Copyright © 2016 by McGraw-Hill Education Chapter 8 Receivables, Bad Debt Expense, and Interest...

66

Copyright © 2016 by McGraw-Hill Education Chapter 8 Receivables, Bad Debt Expense, and Interest Revenue PowerPoint Author: Brandy Mackintosh, CA

-

Upload

brittney-perkins -

Category

Documents

-

view

253 -

download

1

Transcript of Copyright © 2016 by McGraw-Hill Education Chapter 8 Receivables, Bad Debt Expense, and Interest...

Copyright © 2016 by McGraw-Hill Education

Chapter 8Receivables, Bad Debt Expense, and Interest Revenue

PowerPoint Author:Brandy Mackintosh, CA

8-2

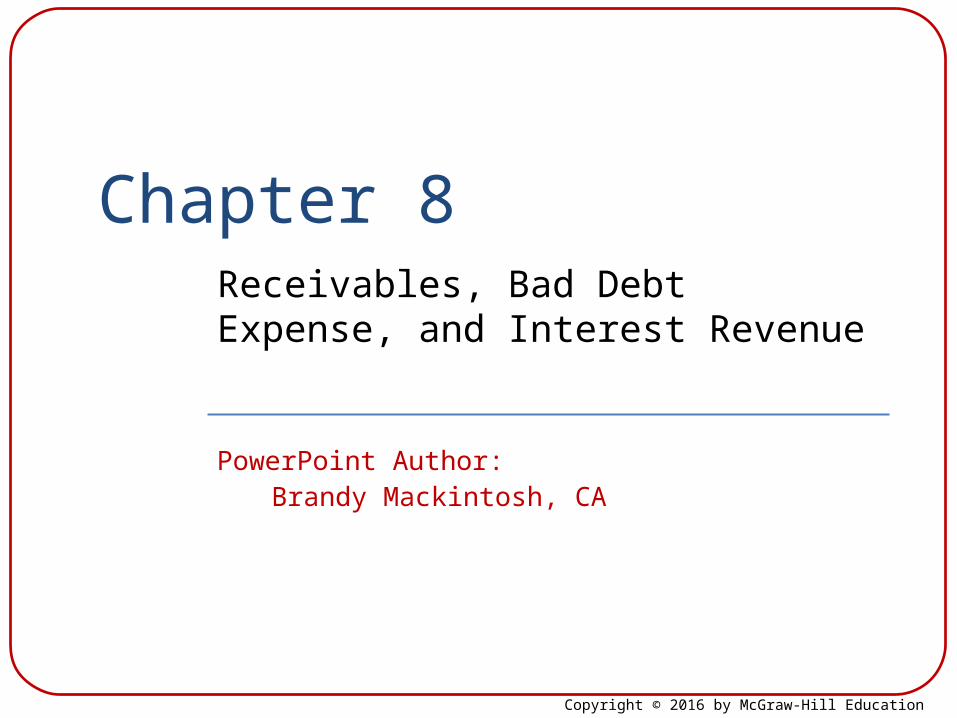

Learning Objective 8-1

Describe the trade-offs of extending credit.

8-3

Pros and Cons of Extending Credit

Disadvantages

1. Increased wage costs.

2. Bad debt costs.

3. Delayed receipt of cash.

Advantage

1. Increases the seller’s revenues.

8-4

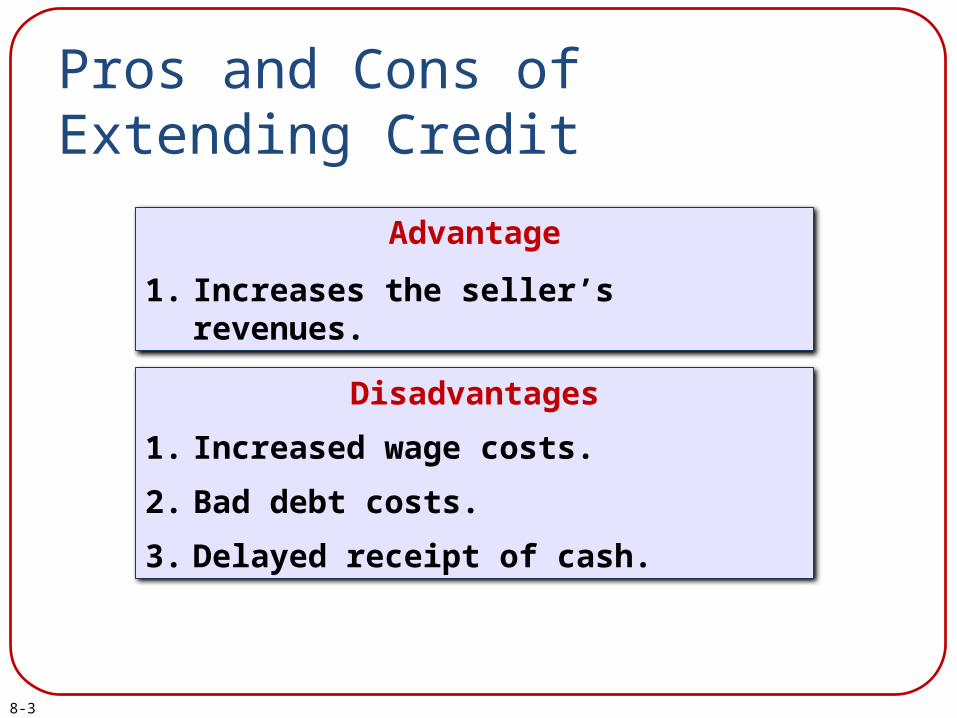

Learning Objective 8-2

Estimate and report the effects of uncollectible accounts.

8-5

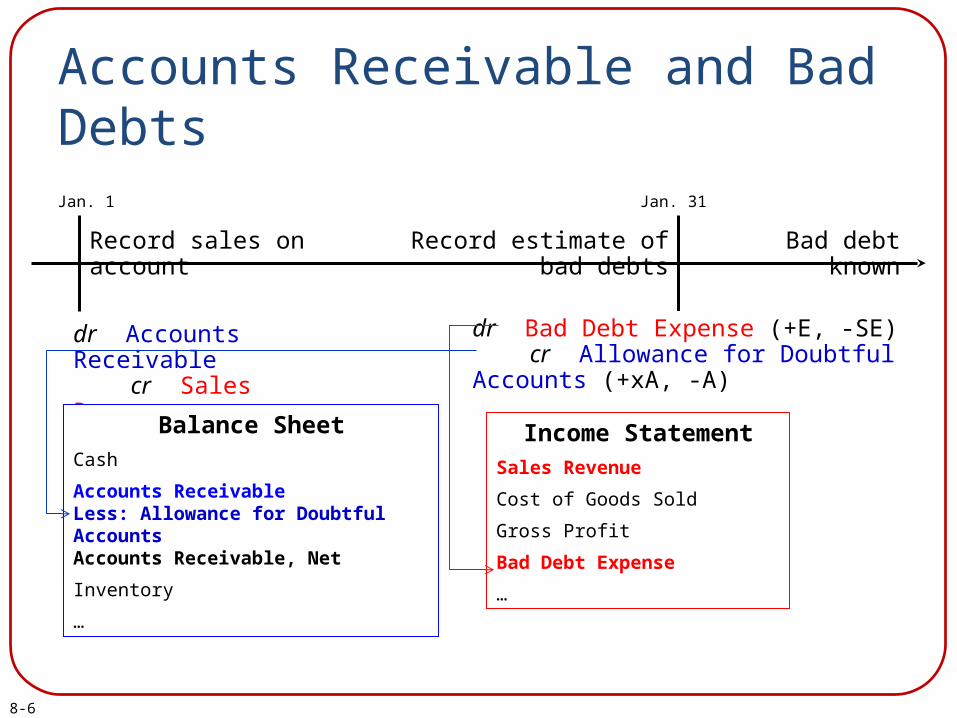

Record sales on account

dr Accounts Receivable cr Sales Revenue

Balance SheetCash

Accounts Receivable

Inventory

…

Income StatementSales Revenue

Cost of Goods Sold

Gross Profit

…

Bad debt known

Accounts Receivable and Bad Debts

Jan. 1

8-6

Record sales on account

dr Accounts Receivable cr Sales Revenue

Balance SheetCash

Accounts Receivable

Inventory

…

Income StatementSales Revenue

Cost of Goods Sold

Gross Profit

…

Bad debt known

Balance SheetCash

Accounts ReceivableLess: Allowance for Doubtful AccountsAccounts Receivable, Net

Inventory

…

Income StatementSales Revenue

Cost of Goods Sold

Gross Profit

Bad Debt Expense

…

Accounts Receivable and Bad Debts

Record estimate of bad debts

Jan. 1 Jan. 31

dr Bad Debt Expense (+E, -SE) cr Allowance for Doubtful Accounts (+xA, -A)

8-7

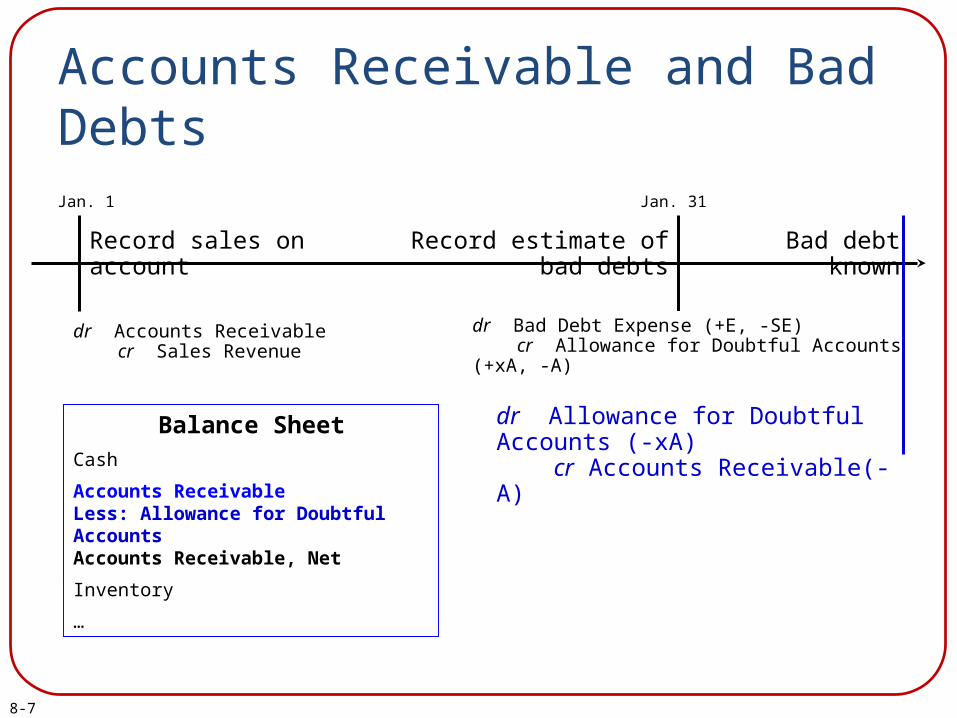

Record sales on account

dr Accounts Receivable cr Sales Revenue

Balance SheetCash

Accounts Receivable

Inventory

…

Bad debt known

Balance SheetCash

Accounts ReceivableLess: Allowance for Doubtful AccountsAccounts Receivable, Net

Inventory

…

Accounts Receivable and Bad Debts

Record estimate of bad debts

Jan. 1 Jan. 31

dr Bad Debt Expense (+E, -SE) cr Allowance for Doubtful Accounts (+xA, -A)

dr Allowance for Doubtful Accounts (-xA) cr Accounts Receivable(-A)

