dedicated to being world class -...

35

BMO Nesbitt Burns Conference March 3, 2005 Saddlebrook Resort, Florida dedicated to being world class Kinross Gold Corporation Corporate Presentation

Transcript of dedicated to being world class -...

BMO Nesbitt Burns ConferenceMarch 3, 2005

Saddlebrook Resort, Florida

dedicated to beingworld class

Kinross Gold CorporationCorporate Presentation

Certain statements set forth in this presentation constitute"forward looking statements" within the meaning of the

United States Private Securities Litigation Reform Act of 1995. Such statements involve risks, uncertainties and

other factors that may cause the actual results, performance or achievements to differ from those expressed or implied by such forward looking statements. Such risks and uncertainties are

described in periodic filings made by Kinross Gold Corporation with the U.S. Securities and Exchange Commission and Canadian provincial

securities regulatory authorities.

All dollar amounts used throughout this presentation are expressed in US dollars, unless otherwise noted.

Forward Looking StatementForward Looking Statement

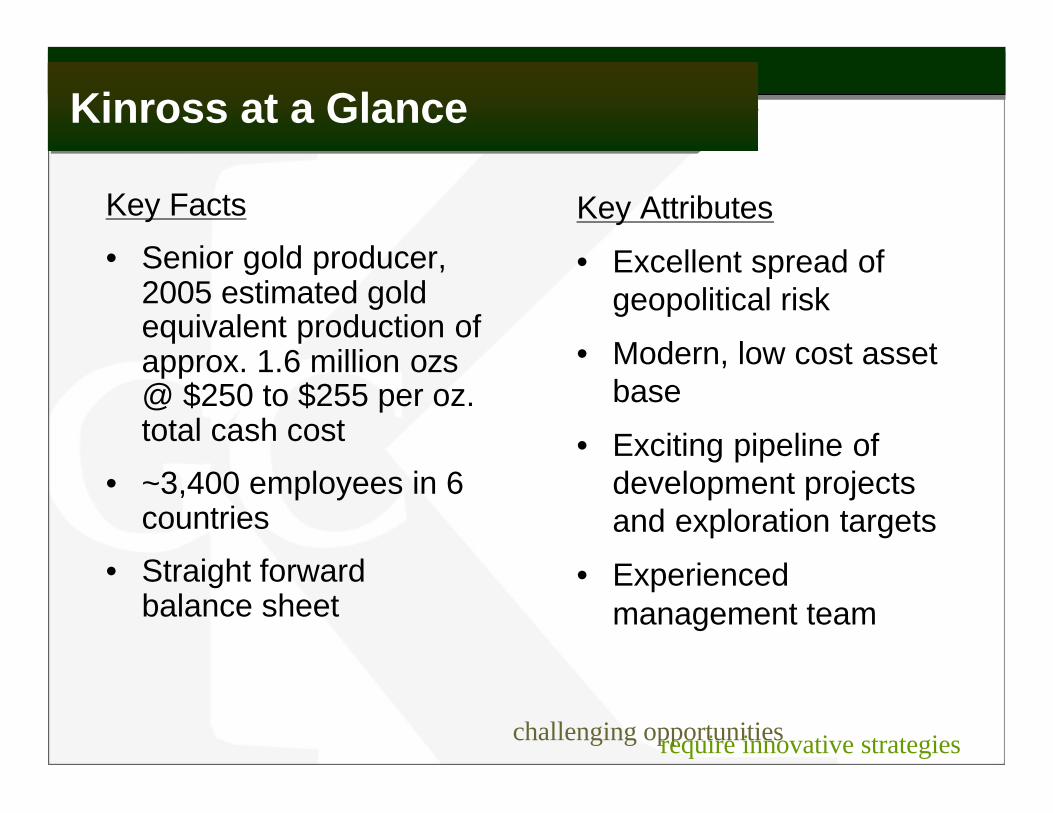

Key Facts

• Senior gold producer, 2005 estimated gold equivalent production of approx. 1.6 million ozs@ $250 to $255 per oz. total cash cost

• ~3,400 employees in 6 countries

• Straight forward balance sheet

Key Attributes

• Excellent spread of geopolitical risk

• Modern, low cost asset base

• Exciting pipeline of development projects and exploration targets

• Experienced management team

Kinross at a GlanceKinross at a Glance

challenging opportunities require innovative strategies

our global producing assetsKinross Gold CorporationKinross Gold Corporation

challenging opportunities require innovative strategies

Fort Knox (100%)Alaska, USA (Open Pit)

Musselwhite (32%)Ontario, Canada (U/G)

Porcupine (49%)Ontario, Canada (Open Pit, U/G)Kettle River (100%)

Washington, USA (U/G)

Round Mountain (50%)Nevada, USA (Open Pit)

La Coipa (50%)Chile (Open Pit)

Refugio (50%)Chile (Open Pit)

Paracatu (100%)Brazil (Open Pit)

Crixas (50%)Brazil (U/G)

Blanket (100%)Zimbabwe (U/G)

Kubaka (98.1%)Magadan, Russia (Open Pit, U/G)

Ø Be a Good Operator

Ø Sustainable Growth and Development

Ø Simplify the Company

Kinross GoalsKinross Goals

Ø Extend Mine Life

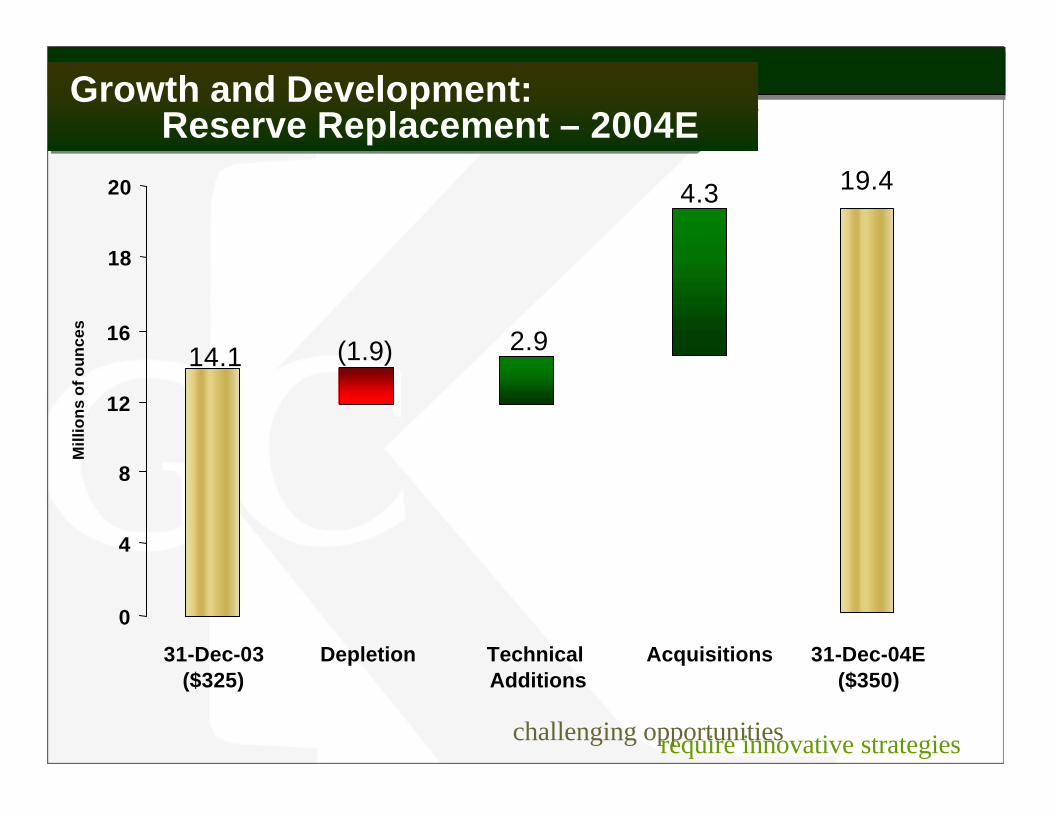

0

4

8

12

16

31-Dec-03($325)

