COULD THE LONG WAIT FOR SUCCESS BE OVER ... Central Riverside Vietcombank Tower MB Sunny Tower C T...

20

THE SLOW ROAD BACK THE SLOW ROAD BACK Presented by: Marc Townsend, Managing Director, CBRE Vietnam Park Hyatt Saigon, HCMC 10 July 2013 10 July, 2013 COULD THE LONG WAIT FOR SUCCESS BE OVER? Andy Murray ended Britain's 77 year wait for a men's Wimbledon champion British and Irish Lions ended barren 16 years with a crushing victory How much longer for the Vietnamese real estate market? 2 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

Transcript of COULD THE LONG WAIT FOR SUCCESS BE OVER ... Central Riverside Vietcombank Tower MB Sunny Tower C T...

THE SLOW ROAD BACKTHE SLOW ROAD BACKPresented by: Marc Townsend, Managing Director, CBRE VietnamPark Hyatt Saigon, HCMC10 July 201310 July, 2013

COULD THE LONG WAIT FOR SUCCESS BE OVER?

Andy Murray ended Britain's 77 year wait for a men's Wimbledon champion

British and Irish Lions ended barren 16 years with a crushing victory

How much longer for the Vietnamese real estate market?

2 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

RECOVERY IS JUST AROUND THE CORNER

3 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

THE ECONOMYTHE ECONOMYMOVING IN THE RIGHT DIRECTION

1H 2013 ECONOMIC OVERVIEWGold and Bank Deposits Become Less Attractive

Global gold price: decreases 2,00050

g p24% YTD.

Local gold price: reached its bottom in June (down 22%) and

1,400

1,600

1,800

38

42

46

al go

ld pri

ce (U

S$)

sell p

rice (

VND m

illion

)

bottom in June (down 22%) and currently down 19% YTD

Deposit rates: 800bps reduction over the last 18 months

1,000

1,200

30

34

09/2011 12/2011 03/2012 06/2012 09/2012 12/2012 03/2013 06/2013

Glob

Loca

l gold

LOCAL GOLD GLOBAL GOLD over the last 18 months.

425

CPI (y-o-y, Vietnam) Rediscounting Rate Refinancing Rate CPI (m-o-m, Vietnam)

Inflation surged

LOCAL GOLD GLOBAL GOLD

Source: SJC

1

2

3

4

15

20

25

% m

-o-m)

nteres

t rate

s (%

) Monetary expansion

-1

0

1

0

5

10

Dec 10 Mar 11 Jun 11 Sep 11 Dec 11 Mar 12 Jun 12 Sep 12 Dec 12 Mar 13 Jun 13

CPI (%

CPI (%

y-o-y

) / In

Monetary contraction Inflation controlled

5 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13

Source: State Bank of Vietnam

1H 2013 ECONOMIC OVERVIEW

Regional stock markets,

Stock Market Recovers, Real Estate to Come Back into Focus?

gy-o-y return as of July 9, 2013:

Thailand (SET) up 23.1%;

Singapore (SGX) up 19.9%;

Indonesia (JCI) up 12.8%;

Vietnam (VNINDEX) peaked at Vietnam (VNINDEX) peaked at 528 points in June, up 26%, but dropped back to 24%.Source: Bloomberg

REAL ESTATE INDEX 2Y 1Y 6M 3M 1M Current

Real Estate Holding & Development Listed Companies (66)

55.5 44.8 39.5 41.9 42.2 45.4(66)

Real Estate Services Listed Companies (2)

84.4 25 23.8 25.3 22.3 26.1

Source: Stockbiz

6 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

Sou ce: S oc b

GOVERNMENT POLICIESSupport on the Way

Expansion Monetary Policies (as June 27)Fiscal Policies - Tax Cut (from July 2013) Expansion Monetary Policies (as June 27)Fiscal Policies Tax Cut (from July 2013)

Devaluation of the dong 1% versus the U Dollar (to VND21,036)

For social housing:

• Corporate tax rate: 10%;

The interest-rate ceilings on short-term dong-denominated bank deposits: lowered to 7.0% from 7.5%

Corporate tax rate: 10%;

• VAT: cut from 10% to 5%.

Personal income tax:

• Level of deduction: increased to VND9 The ceiling on dollar deposits:

• For institutional depositors: fall to 0.25% from 1.0%

• For individual depositors: fall to 1.25%

Level of deduction: increased to VND9 million/month from VND4 million/month.

• Level of deduction for each dependent: increased to VND3.6/month from o d dua depos to s a to 5%

from 2.0%.VND1.6 million/month for one dependent.

• Improve trade balance• Reduce banks' funding costs => Lend at

• Boost domestic consumption and production• Reduce banks funding costs => Lend at

lower rates• Encourage people to transfer USD for VND• Bolster foreign-exchange reserves

7 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

GOVERNMENT POLICIES

VAMCVAMC –come back next year…come back next year…

8 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

SOME PEOPLE ARE STILL SPENDINGCar Sales Volume Recovers

Vietnam Car Sales Volume

0.660,000 Registration fee reduced from 10% -20% to 10% - 15% in April.

-0.2

0.2

20,000

40,000

-0.6-

,

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2008 2009 2010 2011 2012 2012No. of cars selling % change YoY

Source: VAMA

GM and Ford accounted 18% of total personal car sales in 5M/2013

9 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

SOME ARE STILL BUILDING …Steady Construction Progress at Some Major Development Sites