8-8

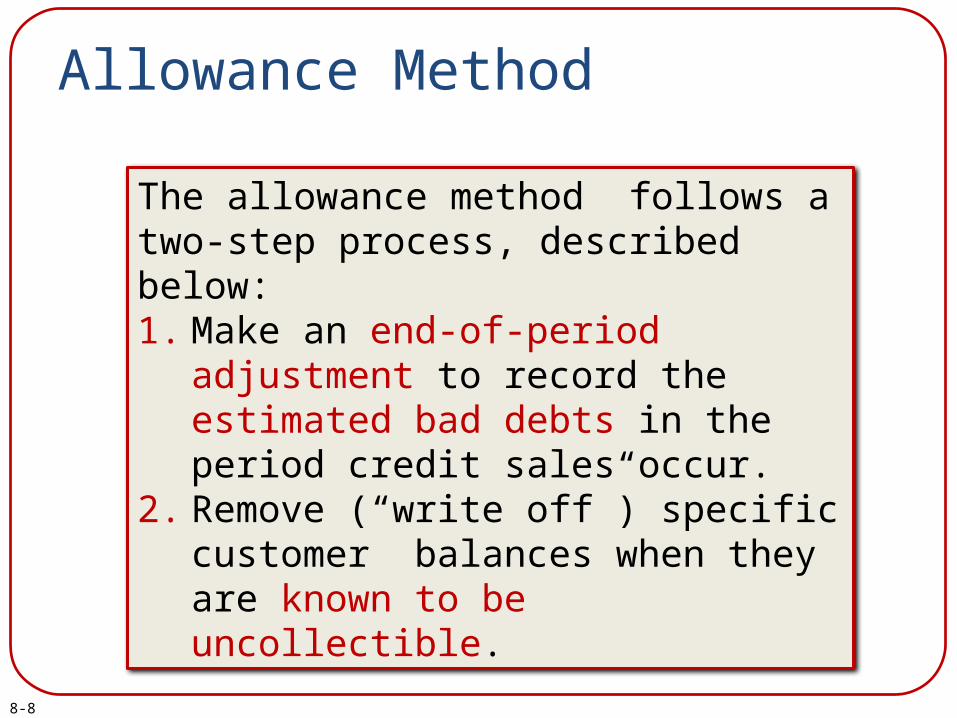

Allowance Method

The allowance method follows a two-step process, described below:1. Make an end-of-period adjustment to

record the estimated bad debts in the period credit sales occur.

2. Remove (“write off”) specific customer balances when they are known to be uncollectible.

8-9

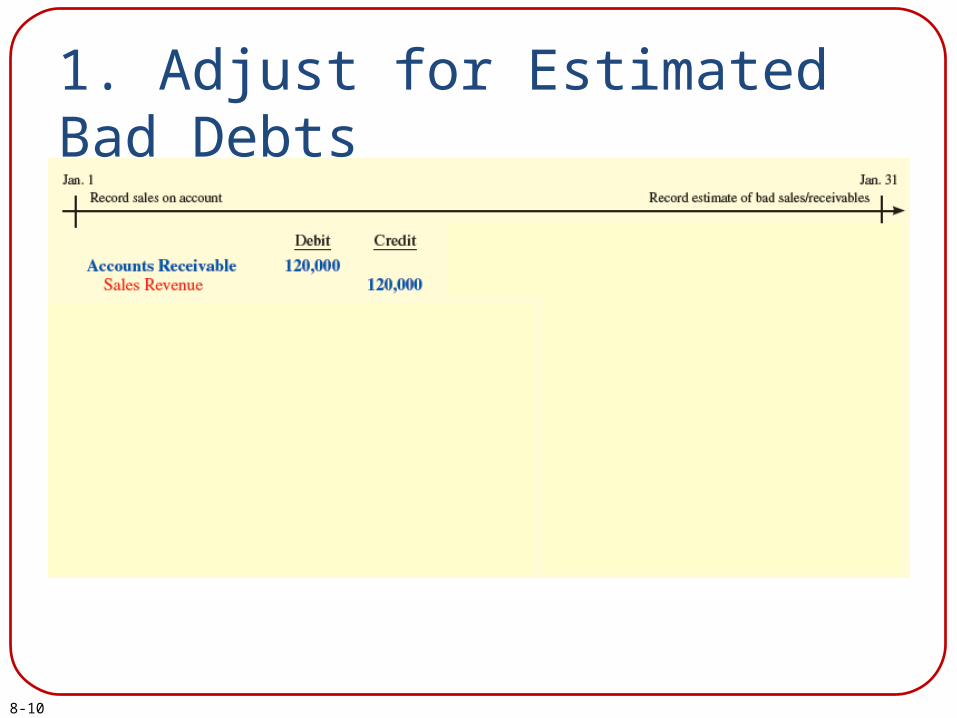

1. Adjust for Estimated Bad DebtsAssume that VFC estimates $900 in bad debts at

the end of the accounting period.

1 AnalyzeLiabilitiesAssets = Stockholders’ Equity+

Allowance for Doubtful Accounts (+xA) -900

Bad DebtExpense (+E) -900

2 Record

Bad Debt Expense Allowance for Doubtful Accounts (+xA) 900

900

8-10

1. Adjust for Estimated Bad Debts

8-11

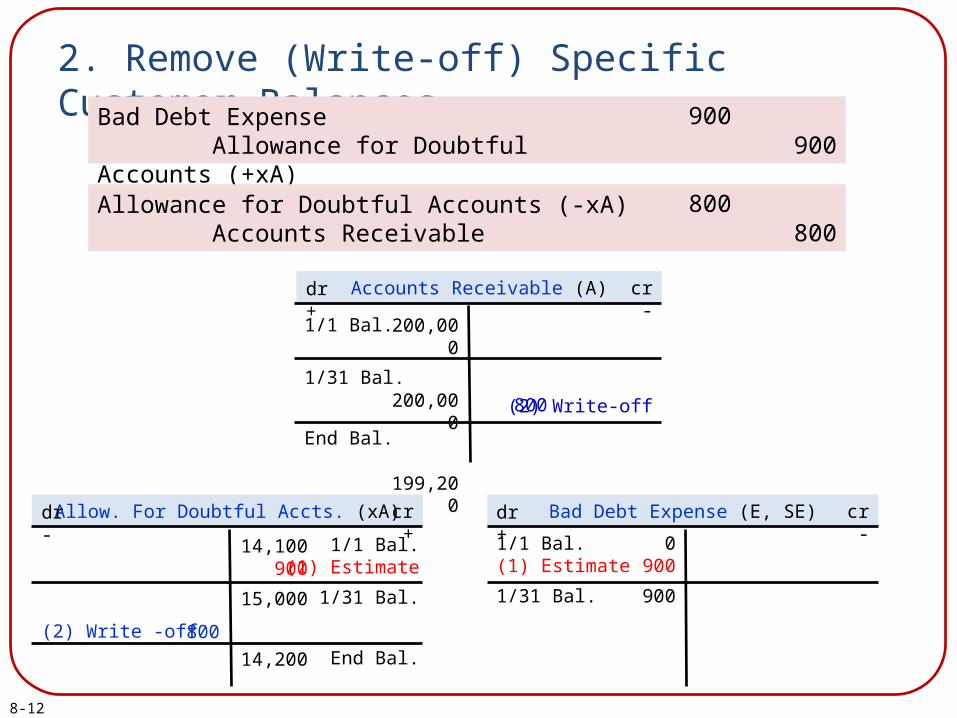

2. Remove (Write-off) Specific Customer Balances

VFC writes off an $800 receivable from Fast Fashions because the company could not pay its account.

1 AnalyzeLiabilitiesAssets = Stockholders’ Equity+

Accounts Receivable -800Allowance for DoubtfulAccounts (-xA) +800

2 Record

Allowance for Doubtful Accounts (-xA) Accounts Receivable 800

800

8-12

2. Remove (Write-off) Specific Customer Balances

Bad Debt Expense Allowance for Doubtful Accounts (+xA) 900

900

Allowance for Doubtful Accounts (-xA) Accounts Receivable 800

800

1/1 Bal.

1/31 Bal.

End Bal.

(2) Write-off

Accounts Receivable (A)dr + cr -

200,000

200,000

199,200

800

(2) Write -off

1/1 Bal.(1) Estimate

1/31 Bal.

End Bal.

Allow. For Doubtful Accts. (xA)dr - cr +

800

14,100900

15,000

14,200

1/1 Bal.(1) Estimate

1/31 Bal.

Bad Debt Expense (E, SE)dr + cr -

0900

900

8-13

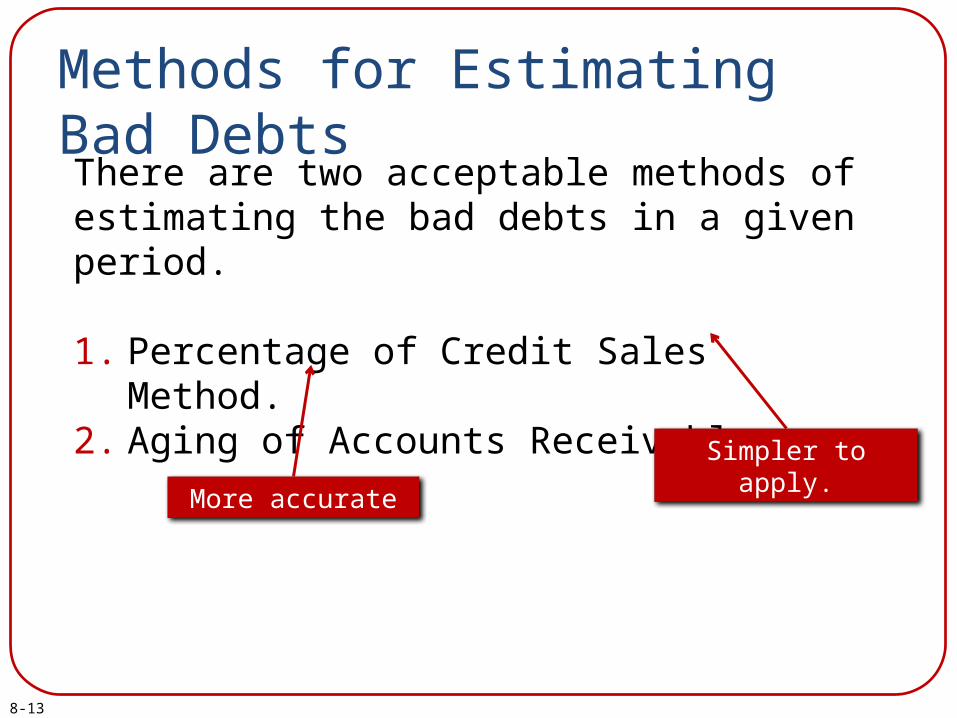

Methods for Estimating Bad Debts

There are two acceptable methods of estimating the bad debts in a given period.