Depletion Technical Additions

Acquisitions 31-Dec-04E($350)

Growth and Development:Reserve Replacement – 2004E

Growth and Development:Reserve Replacement – 2004E

challenging opportunities require innovative strategies

14.1

19.4

(1.9) 2.9

4.3

Mill

ion

s o

f ou

nce

s

18

20

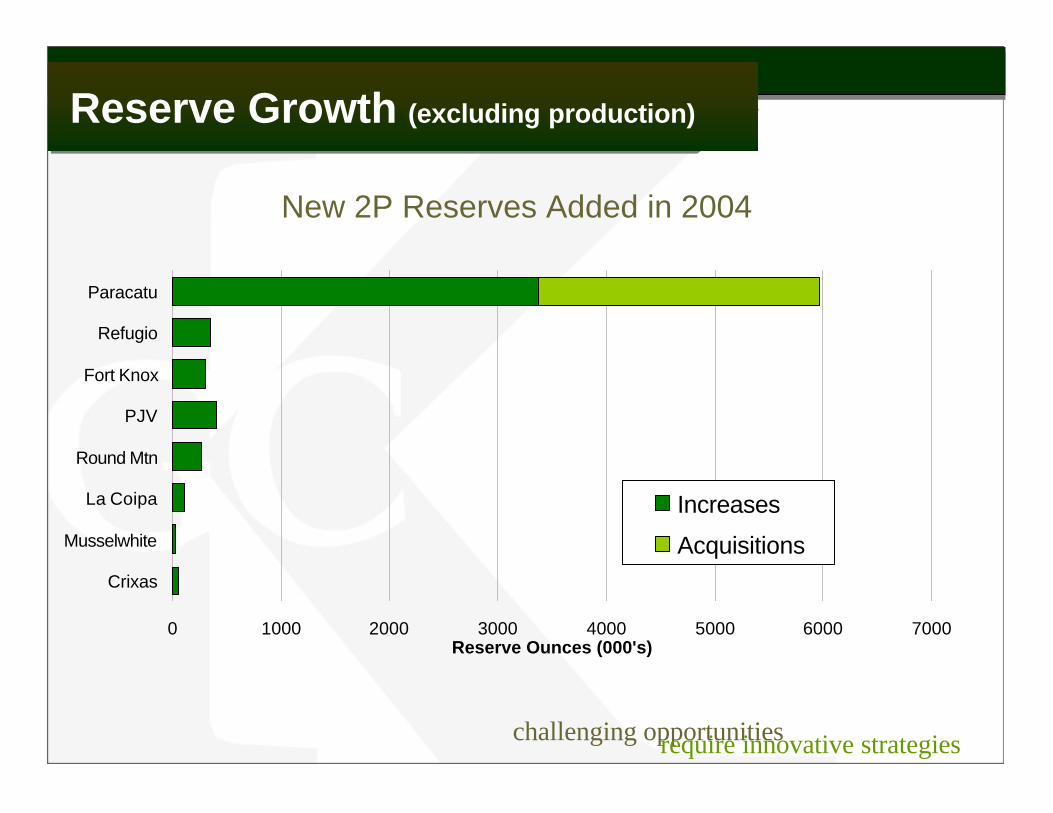

0 1000 2000 3000 4000 5000 6000 7000

Crixas

Musselwhite

La Coipa

Round Mtn

PJV

Fort Knox

Refugio

Paracatu

Reserve Ounces (000's)

Increases

Acquisitions

New 2P Reserves Added in 2004

Reserve Growth (excluding production)Reserve Growth (excluding production)

challenging opportunities require innovative strategies

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005e

Ou

nce

s (m

illio

ns)

Proven and Probable Measured and Indicated

Reserve and Resource HistoryReserve and Resource History

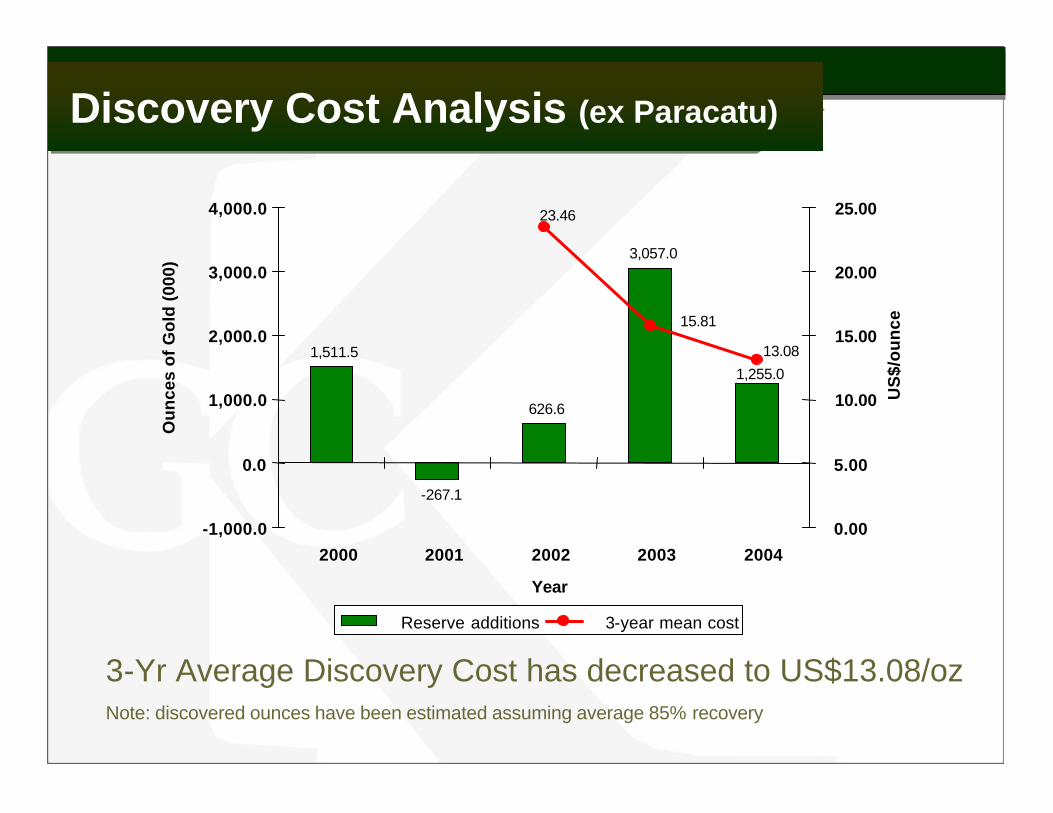

Discovery Cost Analysis (ex Paracatu)Discovery Cost Analysis (ex Paracatu)

3-Yr Average Discovery Cost has decreased to US$13.08/ozNote: discovered ounces have been estimated assuming average 85% recovery

1,511.5

-267.1

626.6

3,057.0

1,255.0

23.46

15.81

13.08

-1,000.0

0.0

1,000.0

2,000.0

3,000.0

4,000.0

2000 2001 2002 2003 2004

Year

Ou

nce

s o

f G

old

(00

0)

