Dairy Situation and Outlook Geoff Benson Dept. of Agricultural & Resource Economics NC State...

56

Dairy Situation and Outlook Geoff Benson Dept. of Agricultural & Resource Economics NC State University Southern Agricultural Outlook Conference Atlanta, September 24-26, 2007

-

date post

22-Dec-2015 -

Category

Documents

-

view

217 -

download

1

Transcript of Dairy Situation and Outlook Geoff Benson Dept. of Agricultural & Resource Economics NC State...

Dairy Situation and Outlook

Geoff BensonDept. of Agricultural & Resource EconomicsNC State University

Southern Agricultural Outlook ConferenceAtlanta, September 24-26, 2007

22

Topics National Short-term Situation and

OutlookNational dairy policiesDemandSupply

Regional Outlook Summary and Conclusions Implications

3

National Dairy Programs

3

4

Dairy Programs

Price support program Milk Income Loss Contract –

MILC Tariff Rate Quotas on imports Federal Orders Cooperatives Working Together

– CWT

4

5

Price Support Program Authorized until Dec 31, 2007 Government acts as a buyer of last resort

for cheese, butter and nonfat dry milk Support price is $9.90/cwt, basically

unchanged since 1990 Current product prices are:

Cheese at $1.1314/lb -- blocksButter at $1.05/lb -- bulkNFDM at $0.80/lb -- unfortified

Indirectly supports farm prices

5

6

Price Support Program Important historically, now provides a low

safety net Since 1989, Government purchases have

been seasonal & relatively smallButter in the early 1990s, NFDM more recently

Farm prices have been market driven and have been very volatile Seasonality in production and sales Inelastic supply & demand Market psychology

6

77

1/75 75 75 75 75 75 75 75 75 75 75 751/76 76 76 76 76 76 76 76 76 76 76 761/77 77 77 77 77 77 77 77 77 77 77 771/78 78 78 78 78 78 78 78 78 78 78 781/79 79 79 79 79 79 79 79 79 79 79 791/80 80 80 80 80 80 80 80 80 80 80 801/81 81 81 81 81 81 81 81 81 81 81 811/82 82 82 82 82 82 82 82 82 82 82 821/83 83 83 83 83 83 83 83 83 83 83 8319841/84 84 84 84 84 84 84 84 84 84 841/85 85 85 85 85 85 85 85 85 85 85 851/86 86 86 86 86 86 86 86 86 86 86 861/87 87 87 87 87 87 87 87 87 87 87 871/88 88 88 88 88 88 88 88 88 88 88 881/89 89 89 89 89 89 89 89 89 89 89 891/9090909090909090909090901/91 91 91 91 91 91 91 91 91 91 91 911/92 92 92 92 92 92 92 92 92 92 92 921/93 93 93 93 93 93 93 93 93 93 93 931/94 94 94 94 94 94 94 94 94 94 94 941/95 95 95 95 95 95 95 95 95 95 95 951/96 96 96 96 96 96 96 96 96 96 96 961/97 97 97 97 97 97 97 97 97 97 97 971/98 98 98 98 98 98 98 98 98 98 98 981/99 99 99 99 99 99 99 99 99 99 99 991/00 00 00 00 00 00 00 00 00 00 00 001/01 01 01 01 01 01 01 01 01 01 01 011/02 02 02 02 02 02 02 02 02 02 02 021/03 03 03 03 03 03 03 03 03 03 03 031/04 04 04 04 04 04 04 04 04 04 04 041/05 05 05 05 05 05 05 05 05 05 05 051/06 06 06 06 06 06 06 06 06 06 06 061/07 07 07 07 07 07 07 070.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

22.00

Federal Dairy Support and Class III (Cheese) Milk Prices, Monthly, 1975-2007

Dairy Support

Class III Milk

$/1

00

lb

8

Milk Income Loss Contract MILC

A countercyclical income support program passed as part of the 2002 Farm Bill; sunset date Sept. 30, 2005

The Agricultural Reconciliation Act of 2005 reauthorized the program through August 31, 2007 (MILC-X)

MILK-X extended one month as part of an Iraq/Katrina/Veterans funding bill. As a consequence, MILC is included in the 2007 Farm Bill baseline

8

9

MILC-X Program Trigger and cap

National target price or trigger for payments = $16.94/cwt Class I price in the Boston zone, Northeast federal order

Payments are limited to 2.4 mil. lb. of milk per operation per fiscal year ~ 125 cows @19,000 lb/cow/year

