Dangote Cement Plc · Headquartered in Lagos, Nigeria, Dangote Cement Plc is Africa's largest...

10

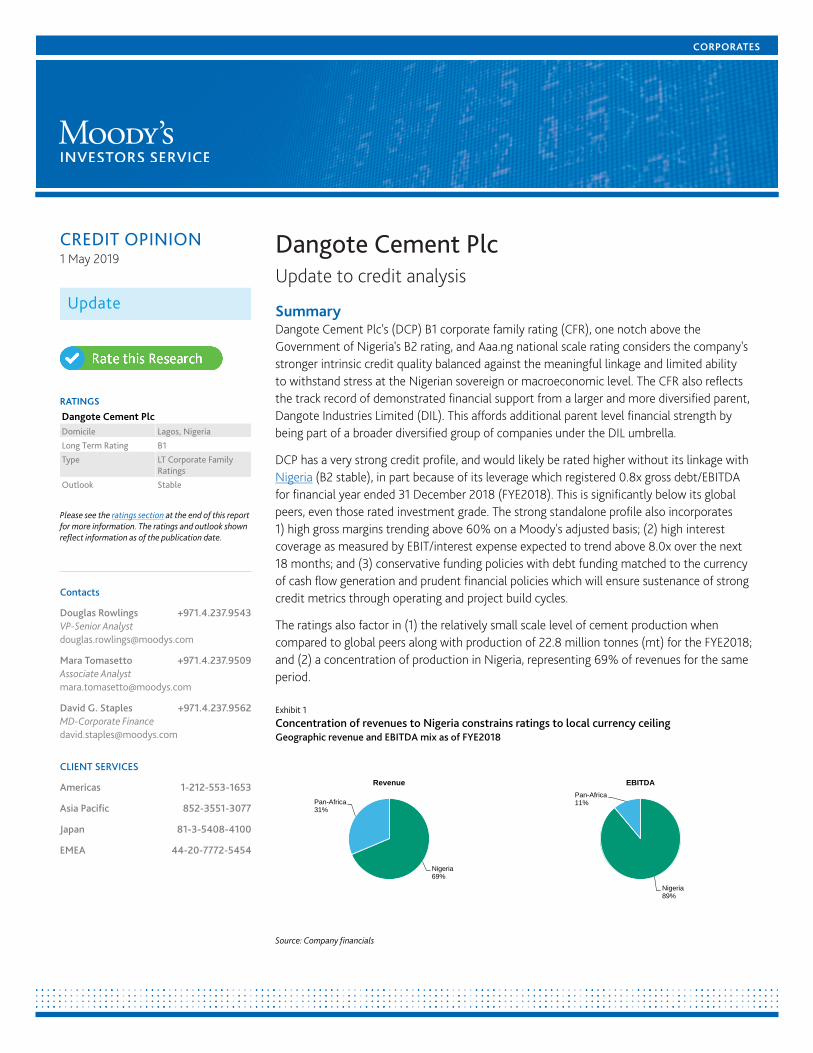

CORPORATES CREDIT OPINION 1 May 2019 Update RATINGS Dangote Cement Plc Domicile Lagos, Nigeria Long Term Rating B1 Type LT Corporate Family Ratings Outlook Stable Please see the ratings section at the end of this report for more information. The ratings and outlook shown reflect information as of the publication date. Contacts Douglas Rowlings +971.4.237.9543 VP-Senior Analyst [email protected] Mara Tomasetto +971.4.237.9509 Associate Analyst [email protected] David G. Staples +971.4.237.9562 MD-Corporate Finance [email protected] CLIENT SERVICES Americas 1-212-553-1653 Asia Pacific 852-3551-3077 Japan 81-3-5408-4100 EMEA 44-20-7772-5454 Dangote Cement Plc Update to credit analysis Summary Dangote Cement Plc's (DCP) B1 corporate family rating (CFR), one notch above the Government of Nigeria's B2 rating, and Aaa.ng national scale rating considers the company's stronger intrinsic credit quality balanced against the meaningful linkage and limited ability to withstand stress at the Nigerian sovereign or macroeconomic level. The CFR also reflects the track record of demonstrated financial support from a larger and more diversified parent, Dangote Industries Limited (DIL). This affords additional parent level financial strength by being part of a broader diversified group of companies under the DIL umbrella. DCP has a very strong credit profile, and would likely be rated higher without its linkage with Nigeria (B2 stable), in part because of its leverage which registered 0.8x gross debt/EBITDA for financial year ended 31 December 2018 (FYE2018). This is significantly below its global peers, even those rated investment grade. The strong standalone profile also incorporates 1) high gross margins trending above 60% on a Moody's adjusted basis; (2) high interest coverage as measured by EBIT/interest expense expected to trend above 8.0x over the next 18 months; and (3) conservative funding policies with debt funding matched to the currency of cash flow generation and prudent financial policies which will ensure sustenance of strong credit metrics through operating and project build cycles. The ratings also factor in (1) the relatively small scale level of cement production when compared to global peers along with production of 22.8 million tonnes (mt) for the FYE2018; and (2) a concentration of production in Nigeria, representing 69% of revenues for the same period. Exhibit 1 Concentration of revenues to Nigeria constrains ratings to local currency ceiling Geographic revenue and EBITDA mix as of FYE2018 Nigeria 69% Pan-Africa 31% Revenue Nigeria 89% Pan-Africa 11% EBITDA Source: Company financials