0.00

5.00

10.00

15.00

20.00

25.00

US

$/o

un

ce

Reserve additions 3-year mean cost

0

100

200

300

400

500

600

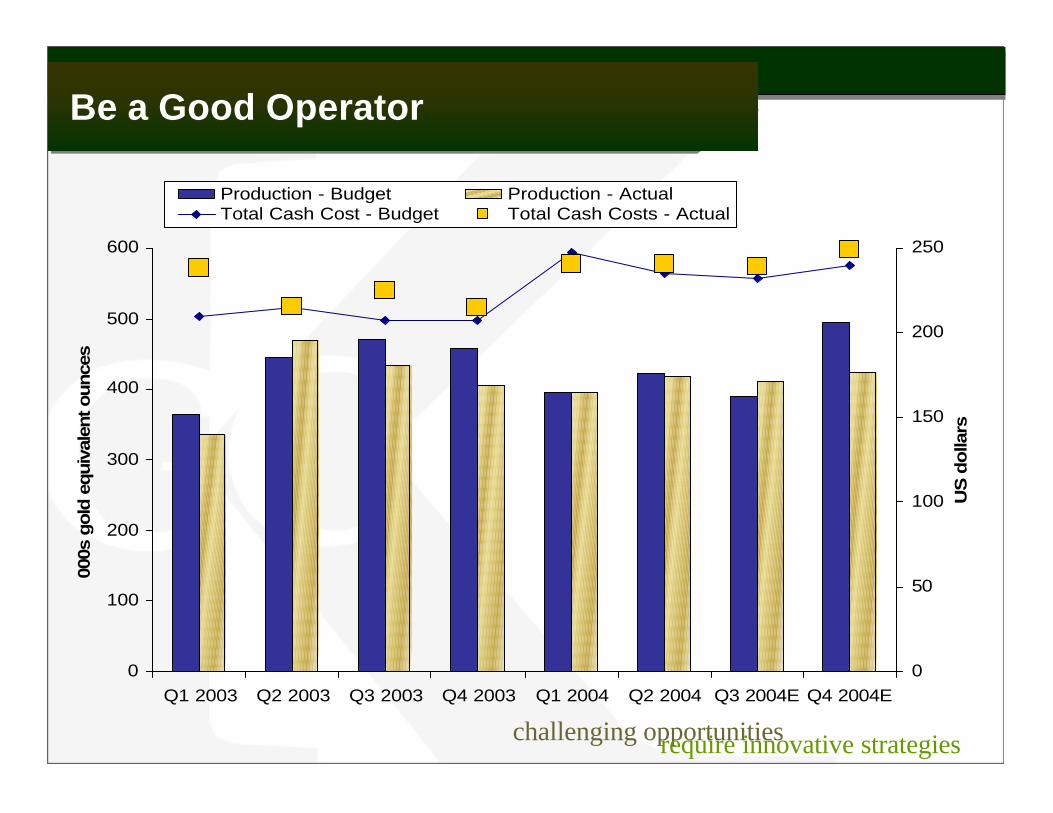

Q1 2003 Q2 2003 Q3 2003 Q4 2003 Q1 2004 Q2 2004 Q3 2004E Q4 2004E

000s

gold

equiv

alen

t ounce

s

0

50

100

150

200

250

US

do

llars

Production - Budget Production - ActualTotal Cash Cost - Budget Total Cash Costs - Actual

Be a Good OperatorBe a Good Operator

challenging opportunities require innovative strategies

2004 Budget2004 Actual2005 Estimate

2004 – 2005 Production2004 – 2005 Production

0

100

200

300

400

Fo

rt K

no

x

Ro

un

dM

ou

nta

in

Po

rcu

pin

e

Ku

bak

a

Par

acat

u

La

Co

ipa

Cri

xas

Mu

ssel

wh

ite

New

Bri

tan

nia

Ket

tle

Riv

er

Lupi

n

Ref

ugio

000s

oun

ces

Paracatu Expansion (100%)Paracatu Expansion (100%)

Optimizing…

Ø Purchased 51% of Paracatu from Rio Tinto for $260 million, transaction closed December 31, 2004

Ø Kinross is 100% owner and operator

Ø Paracatu mine life greater than 20 years

Ø Increases Kinross’ proven and probable gold reserves by 4.2 million oz.

Ø Eliminates one joint venture relationship

Ø Potential synergies with Gurupi in Northern Brazil (currently in feasibility)

Paracatu AcquisitionParacatu Acquisition

Paracatu Expansion (100%)Paracatu Expansion (100%)

Ø Increase milling capacity and improve efficiency resulting in:

• Increased gold recoveries

• Lower costs

• Increased resources due to lower cutoff grade

Ø Increase production to 250,000 oz/yr (100%) thru 2025

• Average yearly production in first 5 years of +300,000 ozs (100%)

Ø Reviewing feasibility

• Construction 2005/06; and production early 2007

• Current cost estimated $111M (100%)

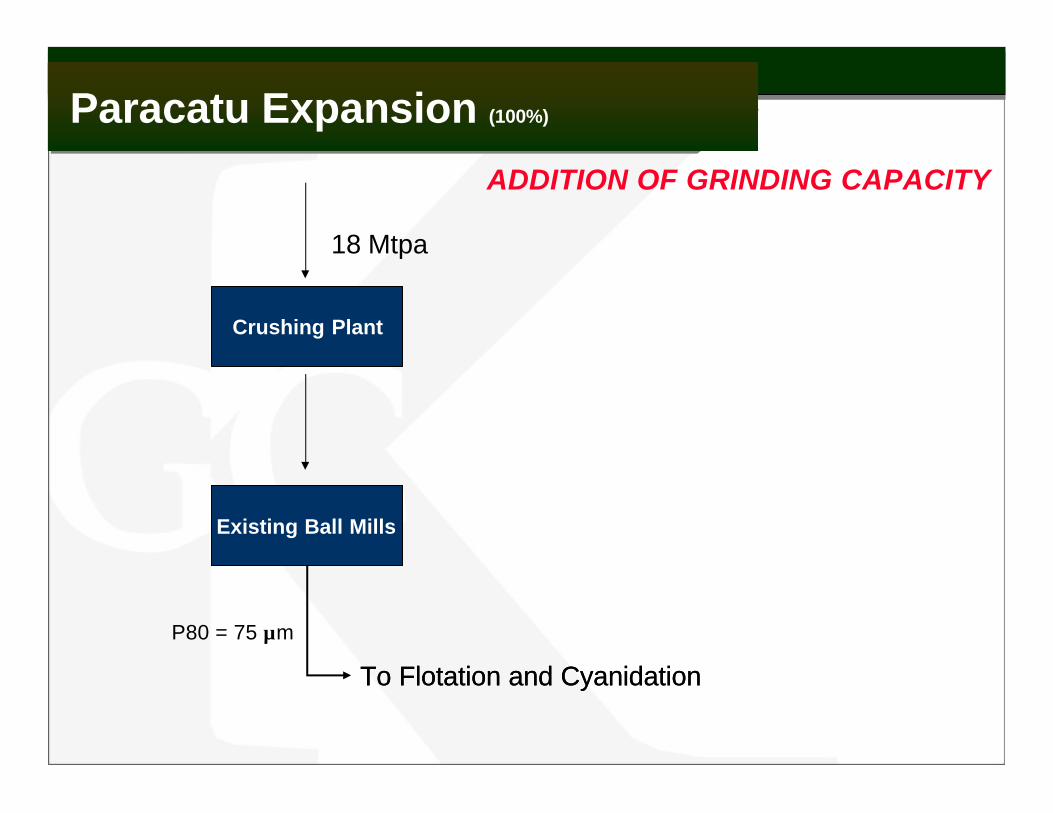

18 Mtpa

Existing Ball Mills

To Flotation and Cyanidation

Paracatu Expansion (100%)Paracatu Expansion (100%)

Crushing Plant

Existing Ball Mills

To Flotation and Cyanidation

P80 = 75 µm

ADDITION OF GRINDING CAPACITY

Paracatu Expansion (100%)Paracatu Expansion (100%)

