors, defaulted securities thathad experienced only interest shortfalls were a minority, making up 19% of all ABS defaults and only 1% of all RMBSdefaults during the sample period. As we showed in prior-year reports, defaults with principal losses are much lesslikely to be cured than those experiencing only interest shortfalls. 3

Analysis of Material Impairments by Sector, Rating, and Vintage

US ABS: IMPAIRMENT RATES DROPPED PRECIPITOUSLYThe US ABS sector, including HEL, demonstrated much-improved performance in 2005, as the number of newimpairments in the troubled manufactured housing loan, franchise loan, and aircraft and equipment lease categoriesfinally dwindled to single digits. While the number of new HEL impairments exceeded those of other ABS assetclasses, its impairment rate remained very low relative to its large number of securities outstanding (see Figure 9).

3. See Moody's Special Comment, "Default & Loss Rates of Structured Finance Securities: 1993-2004," July 2005.

Figure 8 – Number of Uncured Payment Defaults with Interest Shortfalls and Principal Losses by Sector, 1993-2005

Figure 9 – 2005 US ABS New Impairments by Asset Class, Compared to Their Historical Totals

Number of New Impairments in 2005

Securities Outstanding

in 2005

2005 Impairment

Rate

Number of Impairments, 1993-2005

Securities Issued, 1993-2004

Lifetime Impairment Rate

Autos 0 391 0.0% 10 884 1.1%Cards 0 852 0.0% 12 1,634 0.7%Franchise 6 104 5.8% 60 165 36.4%HEL 20 6,381 0.3% 108 7,640 1.4%Health Care 0 6 0.0% 26 32 81.3%Leases 5 224 2.2% 55 507 10.8%Manu. Housing 3 430 0.7% 261 783 33.3%RVs, Trucks 3 57 5.3% 5 119 4.2%Small Business 3 141 2.1% 4 151 2.6%Other ABS 0 1,024 0.0% 0 1,388 0.0%All US ABS 40 9,610 0.4% 541 13,303 4.1%

Note: RVs are recreational vehicles.

0

50

100

150

200

250

300

350

400

US ABS Global CDOs US RMBS US CMBS

Interest Shortfall Only Principal Losses

8 Moody’s Special Comment

Only three manufactured housing and six franchise loan ABS tranches became newly impaired in 2005, which ismuch fewer than the number of impairments in these categories in recent years. Furthermore, 10 MH tranches thathad previously experienced interest shortfalls (some for more than two years) repaid all their interest shortfalls in 2005and became cured, mainly because the housing market remained strong and recovery values increased. These suggestthat the troubles in these two severely impaired ABS categories finally ran out of steam.

In the aircraft and equipment lease categories, two tranches of an Aircraft Finance Trust transaction missedinterest payments in 2005, and two tranches of a DVI VIII transaction were downgraded to Ca or C, althoughpayment defaults were not yet observed on these two tranches. In addition, one tranche from an aircraft transaction(ALPS 96-1) experienced substantial write-downs in December 2005.

In addition, two ABS tranches backed by the retail installment sales contracts of recreational vehicles (RVs) missedinterest payments in 2005 for the first time. A third tranche from a RV deal was originated by Green Tree andexperienced interest shortfalls first in 2002, but was cured three months later. In 2005, however, this security hassuffered substantial losses of principal.

Finally, three small business loan ABS issued in 2000 and originally sponsored by First International Bank (FIB)were downgraded into the Ca/C category in 2005. The pools underlying these transactions performed poorly as aresult of the manufacturing sector's recession in 2000 and 2001.

By rating at the beginning of the year, no securities rated single-A or above suffered any new impairments in 2005(Figure 10), while the Baa one-year impairment rate was the lowest in five years. The one-year impairment rates in thespeculative-grade categories were also much lower in 2005.

The credit performance of US ABS securities also varied across vintages (Figure 11). Tranches issued in 1999 and2000 performed much more poorly than those issued since 2001. For example, about 20% of the 1999 and 2000vintage Baa tranches were impaired, but only 9% of the Baa-rated securities issued in 2001 were impaired. Tranchesissued in 2002 and 2003 have so far performed very well. The higher impairment rates in the Aa category stemmedmainly from problems in the manufactured housing loan, franchise loan, and health care receivable ABS categories.

Figure 10 – US ABS One-Year Impairment Rates by Rating at the Beginning of the YearRating at the Beginning of the Year 2001 2002 2003 2004 2005

Aaa 0.00% 0.40% 0.00% 0.00% 0.00%Aa 0.37% 1.45% 0.00% 1.42% 0.00%A 0.67% 0.32% 0.27% 0.69% 0.00%Baa 1.84% 2.36% 4.50% 1.52% 0.16%Ba 5.61% 25.38% 18.36% 12.36% 1.71%B 18.35% 24.76% 38.67% 20.69% 7.43%Caa 0.00% 60.87% 42.62% 55.86% 23.03%Investment Grade 0.55% 0.87% 0.96% 0.77% 0.04%Speculative Grade 8.20% 26.25% 24.18% 19.22% 5.64%All Ratings 1.06% 2.51% 2.44% 1.98% 0.42%

Figure 11 – US ABS Lifetime Impairment Rates by Original Rating on Securities Issued during 1999-2003Original Rating 1999 Vintage 2000 Vintage 2001 Vintage 2002 Vintage 2003 Vintage

Aaa 1.5% 1.3% 1.8% 0.5% 0.0%Aa 15.6% 13.1% 5.2% 2.4% 0.3%A 8.8% 9.1% 4.1% 1.0% 0.2%Baa 18.8% 19.4% 8.7% 2.0% 0.1%Ba 50.0% 37.8% 37.3% 13.9% 2.4%B 70.0% 72.7% 0.0% 0.0% 0.0%Caa 0.0% n/a 100.0% n/a n/aInvestment Grade 8.9% 9.0% 4.5% 1.4% 0.1%Speculative Grade 53.7% 44.6% 36.4% 13.2% 2.1%All Ratings 11.3% 11.1% 6.0% 2.0% 0.2%

Note: Lifetime impairment rate is the total number of impaired securities to date as a share of all securities issued. No Caa-rated securities were issued in 2000, 2001, and 2003.

Moody’s Special Comment 9

As documented in our prior reports, impairment rates tend to exhibit seasoning patterns. We found that theseseasoning patterns also differed by rating. Figure 12 depicts that in the US ABS sector, the marginal impairment rates,measured by the number of new impairments as a share of all surviving (not previously impaired or withdrawn)securities at the beginning of a year, peaked in the fourth year for speculative-grade securities, and the fifth year forinvestment-grade securities.

The impairment rate experienced its steepest increase in the first three years after issuance. The differentialsbetween the two marginal impairment rates curves vary from roughly 6% in the second year to about 14% in thefourth year. Moreover, the impairment rates even six years after issuance can be material, as demonstrated by the levelof the curves in the fifth, sixth, and seventh year after issuance.

US HEL: IMPAIRMENT RATES EDGED DOWNThe HEL category has traditionally been categorized as an ABS asset class. In recent years, strong growth has made itthe largest segment within the ABS sector. In this section, we examine its impairment experiences separately.

In 2005, there were 20 new impairments in this sector, compared to 16 in 2004. The one-year impairment ratedropped to a five-year low of 0.3% of all securities outstanding at the beginning of 2005 (Figure 13). The one-yearimpairment rates of securities rated single-A or above have remained low for five years in a row, and the Baaimpairment rate was also on the decline at just 0.2% in 2005.

Most of the new 2005 HEL impairments were originated in 2000 and 2001. All but four involved subprimemortgage as their collateral. The remaining four impaired tranches were either backed by reperforming loans orbacked by nonperforming mortgage loans, which have experienced serious payment difficulties in the past.

Figure 12 – US ABS Marginal Impairment Rates by Years after Issuance, 1993-2005

Figure 13 – HEL One-Year Impairment Rates by Rating at the Beginning of the YearRating at the Beginning of the Year 2001 2002 2003 2004 2005

Aaa 0.00% 0.00% 0.00% 0.00% 0.00%Aa 0.00% 0.00% 0.00% 0.00% 0.00%A 0.41% 0.00% 0.00% 0.12% 0.00%Baa 0.85% 1.15% 1.66% 0.56% 0.20%Ba 3.92% 0.00% 10.14% 3.56% 2.88%B 13.33% 10.17% 17.86% 10.34% 20.00%Caa 0.00% 80.00% 71.43% 40.00% 25.00%Investment Grade 0.30% 0.28% 0.44% 0.19% 0.07%Speculative Grade 6.54% 5.15% 14.29% 5.84% 5.50%All Ratings 0.91% 0.71% 1.29% 0.43% 0.31%

0%

2%

4%

6%

8%

10%

1 2 3 4 5 6 7

Years after Issuance

0%

3%

6%

9%

12%

15%

18%

Spec. Grade (right axis)

Invest. Grade (left axis)

10 Moody’s Special Comment

While the overall performance in the HEL sector has been solid across all vintages, Figure 14 shows that the 1999vintage HEL securities on average performed worse than others. In addition, as of year-end 2005, the lifetimeimpairment rates among the 2001, 2002 and 2003 vintages were particularly low. HEL securities issued since 2003recorded no impairments.