Transcript of Dangote Cement Plc · Headquartered in Lagos, Nigeria, Dangote Cement Plc is Africa's largest...

CORPORATES

CREDIT OPINION1 May 2019

Update

RATINGS

Dangote Cement PlcDomicile Lagos, Nigeria

Long Term Rating B1

Type LT Corporate FamilyRatings

Outlook Stable

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Douglas Rowlings +971.4.237.9543VP-Senior [email protected]

Mara Tomasetto +971.4.237.9509Associate [email protected]

David G. Staples +971.4.237.9562MD-Corporate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

Dangote Cement PlcUpdate to credit analysis

SummaryDangote Cement Plc's (DCP) B1 corporate family rating (CFR), one notch above theGovernment of Nigeria's B2 rating, and Aaa.ng national scale rating considers the company'sstronger intrinsic credit quality balanced against the meaningful linkage and limited abilityto withstand stress at the Nigerian sovereign or macroeconomic level. The CFR also reflectsthe track record of demonstrated financial support from a larger and more diversified parent,Dangote Industries Limited (DIL). This affords additional parent level financial strength bybeing part of a broader diversified group of companies under the DIL umbrella.

DCP has a very strong credit profile, and would likely be rated higher without its linkage withNigeria (B2 stable), in part because of its leverage which registered 0.8x gross debt/EBITDAfor financial year ended 31 December 2018 (FYE2018). This is significantly below its globalpeers, even those rated investment grade. The strong standalone profile also incorporates1) high gross margins trending above 60% on a Moody's adjusted basis; (2) high interestcoverage as measured by EBIT/interest expense expected to trend above 8.0x over the next18 months; and (3) conservative funding policies with debt funding matched to the currencyof cash flow generation and prudent financial policies which will ensure sustenance of strongcredit metrics through operating and project build cycles.

The ratings also factor in (1) the relatively small scale level of cement production whencompared to global peers along with production of 22.8 million tonnes (mt) for the FYE2018;and (2) a concentration of production in Nigeria, representing 69% of revenues for the sameperiod.

