Credit suisse industrials conference 12 1-2016-vff

26

The Manitowoc Company, Inc. CREDIT SUISSE 4 TH ANNUAL INDUSTRIALS CONFERENCE MANALAPAN, FL DECEMBER 1, 2016

-

Upload

manitowoccompany -

Category

Investor Relations

-

view

319 -

download

1

Transcript of Credit suisse industrials conference 12 1-2016-vff

The Manitowoc Company, Inc.

CREDIT SUISSE 4TH ANNUAL INDUSTRIALS CONFERENCE

MANALAPAN, FL DECEMBER 1, 2016

2

Safe Harbor Statement

Any statements contained in this presentation that are not historical facts are “forward-looking statements.” These statements are based on the current expectations of the management of the company, only speak as of the date on which they are made, and are subject to uncertainty and changes in circumstances. We undertake no obligation to update or revise forward-looking statements, whether as a result of new information, future events, or otherwise. Forward-looking statements include, without limitation, statements typically containing words such as “intends,” “expects,” “anticipates,” “targets,” “estimates,” and words of similar import. By their nature, forward-looking statements are not guarantees of future performance or results and involve risks and uncertainties because they relate to events and depend on circumstances that will occur in the future.

There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by such forward-looking statements. These factors include, but are not limited to, those relating to revenue growth of the company, future market strength of the company’s business segments and products, market acceptance of existing products and new product introductions and technology, economic conditions, successful acquisitions, manufacturing and facility utilization efficiencies, risks relating to actions of activist shareholders, and other factors listed in the company’s preliminary offering circular with respect to the notes, dated May 5, 2016. Any “forward-looking statements” in this presentation are intended to qualify for the safe harbor from liability under the Private Securities Litigation Reform Act of 1995.

3

Agenda

Building Something Real

Manitowoc Transformation

of Company

Execution of

Plan

Future Growth

Opportunities

4

Agenda

Building Something Real

Manitowoc Transformation

of Company

Execution of

Plan

Future Growth

Opportunities

5

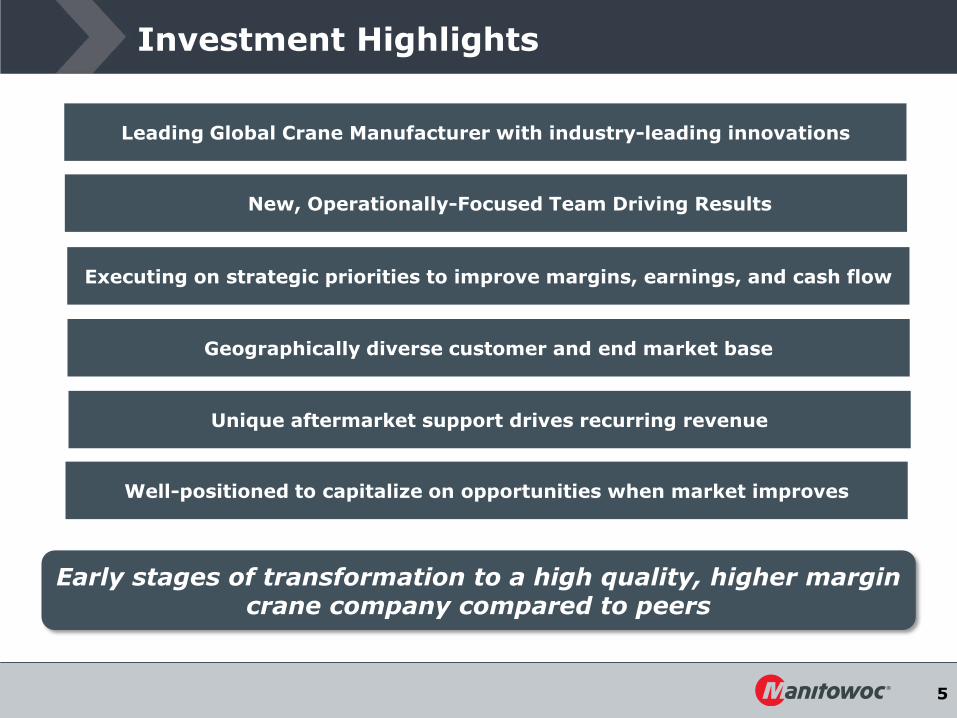

Investment Highlights

Leading Global Crane Manufacturer with industry-leading innovations

Well-positioned to capitalize on opportunities when market improves

Unique aftermarket support drives recurring revenue

Geographically diverse customer and end market base

Executing on strategic priorities to improve margins, earnings, and cash flow

New, Operationally-Focused Team Driving Results

Early stages of transformation to a high quality, higher margin crane company compared to peers