The HEL sector also exhibits some interesting seasoning patterns. Figure 15 depicts the sector's steep increase inthe first four years after issuance in the marginal impairment rate of the speculative-grade category. Like in the USABS sector as a whole, investment-grade marginal impairment rates peaked in the fifth year, and then in the sixth andseven years, remained similar to the fifth year level.

US CMBS: IMPAIRMENT RATES REMAINED LOW The CMBS sector continued to exhibit excellent credit performance overall and a perfect record in the investment-grade category. For the second year in a row, no securities rated investment grade at the beginning of a year becameimpaired within the year (see Figure 16). There were 32 newly impaired tranches from 19 transactions in the CMBSsector, and all but three were conduit deals. The remaining three were large loan deals. Twenty of the impairedtranches were previously impaired, subsequently cured, and became impaired again in 2005. In other words, only 12securities experienced payment defaults for the first time in 2005.

Of the 32 newly impaired CMBS tranches in 2005, 19 were rated Caa, Ca or C as of year-end 2005 and wereexpected to sustain some losses ultimately. Only six of the 32 tranches have so far suffered principal losses.

Figure 14 – HEL Lifetime Impairment Rates by Original Rating on Securities Issued during 1999-2003Original Rating 1999 Vintage 2000 Vintage 2001 Vintage 2002 Vintage 2003 Vintage

Aaa 0.0% 0.0% 0.0% 0.0% 0.0%Aa 0.0% 0.0% 0.0% 0.0% 0.0%A 0.0% 2.8% 0.7% 0.0% 0.0%Baa 8.5% 11.4% 6.2% 0.7% 0.0%Ba 40.0% 0.0% 17.2% 4.2% 0.0%B 71.4% 0.0% 0.0% 0.0% 0.0%Caa n/a n/a n/a n/a n/aInvestment Grade 2.2% 3.5% 1.8% 0.2% 0.0%Speculative Grade 52.9% 0.0% 16.1% 3.8% 0.0%All Ratings 6.7% 3.3% 2.6% 0.3% 0.0%

Note: Lifetime impairment rate is the total number of impaired securities (to date) as a share of all securities issued.

Figure 15 – HEL Marginal Impairment Rates by Years after Issuance, 1993-2005

0%

2%

4%

6%

8%

10%

1 2 3 4 5 6 7

Years after Issuance

0%

3%

6%

9%

12%

15%

18%

Spec. Grade (right axis)

Invest. Grade (left axis)

Moody’s Special Comment 11

By rating at the beginning of the year, the one-year impairment rate in the speculative-grade category inched upto 2.9% in 2005 from 2.6% in 2004.

Within the CMBS sector, the 2000 vintage performed worse than other vintages (Figure 17).4 There were 28impaired securities in that vintage, and 14 of them experienced principal losses or were downgraded to Ca or C andwere expected to sustain significant principal losses. As a result, the lifetime impairment rates in both the investment-grade and speculative-grade categories were higher in the 2000 vintage than in other vintages.

The seasoning patterns of the marginal impairment rates for CMBS shared some similarities with those in theHEL sector, although there were also important distinctions. In the speculative-grade category, the marginalimpairment rates increased significantly over the first five years after issuance, peaking in the fifth year. By comparison,the marginal impairment rates for HEL peaked in the fourth year (see Figure 18).

In the investment-grade category, the seasoning pattern was much weaker because of the very small number ofimpairments in this CMBS category. Nonetheless, the marginal impairment rates increased in the first three yearsafter issuance before declining to zero in the fourth year.

Figure 16 – US CMBS One-Year Impairment Rates by Rating at the Beginning of the YearRating at the Beginning of the Year 2001 2002 2003 2004 2005

Aaa 0.00% 0.00% 0.00% 0.00% 0.00%Aa 0.00% 0.00% 0.00% 0.00% 0.00%A 0.00% 0.00% 0.23% 0.00% 0.00%Baa 0.00% 0.37% 1.05% 0.00% 0.00%Ba 1.23% 0.40% 0.81% 0.00% 1.07%B 1.86% 2.60% 2.50% 3.66% 2.59%Caa 5.88% 0.00% 20.00% 23.68% 21.88%Investment Grade 0.00% 0.14% 0.44% 0.00% 0.00%Speculative Grade 1.74% 1.39% 2.34% 2.56% 2.89%All Ratings 0.44% 0.46% 0.98% 0.77% 0.90%

4. See additional discussions in the CMBS section of Moody's Special Comment, "Structured Finance Rating Transitions: 1983-2005," February 2006.

Figure 17 – US CMBS Lifetime Impairment Rates by Original Rating on Securities Issued during 1999-2003Original Rating 1999 Vintage 2000 Vintage 2001 Vintage 2002 Vintage 2003 Vintage

Aaa 0.0% 0.0% 0.0% 0.0% 0.0%Aa 0.0% 0.0% 0.0% 0.0% 0.0%A 0.0% 2.4% 0.0% 0.0% 0.0%Baa 0.0% 3.7% 2.4% 0.0% 0.0%Ba 0.0% 3.1% 6.7% 2.7% 0.0%B 17.9% 25.0% 14.3% 3.3% 1.1%Caa 44.4% 33.3% 33.3% 0.0% 0.0%Investment Grade 0.0% 2.1% 1.1% 0.0% 0.0%Speculative Grade 12.0% 14.5% 10.5% 2.9% 0.5%All Ratings 3.4% 5.6% 3.6% 0.9% 0.1%

Note: Lifetime impairment rate is the total number of impaired securities to date as a share of all securities issued.

12 Moody’s Special Comment

US RMBS: IMPAIRMENT RATES ROSE IN THE SPECULATIVE-GRADE CATEGORYSimilar to the CMBS sector, the RMBS sector, which mainly includes transactions backed by prime and Alt-Aresidential mortgages, demonstrated superb credit performance in recent years. Nine securities were impaired for thefirst time in 2005, and two (backed by Quality Mortgage USA Inc. loans, which contributed to most of the RMBSimpairments in our data sample) were previously impaired, subsequently cured, and then became impaired again in2005, resulting in a total of 11 new impairments in this sector in 2005.

The nine newly impaired RMBS tranches involved just five transactions, of which four were backed by pools witha considerable proportion of Alt-A mortgage loans. All but one of these nine impaired tranches were downgraded tothe Ca or C category, either because they had already experienced significant principal losses, or were expected shortly.

By rating at the beginning of the year, the 2005 impairment rates remained at low levels in the investment-gradecategories. In the speculative-grade category, while the overall level was still low, the impairment rate did edge up to1.5% in 2005 from 0.6% in 2004 (Figure 19).

Across vintages, securities issued in 1999, 2000 and 2003 had perfect payment records with no impairments todate. The performance of the 2001 and 2002 vintages was largely similar (see Figure 20).

Figure 18 – US CMBS Marginal Impairment Rates by Years after Issuance, 1993-2005

Figure 19 – US RMBS One-Year Impairment Rates by Rating at the Beginning of the YearRating at the Beginning of the Year 2001 2002 2003 2004 2005

Aaa 0.00% 0.00% 0.00% 0.00% 0.00%Aa 0.00% 0.00% 0.00% 0.00% 0.00%A 0.00% 0.00% 0.21% 0.54% 0.00%Baa 0.31% 0.51% 0.40% 0.19% 0.40%Ba 1.27% 0.58% 0.87% 0.77% 1.19%B 3.33% 1.00% 0.00% 0.57% 1.46%Caa 16.67% 0.00% 20.00% 0.00% 28.57%Investment Grade 0.05% 0.09% 0.09% 0.11% 0.07%Speculative Grade 2.34% 0.68% 0.69% 0.64% 1.45%All Ratings 0.33% 0.15% 0.17% 0.17% 0.21%

0%

1%

2%

3%

4%

5%

6%

1 2 3 4 5 6 7

Years after Issuance

Spec. Grade

Invest. Grade

Moody’s Special Comment 13

Using all the data in the sample, Figure 21 reports a seasoning pattern of marginal impairment rates in the RMBSsector that is different from those in the HEL and CMBS sectors (Figures 15 and 18).