MILC payment rate was 45% when the Class I price was below $16.94

MILK-X payment rate is 34% of the difference

9

10

MILC Impacts….US All Milk Price

MILC Payment

$/cwt

MILC as % of All

Milk

FY 2002* $12.72 $1.08 9.0%

FY 2003 $11.91 $1.46 12.2%

FY 2004 $15.64 $0.22 1.4%

FY 2005 $15.37 $0.00 0.0%

FY 2006 $13.24 $0.50 3.8%

10

* 10 Months

1111

1212

Federal Orders Classify milk based on use

Class I = Fluid milkClass II = “Soft” productsClass III = CheeseClass IV = Butter & NFDM

Set monthly minimum class prices based on wholesale prices for cheese, butter and non-fat solids, yield factors, make allowances = Derived demand for milk

Establish pooling rules determining which handlers and producers are in an order

Audit milk handlers

13

Federal Orders 7 orders pay on components – most milk

is used for manufacturing in these FOs 4 high fluid use order markets pay on a

per 100 lb. of milk basis, including the Appalachian and Southeast Orders

Requested changes:Larger “make allowances”Higher Class I & II pricesModifications to Class III & IV formulas Increased transportation credits and new

incentives to move milk and reduce costs in FO 5 and 7

14

CWT Program Dairy coop members of the National Milk

Producers Federation operate a voluntary supply management program to cut production and boost prices

Funded by an assessment Supported by coops with ~70% of milk

1. Herd Reduction – 4 “rounds” with ~ 200,000 cows removed

2. Production Reduction – 1 round3. Export subsidies, mainly cheese

FAPRI estimated impact on milk prices of $2 bil. through first 3 rounds of buyouts

15

Farm Bill Dairy Programs House dairy legislation is similar

to the expiring farm bill Senate?

Some are seeking a higher MILC trigger price and a higher percentage payment rate

The new DFWT wants a national, mandatory “CWT” buyout program

Change federal milk market orders

15

16

Market Demand Cheese &

byproducts Fluid milks &

butterfat Butter & ice-

cream Milk powders

and components

Organic & specialty products

1717

.

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

F140,000

150,000

160,000

170,000

180,000

190,000

200,000

210,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

f(x) = 2296.02857142857 x + 146667.904761905

f(x) = 316.467857142857 x + 15395.4571428571

Total Milk Production and Milk per Cow, 1993-2007F

Total production

Trend in Milk Production

Production per cow

Trend in Milk Per Cow

Mil

k P

rod

uc

tio

n,

Mil

. lb

.

Mil

k p

er

Co

w,

lb.

1818

Consumer Price Indices for All Items (CPI-U), Food and Dairy, 1970-2006. (1982-84=100)

0

50

100

150

200

250

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006

Food Dairy CPI-U

1919

Total and Per Capita Milk Disappearance, Milkfat Basis, 1975-2005

y = 2.2552x + 106.24

300

400

500

600

700

800

900

1000

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005

Per

cap

ita,

lb.

60

80

100

120

140

160

180

200

To

tal,

bil.

lb.

Per Capita

Total

Trend in Total Disapp.

20

Demand

DomesticConventional productsrBST “free” (affects supply)Organic and specialty

productsExports

20

2121

Dairy Exports For 2006 and year-to-date in 2007

exports of dried milk powders, whey products, other milk components, showed strong revenue growthLow US prices in 2006 and early 2007Weakening dollarReduced production & exports from NZ

