Cracking the Code: UCC Article 4A & the ACH Network

36

THE PAYMENTS INSTITUTE — July 16-19, 2017 Emory Conference Center Hotel, Emory University, Atlanta, Georgia Cracking the Code: UCC Article 4A & the ACH Network Presented by: PAUL A. CARRUBBA Adams and Reese LLP Phone: (601) 292-0788 E-Mail: [email protected]

Transcript of Cracking the Code: UCC Article 4A & the ACH Network

THE PAYMENTS INSTITUTE — July 16-19, 2017

Emory Conference Center Hotel, Emory University, Atlanta, Georgia

Cracking the Code:

UCC Article 4A & the

ACH Network

Presented by:

PAUL A. CARRUBBA

Adams and Reese LLP

Phone: (601) 292-0788

E-Mail: [email protected]

Paul Carrubba

Paul is Of Counsel in the law firm of Adams and Reese LLP.

His primary focus is on Banking Law and legal issues dealing

with payments system laws and regulations and bank

operations issues. He has over 45 years of experience in the

banking industry as a Bank Operations Manager, a

consultant, an author, and an attorney. Mr. Carrubba is the

author of six books including: Revised UCC Article 3 and 4, A

Banker’s Guide to Checks and Principles of Banking. He is

the co-author, with Dan Fisher, of both Remote Deposit

Capture – Practical Considerations and most recently, Risk

Management Series – Remote Deposit Capture.

2

THIS PRESENTATION IS DESIGNED TO PROVIDE

ACCURATE AND AUTHORITATIVE INFORMATION

REGARDING ITS SUBJECT MATTER.

IT IS PRESENTED WITH THE UNDERSTANDING THAT

THE PRESENTER IS NOT RENDERING LEGAL,

ACCOUNTING, OR OTHER PROFESSIONAL SERVICES.

IF LEGAL ADVICE OR OTHER EXPERT ASSISTANCE IS

REQUIRED, THE SERVICES OF A COMPETENT

PROFESSIONAL PERSON SHOULD BE SOUGHT.

Presentation Content

@NACHAOnline | #TPISchool

3

Article 4A is state law first promulgated

in 1989 by UCC drafters Uniform Law

Commission and the American Law

Institute.

A “uniform” or “model” law must be

adopted by state legislatures to be

effective.

By 1996, all 50 states and the District

of Columbia had adopted Article 4A.

What is UCC Article 4A?

@NACHAOnline | #TPISchool

4

How Does UCC 4A Relate to

Other Law and Rules?

@NACHAOnline | #TPISchool

5

Federal Reserve Operating Circulars: Drafted to

be consistent with Article 4A, but the circulars

control in the event of any conflict.

Electronic Funds Transfer Act and Regulation E:

Apply generally to consumer electronic funds

transfers, which are not governed by Article 4A.

NACHA Rules: Govern all funds transfers made

over the ACH network, including those to which

Article 4A does and does not apply.

• UCC 4-A is Applicable to Credit Transfers

– Wire Transfers

– ACH Transfers (NACHA Rules)