First, there was a clean hump in the marginal impairment rates of RMBS tranches. The impairment rates peakedin the fourth year for both investment-grade and speculative-grade securities, before declining precipitously in thefifth and sixth years after issuance.

Second, compared to the HEL and CMBS marginal impairment rates, the RMBS marginal impairment rates weremore front-loaded. The impairment rates jumped in the third year after issuance in the speculative-grade category, andthe fourth year after issuance in the investment-grade category. More importantly, the marginal impairment rates weresignificantly lower in the sixth and seventh years than those in the third and fourth years after issuance.

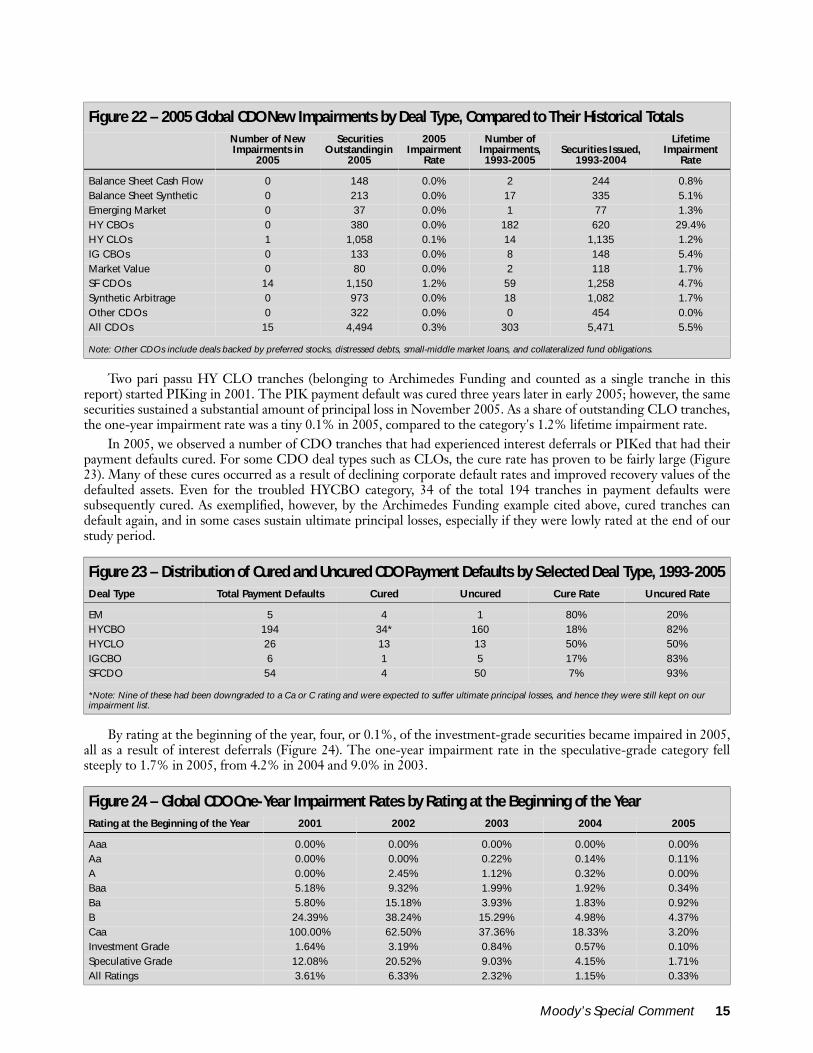

GLOBAL CDOs: IMPAIRMENT RATES PLUNGED ACROSS ALL CATEGORIES2005 was a banner year for global CDOs with just 15 newly impaired tranches, representing 0.3% of the total of 4,494tranches outstanding. In fact, the 0.3% one-year impairment rate was the lowest since 1998 in this sector.

All but one of these new impairments were CDO tranches backed mainly by other structured finance securities(SF CDOs) (see Figure 22). Tranches from balance-sheet CDOs, CBOs, synthetic arbitrage CDOs, and other types ofCDOs such as preferred-stock CDOs and market-value CDOs reported no new impairments. By comparison, thelifetime impairment rates were much higher with 29.4% among HY CBOs, and 4.7% among SF CDOs.

Figure 20 – US RMBS Lifetime Impairment Rates by Original Rating on Securities Issued during 1999-2003Original Rating 1999 Vintage 2000 Vintage 2001 Vintage 2002 Vintage 2003 Vintage

Aaa 0.0% 0.0% 0.0% 0.0% 0.0%Aa 0.0% 0.0% 0.0% 0.0% 0.0%A 0.0% 0.0% 0.0% 1.9% 0.0%Baa 0.0% 0.0% 1.8% 0.5% 0.0%Ba 0.0% 0.0% 4.7% 1.7% 0.0%B 0.0% 0.0% 3.2% 2.4% 0.0%Caa n/a n/a n/a n/a n/aInvestment Grade 0.0% 0.0% 0.3% 0.5% 0.0%Speculative Grade 0.0% 0.0% 4.1% 2.0% 0.0%All Ratings 0.0% 0.0% 0.7% 0.7% 0.0%

Note: Lifetime impairment rate is the total number of impaired securities to date as a share of all securities issued.

Figure 21 – US RMBS Marginal Impairment Rates by Years after Issuance, 1993-2005

0%

1%

2%

3%

4%

5%

1 2 3 4 5 6 7

Years after Issuance

Spec. Grade

Invest. Grade

14 Moody’s Special Comment

Two pari passu HY CLO tranches (belonging to Archimedes Funding and counted as a single tranche in thisreport) started PIKing in 2001. The PIK payment default was cured three years later in early 2005; however, the samesecurities sustained a substantial amount of principal loss in November 2005. As a share of outstanding CLO tranches,the one-year impairment rate was a tiny 0.1% in 2005, compared to the category's 1.2% lifetime impairment rate.

In 2005, we observed a number of CDO tranches that had experienced interest deferrals or PIKed that had theirpayment defaults cured. For some CDO deal types such as CLOs, the cure rate has proven to be fairly large (Figure23). Many of these cures occurred as a result of declining corporate default rates and improved recovery values of thedefaulted assets. Even for the troubled HYCBO category, 34 of the total 194 tranches in payment defaults weresubsequently cured. As exemplified, however, by the Archimedes Funding example cited above, cured tranches candefault again, and in some cases sustain ultimate principal losses, especially if they were lowly rated at the end of ourstudy period.

By rating at the beginning of the year, four, or 0.1%, of the investment-grade securities became impaired in 2005,all as a result of interest deferrals (Figure 24). The one-year impairment rate in the speculative-grade category fellsteeply to 1.7% in 2005, from 4.2% in 2004 and 9.0% in 2003.

Figure 22 – 2005 Global CDO New Impairments by Deal Type, Compared to Their Historical TotalsNumber of New Impairments in

2005

Securities Outstanding in

2005

2005 Impairment

Rate

Number of Impairments, 1993-2005

Securities Issued, 1993-2004

Lifetime Impairment

Rate

Balance Sheet Cash Flow 0 148 0.0% 2 244 0.8%Balance Sheet Synthetic 0 213 0.0% 17 335 5.1%Emerging Market 0 37 0.0% 1 77 1.3%HY CBOs 0 380 0.0% 182 620 29.4%HY CLOs 1 1,058 0.1% 14 1,135 1.2%IG CBOs 0 133 0.0% 8 148 5.4%Market Value 0 80 0.0% 2 118 1.7%SF CDOs 14 1,150 1.2% 59 1,258 4.7%Synthetic Arbitrage 0 973 0.0% 18 1,082 1.7%Other CDOs 0 322 0.0% 0 454 0.0%All CDOs 15 4,494 0.3% 303 5,471 5.5%

Note: Other CDOs include deals backed by preferred stocks, distressed debts, small-middle market loans, and collateralized fund obligations.

Figure 23 – Distribution of Cured and Uncured CDO Payment Defaults by Selected Deal Type, 1993-2005Deal Type Total Payment Defaults Cured Uncured Cure Rate Uncured Rate

EM 5 4 1 80% 20%HYCBO 194 34* 160 18% 82%HYCLO 26 13 13 50% 50%IGCBO 6 1 5 17% 83%SFCDO 54 4 50 7% 93%

*Note: Nine of these had been downgraded to a Ca or C rating and were expected to suffer ultimate principal losses, and hence they were still kept on our impairment list.

