Copyright © 2016 by McGraw-Hill Education Chapter 5 Fraud, Internal Control, and Cash PowerPoint...

53

Copyright © 2016 by McGraw-Hill Education Chapter 5 Fraud, Internal Control, and Cash PowerPoint Author: Brandy Mackintosh, CA

-

Upload

diane-anthony -

Category

Documents

-

view

247 -

download

0

Transcript of Copyright © 2016 by McGraw-Hill Education Chapter 5 Fraud, Internal Control, and Cash PowerPoint...

Copyright © 2016 by McGraw-Hill Education

Chapter 5Fraud, Internal Control, and Cash

PowerPoint Author:Brandy Mackintosh, CA

5-2

Learning Objective 5-1

Define fraud and internal control.

5-3

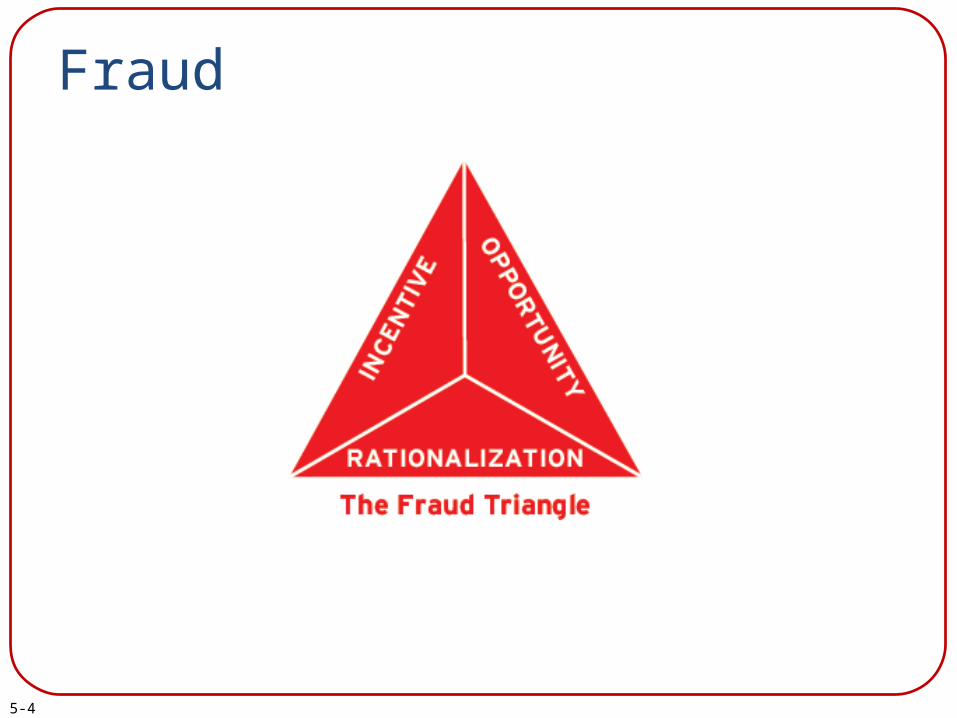

Fraud

Fraud is generally defined as an attempt to deceive others for personal gain.

Corruption

Asset Misappropriation

Financial Statement Fraud

5-4

Fraud

5-5

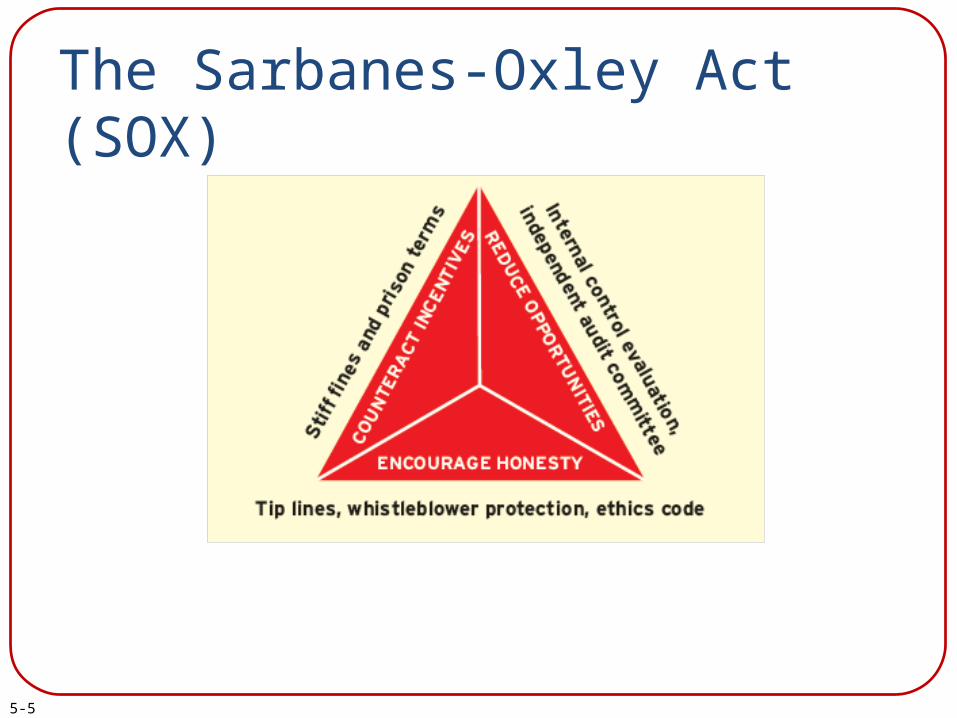

The Sarbanes-Oxley Act (SOX)

5-6

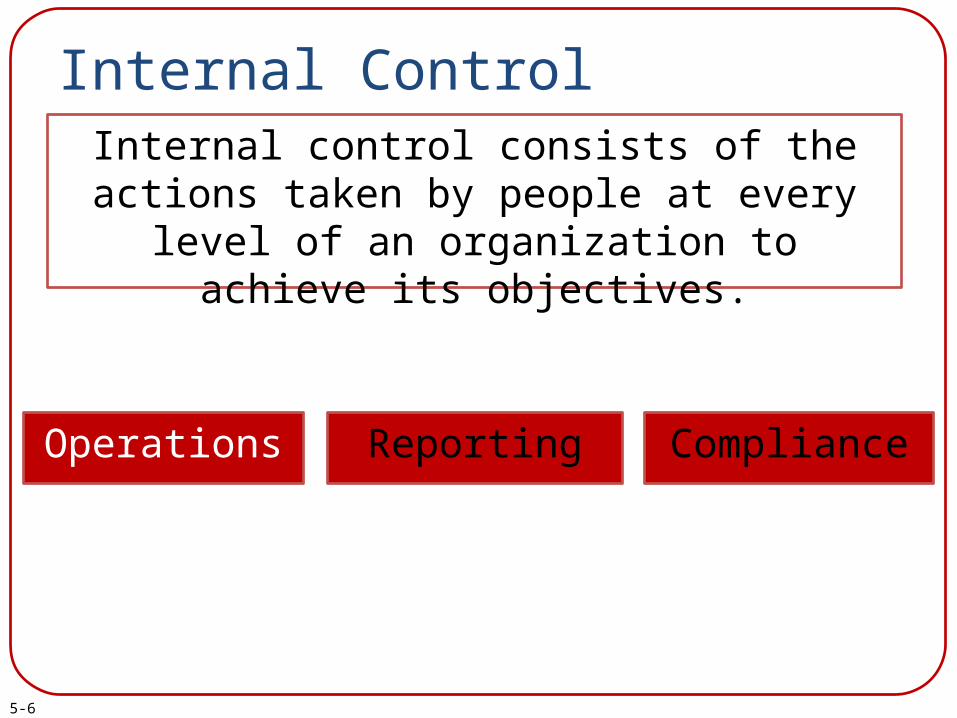

Internal Control ObjectivesInternal control consists of the actions taken by

people at every level of an organization to achieve its objectives.

Operations Reporting Compliance

5-7

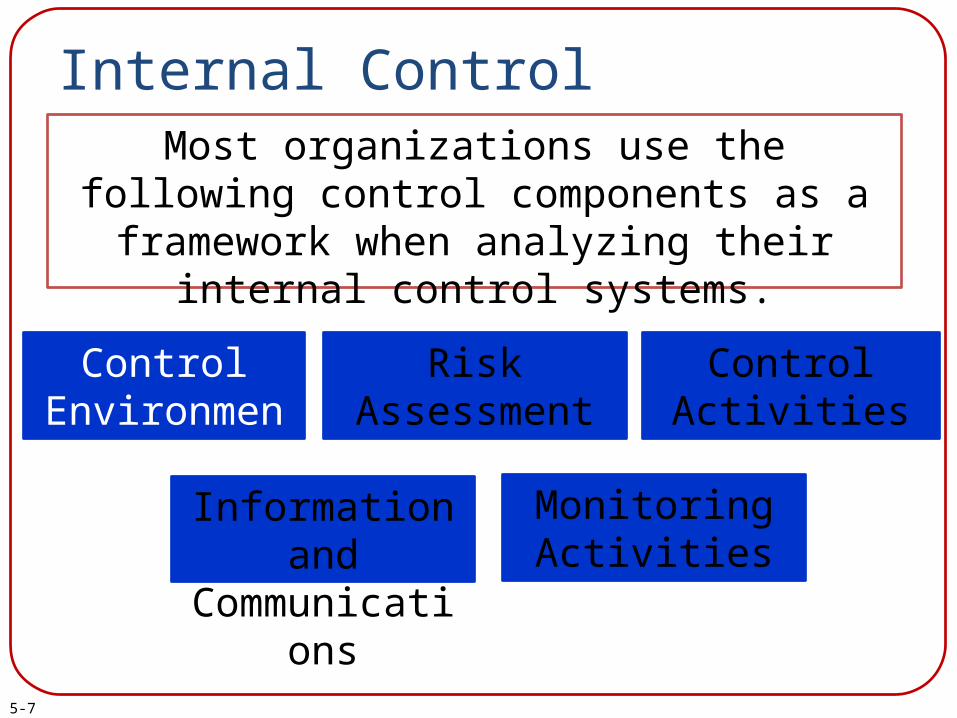

Internal Control ComponentsMost organizations use the following control components as a framework when analyzing

their internal control systems.