Exhibit 1

Concentration of revenues to Nigeria constrains ratings to local currency ceilingGeographic revenue and EBITDA mix as of FYE2018

Nigeria69%

Pan-Africa31%

Revenue

Nigeria89%

Pan-Africa11%

EBITDA

Source: Company financials

MOODY'S INVESTORS SERVICE CORPORATES

Credit strengths

» High operating margins supported by vertically integrated and largely market protected production

» Strong credit metrics being maintained through conservative financial policies with parent support

» Cement market share of 65% in Nigeria, sub-Saharan Africa’s largest cement market

» Strong potential to export cement from Nigeria to neighboring countries that lack limestone

Credit challenges

» Small scale cement producer compared to global rated peers

» Concentration of operations to Nigeria representing 69% of revenues creates sovereign rating linkage

Rating outlookThe stable ratings outlook reflects our expectation that DCP will continue to maximize output from existing plants outside Nigeria,while continuing to observe conservative financial policies. At the same time, the stable outlook assumes the ability to refinancematuring debt predominantly due to DIL in a timely manner.

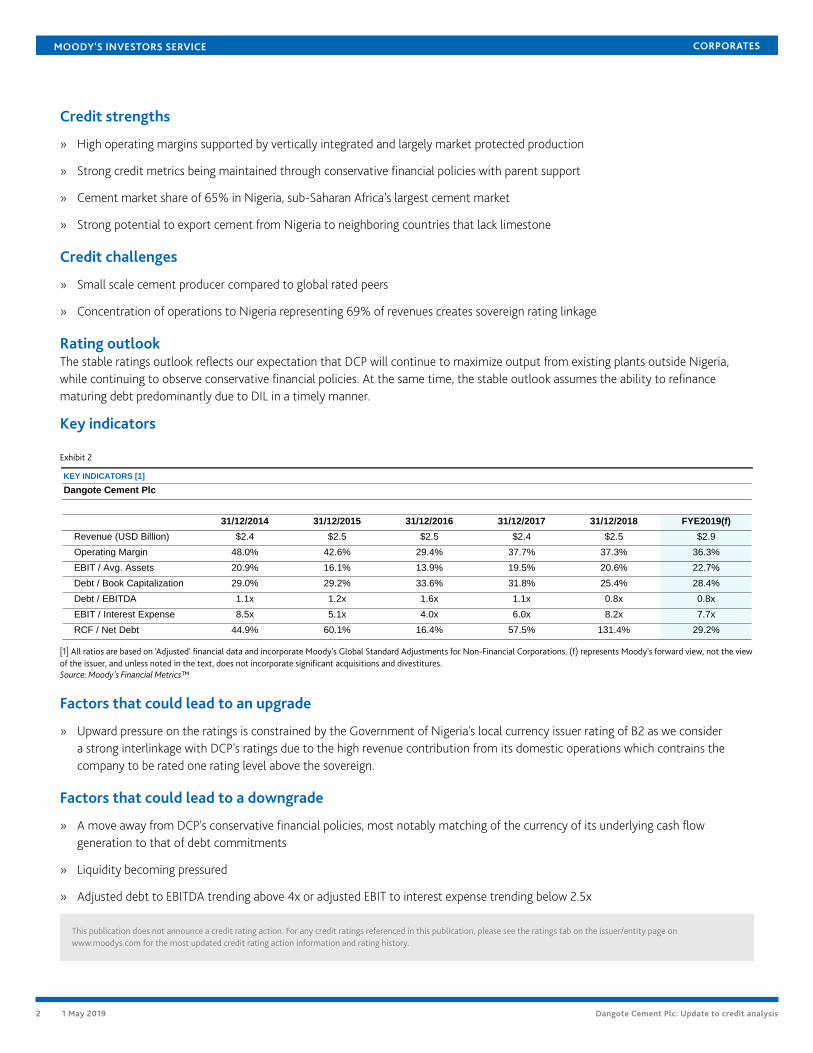

Key indicators

Exhibit 2

KEY INDICATORS [1]

Dangote Cement Plc

31/12/2014 31/12/2015 31/12/2016 31/12/2017 31/12/2018 FYE2019(f)