& AustraliaReduced exports from the EU as a

result of CAP reformsDemand growth, especially in Asia

2222

Jan-9

0

Nov-90

Sep-9

1

Jul-9

2

May

-93

Mar

-94

Jan-9

5

Nov-95

Sep-9

6

Jul-9

7

May

-98

Mar

-99

Jan-0

0

Nov-00

Sep-0

1

Jul-0

2

May

-03

Mar

-04

Jan-0

5

Nov-05

Sep-0

60.000

0.500

1.000

1.500

2.000

2.500

3.000Exchange Rates, Foreign Currency per

US$ New Zealand

EU12 Euro

2323

Milk P owder P ric es , US and Oc eania, US $ per Metric T on, 2000-07

0

1000

2000

3000

4000

5000

6000

2000:1 2001:1 2002:1 2003:1 2004:1 2005:1 2006:1 2007:1

$ per

Met

ric T

on

0

1000

2000

3000

4000

5000

6000

OC E ANIA S K IM MIL K P OWDE R

US NF DM, G rade A

2424

2000:129 5 33 9 37 13 41 17 45 21 49 252007:1290

1000

2000

3000

4000

5000

6000

0

1000

2000

3000

4000

5000

6000

Cheese Prices, US and Oceania, $ per Metric Ton, 2000-07

Oceania Cheddar Cheese

US American Cheese, Barrels

$ p

er

Me

tric

To

n

25

US Dairy Product Trade, US$, 1997-2006

0

0.5

1

1.5

2

2.5

3

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

$bill

ion

ExportsImports

26

US Nonfat Dry Milk Powder Exports, 1996-2006

0

100

200

300

400

500

600

700

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

$mill

ions

0

50

100

150

200

250

300

350

'000

Met

ric

Tons

ValueQuantity

27

2007 Exports Total Value of US dairy exports up

35% Jan-July ‘07 v. ’06 Sharply higher prices since January

Skim Milk Powder up 70%Cheese up 70%Butter up 90%

We may be seeing some price resistance

28

Current Situation 2006 US Milk Production @ 181.8 bil.

lb. 2.8%Milk per cow 19,951 lb, 2.0%Cow numbers @ 9.1 mil, 0.1%

2006 Commercial Sales 2.5%Cheese 4.6%Butter 0.5%Nonfat dry milk 4.5%Fluid milk 0.1%

28

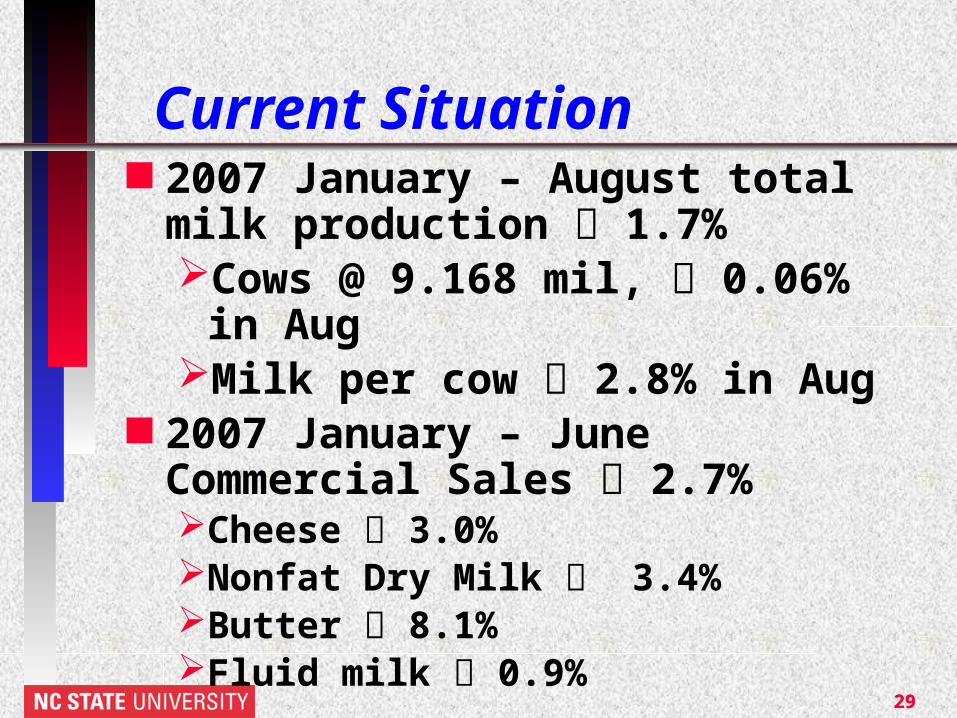

29

Current Situation 2007 January – August total milk

production 1.7%Cows @ 9.168 mil, 0.06% in AugMilk per cow 2.8% in Aug

2007 January – June Commercial Sales 2.7%Cheese 3.0%Nonfat Dry Milk 3.4%Butter 8.1%Fluid milk 0.9%

29

30

Outlook for 2008

30

31

Export Prospects Continued world demand growth but

consumer price resistance Continued weakness of the US$ Supply-demand balance in EU27 Normal supplies from New Zealand

but continued drought related problems in Australia

Some expansion of world supplies

World market prices will soften?31

3232

US Sales Outlook US Demand

+ Slow economic growth+ Continued population growth+ Continued producer & processor funded

advertising and promotion+ Lower consumer prices v. 2007

Overall sales will grow at trend rates, say +2.0%Cheese: 2-3%, adequate stocks, lower

pricesButter: adequate stocks, lower pricesFluid milk: little change Milk powders: little change in use