Control Environment

Risk Assessment

Control Activities

Monitoring Activities

Information and Communication

s

5-8

Relationship of Control Objectives and Components

5-9

Learning Objective 5-2

Explain common principles and limitations of internal

control.

5-10

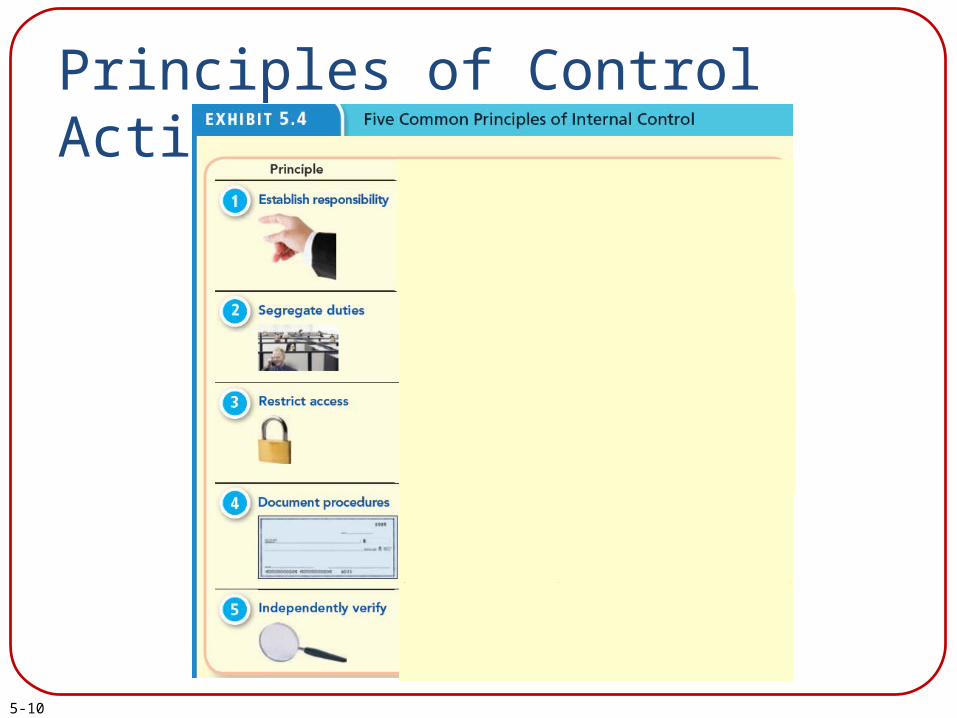

Principles of Control Activities

5-11

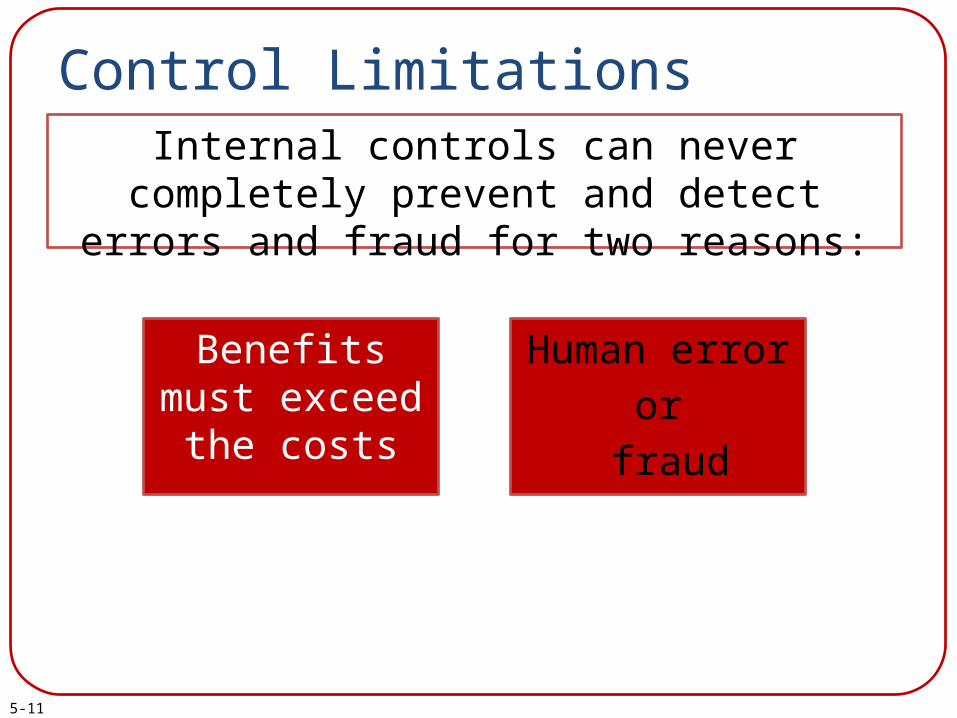

Control LimitationsInternal controls can never completely prevent and detect errors and fraud for two reasons:

Benefits must exceed the

costs

Human error

or

fraud

5-12

Learning Objective 5-3

Apply internal control principles to cash receipts and

payments.

5-13

Internal Control for Cash

Internal controls for cash are important because the volume of cash transactions is enormous and

because cash is valuable and portable and therefore poses a high risk of theft.

5-14

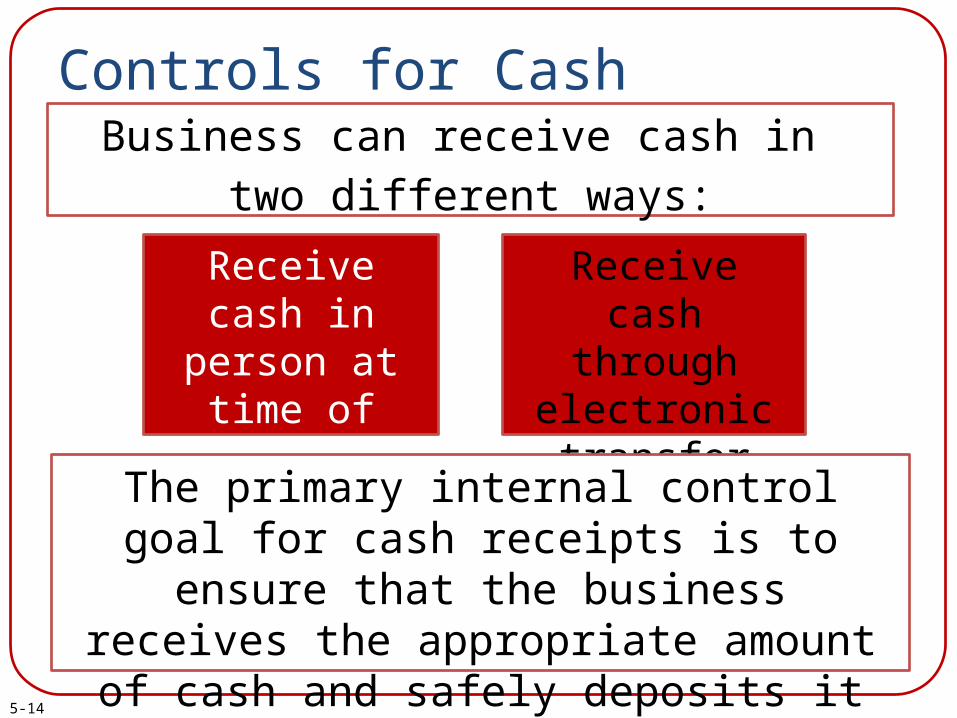

Controls for Cash Receipts

Receive cash in person at time of sale

Receive cash through

electronic transfer

The primary internal control goal for cash receipts is to ensure that the business

receives the appropriate amount of cash and safely deposits it in the bank.

Business can receive cash in

two different ways:

5-15

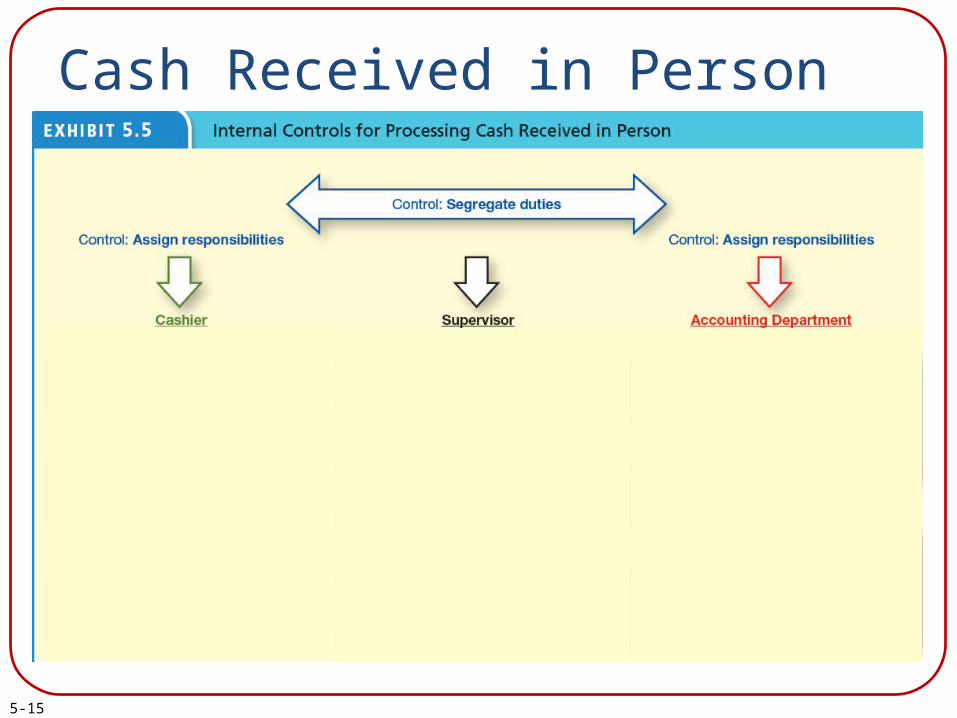

Cash Received in Person

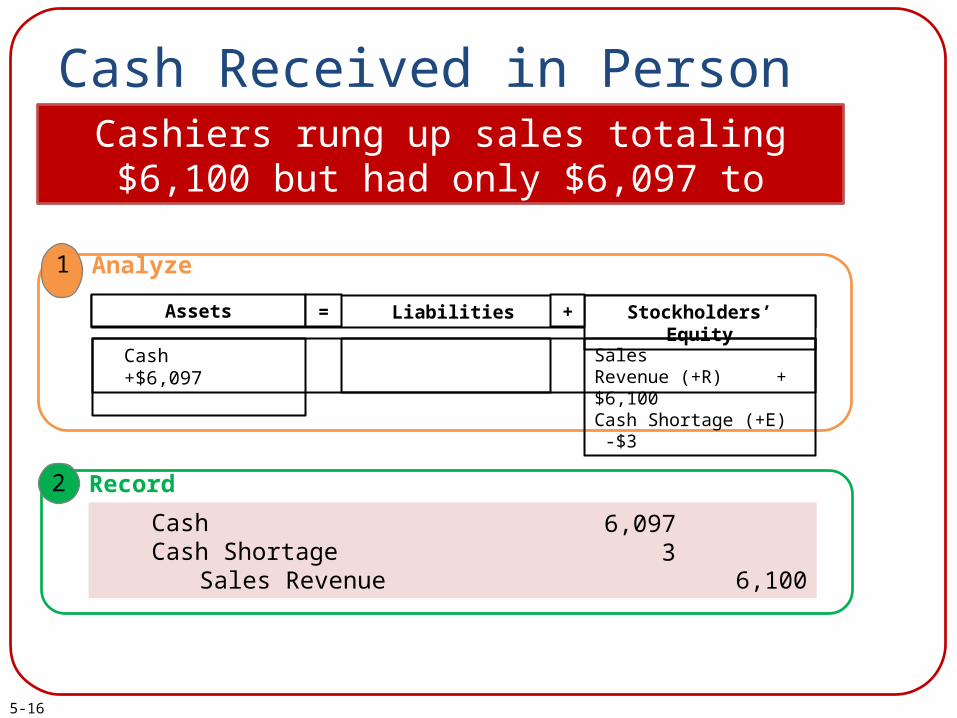

5-16

Cash Received in Person

2 Record

Cash Cash Shortage

Sales Revenue 6,100

6,0973

1 Analyze

LiabilitiesAssets = Stockholders’ Equity+

Cash +$6,097

SalesRevenue (+R) +$6,100Cash Shortage (+E) -$3

Cashiers rung up sales totaling $6,100 but had only $6,097 to deposit.

5-17

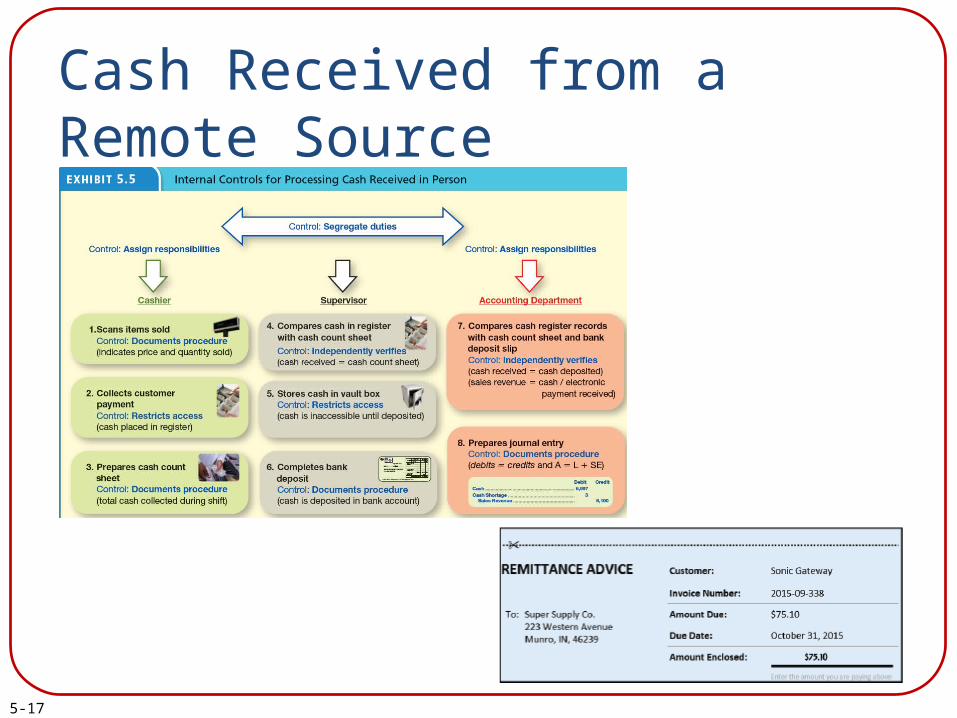

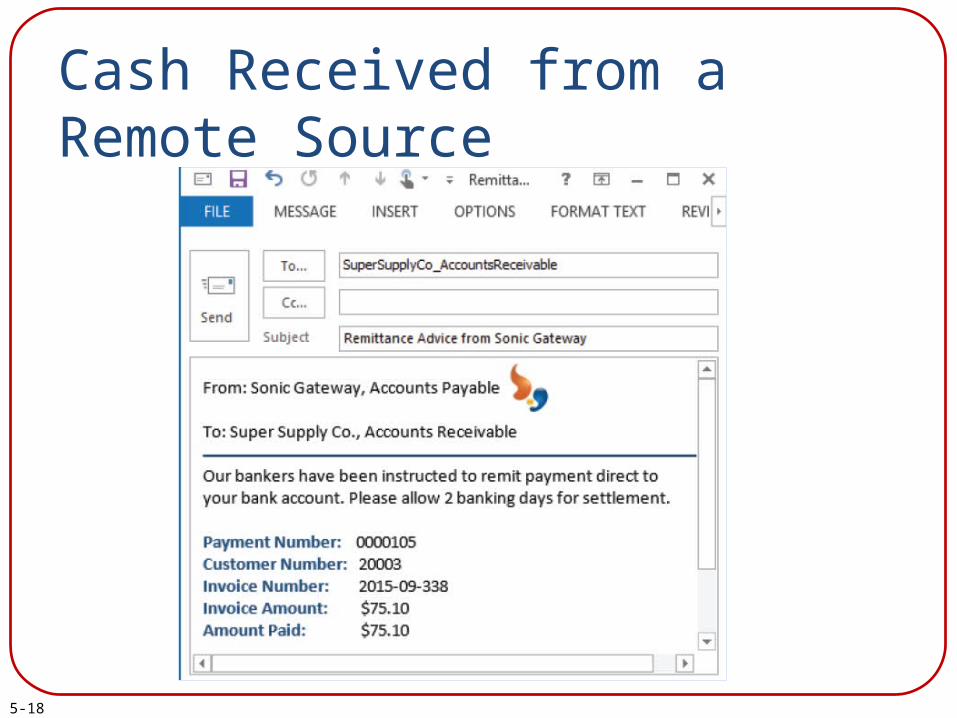

Cash Received from a Remote Source

5-18

Cash Received from a Remote Source

5-19

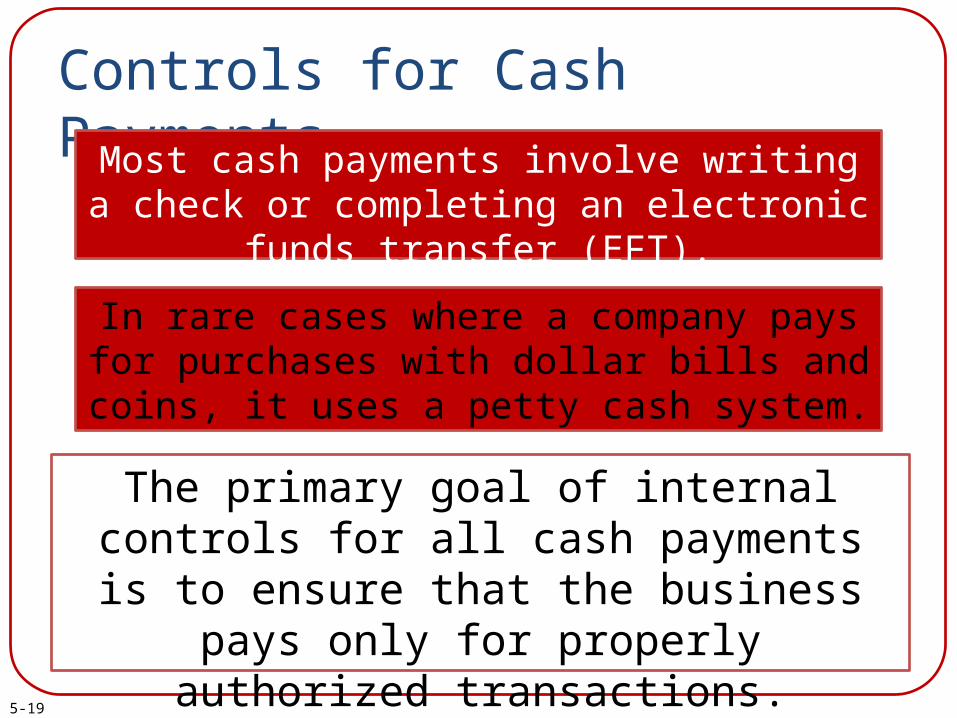

Controls for Cash Payments

Most cash payments involve writing a check or completing an electronic funds transfer (EFT).