1. Percentage of Credit Sales Method.2. Aging of Accounts Receivable.

Simpler to apply.

More accurate

8-14

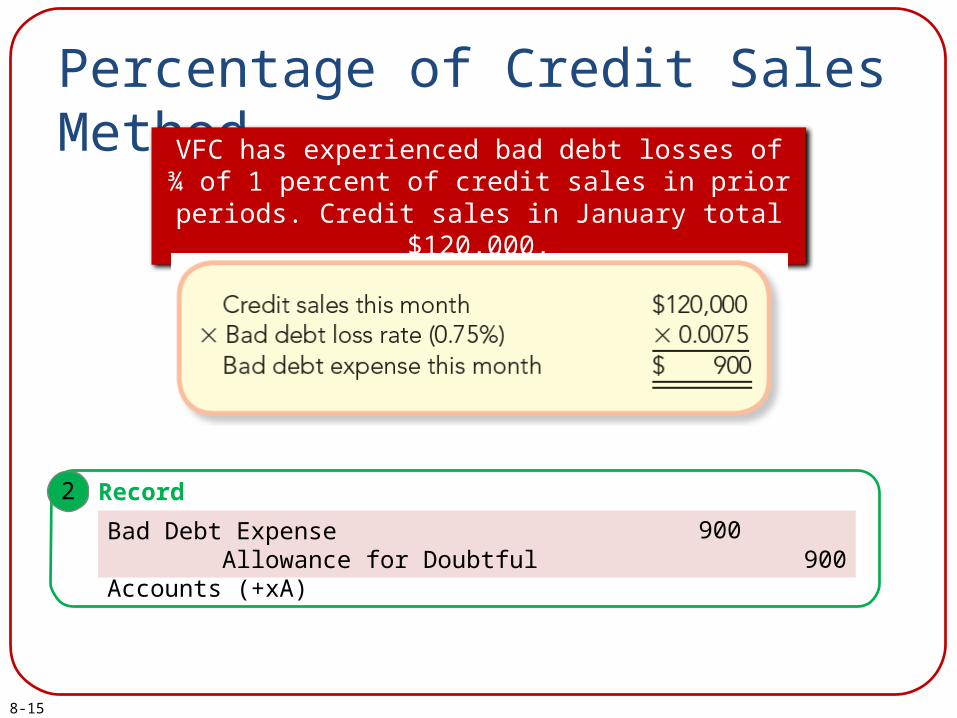

Percentage of Credit Sales Method

The percentage of credit sales method estimates bad debt expense by

multiplying the historical percentage of bad debt losses by the current period’s

credit sales.

8-15

Percentage of Credit Sales MethodVFC has experienced bad debt losses of ¾ of 1

percent of credit sales in prior periods. Credit sales in January total $120,000,

2 Record

Bad Debt Expense Allowance for Doubtful Accounts (+xA) 900

900

8-16

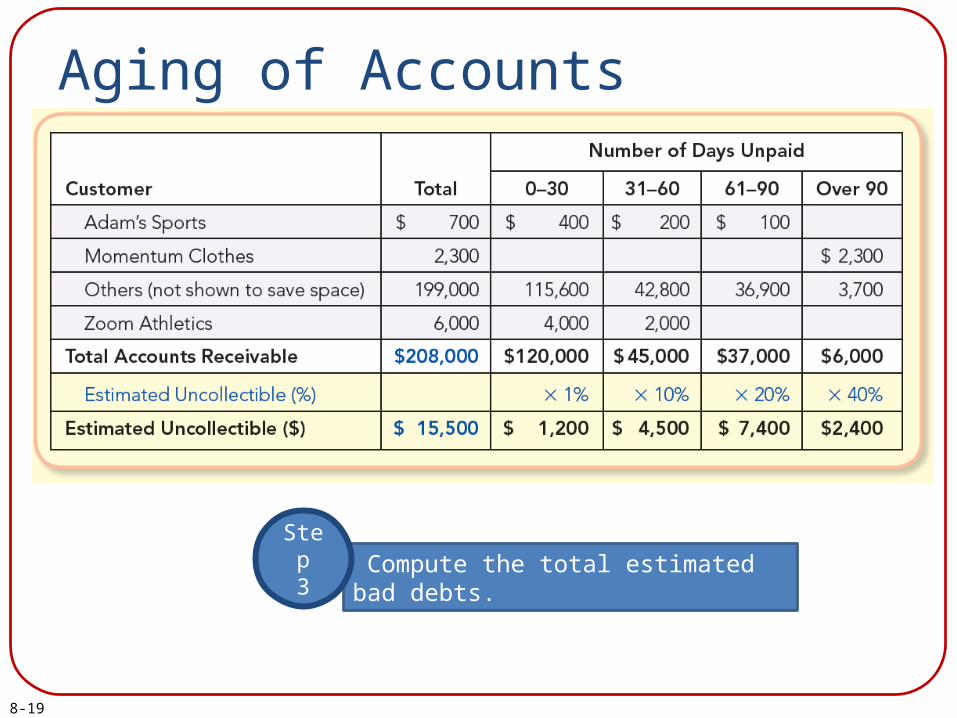

Aging of Accounts Receivable

While the percentage of credit sales method focuses on estimating Bad Debt Expense (income statement approach) for the period, the aging of accounts receivable method focuses on

estimating the ending balance in the Allowance for Doubtful Accounts (balance sheet approach).

The aging method gets its name because it is based on the “age” of each amount in Accounts Receivable at the end of the

period. The older and more overdue an account receivable becomes, the less likely it is to be collectible.

8-17

Aging of Accounts ReceivableVFC applies the aging of accounts receivable method to its Accounts

Receivable balances on February 28, after taking into account February sales and cash collections. The method includes three steps: (1) Prepare

an aged list of accounts receivable, (2) Estimate bad debt loss percentages for each category, and (3) Compute the total estimated bad

debts.

Age Accounts Receivable.Step

1

8-18

Aging of Accounts Receivable

Estimate bad debt loss percentages for each category.Step

2

8-19

Aging of Accounts Receivable

Compute the total estimated bad debts.Step

3

8-20

Aging of Accounts Receivable

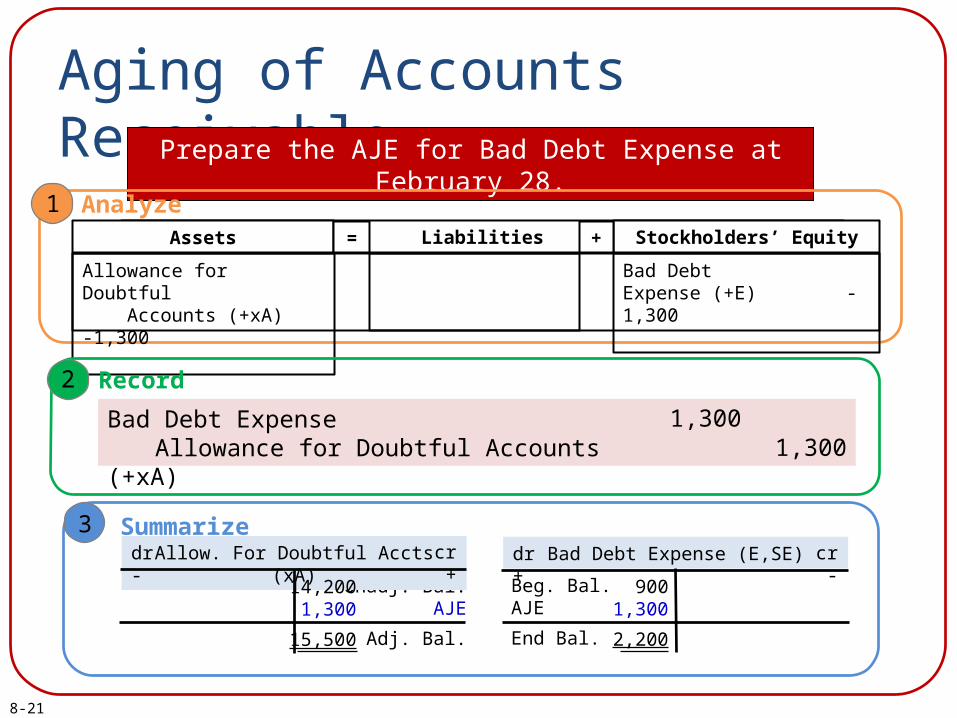

AJE = ($15,500 - $14,200) = $1,300

8-21

Aging of Accounts ReceivablePrepare the AJE for Bad Debt Expense at February 28.

1 AnalyzeLiabilitiesAssets = Stockholders’ Equity+

Allowance for Doubtful Accounts (+xA) -1,300

Bad DebtExpense (+E) -1,300

2 Record

Bad Debt Expense Allowance for Doubtful Accounts (+xA) 1,300

1,300

3 Summarize

Unadj. Bal.AJE

Adj. Bal.

Allow. For Doubtful Accts (xA)dr - cr +

14,2001,300

15,500

Beg. Bal.AJE

End Bal.

Bad Debt Expense (E,SE)dr + cr -

9001,300

2,200

8-22

Other Issues

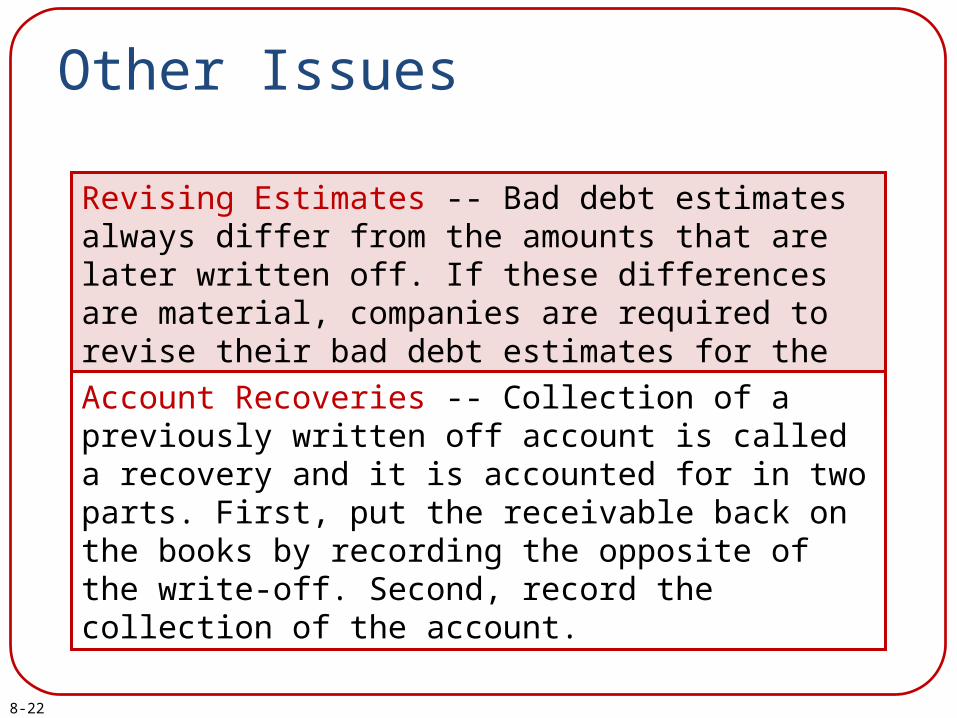

Revising Estimates -- Bad debt estimates always differ from the amounts that are later written off. If these differences are material, companies are required to revise their bad debt estimates for the current period.

