CPPIB Debt Issuance Presentation - CPP Investment … Debt Issuance Presentation. ... company under...

23

Copyright © 2017. Canada Pension Plan Investment Board. All rights reserved. Spring 2017 CPPIB Debt Issuance Presentation

Transcript of CPPIB Debt Issuance Presentation - CPP Investment … Debt Issuance Presentation. ... company under...

Copyright © 2017. Canada Pension Plan Investment Board. All rights reserved.

Spring 2017

CPPIB Debt Issuance Presentation

IMPORTANT NOTICES

• This material has been prepared solely for informational purposes and does not constitute or form part of, and should not be construed as, an offer, invitation or inducement to purchase or subscribe for any securities. No part of this material, nor the fact of its publication, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. No representation or warranty, either express or implied, is provided in relation to the fairness, accuracy, completeness or reliability of the information or any opinions contained herein and no reliance whatsoever should be placed on such information. Any opinions expressed in this material are subject to change without notice and neither Canada Pension Plan Investment Board (“CPPIB”) nor any other person is under any obligation to update or keep current the information contained herein.

• Neither the Notes to be issued by CPPIB Capital Inc. (“CPPIB Capital”) from time to time under the Debt Issuance Programme described in this presentation or the Guarantee thereof by CPPIB have been registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”) or the securities laws of any other jurisdiction, and CPPIB Capital is not registered and does not intend to register as an investment company under the U.S. Investment Company Act of 1940, as amended (the “Investment Company Act”). Any Notes offered under the Debt Issuance Programme are offered in the United States only to “qualified institutional buyers” (as defined in Rule 144A under the Securities Act) who are also “qualified purchasers” (as defined in Section 2(a)(51)(A) of the Investment Company Act and the rules thereunder) and outside the United States to non-U.S. persons in compliance with Regulation S of the Securities Act.

• This material is directed at and is only being distributed in the United Kingdom to: (i) persons who have professional experience in matters relating to investments who fall within the definition of “investment professionals” in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”); (ii) high net worth entities and other persons to whom it may lawfully be communicated falling within Article 49 of the Order or (iii) persons to whom it may otherwise lawfully be communicated. Other persons in the United Kingdom should not read, rely upon or act upon this material. By accepting receipt of this material, each recipient in the United Kingdom acknowledges that it is a person falling within one of the foregoing categories. Other persons in the United Kingdom should not rely or act upon this material.

• Pursuant to applicable securities laws (including, but not limited to, the European Market Abuse Regulation), the recipients of this material should not use this information to acquire or sell, or attempt to acquire or sell, for themselves or for a third party, either directly or indirectly, any Notes until after the information has been made available to the public. It is also forbidden for the recipients to pass on the materials to another person outside the scope of his work, profession or function and to recommend, or arrange for, on the basis of these materials, the acquisition or the selling of, Notes so long as the information has not been made available to the public. The same obligation applies to any other person who obtains this material and knows or should have known that the information that it contains is inside information (within the scope of the Market Abuse Regulation and other applicable securities laws).

• No securities commission or similar authority in Canada has in any way passed upon the merits of the securities referred to hereunder nor has it reviewed this document, and any representation to the contrary is an offence. The securities that may be offered hereunder have not been and will not be qualified for distribution to the public under the securities laws of any province or territory of Canada and will only be offered in Canada pursuant to applicable private placement exemptions.

• Certain statements in this presentation constitute “forward-looking statements,” including statements regarding CPPIB’s expectations and projections for future operating performance and business prospects. The words “believe”, “expect”, “anticipate”, “intend”, “estimate”, “may impact” and other similar expressions or future or conditional verbs such as “will”, “should”, “would” and “could” and similar expressions or variations of these expressions identify forward-looking statements. In addition, all statements other than statements of historical facts included in this presentation, including, without limitation, those regarding CPPIB’s financial position and results, business strategy, plans and objectives of management for future operations, including development plans and objectives relating to CPPIB’s products and services, are forward-looking statements. Such forward-looking statements and any other projections contained in this presentation (whether made by us, CPPIB Capital or any third party) involve known and unknown risks, uncertainties and other factors which may cause CPPIB’s actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by forward-looking statements. A variety of factors, many of which are beyond CPPIB’s control, may cause actual results to differ materially from the expectations expressed in the forward-looking statements.

