Customer Life Cycle and Risk into one Department

20

Converging Customer Life Cycle Risks Into a Single Department Javier Mendez-Castillero Risk Management Director October 17 2011

-

Upload

javier-mendez-mba -

Category

Documents

-

view

13 -

download

0

Transcript of Customer Life Cycle and Risk into one Department

Converging Customer Life Cycle Risks Into a Single Department

Javier Mendez-Castillero Risk Management Director

October 17 2011

Agenda � The true meaning of synergies and

efficiency in risk management

� From sales to collections, holistic risk management solutions

� Using analytics to predict customer behavior and mitigate exposure to risk

� Using risk management to influence and increase EBITDA

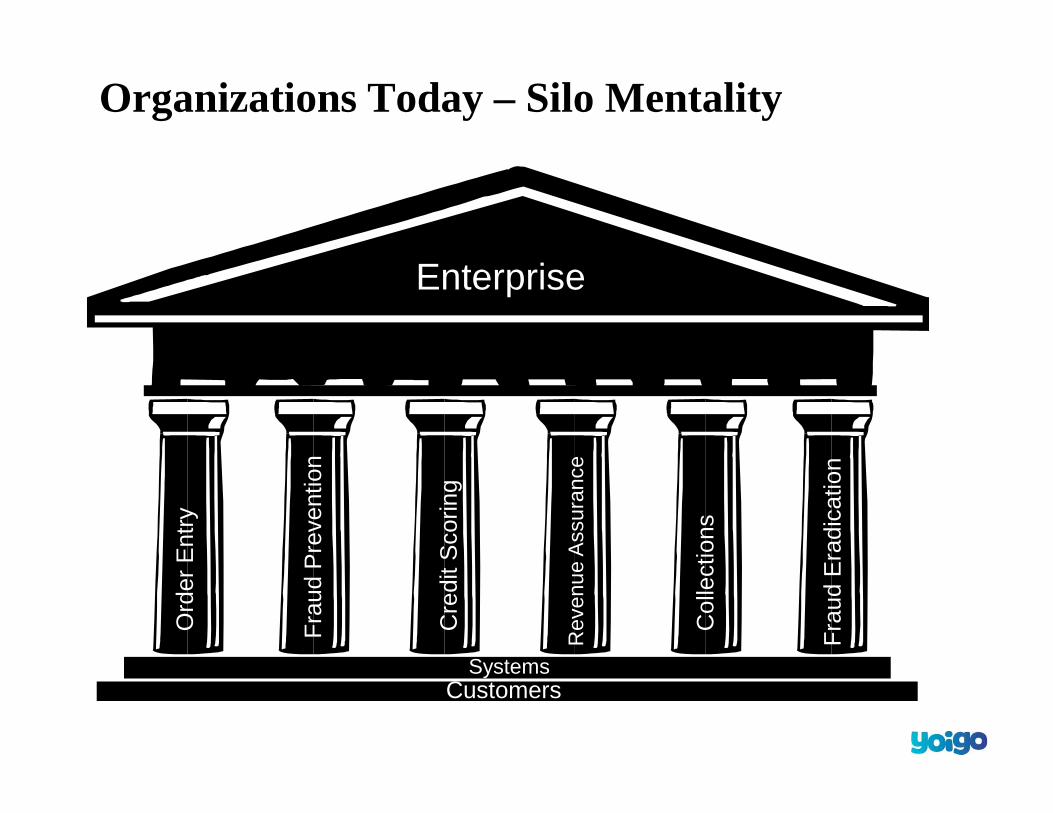

Organizations Today – Silo Mentality

Customers

Ord

er E

ntry

Fra

ud P

reve

ntio

n

Cre

dit S

corin

g

Rev

enue

Ass

uran

ce

Col

lect

ions

Fra

ud E

radi

catio

n

Systems

Enterprise

Why Converging into a Single Entity?