Account Recoveries -- Collection of a previously written off account is called a recovery and it is accounted for in two parts. First, put the receivable back on the books by recording the opposite of the write-off. Second, record the collection of the account.

8-23

Other IssuesLet’s assume that VFC collects the $800 from Fast Fashions that was previously written off. This recovery would be recorded with the following journal entries:

(1) Reverse the write-off.

(2) Record the collection.

8-24

Learning Objective 8-3

Compute and report interest on notes receivable.

8-25

Notes Receivable and Interest Revenue

A company reports Notes Receivable if it uses a promissory note to document its right to collect money from another party.

Unlike accounts receivable, which are generally interest free, notes receivable charge interest from the day they are created to the day they are due (their maturity date).

8-26

Calculating Interest

Interest (I) = Principal (P) × Interest Rate (R) × Time (T)

The time period forinterest calculation

The amount of thenote receivable

The annual interest ratecharged on the note

8-27

Recording Notes Receivable and Interest Revenue

The four key events that occur with any note receivable are:

12

3

4

Date of Note Receivable November 1, 2015Annual Interest Rate 6%Amount of the Note $100,000Maturity Date of Note October 31, 2016Year End of Company December 31, 2015

8-28

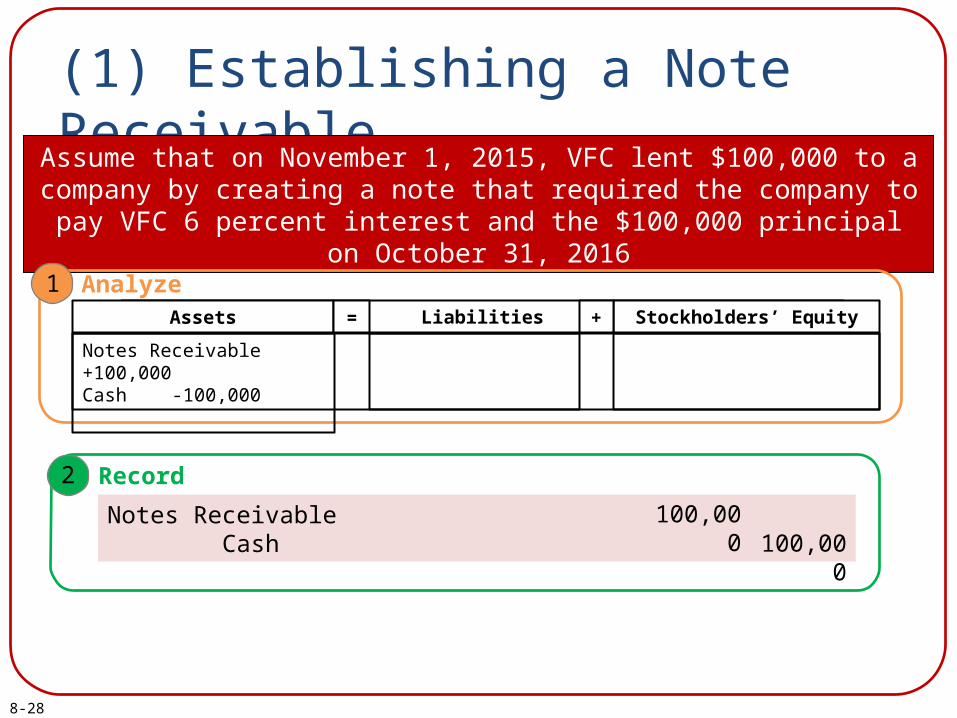

(1) Establishing a Note Receivable

Assume that on November 1, 2015, VFC lent $100,000 to a company by creating a note that required the company to pay VFC 6 percent interest

and the $100,000 principal on October 31, 2016

1 AnalyzeLiabilitiesAssets = Stockholders’ Equity+

Notes Receivable +100,000Cash -100,000

2 Record

Notes Receivable Cash 100,000

100,000

8-29

(2) Accruing Interest EarnedAccrue the interest earned at year-end, December 31, 2015.

Principal (P) × Interest Rate (R) × Time (T) = Interest (I)

$100,000 × 6% × 2/12 = $1,000

2

8-30

(2) Accruing Interest EarnedAccrue the interest earned at year-end, December 31, 2015.

1 AnalyzeLiabilitiesAssets = Stockholders’ Equity+

InterestReceivable +1,000

Interest Revenue (+R) +1,000

2 Record

Interest Receivable Interest Revenue 1,000

1,000

8-31

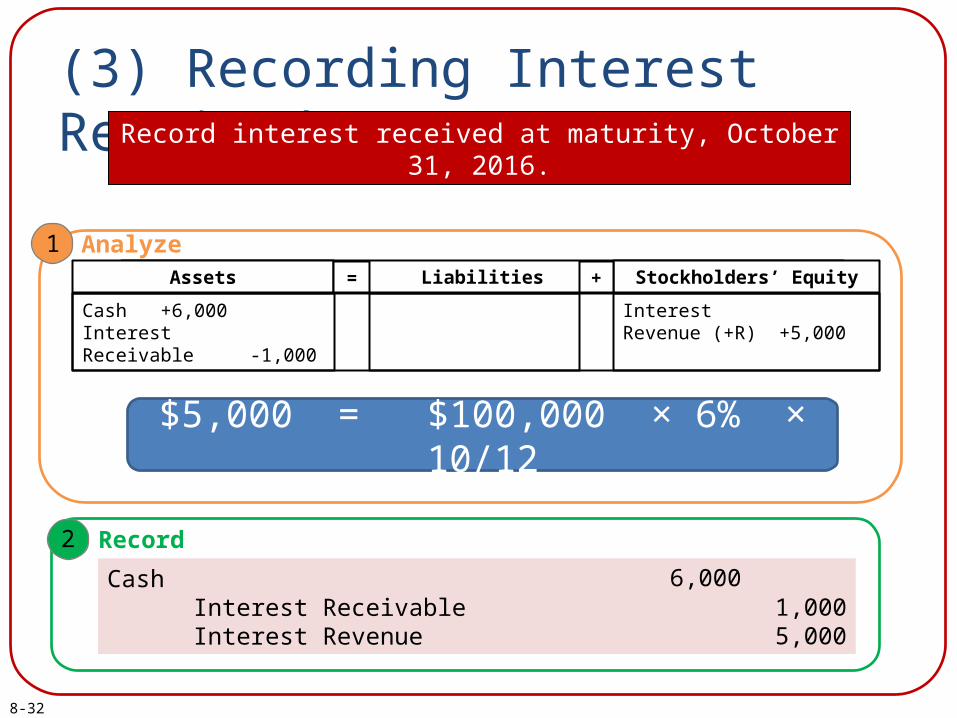

(3) Recording Interest ReceivedRecord interest received at maturity, October 31, 2016.

Principal (P) × Interest Rate (R) × Time (T) = Interest (I)

$100,000 × 6% × 12/12 = $6,000

8-32

(3) Recording Interest ReceivedRecord interest received at maturity, October 31, 2016.

2 Record

Cash Interest Receivable Interest Revenue

1,0005,000

6,000

1 AnalyzeLiabilitiesAssets = Stockholders’ Equity+

Cash +6,000 InterestReceivable -1,000

Interest Revenue (+R) +5,000

$5,000 = $100,000 × 6% × 10/12

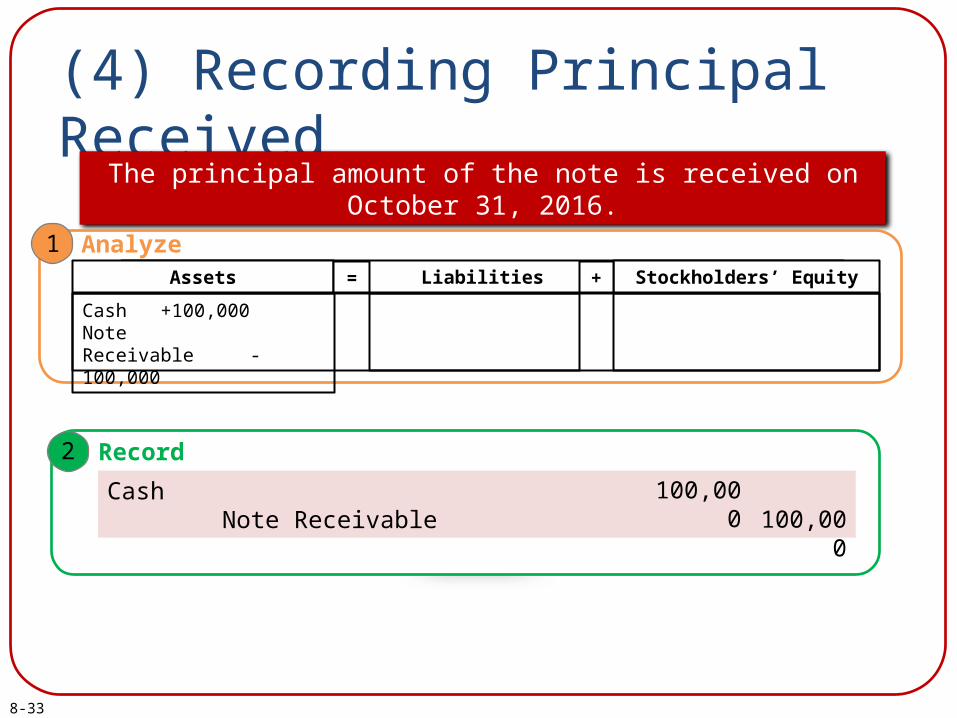

8-33

(4) Recording Principal Received

The principal amount of the note is received on October 31, 2016.

1 AnalyzeLiabilitiesAssets = Stockholders’ Equity+

Cash +100,000Note Receivable -100,000

2 Record

Cash Note Receivable 100,000

100,000

8-34

Learning Objective 8-4

Compute and interpret the receivables turnover ratio.