In rare cases where a company pays for purchases with dollar bills and coins, it uses a

petty cash system.

The primary goal of internal controls for all cash payments is to ensure that the

business pays only for properly authorized transactions.

5-20

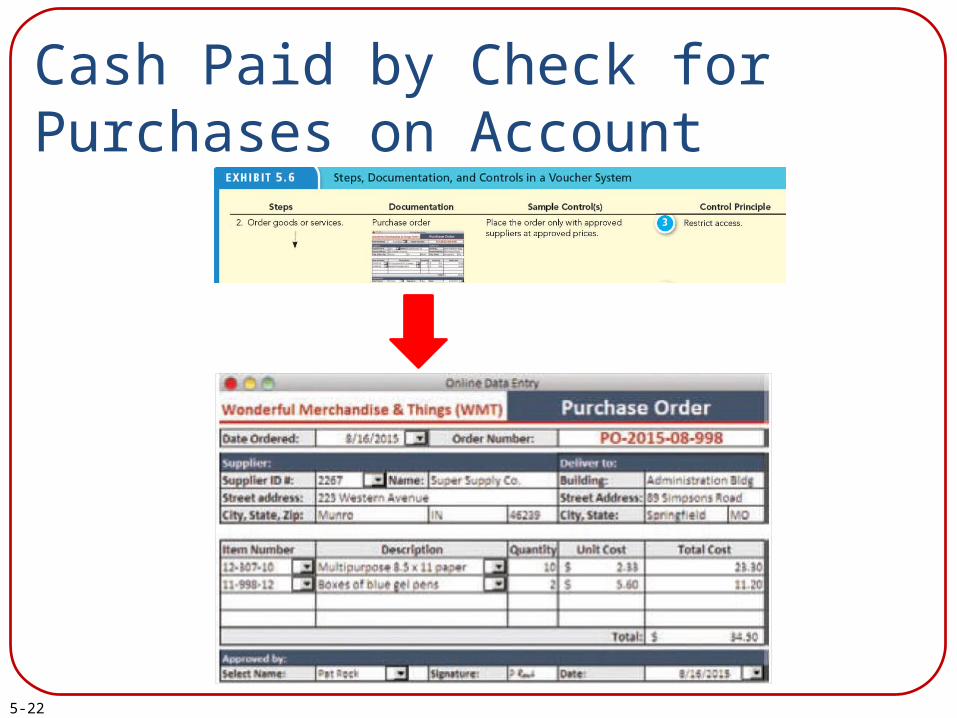

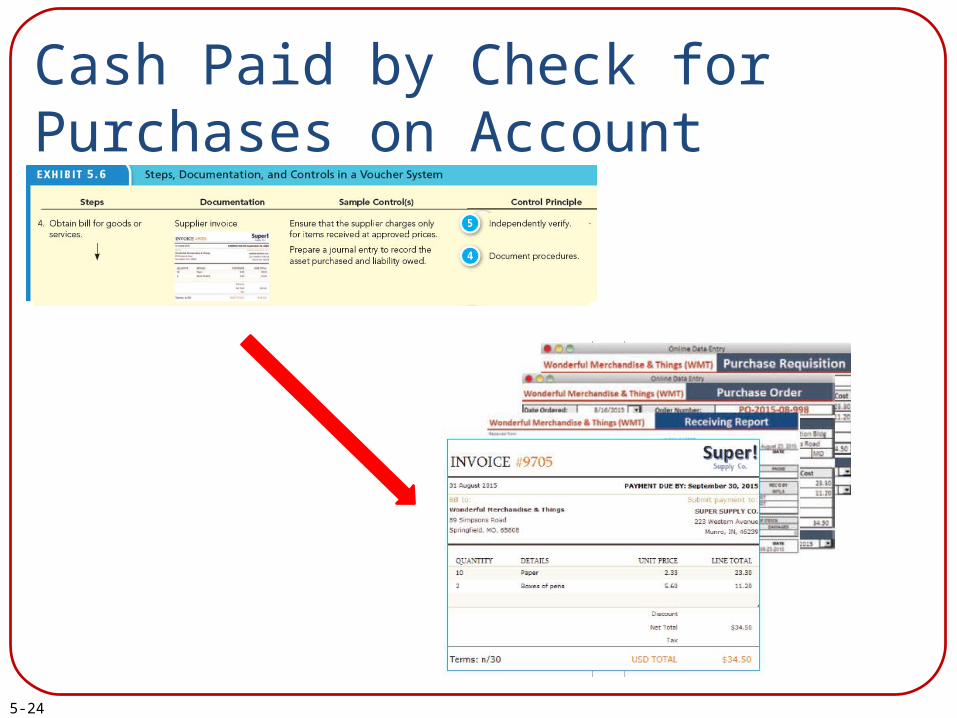

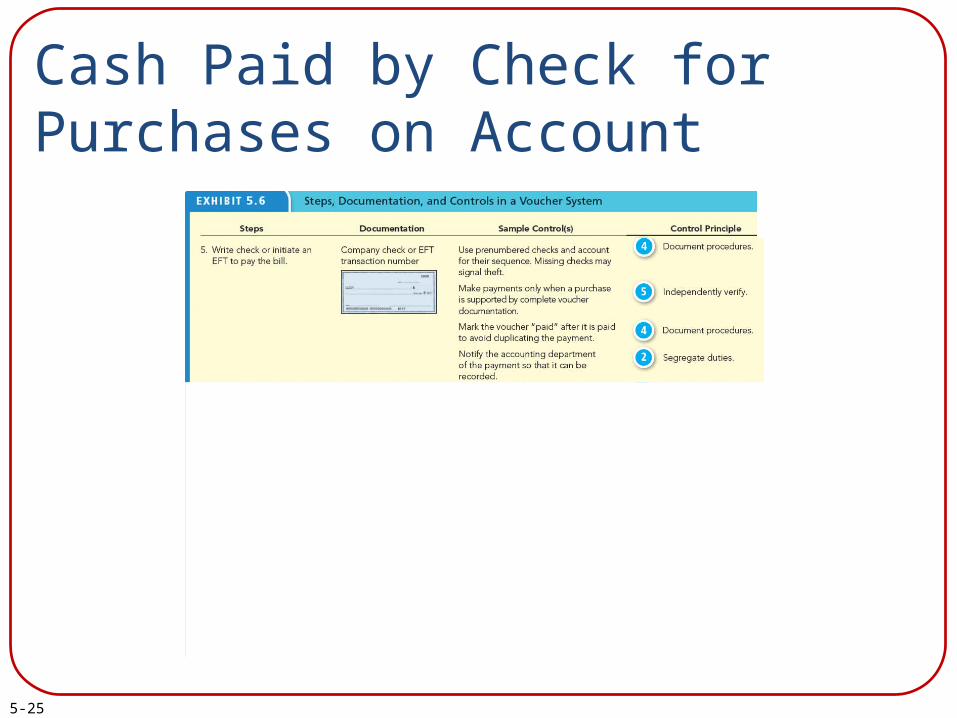

Cash Paid by Check for Purchases on Account

5-21

Cash Paid by Check for Purchases on Account

5-22

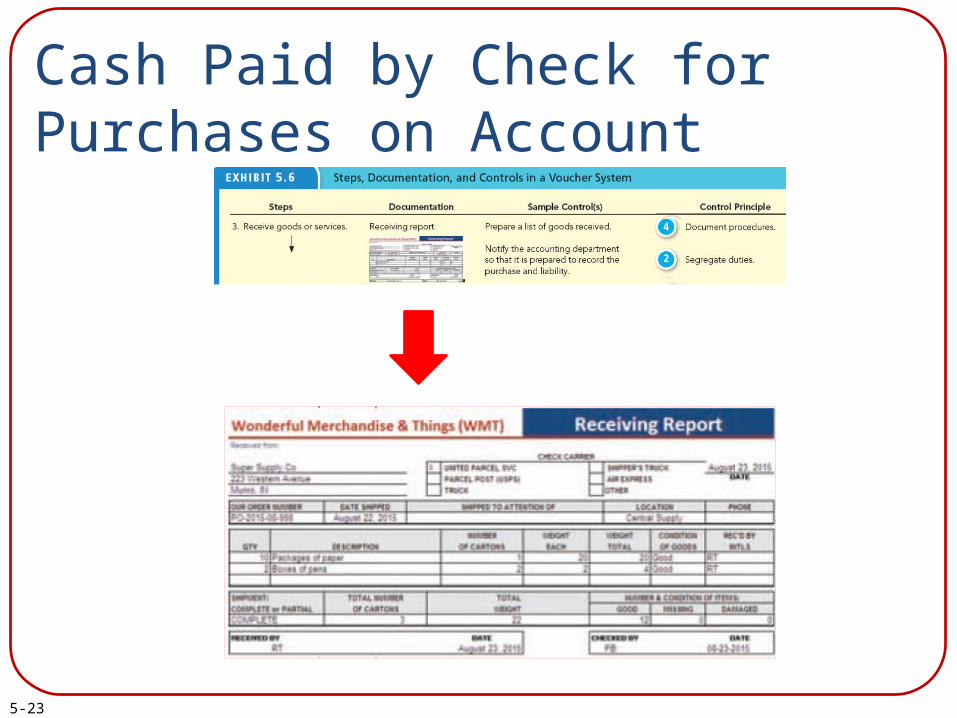

Cash Paid by Check for Purchases on Account

5-23

Cash Paid by Check for Purchases on Account

5-24

Cash Paid by Check for Purchases on Account

5-25

Cash Paid by Check for Purchases on Account

5-26

Cash Paid to Employees via Electronic Funds Transfer

Most companies pay cash to their employees through EFTs, which are known by

employees as direct deposits.

To reduce the risk of the bank accidentally overpaying or underpaying an employee, many companies use an imprest system.