• Many hands into one head creates fast decisions and single coordination of efforts

• Revenue loses, missed cash opportunities and unnecessary cost are all paid by the company after all.

• Single objective of the company � Get profitable customers. Only achieved if we create the correct environment for team work and eliminated duplicity of efforts.

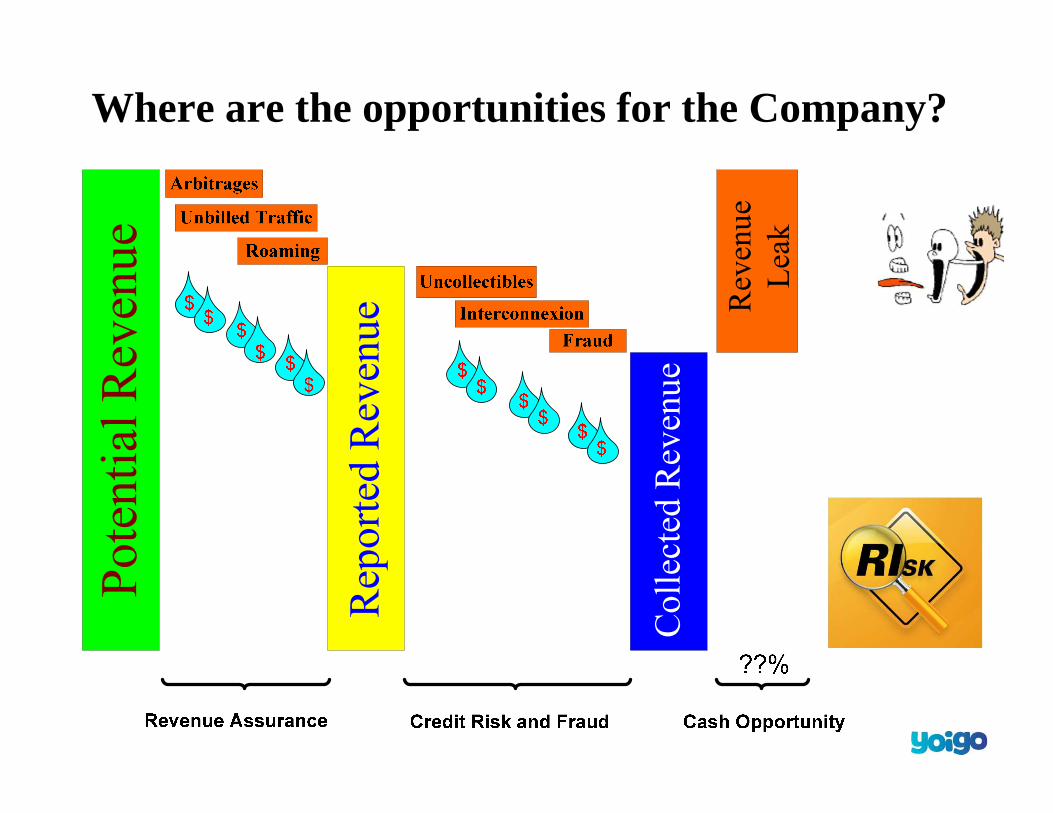

Where are the opportunities for the Company?

Reported Revenue

Collected Revenue

Revenue

Leak

Where is the Risk in Telcos?

• When something goes wrong, most likely will end up in Bad Debt Expense

• Fraud losses (bad debt mostly) is a direct consequence of credit risk policy

• The key is to find the balance in accepting the most customers with the minimun risk and have enough controls to minimize errors in operations