3333

Supply Outlook Cheese & butter inventories are edging up August cow numbers were up 54,000 over

August 2006 and up 11,000 over July ‘07July 1 heifer inventory was up 3.0% US will re-open Canadian border to

breeding stock November 19, 2007 Feed costs have increased but feed-milk

price ratio has been favorable = Cow cull rate is fairly neutral Milk/cow will be affected by reduced rBST Higher fertilizer and energy related costs

3535

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 5230

35

40

45

50

55

60

65

70

Dairy Cow Slaughter, F.I., Weekly, 2003-2007

2003

2005

2006

2007

Week

'00

0 H

ea

d

3636

Dairy Cattle, US & Canada

ItemUS

Mil. HeadCanada

Mil. HeadCanada % of US

Dairy Cows 9.15 0.98 10.7 %

Dairy Heifers

3.9(Over 500 lb.)

0.48(Over 12 mo.)

12.3 %

Heifers as % of cows 42.6 % 49.0 % --

Historically, US heifer imports = 50-75,000 head/year

3737

.Total Milk Production and Milk per Cow, 1993-2007

140,000

150,000

160,000

170,000

180,000

190,000

200,000

210,000M

ilk P

rod

uct

ion

, Mil.

lb.

.

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

Milk

per

Co

w, l

b.

Total productionProduction per cowTrend in Milk Per CowTrend in Milk Production

38

Fuel & Feed Costs Persistent higher oil & energy prices Ethanol demand and the knock-on

effects on other crops represents a permanent increase in feed costs for dairy farmers

Feed prices are projected to continue above historic averages in 2007-08Corn @ $3.10/bu, US farm avg.48% soybean meal @ $220/ton

Current Milk:Feed Price ratio remains high enough to make some more milk but forecast price ratio is unfavorable

38

3939

Feed costs $1.00 per bushel = $36/ton If you feed 2 tons of corn per cow per year

and if the cost increase: is $1.00/bu. = $72/cow/year is $1.50/bu. = $108/cow/year

If you feed 3 tons of corn per cow per year and if the cost increase: is $1.00/bu. = $108/cow/year is $1.50/bu. = $162/cow/year

If you sell 20,000 lb. of milk per cow, an increase of $100 = $0.50 per 100 lb.

40

Milk:Feed Price Ratio, Monthly, 2002-07

0

0.5

1

1.5

2

2.5

3

3.5

4

41

Prices Paid for Feed and Fuel

ItemApril 2003

April 2005

April 2006

April 2007

% 2003-07

Diesel, $/gal 1.24 1.97 2.28 2.43 + 96%

Gasoline, $/gal 1.60 2.23 2.60 2.64 + 65%

L.P. Gas, $/gal 1.21 1.47 1.69 1.73 + 43%

20% CP dairy Feed, $/ton 201 206 226 258 + 28%

41

Source: Ag. Prices, NASS, April issues, selected years

42

Prices Paid for Selected Fertilizers, $/ton

ItemApril 2003

April 2005

April 2006

April 2007

% 2003-07

Amm. Nitrate 243 292 366 382 + 57%Urea 261 332 362 453 + 74%30% N Solution 161 215 232 277 + 72%Super-phosphate 243 299 324 418 + 72%

Muriate of Potash 165 245 273 280 + 70%

42

Source: Ag. Prices, NASS, April issues, selected years

4343

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

F

-3.0

-1.5

0.0

1.5

3.0

4.5

6.0

7.5

Year-to-Year Changes in Total Milk Production, Cow Numbers and Milk per Cow, 1989-2007

Year-to-Year Change in Cow NumbersYear-to-Year Change in Milk per CowYear-to-Year Change in Total Milk Produc-tion10-year Average Change in Cow Numbers10-year Change in Milk per Cow

Pe

rce

nt

4444

USDA Forecast 2007 production

9.13 mil. cows -- 0.2%20,250 lb. per cow -- 1.5%184.9 bil. lb. milk -- 1.7%

2007 prices, midpointAll Milk @ $19.30/cwt -- $6.40 from

2006 at $12.90/cwtClass III Milk @ $ 18.20/cwt -- $6.31

from 2006 at $11.89/cwtClass IV Milk @ $18.45/cwt -- $7.39

from 2006 at $11.06/cwt. !!!!