6

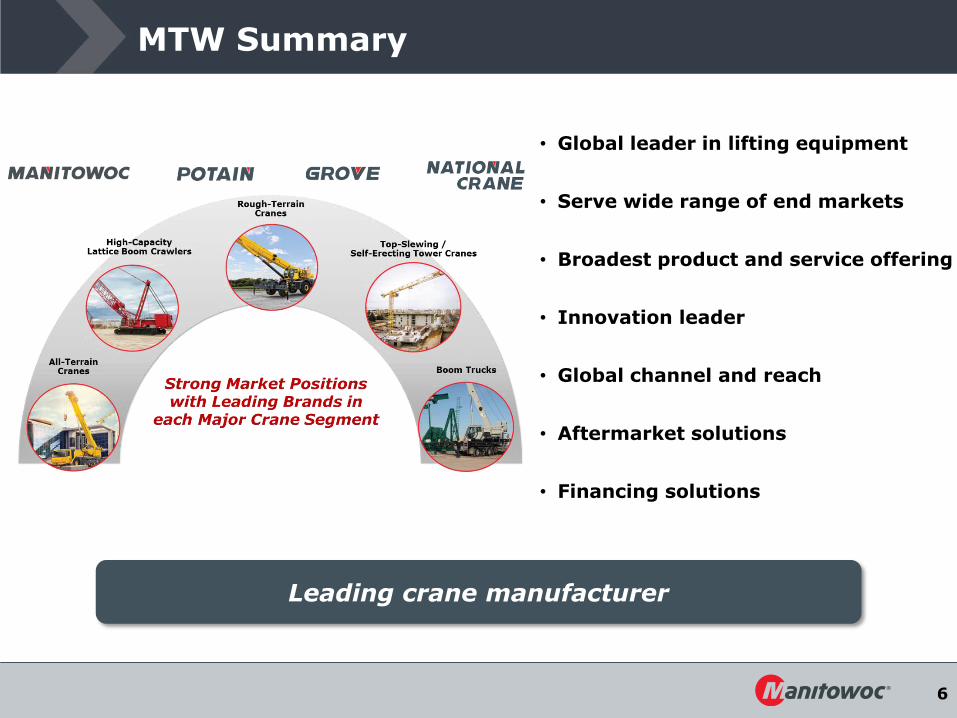

MTW Summary

• Global leader in lifting equipment

• Serve wide range of end markets

• Broadest product and service offering

• Innovation leader

• Global channel and reach

• Aftermarket solutions

• Financing solutions

Leading crane manufacturer

7

Manitowoc Transformation

of Company

Execution of

Plan

Future Growth

Opportunities

Building Something Real

8

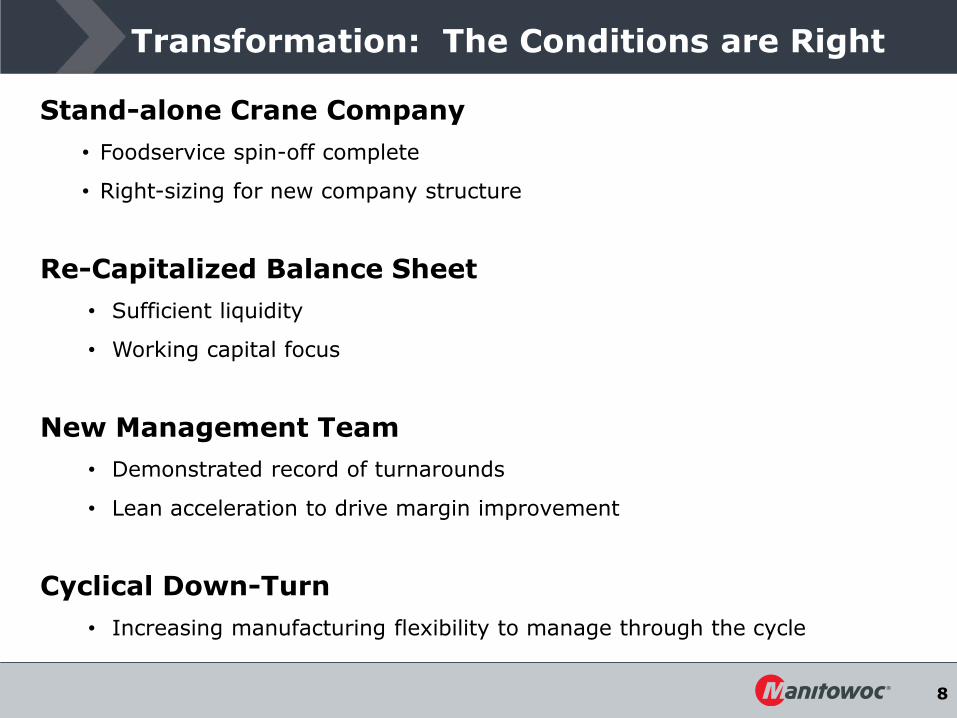

Transformation: The Conditions are Right

Stand-alone Crane Company

• Foodservice spin-off complete

• Right-sizing for new company structure

Re-Capitalized Balance Sheet

• Sufficient liquidity

• Working capital focus

New Management Team

• Demonstrated record of turnarounds

• Lean acceleration to drive margin improvement

Cyclical Down-Turn