IMPORTANT NOTICES CONT/…

OVERVIEW

Overview

CPPIB OVERVIEW 1

• CPPIB is a Canadian federal Crown corporation but operates independently from government.

• CPPIB is a standalone AAA/Aaa credit.*

• The Funds of the CPP invested by CPPIB are fully segregated from all government accounts.

• Its legislated mandate is to invest net contributions to Canada’s national pension plan.

• Current assets of $300 billion are projected to grow to $1.0 trillion by 2042.**

* A credit rating is not a recommendation to buy, sell or hold investments, and may be subject to revision or withdrawal at any time by the relevant rating agency.** 27th Actuarial Report

AAA

Aaa

AAA

What is CPPIB?

WHAT IS CPPIB? 2

• CPPIB invests the net contributions on behalf of 20 million Canadian contributors and beneficiaries.• CPPIB employs approximately 1,500 people in eight global offices to fulfill CPPIB’s “investment-only”

mandate.

• Contributions are legally mandated and the fund is not subject to withdrawal or redemption risk.

CPP INVESTMENT

BOARD

CANADA PENSION

PLAN

GLOBAL MARKETS

$48 BILLION CONTRIBUTIONS*

CONTRIBUTIONS

EMPLOYEES

EMPLOYERSPENSIONERS

$45 BILLION PAYMENT TO OTTAWA

INVEST IN MARKETS

INVESTMENT RETURNS

$45 BILLION BENEFIT PAYMENTS

* Figures are based on the December 31, 2015 Actuarial Report (27th)

DEBT ISSUANCE

Why issue debt?

DEBT ISSUANCE 3

• Allows CPPIB to benefit from our standalone ‘AAA/Aaa’ ratings.

• Better tailoring of CPPIB’s risk profile via selective leverage.

• Prudent liquidity management provides CPPIB with the flexibility to invest in dislocated/stressed markets.

Debt Issuance Programme

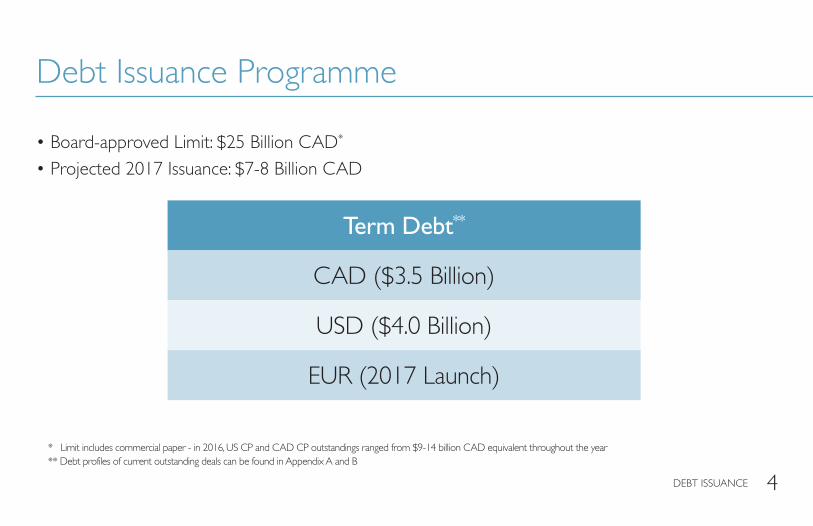

DEBT ISSUANCE 4

• Board-approved Limit: $25 Billion CAD*

• Projected 2017 Issuance: $7-8 Billion CAD

Term Debt**

CAD ($3.5 Billion)

USD ($4.0 Billion)

EUR (2017 Launch)

* Limit includes commercial paper - in 2016, US CP and CAD CP outstandings ranged from $9-14 billion CAD equivalent throughout the year** Debt profiles of current outstanding deals can be found in Appendix A and B

LEGISLATION

Amending Formula

5LEGISLATION

Parliament cannot amend the CPPIB Act, or pass any other laws which directly or indirectly alter the CPPIB Act, without approval “of at least two thirds of the included provinces, having in the aggregate not less than two

thirds of the population of all of the included provinces.” (CPP Act, s. 114 (4))

• This is the cornerstone of CPPIB’s legal structure.