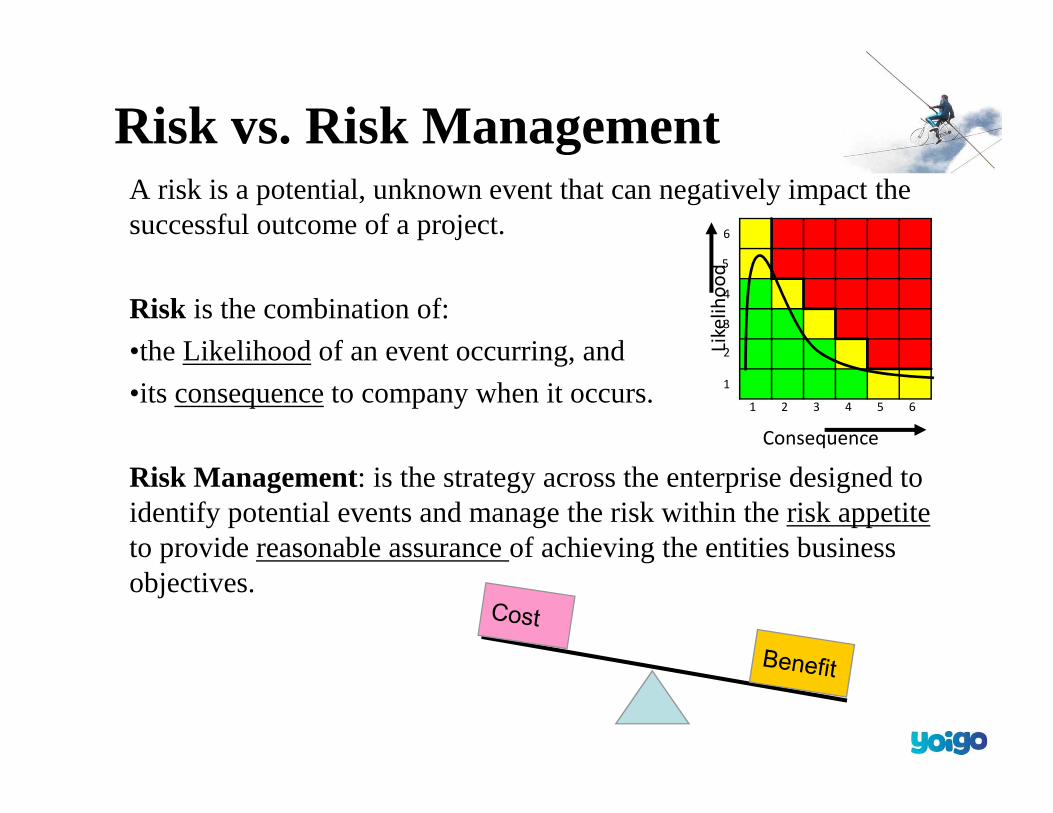

Risk vs. Risk Management A risk is a potential, unknown event that can negatively impact the successful outcome of a project.

Risk is the combination of:

•the Likelihood of an event occurring, and

•its consequence to company when it occurs.

Risk Management: is the strategy across the enterprise designed to identify potential events and manage the risk within the risk appetite to provide reasonable assurance of achieving the entities business objectives.