– Transfers Between Accounts

• UCC 4-A is NOT Applicable to

– Regulation E Transactions

– Debit Transactions

UCC 4-A Applicability

@NACHAOnline | #TPISchool

6

Cannot Rely Exclusively on NACHA Rules

– Rules Generally Not Applicable to

Issues Between FI and Customer

– Rules May Not Vary UCC4A

Provisions

– Rules May Require Conforming Provisions

– Rules Do Not Apply to On-Us Entries

NACHA Rules Applicability

@NACHAOnline | #TPISchool

7

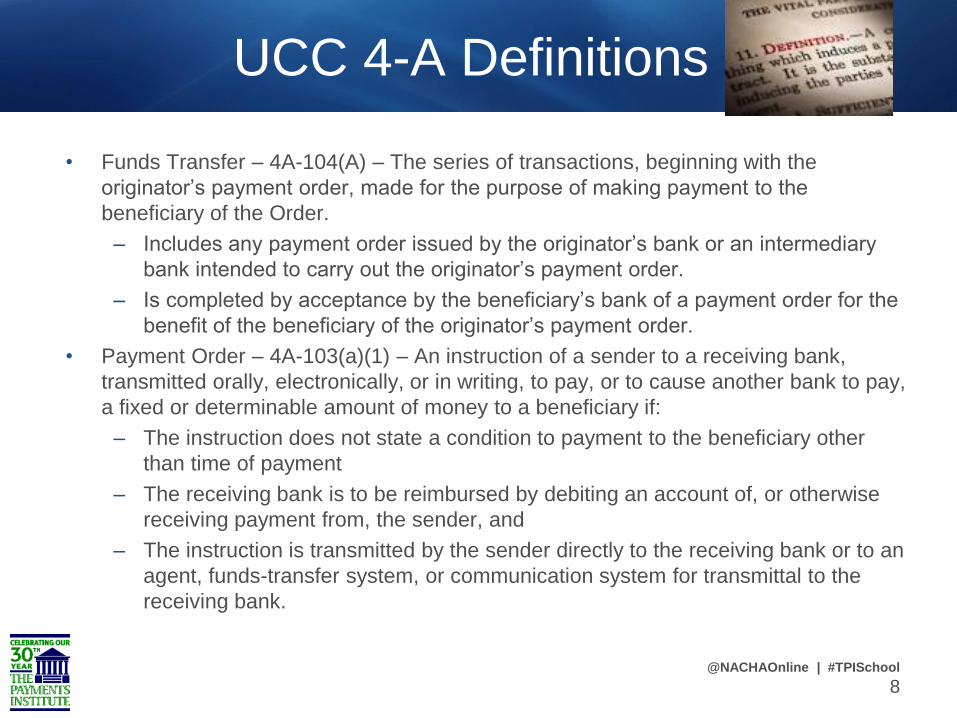

• Funds Transfer – 4A-104(A) – The series of transactions, beginning with the

originator’s payment order, made for the purpose of making payment to the

beneficiary of the Order.

– Includes any payment order issued by the originator’s bank or an intermediary

bank intended to carry out the originator’s payment order.

– Is completed by acceptance by the beneficiary’s bank of a payment order for the

benefit of the beneficiary of the originator’s payment order.

• Payment Order – 4A-103(a)(1) – An instruction of a sender to a receiving bank,

transmitted orally, electronically, or in writing, to pay, or to cause another bank to pay,

a fixed or determinable amount of money to a beneficiary if:

– The instruction does not state a condition to payment to the beneficiary other

than time of payment

– The receiving bank is to be reimbursed by debiting an account of, or otherwise

receiving payment from, the sender, and

– The instruction is transmitted by the sender directly to the receiving bank or to an

agent, funds-transfer system, or communication system for transmittal to the

receiving bank.

UCC 4-A Definitions

@NACHAOnline | #TPISchool

8

• Originator – 4A-104(c) – The sender of the first payment order in a funds

transfer.

• Originator’s Bank – 4A-104(d) – (i) the receiving bank to which the payment

order of the originator is issued if the originator is not a bank, or (ii) the originator

if the originator is a bank.

• Sender – 4A-103(a)(5) – The person giving the instruction to the receiving bank.

• Receiving Bank – 4A-103(a)(4) – The bank to which the sender’s instruction is

addressed.

• Beneficiary – 4A-103(a)(2) – The person to be paid by the beneficiary’s bank.

• Beneficiary’s Bank – 4A-103(a)(3) – The bank identified in a payment order in

which an account of the beneficiary is to be credited pursuant to the order or

which otherwise is to make payment to the beneficiary if the order does not

provide for payment to an account.

• Authorized Account – 4A-105(a)(1) – A deposit account of a customer in a bank

designated by the customer as a source of payment of payment orders issued

by the customer to the bank.

Definitions, cont.