8-35

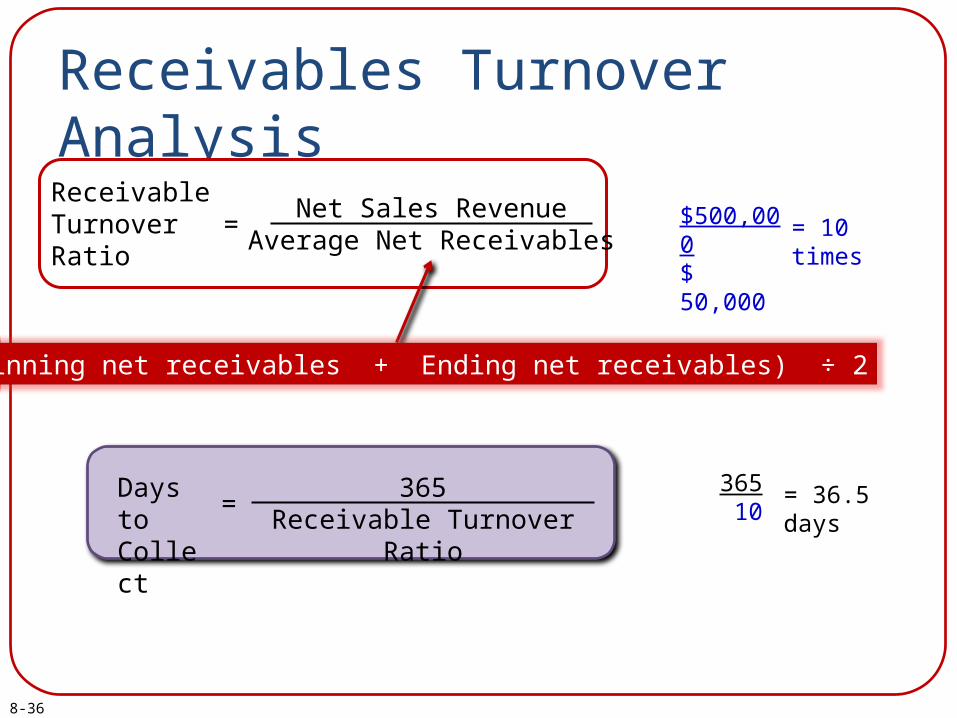

Receivables Turnover Analysis

The receivables turnover ratio indicates how many times, on average, this process of selling and collecting is repeated during the period. The higher the ratio, the faster the collection of receivables.

Rather than evaluate the number of times accounts receivable turn over, some people find it easier to think in terms of the number of days to collect receivables (called days to collect).

8-36

Receivables Turnover Analysis

ReceivableTurnoverRatio

=Net Sales Revenue

Average Net Receivables

(Beginning net receivables + Ending net receivables) ÷ 2

$500,000$ 50,000

= 10 times

Days toCollect

=365

Receivable Turnover Ratio

365 10

= 36.5 days

8-37

Comparison to BenchmarksCredit Terms

When companies sell on account, they specify the length of credit period (and any cash discounts for prompt payment). By comparing the number of days to collect to the length of credit period, you can gain a sense of whether customers are complying with the stated policy.

8-38

Speeding Up CollectionsFactoring Receivables

One way to speed up collections is to sell outstanding accounts receivable to another company (called a factor). Your company receives cash for the receivables it sells to the factor (minus a factoring fee).

Credit Card SalesAnother way to avoid lengthy collection periods is to allow customers to pay for goods using PayPal or national credit cards. This not only speeds up the seller’s cash collection, but also reduces losses from customers writing bad checks. PayPal and Credit card companies charge a fee for their services.

Copyright © 2016 by McGraw-Hill Education

Chapter 8Supplement 8A

Direct Write-Off Method

8-40

Learning Objective 8-S1

Record bad debts using the direct write-off

method.

8-41

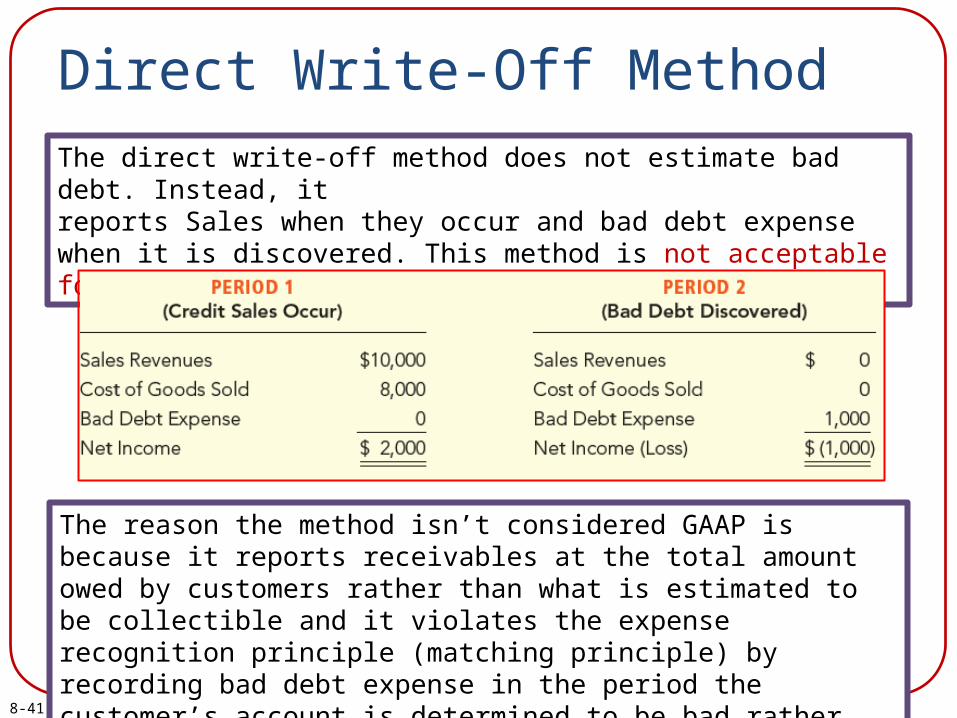

Direct Write-Off MethodThe direct write-off method does not estimate bad debt. Instead, itreports Sales when they occur and bad debt expense when it is discovered. This method is not acceptable for GAAP.

The reason the method isn’t considered GAAP is because it reports receivables at the total amount owed by customers rather than what is estimated to be collectible and it violates the expense recognition principle (matching principle) by recording bad debt expense in the period the customer’s account is determined to be bad rather than the period when the credit sales are actually made.

8-42

Direct Write-Off MethodA customer account is determined to be uncollectible and

$1,000 of Bad Debt Expense needs to be recorded.

2 Record

Bad Debt Expense Accounts Receivable 1,000

1,000

Copyright © 2016 by McGraw-Hill Education

Chapter 8Solved Exercises

M8-10, E8-7, E8-8, E8-9, CP8-4, C8-1

8-44

M8-10 Using the Interest Formula to Compute InterestComplete the following table by computing the missing amounts (?) for the following independent cases.

Case a. $100,000 × 10% × (6/12) = $5,000

Case b. $3,000 ÷ [$50,000 × (9/12)] = 8%

Case c. [$4,000 ÷ 10%] × (12/12) = $40,000

a.

b.

c.

Principal Amount of

Note Receivable

$ 100,000

$ 50,000

?

Annual

Interest Rate

10%

?

10%

Time Period

in Months

6

9

12

Interest

Earned

?

$ 3,000

$ 4,000

8-45

E8-7 Computing Bad Debt Expense Using Aging of Accounts Receivable MethodBrown Cow Dairy uses the aging approach to estimate Bad Debt Expense. The balance of each account receivable is aged on the basis of three time periods as follows: (1) 1–30 days old, $12,000; (2) 31–90 days old, $5,000; and (3) more than 90 days old, $3,000. Experience has shown that for each age group, the average loss rate on the amount of the receivable due to uncollectibility is (1) 5 percent, (2) 10 percent, and (3) 20 percent, respectively. At December 31 (end of the current year), the Allowance for Doubtful Accounts balance was $800 (credit) before the end-of-period adjusting entry is made.Required:1. Prepare a schedule to estimate an appropriate year-end balance for the

Allowance for Doubtful Accounts.2. What amount should be recorded as Bad Debt Expense for December

31?3. If the unadjusted balance in the Allowance for Doubtful Accounts was a

$600 debit balance, what amount of Bad Debt Expense should be recorded on December 31?

8-46

E8-7 Computing Bad Debt Expense Using Aging of Accounts Receivable Method

Req. 1

Total

$ 20,000

$ 1,700

>90

$ 3,000

20%

$ 600

31-90

$ 5,000

10%

$ 500

1 - 30

$ 12,000

5%

$ 600

Estimate Balance in Allowance

Existing Credit Balance in Allowance

Adjusting Journal Entry Amount

$ 1,700

800

$ 900

Req. 2 Allowance for Doubtful Accounts

800

900

1,700

Unadj. Bal.

AJE

Bal.

Req. 3 Allowance for Doubtful Accounts

2,300

1,700

AJE

Bal.

600Unadj. Bal.

8-47

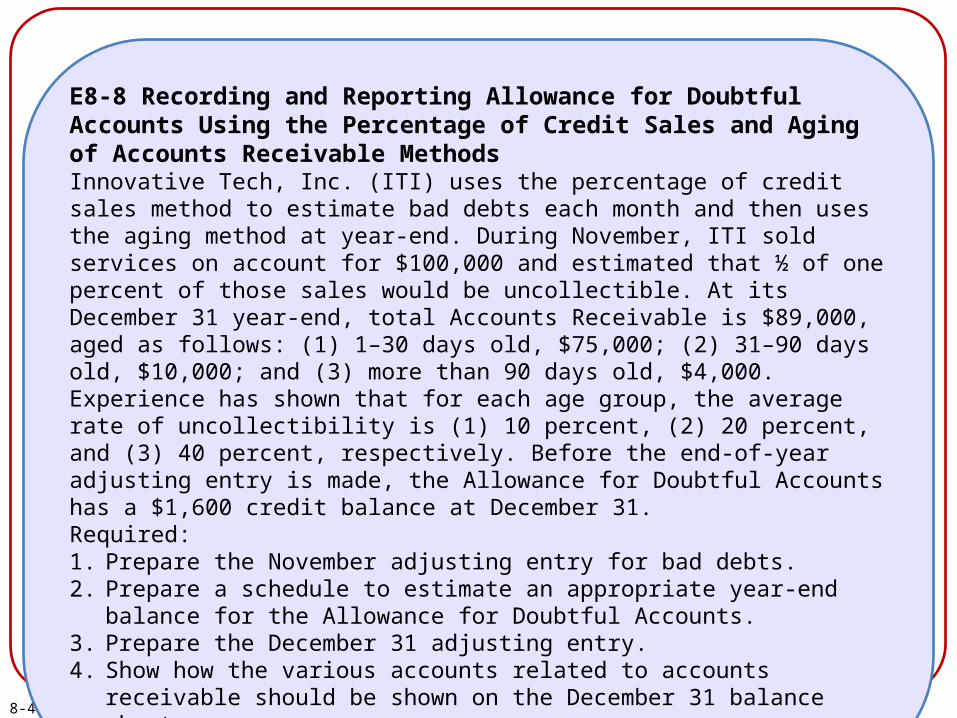

E8-8 Recording and Reporting Allowance for Doubtful Accounts Using the Percentage of Credit Sales and Aging of Accounts Receivable MethodsInnovative Tech, Inc. (ITI) uses the percentage of credit sales method to estimate bad debts each month and then uses the aging method at year-end. During November, ITI sold services on account for $100,000 and estimated that ½ of one percent of those sales would be uncollectible. At its December 31 year-end, total Accounts Receivable is $89,000, aged as follows: (1) 1–30 days old, $75,000; (2) 31–90 days old, $10,000; and (3) more than 90 days old, $4,000. Experience has shown that for each age group, the average rate of uncollectibility is (1) 10 percent, (2) 20 percent, and (3) 40 percent, respectively. Before the end-of-year adjusting entry is made, the Allowance for Doubtful Accounts has a $1,600 credit balance at December 31.Required:1. Prepare the November adjusting entry for bad debts.2. Prepare a schedule to estimate an appropriate year-end balance for the

Allowance for Doubtful Accounts.3. Prepare the December 31 adjusting entry.4. Show how the various accounts related to accounts receivable should be

shown on the December 31 balance sheet.