Consequence

Like

lih

oo

d

6 5 4 3 2 1

1

2

3

4

6

5

Consequence

Like

liho

od

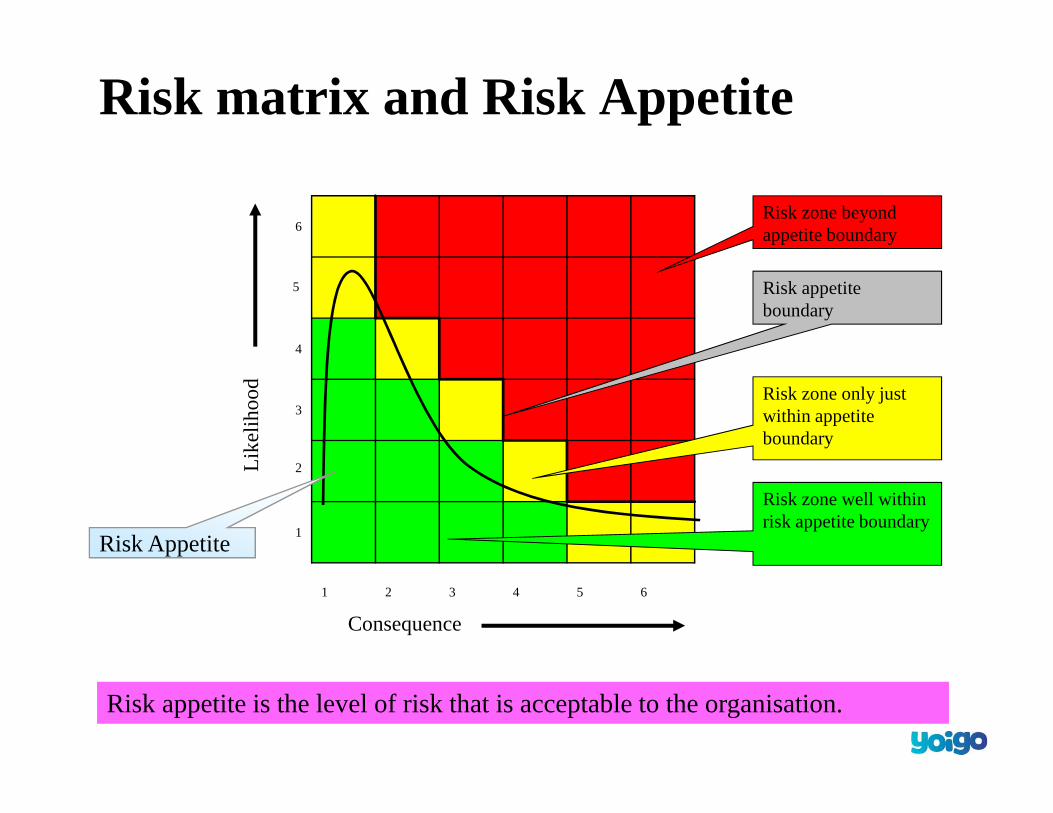

Risk matrix and Risk Appetite

6 5 4 3 2 1

1

2

3

4

6

5

Risk zone beyond appetite boundary

Risk appetite boundary

Risk zone only just within appetite boundary

Risk zone well within risk appetite boundary

Risk Appetite

Risk appetite is the level of risk that is acceptable to the organisation.

Why Risk Managements Should be Holistic?