@NACHAOnline | #TPISchool

9

UCC Article 4A Terminology

@NACHAOnline | #TPISchool

10

Article 4A Credit Transfer in

NACHA Rules Terminology

@NACHAOnline | #TPISchool

11

Originator = Originator Beneficiary’s Bank = RDFI

Originator’s Bank = ODFI Beneficiary = Receiver

The most common NACHA Standard Entry Class codes for credit transfers

governed by Article 4A are CCD (Corporate Credit or Debit) and CTX (Corporate

Trade Exchange).

Funds Transfer Process

@NACHAOnline | #TPISchool

12

Originator Issues Payment Order

Receiving Bank

Intermediary Bank

Beneficiary’s Bank

Beneficiary

Fu

nd

s T

ran

sfe

r

Funds Transfer Process from Issuance to Payment

@NACHAOnline | #TPISchool

13

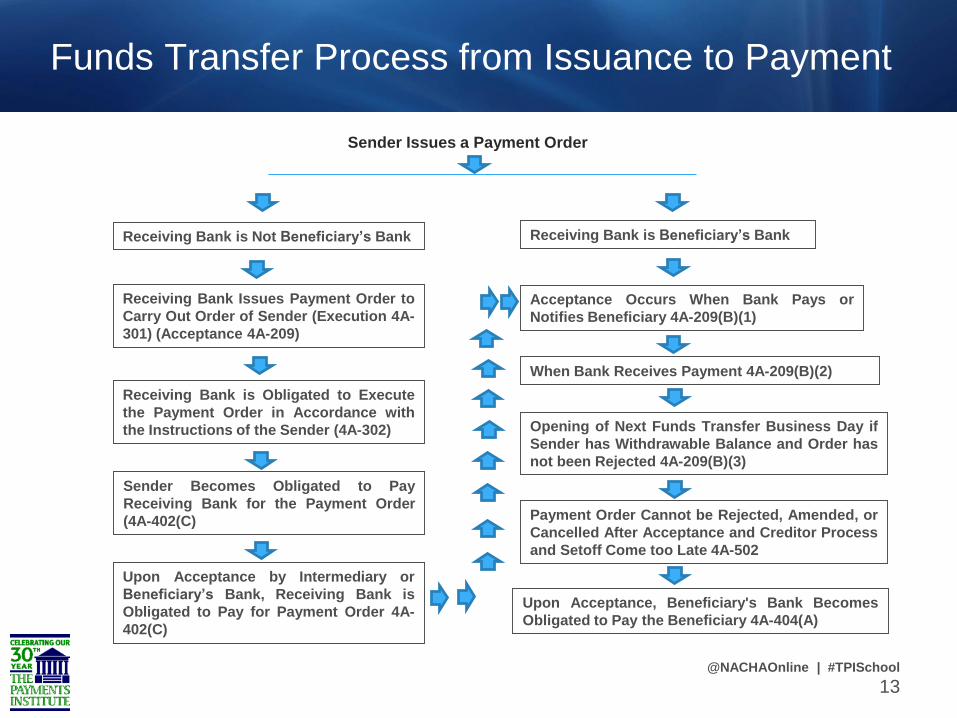

Sender Issues a Payment Order

Receiving Bank is Not Beneficiary’s Bank

Receiving Bank Issues Payment Order to

Carry Out Order of Sender (Execution 4A-

301) (Acceptance 4A-209)

Receiving Bank is Obligated to Execute

the Payment Order in Accordance with

the Instructions of the Sender (4A-302)

Sender Becomes Obligated to Pay

Receiving Bank for the Payment Order

(4A-402(C)

Upon Acceptance by Intermediary or

Beneficiary’s Bank, Receiving Bank is

Obligated to Pay for Payment Order 4A-

402(C)

Receiving Bank is Beneficiary’s Bank

Acceptance Occurs When Bank Pays or

Notifies Beneficiary 4A-209(B)(1)

When Bank Receives Payment 4A-209(B)(2)

Opening of Next Funds Transfer Business Day if

Sender has Withdrawable Balance and Order has

not been Rejected 4A-209(B)(3)

Payment Order Cannot be Rejected, Amended, or

Cancelled After Acceptance and Creditor Process

and Setoff Come too Late 4A-502

Upon Acceptance, Beneficiary's Bank Becomes

Obligated to Pay the Beneficiary 4A-404(A)

• Orally

• In Person

• By Phone

• Electronically

• On Line

• File Transmission

• Storage Media

• Fax

• Writing

• Letter

• Signed Funds Transfer Document

How is a Payment Order Issued?