• Increasing manufacturing flexibility to manage through the cycle

10

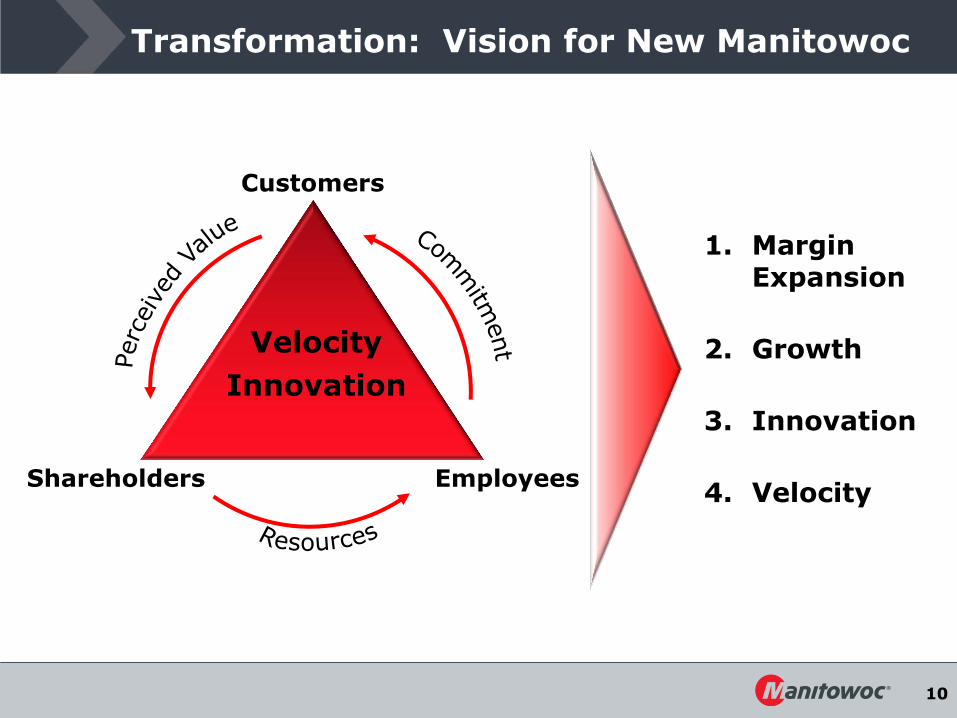

Transformation: Vision for New Manitowoc

Customers

Shareholders Employees

Velocity

Innovation

1. Margin Expansion

2. Growth

3. Innovation

4. Velocity

11

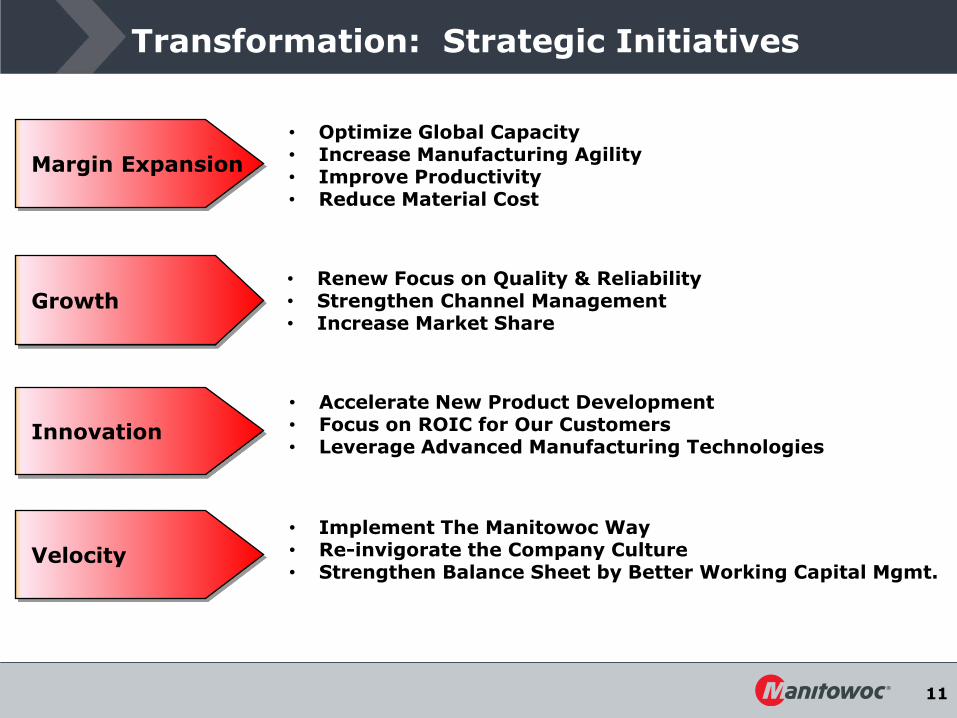

Transformation: Strategic Initiatives

• Renew Focus on Quality & Reliability • Strengthen Channel Management • Increase Market Share

• Optimize Global Capacity • Increase Manufacturing Agility • Improve Productivity • Reduce Material Cost

• Accelerate New Product Development • Focus on ROIC for Our Customers • Leverage Advanced Manufacturing Technologies

Margin Expansion

Growth

Innovation

Velocity

• Implement The Manitowoc Way • Re-invigorate the Company Culture • Strengthen Balance Sheet by Better Working Capital Mgmt.