• Identify risks that reduces revenue

• Determine likelihood and consequence

• Adapt the risk to the company appetite

• Propose actions to treat the risk • Avoid or Eliminate

• Reduce or Mitigate

• Transfer or Insure it

• Retain or accept it

• Communicate decision plan

• Monitor and review periodically

From Theory to Practice

Risk Management Controls Map in Yoigo

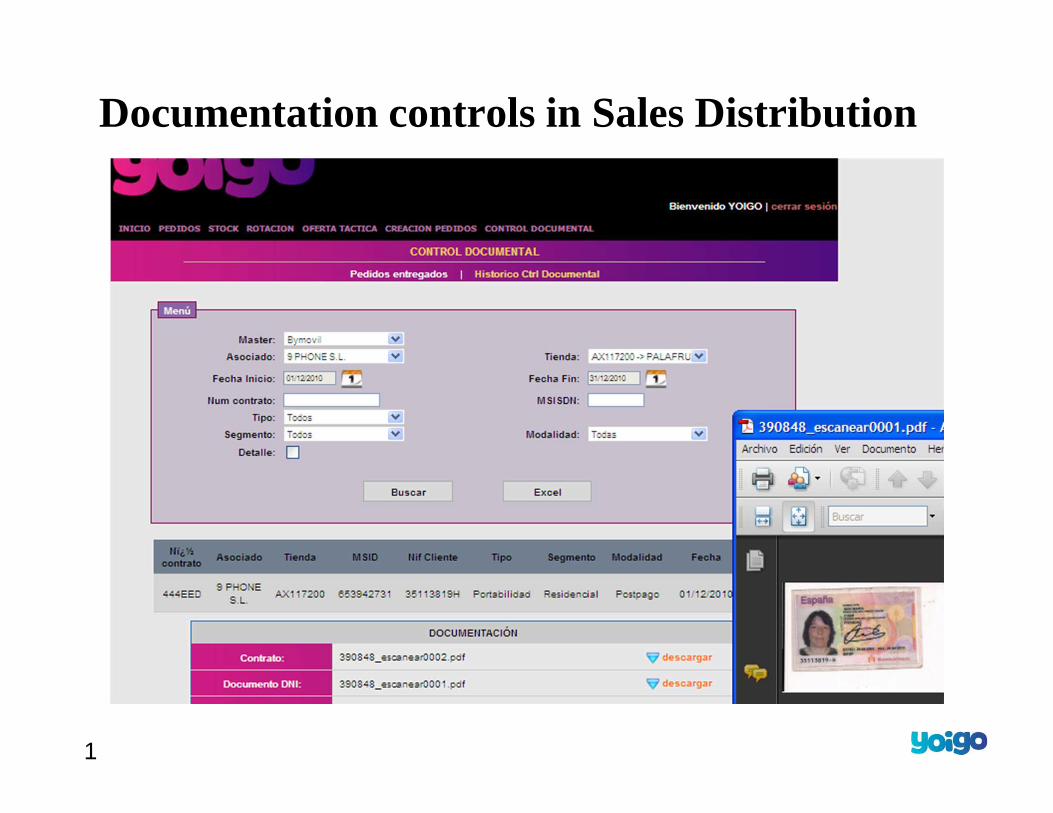

Risk Mgmt. Controls in Yoigo Preventive Controls: 1. Documentation Control at point of sale

2. Customer data capturing normalization

3. Subscription limit per customer

4. Payment behavior for add-on customers

5. Deny list for known fraud cases

6. Credit scoring for new customers

7. Subscription redundancy verification

8. Sales monitoring of high risk products

9. Verification of bank account veracity

10. Logistics verification check for On-line orders

11. Communication with sales channel

12. HUR reports

13. Traffic Counters

14. Roaming fraud tool

15. Forensic Analysis

16. Payment Behavior Smart Collection Strategies

Documentation controls in Sales Distribution

1

Credit Modeling: Predicting Customer Behavior

• Modeled data from Yoigo customer to better predict behavior

• Negative credit bureau to look for know debtors

• Yoigo business rules to adapt to market and strategies and produce best scoring outcome