8-48

E8-8 Recording and Reporting Allowance for Doubtful Accounts Using the Percentage of Credit Sales and Aging of Accounts Receivable Methods

Req. 3 Allowance for Doubtful Accounts

1,600

9,500

11,100

Unadj. Bal.

AJE

Bal.

Req. 2 Total

$ 89,000

$ 11,100

>90

$ 4,000

40%

$ 1,600

31-90

$ 10,000

20%

$ 2,000

1 - 30

$ 75,000

10%

$ 7,500

Req. 1 November 30 AJE

Bad Debt Expense Allowance for Doubtful Accounts (+xA)

($500 = $100,000 x 0.005)

500500

8-49

E8-8 Recording and Reporting Allowance for Doubtful Accounts Using the Percentage of Credit Sales and Aging of Accounts Receivable Methods

Req. 4 The accounts related to the accounts receivable can be shown one of two ways on the December 31 balance sheet:

OR

Accounts Receivable

Less: Allowance for Doubtful Accounts

Accounts Receivable, net of allowance

$ 89,000

(11,100)

$ 77,900

Accounts Receivable, net of Allowance for

Doubtful Accounts of $11,100 $ 77,900

8-50

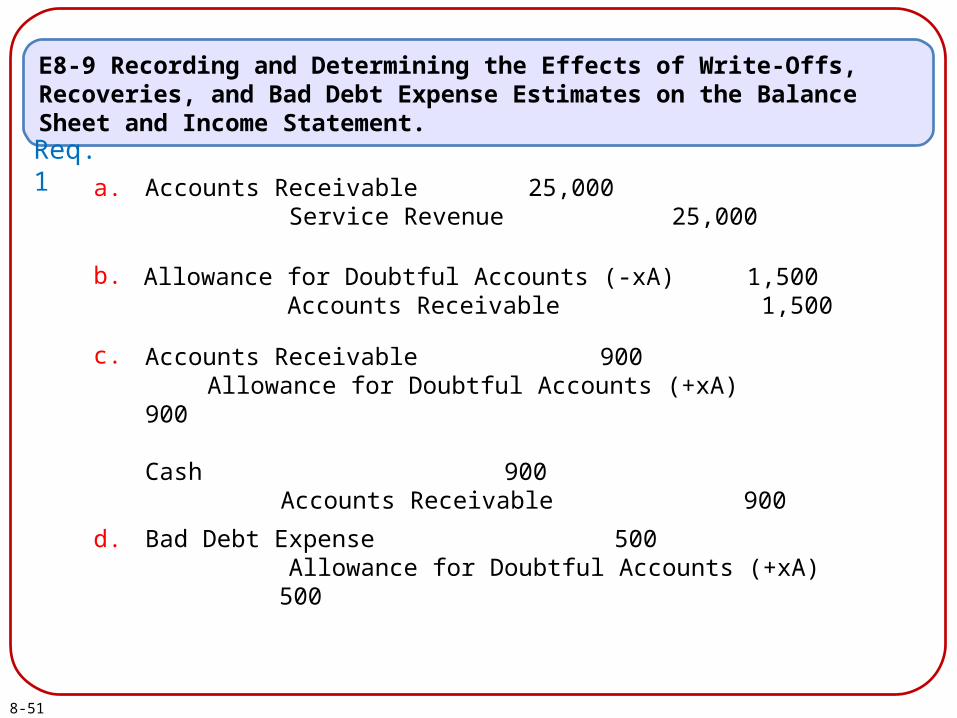

E8-9 Recording and Determining the Effects of Write-Offs, Recoveries, and Bad Debt Expense Estimates on the Balance Sheet and Income Statement.Fraud Investigators Inc. operates a fraud detection service. Required:1. Prepare journal entries for each transaction below.

a. On March 31, 10 customers were billed for detection services totaling $25,000.b. On October 31, a customer balance of $1,500 from a prior year was determined

to be uncollectible and was written off.c. On December 15, a customer paid an old balance of $900, which had been

written off in a prior year.d. On December 31, $500 of bad debts were estimated and recorded for the year.

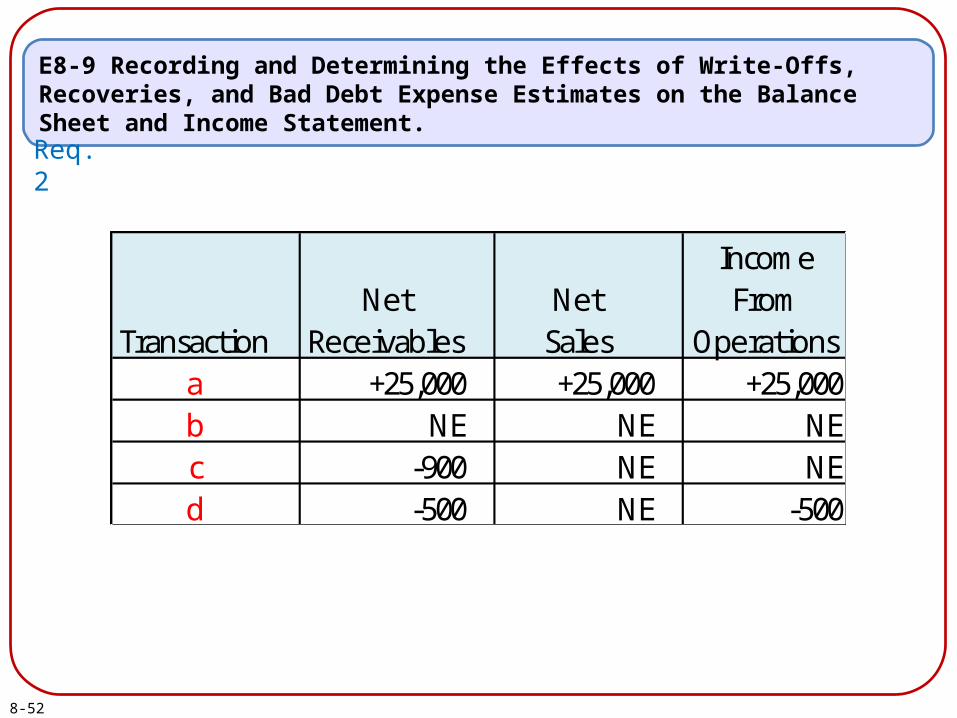

2. Complete the following table, indicating the amount and effect ( + for increase, - for decrease, and NE for no effect) of each transaction.

8-51

E8-9 Recording and Determining the Effects of Write-Offs, Recoveries, and Bad Debt Expense Estimates on the Balance Sheet and Income Statement.

Req. 1

Accounts Receivable 25,000 Service Revenue 25,000

a.

b.

c.

d. Bad Debt Expense 500 Allowance for Doubtful Accounts (+xA) 500

Accounts Receivable 900 Allowance for Doubtful Accounts (+xA) 900

Cash 900 Accounts Receivable 900

Allowance for Doubtful Accounts (-xA) 1,500 Accounts Receivable 1,500

8-52

IncomeNet Net From

Transaction Receivables Sales Operationsa +25,000 +25,000 +25,000b NE NE NEc -900 NE NEd -500 NE -500

IncomeNet Net From

Transaction Receivables Sales Operationsa +25,000 +25,000 +25,000b NE NE NEc -900 NE NEd -500 NE -500

IncomeNet Net From

Transaction Receivables Sales Operationsa +25,000 +25,000 +25,000b NE NE NEc -900 NE NEd -500 NE -500

E8-9 Recording and Determining the Effects of Write-Offs, Recoveries, and Bad Debt Expense Estimates on the Balance Sheet and Income Statement.

Req. 2

IncomeNet Net From

Transaction Receivables Sales Operationsa +25,000 +25,000 +25,000b NE NE NEc -900 NE NEd -500 NE -500

8-53

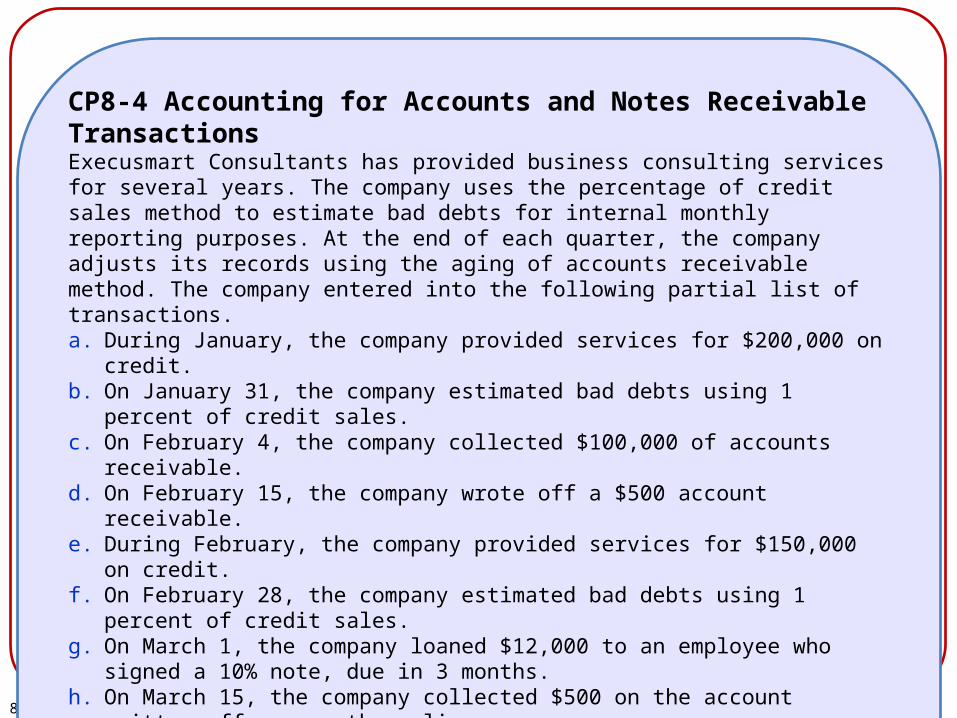

CP8-4 Accounting for Accounts and Notes Receivable TransactionsExecusmart Consultants has provided business consulting services for several years. The company uses the percentage of credit sales method to estimate bad debts for internal monthly reporting purposes. At the end of each quarter, the company adjusts its records using the aging of accounts receivable method. The company entered into the following partial list of transactions.a. During January, the company provided services for $200,000 on credit.b. On January 31, the company estimated bad debts using 1 percent of credit sales.c. On February 4, the company collected $100,000 of accounts receivable.d. On February 15, the company wrote off a $500 account receivable.e. During February, the company provided services for $150,000 on credit.f. On February 28, the company estimated bad debts using 1 percent of credit sales.g. On March 1, the company loaned $12,000 to an employee who signed a 10% note,

due in 3 months.h. On March 15, the company collected $500 on the account written off one month

earlier.i. On March 31, the company accrued interest earned on the note.j. On March 31, the company adjusted for uncollectible accounts, based on the aging

analysis shown on the next screen. Allowance for Doubtful Accounts has an unadjusted credit balance of $6,000.