Existing Ball Mills

To Flotation and Cyanidation

Existing Ball Mills

To Flotation and Cyanidation

30 Mtpa

P80 = 75 µm

ADDITION OF GRINDING CAPACITY

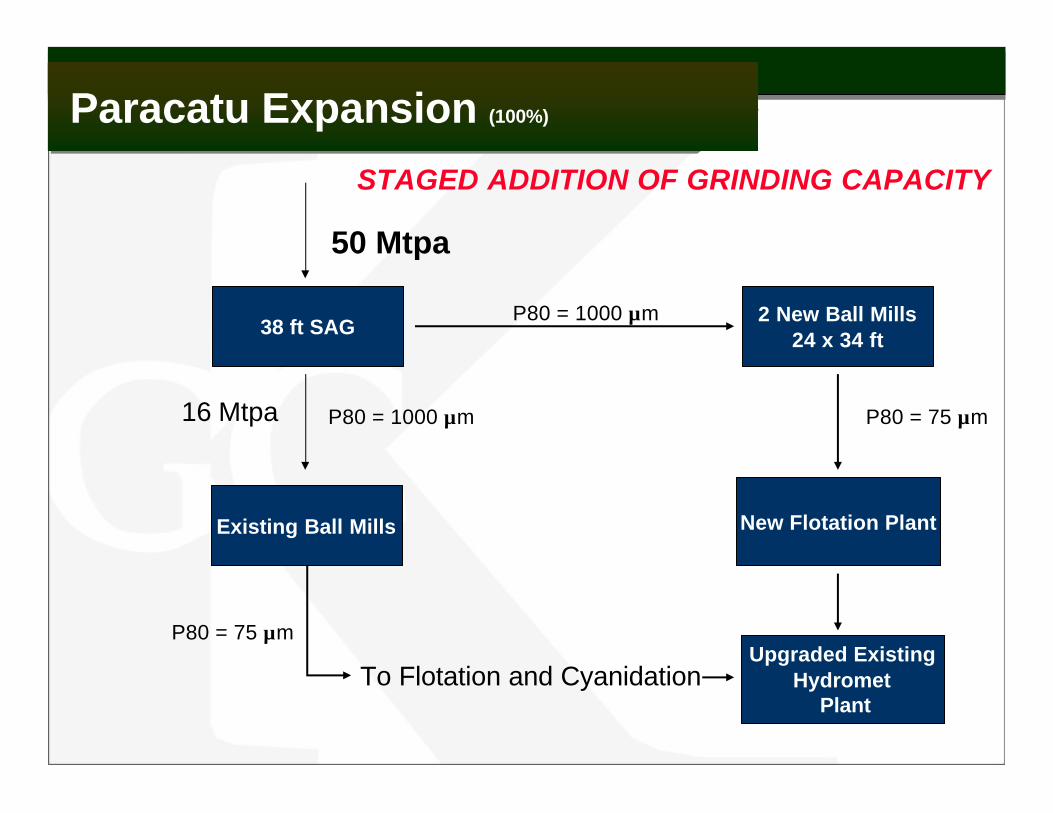

Crushing Plant38 ft SAG

STAGED ADDITION OF GRINDING CAPACITY

Paracatu Expansion (100%)Paracatu Expansion (100%)

Existing Ball Mills

P80 = 75 µm

To Flotation and Cyanidation

38 ft SAG

50 Mtpa

P80 = 1000 µm16 Mtpa

Upgraded ExistingHydromet

Plant

2 New Ball Mills24 x 34 ft

P80 = 75 µm

P80 = 1000 µm

New Flotation Plant

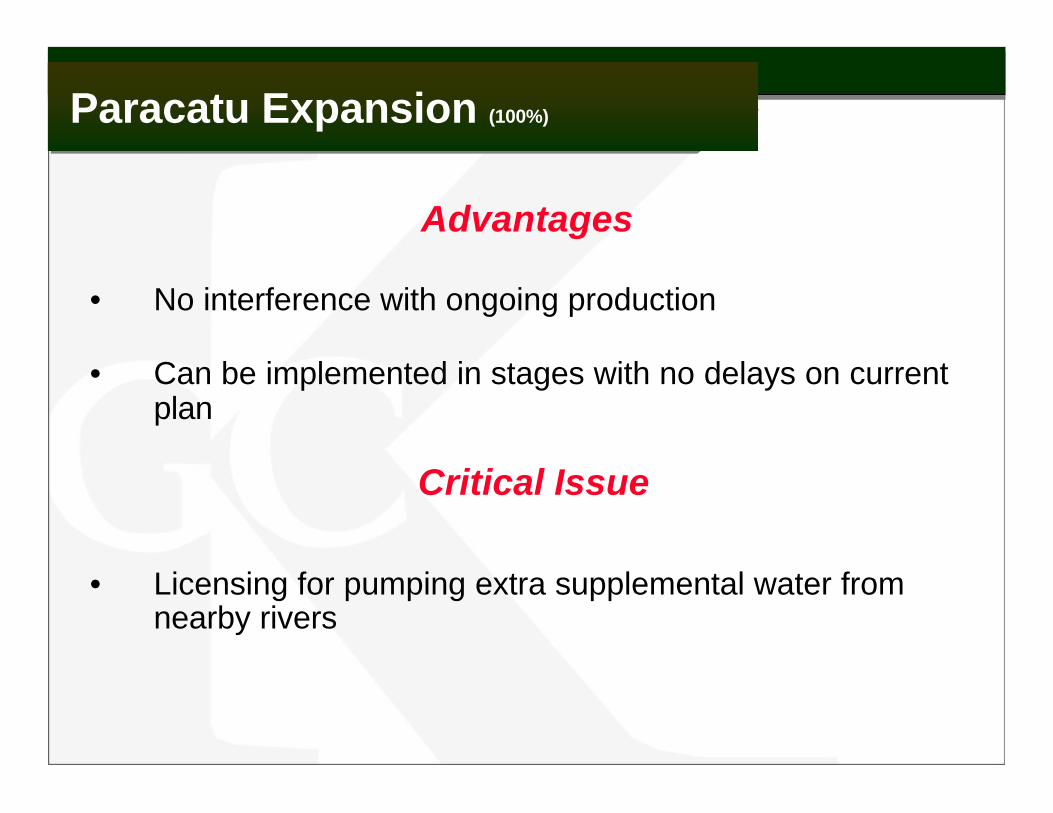

Advantages

• No interference with ongoing production

• Can be implemented in stages with no delays on current plan

• Licensing for pumping extra supplemental water from nearby rivers

Critical Issue

Paracatu Expansion (100%)Paracatu Expansion (100%)