5-27

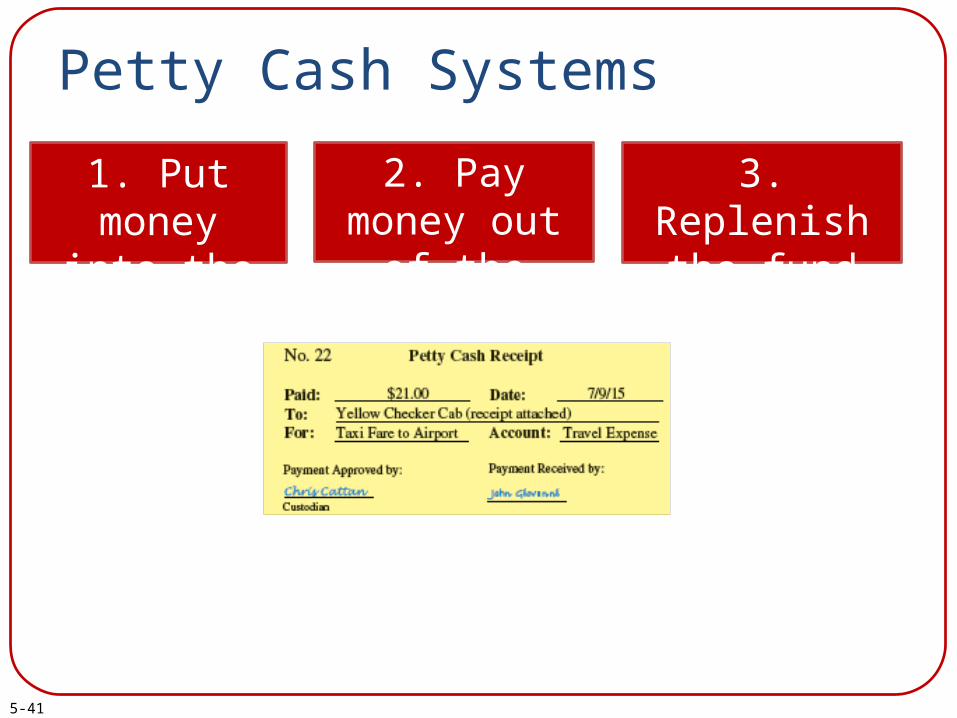

Cash Paid to Reimburse Employees (Petty Cash)

A petty cash system is used to reimburse employees for small expenditures they have

made on behalf of the organization.

5-28

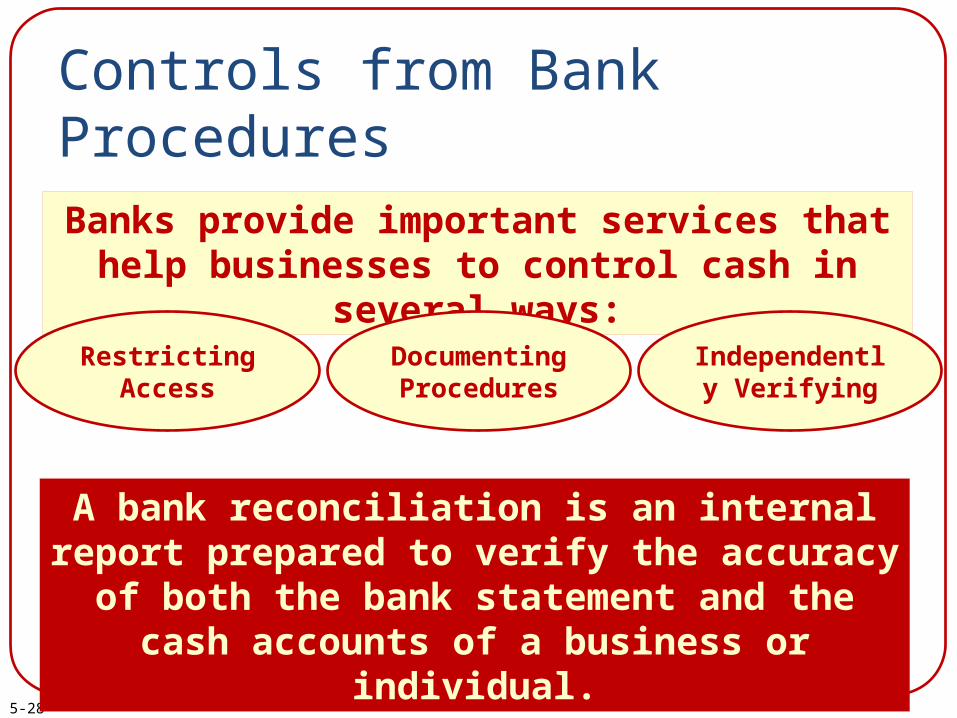

Controls from Bank Procedures

Banks provide important services that help businesses to control cash in several ways:

Restricting Access

Documenting Procedures

Independently Verifying

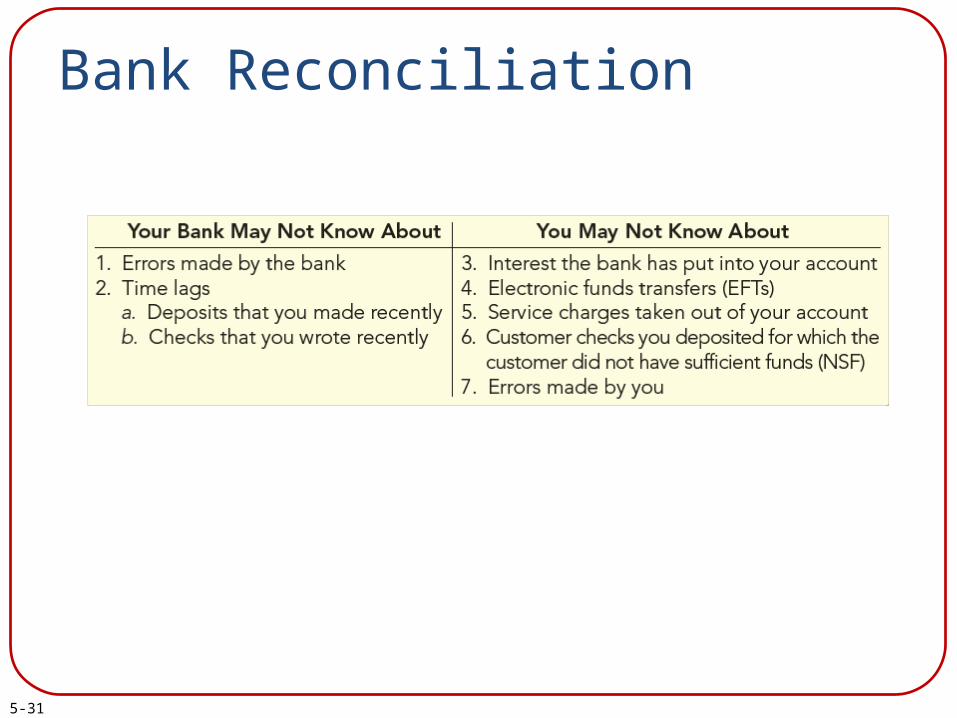

A bank reconciliation is an internal report prepared to verify the accuracy of both the bank statement and the cash accounts of a

business or individual.

5-29

Learning Objective 5-4

Perform the key control of reconciling cash to bank

statements.