• Changing the legislation governing the CPPIB requires the cooperation of the stewards – the federal and provincial finance ministers who oversee the CPP. This process is more onerous than the constitutional amending formula and requires agreement among the federal government and two-thirds of the provinces representing two-thirds of the population.

• The certainty around its legislative framework enables CPPIB to invest for the long term.

Triennial Review

6LEGISLATION

• The Chief Actuary of Canada, an independent official within the Office of the Superintendent of Financial Institutions, prepares a report every three years setting out the results of an actuarial examination of the Canada Pension Plan based on the state of the Canada Pension Plan Account and the investments of CPPIB, including the minimum contribution rate required to sustain the Canada Pension Plan. (s. 115 CPP)

• In his most recent report (December 31, 2015), the Chief Actuary stated that “despite the projected substantial increase in benefits paid as a result of an aging population, the Plan is expected to be able to meet its obligations throughout the projection period (of 75 years).” (Actuarial Report, p.12)

• CPPIB’s stewards (the federal and provincial finance ministers) review the financial state of the Canada Pension Plan every three years and may make recommendations as to whether contribution rates should be changed by regulation. (s. 113.1(1) CPP)

Minimum Assets Held

7LEGISLATION

Under the statutory framework:“No payment shall be made out of the Consolidated Revenue Fund under

[Section 108 of the CPP] in excess of the total of:a) The amount of the balance to the credit of the Canada Pension

Plan Account, andb) The fair market value of the assets of the Investment Board less

its liabilities” (s.108(4) CPP)

Accordingly, Note holders have the assurance that CPPIB cannot be required to transfer amounts to fund CPP benefits if,

after any such transfer, CPPIB would not be in a position to meet all of its obligations including under the Notes.

PERFORMANCE AND PORTFOLIO COMPOSITION

Investment Mandate

PERFORMANCE AND PORTFOLIO COMPOSITION 8

Our ”investment-only” mandate is:

“to manage any amounts transferred to it [from the Canada Pension Plan]…in the best interests of the contributors and beneficiaries [of the Canada Pension Plan]” and “to invest its assets with a view to achieving a maximum rate of return, without undue risk of loss …having regard to the factors that may affect the funding of the Canada Pension Plan and the ability of the Canada

Pension Plan to meet its financial obligations on any given business day.” (s.5 CPPIB Act)

As a result, investments are made without political direction or any other non-investment objectives.

Geographic Breakdown

PERFORMANCE AND PORTFOLIO COMPOSITION 9

0

20

40

60

80

100

F2015F2010F2005 F2016F2000

Canada United States Europe (ex UK) Asia (ex Japan)

Japan Latin America Australia Other

United Kingdom

Asset Breakdown

PERFORMANCE AND PORTFOLIO COMPOSITION 10

0

20

40

60

80

F2000

Bonds & Money Market Securities

In�ation-linked Bonds

Canadian Equities Foreign DevelopedMarket Equities

Emerging MarketEquities

Real Estate Infrastructure Other

F2016F2015F2010F2005

LIQUIDITY

Cash & Liquidity Group (CLG)

11LIQUIDITY

• Responsible for optimizing firm financing across three tools:

1. Global unsecured issuance - Term Debt - CAD/US/ECP

2. Secured Financing - Repo - Illiquid asset financing

3. Synthetic Beta - Swaps & Futures

• Responsible for liquidity monitoring and planning

• Monitor liquidity through internal 10 day, 6 month and 1 year Liquidity Coverage Ratios