Revenue (USD Billion) $2.4 $2.5 $2.5 $2.4 $2.5 $2.9

Operating Margin 48.0% 42.6% 29.4% 37.7% 37.3% 36.3%

EBIT / Avg. Assets 20.9% 16.1% 13.9% 19.5% 20.6% 22.7%

Debt / Book Capitalization 29.0% 29.2% 33.6% 31.8% 25.4% 28.4%

Debt / EBITDA 1.1x 1.2x 1.6x 1.1x 0.8x 0.8x

EBIT / Interest Expense 8.5x 5.1x 4.0x 6.0x 8.2x 7.7x

RCF / Net Debt 44.9% 60.1% 16.4% 57.5% 131.4% 29.2%

[1] All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations. (f) represents Moody's forward view, not the viewof the issuer, and unless noted in the text, does not incorporate significant acquisitions and divestitures.Source: Moody's Financial Metrics™

Factors that could lead to an upgrade

» Upward pressure on the ratings is constrained by the Government of Nigeria's local currency issuer rating of B2 as we considera strong interlinkage with DCP's ratings due to the high revenue contribution from its domestic operations which contrains thecompany to be rated one rating level above the sovereign.

Factors that could lead to a downgrade

» A move away from DCP's conservative financial policies, most notably matching of the currency of its underlying cash flowgeneration to that of debt commitments

» Liquidity becoming pressured

» Adjusted debt to EBITDA trending above 4x or adjusted EBIT to interest expense trending below 2.5x

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 1 May 2019 Dangote Cement Plc: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

» Operating margins falling below 20% on a sustained basis

» Any downward momentum on the Federal Government of Nigeria's rating, or the introduction of special taxes, levies or otherpunitive measures in respect of profits or cashflow by the government of Nigeria

ProfileHeadquartered in Lagos, Nigeria, Dangote Cement Plc is Africa's largest cement producer. The group operates nine fully integratedcement plants, a grinding plant and two import terminals across Africa, with a combined capacity of 45.6 Mtpa and 65% share of themarket in Nigeria, Africa's largest economy and population. DCP has expanded its production base over the past three years with newplants in several African countries and is expected to increase further the total capacity to 47 Mtpa by the end of 2020.

For the FYE2018, DCP reported revenues of NGN901 billion ($2.5 billion) and an EBITDA of NGN444 billion ($1.2 billion) on a Moody'sadjusted basis. DCP has the largest market capitalisation on the Nigerian Stock Exchange at NGN3.2 trillion ($9.0 billion) as at 30 April2019 and is majority owned by Dangote Industries Limited (DIL).

Detailed credit considerationsHigh operating margins supported by vertically integrated and largely market protected productionDCP’s operating margin of 37.3% on a Moody's adjusted basis for the FYE2018 is the highest of the cement producers we rate globally,above West China Cement Limited (Ba3 stable) at 30.9% for the last twelve months ending 30 June 2018, with the next highestoperating margin.

Exhibit 3

DCP has the highest operating margins out of all the cement producers that Moody's rates globallyOperating margins: DCP versus peers

0%

5%

10%

15%

20%

25%

30%

35%

40%

Vulcan Materials Company(Baa3)

Union Andina de CementosS.A.A. (Ba2)

Votorantim Cimentos S.A. (Ba2) West China Cement Limited(Ba3)

Dangote Cement Plc (B1) Hi-Crush Partners LP (B2)

All figures are as of FYE2018 excluding Union Andina de Cementos S.A.A. (as of LTM Sep-2018) and West China Cement Limited (as of LTM Jun-2018).Source:Moody's Financial Metrics™

DCP’s portfolio of plants is comparable with the most efficient and modern plants in the industry using dry process technology. Theyrely upon well-known manufacturers for key equipment and componentry while using automation to ensure quality and reducedoverhead costs. Together, the scale and efficiency facilitated by the plants ensure low cost production, packaging and loading processes.

Given the scale of operations from a fleet of over 5,000 delivery trucks, production capacity of 45.6 million tons per annum (Mtpa)ramping up to 47 Mtpa by the end of 2020 with up to 55 Mtpa by 2022, large plants and mining operations, per unit costs arereduced as result of economies of scale. Critical mass achieved throughout DCP’s vertically integrated operations also allow for bulkprocurement discounts, low servicing and logistics costs and optimisation of overhead allocation.