5-30

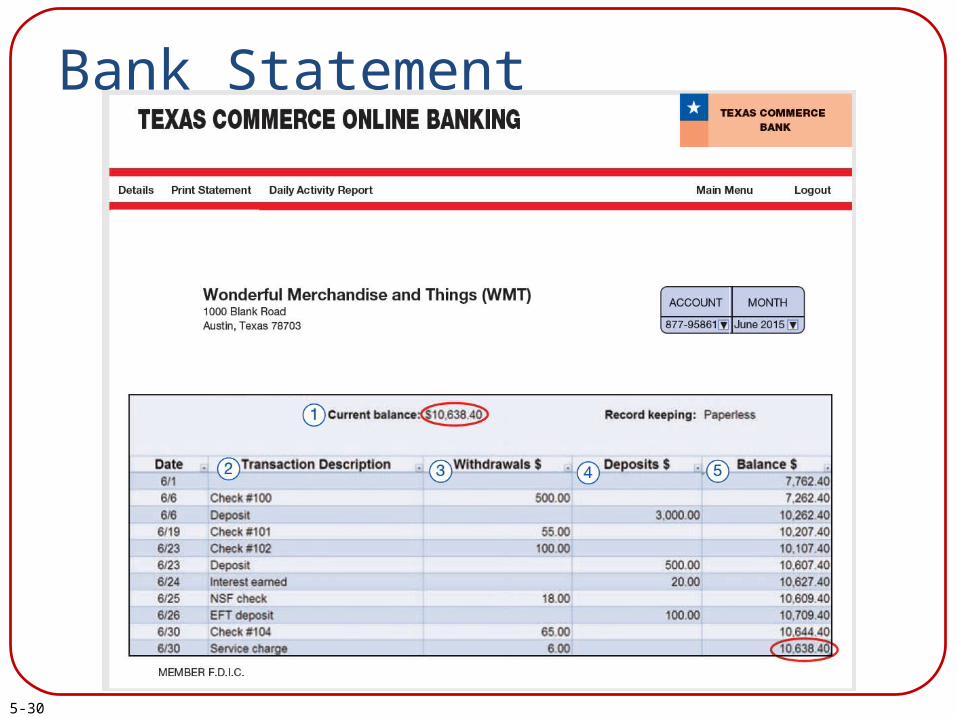

Bank Statement

5-31

Bank Reconciliation

5-32

Bank Reconciliation

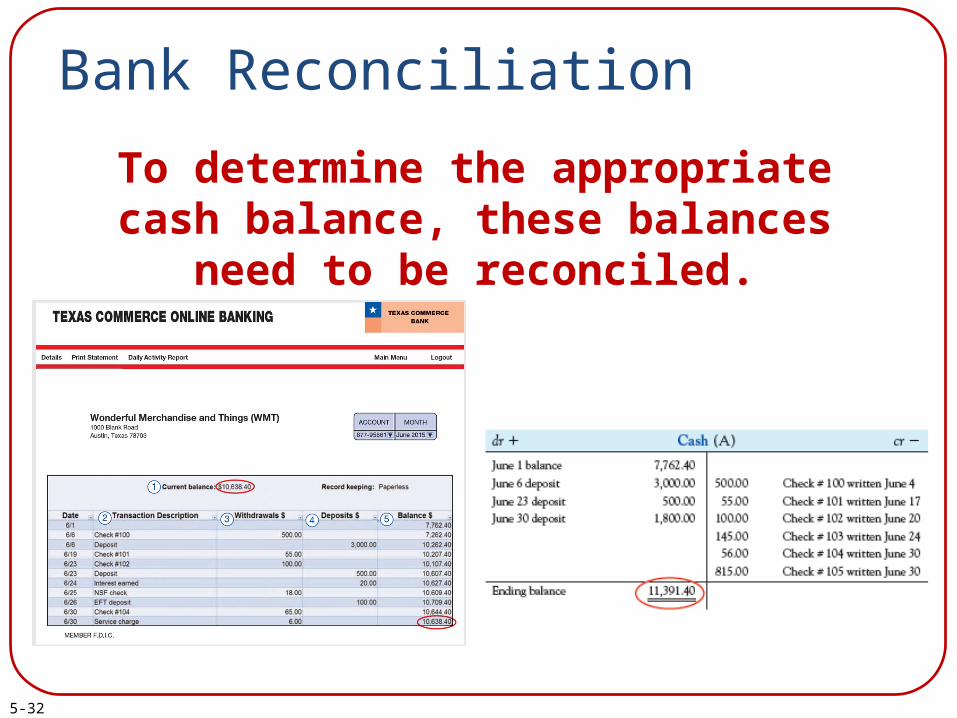

To determine the appropriate cash balance, these balances need to be

reconciled.

5-33

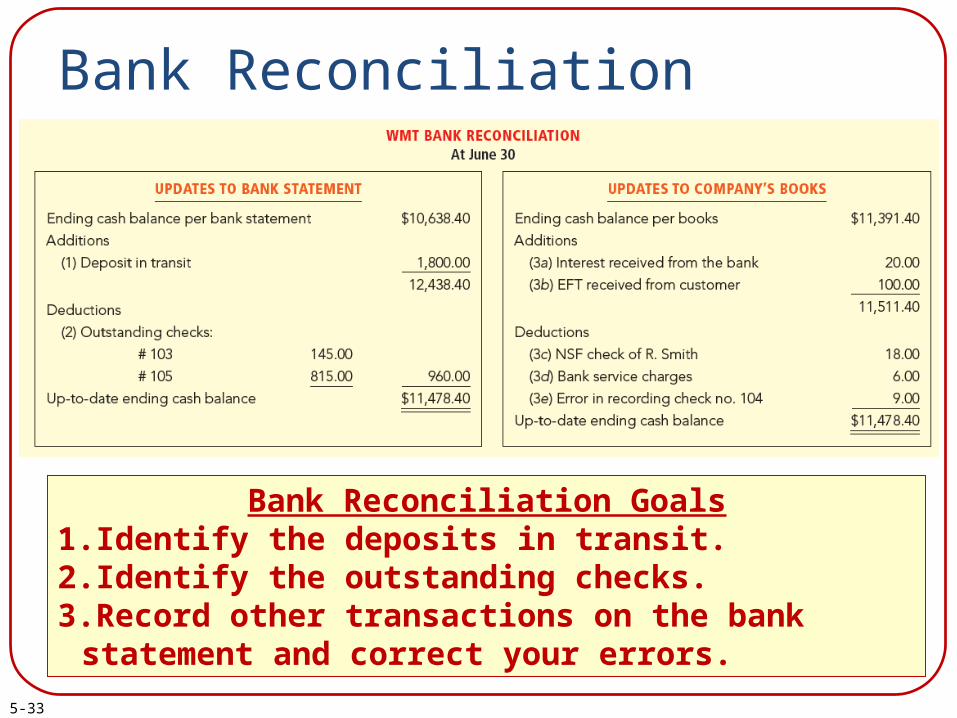

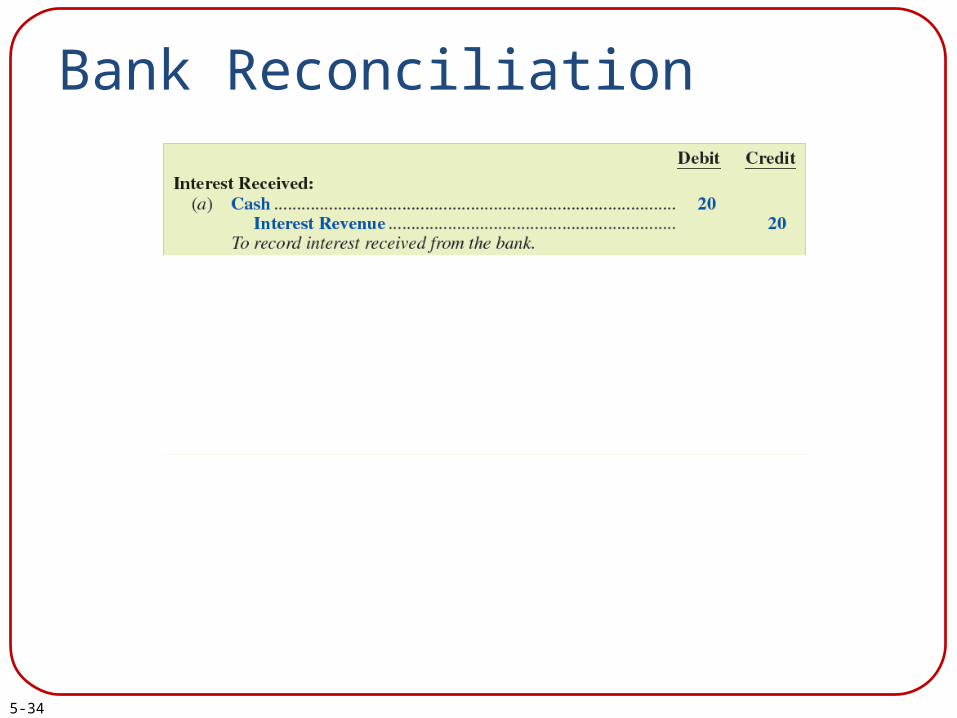

Bank Reconciliation

Bank Reconciliation Goals1.Identify the deposits in transit. 2.Identify the outstanding checks. 3.Record other transactions on the bank statement and

correct your errors.

5-34

Bank Reconciliation

5-35

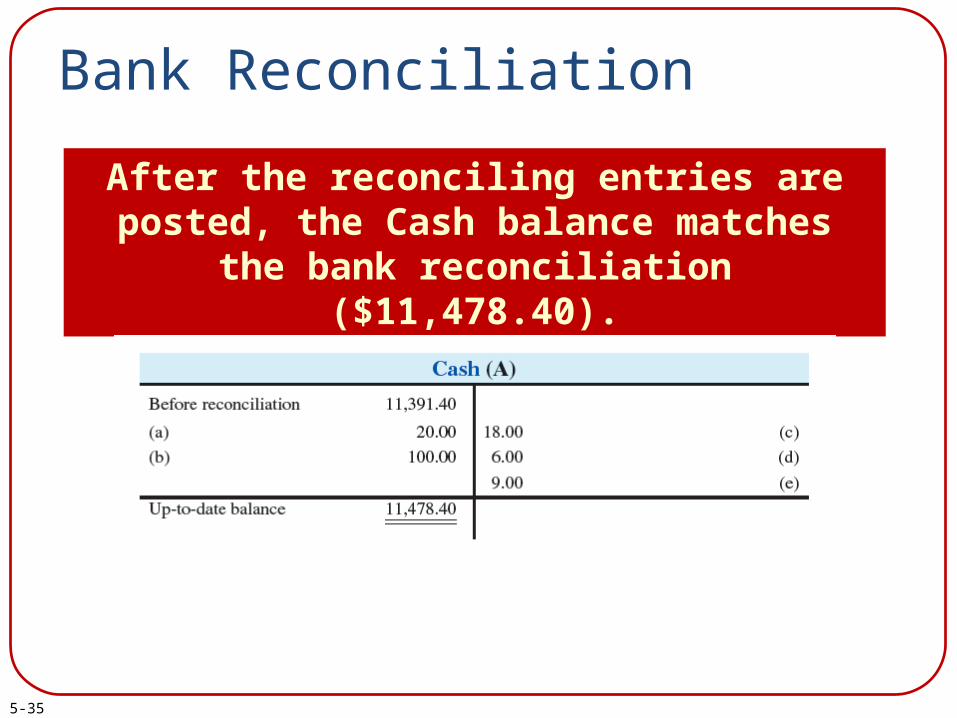

Bank Reconciliation

After the reconciling entries are posted, the Cash balance matches the bank

reconciliation ($11,478.40).

5-36

Learning Objective 5-5

Explain the reporting of cash.

5-37

Reporting Cash

(in millions)

Copyright © 2016 by McGraw-Hill Education

Supplement 5A

Petty Cash Systems

5-39

Learning Objective 5-S1

Describe the operations of petty cash systems.

5-40

Petty Cash Systems

1. Put money into the fund

2. Pay money out of the fund

3. Replenish the fund

1 Analyze

LiabilitiesAssets = Stockholders’ Equity+

Cash -$100 Petty Cash +$100

2 Record

Petty Cash Cash 100

100

5-41

Petty Cash Systems

1. Put money into the fund

2. Pay money out of the fund

3. Replenish the fund

5-42

Petty Cash Systems

1. Put money into the fund

2. Pay money out of the fund

3. Replenish the fund

1 Analyze

LiabilitiesAssets = Stockholders’ Equity+

Cash - $67 Supplies + $40

Travel Expense (+E) -$21Office Expense (+E) -$6

2 Record

SuppliesTravel ExpenseOffice Expense Cash 67

4021

6

Copyright © 2016 by McGraw-Hill Education

Chapter 5Solved Exercises

M5-3, M5-8, M5-14, M5-16, E5-5, E5-9

5-44

M5-3 Identifying Internal Control Principles Applied by a Merchandiser Identify the internal control principle represented by each point in the following diagram.