@NACHAOnline | #TPISchool

14

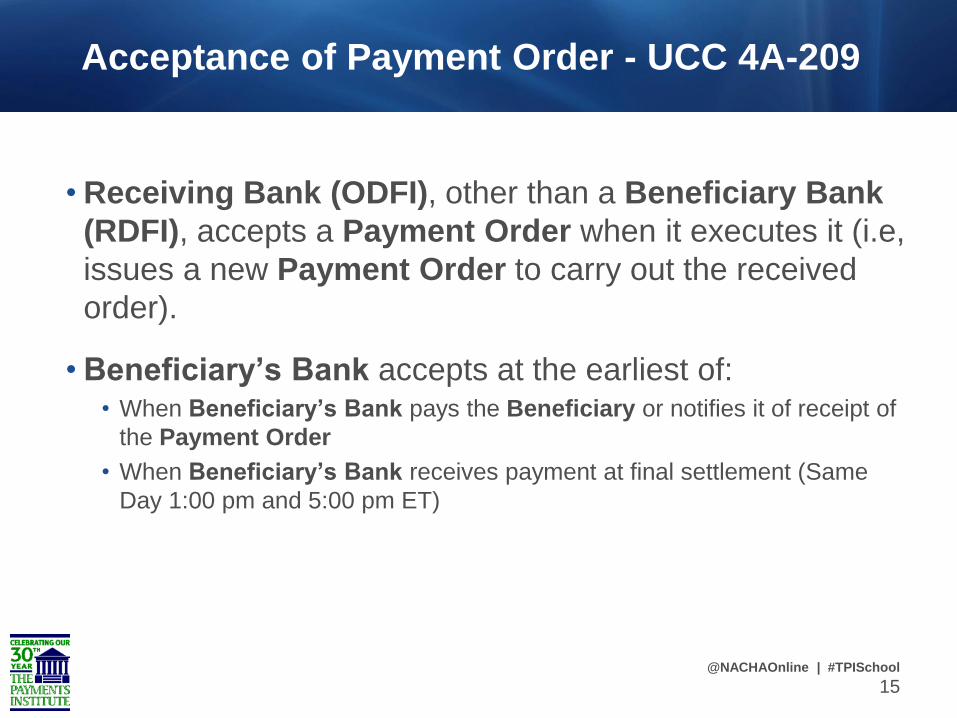

• Receiving Bank (ODFI), other than a Beneficiary Bank

(RDFI), accepts a Payment Order when it executes it (i.e,

issues a new Payment Order to carry out the received

order).

• Beneficiary’s Bank accepts at the earliest of:• When Beneficiary’s Bank pays the Beneficiary or notifies it of receipt of

the Payment Order

• When Beneficiary’s Bank receives payment at final settlement (Same

Day 1:00 pm and 5:00 pm ET)

Acceptance of Payment Order - UCC 4A-209

@NACHAOnline | #TPISchool

15

• Rules Do Not Require The RDFI To Notify

Receiver of Acceptance.

• RDFI Must Give Notice That It Is Not Required

To Give Notice of Acceptance.

Sample Language:Notice of Receipt of Entry

Under the operating rules of the National Automated Clearing House Association, which

are applicable to ACH transactions involving your account, we are not required to give

next day notice to you in receipt of an ACH item and we will not do so. However, we will

continue to notify you of the receipt of payments in the periodic statement we provide to

you.

Obligation To Notify The Receiver

@NACHAOnline | #TPISchool

16

4A-504(d) Payment may be provisional if a funds-

transfer system rule provides so.

• The Originator and Beneficiary are given notice

• Beneficiary, Beneficiary’s Bank, and Originator’s

Bank agree to be bound by the Rules.