8-54

CP8-4 Accounting for Accounts and Notes Receivable Transactions (continued)

Required:1. For items a – j, analyze the amount and direction (+ or -) of effects on specific

financial statement accounts and the overall accounting equation.2. Prepare journal entries for items (a) – (j).3. Show how Accounts Receivable, Notes Receivable, and their related accounts would

be reported in the current assets section of a classified balance sheet at the end of the quarter on March 31.

4. Sales Revenue and Service Revenue are two income statement accounts that relate to Accounts Receivable. Name two other accounts related to Accounts Receivable and Note Receivable that would be reported on the income statement and indicate whether each would appear before, or after, Income from Operations for Execusmart Consultants.

8-55

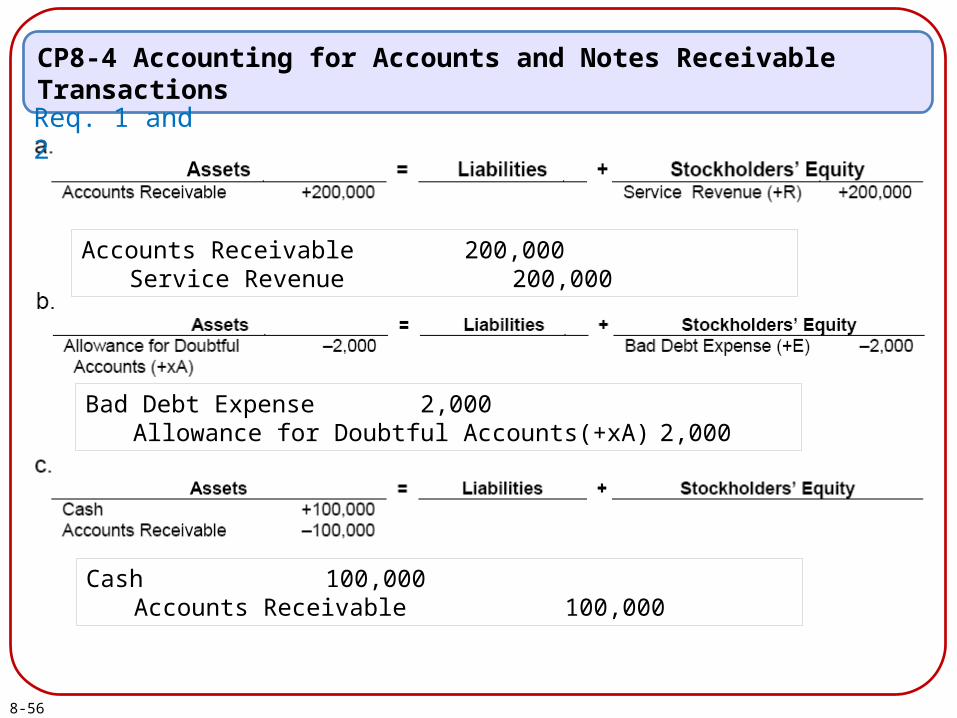

CP8-4 Accounting for Accounts and Notes Receivable Transactions

Req. 1 and 2

Accounts Receivable 200,000Service Revenue 200,000

Bad Debt Expense 2,000Allowance for Doubtful Accounts(+xA) 2,000

8-56

CP8-4 Accounting for Accounts and Notes Receivable Transactions

Req. 1 and 2

Accounts Receivable 200,000Service Revenue 200,000

Bad Debt Expense 2,000Allowance for Doubtful Accounts(+xA) 2,000

Cash 100,000Accounts Receivable 100,000

8-57

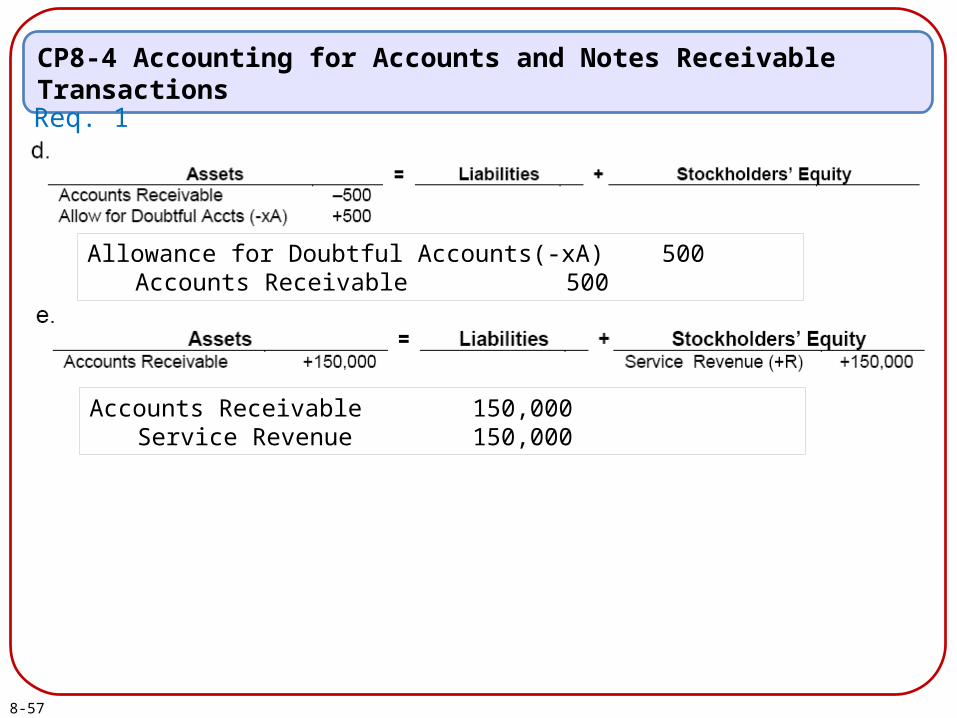

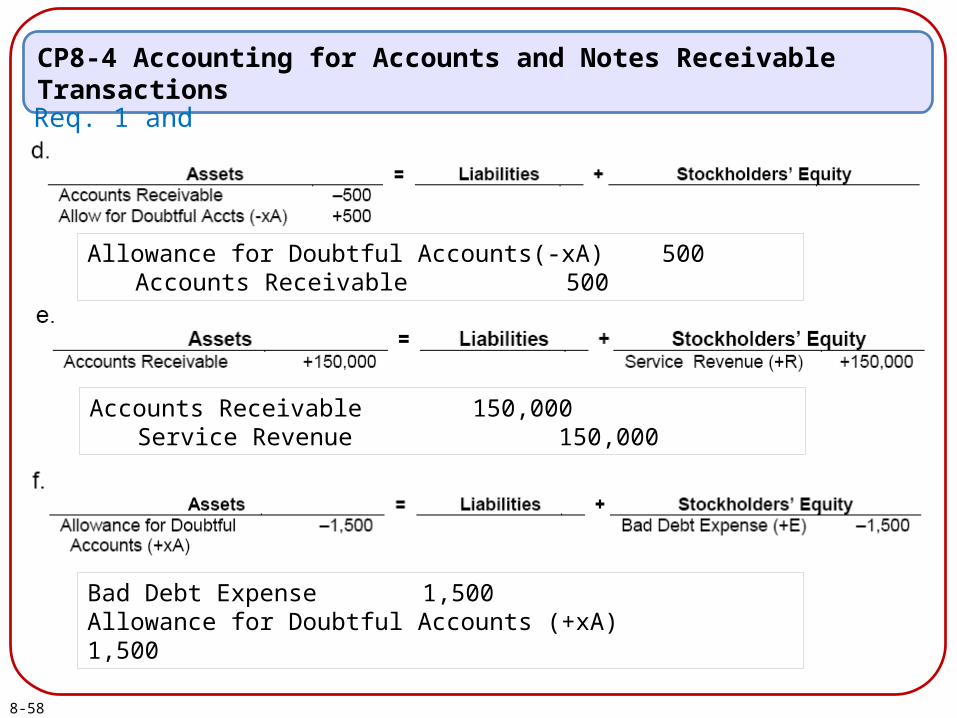

CP8-4 Accounting for Accounts and Notes Receivable Transactions

Req. 1 and 2

Allowance for Doubtful Accounts(-xA) 500Accounts Receivable 500

Accounts Receivable 150,000Service Revenue 150,000

8-58

CP8-4 Accounting for Accounts and Notes Receivable Transactions

Req. 1 and 2

Allowance for Doubtful Accounts(-xA) 500Accounts Receivable 500

Accounts Receivable 150,000Service Revenue 150,000

Bad Debt Expense 1,500Allowance for Doubtful Accounts (+xA) 1,500

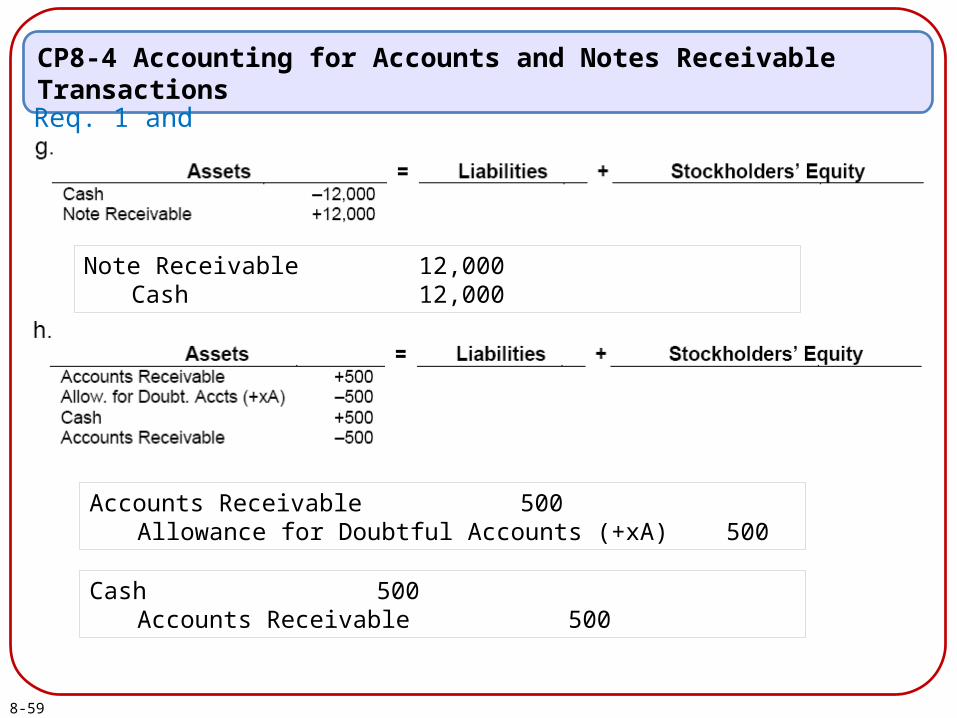

8-59

CP8-4 Accounting for Accounts and Notes Receivable Transactions

Req. 1 and 2

Note Receivable 12,000Cash 12,000

Accounts Receivable 500Allowance for Doubtful Accounts (+xA) 500

Cash 500Accounts Receivable 500

8-60

CP8-4 Accounting for Accounts and Notes Receivable Transactions

Req. 1 and 2

Total 0-30 31-60 61-90 >90Total Accounts Receivable 90,000$ 36,500$ 42,400$ 5,100$ 6,000$ Estimated Uncollectible (%) 2% 10% 20% 40%Estimated Uncollectible ($) 8,390$ 730$ 4,240$ 1,020$ 2,400$

Desired $8,390 – Current -$6000 = Adjustment $2,390

Interest Receivable 100Interest Revenue 100

Bad Debt Expense 2,390Allowance for Doubtful Accounts (+xA) 2,390

8-61

CP8-4 Accounting for Accounts and Notes Receivable Transactions

Req. 3

Execusmart Consultants would report Bad Debt Expense before Income from Operations, and Interest Revenue after Income for Operations.

Req. 4

EXECUSMART CONSULTANTSPartial Balance Sheet

At March 31

Assets

Current Assets:

Accounts Receivable

Less: Allowance for Doubtful Accounts

Accounts Receivable, Net of Allowance

Note Receivable

Interest Receivable

$ 90,000

8,390

$ 81,610

12,000

100

8-62

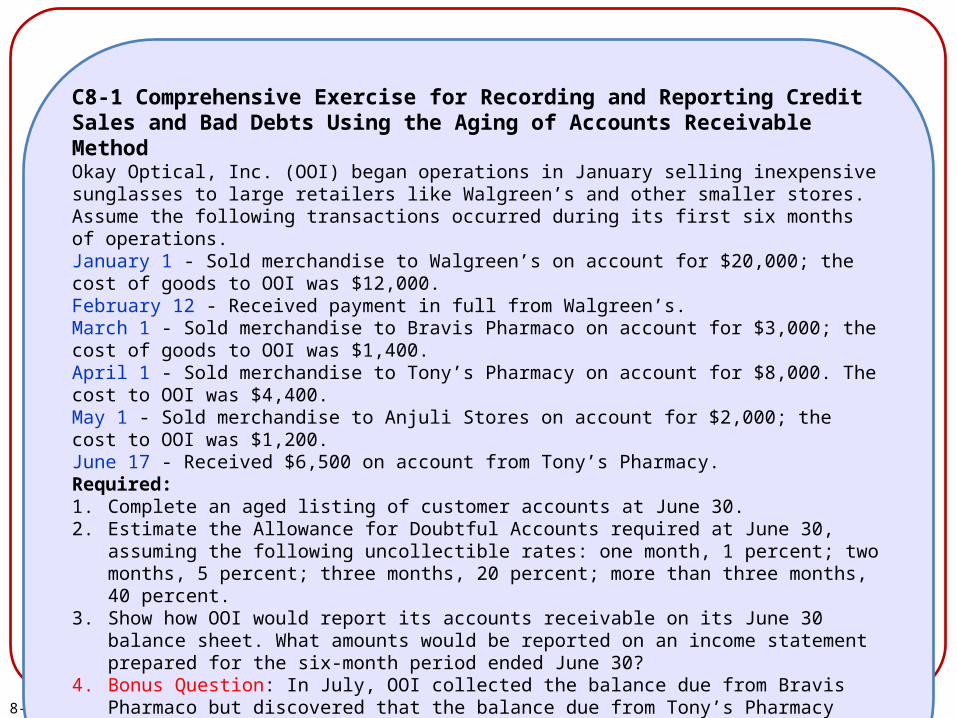