12

Manitowoc Transformation

of Company

Execution of

Plan

Future Growth

Opportunities

Building Something Real

13

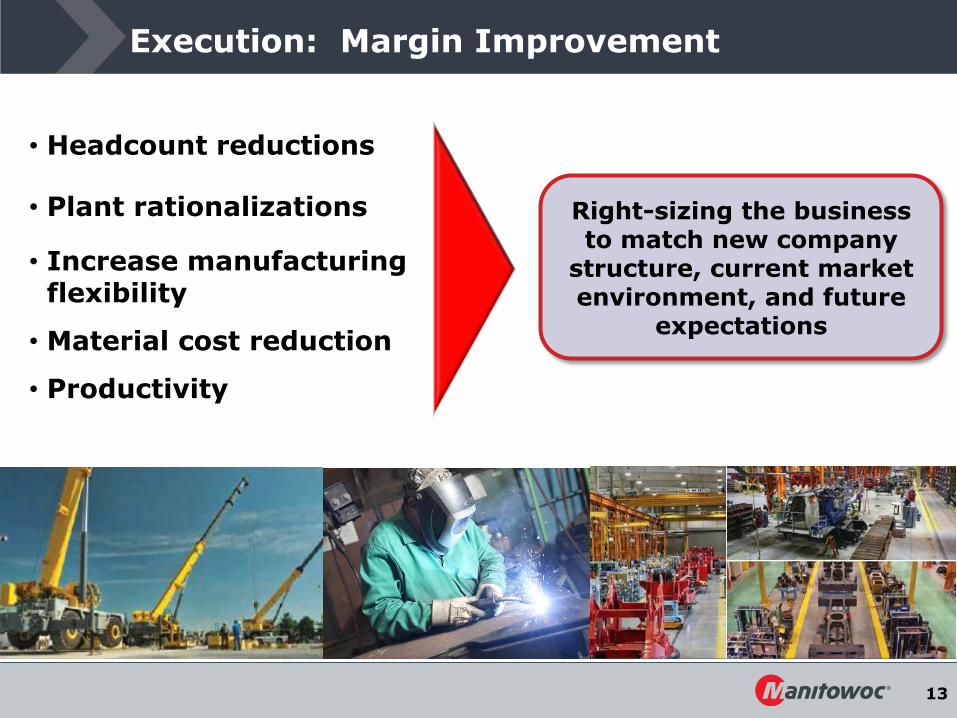

Execution: Margin Improvement

• Headcount reductions

• Plant rationalizations

• Increase manufacturing flexibility

• Material cost reduction

• Productivity

Right-sizing the business to match new company

structure, current market environment, and future

expectations

14

Execution: Growth

• Improved quality & reliability

• Strengthen dealer engagement

• Sales excellence & training

Improving competitive position to re-gain

market share

15

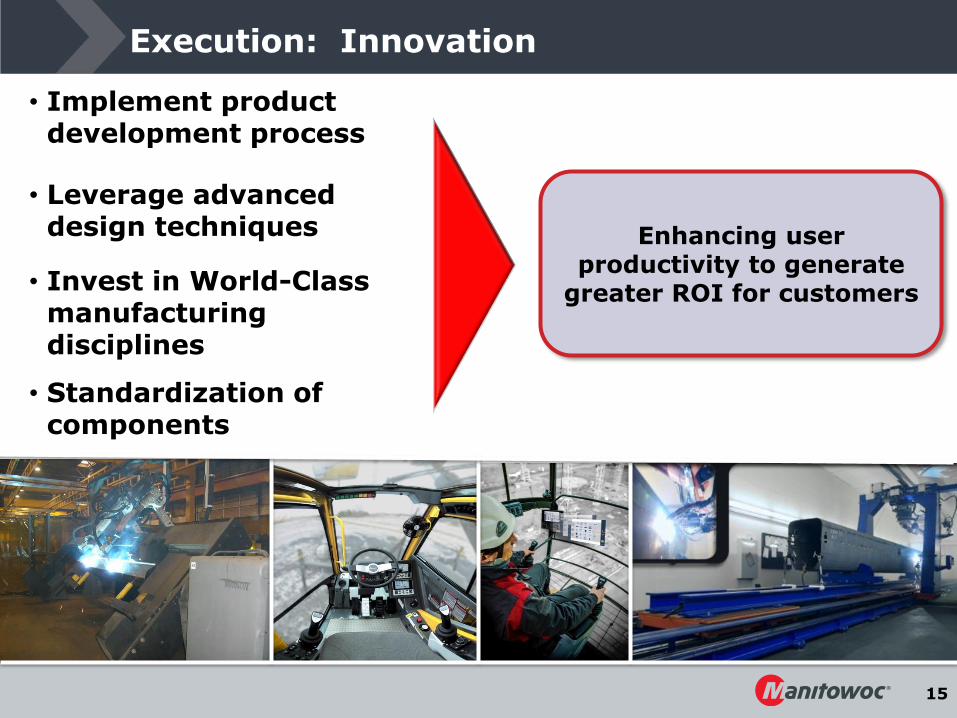

Execution: Innovation

• Implement product development process

• Leverage advanced design techniques

• Invest in World-Class manufacturing disciplines

• Standardization of components

Enhancing user productivity to generate

greater ROI for customers

16

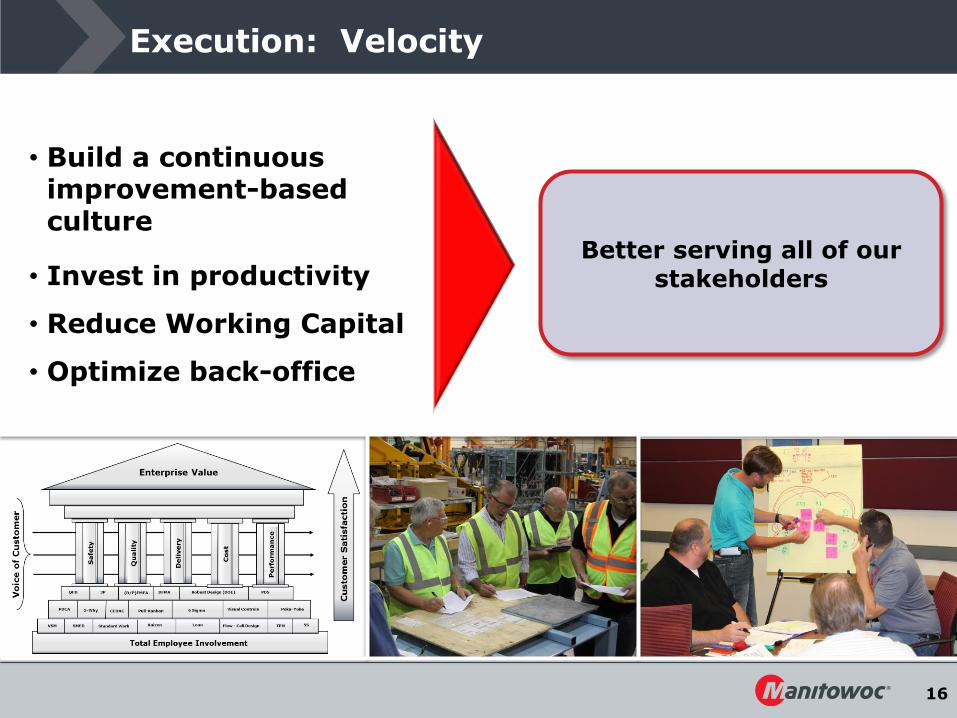

Execution: Velocity

• Build a continuous improvement-based culture

• Invest in productivity

• Reduce Working Capital

• Optimize back-office

Better serving all of our stakeholders

17

Manitowoc Transformation

of Company

Execution of

Plan

Future Growth

Opportunities

Building Something Real

18

Future Growth Opportunities

• Customer Engagement

• Innovation

• External Growth

• Manufacturing Technology