• Beneficiary’s Bank did not Receive Payment.

Provisional Payment – UCC 4A

@NACHAOnline | #TPISchool

17

Subsection 3.3.1.4 Credit Entries Subject to UCC

4A are Provisional• Credit to Receiver is Provisional Until RDFI Receives Final

Settlement

• RDFI Entitled to Refund From Receiver

• Receiver Must Agree to Be Bound By The Rules

Sample Language:

Provisional Payment

Credit given by us to you with respect to an automated clearing house credit entry is provisional

until we receive final settlement for such entry through a Federal Reserve Bank. If we do not

receive such final settlement, you are hereby notified and agree that we are entitled to a refund

of the amount credited to you in connection with such entry, and the party making payment to

you via such entry (i.e. the originator of the entry) shall not be deemed to have paid you in the

amount of such entry.

Provisional Payment – NACHA Rules

@NACHAOnline | #TPISchool

18

• Bank is NOT required to accept a payment order.

• How can a bank reject a payment order?

• By sending rejection

• Bank does not execute

• Bank fails

• Acceptance precludes rejection

Rejection of Payment Order - UCC 4A-210

@NACHAOnline | #TPISchool

19

• UCC § 4A-210. Rejection of Payment Order.

(a) A payment order is rejected by the receiving bank (ODFI) by a notice of rejection transmitted to the sender orally, electronically, or in writing. A notice of rejection need not use any particular words and is sufficient if it indicates that the receiving bank is rejecting the order or will not execute or pay the order. Rejection is effective when the notice is given if transmission is by a means that is reasonable in the circumstances. If notice of rejection is given by a means that is not reasonable, rejection is effective when the notice is received. If an agreement of the sender and receiving bank establishes the means to be used to reject a payment order, (i) any means complying with the agreement is reasonable and (ii) any means not complying is not reasonable unless no significant delay in receipt of the notice resulted from the use of the noncomplying means.

(b) Timing consideration – method of rejection notice for Same Day entry – possible coverage in security procedures

The “Fine Print” on Rejection

@NACHAOnline | #TPISchool

20

• Procedures Established by Agreement

– Verification of Authenticity of Order or Cancellation

– Error Detection

• Commercially Reasonable Security Procedure

– Question of Law

• Circumstances Known to Bank

• Security Procedures in General Use

• Alternative Security Procedures Offered

Security Procedures 4A-201

@NACHAOnline | #TPISchool

21

• Authorized Transfers Enforceable

• Unauthorized Transfers Enforceable if:

– Verified Pursuant to Security Procedure

– Security Procedure is Commercially Reasonable

– Bank Accepted it in Good Faith and in Compliance with Security Procedure

Enforceability of Funds Transfer

@NACHAOnline | #TPISchool

22

• Unauthorized Transfers Not Enforceable if:

– Bank Agrees not to Enforce

– No Security Procedure

– Security Procedure is not Commercially Reasonable

– Not Made by Authorized Person or Person Entrusted with Security Procedure

– Not Made by Person who Obtained to Access to Transmitting Facility

– Made by Person that Obtained Security Procedure from a Source not Controlled by the Customer

Unenforceable Funds Transfer

@NACHAOnline | #TPISchool

23

What is Accessed

Online Banking

Information

Wire Transfer

ACH Origination

Bill Pay

Internal Transfers

Remote Deposit Capture

Other

Customer

Commercial

Consumer

Customer Circumstances Known to Bank

FFIEC Guidance

Are Security Procedures Commercially Reasonable?

Factors to Consider

@NACHAOnline | #TPISchool

24

• Dual Control.

• Personal Identification Numbers (“PIN”)

• RSA Token.

• Out-of-Band Authentication.

• Call-Back Verification

• Dedicated Computer.

• Payment Activity Review.