29,

0%30

,2%

29,

6%28

,2%

31,

1%

29,

2%25

,9%

25,

0%24,

8%25

,6%

26,

1%24

,2%

21,8

%21,

1%23

,3%

26,8

%27

,7%

26,

4%23,

3%32

,3%

39,5

%36,

4%26,

4%22,

4%23

,6% 27

,8%

29,4

%28

,8%

26,7

%30,

3% 34,6

%35

,5%

34,3

%

14%

16%

18%

20%

22%

24%

26%

28%

30%

32%

34%

36%

38%

40%

en

e-0

9fe

b-0

9m

ar-

09

abr-

09

may-0

9ju

n-0

9ju

l-09

ag

o-0

9sep

-09

oct-

09

no

v-0

9d

ic-0

9Jan

-10

feb-1

0m

ar-

10

abr-

10

may-1

0ju

n-1

0ju

l-10

ag

o-1

0sep

-10

oct-

10

no

v-1

0d

ic-1

0en

e-1

1fe

b-1

1m

ar-

11

abr-

11

may-1

1ju

n-1

1ju

l-11

ag

o-1

1sep

-11

oct-

11

no

v-1

1d

ic-1

1

Monthly Credit Rejection Rate3%

4%

3%

3%

2%

2%

3%

2%

1%

2%

2%

0%

2%

2%

2%

1%

1%

1%

2%

2%

0%

0%

0%

0%

0%

0%

0%

2%

1%

1%

40%

39%

40%

35%

32%

36%

38%

37%

41%

39%

36%

36%

28%

28%

28%

26%

26%

25%

23%

26%

25%

24%

26%

27%

25%

26%

25%

25%

26%

25%

20%

22%

21%

22%

17%

24%

23%

25%

24%

25%

27%

15%

15%

18%

17%

17%

16%

17%

13%

16%

17%

17%

15%

18%

15%

14%

15%

17%

17%

16%

0,00

%

0,08

%

0,00

%

0,00

%

0,00

%

0,18

%

0,17

%

0,00

%

0,00

%

0,10

%

0,18

%

0,00

%

0,00

%

0,13

%

0,07

%

0,00

%

0,00

%

0,26

%

0,00

%

0,00

%

0,14

%

0,07

%

0,00

%

0,00

%

0,14

%

0,00

%

0,00

%

0,00

%

0,00

%

0,07

%

36%

35%

36%

39%

48%

39%

36%

36%

33%

33%

35%

50%

55%

53%

53%

55%

57%

57%

62%

57%

56%

57%

57%

53%

57%

59%

58%

56%

55%

58%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Experian Rejection Reasons Scoring N. Riesgo B. Otro B. Telco Lista negra

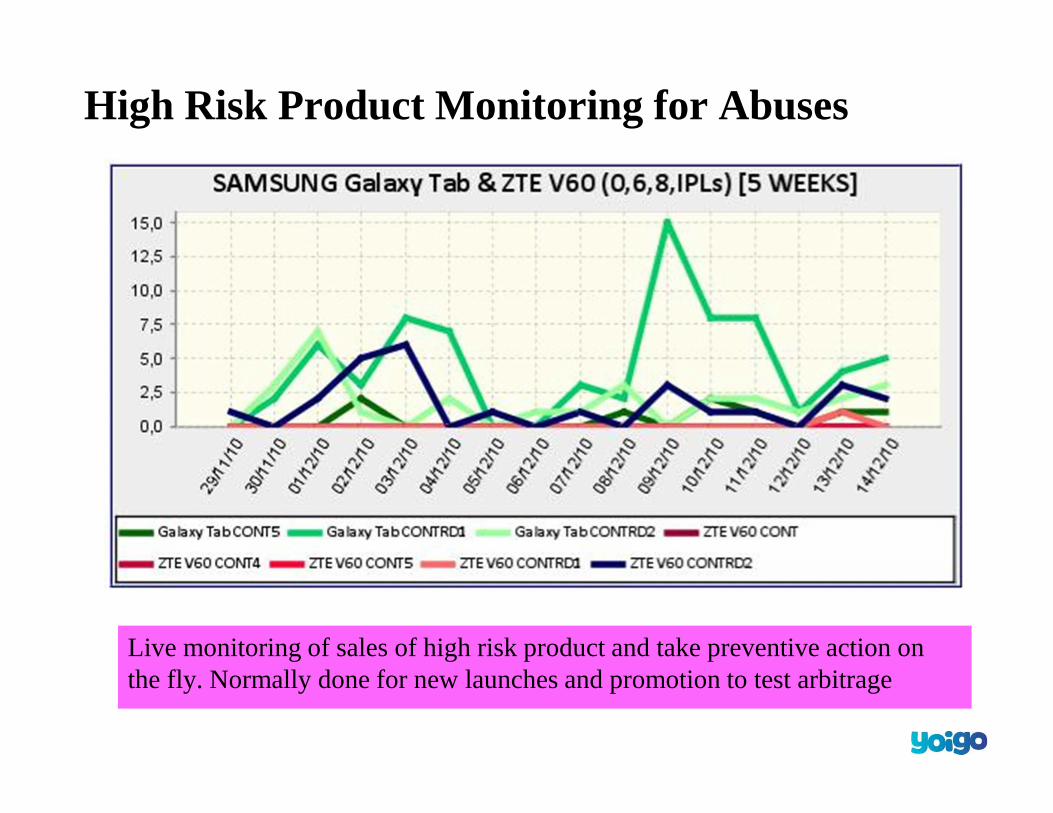

High Risk Product Monitoring for Abuses

Live monitoring of sales of high risk product and take preventive action on the fly. Normally done for new launches and promotion to test arbitrage