Establish Responsibility

Segregate Duties

Restrict Access

Document Procedures

Document Procedures

Independent Verify

5-45

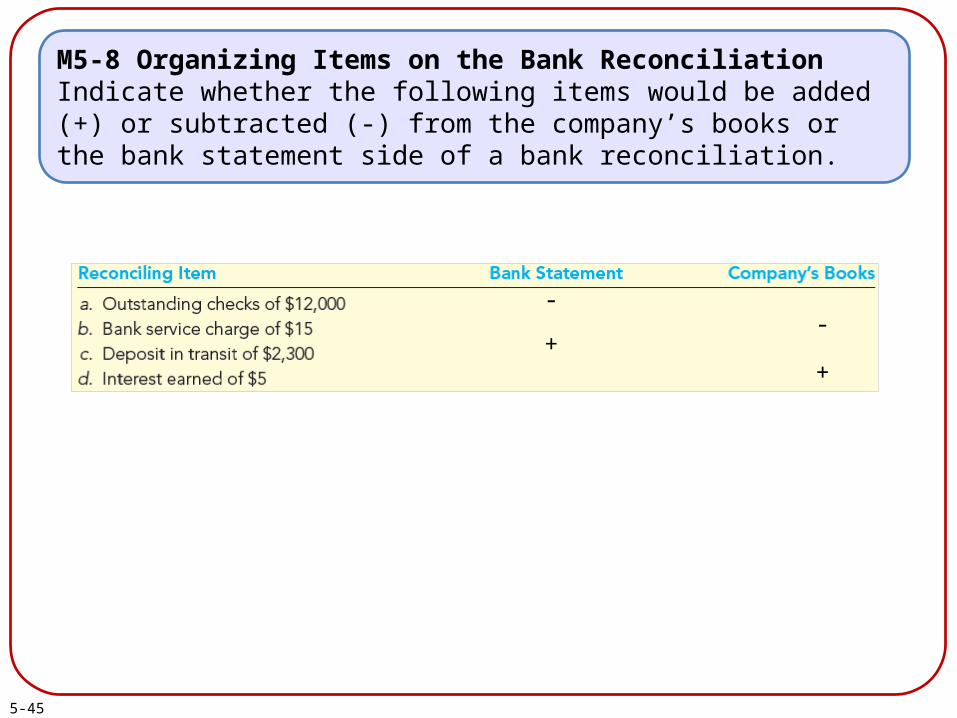

M5-8 Organizing Items on the Bank ReconciliationIndicate whether the following items would be added (+) or subtracted (-) from the company’s books or the bank statement side of a bank reconciliation.

--

++

5-46

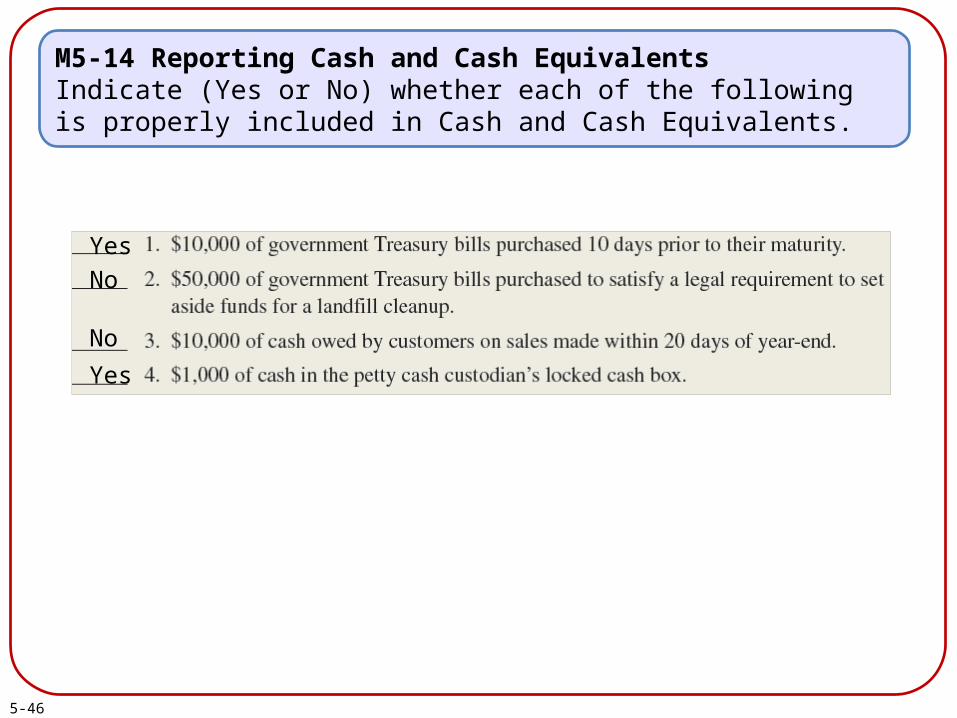

M5-14 Reporting Cash and Cash EquivalentsIndicate (Yes or No) whether each of the following is properly included in Cash and Cash Equivalents.

Yes

No

No

Yes

5-47

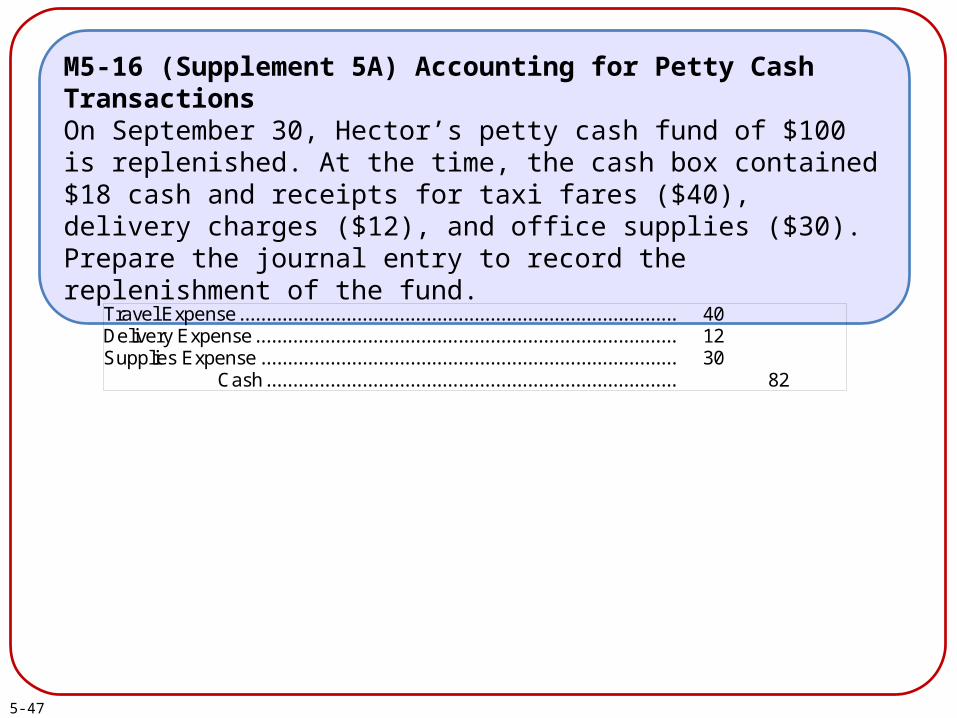

M5-16 (Supplement 5A) Accounting for Petty Cash TransactionsOn September 30, Hector’s petty cash fund of $100 is replenished. At the time, the cash box contained $18 cash and receipts for taxi fares ($40), delivery charges ($12), and office supplies ($30). Prepare the journal entry to record the replenishment of the fund.

Travel Expense .................................................................................. 40 Delivery Expense ............................................................................... 12 Supplies Expense .............................................................................. 30 Cash ............................................................................. 82

5-48

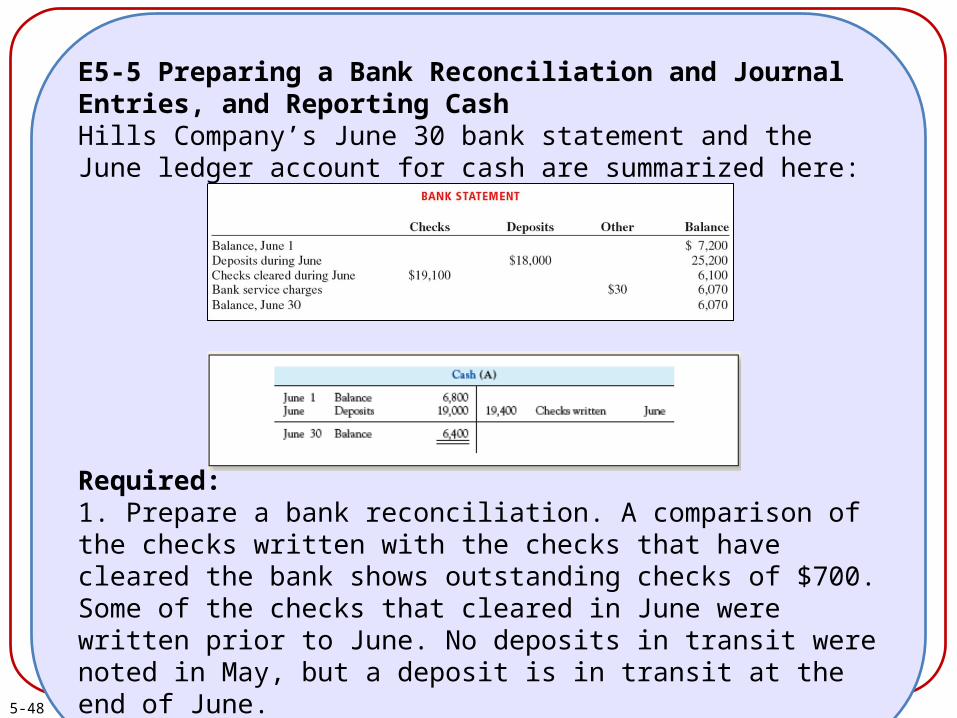

E5-5 Preparing a Bank Reconciliation and Journal Entries, and Reporting CashHills Company’s June 30 bank statement and the June ledger account for cash are summarized here:

Required:1. Prepare a bank reconciliation. A comparison of the checks written with the checks that have cleared the bank shows outstanding checks of $700. Some of the checks that cleared in June were written prior to June. No deposits in transit were noted in May, but a deposit is in transit at the end of June.