Figure 24 – Global CDO One-Year Impairment Rates by Rating at the Beginning of the YearRating at the Beginning of the Year 2001 2002 2003 2004 2005

Aaa 0.00% 0.00% 0.00% 0.00% 0.00%Aa 0.00% 0.00% 0.22% 0.14% 0.11%A 0.00% 2.45% 1.12% 0.32% 0.00%Baa 5.18% 9.32% 1.99% 1.92% 0.34%Ba 5.80% 15.18% 3.93% 1.83% 0.92%B 24.39% 38.24% 15.29% 4.98% 4.37%Caa 100.00% 62.50% 37.36% 18.33% 3.20%Investment Grade 1.64% 3.19% 0.84% 0.57% 0.10%Speculative Grade 12.08% 20.52% 9.03% 4.15% 1.71%All Ratings 3.61% 6.33% 2.32% 1.15% 0.33%

Moody’s Special Comment 15

CDO performance also improved steadily across vintages, as the lifetime impairment rates dropped from 20.6%within the 1999 vintage to 1.5% and 0% within the 2002 and 2003 vintages (see Figure 25). In addition, theseimprovements were evident across all rating categories.

Figure 26 describes the seasoning patterns of CDO marginal impairment rates. The marginal impairment ratesrose steadily in the first four years before they declined in the fifth year in both the speculative-grade and investment-grade categories. Similar to our findings in the ABS and HEL sectors, the marginal impairment rates in the fifth andsixth years after issuance were significantly above zero.

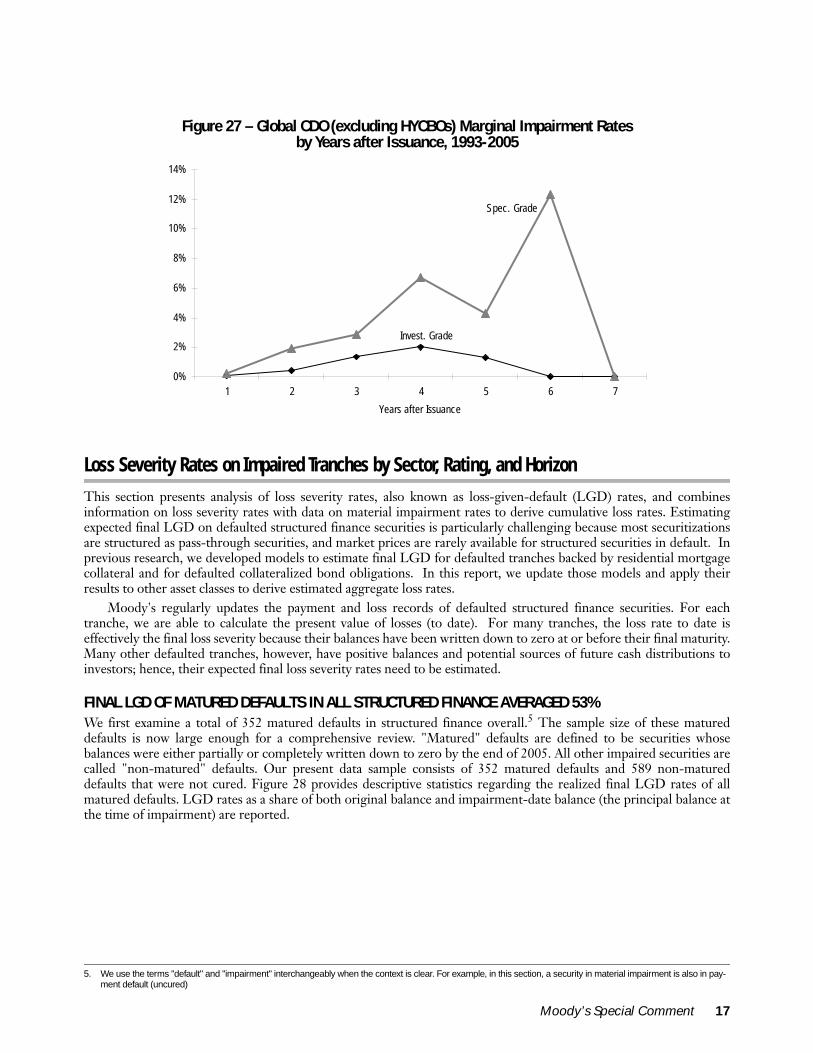

By comparison, the marginal impairment rates of CDOs excluding HYCBOs were much lower, and declined tozero in the sixth and seventh year for both the investment-grade and speculative-grade categories (see Figure 27).

Figure 25 – Global CDO Lifetime Impairment Rates by Original Rating on Securities Issued during 1999-2003Original Rating 1999 Vintage 2000 Vintage 2001 Vintage 2002 Vintage 2003 Vintage

Aaa 0.0% 0.0% 0.0% 0.0% 0.0%Aa 3.2% 2.4% 1.5% 0.0% 0.0%A 12.7% 10.2% 1.9% 1.0% 0.0%Baa 35.2% 20.6% 15.6% 3.2% 0.0%Ba 40.7% 29.1% 11.0% 6.6% 0.0%B 59.3% 22.2% 12.5% 0.0% 0.0%CaaInvestment Grade 13.9% 8.7% 5.1% 1.0% 0.0%Speculative Grade 46.5% 28.4% 11.1% 6.2% 0.0%All Ratings 20.6% 11.8% 6.0% 1.5% 0.0%

Note: Lifetime impairment rate is the total number of impaired securities to date as a share of all securities issued.

Figure 26 – Global CDO Marginal Impairment Rates by Years after Issuance, 1993-2005

0%

2%

4%

6%

8%

10%

12%

14%

16%

1 2 3 4 5 6 7

Years after Issuance

Spec. Grade

Invest. Grade

16 Moody’s Special Comment

Loss Severity Rates on Impaired Tranches by Sector, Rating, and Horizon

This section presents analysis of loss severity rates, also known as loss-given-default (LGD) rates, and combinesinformation on loss severity rates with data on material impairment rates to derive cumulative loss rates. Estimatingexpected final LGD on defaulted structured finance securities is particularly challenging because most securitizationsare structured as pass-through securities, and market prices are rarely available for structured securities in default. Inprevious research, we developed models to estimate final LGD for defaulted tranches backed by residential mortgagecollateral and for defaulted collateralized bond obligations. In this report, we update those models and apply theirresults to other asset classes to derive estimated aggregate loss rates.

Moody's regularly updates the payment and loss records of defaulted structured finance securities. For eachtranche, we are able to calculate the present value of losses (to date). For many tranches, the loss rate to date iseffectively the final loss severity because their balances have been written down to zero at or before their final maturity.Many other defaulted tranches, however, have positive balances and potential sources of future cash distributions toinvestors; hence, their expected final loss severity rates need to be estimated.