At the same, DCP benefits from access to cheap raw material inputs with over 95% excluding fuel sourced domestically, mostly fromDCP’s own on-site mining operations. Plants are located next to limestone mining operations, mainly with conveyer systems for directdelivery, reducing mine to production logistics costs. Although gypsum is mainly imported, import prices over the past three years havedeclined.

3 1 May 2019 Dangote Cement Plc: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Energy, making up close to half of cement production costs, is sourced or generated at competitive comparative global kilowattper hour rates. Nigerian plants benefit from globally comparable cheap domestic gas supply through 20-year contracts with agreedpricing formulas. While gas remains a key source of energy across its Nigerian plants, coal has become predominant. This adds furtherflexibility to switch between various energy sources and phase-out the reliance on higher cost low-pour fuel oil. DIL has added coalmining as an additional component to DCP’s vertically integrated operations which provides an alternative as cheap feedstock for kilnfuel. At the same time, DCP has the ability to generate its own uninterrupted low-cost power at most of its plants using its own powerplants, which are powered by gas at its larger Obajana and Ibese plants.

With vertical integration across its operations, DCP locks in the margin added from sourcing raw material, to processing and productionthen onto end delivery. DCP has significant access to vast limestone reserves in Nigeria, with ownership or optionality of mining rights.These reserves have the capacity to provide limestone from its mining operations to DCP’s plants in Nigeria. Obajana has over 45 yearsof reserves, Ibese over 75 years and Gboko over 30 years. At the same time, DCP has a vast network of warehouses and trucks whichsupport a broad footprint for convenient low-cost delivery of cement to its customer base. Maintenance activities are also largelycarried out internally.

Bans or high import duties on imported cement in Nigeria along with several other countries in which DCP operates have boosted andprotected domestic production. DCP complies with these local rules by opening large integrated production units in these countries.DCP benefits further from protection in the markets where it operates, through always striving to be the lowest cost producer basedupon the aforementioned factors.

Strong credit metrics being maintained through conservative financial policies with parent supportDCP benefits from conservatively positioned credit metrics as evidenced by our adjusted Debt/EBITDA of 0.8x and EBIT to InterestExpense of 8.2x for the FYE2018. This compares favourably to our global peers which face a high degree of capital intensity given thenature of cement production.

Exhibit 4

DCP ranks very strongly relative to its peers leverage and interest coverageDebt/EBITDA and EBIT to Interest Expense: DCP versus peers

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

Vulcan Materials Company(Baa3)

Union Andina de CementosS.A.A. (Ba2)

Votorantim Cimentos S.A. (Ba2) West China Cement Limited(Ba3)

Dangote Cement Plc (B1) Hi-Crush Partners LP (B2)

Debt / EBITDA EBIT / Interest Expense

All figures are as of FYE2018 excluding Union Andina de Cementos S.A.A. (as of LTM Sep-2018) and West China Cement Limited (as of LTM Jun-2018).Source: Moody's Financial Metrics™

Despite the ongoing expansion plan to increase production capacity to 47 Mtpa by end of 2020 with up to 55 Mtpa by 2022, weexpect DCP’s Debt/EBITDA and EBIT to Interest Expense to remain below 1.0x and above 8.0x, respectively. Management has a trackrecord of conservative financial policy through primarily funding expansion with internal cash generation with a board-approvedmaximum Net Debt/ EBITDA level of 2x.

Cement market share of 65% in Nigeria, Africa’s largest population and economy, with growing GDPDCP’s core market, Nigeria, representing 69% of revenue for FYE2018, offers an enticing cement market proposition as Africa’s mostpopulous country with 194 million inhabitants and its largest economy with nominal GDP of $447 billion estimated for 2018. At thesame time, Nigeria benefits from a favourable demographic age distribution, where most of the population is below the age of 30.