Manage exposure risk with credit limit counters

Three different counters (based on money spent) – Premium Numbers (Voice, SMS y WAP)

– Roaming and International calls

– Total consumption

Two-step approach. Warning SMS and Barring – Premium 50 - 70€ (Barring Premium)

– International 50 - 70€ (Barring Intl. and Roaming)

– Total Charge 80 - 120€ (Barring outgoing calls)

International NRTRDE traffic counter – All countries grouped in 3 risk categories lists

– Counter base on number of MTC

– Counter base on rated amount of MTC

Intelligent preventing barring: Only calls allowed to visited country and home country

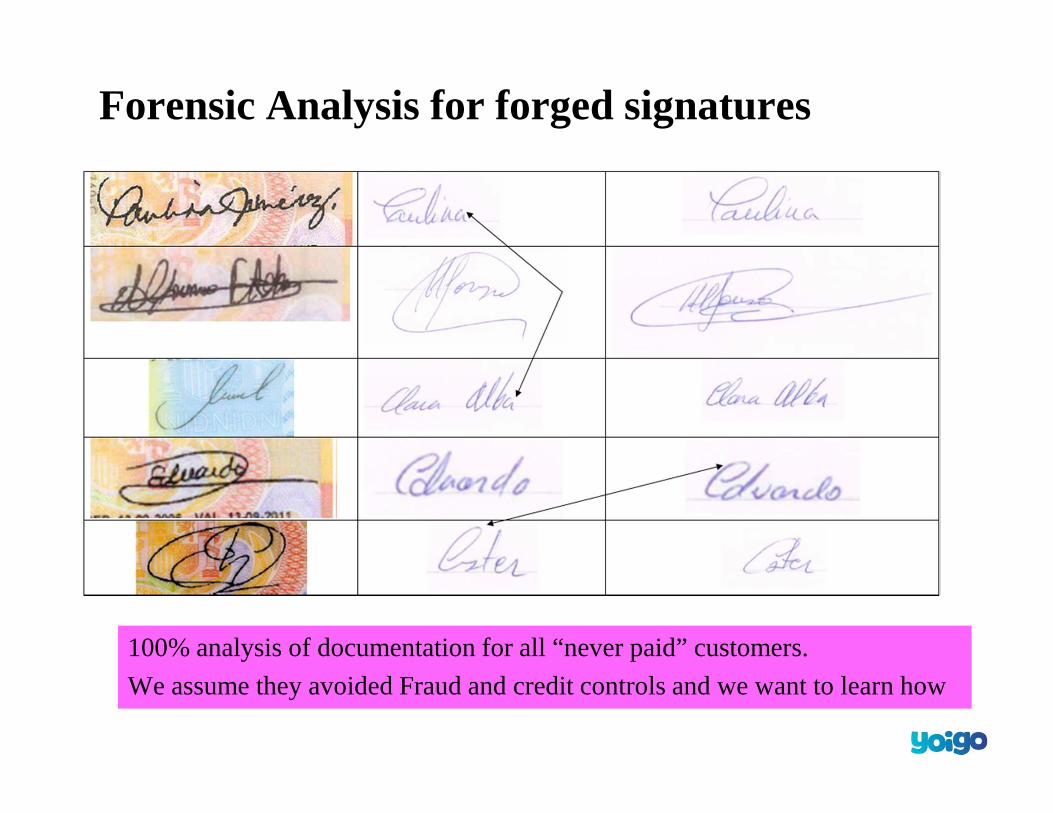

Forensic Analysis for forged signatures

100% analysis of documentation for all “never paid” customers.