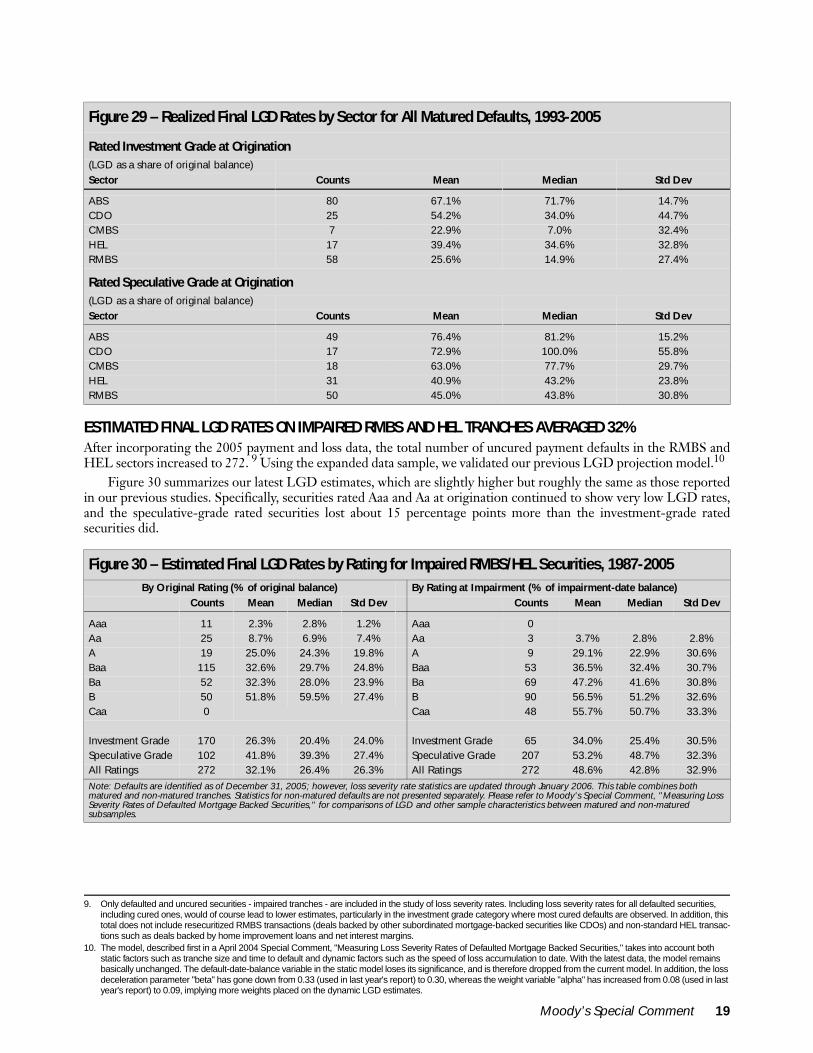

FINAL LGD OF MATURED DEFAULTS IN ALL STRUCTURED FINANCE AVERAGED 53%We first examine a total of 352 matured defaults in structured finance overall.5 The sample size of these matureddefaults is now large enough for a comprehensive review. "Matured" defaults are defined to be securities whosebalances were either partially or completely written down to zero by the end of 2005. All other impaired securities arecalled "non-matured" defaults. Our present data sample consists of 352 matured defaults and 589 non-matureddefaults that were not cured. Figure 28 provides descriptive statistics regarding the realized final LGD rates of allmatured defaults. LGD rates as a share of both original balance and impairment-date balance (the principal balance atthe time of impairment) are reported.

Figure 27 – Global CDO (excluding HYCBOs) Marginal Impairment Rates by Years after Issuance, 1993-2005

5. We use the terms "default" and "impairment" interchangeably when the context is clear. For example, in this section, a security in material impairment is also in pay-ment default (uncured)

0%

2%

4%

6%

8%

10%

12%

14%

1 2 3 4 5 6 7

Years after Issuance

Spec. Grade

Invest. Grade

Moody’s Special Comment 17

6

The descriptive statistics have at least three notable implications:First, impaired tranches that were rated higher experienced lower loss severity. In particular, those rated Aaa lost

only a tiny fraction (3%) of their original balance, while those rated Aa lost less than 30% of their original balance. 7The impaired tranches that were rated single-B and Caa at origination had much higher loss severity rates than werethose rated single-A, Baa and Ba.

Second, the distribution of LGD rates within certain rating categories was skewed. For example, the median LGDrates of Aa-rated securities were much lower than their means, suggesting that more than half of the impaired Aa-securities suffered LGD rates that were lower than their means. In addition, the medians were higher than the meansin the Baa, Ba and single-B categories, implying that in these categories there were more than half of the securitieswith LGD rates higher than their means.

Third, by rating at impairment, securities rated Aa suffered only minor losses, but those rated Baa or below lost asignificant amount with their medians at above 90% of their impairment-date balance.

In addition to the differentiation of LGD rates by rating, there were also large differences across sectors amongmatured defaults. Figure 29 summarizes the final LGD rates by sector and reveals three interesting findings.

First, for impaired tranches that were rated investment grade, the LGD rates were the lowest in the CMBS sectorand the highest in the ABS sector.8 The LGD rates of impaired RMBS and HEL tranches were generally betweenthose in the ABS and CMBS categories, and the average RMBS LGD rates were lower than the average HEL LGDrates. Additionally, CDO tranches that were impaired and carried an investment-grade rating at origination generallyexperienced LGD rates that were lower than those of ABS tranches but higher than those of RMBS and HELtranches.

Second, for impaired tranches that were rated speculative grade, the LGD rates were much lower in the RMBSand HEL sectors than in the ABS and CDO sectors. The LGD rates of speculative-grade securities in the CMBSsector were ranked in between those of RMBS/HEL and ABS/CDOs.

Third, the variation of final LGD rates within the investment-grade and speculative-grade categories differedacross sectors. The standard deviation of LGD rates was much larger in both rating grade categories in the CDOsector than in the ABS sector, whereas those in the CMBS, HEL, and RMBS sectors appeared to be similar.

Figure 28 – Realized Final LGD Rates by Rating for All Matured Defaults in the All Structured Finance Category, 1993-20056

By original rating (% of original balance) By rating at impairment (% of impairment-date balance)Rating at origination Counts Mean Median Std Dev

Rating at impairment Counts Mean Median Std Dev

Aaa 6 2.6% 2.9% 1.1% Aaa 0Aa 15 28.4% 15.0% 28.5% Aa 1 2.8% 2.8% n/aA 29 52.0% 69.2% 32.7% A 7 47.5% 22.9% 45.4%Baa 137 51.7% 58.8% 31.4% Baa 53 63.0% 94.6% 41.2%Ba 93 53.9% 60.7% 33.1% Ba 90 72.0% 93.9% 36.7%B 70 63.8% 73.1% 32.3% B 103 74.0% 94.0% 35.0%Caa 2 78.1% 78.1% 9.5% Caa 98 72.0% 83.7% 34.5%Investment Grade 187 48.3% 53.4% 32.5% Investment Grade 61 60.2% 93.7% 41.9%Speculative Grade 165 58.4% 67.9% 32.9% Speculative Grade 291 72.7% 92.9% 35.3%All Rating 352 53.0% 64.8% 33.0% All Rating 352 70.5% 92.9% 36.8%

6. In a Moody's Special Comment, "Measuring Loss Severity Rates of Defaulted Residential Mortgage-Backed Securities: A Methodology," we compared LGD rates of matured and non-matured tranches, and found that there was a survival bias in the sense that non-matured defaults were expected to sustain lower final LGD rates than were matured defaults.

7. Impaired health care receivable ABS tranches involving a number of NPF transactions were not included in this calculation.8. Most of the investment-grade impairments were Baa-rated. Therefore, the contrast of LGD rates across sectors reflects their differences at the Baa rating level as well.

18 Moody’s Special Comment

ESTIMATED FINAL LGD RATES ON IMPAIRED RMBS AND HEL TRANCHES AVERAGED 32%After incorporating the 2005 payment and loss data, the total number of uncured payment defaults in the RMBS andHEL sectors increased to 272. 9 Using the expanded data sample, we validated our previous LGD projection model.10

Figure 30 summarizes our latest LGD estimates, which are slightly higher but roughly the same as those reportedin our previous studies. Specifically, securities rated Aaa and Aa at origination continued to show very low LGD rates,and the speculative-grade rated securities lost about 15 percentage points more than the investment-grade ratedsecurities did.

Figure 29 – Realized Final LGD Rates by Sector for All Matured Defaults, 1993-2005

Rated Investment Grade at Origination(LGD as a share of original balance)Sector Counts Mean Median Std Dev

ABS 80 67.1% 71.7% 14.7%CDO 25 54.2% 34.0% 44.7%CMBS 7 22.9% 7.0% 32.4%HEL 17 39.4% 34.6% 32.8%RMBS 58 25.6% 14.9% 27.4%

Rated Speculative Grade at Origination(LGD as a share of original balance)Sector Counts Mean Median Std Dev

ABS 49 76.4% 81.2% 15.2%CDO 17 72.9% 100.0% 55.8%CMBS 18 63.0% 77.7% 29.7%HEL 31 40.9% 43.2% 23.8%RMBS 50 45.0% 43.8% 30.8%

9. Only defaulted and uncured securities - impaired tranches - are included in the study of loss severity rates. Including loss severity rates for all defaulted securities, including cured ones, would of course lead to lower estimates, particularly in the investment grade category where most cured defaults are observed. In addition, this total does not include resecuritized RMBS transactions (deals backed by other subordinated mortgage-backed securities like CDOs) and non-standard HEL transac-tions such as deals backed by home improvement loans and net interest margins.

10. The model, described first in a April 2004 Special Comment, "Measuring Loss Severity Rates of Defaulted Mortgage Backed Securities," takes into account both static factors such as tranche size and time to default and dynamic factors such as the speed of loss accumulation to date. With the latest data, the model remains basically unchanged. The default-date-balance variable in the static model loses its significance, and is therefore dropped from the current model. In addition, the loss deceleration parameter "beta" has gone down from 0.33 (used in last year's report) to 0.30, whereas the weight variable "alpha" has increased from 0.08 (used in last year's report) to 0.09, implying more weights placed on the dynamic LGD estimates.