4 1 May 2019 Dangote Cement Plc: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

DCP's ratings are further predicated upon a continuing growing cement market share of 65% in Nigeria as Africa's most populouscountry and its largest economy where GDP is expected grow in real terms by 2.3% in 2019. Worth noting that Nigeria's economy islargely diversified, with the oil and gas sector making up less than 10% of GDP.

Exhibit 5

DCP continues to maintain a dominant revenue market share in its domestic market in NigeriaDCP market share for the past 3 years (estimate)

65.0% 64.6% 64.6% 64.4%

50%

55%

60%

65%

70%

FYE2016 FYE2017 FYE2018 Q1 2019

Source: Company information

Furthermore DCP's sales and margins continue to benefit from the ongoing activity in the Nigerian economy. Nevertheless DCPremains at this stage strongly linked to Nigeria and its economy, with 89% of its EBITDA anchored in the country for FYE2018. Itsinvestments in new plant capacity in other sub Saharan countries will provide more diversification in future but it will take several yearsbefore there is a meaningful diversification of revenue, profits and cashflows away from the Nigerian economy. Pan-African volumesexpected to reach 40% of total sales volumes by 2020.

Cement will continue to feature prominently in consumer spending, driven by an increasingly urbanised youth entering the housingmarket, where housing demand in metropolitan areas continues to significantly exceed supply. DCP is actively building a brandpresence with individuals using targeted marketing. A planned $20 billion public infrastructure spend over the next 10 years by theNigerian government will add to demand. Therefore, infrastructure spend presents upside to cash flow generation for DCP’s centralbusiness model.

DCP and Lafarge Africa Plc make up approximately 88% of Nigeria’s cement market in 2018, with DCP as the market leader withmore than 65% share. Despite the attractive demand growth characteristics of the Nigerian cement market, we view the risk of newentrants as limited. This is predicated by (1) a government ban on cement imports which limits competition to new onshore productionentrants; and (2) the very high capital equipment cost associated with cement plant construction to compete on the same level ofscale and efficiency offered by domestic production plants. In addition, given its large production capacity – which is only utilised ataround 50% – and its vertically integrated operations, DCP is able to drive Nigerian cement price determination to a large extent of itsown accord. This reduces the attractiveness for new entrants when it comes to margin levels and cement supply opportunities.

Smaller scale cement producer compared to global rated peers with concentration of operations in Nigeria creatingsovereign linkageDCP’s ratings are constrained by its smaller scale when compared to its global cement peers, along with limited product and geographicdiversity. At present, DCP’s revenue is derived from the sale of cement, but there are plans to export clinker to Ghana, Ivory Coast andCameroon in the coming years. DCP’s revenue generation is concentrated in Nigeria, representing 69% total sales for FYE2018. DCP’sscale of revenue of NGN901 billion ($2.5 billion) for FYE2018 is in the lower quartile of global cement peers rated by us.

5 1 May 2019 Dangote Cement Plc: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 6

DCP operations are small relative to its global cement peersRevenue in USD million

0

1,000

2,000

3,000

4,000

5,000

Vulcan Materials Company(Baa3)

Union Andina de CementosS.A.A. (Ba2)

Votorantim Cimentos S.A.(Ba2)

West China Cement Limited(Ba3)

Dangote Cement Plc (B1) Hi-Crush Partners LP (B2)

US

D m

illio

n

All figures are as of FYE2018 excluding Union Andina de Cementos S.A.A. (as of LTM Sep-2018) and West China Cement Limited (as of LTM Jun-2018).Source: Moody's Financial Metrics™

With the exception of South Africa (Baa3 stable), we see the countries where DCP either has operations or is adding operations ashaving commensurate or higher risk to that of Nigeria. We recognise that DCP has a robust track record when it comes to navigatinghigh risk operating jurisdictions. Investment by DCP is seen to strategically benefit countries in its ability to provide low-cost high-quality cement to customers. This is key to facilitating economic and social upliftment in Africa - a focus for many of its governments.