Liberty Central Riverside

Vietcombank Tower

MB Sunny Tower

C T Leman PlazaC.T Leman Plaza

New Pearl

Hi L Ri id

10 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

Him Lam Riverside

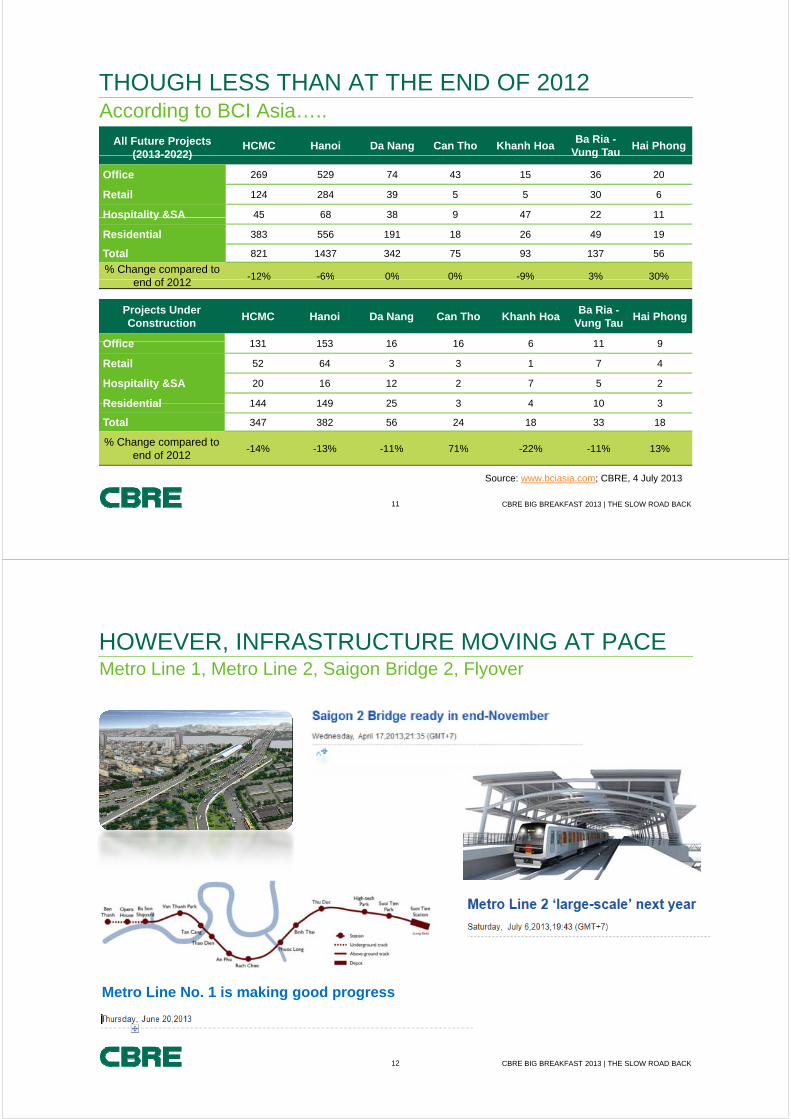

THOUGH LESS THAN AT THE END OF 2012According to BCI Asia…..

All Future Projects(2013-2022)

HCMC Hanoi Da Nang Can Tho Khanh HoaBa Ria -

Vung TauHai Phong

(2013-2022) Vung Tau

Office 269 529 74 43 15 36 20

Retail 124 284 39 5 5 30 6

Hospitality &SA 45 68 38 9 47 22 11Hospitality &SA 45 68 38 9 47 22 11

Residential 383 556 191 18 26 49 19

Total 821 1437 342 75 93 137 56

% Change compared to d f 2012

-12% -6% 0% 0% -9% 3% 30%end of 2012

12% 6% 0% 0% 9% 3% 30%

Projects Under Construction

HCMC Hanoi Da Nang Can Tho Khanh HoaBa Ria -

Vung TauHai Phong

Offi 131 153 16 16 6 11 9Office 131 153 16 16 6 11 9

Retail 52 64 3 3 1 7 4

Hospitality &SA 20 16 12 2 7 5 2

Residential 144 149 25 3 4 10 3Residential 144 149 25 3 4 10 3

Total 347 382 56 24 18 33 18

% Change compared to end of 2012

-14% -13% -11% 71% -22% -11% 13%

11 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

Source: www.bciasia.com; CBRE, 4 July 2013

HOWEVER, INFRASTRUCTURE MOVING AT PACEMetro Line 1, Metro Line 2, Saigon Bridge 2, Flyover