• People Development

• Utilize Balance Sheet

Increasing ROIC for All Stakeholders

19

Additional Materials and Financials

20

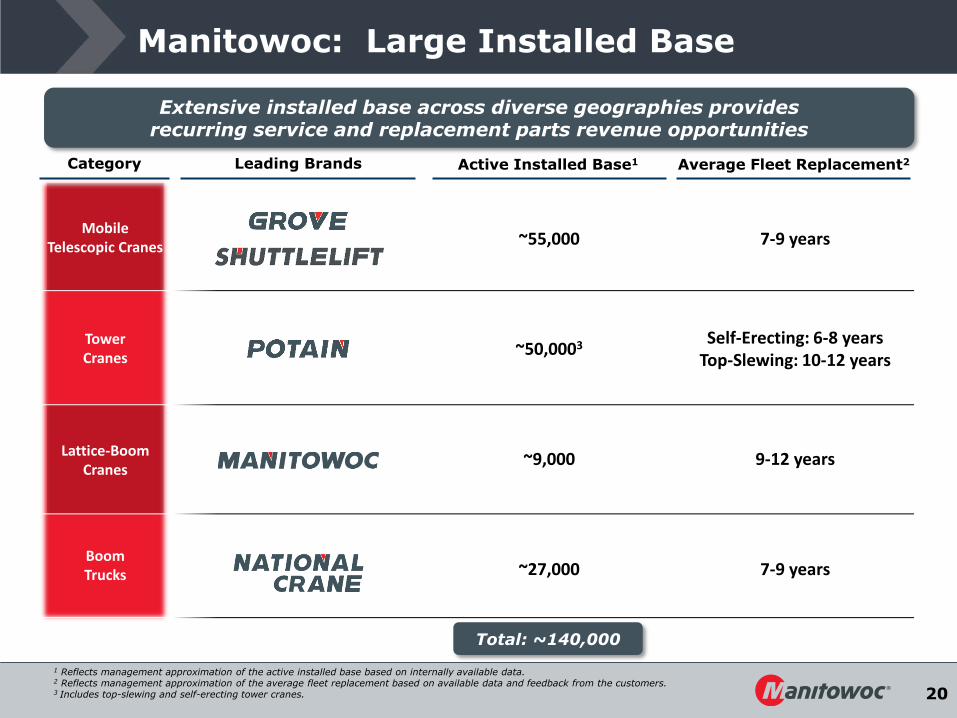

Manitowoc: Large Installed Base

~55,000 7-9 years

~50,0003 Self-Erecting: 6-8 years Top-Slewing: 10-12 years

~9,000 9-12 years

~27,000 7-9 years

Mobile Telescopic Cranes

Tower Cranes

Lattice-Boom Cranes

Boom Trucks

Leading Brands Active Installed Base1 Category

Extensive installed base across diverse geographies provides recurring service and replacement parts revenue opportunities

1 Reflects management approximation of the active installed base based on internally available data. 2 Reflects management approximation of the average fleet replacement based on available data and feedback from the customers. 3 Includes top-slewing and self-erecting tower cranes.

Average Fleet Replacement2

Total: ~140,000

21

Diversified by Region, End Market and Product

Key Brands

2015 Geographic Exposure

2015 End Market Exposure1

2016 YTD Revenue by Product3

Americas52%

APAC12%

EMEA36%

1 Includes new equipment sales only. 2 Represents 2015 gross sales. Includes new equipment sales only. Government sales do not reflect our recent $192 million contract with the U.S. Army which will impact revenue over the next several years. 3 Crane Products includes new equipment sales only.