Figure 30 – Estimated Final LGD Rates by Rating for Impaired RMBS/HEL Securities, 1987-2005By Original Rating (% of original balance) By Rating at Impairment (% of impairment-date balance)

Counts Mean Median Std Dev Counts Mean Median Std Dev

Aaa 11 2.3% 2.8% 1.2% Aaa 0Aa 25 8.7% 6.9% 7.4% Aa 3 3.7% 2.8% 2.8%A 19 25.0% 24.3% 19.8% A 9 29.1% 22.9% 30.6%Baa 115 32.6% 29.7% 24.8% Baa 53 36.5% 32.4% 30.7%Ba 52 32.3% 28.0% 23.9% Ba 69 47.2% 41.6% 30.8%B 50 51.8% 59.5% 27.4% B 90 56.5% 51.2% 32.6%Caa 0 Caa 48 55.7% 50.7% 33.3%

Investment Grade 170 26.3% 20.4% 24.0% Investment Grade 65 34.0% 25.4% 30.5%Speculative Grade 102 41.8% 39.3% 27.4% Speculative Grade 207 53.2% 48.7% 32.3%All Ratings 272 32.1% 26.4% 26.3% All Ratings 272 48.6% 42.8% 32.9%Note: Defaults are identified as of December 31, 2005; however, loss severity rate statistics are updated through January 2006. This table combines both matured and non-matured tranches. Statistics for non-matured defaults are not presented separately. Please refer to Moody's Special Comment, "Measuring Loss Severity Rates of Defaulted Mortgage Backed Securities," for comparisons of LGD and other sample characteristics between matured and non-matured subsamples.

Moody’s Special Comment 19

ESTIMATED FINAL LGD RATES ON IMPAIRED CDO TRANCHES AVERAGED 72%In our first study of CDO defaults and losses, we derived a simple model to project final LGD rates for defaulted high-yield CBO tranches, which have historically experienced the greatest number of defaults within the broader CDOsector. At present, we continue to use the same model we derived for CBOs and apply it to all impaired cash SF CDOsand CLOs.11 Figure 31 summarizes the estimated final LGD rates of all impaired CDOs including both matured andnon-matured, cash and synthetic securities, some of which were from European transactions.

Figure 31 reveals several interesting findings about LGDs of impaired CDO tranches:• LGD rates have varied systematically with original rating levels – single-B and Ba rated securities have

experienced higher LGDs than securities rated Baa and single-A, which in turn have higher LGDs than Aa-rated securities.

• In contrast, LGD rates by impairment date balance were generally at similarly high levels across the variousrating categories at the time of impairment.

• The median LGD rates were higher than the mean LGD rates for almost all rating categories except Aa,implying that there were more than half of the securities with LGD rates higher than the means.

• While the average LGD rates in the speculative-grade category were similar both as a share of originalbalance and as a share of impairment-date balance, in the investment-grade category, the LGD rates as ashare of impairment-date balance averaged much higher than those as a share of original balance. This islargely the result of amortization (occurring first to more senior tranches) that made principal balancessmaller than the balance at origination by the time the securities experienced impairments.

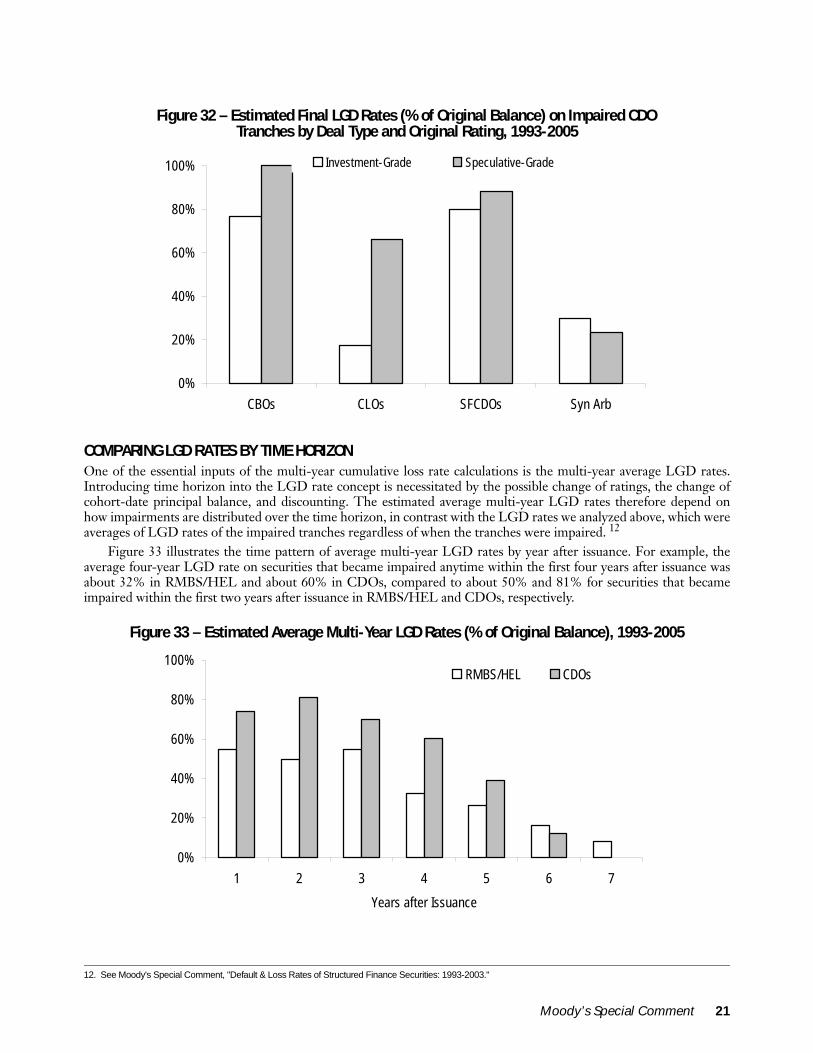

The LGD rates on impaired CDO tranches also varied by deal type. Figure 32 highlights the similarities anddifferences in the estimated final LGD rates across four CDO deal types. In particular, the LGD rates were similarbetween CBOs (including both HY CBOs and Investment-Grade CBOs) and SF CDOs in the investment-gradecategory. In this same category, the LGD rates of impaired CLO and synthetic arbitrage tranches were much lowerthan those of CBOs and SFCDOs. In the speculative-grade category, however, the LGD rates of CBOs and SF CDOswere similar, and higher than those of CLOs and synthetic arbitrage CDOs.

11. See "Default & Loss Rates of U.S. CDOs: 1993-2003," Moody's Special Comment, March 2005. The model uses the weighted average rating factor (WARF) and the weighted average maturity (WAM), as reported by Moody's deal performance reports, to find the weighted average loss rates expected in the pool. These expected pool loss rates are used to adjust the 2005 year-end OC ratios, after taking into account the potential excess interests that would become available in the deal, if any excess exists. The adjusted OC ratios are then used to derive future payments available to the impaired tranches and compute the tranches' projected loss rates.

Figure 31 – Estimated Final LGD Rates by Rating for Impaired CDO Securities, 1993-2005By original rating (% of original balance) By rating at impairment (% of impairment-date balance)

Counts Mean median Std Dev Counts Mean median Std Dev

Aaa 0 Aaa 0Aa 8 38.8% 33.8% 30.8% Aa 0A 18 64.3% 82.6% 38.0% A 12 79.8% 100.0% 38.8%Baa 132 66.8% 79.0% 33.3% Baa 56 88.2% 100.0% 29.1%Ba 56 81.0% 100.0% 31.0% Ba 56 88.8% 100.0% 29.1%B 36 89.2% 100.0% 23.8% B 70 81.5% 100.0% 34.3%Caa 0 Caa 56 80.6% 100.0% 33.3%

Investment Grade 158 65.1% 78.6% 34.1% Investment Grade 68 86.7% 100.0% 30.9%Speculative Grade 92 84.2% 100.0% 28.5% Speculative Grade 182 83.5% 100.0% 32.5%All Ratings 250 72.1% 84.3% 33.4% All Ratings 250 84.4% 100.0% 32.0%Note: Defaults are identified as of December 31, 2005; however, loss severity rate statistics are updated through January 2006. This table combines both matured and non-matured tranches. The sample size is smaller than the total number of impaired tranches in this sector because some impaired tranches lack complete information for predicting final LGD rates. Statistics for non-matured defaults are not presented separately. Please refer to Moody's Special Comment, "Measuring Loss Severity Rates of Defaulted Mortgage Backed Securities," for comparisons of LGD and other sample characteristics between matured and non-matured subsamples.

20 Moody’s Special Comment

COMPARING LGD RATES BY TIME HORIZONOne of the essential inputs of the multi-year cumulative loss rate calculations is the multi-year average LGD rates.Introducing time horizon into the LGD rate concept is necessitated by the possible change of ratings, the change ofcohort-date principal balance, and discounting. The estimated average multi-year LGD rates therefore depend onhow impairments are distributed over the time horizon, in contrast with the LGD rates we analyzed above, which wereaverages of LGD rates of the impaired tranches regardless of when the tranches were impaired. 12

Figure 33 illustrates the time pattern of average multi-year LGD rates by year after issuance. For example, theaverage four-year LGD rate on securities that became impaired anytime within the first four years after issuance wasabout 32% in RMBS/HEL and about 60% in CDOs, compared to about 50% and 81% for securities that becameimpaired within the first two years after issuance in RMBS/HEL and CDOs, respectively.