,

Metro Line No. 1 is making good progress

12 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

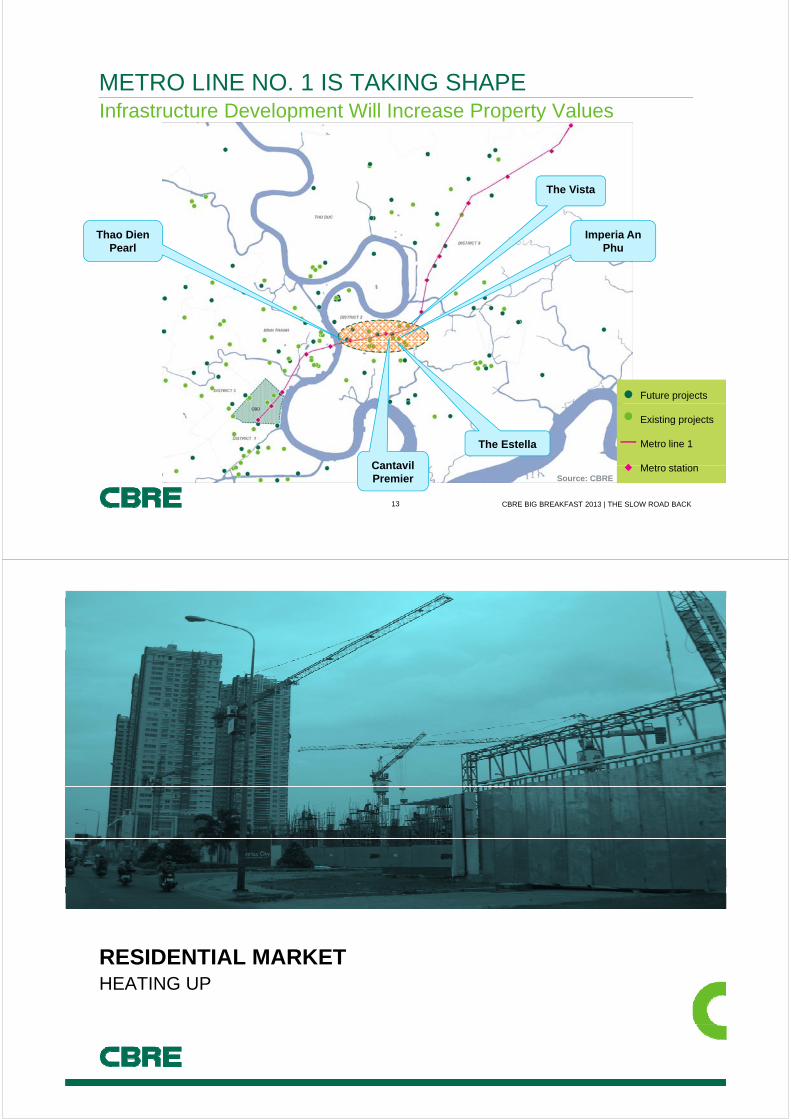

METRO LINE NO. 1 IS TAKING SHAPEInfrastructure Development Will Increase Property Values

The Vista

Thao DienPearl

Imperia An Phu

Future projects

The Estella

Cantavil

Existing projects

Metro line 1

M t t ti

13 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

CantavilPremier

Metro stationSource: CBRE

RESIDENTIAL MARKETRESIDENTIAL MARKETHEATING UP

REGIONAL LUXURY CONDOMINIUMPrices in HCMC Rank Second after Bangkok

Condominium Selling Price (US$/sm)

Bangkok, 5,1575,000

6,000

Ho Chi Minh, 3,838

Hanoi, 2,5962 000

3,000

4,000

US$/

sm

Phnom Penh, 1,470

Yangon, 1,611

0

1,000

2,000U

02004 2005 2006 2007 2008 2009 2010 2011 2012 Q1 2013

Bangkok Ho Chi Minh Hanoi Phnom Penh Yangon

* HCMC’s CBD Luxury projects: The Lancaster, Sailing Tower, Avalon, Saigon Luxury Apartment, Leman CT Plaza. (Except: Vincom Center B)** Hanoi Luxury projects: Pacific Place, Vincom Park Place, Golden Westlake, Landmark 72 (Keangnam Landmark), Indochina Plaza Hanoi, Hoang Thanh Tower, D’ Palais de Louis

Source: CBRE Research

15 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

GOVERNMENT POLICIESResolution 02/NQ – A Push For Real Estate

30 trillion loan scheme for residential real estate:

• Unit size: < 70 sm each

• Price: < VND15 million psm

The interest rate will be capped at 6% per annum for 10 yearsper annum for 10 years.

Khang Gia Tan Huong (Tan Phu District) - 289 units - the firstDistrict) 289 units the first

project in HCMC to benefit from the loan scheme

• Address apparent demand issues by providing mortgages to buyers• Address apparent demand issues by providing mortgages to buyers

• Encourages developers to focus on the mass market

16 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

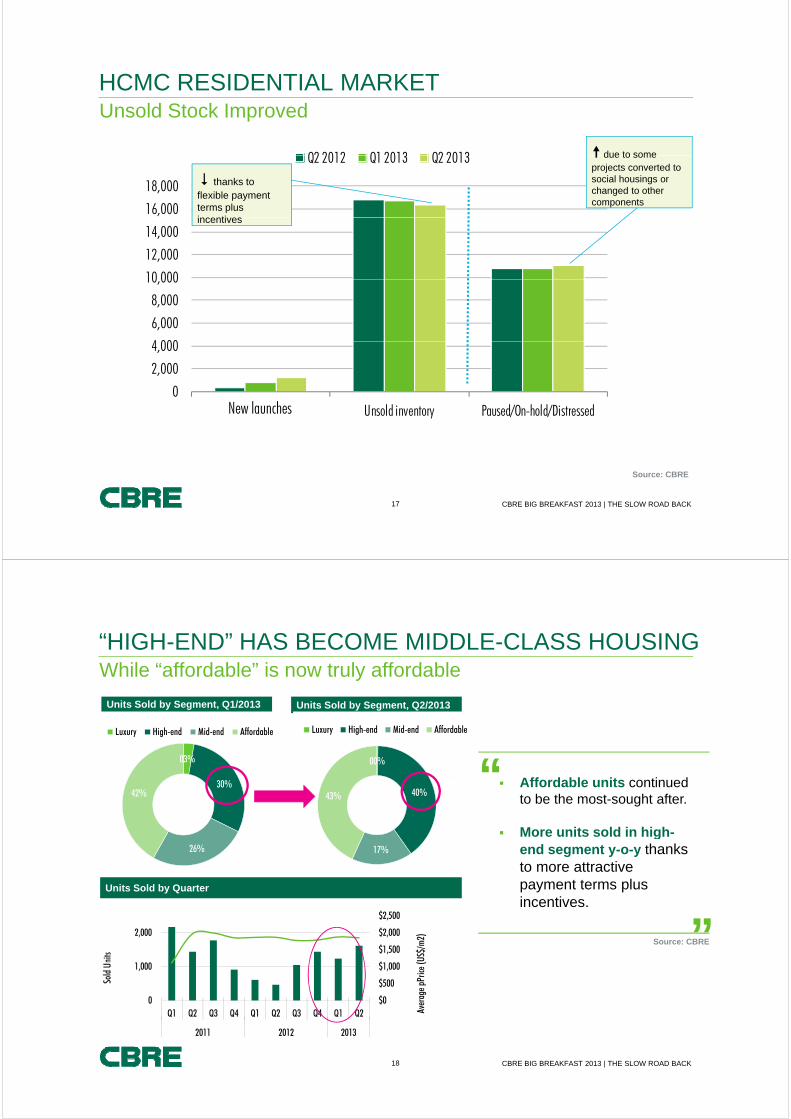

HCMC RESIDENTIAL MARKETUnsold Stock Improved

Q2 2012 Q1 2013 Q2 2013 due to some

16,000

18,000

Q2 2012 Q1 2013 Q2 2013 due to some projects converted to social housings or changed to other components

thanks to flexible payment terms plus i ti

10 000

12,000

14,000incentives

4 000

6,000

8,000

10,000

0

2,000

4,000

N l hNew launch Unsold inventory Paused/On-hold/DistressedNew launches

17 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

Source: CBRE

“HIGH-END” HAS BECOME MIDDLE-CLASS HOUSINGWhile “affordable” is now truly affordable

Units Sold by Segment, Q1/2013 Units Sold by Segment, Q2/2013

03%

Luxury High-end Mid-end Affordable

“00%

Luxury High-end Mid-end Affordable

30%42%

Affordable units continued to be the most-sought after.