The low geographical diversification in Nigeria is partially offset by the broad customer base, with its top 10 customers accountingfor 34% of total sales in Nigeria, but much of which was ordered on behalf of smaller distributors, given the incentives given to theirlarger counterparts. The domestic market is indeed primarily made up of individual buyers and only 3% is sold on a bulk basis, thereinreducing customer concentration exposures.

We see DCP’s expansion plan as largely de-risked as a result of (1) the fact that all the 15 Mtpa operations outside Nigeria werefunctional in 2018, (2) early successes in gaining market share in countries such as Senegal, South Africa, Cameroon, Zambia andEthiopia (3) the geographical diversity of the projects; and (4) DCP’s successful track record to date of project development.

Liquidity AnalysisUnder our forecasts DCP's liquidity profile is sufficient to meet the company's cash needs over the next 12 months. We estimate thatfunds from operations generation of NGN485 billion ($1.3 billion) for the next 12 months and an unrestricted cash balance of NGN167billion ($459 million) as of FYE2018 are sufficient to cover capex of NGN148 billion ($410 million) and dividends of NGN272 billion($760 million).

This will be supported by DCP's four committed trade finance facilities for a total amount of NGN122 billion ($340 million), of whichNGN2 billion ($56 million) was undrawn as of FYE2018, to be used to cover import payments via issuance of letters of credit.

Additionally, DCP's liquidity benefits from proven ongoing support from DIL. Although we do not expect that DCP would requireliquidity support from DIL, we expect that this would be forthcoming if ever needed.

Rating methodology and scorecard factorsWe have applied Moody's Global Building Materials Industry methodology (published in January 2017) to DCP, under which the groupscores at A2 on current credit metrics and A3 forecast credit metrics for the next 12-18 months. The deviation of the CFR from thegrid-indicated rating is explained by the concentration of cash flow generation to Nigeria and other high geopolitical risk operatingjurisdictions with low sovereign credit ratings.

6 1 May 2019 Dangote Cement Plc: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 7

Rating Factors

Dangote Cement Plc

Building Materials Industry Grid [1][2]

Factor 1 : Scale (5%) Measure Score Measure Score

a) Revenue (USD Billion) $2.5 Ba $2.5 - $2.9 Ba

Factor 2 : Business Profile (15%)

a) Business Profile Ba Ba Ba Ba

Factor 3 : Profitability and Efficiency (30%)

a) Operating Margin 37.3% Aaa 36% - 37% Aaa

b) Operating Margin Volatility 17.7% Ba 12% - 18% Baa

c) EBIT / Avg. Assets 20.6% Aa 22% - 24% Aa

Factor 4 : Leverage and Coverage (40%)

a) Debt / Book Capitalization 25.4% A 25% - 28% A

b) Debt / EBITDA 0.8x Aaa 0.8x - 0.9x Aaa

c) EBIT / Interest Expense 8.2x A 8x - 9x A

d) RCF / Net Debt 131.4% Aaa 30% - 40% A

Factor 5 : Financial Policy (10%)

a) Financial Policy Baa Baa Baa Baa

Rating:

a) Indicated Rating from Grid A2 A3

b) Actual Rating Assigned B1

Moody's 12-18 Month Forward View

As of 4/23/2019 [3]

Current

FY 12/31/2018

[1] All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations.[2] As of 12/31/2018.[3] This represents Moody's forward view, not the view of the issuer, and unless noted in the text, does not incorporate significant acquisitions and divestitures.Source: Moody's Financial Metrics™

7 1 May 2019 Dangote Cement Plc: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Appendix

Exhibit 8

Peer comparison table

(in USD million)

FYE

Dec-16

FYE

Dec-17

FYE

Dec-18

FYE

Dec-16

FYE

Dec-17

LTM

Sep-18

FYE

Dec-16

FYE

Dec-17

FYE

Dec-18

FYE

Dec-16

FYE

Dec-17

LTM

Jun-18

Revenue $2,500 $2,436 $2,493 $1,040 $1,085 $1,188 $3,437 $3,423 $3,474 $560 $705 $807