Balanced Sales Footprint and Customer Segments We Serve

2015 Overall Customer Mix2

Industrial / Petrochemical

35%

Power / Utilities18%

Commercial25%

Residential5%

Infrastructure17%

Contractor13%

Dealer66%

Gov't0.2%

Other4%

Rental17%

Crane Care 17%

Crane Products 83%

22

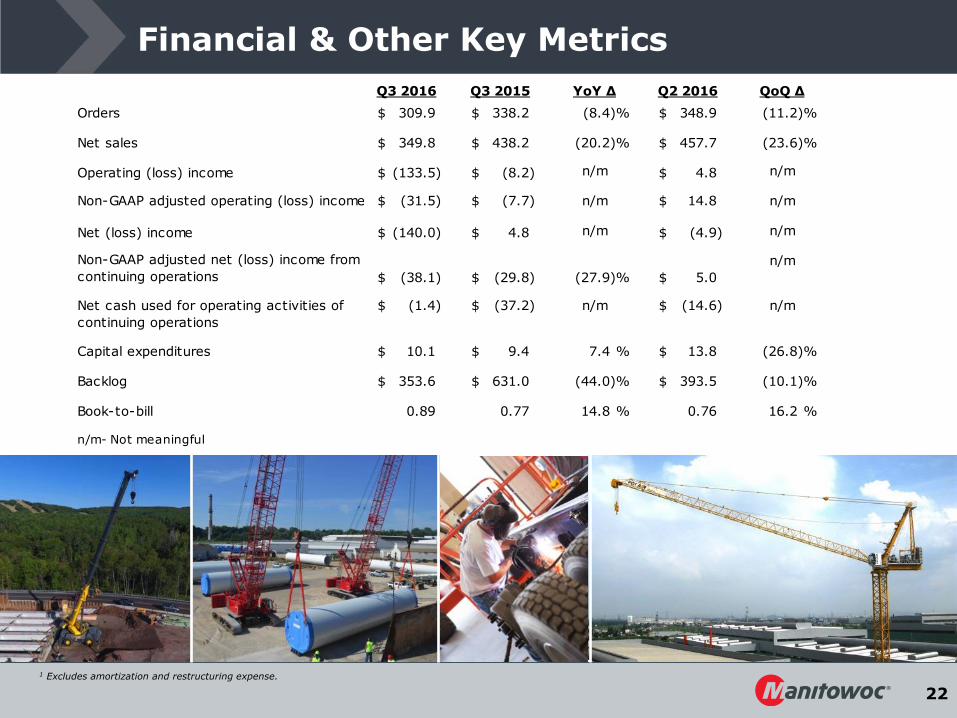

Q3 2016 Q3 2015 YoY ∆ Q2 2016 QoQ ∆

Orders 309.9$ 338.2$ (8.4)% 348.9$ (11.2)%

Net sales 349.8$ 438.2$ (20.2)% 457.7$ (23.6)%

Operating (loss) income (133.5)$ (8.2)$ n/m 4.8$ n/m

Non-GAAP adjusted operating (loss) income (31.5)$ (7.7)$ n/m 14.8$ n/m

Net (loss) income (140.0)$ 4.8$ n/m (4.9)$ n/m

Non-GAAP adjusted net (loss) income from

continuing operations (38.1)$ (29.8)$ (27.9)% 5.0$

n/m

Net cash used for operating activities of

continuing operations

(1.4)$ (37.2)$ n/m (14.6)$ n/m

Capital expenditures 10.1$ 9.4$ 7.4 % 13.8$ (26.8)%

Backlog 353.6$ 631.0$ (44.0)% 393.5$ (10.1)%

Book-to-bill 0.89 0.77 14.8 % 0.76 16.2 %