More units sold in high-

40%43%

26%

Units Sold by Quarter

gend segment y-o-y thanks to more attractive payment terms plus incentives

17%

incentives.

”Source: CBRE

$1 000

$1,500

$2,000

$2,500

1 000

2,000

(US$

/m2)

nits

$0

$500

$1,000

0

1,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Aver

age p

Price

(

Sold

U

18 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

2011 2012 2013

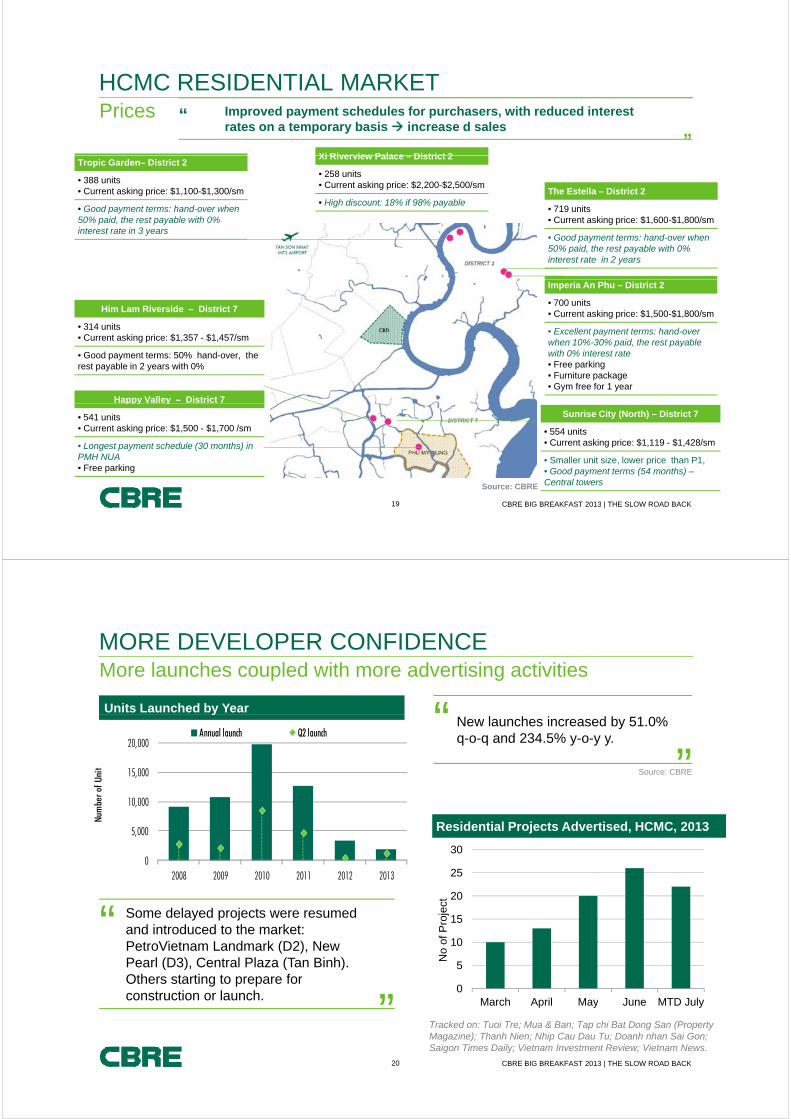

HCMC RESIDENTIAL MARKETPrices

Xi Riverview Palace District 2

“ Improved payment schedules for purchasers, with reduced interest rates on a temporary basis increase d sales

”

The Estella – District 2

• 719 unitsC t ki i $1 600 $1 800/

Tropic Garden– District 2

• 388 units• Current asking price: $1,100-$1,300/sm

• Good payment terms: hand-over when 50% id th t bl ith 0%

Xi Riverview Palace – District 2

• 258 units• Current asking price: $2,200-$2,500/sm

• High discount: 18% if 98% payable

• Current asking price: $1,600-$1,800/sm

• Good payment terms: hand-over when 50% paid, the rest payable with 0% interest rate in 2 years

50% paid, the rest payable with 0% interest rate in 3 years

Imperia An Phu – District 2

• 700 units• Current asking price: $1,500-$1,800/sm

• Excellent payment terms: hand-over when 10% 30% paid the rest payable

Him Lam Riverside – District 7

• 314 units• Current asking price: $1,357 - $1,457/sm when 10%-30% paid, the rest payable

with 0% interest rate • Free parking• Furniture package• Gym free for 1 year

g p $ , $ ,

• Good payment terms: 50% hand-over, the rest payable in 2 years with 0%

Happy Valley – District 7

Sunrise City (North) – District 7

• 554 units• Current asking price: $1,119 - $1,428/sm

• Smaller unit size, lower price than P1,

ppy y

• 541 units• Current asking price: $1,500 - $1,700 /sm

• Longest payment schedule (30 months) in PMH NUA

F ki

19 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

• Good payment terms (54 months) –Central towers

• Free parking

Source: CBRE

MORE DEVELOPER CONFIDENCEMore launches coupled with more advertising activities

Units Launched by Year “y

15,000

20,000

nit

Annual launch Q2 launchNew launches increased by 51.0% q-o-q and 234.5% y-o-y y.