C8-1 Comprehensive Exercise for Recording and Reporting Credit Sales and Bad Debts Using the Aging of Accounts Receivable MethodOkay Optical, Inc. (OOI) began operations in January selling inexpensive sunglasses to large retailers like Walgreen’s and other smaller stores. Assume the following transactions occurred during its first six months of operations.January 1 - Sold merchandise to Walgreen’s on account for $20,000; the cost of goods to OOI was $12,000.February 12 - Received payment in full from Walgreen’s.March 1 - Sold merchandise to Bravis Pharmaco on account for $3,000; the cost of goods to OOI was $1,400.April 1 - Sold merchandise to Tony’s Pharmacy on account for $8,000. The cost to OOI was $4,400.May 1 - Sold merchandise to Anjuli Stores on account for $2,000; the cost to OOI was $1,200.June 17 - Received $6,500 on account from Tony’s Pharmacy.Required:1. Complete an aged listing of customer accounts at June 30.2. Estimate the Allowance for Doubtful Accounts required at June 30, assuming the following

uncollectible rates: one month, 1 percent; two months, 5 percent; three months, 20 percent; more than three months, 40 percent.

3. Show how OOI would report its accounts receivable on its June 30 balance sheet. What amounts would be reported on an income statement prepared for the six-month period ended June 30?

4. Bonus Question: In July, OOI collected the balance due from Bravis Pharmaco but discovered that the balance due from Tony’s Pharmacy needed to be written off. Using this information, determine how accurate OOI was in estimating the Allowance for Doubtful Accounts needed for each of these two customers and in total.

8-63

C8-1 Comprehensive Exercise for Recording and Reporting Credit Sales and Bad Debts Using the Aging of Accounts Receivable Method

Req. 2Accounts Receivable

Estimated Uncollectible (%)

Estimated Uncollectible ($)

Total

$ 6,500

$ 1,600

>3 months

$ 3,000

40%

$ 1,200

3 months

$ 1,500

20%

$ 300

2 months

$ 2,000

5%

$ 100

Req. 1Customer

Anjuli Stores

Bravis Pharmaco

Tony’s Pharmacy

Walgreens

Total

June

(1 Month)

$ -

>3

Months

$ 3,000

$ 3,000

April

(3 Months)

$ 1,500

$ 1,500

May

(2 Months)

$ 2,000

$ 2,000

Total

$ 2,000

3,000

1,500

-

$ 6,500

8-64

C8-1 Comprehensive Exercise for Recording and Reporting Credit Sales and Bad Debts Using the Aging of Accounts Receivable Method

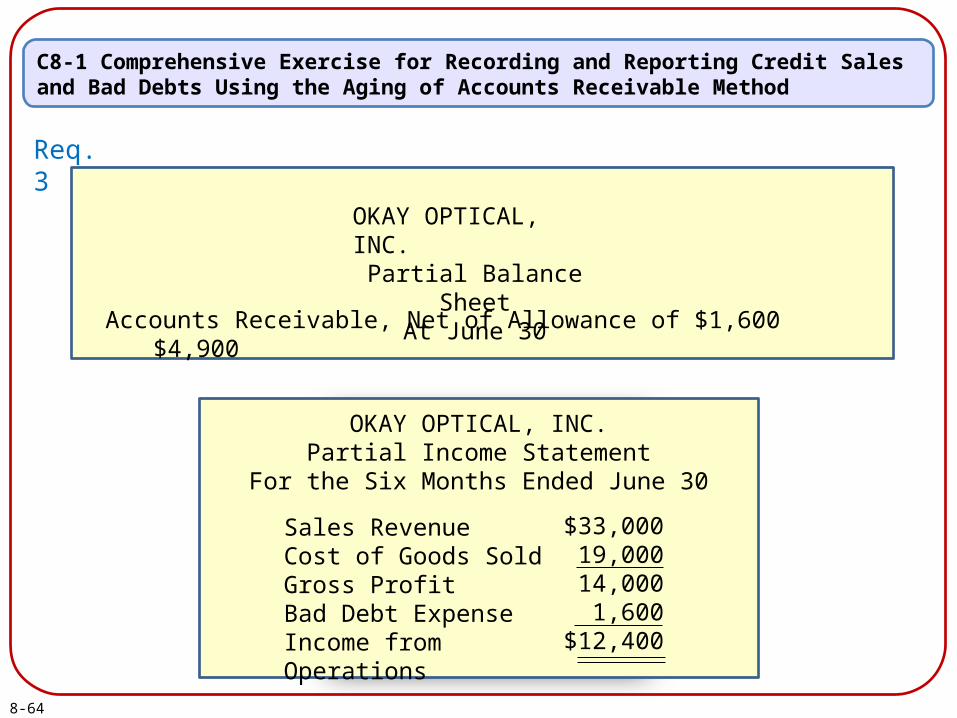

Req. 3

OKAY OPTICAL, INC.Partial Balance Sheet

At June 30

Accounts Receivable, Net of Allowance of $1,600 $4,900

OKAY OPTICAL, INC.Partial Income Statement

For the Six Months Ended June 30

Sales RevenueCost of Goods SoldGross ProfitBad Debt ExpenseIncome from Operations

$33,00019,00014,000

1,600$12,400

8-65

C8-1 Comprehensive Exercise for Recording and Reporting Credit Sales and Bad Debts Using the Aging of Accounts Receivable Method

Req. 4 OOI did not accurately estimate the precise amounts that would be collected from each customer, yet the total estimate was accurate. That is, OOI underestimated the amount collectible from Bravis Pharmaco (40% of $3,000, or $1,200, was estimated uncollectible where it later turned out to be collectible in full). It overestimated the amount collectible from Tony’s Pharmacy (20% of $1,500, or $300, was estimated uncollectible where it later turned out to show that $1,500 was uncollectible). Looking at Tony’s Pharmacy and Bravis Pharmaco combined, the estimated bad debt for both customers was $1,500, which is almost the same as the amount the company wrote off.

8-66

End of Chapter 8