• Multi-year cashflow forecasting

• Determine optimal liability duration

CLG is the firm’s liability manager which is divided into two sub-groups outlined below:

Central Financing Asset Liability Management

APPENDIX

Asia-Paci�c

Latin America

US

EMEA

Canada

Other

Central Banks and Of�cial Institutions

Pension & Insurance

Asset Manager

Treasury

Corporate

Asia-Paci�c

Latin America

US

EMEA

Canada

Other

Central Banks and Of�cial Institutions

Pension & Insurance

Asset Manager

Treasury

Corporate

Asia-Paci�c

Latin America

US

EMEA

Canada

Other

Central Banks and Of�cial Institutions

Pension & Insurance

Asset Manager

Treasury

Corporate

Asia-Paci�c

Latin America

US

EMEA

Canada

Other

Central Banks and Of�cial Institutions

Pension & Insurance

Asset Manager

Treasury

Corporate

Asia-Paci�c

Latin America

US

EMEA

Canada

Other

Central Banks and Of�cial Institutions

Pension & Insurance

Asset Manager

Treasury

Corporate

Asia-Paci�c

Latin America

US

EMEA

Canada

Other

Central Banks and Of�cial Institutions

Pension & Insurance

Asset Manager

Treasury

Corporate

A. Current Outstanding USD Debt Profile

APPENDIX 12

29%26%

47%

35%

6%

3% 5%

7%8%

28%3%

23% 24%

13%

34%

12% 14%

8%

38% 37%

Currency

Description

Outstanding

Issue Date

Issue Spread (v Mid Swaps)

Currency

Description

Outstanding

Issue Date

Issue Spread (v Mid Swaps)

USD

1.25% 20-Sep-19

$2.0 Billion USD

13-Sep-16

+25

USD

2.25% 25-Jan-22

$2.0 Billion USD

13-Jan-17

+44

SERIES A SERIES B

By Geography

By Investor Type

Details

Pension Insurance

Asset Manager SSA

Treasury

Retail

Other

UK EMEA

Canada US

Asia South America

Pension Insurance

Asset Manager SSA

Treasury

Retail

Other

UK EMEA

Canada US

Asia South America

Pension Insurance

Asset Manager SSA

Treasury

Retail

Other

UK EMEA

Canada US

Asia South America

Pension Insurance

Asset Manager SSA

Treasury

Retail

Other

UK EMEA

Canada US

Asia South America

Currency

Description

Outstanding

Issue Date

Issue Spread (v GoC)

Currency

Description

Outstanding

Issue Date

Issue Spread (v GoC)

Currency

Description

Outstanding

Issue Date

Issue Spread (v GoC)

CAD

1.40% 4-Jun-20

$1.00 Billion

1-Jun-15

+49

CAD

1.00% 15-Jan-19

$1.25 Billion

12-Jan-16

+61

CAD

1.10% 10-Jun-19

$1.25 Billion

06-Jun-16

+55

B. Current Outstanding CAD Debt Profile

APPENDIX 13

SERIES A SERIES B SERIES C

By Geography

By Investor Type

Details

31.85%

95.20%

4.80%

80.80%

5.00% 6.50%5.00% 9.20%

2.40%

9.10% 2.90%0.80%

78.20%

25.81% 29.33%

18.10% 0.96% 2.87%13.93% 9.60%

11.20% 6.90% 4.60%

38.50% 52.28% 52.94%

0.02%0.35% 0.12%0.63%

C. Key Links*

14APPENDIX

Performance and Sustainability

Financial highlights

Quarterly and annual results

Actuary and Special Exam Reports

Sustainability of the CPP

Chief Actuary Reports

Governance

Independence

Accountability

Board of Directors

Policies

Legislation and Regulations

Canada Pension Plan

Canada Pension Plan Regulations

Canada Pension Plan Investment Board Act

Canada Pension Plan Investment Board Regulations

* These links are provided as information only and are not incorporated by reference in this presentation.