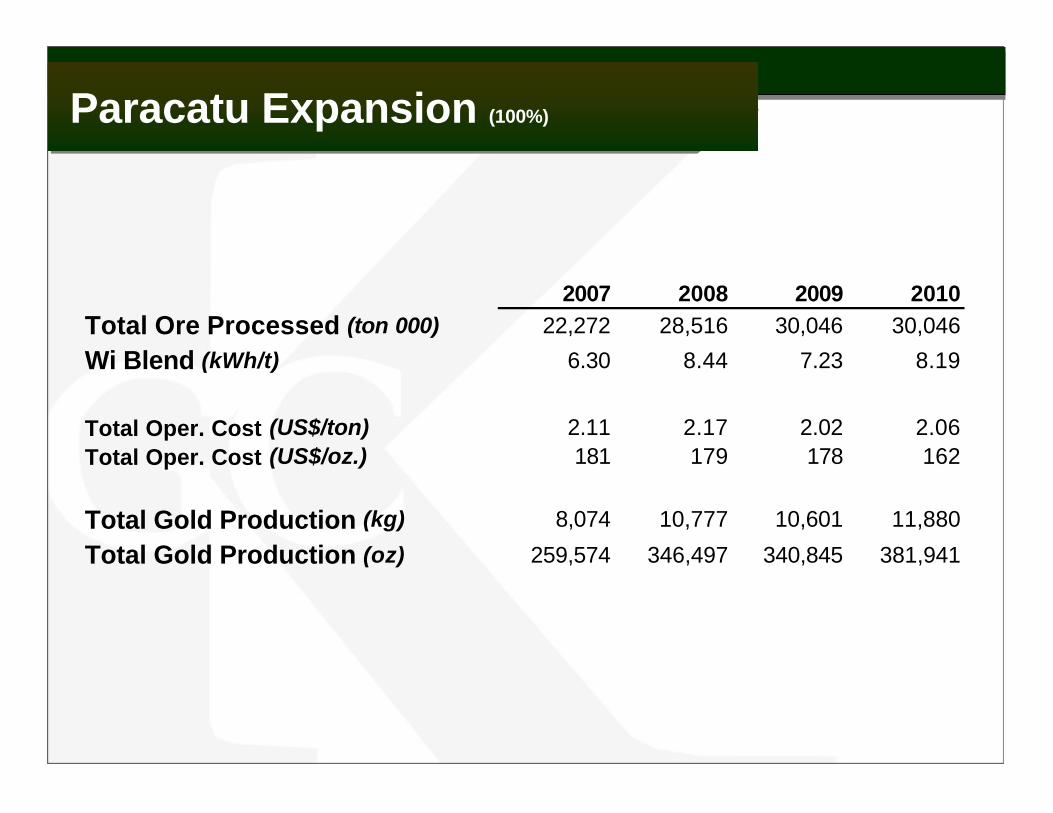

2007 2008 2009 2010Total Ore Processed (ton 000) 22,272 28,516 30,046 30,046

Wi Blend (kWh/t) 6.30 8.44 7.23 8.19

Total Oper. Cost (US$/ton) 2.11 2.17 2.02 2.06Total Oper. Cost (US$/oz.) 181 179 178 162

Total Gold Production (kg) 8,074 10,777 10,601 11,880

Total Gold Production (oz) 259,574 346,497 340,845 381,941

Paracatu Expansion (100%)Paracatu Expansion (100%)

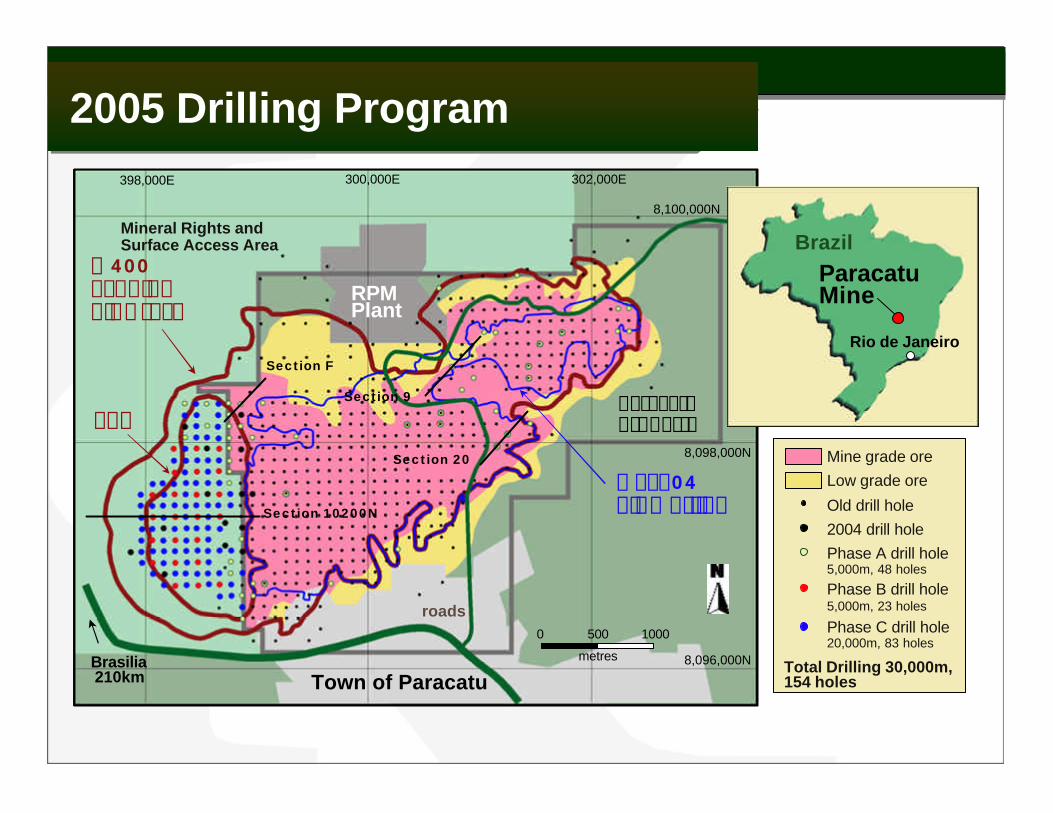

Paracatu Mine

Brazil

Rio de Janeiro

Town of Paracatu

398,000E

8,100,000N

Brasilia210km

$400 Scoping Pit Crest

ParacatuProperty

roads

Mine grade oreLow grade ore

Old drill hole2004 drill holePhase A drill hole5,000m, 48 holes

Phase B drill hole5,000m, 23 holes

Phase C drill hole20,000m, 83 holes

Mineral Rights andSurface Access Area

300,000E 302,000E

8,098,000N

8,096,000N

Dec.04 Pit Outline

0 500 1000

metres

RPMPlant

Toe

Section 10200N

Section F

Section 9

Section 20

Total Drilling 30,000m, 154 holes

2005 Drilling Program 2005 Drilling Program

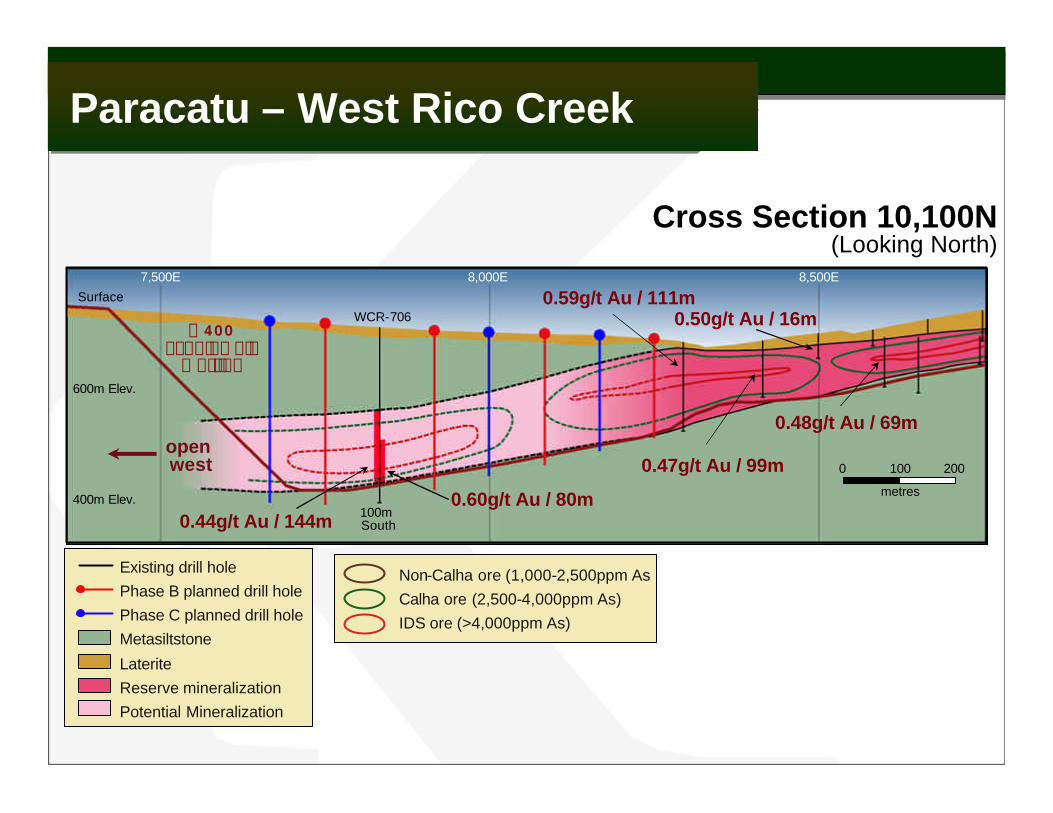

Cross Section 10,100N(Looking North)

Paracatu – West Rico CreekParacatu – West Rico Creek

7,500E 8,000E 8,500E

600m Elev.