We assume they avoided Fraud and credit controls and we want to learn how

Payment Behavior Smart Collection Strategy

Dunning strategy based on customer payment behavior

– Hot-lining to recurring debtors

– Payment promises to unemployed

– Pre due-date SMS to new customers

– Blaster message to procrastinators

– Intelligent IVR based on segmentation

Results: – 70% of collection is done with no

human intervention

– IVR account for 60% of payments

– Reduced cost of collection to 10%

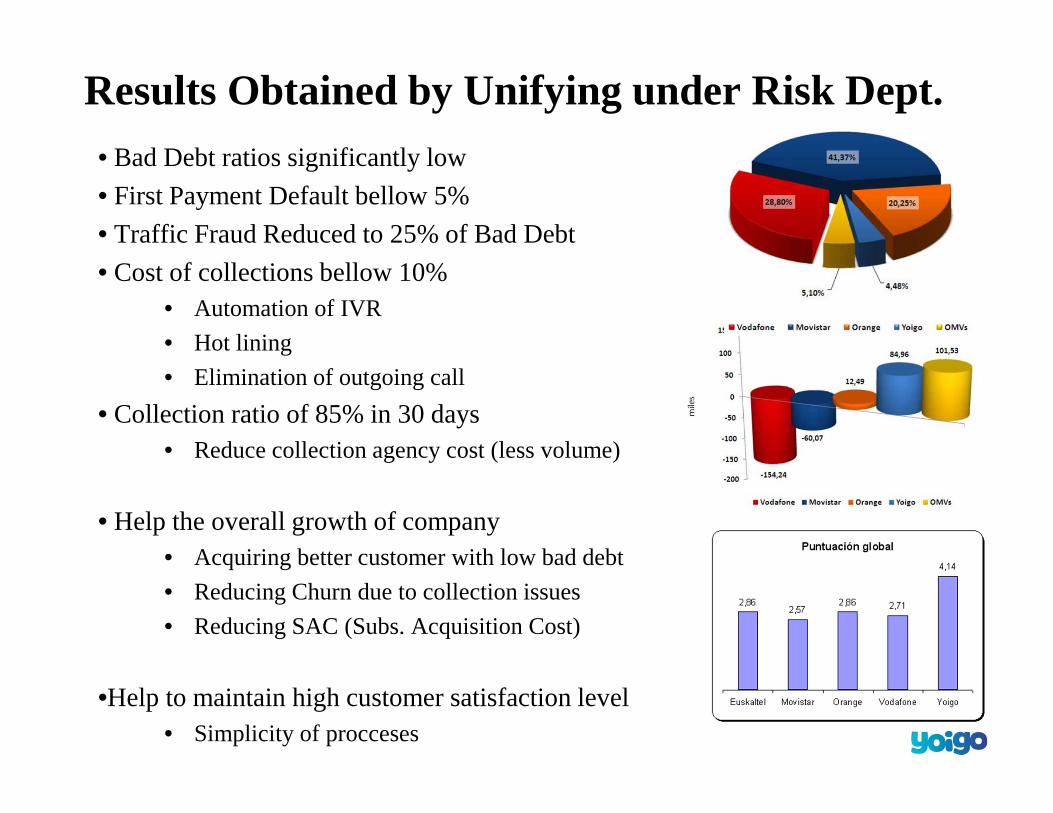

Results Obtained by Unifying under Risk Dept.

• Bad Debt ratios significantly low

• First Payment Default bellow 5%

• Traffic Fraud Reduced to 25% of Bad Debt

• Cost of collections bellow 10% • Automation of IVR

• Hot lining

• Elimination of outgoing call

• Collection ratio of 85% in 30 days • Reduce collection agency cost (less volume)

• Help the overall growth of company • Acquiring better customer with low bad debt

• Reducing Churn due to collection issues

• Reducing SAC (Subs. Acquisition Cost)

•Help to maintain high customer satisfaction level • Simplicity of procceses