5-49

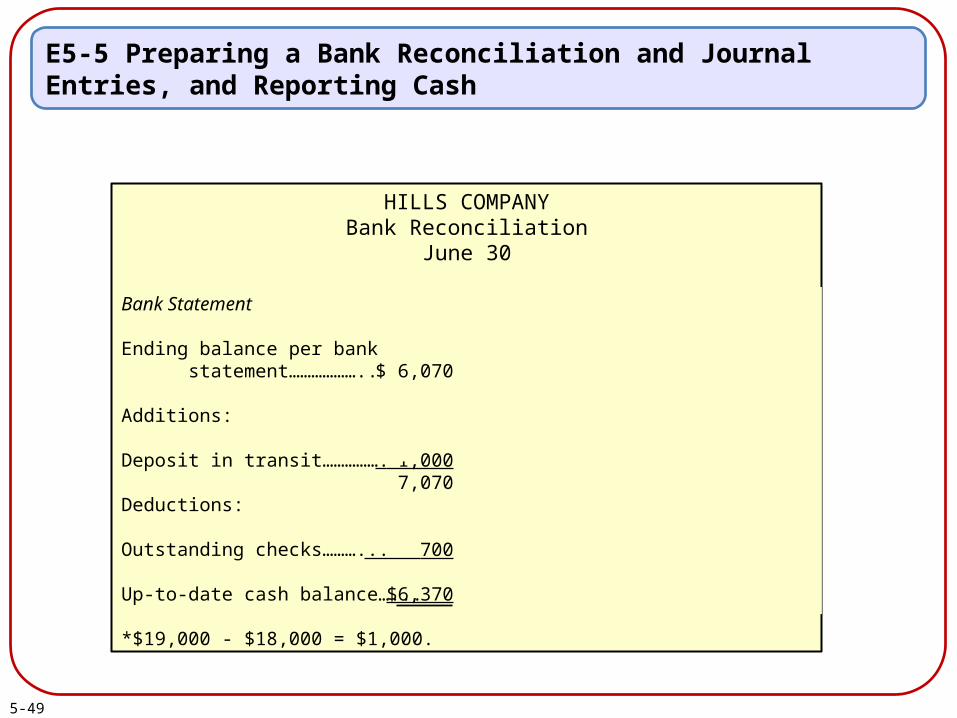

HILLS COMPANYBank Reconciliation

June 30

Bank Statement

Ending balance per bank statement………………..

Additions:

Deposit in transit…………….

Deductions:

Outstanding checks………...

Up-to-date cash balance…...

*$19,000 - $18,000 = $1,000.

$ 6,070

*1,0007,070

700

$6,370

Company’s Books

Ending balance per Cash account ………………..

Additions:

None

Deductions:

Bank service charge...……...

Up-to-date cash balance…...

$ 6,400

6,400

30

$6,370

E5-5 Preparing a Bank Reconciliation and Journal Entries, and Reporting Cash

5-50

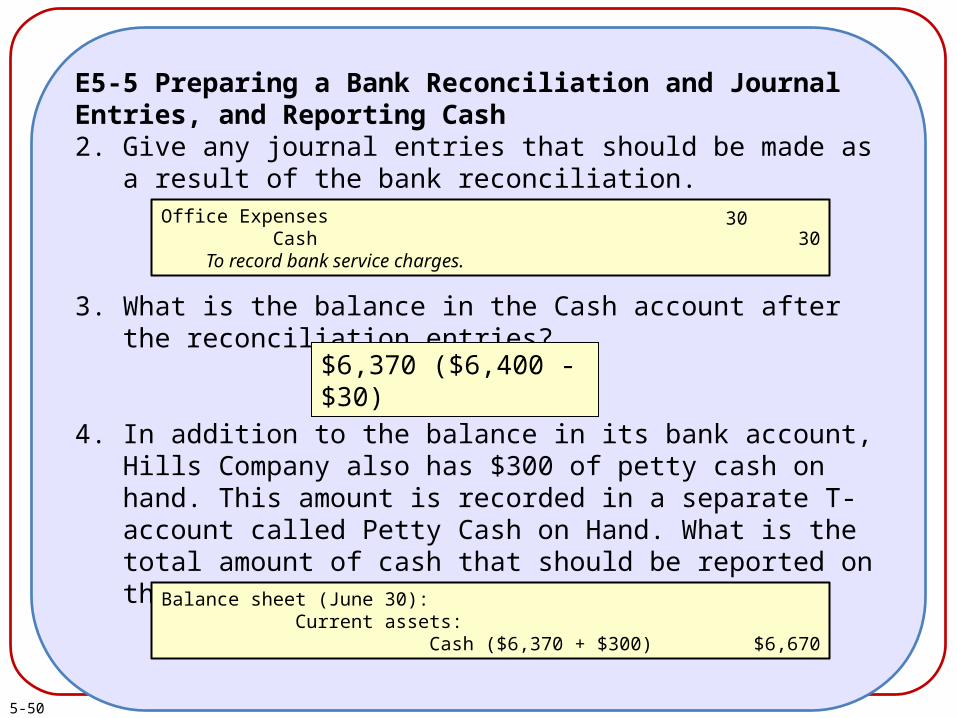

E5-5 Preparing a Bank Reconciliation and Journal Entries, and Reporting Cash2. Give any journal entries that should be made as a result of the

bank reconciliation.

3. What is the balance in the Cash account after the reconciliation entries?

4. In addition to the balance in its bank account, Hills Company also has $300 of petty cash on hand. This amount is recorded in a separate T-account called Petty Cash on Hand. What is the total amount of cash that should be reported on the balance sheet at June 30?

$6,370 ($6,400 - $30)

Office Expenses Cash To record bank service charges.

3030

Balance sheet (June 30): Current assets: Cash ($6,370 + $300) $6,670

5-51

E5-9 (Supplement 5A) Recording Petty Cash TransactionsSunshine Health established a $100 petty cash fund on January 1. From January 2 through 10, payments were made from the fund, as listed below. On January 12, the fund had only $10 remaining;a check was written to replenish the fund.

a. January 2- Paid cash for deliveries to customers - $23.b. January 7- Paid cash for taxi fare incurred by office manager- $50.c. January 10- Paid cash for pens and other office supplies - $17.

Required:1. Prepare the journal entry, if any, required on January 1.

Petty Cash Cash

100100

5-52

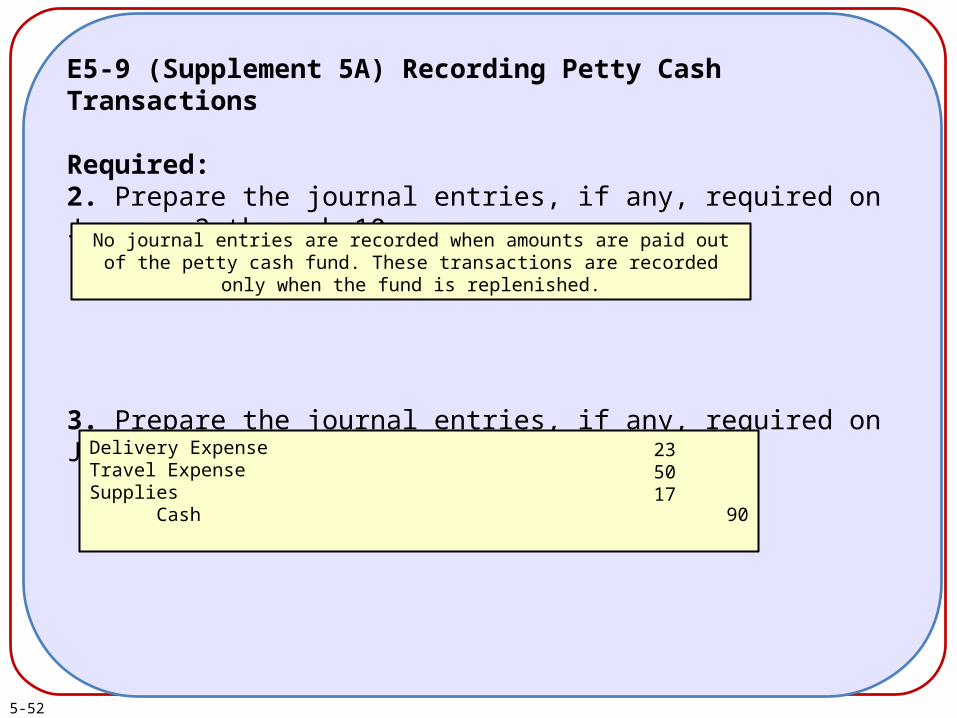

E5-9 (Supplement 5A) Recording Petty Cash Transactions

Required:2. Prepare the journal entries, if any, required on January 2 through 10.

3. Prepare the journal entries, if any, required on January 12.

No journal entries are recorded when amounts are paid out of the petty cash fund. These transactions are recorded only when the fund is replenished.

Delivery ExpenseTravel ExpenseSupplies Cash

90

235017

5-53

End of Chapter 5