EBITDA $1,052 $1,203 $1,230 $333 $350 $371 $906 $739 $900 $200 $284 $380

Operating Margin 29.4% 37.7% 37.3% 19.9% 18.5% 18.4% 10.0% 6.0% 12.0% 14.4% 22.8% 30.9%

Oper. Margin Volatility 19.7% 20.4% 17.7% 7.2% 9.8% 18.0% 32.0% 45.1% 41.3% 28.9% 40.7% 65.7%

ROA - EBIT / Avg. Assets 13.9% 19.5% 20.6% 6.5% 6.3% 6.9% 6.4% 4.1% 6.8% 4.9% 9.8% 14.7%

EBIT / Int. Exp. 4.0x 6.0x 8.2x 2.5x 2.4x 2.8x 1.4x 0.9x 1.9x 2.1x 4.5x 7.3x

Debt / EBITDA 1.6x 1.1x 0.8x 4.4x 3.9x 3.5x 5.2x 6.5x 4.7x 3.0x 2.0x 1.4x

Total Debt/Capital 33.6% 31.8% 25.4% 51.1% 48.0% 46.0% 66.3% 61.0% 60.3% 40.3% 35.8% 32.5%

RCF / Net Debt 16.4% 57.5% 131.4% 10.2% 11.0% 13.6% 6.7% 6.3% 10.9% 33.9% 60.6% 82.2%

Dangote Cement Plc Union Andina de Cementos S.A Votorantim Cimentos S.A. West China Cement Limited

B1 stable Ba2 Stable Ba2 stable Ba3 stable

All figures and ratios are calculated using Moody's estimates and standard adjustments. FYE = financial year-end; LTM = last twelve months.Source: Moody's Financial Metrics™

Exhibit 9

Moody's-adjusted debt breakdown

(in USD million)

FYE

Dec-13

FYE

Dec-14

FYE

Dec-15

FYE

Dec-16

FYE

Dec-17

FYE

Dec-18

As Reported Debt 1,132 1,326 1,231 1,132 1,034 922

Pensions 12 11 20 0 0 0

Operating Leases 14 19 12 8 16 31

Non-Standard Adjustments 0 0 123 191 115 49

Moody's-Adjusted Debt 1,159 1,355 1,386 1,330 1,165 1,002

All figures and ratios are calculated using Moody's estimates and standard adjustments.Source: Moody's Financial Metrics™

Exhibit 10

Moody's-adjusted EBITDA breakdown

(in USD million)

FYE

Dec-13

FYE

Dec-14

FYE

Dec-15

FYE

Dec-16

FYE

Dec-17

FYE

Dec-18

As Reported EBITDA 1,489 1,458 1,405 1,218 1,288 1,214

Pensions 0 1 1 0 0 0

Operating Leases 5 7 4 3 5 4

Unusual -9 -75 -276 -169 -83 13

Non-Standard Adjustments 0 0 0 0 -7 -2

Moody's-Adjusted EBITDA 1,484 1,390 1,135 1,052 1,203 1,230

All figures and ratios are calculated using Moody's estimates and standard adjustments.Source: Moody's Financial Metrics™

8 1 May 2019 Dangote Cement Plc: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

Ratings

Exhibit 11Category Moody's RatingDANGOTE CEMENT PLC

Outlook StableCorporate Family Rating B1NSR LT Corporate Family Ratings (Domestic) Aaa.ng

Source: Moody's Investors Service

9 1 May 2019 Dangote Cement Plc: Update to credit analysis

MOODY'S INVESTORS SERVICE CORPORATES

© 2019 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEEMOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’SRATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDITRATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAYALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDITRATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONSARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONSWITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDERCONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSESAND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDITRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for ratings opinions and services rendered by it fees ranging from $1,000 to approximately $2,700,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as tothe creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for ratings opinions and services rendered by it feesranging from JPY125,000 to approximately JPY250,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1172171

10 1 May 2019 Dangote Cement Plc: Update to credit analysis