400m Elev.

$400 Scoping Pit

Outline

0 100 200

metres

Existing drill holePhase B planned drill holePhase C planned drill holeMetasiltstone

LateriteReserve mineralizationPotential Mineralization

Surface

WCR-706

0.60g/t Au / 80m100m South

Non-Calha ore (1,000-2,500ppm AsCalha ore (2,500-4,000ppm As)IDS ore (>4,000ppm As)

0.59g/t Au / 111m

0.47g/t Au / 99m

0.50g/t Au / 16m

0.48g/t Au / 69m

0.44g/t Au / 144m

open west

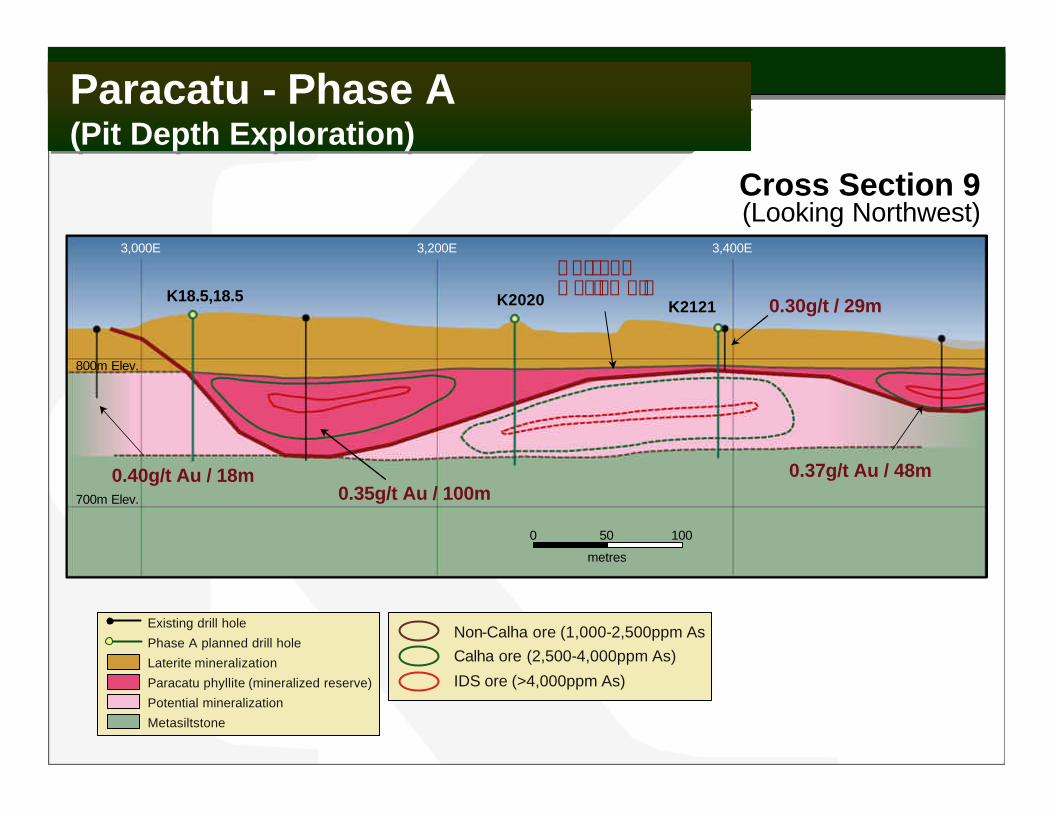

Cross Section 9(Looking Northwest)

Paracatu - Phase A (Pit Depth Exploration)Paracatu - Phase A (Pit Depth Exploration)

3,000E 3,200E 3,400E

800m Elev.

700m Elev. 0.35g/t Au / 100m

0.30g/t / 29m

0 50 100

metres

K2020

Existing drill hole

Phase A planned drill hole

Laterite mineralization

Paracatu phyllite (mineralized reserve)

Potential mineralization

Metasiltstone

Non-Calha ore (1,000-2,500ppm AsCalha ore (2,500-4,000ppm As)

IDS ore (>4,000ppm As)

0.40g/t Au / 18m 0.37g/t Au / 48m

CurrentDesign Pit

K2121K18.5,18.5

Fort Knox (100%)Fort Knox (100%)

Fort Knox – 7,600E (looking west)Fort Knox – 7,600E (looking west)

9,000E 10,000E 11,000E

2,000 ft.

1,000 ft.

Current Pit

$400 Pit Shell

0.100opt Au/35ft.

South North

FFC-04-727

0.291opt Au/15ft.

0.031opt Au/10ft.0. 048opt Au/10ft.

0.031opt Au/10ft.

0.038opt Au/120ft. 0.106opt Au/20ft.

GraniteSchistMineralized zoneOld exploration drill holeKinross drill hole

0 250 500

feet

UltimatePit

Open

Nice Photo of Round Mountain?Round Mountain (50%)Round Mountain (50%)

FairviewFinger Dump

South Pad Ramp

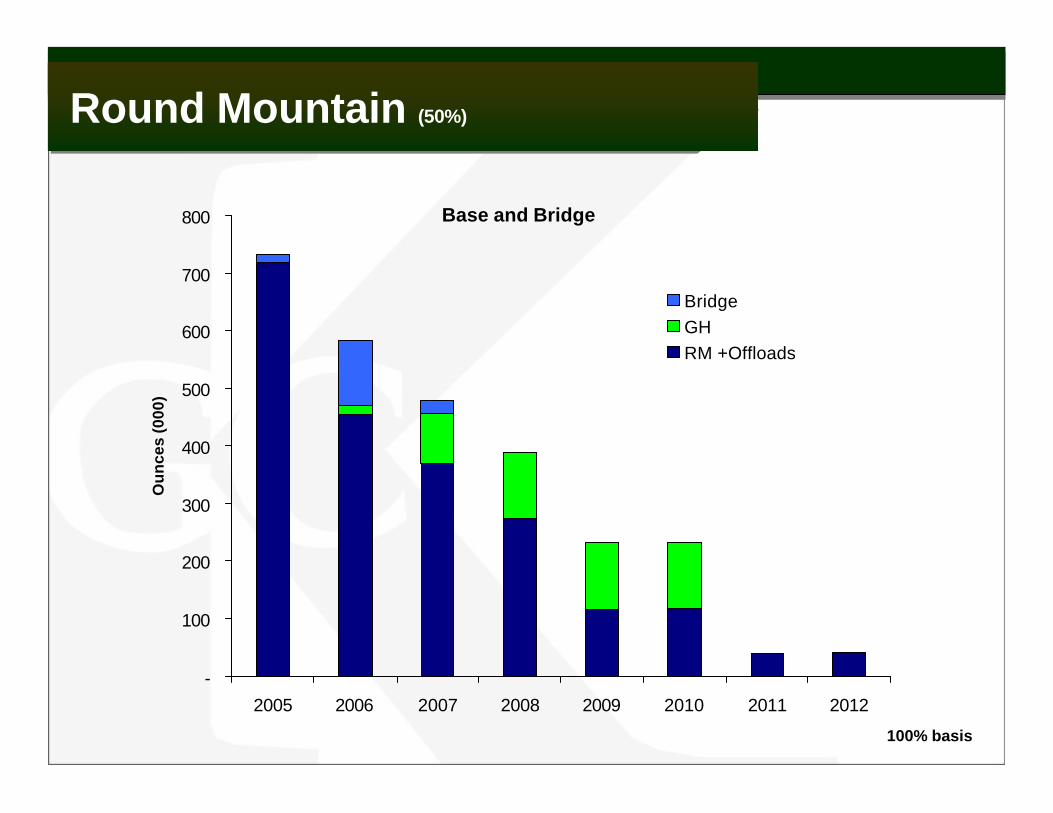

Round Mountain (50%)Round Mountain (50%)