4545

USDA Forecast 2008 production

9.15 mil. cows -- 0.2%20,610 lb. per cow -- 1.8%188.6 bil. lb. milk -- 2.3%

2008 prices, midpointAll Milk @ $18.75/cwt -- $0.55 from

2007 Class III Milk @ $16.90/cwt -- $1.30

from 2007Class IV Milk @ $18.00/cwt -- $0.45

from 2007

46

Class III prices, $/100 lb.

46

47

US & FO5 Milk Prices, $/cwt.

Item 2002 2003 2004 2005 2006 2007F 2008P

US All Milk

12.14 12.52 16.04 15.15 12.90 19.30 18.00

US Class III Milk

10.42 11.42 15.39 14.05 11.89 18.20 16.00

FO 5Blend

13.24 13.55 17.01 16.23 13.99 20.50 19.50

MILC 1.21 1.09 0.22 0.04 0.60 0.01 0.0

4848

.

Dairy Farms and Cows, United States, 1997-2006

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Dai

ry F

arm

s

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

Co

ws,

'000

s

Farms Cows

10-yr decrease in farms = 39%

10-yr decrease in cows = 1.5%

4949

.

1-29 Cows

30-49 Cows

50-99 Cows

100-199 Cows

200-499 Cows

500+ Cows

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

US Dairy Farm Structure, 1997 & 2006

1997

2006

Herd Size

Fa

rms

5050

.Regional Changes in Milk Production and Population

-100%

-50%

0%

50%

100%

150%

200%

250%

No

rth

east

Lak

e S

tate

s

Co

rn B

elt

N. P

lain

s

S. P

lain

s

Ap

pal

ach

ia

So

uth

east

Del

ta

Mo

un

tain

Pac

ific

U.S

.

Milk, % Change ('89+'90) to ('05+'06)

Pop, % Change '90-'06

5151

Regional Per Capita Milk Production, lb. 2006

462

1,867

408

906

309184

111 100

1,334

961

607

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Nor

thea

st

Lake

Sta

tes

Cor

n B

elt

N. P

lain

s

S. P

lain

s

App

alac

hia

Sou

thea

st

Del

ta

Mou

ntai

n

Pac

ific

U.S

.

52

Causes of Structural Change Productivity (milk/cow) has grown at a faster rate

than the rate of growth in dairy product sales Pressure on milk prices and profit margins per cow

and per cwt. Milk price pressures plus advances in

mechanization create incentives and opportunities to increase herd size, both to achieve economies of size and to sustain family living standards

Declining farm numbers as smaller farms leave & survivors expand

Regional differences in dairy farming systems and input costs create differences in profitability

Production is increasing in the west, with other regions losing market share

5353

Regional Competitiveness The southern region is quite diverse

The average herd size in Florida is 825 cows, selling 13.5 million pounds of milk annually

The average herd size in Kentucky is 79, selling 1.0 million pounds of milk annually

90% or more of the herds in Florida, Georgia, and North Carolina are confinement operations

~95% of the herds in Louisiana and ~75% in Mississippi are pasture-based

Several states have organic herds and/or on-farm processing, some have neither

5454

Summary 2007 saw record high milk prices The dairy industry is still on the price

rollercoaster – will it be a crash landing or will export markets continue to support prices?

Outlook is for continued growth in total US milk production and lower milk prices

Production costs have increased and will stay at higher levelsHigher corn and other feed pricesHigher energy pricesHigher fertilizer costs

5555

Summary Projections are for higher net incomes in

2007 because higher milk prices more than offset increases in production costs

Net income will be lower in 2008 Structural change will continue Regional competitiveness determines the

market share of the national milk production “pie”

Dairy diversity means at least some farms in a state and region are competitive

56

Implications The future will look a lot like the past Price volatility is not the cause of structural

change and there are strategies for managing around these price swings

National policies are unlikely to help but some states have provided subsidies

Some southeastern dairy producers are competitive but many will need to become more focused on profitability -- Many farmers do not know their cost of production, financial performance and financial status. Infrastructure is a concern

Is there more the LGUs can & should do?

57

Geoff Benson

Phone: 919.515.5184 Fax: 919.515.6268 E-mail:

[email protected] Web page: http://www.ag-econ.ncsu.edu/

faculty/benson/benson.html

57