Figure 32 – Estimated Final LGD Rates (% of Original Balance) on Impaired CDO Tranches by Deal Type and Original Rating, 1993-2005

12. See Moody's Special Comment, "Default & Loss Rates of Structured Finance Securities: 1993-2003."

Figure 33 – Estimated Average Multi-Year LGD Rates (% of Original Balance), 1993-2005

0%

20%

40%

60%

80%

100%

CBOs CLOs SFCDOs Syn Arb

Investment-Grade Speculative-Grade

0%

20%

40%

60%

80%

100%

1 2 3 4 5 6 7

Years after Issuance

RMBS/HEL CDOs

Moody’s Special Comment 21

In addition to the original-rating-based impairment rate and LGD rates, Moody's also provides cohort-ratingbased impairment rate and LGD rates. Figure 34 compares the four-year LGD rates as a share of cohort-datebalances, i.e. the principal balances at the beginning of the impairment year and of each of the years prior to theobserved impairments. Figure 34 reveals that the cohort ratings, i.e. ratings at the beginning of a year, ranked-orderLGD rates better in the RMBS/HEL sector than in the CDO sector.

Multi-Year Cumulative Loss Rates by Rating and Sector

Multi-year cumulative loss rates are the product of multi-year cumulative impairment rates and multi-year cumulativeLGD rates. To derive these multi-year loss rates, we continue to use the approach we employed in our previous report;namely, we combine the estimated LGD rates of non-matured impairments and the realized final LGD rates ofmatured impairments to derive the average LGD rates in the RMBS/HEL and CDO sectors. Further, we apply:• the estimated LGD rates based on impaired RMBS and HEL tranches to the calculation of loss rates in the

RMBS, HEL, RMBS/HEL sectors combined, and the CMBS sector;• the estimated LGD rates based on impaired CDO tranches to the calculation of loss rates in the CDO sector; • the equally-weighted averages of LGD rates in RMBS/HEL and CDOs to the calculation of loss rates in the ABS

sector as well as in the all structured finance category. Figure 35 provides the resulting estimated five-year cumulative loss rates by rating, with comparisons between

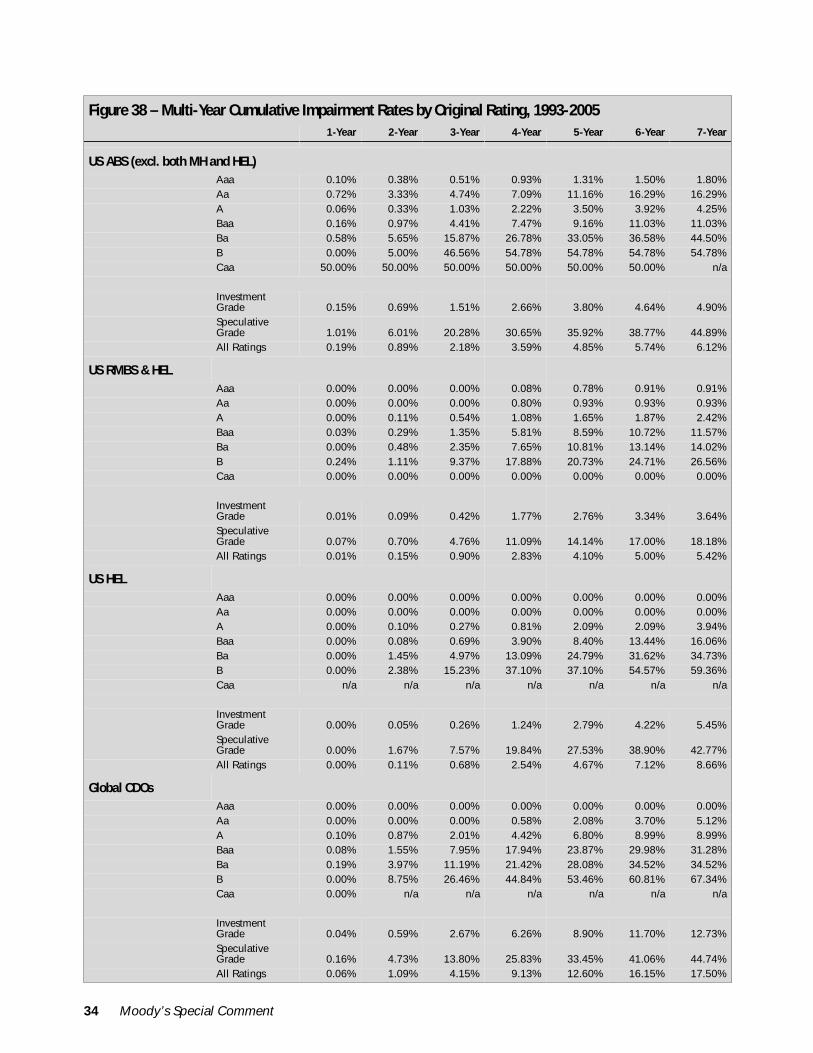

original-rating and cohort-rating-based loss rates in structured finance and those in the corporate sector. Detailedmulti-year cumulative loss rates by rating, horizon, and sector appear in Appendix 3.

Figure 34 – Estimated Average Four-Year LGD Rates (% of Cohort-Date Balance) by Cohort Rating, 1993-2005

Note: Cohort ratings are ratings on securities outstanding at the beginning of a cohort horizon (four-year horizon in this Figure), regardless of when they were issued. The four-year LGD rates are the averages of realized LGD rates on tranches impaired in each of the four years, weighted by the incremental impairment rates of each year.

0%

20%

40%

60%

80%

100%

Aaa Aa A Baa Ba B

Cohort Rating

RMBS/HEL CDOs

22 Moody’s Special Comment

Moody’s Special Comment 23

These newly estimated loss rates by rating are largely similar to what we provided in previous reports. Inparticular:

• The estimated five-year loss rates continued to be increasing as ratings decrease, and the relationshipbetween loss rates and ratings was similar between those measured by cohort rating and those measured byoriginal rating.

• Moody's continues to observe generally higher loss rates when measured by cohort rating than by originalrating in the all structured finance category. It is important to note that this ordering of loss rates betweencohort rating and original rating does not hold for all asset classes and all time horizons.

• Estimated loss rates by original rating are slightly higher, relative to those in last year's report, mostly due tothe increases in the estimated LGD rates at the fourth and fifth year horizons. By contrast, the estimatedloss rates by cohort rating declined a bit, relative to our previously reported numbers.

• Estimated loss rates remain higher in structured finance as a whole than in the corporate sector. Variationscontinued to persist across different structured finance sectors, with the CMBS and RMBS sectorsdemonstrating the lowest loss rates by rating (Figure 36).

Finally, it is important to note that all statistics presented in this report so far are not weighted by dollar volume,and we generally do not provide volume-based impairment and loss rates. Using the same data underlying Figure 35(details appear in Appendix 3) and weighting them by the total original balances in each rating category, we find thatoverall five-year loss rates as a share of original balance averaged about 49 basis points for all securities combined – 1.7basis points in the Aaa category, 2.3% for non-Aaa investment-grade securities, and 10.6% for speculative-gradesecurities. 13

Figure 35 – Estimated Five-Year Cumulative Loss Rates by Rating for All Structured Finance, 1993-2005Global Structured Finance, Global Structured Finance, Global Corporate,

By Original Rating By Cohort Rating by Cohort Rating

Aaa 0.017% 0.019% 0.004%Aa 0.74% 0.85% 0.08%A 1.78% 1.40% 0.23%Baa 5.81% 6.92% 1.24%Ba 8.65% 11.97% 7.04%B 16.22% 17.95% 18.61%Caa n/a 22.33% 37.70%

Investment Grade 2.04% 2.17% 0.77%Speculative Grade 11.65% 15.06% 26.97%All Ratings 3.16% 3.71% 6.97%Note: All structured finance securities are included. We assume that the LGD rates of all structured finance securities are the equally-weighted averages of the estimated LGD rates in RMBS and HEL and the estimated LGD rates in CDOs. Loss rates by cohort rating in the corporate sector are reproduced from Moody's 2005 corporate bond default study, "Default and Recovery Rates of Corporate Bond Issuers, 1920-2005," Moody's Special Comment, March 2005.