”Source: CBRE

Residential Projects Advertised, HCMC, 20135,000

10,000

,

Num

ber o

f U

20

25

30

t

02008 2009 2010 2011 2012 2013

5

10

15

No

of P

roje

ct

“ Some delayed projects were resumed and introduced to the market: PetroVietnam Landmark (D2), New Pearl (D3) Central Plaza (Tan Binh)

0

5

March April May June MTD July

Tracked on: Tuoi Tre; Mua & Ban; Tap chi Bat Dong San (Property

Pearl (D3), Central Plaza (Tan Binh). Others starting to prepare for construction or launch. ”

20 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

Tracked on: Tuoi Tre; Mua & Ban; Tap chi Bat Dong San (Property Magazine); Thanh Nien; Nhip Cau Dau Tu; Doanh nhan Sai Gon; Saigon Times Daily; Vietnam Investment Review; Vietnam News.

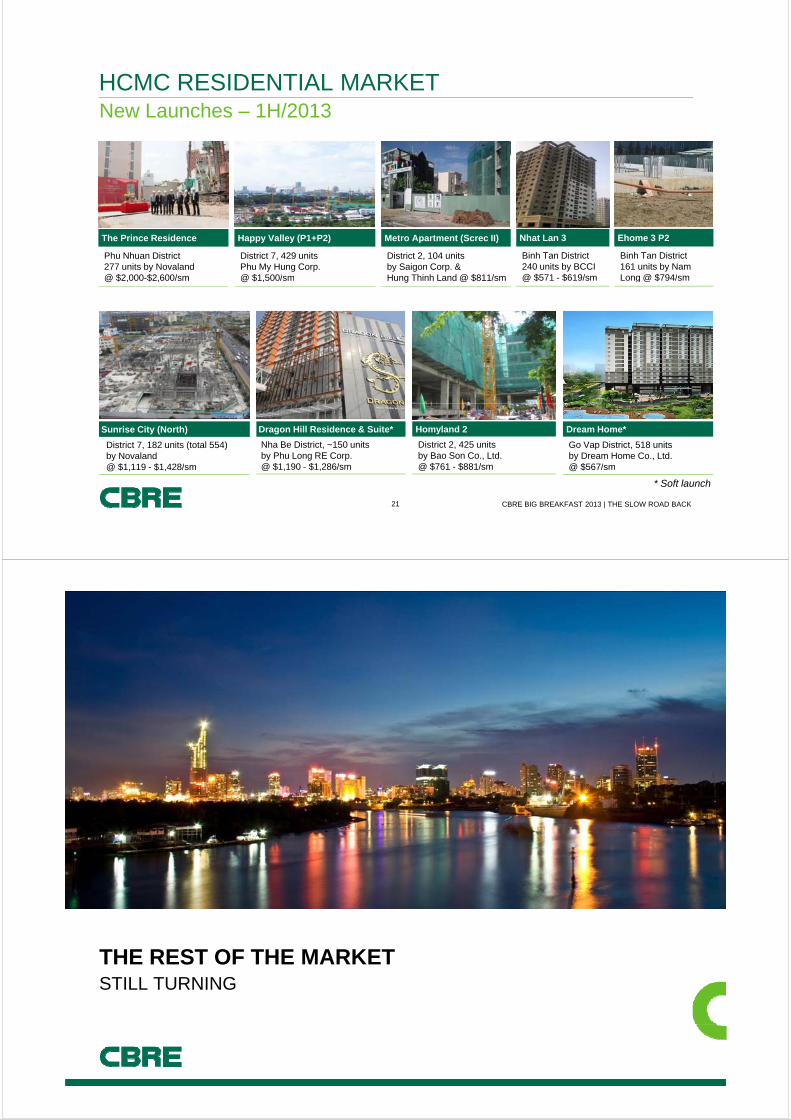

HCMC RESIDENTIAL MARKETNew Launches – 1H/2013

The Prince Residence

Phu Nhuan District277 units by Novaland@ $2 000-$2 600/sm

Happy Valley (P1+P2)

District 7, 429 unitsPhu My Hung Corp.@ $1 500/sm

Metro Apartment (Screc II)

District 2, 104 unitsby Saigon Corp. & Hung Thinh Land @ $811/sm

Nhat Lan 3

Binh Tan District240 units by BCCI@ $571 - $619/sm

Ehome 3 P2

Binh Tan District161 units by Nam Long @ $794/sm@ $2,000 $2,600/sm @ $1,500/sm Hung Thinh Land @ $811/sm @ $571 $619/sm Long @ $794/sm

Sunrise City (North)