Gold Production Estimate

Base and Bridge

-

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009 2010 2011 2012

Ou

nce

s (0

00)

BridgeGHRM +Offloads

Round Mountain (50%)Round Mountain (50%)

100% basis

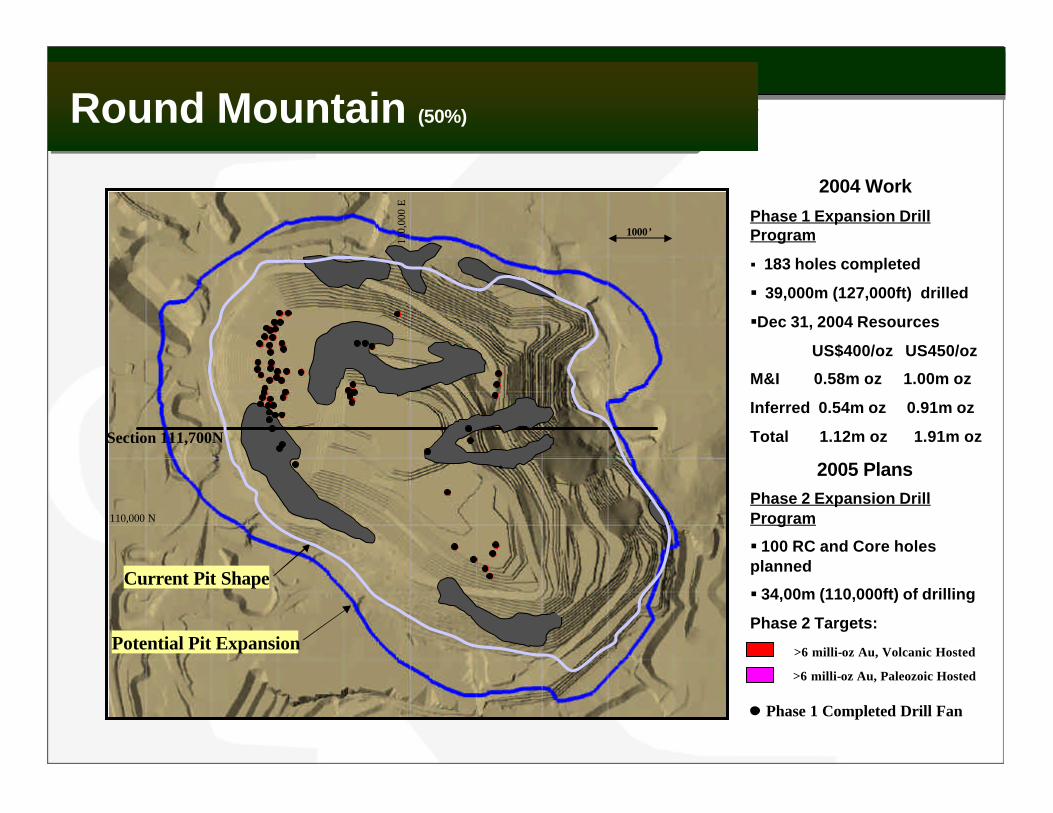

Round Mountain (50%)Round Mountain (50%)

>6 milli-oz Au, Paleozoic Hosted

>6 milli-oz Au, Volcanic Hosted

2004 Work

Phase 1 Expansion Drill Program

§ 183 holes completed

§ 39,000m (127,000ft) drilled

§Dec 31, 2004 Resources

US$400/oz US450/oz

M&I 0.58m oz 1.00m oz

Inferred 0.54m oz 0.91m oz

Total 1.12m oz 1.91m oz

2005 PlansPhase 2 Expansion Drill Program

§ 100 RC and Core holes planned

§ 34,00m (110,000ft) of drilling

Phase 2 Targets:Potential Pit Expansion

110,

000

E

110,000 N

1000’

Phase 1 Completed Drill Fan

Current Pit Shape

Section 111,700N

Round Mountain, Pit Expansion

108,000E

6,000 ft.

4,000 ft.

Current Pit

Phase 2Potential Pit Expansion

0 1000 2000

feet

110,000E 112,000EW E

Cross Section 111,700N, Looking North

?

Current Planned Pit

?

?

?

Alluvium

Volcanic sediments

Type 1 (welded tuff)

Type 2 (non-welded tuff)

Type 9 (transition)

Type 3 (welded lithic tuff)

Type 4 (Paleozoic sediments)

Granite + Paleozoic sediments

Ore reserve

Potential reserve addition

Mineralized envelope

Fault

Round Mountain (50%)Round Mountain (50%)

Gold Production EstimateRound Mountain (50%)Round Mountain (50%)

Base and Bridge

-

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009 2010 2011 2012

Ou

nce

s (0

00)

UGRM EXPBridgeGHRM +Offloads

100% basis

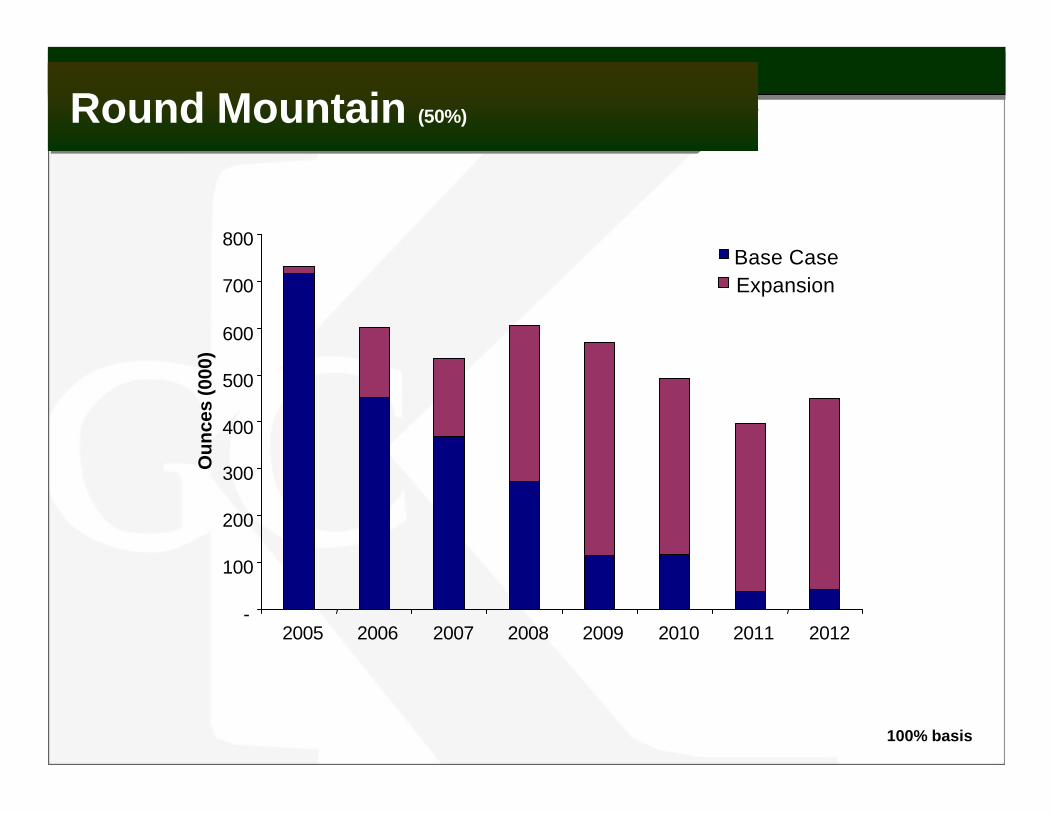

Gold Ounce ProductionRound Mountain (50%)Round Mountain (50%)