Figure 36 – Estimated Five-Year Cumulative Loss rates by Sector and Cohort Rating, 1993-2005

US CMBS US RMBS US HELGlobal CDOs excl. HYCBOs

ABS excl. MH HEL Global Corporate

Aaa 0.000% 0.028% 0.000% 0.000% 0.027% 0.004%Aa 0.00% 0.06% 0.00% 0.92% 2.69% 0.08%A 0.09% 0.34% 0.47% 2.47% 1.31% 0.23%Baa 0.36% 2.17% 3.42% 10.28% 6.31% 1.24%Ba 1.40% 3.26% 10.25% 12.60% 21.46% 7.04%B 9.06% 5.82% 22.44% 27.63% 28.04% 18.61%Caa 14.88% 19.77% n/a n/a n/a 37.70%

Investment Grade 0.14% 0.51% 0.95% 3.73% 1.67% 0.77%Speculative Grade 5.70% 4.42% 14.19% 17.07% 25.71% 26.97%All Ratings 1.46% 1.00% 2.03% 5.67% 2.69% 6.97%

13. Moody's generally focuses on issue-weighted statistics, not volume-weighted statistics, because issue-weighted statistics are likely to be more useful in predicting future performance level of a wide variety of portfolios. The volume-weighted statistics are more representative of the average historical experience of individual inves-tors.

Appendix 1: Descriptions of Data Sample and Glossary

DESCRIPTION OF DATA SAMPLEThe data sample for the study covers all structured finance rating observations globally between 1993 and 2005 anduses the following set of criteria:

• Only securities carrying long-term bond ratings are included, whereas short-term ratings, foreign nationalratings, provisional ratings, and rating estimates are excluded.

• Tranches wrapped by financial guarantors, government agencies, or government sponsored enterprises(GSEs) are excluded.

• Interest-only (IO) tranches and residual tranches are excluded.• Deals whose credit quality are entirely dependent on a single corporate rating, such as single borrower

credit tenant lease (CTL) deals in CMBS, are excluded. Derivative ratings, which are generally linked tothe credit rating of a single entity, are also excluded.

• Tranches carrying the same rating from the same deal are collapsed into a single rating observation, withthe following exception: if two or more tranches share the same rating in the same deal, but arecollateralized by distinct groups of loan pools, then the tranches are not collapsed.

During each year's update, Moody's not only adds new rating and default/loss data to the data sample, but alsoupdates past data observations using the latest information from servicers and trustees, who periodically produces newreports as well as updates on their past reports. The number of outstanding securities, impairments, and the amount oflosses may change depending on the securities' latest payment reports. In addition, small data errors may also havebeen discovered and corrected. As a result, past impairment and loss rates are subject to minor revisions. This reporthas incorporated all these necessary changes. Finally, the structured finance data set used in this study is availablethrough Moody's Structured Finance Default Risk Service (DRS) database.

GLOSSARY

Payment DefaultStructured finance securities are defined as being in payment default if they have suffered:• an interest shortfall, or• a principal write-down.

Moody's identifies structured finance securities' interest shortfalls and principal write-downs by reviewing all ofMoody's performance data reports, both in electronic and physical form. Prepayment-related interest shortfalls arenot considered to be payment defaults, but PIKing tranches are. Only explicit principal write-downs are included aspayment defaults as reported by servicers or trustees. Implicit principal losses or undercollateralizations are notincluded.

Material ImpairmentStructured finance securities are defined as being in material impairment if they have:• sustained a payment default that remained uncured, or• been downgraded to Ca or C.

The impairment status of a security may change as it goes from cured (i.e. all outstanding shortfalls and losseswere repaid in full) to uncured (i.e. positive interest shortfalls or principal losses outstanding), or vice versa. If anysecurities rated Ca or C but not in payment default are upgraded, they are considered to be no longer in materialimpairment. Securities rated Ca or C that were not upgraded are in material impairment even if their payment defaultshave been cured. Finally, securities with very minor shortfalls or losses are excluded.

One-Year Impairment RateThis is the number of securities that became newly impaired in a given year divided by the number of securitiesoutstanding at the beginning of a year.

24 Moody’s Special Comment

Lifetime Impairment RateThis is the total number of impaired securities divided by the total number of securities issued over a particular timeperiod without regard to the time horizon of impairments.

Marginal Impairment RateFor a cohort of securities outstanding (or issued if by original rating) at the beginning of year t, the N-th year marginalimpairment rate is the number of securities newly impaired in year (t+N) divided by the total number of securities thatsurvived to that year. Securities that are impaired or withdrawn before the year have not survived, and therefore do notappear in the denominator of this rate.

Marginal Cure RateFor a cohort of securities that experienced payment defaults in year t, the N-th year marginal cure rate measures thenumber of payment defaults cured in year (t+N) (measured in calendar years, not in actual number of months), as ashare of all payment defaults occurred in year t.

Loss Severity or LGDThe LGD rate of an impaired structured finance security is measured by the sum of the present values of net losses,including both interest shortfalls and principal losses, discounted by the security's coupon rate and expressed as apercentage of a given principal balance such as the principal balance at origination, at impairment date, or any givencohort date.

Matured and Non-Matured DefaultsSecurities that have sustained payment defaults are called "matured defaults" if their principal balance has beenreduced to zero. They are called "non-matured defaults" if they have positive principal balance outstanding as of theend of the study period.

Multi-Year Cumulative Loss RateThis is the product of the multi-year cumulative impairment rate and multi-year average LGD rate. The multi-yearaverage LGD rate is estimated using the realized and estimated final LGD rates of impaired securities that have knownloss rates, after taking into account the uncertainty of impairment timing.

ABSABS stand for asset-backed securities. This structured finance sector includes securities backed by home equity loans(HEL) and both traditional asset types such as auto loans, credit card receivables, student loans, and manufacturedhousing loans, and non-traditional asset types such as mutual fund fees, tax liens, tobacco settlement payments, andintellectual property.

HELThe home equity loan or HEL sector includes securities backed by subprime (B&C) mortgage loans, homeimprovement loans, high loan-to-value (high LTV) loans, home equity lines of credit (HELOCs), and closed-endsecond-lien loans, as well as net interest margin (NIM) securitizations. It does not include securities backed by Alt-Amortgages, which are included in the RMBS sector. HEL is part of the ABS sector.

CDOsCDOs stand for collateralized debt obligations. Derivative securities such as structured notes, repackaged securities,and credit derivatives are not considered to be part of this sector.

CMBSCMBS stand for commercial mortgage-backed securities.

RMBSRMBS stand for residential mortgage-backed securities. The large majority of these securities are backed by first-lienprime mortgages, but some are backed by Alt-A mortgages. HEL is not considered to be part of this sector.

Moody’s Special Comment 25

All Structured FinanceAll structured finance captures global structured securities in four major sectors: ABS, CDO, CMBS, and RMBS.

U.S. Structured FinanceU.S. structured finance securities are denominated in U.S. dollars and issued in the U.S. market.

European Structured FinanceEuropean structured finance securities are denominated in a European currency or issued in a European country.

Structured Finance in Other RegionsStructured finance securities in other regions are non-U.S. and non-European securities.

26 Moody’s Special Comment

Appendix 2: How to Calculate Multi-Year Material Impairment Rate and LGD Rate

CUMULATIVE IMPAIRMENT RATE BY COHORT RATINGMoody's uses the same method to calculate multi-year cumulative impairment rates as that used in Moody's corporateissuer default studies. In particular, we make an adjustment to the denominator of a marginal impairment rate in agiven period (such as a year) to reflect tranches whose ratings were withdrawn or impaired prior to that period. Suchadjustment ensures future impairments can only occur to survived tranches, i.e. withdrawn tranches or impairedtranches are not eligible for impairments in the subsequent periods.

The cumulative impairment rate for a time horizon T is therefore calculated as:

Where dt is the marginal impairment rate:

Where xt is the number of impairments in year t, wt is the number of rating withdrawals in year t, and

which is the number of tranches that survived into the cohort at time t. When the time horizon T is equal to 1, thecumulative impairment rate and the marginal impairment rate are equal. Note that in addition to removing the prior-year withdrawals from the denominator, half of the withdrawals in time t are also removed. This is because we usediscrete data to estimate marginal impairment rate and the timing of withdrawals within a given period is assumed tobe uniformly distributed.

Let us now look at an example, assuming all securities are carrying the same rating in both 2004 and 2005.

In the example, the average first-year marginal impairment rate is (10+5)/(200+95-95/2-90/2), or 7.41%. Thesecond-year marginal impairment rate is 5/(95-90/2)=10%.14 The average marginal survival rates are 92.6% and90.0% in the first and second year, respectively. The average two-year cumulative survival rate is92.6%*90.0%=83.3%. Therefore, the average two-year cumulative impairment rate is 16.7%.