n/m- Not meaningful

Financial & Other Key Metrics

1 Excludes amortization and restructuring expense.

23

GAAP Reconciliation Summary

24

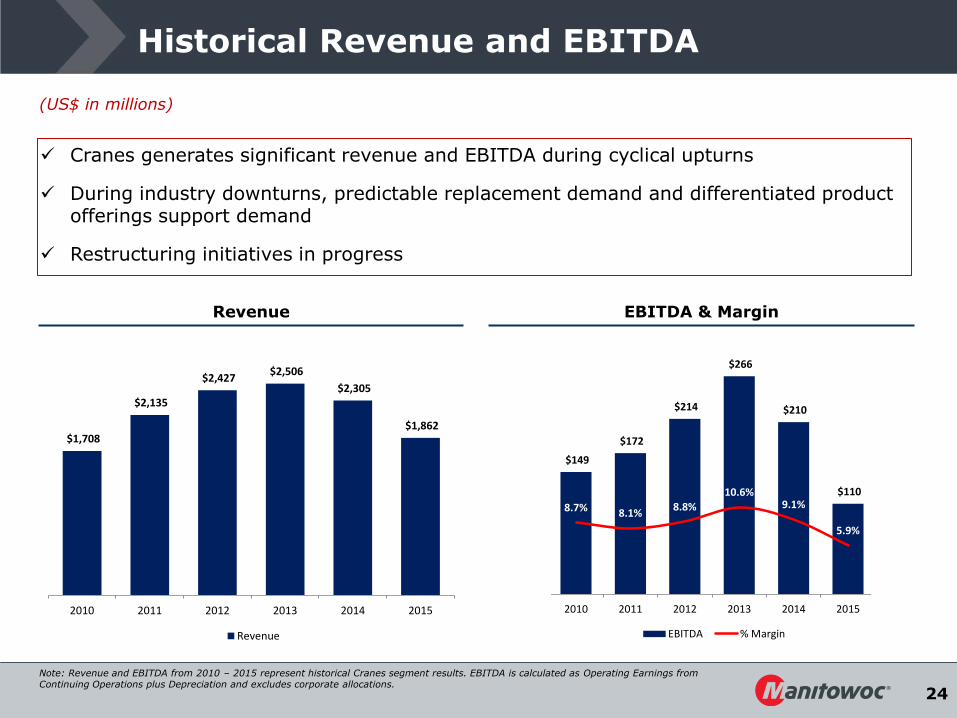

Historical Revenue and EBITDA

(US$ in millions)

Revenue EBITDA & Margin

Cranes generates significant revenue and EBITDA during cyclical upturns

During industry downturns, predictable replacement demand and differentiated product offerings support demand

Restructuring initiatives in progress

$1,708

$2,135

$2,427 $2,506

$2,305

$1,862

2010 2011 2012 2013 2014 2015

Revenue

$149

$172

$214

$266

$210

$110

8.7% 8.1%8.8%

10.6%9.1%

5.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

$-

$50

$100

$150

$200

$250

$300

2010 2011 2012 2013 2014 2015

EBITDA % Margin

Note: Revenue and EBITDA from 2010 – 2015 represent historical Cranes segment results. EBITDA is calculated as Operating Earnings from Continuing Operations plus Depreciation and excludes corporate allocations.