Wire Transfer Security Procedures

@NACHAOnline | #TPISchool

25

• Security Procedures Generally in Use

• Customer Agreements

• Alternative Security Procedures

• Transaction Monitoring

• Case Law

Factors to Consider

@NACHAOnline | #TPISchool

26

• Bank must refund if:

– Transfer not Authorized

– Not Enforceable

• Customer must notify Bank within Reasonable Time not

exceeding 90 Days.

– Bank not Required to Pay Interest

– Bank must Refund

– May not be varied by Agreement

• Must make claim within ONE year

– May not be varied by Agreement

Refund of Payment 4A-204

@NACHAOnline | #TPISchool

27

• Acceptance cannot occur if:

– Name, Account or other Number refers to nonexistent or

unidentifiable person.

• If Payment Order identifies Beneficiary by both name

and account number and name and number identify

different persons:

– If Bank does not know, Bank may rely on number

– If Bank does know, Bank may pay person named or account

number if person is entitled

– Bank liable if wrong person is paid

• Similar Rule applies to Intermediary Bank

Mis-description of Beneficiary – 4A-207

@NACHAOnline | #TPISchool

28

• Bank is NOT required to accept

• Bank Rejects Payments Order

– By sending rejection

– Bank does not execute

– Bank fails

– Acceptance precludes rejection

Rejection of Payment Order 4A-210

@NACHAOnline | #TPISchool

29

• Made orally, electronically or in writing

• Received before accepted

• Not effective after acceptance

• Unaccepted Payment Order is cancelled after

5 Business Days

• Cancelled Payment Order cannot be

accepted

• Agreement or Funds-Transfer System Rule

Cancellation and Amendment 4A-211

@NACHAOnline | #TPISchool

30

• With the exception of duplicate or erroneous entries,

Entries cannot be amended or cancelled after receipt by

the ACH Operator

• ODFI may request RDFI to return Erroneous Entry

• ODFI Indemnifies RDFI if Entry is returned

• A payment order may be cancelled after acceptance if

allowed by a funds transfer rule and the NACHA Rules

allow for a reversal. (Reversing Entries OR 27 – 28).

Cancellation and Amendment Rules

@NACHAOnline | #TPISchool

31

• Document Current Security Procedures

– Online Access

– Wire Transfer & ACH Origination

– Customer Selected Security Procedure

• Document Transaction Monitoring

• Compare Bank Security Procedures to FFIEC

• Compare Bank Security Procedure to Other Bank’s

Security Procedures

• Compare Bank Security Procedure to Cases

• Review Customer Agreements

Commercially Reasonable

Security Procedure Checklist

@NACHAOnline | #TPISchool

32

– Online/Internet Banking Agreements

– Wire Transfer Agreements

– ACH Origination Agreements

– Security Procedure

– Customer Agrees is Commercially Reasonable

– Customer Agrees to be Bound

– Customer will Safeguard Security Procedure

– Customer will Scan Personal Computer

– Customer will Give Notification of Unauthorized Transfer

AGREEMENTS

@NACHAOnline | #TPISchool

33

• UCC 4A Designates the applicable law based on the location of the

parties subject to agreement between the parties and ACH Rules.

• NACHA Rules – In the absence of an agreement, the laws of the

state of New York are applicable.

• The RDFI may provide a choice of law provision to the Receivers

• Sample Language

Choice of Law

We may accept on your behalf payments to your account, which have been transmitted

through one or more Automated Clearing Houses and which are not subject to the

Electronic Funds Transfer Act and your rights and obligations with respect to such

payments shall be construed in accordance with and governed by the laws of the state of

_______, unless it has otherwise specified in a separate agreement that the law of some

other state shall govern.

Choice Of Law

@NACHAOnline | #TPISchool

34

Conclusions and Questions

@NACHAOnline | #TPISchool

35

www.adamsandreese.com

Email: [email protected]

THE PAYMENTS INSTITUTE — July 16-19, 2017

Emory Conference Center Hotel, Emory University, Atlanta, Georgia

Cracking the Code:

UCC Article 4A & the

ACH Network

Presented by:

PAUL A. CARRUBBA

Adams and Reese LLP

Phone: (601) 292-0788

E-Mail: [email protected]