Expansion

-

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009 2010 2011 2012

Ou

nce

s (0

00)

Base Case

100% basis

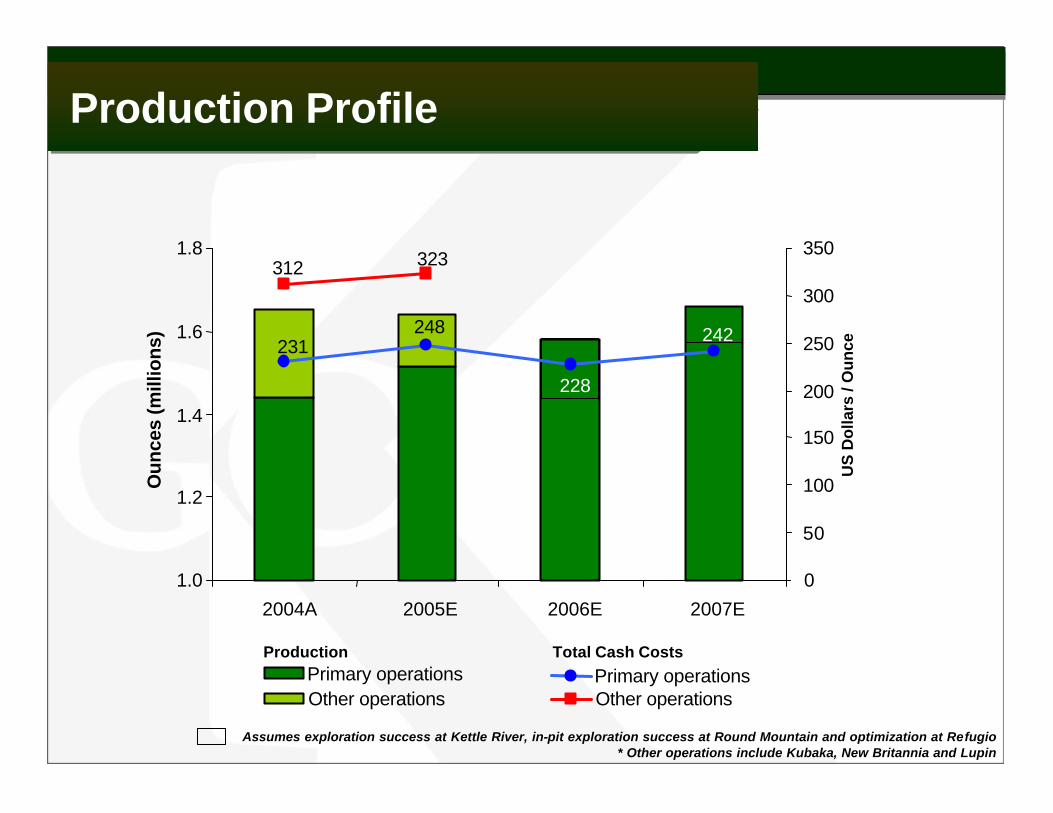

Production ProfileProduction Profile

323312

1.0

1.2

1.4

1.6

1.8

2004A 2005E 2006E 2007E

Ou

nce

s (m

illio

ns)

0

50

100

150

200

250

300

350

US

Do

llars

/ O

un

ce

Other operations Other operationsPrimary operations

Total Cash CostsPrimary operations

Production

Assumes exploration success at Kettle River, in-pit exploration success at Round Mountain and optimization at Refugio * Other operations include Kubaka, New Britannia and Lupin

242

228

248231

SummarySummary

Ø Paracatu – excellent potential to increase reserves and production rates

Ø Fort Knox – continuing to replace reserves

Ø Round Mountain – Feasibility of pit layback and U/G extend life

Ø Other opportunities – Crixas, La Coipa

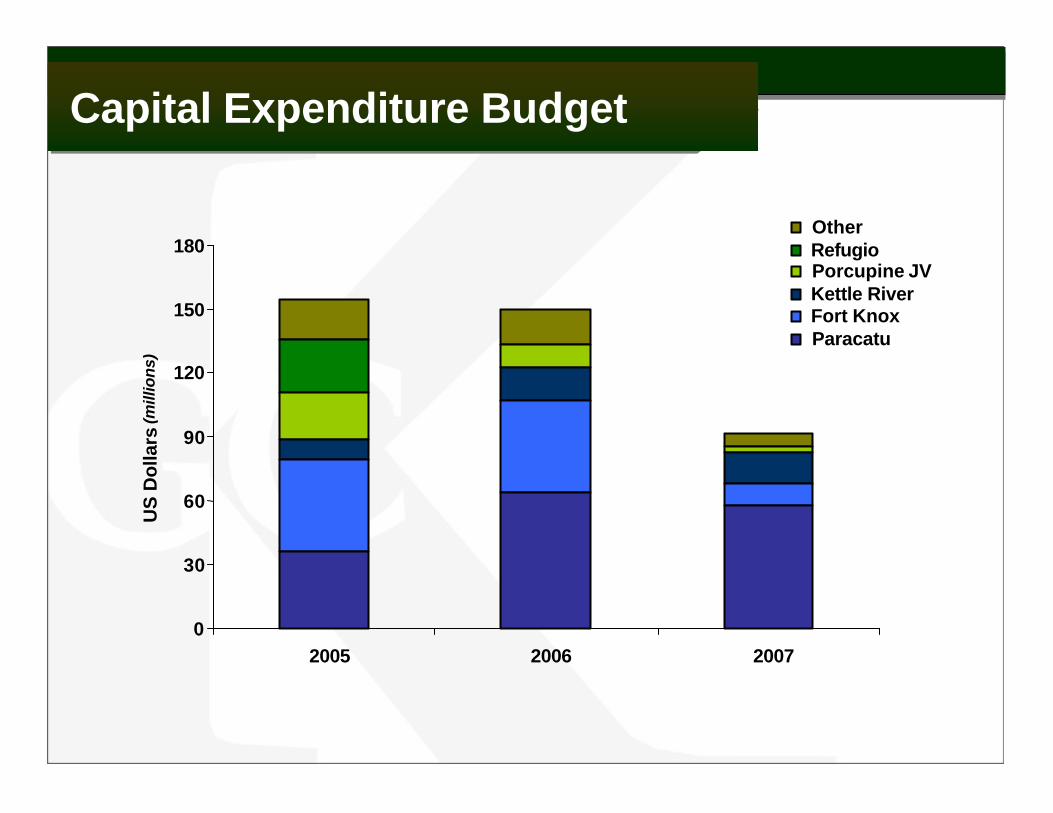

Capital Expenditure BudgetCapital Expenditure Budget

0

30

60

90

120

150

180

2005 2006 2007

US

Do

llars

(mill

ions

)

OtherRefugioPorcupine JVKettle RiverFort KnoxParacatu

dedicated tobeing world class

Kinross Gold Corporation40 King Street West, 52nd Floor

Scotia PlazaToronto, ON M5H 3Y2

416-365-5123416-363-6622866-561-3636

Shares outstanding: 346.6 millionMarket cap.: US$2.9 billion

KGC: NYSE K: TSXK.U: TSX (US dollar trading symbol)K.WT: TSX

www.kinross.com