25

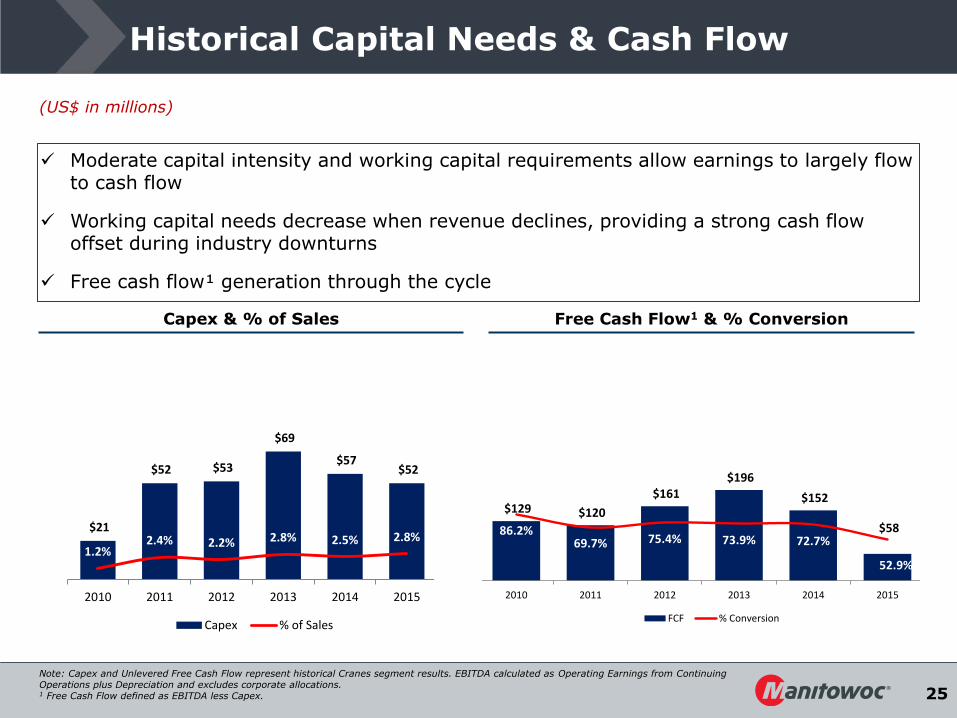

Historical Capital Needs & Cash Flow

(US$ in millions)

Capex & % of Sales

Note: Capex and Unlevered Free Cash Flow represent historical Cranes segment results. EBITDA calculated as Operating Earnings from Continuing Operations plus Depreciation and excludes corporate allocations. 1 Free Cash Flow defined as EBITDA less Capex.

Free Cash Flow1 & % Conversion

Moderate capital intensity and working capital requirements allow earnings to largely flow to cash flow

Working capital needs decrease when revenue declines, providing a strong cash flow offset during industry downturns

Free cash flow¹ generation through the cycle

$21

$52 $53

$69

$57 $52

1.2%2.4% 2.2% 2.8% 2.5% 2.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

$-

$20

$40

$60

$80

$100

$120

$140

2010 2011 2012 2013 2014 2015

Capex % of Sales

$129 $120

$161 $196

$152

$58 86.2%69.7% 75.4% 73.9% 72.7%

52.9%0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

0

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 2014 2015

FCF % Conversion

26

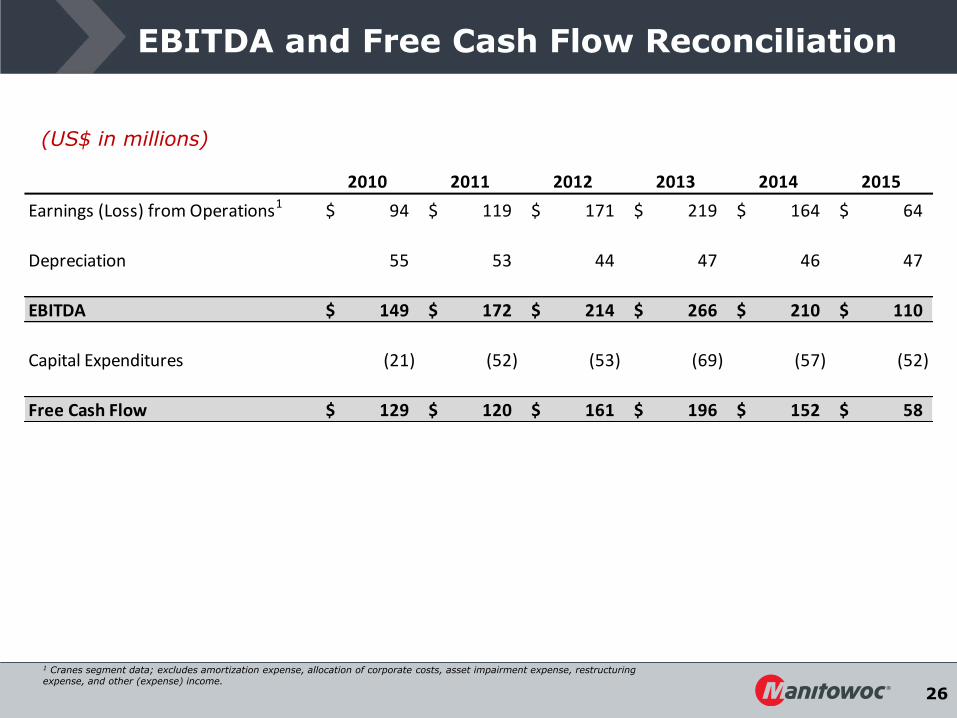

EBITDA and Free Cash Flow Reconciliation

(US$ in millions)

2010 2011 2012 2013 2014 2015

Earnings (Loss) from Operations1 94$ 119$ 171$ 219$ 164$ 64$

Depreciation 55 53 44 47 46 47

EBITDA 149$ 172$ 214$ 266$ 210$ 110$

Capital Expenditures (21) (52) (53) (69) (57) (52)

Free Cash Flow 129$ 120$ 161$ 196$ 152$ 58$

1 Cranes segment data; excludes amortization expense, allocation of corporate costs, asset impairment expense, restructuring expense, and other (expense) income.

27