District 7, 182 units (total 554)by Novaland@ $1 119 $1 428/sm

Dragon Hill Residence & Suite*

Nha Be District, ~150 units by Phu Long RE Corp. @ $1 190 $1 286/sm

Homyland 2

District 2, 425 units by Bao Son Co., Ltd.@ $761 $881/sm

Dream Home*

Go Vap District, 518 units by Dream Home Co., Ltd. @ $567/sm

21 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

@ $1,119 - $1,428/sm @ $1,190 - $1,286/sm @ $761 - $881/sm @ $567/sm

* Soft launch

THE REST OF THE MARKETTHE REST OF THE MARKETSTILL TURNING

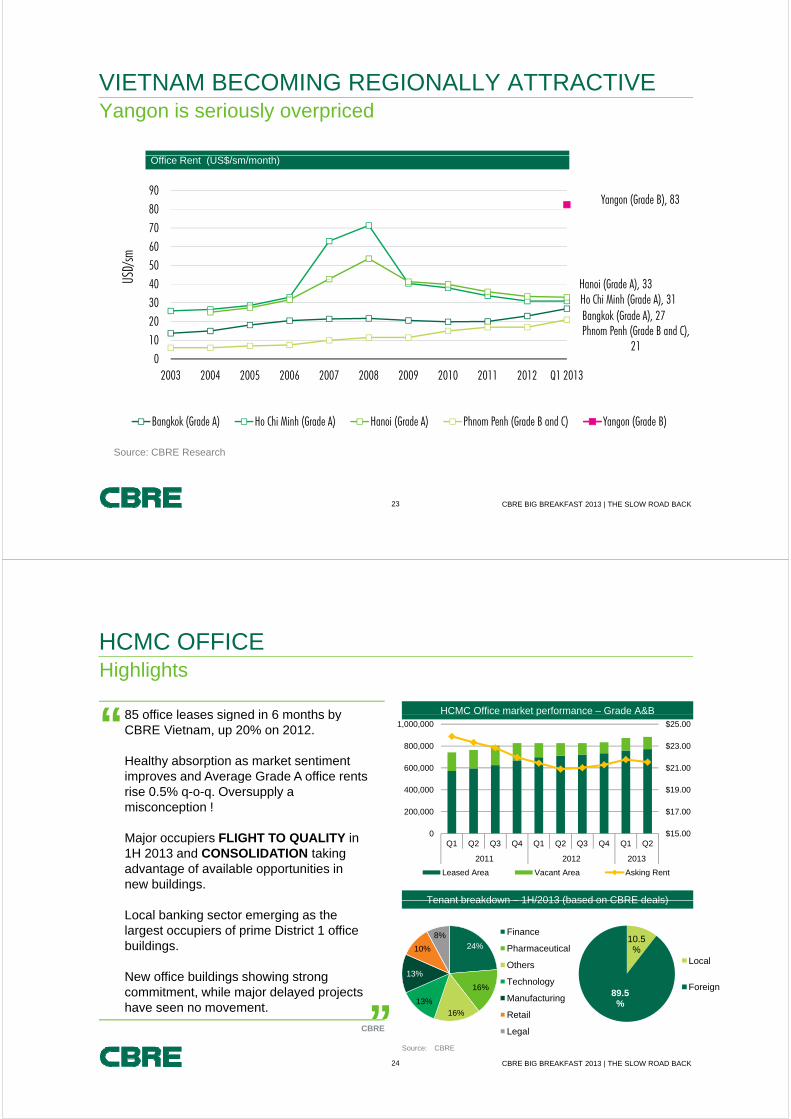

VIETNAM BECOMING REGIONALLY ATTRACTIVEYangon is seriously overpriced

Yangon (Grade B), 838090

Office Rent (US$/sm/month)

H (G d A) 3340506070

USD/

sm

Bangkok (Grade A), 27Ho Chi Minh (Grade A), 31Hanoi (Grade A), 33

Phnom Penh (Grade B and C), 2110

203040U

210

10

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Q1 2013

Bangkok (Grade A) Ho Chi Minh (Grade A) Hanoi (Grade A) Phnom Penh (Grade B and C) Yangon (Grade B)

Source: CBRE Research

23 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

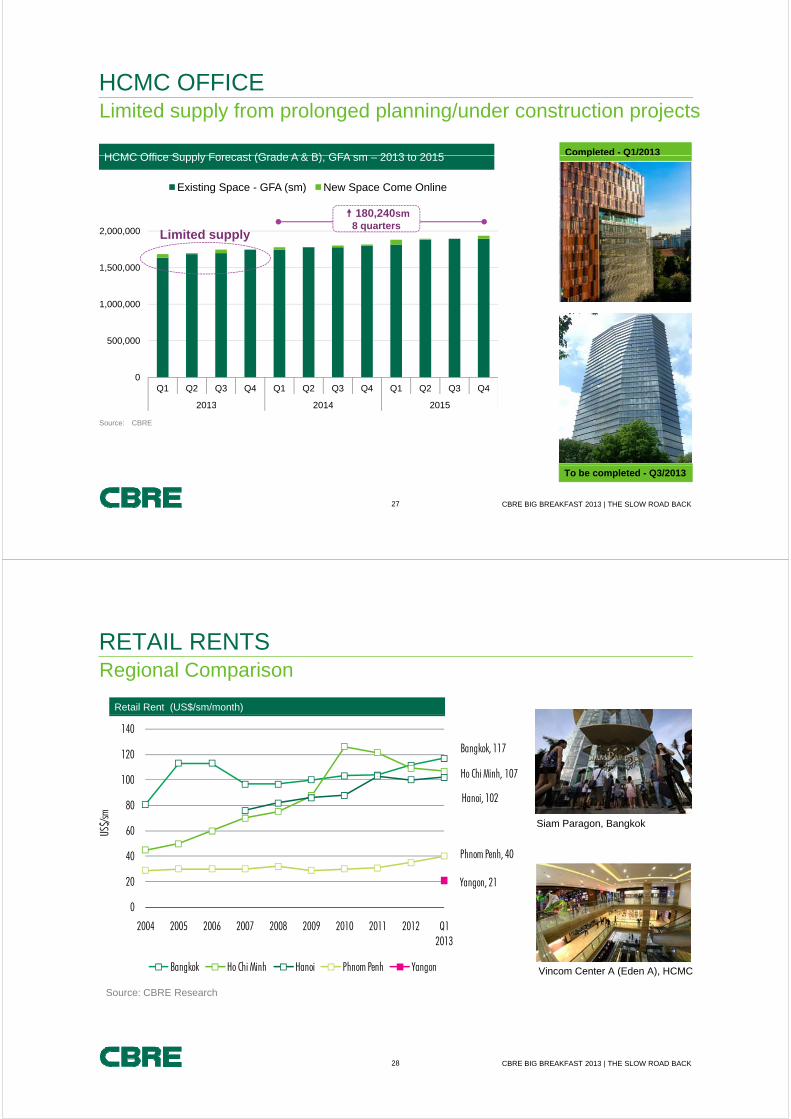

HCMC OFFICEHighlights

“85 office leases signed in 6 months by HCMC Office market performance – Grade A&B“85 office leases signed in 6 months by CBRE Vietnam, up 20% on 2012.

Healthy absorption as market sentiment improves and Average Grade A office rents

$21.00

$23.00

$25.00

600,000

800,000

1,000,000

p

improves and Average Grade A office rents rise 0.5% q-o-q. Oversupply a misconception !

Major occupiers FLIGHT TO QUALITY in $15.00

$17.00

$19.00

0

200,000

400,000

Major occupiers FLIGHT TO QUALITY in 1H 2013 and CONSOLIDATION taking advantage of available opportunities in new buildings.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2011 2012 2013

Leased Area Vacant Area Asking Rent

Tenant breakdown – 1H/2013 (based on CBRE deals)

Local banking sector emerging as the largest occupiers of prime District 1 office buildings. 24%10%

8% Finance

Pharmaceutical

Oth

Tenant breakdown – 1H/2013 (based on CBRE deals)

10.5%

Local

New office buildings showing strong commitment, while major delayed projects have seen no movement. ”

16%

16%13%

13%Others

Technology

Manufacturing

Retail

89.5%

Local

Foreign

24 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

CBRE Legal

Source: CBRE

HCMC OFFICEOversupply is beginning to disappear

“ Number of successful deals during the first half of 2013 done by CBRE Vi t t 20% 2012Vietnam went up 20% on 2012.

”CBRE

Office Vacancy Spaces – NLA (sm) Office net absorption (Grade A &B) – NLA (sm)

40%

Grade A Grade B

50,000

60,000

Grade B Grade A

0%

10%

20%

30%

10 000

20,000

30,000

40,000

50,000

0%Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2011 2012 2013

-

10,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2011 2012 2013

Source: CBRE

25 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

HCMC OFFICEPresident Place - LEED Office building achieved noticeable performance

Key facts

More than 75% of total space occupied after 3 months of official opening with the remaining 25% under offer

100% of Tenants are multinational organisations, with 66% of committed i t h l b d li toccupiers technology based clients

Key tenants:

• Canon

• Diageo Vietnam LimitedDiageo Vietnam Limited

• Microsoft Vietnam LLC

• Schindler Vietnam

“ A pioneering office development becoming Ho Chi Minh City's first LEED Gold accredited office building.

President Place

Developer Sapphire Vietnam

Point of difference is key ”Address 93 Nguyen Du, D1

Total GFA 11,475 sm

Note: Leadership in Energy and Environmental Design (LEED) consists of a suite of rating systems for the design, construction and operation of high performance green buildings homes and neighborhoods

26 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

of high performance green buildings, homes and neighborhoods.

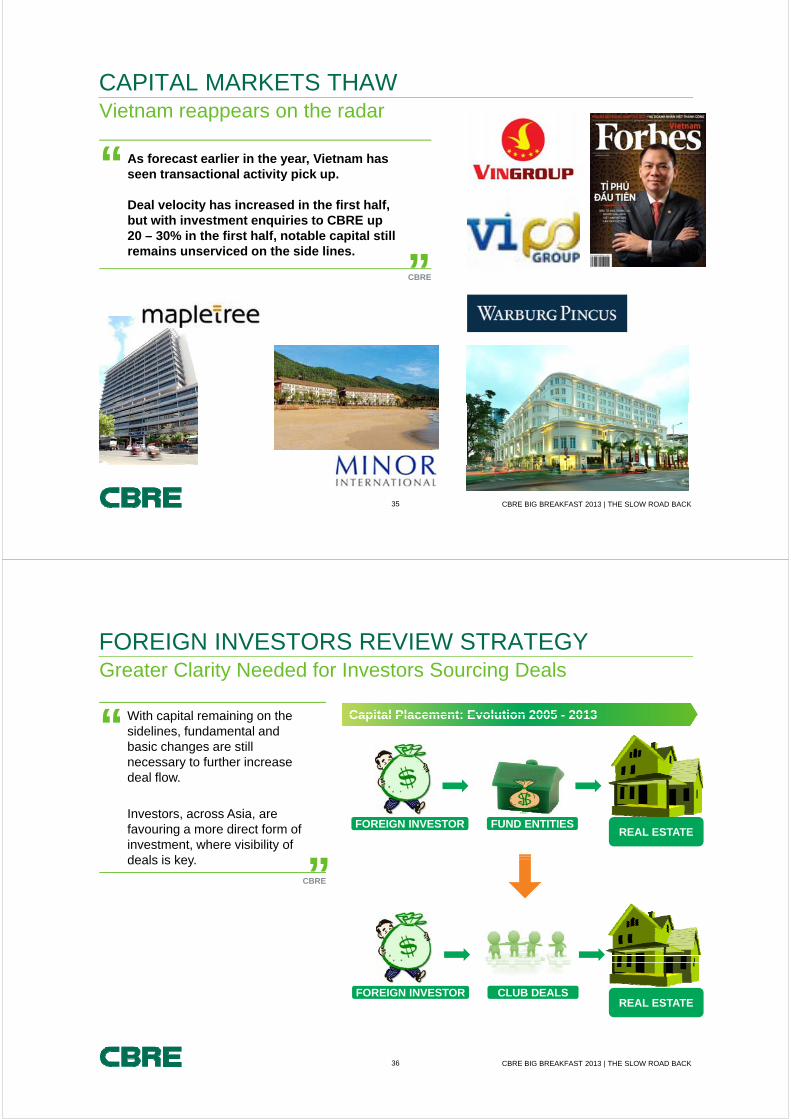

HCMC OFFICELimited supply from prolonged planning/under construction projects

HCMC Office Supply Forecast (Grade A & B) GFA sm 2013 to 2015 Completed - Q1/2013

Existing Space - GFA (sm) New Space Come Online

HCMC Office Supply Forecast (Grade A & B), GFA sm – 2013 to 2015 p Q

180,240sm

1,500,000

2,000,000 Limited supply

,8 quarters

500 000

1,000,000

0

500,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 20152013 2014 2015

Source: CBRE

27 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

To be completed - Q3/2013

RETAIL RENTSRegional Comparison

Retail Rent (US$/sm/month)

Bangkok, 117

Ho Chi Minh, 107100

120

140

Siam Paragon, Bangkok

Ho Chi Minh, 107

Hanoi, 102

60

80

100

US$/

sm

Phnom Penh, 40

Yangon, 2120

40

0

2004 2005 2006 2007 2008 2009 2010 2011 2012 Q1 2013

B k k H Ch M h H Ph P h Y

Source: CBRE Research

Vincom Center A (Eden A), HCMCBangkok Ho Chi Minh Hanoi Phnom Penh Yangon

28 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

ASIAN RETAIL

Asia Pacific will continue to

Retailer Expansion: Asia is Not Easy but Still THE Strategy

Top Cities for New Retailer Entries, 2012

drive global retail growth in 2013.

Slower economic growth posesSlower economic growth poses significant obstacles for retailers planning to expand.

Source: CBRE Global Research & Consulting

2013 50th store opening

29 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

Source: CBRE Global Research & Consulting

HCMC RETAILTaxation and Infrastructure Create Cost Burdens Restricting Both Retailers & ConsumersNet absorption (NLA, sm)

23%60 000

Net Absorption (sm) Vacancy Rate (%)

17%

23%

40,000

60,000

11%20,000

-1%

5%

-20,000

02010 2011 2012 2013

S CBRE

-7%-40,000

,

30 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

Source: CBRE

HCMC RETAILBusy High-street Leasing

“ The retail market is still driven by high street“ The retail market is still driven by high-street leasing due to ready availability. Retail is constrained by infrastructure, mass public transport that generates foot traffic.

”Number of shop houses for

l 1H/2012 2H/2012 1H/2013

”CBRE

lease 1H/2012 2H/2012 1H/2013

Hai Ba Trung 10 8 10

Mac Thi Buoi 4 1 2

Le Loi 3 4 4

Nguyen Trai 7 5 8

Cao Thang 3 2 2

Vo Van Tan 3 6 5

31 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

HOTELRegional Comparison

Hotel ADR (US$)

Yangon 235250

300

( )

Ho Chi Minh, 135*Phnom Penh, 150

Yangon, 235

150

200

S$)

Bangkok, 108,

Hanoi, 103

50

100ADR (

US

02006 2007 2008 2009 2010 2011 2012 Q1 2013

Bangkok Ho Chi Minh Hanoi Phnom Penh Yangon

Source: CBRE Research

32 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

HOTELFlurry of Construction Activity at Significant Projects

PULLMAN148 Tran Hung Dao, D1No. of rooms: 350 Completion: 2014

LIBERTY CENTRAL RIVERSIDE17 Ton Duc Thang, D1No. of rooms: 170 Completion: Q4/2013

p

SENLA BOUTIQUE HOTEL111 Hai Ba Trung, D1No. of rooms: 60 Completion: 2014

SAIGON HOTEL41 – 47 Dong Du, D1No. of rooms: 100Completion: 2014

33 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

HOTEL

Budget hotels are still a favourable choice

1H 2013 – an enjoyable season for budget hotels

gfor tourist arrivals the city given the spending power of tourists.

Budget hotels within the CBD, particularly 2-3 star hotels around Ben Thanh Market, enjoyed a very good season with average occupancy rate around 80%.

International tourist arrivals to HCMC in 1H 2013: 2 million, up 5% y-o-y.

N f 3 t h t l 1H/2013 2012No. of 3-star hotels 1H/2013 2012

Ly Tu Trong 10 8

Le Thanh Ton 9 6

Thi Sach 8 6

Le Anh Xuan 3 2

34 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

CAPITAL MARKETS THAWVietnam reappears on the radar

“A f t li i th Vi t h“ As forecast earlier in the year, Vietnam has seen transactional activity pick up.

Deal velocity has increased in the first half, b t ith i t t i i t CBREbut with investment enquiries to CBRE up 20 – 30% in the first half, notable capital still remains unserviced on the side lines.

”CBRECBRE

35 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

FOREIGN INVESTORS REVIEW STRATEGYGreater Clarity Needed for Investors Sourcing Deals

Capital Placement: Evolution 2005 - 2013“With capital remaining on the Capital Placement: Evolution 2005 - 2013“With capital remaining on the sidelines, fundamental and basic changes are still necessary to further increase deal flowdeal flow.

Investors, across Asia, are favouring a more direct form of FUND ENTITIESFOREIGN INVESTOR

REAL ESTATEinvestment, where visibility of deals is key. ”CBRE

CLUB DEALSFOREIGN INVESTORREAL ESTATE

36 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

DOMESTIC PLAYERS NEED TO FORGET 2005Quite simply - It is called Investment, not Charity

Foreign investors are not here VALUATIONgto make you rich!

The big four questions still remain– without a realistic andremain without a realistic and honest approach to these, foreigners will look elsewhere.

TRANSPARENCY STRUCTURING TRACK RECORD

37 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

CBRE’S FORECASTS - 2H 2013

After several years of hurt, Vietnam shows opportunity and return….;

From our Crystal Ball

y pp y

• (Unfortunately, where ever there is a winner, there will always be a loser)

Residential Real Estate again becomes attractive to Vietnamese investors as th lt ti ( ld t k k t d it t ) ff li it d tother alternatives (gold, stock market, deposit accounts) offer limited returns;

• By the 2014 Fearless Forecast – the residential market will have passed the bottom

As Andy Murray will testify, a win does not come easily;

• Those already committed to Vietnam, still have many battles to survive;

• Particularly for residential developers, flexibility will still be the key for success – buyers still need to be nurtured;

38 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

CBRE’S FORECASTS – 2H 2013

The next round of interest cuts proves to be one of the most decisive in

A Few More Thoughts….

The next round of interest cuts proves to be one of the most decisive in improving residential purchaser sentiment;

“Middle-class” housing projects, such as those seen on the Hanoi Highway in District 2, will see over 50% of the lights switched on by year end;

Grade A office rents finish the year unchanged or slightly up as vacancy drops below 10% and new options on the horizon look slim;p ;

High street corners to become further dominated by foreign brands looking to expand their foot print;

Investment deal flows continues to be at heightened levels as in the first half;

• However, many foreign investors still fly out of Vietnam without their wallets having been opened;g p ;

• Vietnam upgraded from completely toxic to just toxic; however further upgrades expected later this year.

39 CBRE BIG BREAKFAST 2013 | THE SLOW ROAD BACK

CBRE QUARTERLY REPORTAvailable now with new pricing options,

longer historical data and more in-depth analysis.l @ b [email protected]

For more information regarding this presentation please contact:MARC TOWNSENDManaging DirectorT +84 8 3824 6125F +84 8 3823 8418Email: [email protected]